Management Accounting Report: Break-Even, Cost, and Budgeting

VerifiedAdded on 2020/12/30

|11

|2267

|333

Report

AI Summary

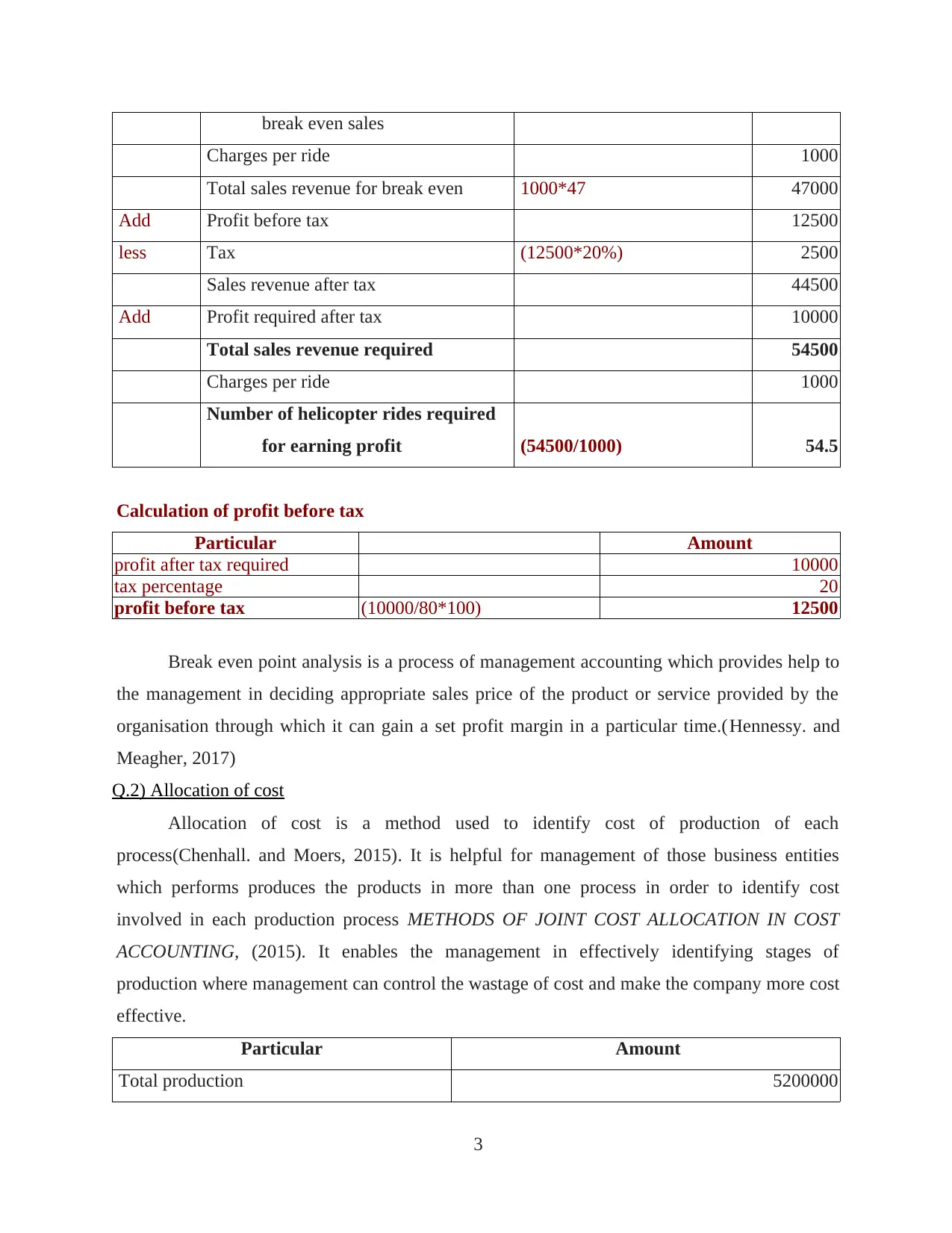

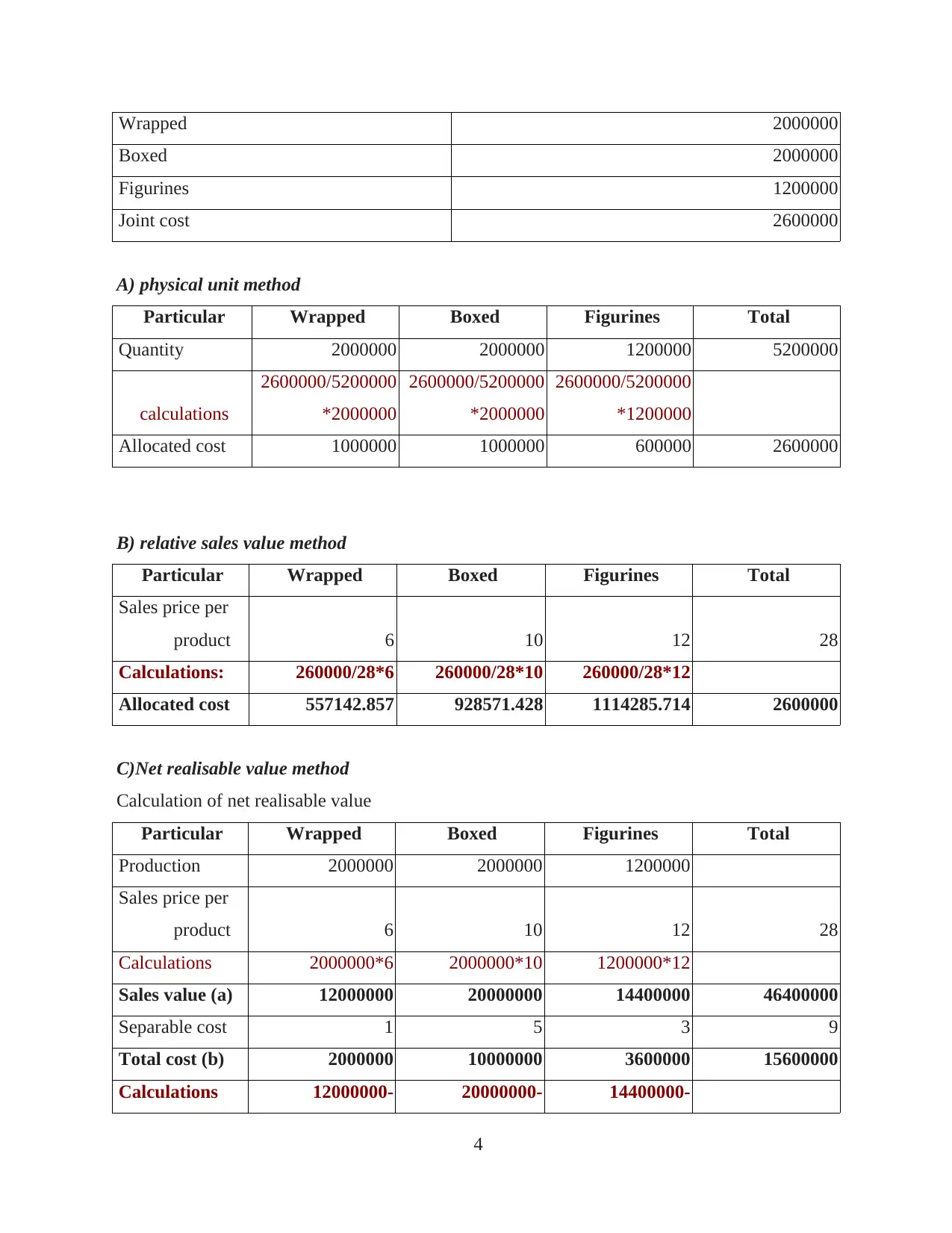

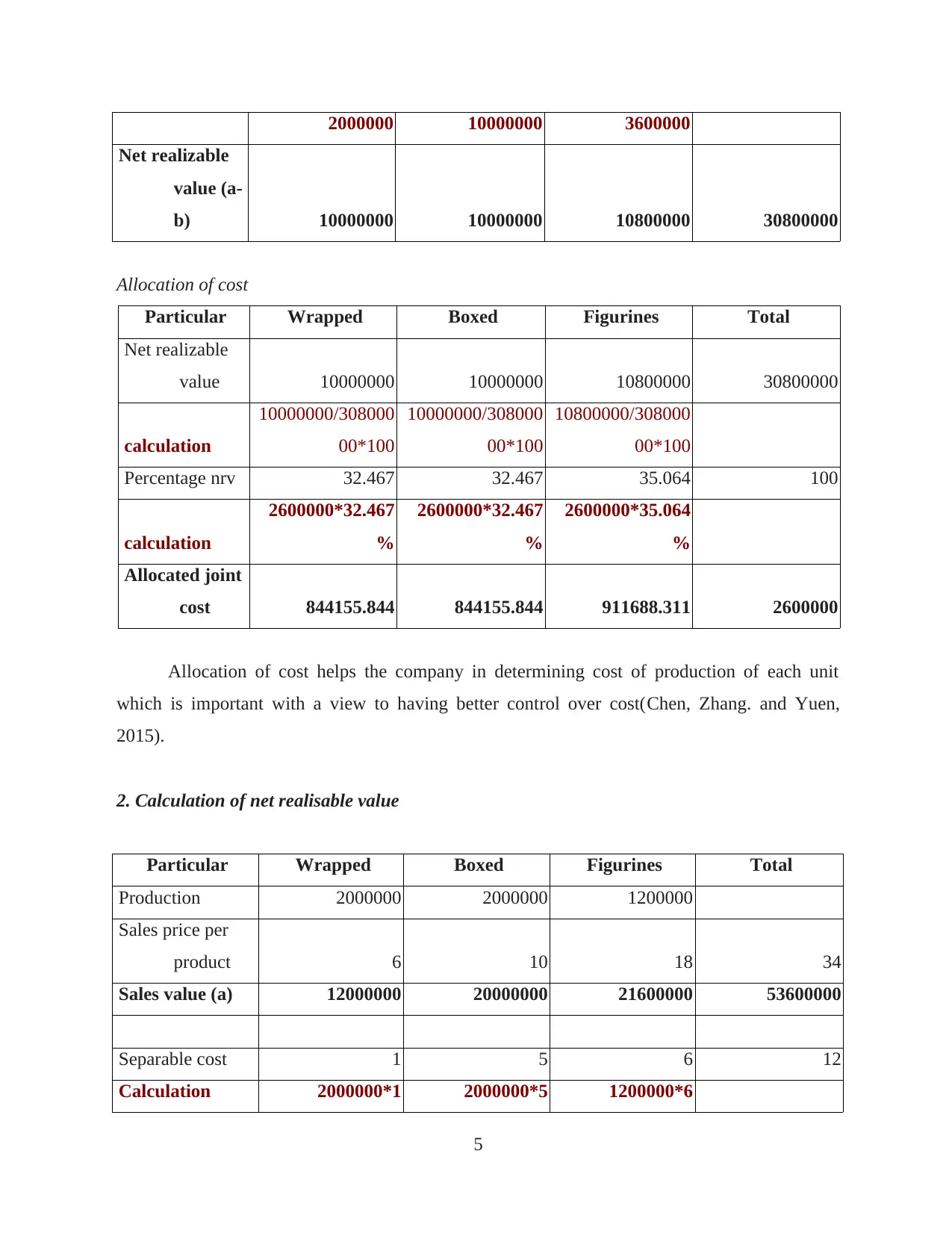

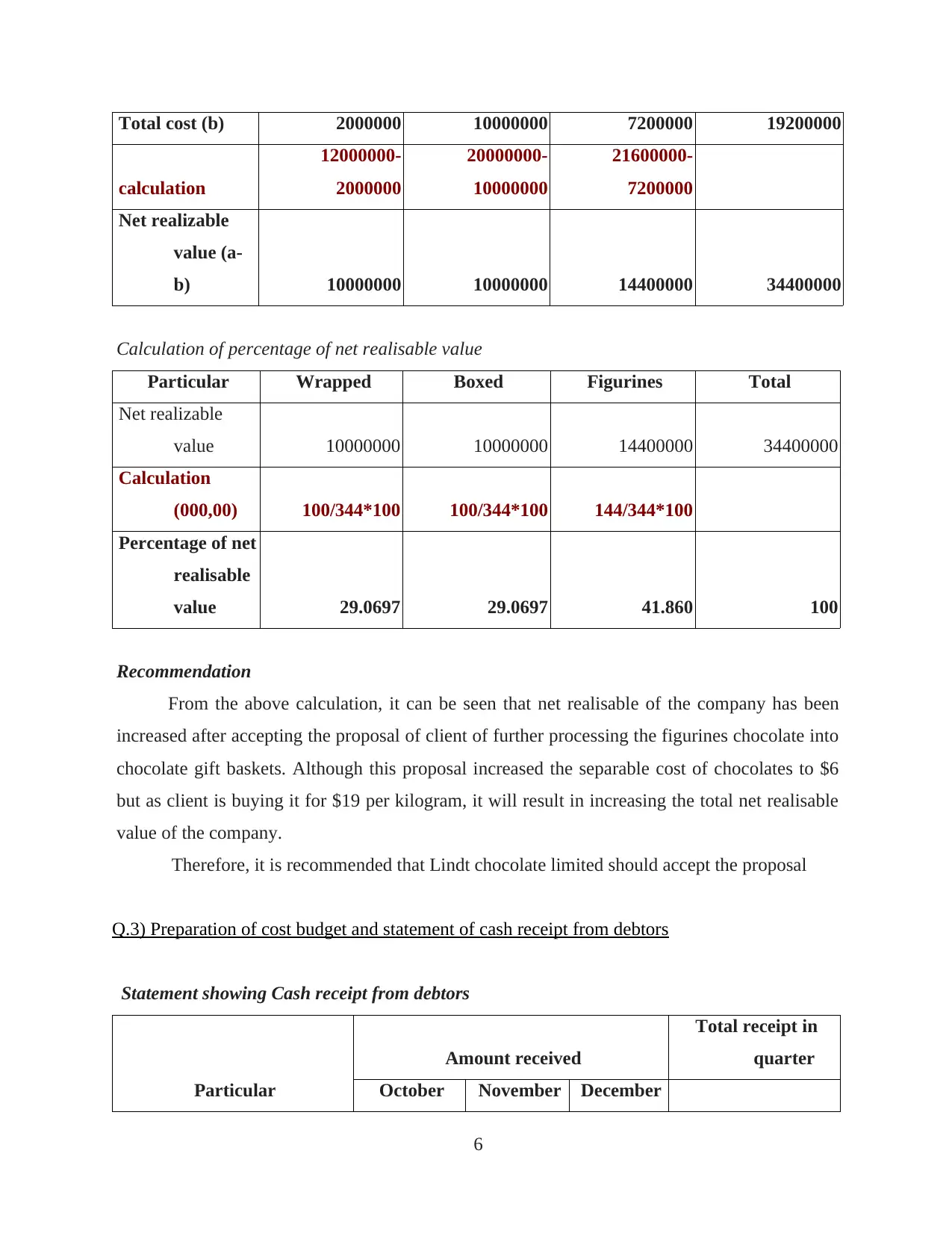

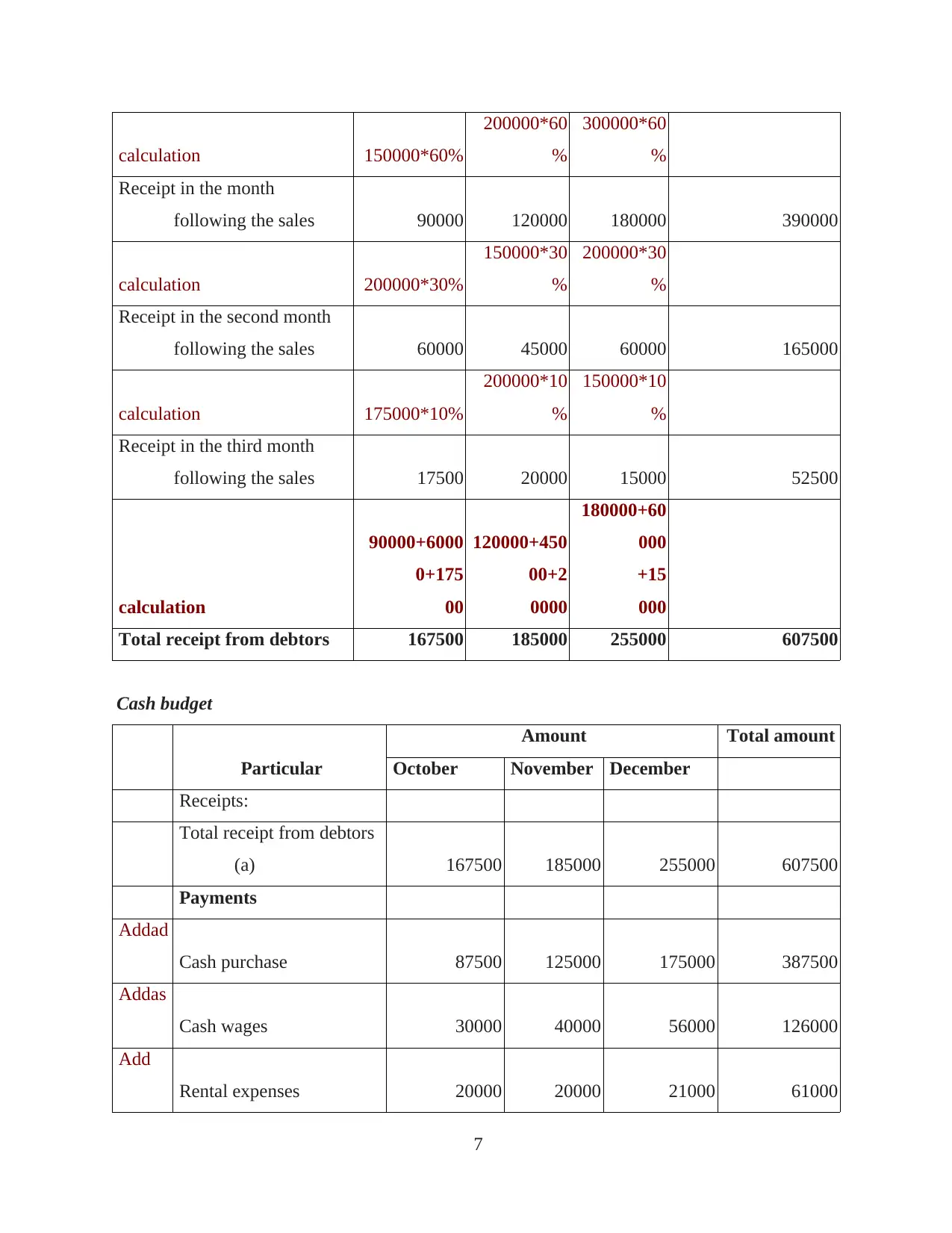

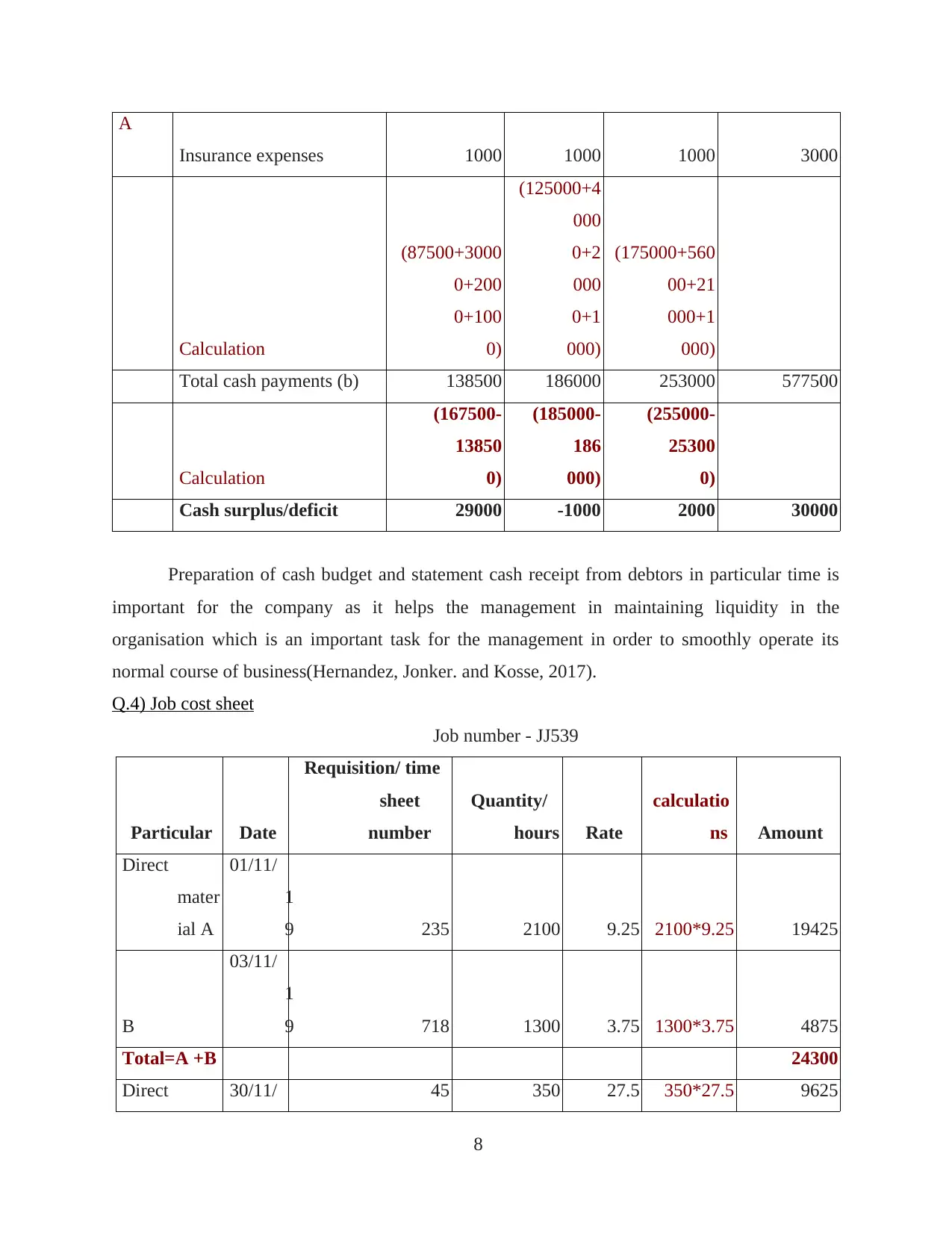

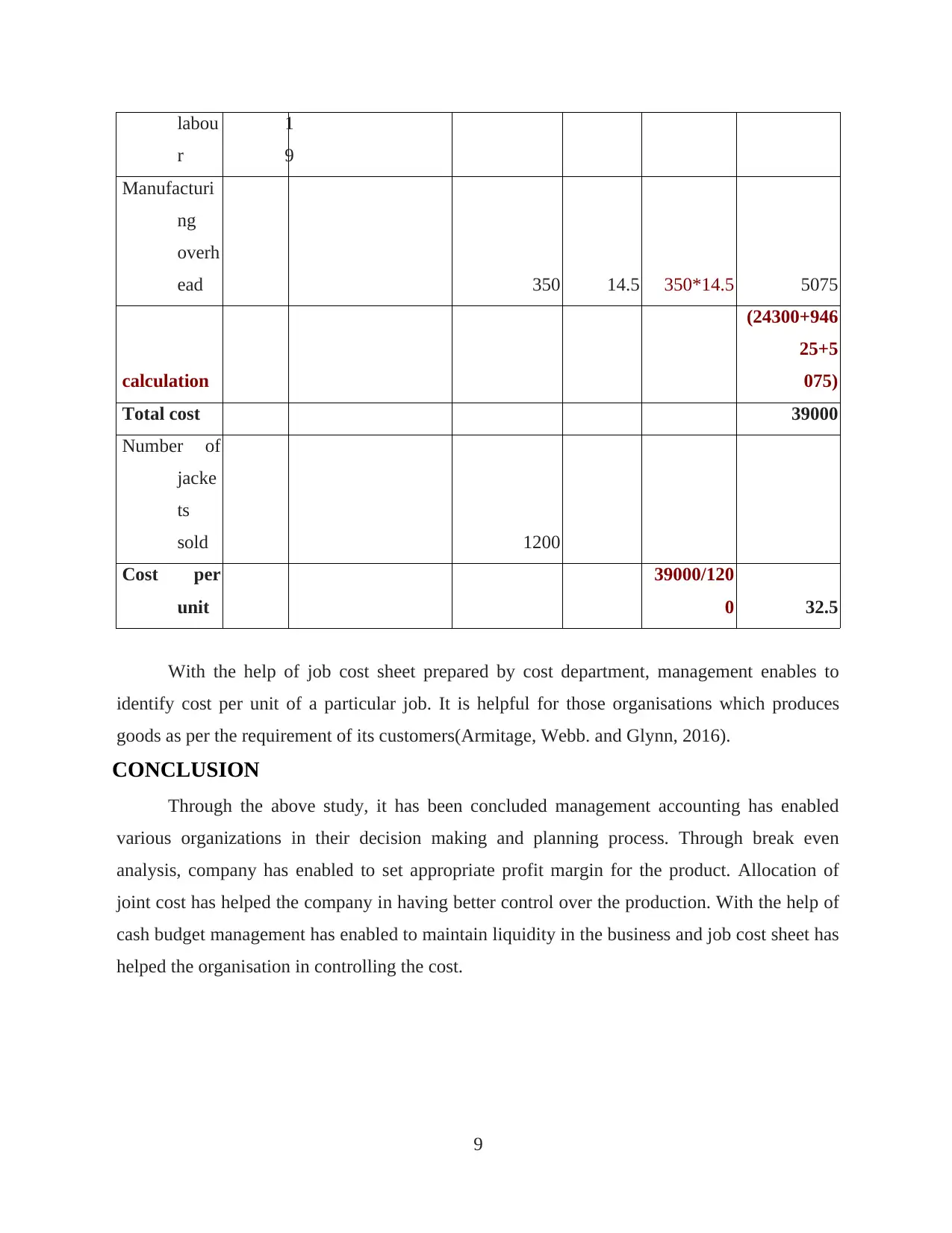

This report delves into various aspects of management accounting, providing a comprehensive overview of essential concepts and techniques. It begins with a detailed calculation of the break-even point, exploring scenarios with and without commissions, and determining the sales revenue required to achieve profitability. The report then examines cost allocation methods, including the physical unit, relative sales value, and net realizable value methods, illustrating how to allocate joint costs effectively. Furthermore, it presents a statement of cash receipts from debtors and a cash budget, highlighting the importance of liquidity management. Finally, the report includes a job cost sheet, demonstrating how to track and analyze costs associated with specific jobs. Through these analyses, the report emphasizes the role of management accounting in decision-making, cost control, and financial planning.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.