Role of Management Accounting and Types of MAS

VerifiedAdded on 2023/01/19

|20

|5239

|36

AI Summary

This article discusses the role of management accounting (MA) and different types of management accounting systems (MAS). It explains how MA helps in long and short term planning, better controlling, and participating in the management process. It also explores the benefits and applications of MAS in British American Tobacco Plc. The article further evaluates the integration of MAS and MA reports with organizational processes. Overall, it provides a comprehensive understanding of the importance and implementation of MA and MAS in business entities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................8

TASK 3..........................................................................................................................................11

TASK 4..........................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

TASK 1............................................................................................................................................3

TASK 2............................................................................................................................................8

TASK 3..........................................................................................................................................11

TASK 4..........................................................................................................................................13

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

The term MA is an accounting process of assessing data regards to monetary & non

monetary transactions and activities with an aim of producing reports (Fleischman and Parker,

2017). In the aspect of today's competitive business environment, this is essential for business

entities to manage their all activities and operations in a systematic manner by implementation of

an effective accounting system so that desired outcomes can be achieved. In this project report a

company is selected that is British American Tobacco Plc. The company is located in London

and manufacturer of cigarette and tobacco. As well as this business entity is the second largest

cigarette maker in the world as accordance of financial information of year 2012. The project

report covers about a vital range of MAS and MA reports. As well as income statements are

produced by help of costing techniques. Along with, variety of planning tools and significance of

MAS in order to sort out the monetary problems is covered under the project report.

MAIN BODY

TASK 1

Role of MA and types of MAS.

Management accounting – The MA is an accounting process in that reports are produced

for internal stakeholders' perspective. By deriving useful data from these reports managers of

business entities become able to take corrective actions as accordance of need (Gurarda, 2015).

In other words, under this accounting internal reports are prepared by accountants which consists

information regards to monetary and anti monetary aspects. These reports help to management

department in order to take corrective actions.

Herein, it is important to know that these reports are not disclosed to external stakeholders.

Below the role of MA is mentioned that is as followings :

Beneficial for long and short term planning – By help of MA, the companies can make

plan effectively for long and short time period. It becomes possible because managers

assess useful information through these reports and take decisions accordingly.

Better controlling – In addition, another role of MA is to focusing on better controlling

over different aspects of businesses. This is so because by utilising important

The term MA is an accounting process of assessing data regards to monetary & non

monetary transactions and activities with an aim of producing reports (Fleischman and Parker,

2017). In the aspect of today's competitive business environment, this is essential for business

entities to manage their all activities and operations in a systematic manner by implementation of

an effective accounting system so that desired outcomes can be achieved. In this project report a

company is selected that is British American Tobacco Plc. The company is located in London

and manufacturer of cigarette and tobacco. As well as this business entity is the second largest

cigarette maker in the world as accordance of financial information of year 2012. The project

report covers about a vital range of MAS and MA reports. As well as income statements are

produced by help of costing techniques. Along with, variety of planning tools and significance of

MAS in order to sort out the monetary problems is covered under the project report.

MAIN BODY

TASK 1

Role of MA and types of MAS.

Management accounting – The MA is an accounting process in that reports are produced

for internal stakeholders' perspective. By deriving useful data from these reports managers of

business entities become able to take corrective actions as accordance of need (Gurarda, 2015).

In other words, under this accounting internal reports are prepared by accountants which consists

information regards to monetary and anti monetary aspects. These reports help to management

department in order to take corrective actions.

Herein, it is important to know that these reports are not disclosed to external stakeholders.

Below the role of MA is mentioned that is as followings :

Beneficial for long and short term planning – By help of MA, the companies can make

plan effectively for long and short time period. It becomes possible because managers

assess useful information through these reports and take decisions accordingly.

Better controlling – In addition, another role of MA is to focusing on better controlling

over different aspects of businesses. This is so because by utilising important

information, managers can aware about actual financial performance and controls

accordingly.

Participating in management process – The another role of MA is that, it is helpful for

making participation in managerial process. Due to this accounting, the business entities

can derive both types of information in the aspect of management.

MAS- In the aspect of companies' different operations and activities, this is too crucial to apply

different accounting systems as accordance of requirement. The MAS can be defined as those

accounting systems that provide framework in order to manage different aspects of companies.

Types of MAS :

Cost accounting system – It is an accounting system which is involved in the process of

gathering and summarising all information regards to cost of various activities (Verma,

2015). Under this accounting system, projection of future possible costs and expenses is

done in an accurate manner so that managers can allocate their resources accordingly.

This accounting system is essential for businesses in order to trace the variances between

actual cost and estimated cost. As well as this accounting system is needed in business

entities for proper management of occurred expenditures in a better way. In the above

respective company, British American Tobacco Plc their finance department is using this

accounting system in order to control total cost of different aspects. In addition, due to

this accounting system they estimate future possible costs that helps in creation of

accurate budget.

Inventory management system – This is an accounting system which is aligned with

procedure of in and outing of materials from warehouses. By implementation of the stock

management system, the managers of companies can gather useful data in order to take

futuristic steps corrective. Additionally, it is required in companies for making balance

between supply and demand of materials. Eventually, for manufacturing business entities

it is very beneficial because by getting information regards to remained quantity of

commodities in stores the managers make further financial plan for buying and

manufacturing of outputs. In the absence of proper management of inventories, this may

lead to higher cost of storing materials. As well as companies will not be able to take

corrective actions accordance to need. The stock management system is needed for

accordingly.

Participating in management process – The another role of MA is that, it is helpful for

making participation in managerial process. Due to this accounting, the business entities

can derive both types of information in the aspect of management.

MAS- In the aspect of companies' different operations and activities, this is too crucial to apply

different accounting systems as accordance of requirement. The MAS can be defined as those

accounting systems that provide framework in order to manage different aspects of companies.

Types of MAS :

Cost accounting system – It is an accounting system which is involved in the process of

gathering and summarising all information regards to cost of various activities (Verma,

2015). Under this accounting system, projection of future possible costs and expenses is

done in an accurate manner so that managers can allocate their resources accordingly.

This accounting system is essential for businesses in order to trace the variances between

actual cost and estimated cost. As well as this accounting system is needed in business

entities for proper management of occurred expenditures in a better way. In the above

respective company, British American Tobacco Plc their finance department is using this

accounting system in order to control total cost of different aspects. In addition, due to

this accounting system they estimate future possible costs that helps in creation of

accurate budget.

Inventory management system – This is an accounting system which is aligned with

procedure of in and outing of materials from warehouses. By implementation of the stock

management system, the managers of companies can gather useful data in order to take

futuristic steps corrective. Additionally, it is required in companies for making balance

between supply and demand of materials. Eventually, for manufacturing business entities

it is very beneficial because by getting information regards to remained quantity of

commodities in stores the managers make further financial plan for buying and

manufacturing of outputs. In the absence of proper management of inventories, this may

lead to higher cost of storing materials. As well as companies will not be able to take

corrective actions accordance to need. The stock management system is needed for

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

companies with an objective of tracking quantity of stored material so that accurate

decisions can be taken. In relation to above chosen business entity British American

Tobacco Plc, this accounting system is being applied by their production department and

as per it they take decision for manufacturing and purchasing of materials.

Price optimisation system – It is an accounting system which has different features and

roles for companies as compare to other accounting systems. This is associated with

process of gathering information about customers' thought and their response towards

companies products. It is done by proper research of customers perception, their buying

habits and many more. The collected data is being used by sales department of companies

for setting prices at a suitable level through at which customers can get value of their

spent money. Thus, it is needed in companies for making competitive strategies by

setting prices of new and exist products at an effective level. As well as for determining

those aspects which are needed to be improved and demanded by customers in products.

Along with, this accounting system plays a significant role for overcoming the issues

regards to lower sales. In the context of British American Tobacco Plc, this can be stated

that they are using above accounting system and their sales department flex their prices as

accordance of competitors movement and customers' demand.

Job order costing system – This is an accounting system which is related with process of

determining production cost of each manufactured unit (Baumann and Losbichler, 2015).

It consists detailed information about total number of individuals are assigned in order to

produce a single unit of output. As well as total cost of job which occurred in the process

of manufacturing. Hence, it is needed in business entities for determining cost of job for

each unit separately. In addition, this accounting system is required for keeping cost of

job lower as much as possible. If companies do not implement this accounting system

then it can be difficult for them to assess each produced units' cost separately. In addition,

this accounting enables business entities to keep the job cost under control. In the aspect

of British American Tobacco Plc, it can be stated that their production department is

using this system for computing each manufactured units' cost. As they are involved in

production of different kind of tobacco products and this is helping them in order to

control each product's cost. In addition, under this accounting system mainly three types

of cost information is included such as direct labour, material and factory overheads.

decisions can be taken. In relation to above chosen business entity British American

Tobacco Plc, this accounting system is being applied by their production department and

as per it they take decision for manufacturing and purchasing of materials.

Price optimisation system – It is an accounting system which has different features and

roles for companies as compare to other accounting systems. This is associated with

process of gathering information about customers' thought and their response towards

companies products. It is done by proper research of customers perception, their buying

habits and many more. The collected data is being used by sales department of companies

for setting prices at a suitable level through at which customers can get value of their

spent money. Thus, it is needed in companies for making competitive strategies by

setting prices of new and exist products at an effective level. As well as for determining

those aspects which are needed to be improved and demanded by customers in products.

Along with, this accounting system plays a significant role for overcoming the issues

regards to lower sales. In the context of British American Tobacco Plc, this can be stated

that they are using above accounting system and their sales department flex their prices as

accordance of competitors movement and customers' demand.

Job order costing system – This is an accounting system which is related with process of

determining production cost of each manufactured unit (Baumann and Losbichler, 2015).

It consists detailed information about total number of individuals are assigned in order to

produce a single unit of output. As well as total cost of job which occurred in the process

of manufacturing. Hence, it is needed in business entities for determining cost of job for

each unit separately. In addition, this accounting system is required for keeping cost of

job lower as much as possible. If companies do not implement this accounting system

then it can be difficult for them to assess each produced units' cost separately. In addition,

this accounting enables business entities to keep the job cost under control. In the aspect

of British American Tobacco Plc, it can be stated that their production department is

using this system for computing each manufactured units' cost. As they are involved in

production of different kind of tobacco products and this is helping them in order to

control each product's cost. In addition, under this accounting system mainly three types

of cost information is included such as direct labour, material and factory overheads.

Methods of MA reports :

MA reports – The MA reports can be defined as those reports which are prepared by accountants

containing detailed information about monetary and non monetary transactions of a particular

time period. Management accounting reports are too crucial in the aspect of companies because

these reports assure that monetary and non monetary goals have been achieved or not. This is

particularly relevant for businesses, that can gain major strategic perspectives from such vital

documents. In the context of above British American Tobacco Plc, they are preparing different

types of reports which are as followings :

Budget Report - Budget management accounting reports are very crucial in the

measurement of financial performance and are produced as a whole for tiny companies and big

organisations, departmentally speaking. Under this report detailed information monetary and non

monetary aspects is included which play a significant role in order to manage overall functions.

This report is prepared by the British American Tobacco Plc to predict and estimate overall

business activities. It is produced on the basis of last year experience and add additional amount

of unforeseen circumstances. Budgeting-related management accounting reports can direct

executives to give good opportunities for employees, cut expenses, and negotiate a new

conditions with sellers and distributors. Thus, any company is important to a budget report

(Endenich and et.al, 2016).

MA reports – The MA reports can be defined as those reports which are prepared by accountants

containing detailed information about monetary and non monetary transactions of a particular

time period. Management accounting reports are too crucial in the aspect of companies because

these reports assure that monetary and non monetary goals have been achieved or not. This is

particularly relevant for businesses, that can gain major strategic perspectives from such vital

documents. In the context of above British American Tobacco Plc, they are preparing different

types of reports which are as followings :

Budget Report - Budget management accounting reports are very crucial in the

measurement of financial performance and are produced as a whole for tiny companies and big

organisations, departmentally speaking. Under this report detailed information monetary and non

monetary aspects is included which play a significant role in order to manage overall functions.

This report is prepared by the British American Tobacco Plc to predict and estimate overall

business activities. It is produced on the basis of last year experience and add additional amount

of unforeseen circumstances. Budgeting-related management accounting reports can direct

executives to give good opportunities for employees, cut expenses, and negotiate a new

conditions with sellers and distributors. Thus, any company is important to a budget report

(Endenich and et.al, 2016).

Performance Report – It is developed by the company to analysis the performance of

employees as well as organization. In this report information about variation between actual and

estimated outcomes is included. On the basis of it, managers of companies take decision about

growth and development of employees. This reports prepared by the manager of British

American Tobacco Plc, department basis to make strategic decisions regarding the future of a

company. The performance of the employees analyses as per the task, how efficiently they

conducting task and laid off with as required.

Inventory management Report – The particular report produce by the manufacturing

companies to keep detail information regarding to stock (Golyagina and Valuckas, 2016).

Inventory management report help to arrange stock level at every stage efficiently. The report

contains information about how much quantity of raw material is stored in warehouses. On the

basis of this report the future requirement of material is assessed in an effective manner. If any

order come to British American Tobacco Plc that time provide information how much raw

material need for further process. It is helpful for the British American Tobacco Plc to efficiently

allocate of very it every stage to producers. If there are recognised any wastages that will use in

other procedure but did not easily increase wastages.

Cost Managerial accounting Report – This report produced to measure the cost of

products that are manufactured. There are consisting of all raw material costs, overhead, labour

and added any cost are interpreted into achievement. Basically in the absence of this report, it

can become difficult for companies' finance department to keep their cost under control. The

report consists detailed information about each aspects' total cost and variation from estimated

cost. A cost report provide summary of information of British American Tobacco Plc. On the

basis of this report manager of British American Tobacco Plc realize the capacity of cost of

several items versus their marketing price. It is mainly applied by the company focus on the

labour cost, wastages of stock and overhead cost. They enable a right understanding of all

expenses that is important for better allocation of resources between all sections.

Benefits of MAS and their applications in the aspect of chosen organisation.

MAS Benefits

Cost accounting system This accounting system helps to companies in controlling total

cost by proper estimation of futuristic costs. Such as in above

chosen business entity they are applying this accounting

employees as well as organization. In this report information about variation between actual and

estimated outcomes is included. On the basis of it, managers of companies take decision about

growth and development of employees. This reports prepared by the manager of British

American Tobacco Plc, department basis to make strategic decisions regarding the future of a

company. The performance of the employees analyses as per the task, how efficiently they

conducting task and laid off with as required.

Inventory management Report – The particular report produce by the manufacturing

companies to keep detail information regarding to stock (Golyagina and Valuckas, 2016).

Inventory management report help to arrange stock level at every stage efficiently. The report

contains information about how much quantity of raw material is stored in warehouses. On the

basis of this report the future requirement of material is assessed in an effective manner. If any

order come to British American Tobacco Plc that time provide information how much raw

material need for further process. It is helpful for the British American Tobacco Plc to efficiently

allocate of very it every stage to producers. If there are recognised any wastages that will use in

other procedure but did not easily increase wastages.

Cost Managerial accounting Report – This report produced to measure the cost of

products that are manufactured. There are consisting of all raw material costs, overhead, labour

and added any cost are interpreted into achievement. Basically in the absence of this report, it

can become difficult for companies' finance department to keep their cost under control. The

report consists detailed information about each aspects' total cost and variation from estimated

cost. A cost report provide summary of information of British American Tobacco Plc. On the

basis of this report manager of British American Tobacco Plc realize the capacity of cost of

several items versus their marketing price. It is mainly applied by the company focus on the

labour cost, wastages of stock and overhead cost. They enable a right understanding of all

expenses that is important for better allocation of resources between all sections.

Benefits of MAS and their applications in the aspect of chosen organisation.

MAS Benefits

Cost accounting system This accounting system helps to companies in controlling total

cost by proper estimation of futuristic costs. Such as in above

chosen business entity they are applying this accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system and it is helping their managers in reducing unwanted

additional costs.

Inventory management system This accounting system acts with coordination of production

department for controlling of over-purchasing and

manufacturing. In British American Tobacco Plc, their

production department derives useful information through this

accounting system and take suitable actions accordingly.

Price optimisation system It is associated with the process of setting prices of produced

outputs (Oldroyd, 2017). The British American Tobacco Plc, is

applying this accounting system for collecting useful about

customers' perception and need. As accordance they determine

the price of their tobacco products.

Job order costing system It is linked with computing cost of each individual output

effectively. In the context of above British American Tobacco

Plc, they are producing different kinds of tobacco items. Thus,

by help of this accounting system they determine prices as

accordance of customers' requirement.

Evaluation of integration of MAS and MA reports with organisational process.

In the aspect of scenario of business entities, there are different kind of operations and

activities are performed at various levels. These vital range of activities are managed by

implementation of an effective accounting system (Busco and Quattrone, 2015). For an example

in British American Tobacco Plc, their departments are linked with accounting systems. Such as

price optimisation system is aligned with sales department as well as cost accounting system

with finance department. It shows that MAS are integrated with process of companies. Along

with, MA reports are also linked to above business entities' process like stock report helps to

production department and rest of other reports are also aligned with their process.

TASK 2

Preparation of income statement as per the absorption and marginal costing method.

additional costs.

Inventory management system This accounting system acts with coordination of production

department for controlling of over-purchasing and

manufacturing. In British American Tobacco Plc, their

production department derives useful information through this

accounting system and take suitable actions accordingly.

Price optimisation system It is associated with the process of setting prices of produced

outputs (Oldroyd, 2017). The British American Tobacco Plc, is

applying this accounting system for collecting useful about

customers' perception and need. As accordance they determine

the price of their tobacco products.

Job order costing system It is linked with computing cost of each individual output

effectively. In the context of above British American Tobacco

Plc, they are producing different kinds of tobacco items. Thus,

by help of this accounting system they determine prices as

accordance of customers' requirement.

Evaluation of integration of MAS and MA reports with organisational process.

In the aspect of scenario of business entities, there are different kind of operations and

activities are performed at various levels. These vital range of activities are managed by

implementation of an effective accounting system (Busco and Quattrone, 2015). For an example

in British American Tobacco Plc, their departments are linked with accounting systems. Such as

price optimisation system is aligned with sales department as well as cost accounting system

with finance department. It shows that MAS are integrated with process of companies. Along

with, MA reports are also linked to above business entities' process like stock report helps to

production department and rest of other reports are also aligned with their process.

TASK 2

Preparation of income statement as per the absorption and marginal costing method.

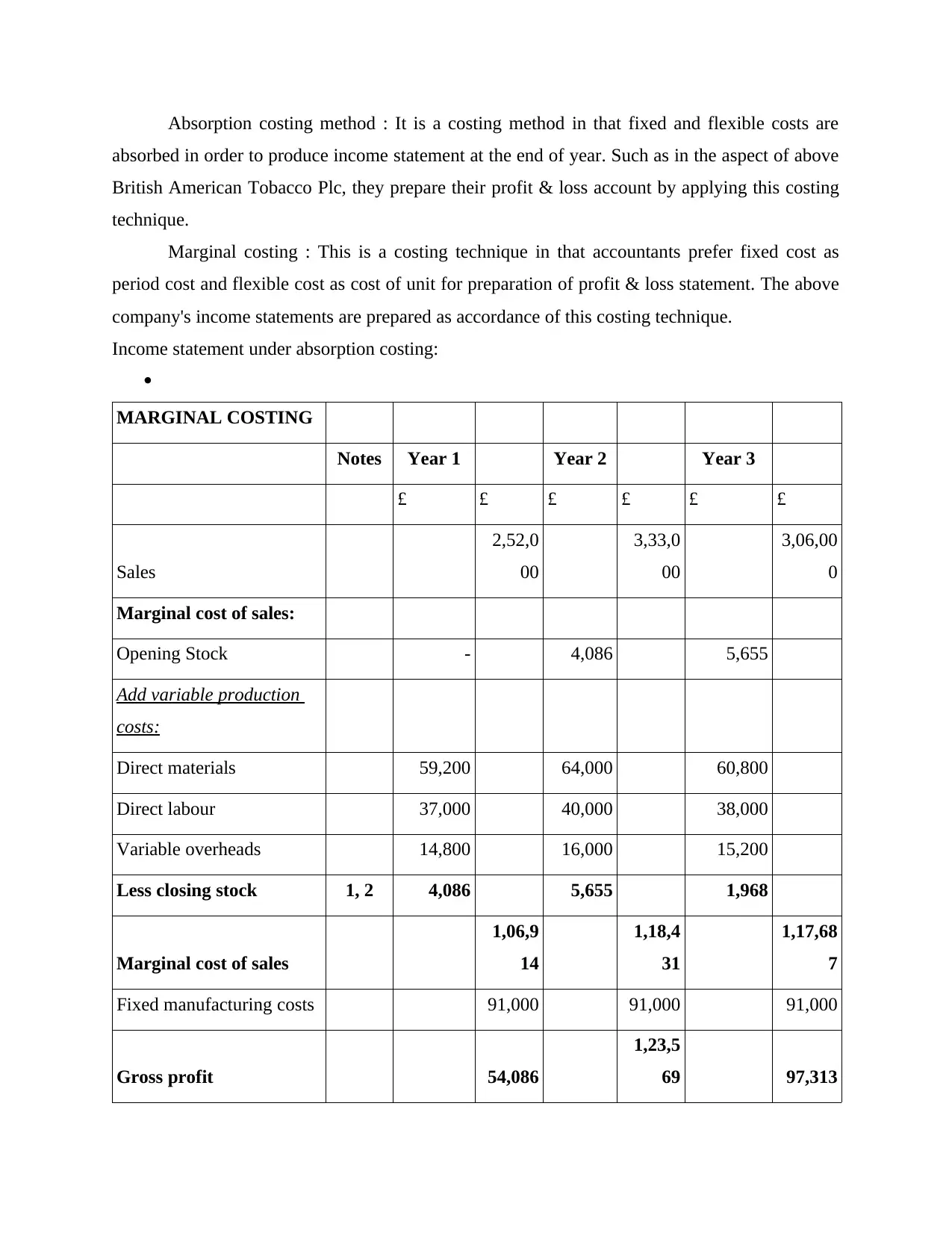

Absorption costing method : It is a costing method in that fixed and flexible costs are

absorbed in order to produce income statement at the end of year. Such as in the aspect of above

British American Tobacco Plc, they prepare their profit & loss account by applying this costing

technique.

Marginal costing : This is a costing technique in that accountants prefer fixed cost as

period cost and flexible cost as cost of unit for preparation of profit & loss statement. The above

company's income statements are prepared as accordance of this costing technique.

Income statement under absorption costing:

MARGINAL COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,00

0

Marginal cost of sales:

Opening Stock - 4,086 5,655

Add variable production

costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Less closing stock 1, 2 4,086 5,655 1,968

Marginal cost of sales

1,06,9

14

1,18,4

31

1,17,68

7

Fixed manufacturing costs 91,000 91,000 91,000

Gross profit 54,086

1,23,5

69 97,313

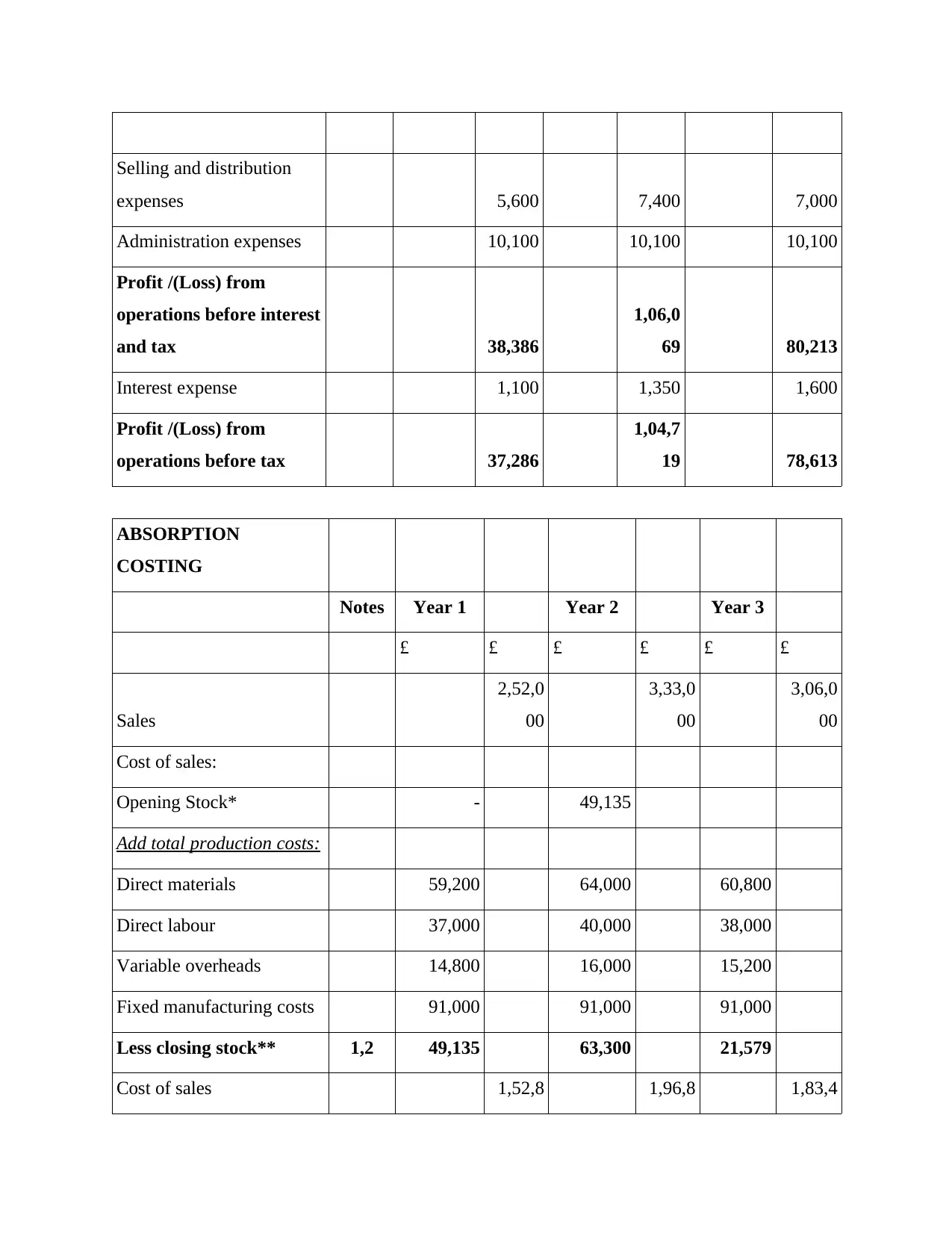

absorbed in order to produce income statement at the end of year. Such as in the aspect of above

British American Tobacco Plc, they prepare their profit & loss account by applying this costing

technique.

Marginal costing : This is a costing technique in that accountants prefer fixed cost as

period cost and flexible cost as cost of unit for preparation of profit & loss statement. The above

company's income statements are prepared as accordance of this costing technique.

Income statement under absorption costing:

MARGINAL COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,00

0

Marginal cost of sales:

Opening Stock - 4,086 5,655

Add variable production

costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Less closing stock 1, 2 4,086 5,655 1,968

Marginal cost of sales

1,06,9

14

1,18,4

31

1,17,68

7

Fixed manufacturing costs 91,000 91,000 91,000

Gross profit 54,086

1,23,5

69 97,313

Selling and distribution

expenses 5,600 7,400 7,000

Administration expenses 10,100 10,100 10,100

Profit /(Loss) from

operations before interest

and tax 38,386

1,06,0

69 80,213

Interest expense 1,100 1,350 1,600

Profit /(Loss) from

operations before tax 37,286

1,04,7

19 78,613

ABSORPTION

COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,0

00

Cost of sales:

Opening Stock* - 49,135

Add total production costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Fixed manufacturing costs 91,000 91,000 91,000

Less closing stock** 1,2 49,135 63,300 21,579

Cost of sales 1,52,8 1,96,8 1,83,4

expenses 5,600 7,400 7,000

Administration expenses 10,100 10,100 10,100

Profit /(Loss) from

operations before interest

and tax 38,386

1,06,0

69 80,213

Interest expense 1,100 1,350 1,600

Profit /(Loss) from

operations before tax 37,286

1,04,7

19 78,613

ABSORPTION

COSTING

Notes Year 1 Year 2 Year 3

£ £ £ £ £ £

Sales

2,52,0

00

3,33,0

00

3,06,0

00

Cost of sales:

Opening Stock* - 49,135

Add total production costs:

Direct materials 59,200 64,000 60,800

Direct labour 37,000 40,000 38,000

Variable overheads 14,800 16,000 15,200

Fixed manufacturing costs 91,000 91,000 91,000

Less closing stock** 1,2 49,135 63,300 21,579

Cost of sales 1,52,8 1,96,8 1,83,4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

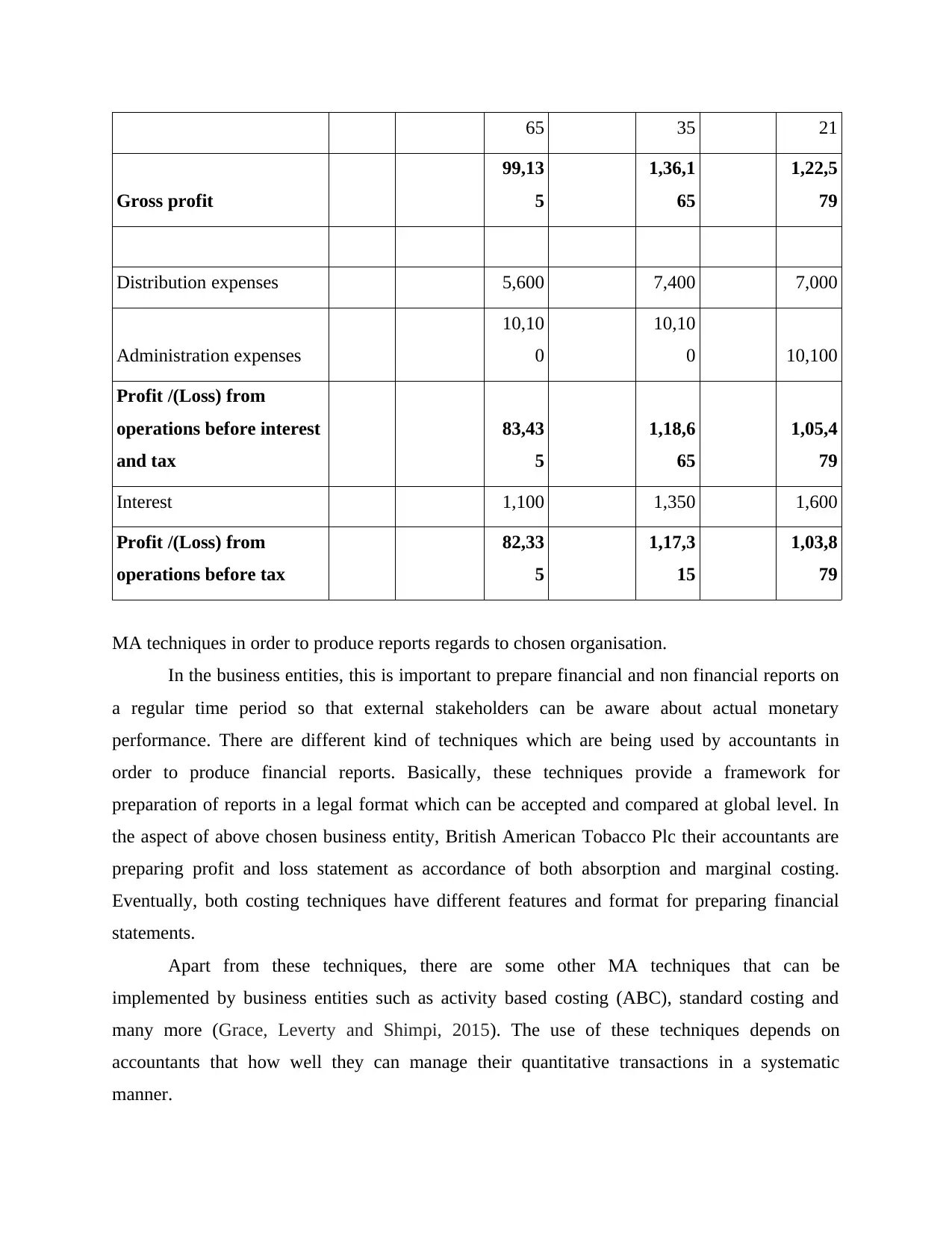

65 35 21

Gross profit

99,13

5

1,36,1

65

1,22,5

79

Distribution expenses 5,600 7,400 7,000

Administration expenses

10,10

0

10,10

0 10,100

Profit /(Loss) from

operations before interest

and tax

83,43

5

1,18,6

65

1,05,4

79

Interest 1,100 1,350 1,600

Profit /(Loss) from

operations before tax

82,33

5

1,17,3

15

1,03,8

79

MA techniques in order to produce reports regards to chosen organisation.

In the business entities, this is important to prepare financial and non financial reports on

a regular time period so that external stakeholders can be aware about actual monetary

performance. There are different kind of techniques which are being used by accountants in

order to produce financial reports. Basically, these techniques provide a framework for

preparation of reports in a legal format which can be accepted and compared at global level. In

the aspect of above chosen business entity, British American Tobacco Plc their accountants are

preparing profit and loss statement as accordance of both absorption and marginal costing.

Eventually, both costing techniques have different features and format for preparing financial

statements.

Apart from these techniques, there are some other MA techniques that can be

implemented by business entities such as activity based costing (ABC), standard costing and

many more (Grace, Leverty and Shimpi, 2015). The use of these techniques depends on

accountants that how well they can manage their quantitative transactions in a systematic

manner.

Gross profit

99,13

5

1,36,1

65

1,22,5

79

Distribution expenses 5,600 7,400 7,000

Administration expenses

10,10

0

10,10

0 10,100

Profit /(Loss) from

operations before interest

and tax

83,43

5

1,18,6

65

1,05,4

79

Interest 1,100 1,350 1,600

Profit /(Loss) from

operations before tax

82,33

5

1,17,3

15

1,03,8

79

MA techniques in order to produce reports regards to chosen organisation.

In the business entities, this is important to prepare financial and non financial reports on

a regular time period so that external stakeholders can be aware about actual monetary

performance. There are different kind of techniques which are being used by accountants in

order to produce financial reports. Basically, these techniques provide a framework for

preparation of reports in a legal format which can be accepted and compared at global level. In

the aspect of above chosen business entity, British American Tobacco Plc their accountants are

preparing profit and loss statement as accordance of both absorption and marginal costing.

Eventually, both costing techniques have different features and format for preparing financial

statements.

Apart from these techniques, there are some other MA techniques that can be

implemented by business entities such as activity based costing (ABC), standard costing and

many more (Grace, Leverty and Shimpi, 2015). The use of these techniques depends on

accountants that how well they can manage their quantitative transactions in a systematic

manner.

Interpretation of produced income statements.

The British American Tobacco Plc 's income statements are prepared by help of both

absorption and marginal costing techniques. In the aspect of absorption costing technique, this

can be stated that their net profit is of £40000. As well as in this technique both fixed and

variable costs are absorbed by considering this cost as unit cost. On the other hand, under

marginal costing technique their net profit is of £32000. Herein, this can be find out there are

similar data is used for preparation of income statements but resulted outcome is variant. The

cause of this variation is way of taking both costs in different manner. In comparison manner of

both costing techniques, the absorption costing seems suitable to use for businesses. This is so

because in this technique, value of both costs are assigned in an equal way.

TASK 3

Benefits and drawback of planning tools.

Budgetary control – This can be defined as a kind of approach which is related to managing

businesses monetary performance by help of different types of budgets. There are different kind

of budgets that have their own importance in order to trace the actual outcome and allocating

funds effectively. Below some types of budgets are elaborated that are as followings :

Capital budgeting- This is a type of budgeting in which different types of investment assessments

are evaluated to assess their effectiveness (Sithole, Chandler, Abeysekera and Paas, 2017).

Under it, various types of methods are used, such as net present value, rate of return accounting,

etc. These techniques plays a key role in order to assess efficiency of investment proposals.

Herein, below analysis of these techniques is done:

Net present value- It can be defined as a difference between present value of cash flows

including in and out flows of a particular time period.

IRR- This is related with computing rate of interest on that net present value of cash

flows of any particular project becomes at zero level.

Payback period- It is type of technique which is used to compute time period needed to

recover investment cost.

The British American Tobacco Plc 's income statements are prepared by help of both

absorption and marginal costing techniques. In the aspect of absorption costing technique, this

can be stated that their net profit is of £40000. As well as in this technique both fixed and

variable costs are absorbed by considering this cost as unit cost. On the other hand, under

marginal costing technique their net profit is of £32000. Herein, this can be find out there are

similar data is used for preparation of income statements but resulted outcome is variant. The

cause of this variation is way of taking both costs in different manner. In comparison manner of

both costing techniques, the absorption costing seems suitable to use for businesses. This is so

because in this technique, value of both costs are assigned in an equal way.

TASK 3

Benefits and drawback of planning tools.

Budgetary control – This can be defined as a kind of approach which is related to managing

businesses monetary performance by help of different types of budgets. There are different kind

of budgets that have their own importance in order to trace the actual outcome and allocating

funds effectively. Below some types of budgets are elaborated that are as followings :

Capital budgeting- This is a type of budgeting in which different types of investment assessments

are evaluated to assess their effectiveness (Sithole, Chandler, Abeysekera and Paas, 2017).

Under it, various types of methods are used, such as net present value, rate of return accounting,

etc. These techniques plays a key role in order to assess efficiency of investment proposals.

Herein, below analysis of these techniques is done:

Net present value- It can be defined as a difference between present value of cash flows

including in and out flows of a particular time period.

IRR- This is related with computing rate of interest on that net present value of cash

flows of any particular project becomes at zero level.

Payback period- It is type of technique which is used to compute time period needed to

recover investment cost.

ARR- It is defined as a rate of return needed for initial capital expenditure on any specific

investment.

In the aspect of above British American Tobacco Plc, their finance managers implement this

budgeting approach to evaluate their investments. It has below mentioned advantages and

disadvantages such as:

Advantage- It helps businesses to choose an effective way to choose investment options inn that

leads to higher returns.

Disadvantage- To evaluate different options, it absorbs too much time and expense that is not

suitable for small businesses.

Operational budgeting - It is a kind of budgeting strategy in which different kinds of things are

projected to be effectively accomplished in various operations. This is perfect for those

companies that run a large number of functions (Akroyd, Biswas and Chuang, 2016). In this

budgeting approach, a detailed analysis of variability is carried out by comparing the actual

results with the estimated results. Herein, below some techniques are mentioned such as:

Forecasting- Accounting forecasting refers to the practice of predicting future costs by

using current and historical cost information.

Variance analysis- Analysis of variability is the statistical analysis of the disparity

between real and expected behaviour.

Standard costing- Standard costing is the method of replacing an estimated cost in the

accounting records with a real cost.

British American Tobacco Plc, is preparing this budget for managing their over all operations. It

has below mentioned advantages and disadvantages such as:

Advantage - This budget benefits as well as being flexible in the field of assigning total resources

for lengthy-term planning.

Disadvantage- This budgeting strategy takes too much time and expense for small business

companies that is not sustainable.

Flexible budgeting- It can be described as a form of budgeting technique in that the sums entered

in the budget can be adjusted as variation in total units and quantities (Jacobs, 2016). In the

investment.

In the aspect of above British American Tobacco Plc, their finance managers implement this

budgeting approach to evaluate their investments. It has below mentioned advantages and

disadvantages such as:

Advantage- It helps businesses to choose an effective way to choose investment options inn that

leads to higher returns.

Disadvantage- To evaluate different options, it absorbs too much time and expense that is not

suitable for small businesses.

Operational budgeting - It is a kind of budgeting strategy in which different kinds of things are

projected to be effectively accomplished in various operations. This is perfect for those

companies that run a large number of functions (Akroyd, Biswas and Chuang, 2016). In this

budgeting approach, a detailed analysis of variability is carried out by comparing the actual

results with the estimated results. Herein, below some techniques are mentioned such as:

Forecasting- Accounting forecasting refers to the practice of predicting future costs by

using current and historical cost information.

Variance analysis- Analysis of variability is the statistical analysis of the disparity

between real and expected behaviour.

Standard costing- Standard costing is the method of replacing an estimated cost in the

accounting records with a real cost.

British American Tobacco Plc, is preparing this budget for managing their over all operations. It

has below mentioned advantages and disadvantages such as:

Advantage - This budget benefits as well as being flexible in the field of assigning total resources

for lengthy-term planning.

Disadvantage- This budgeting strategy takes too much time and expense for small business

companies that is not sustainable.

Flexible budgeting- It can be described as a form of budgeting technique in that the sums entered

in the budget can be adjusted as variation in total units and quantities (Jacobs, 2016). In the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

aspect of British American Tobacco Plc, this budget is used for those activities which have

nature of fluctuation during accounting period.

Benefits - This budget's major benefit is that it's simple to use.

Drawback- This budget leads to information theft and abuse as it requires changes to be made by

employees.

Planning tools for preparation of budgets.

For business entities, this is important to estimate futuristic expenses and revenues in an

effective manner so that budgets can be prepared accurately (Burritt and Christ, 2017). In this

aspect planning tools are very useful because under planning tools different kind of budgets are

included and each of them has own role for preparation of budgets. In the British American

Tobacco Plc, their managers are utilising important information about monetary transactions for

a specific time period. Basically, in the absence of budgets this can be tough for companies to

use their financial resources in an effective manner.

TASK 4

MAS to solve the financial issues.

Financial problem – In the recent business scenario, companies are trying to expand their

business operations across the nations and in this process a vital range of issues occur that can be

of financial or non financial nature. Basically, the monetary problems incur in businesses due to

inefficiency of internal aspects. There are different kind of issues which are faced by companies

and some of them are demonstrated below such as :

Inadequate protection of company's assets- This is a kinds of problem which occurs in

business entities because of lack of effective control over assets (Arnaboldi and

Cuganesan, 2017). Due to ineffective control over assets, it becomes difficult to

companies in order to make better utilisation of their resources in an effective manner. In

the context of British American Tobacco plc, they are facing this financial issue and as a

result they are not able to take proper advantage from their assets.

Error in accounting records- It is a type of financial issue that is related with making

error in accounting records. Due to this issue, it becomes difficult for managers in order

to take suitable decisions because of wrong financial information.

nature of fluctuation during accounting period.

Benefits - This budget's major benefit is that it's simple to use.

Drawback- This budget leads to information theft and abuse as it requires changes to be made by

employees.

Planning tools for preparation of budgets.

For business entities, this is important to estimate futuristic expenses and revenues in an

effective manner so that budgets can be prepared accurately (Burritt and Christ, 2017). In this

aspect planning tools are very useful because under planning tools different kind of budgets are

included and each of them has own role for preparation of budgets. In the British American

Tobacco Plc, their managers are utilising important information about monetary transactions for

a specific time period. Basically, in the absence of budgets this can be tough for companies to

use their financial resources in an effective manner.

TASK 4

MAS to solve the financial issues.

Financial problem – In the recent business scenario, companies are trying to expand their

business operations across the nations and in this process a vital range of issues occur that can be

of financial or non financial nature. Basically, the monetary problems incur in businesses due to

inefficiency of internal aspects. There are different kind of issues which are faced by companies

and some of them are demonstrated below such as :

Inadequate protection of company's assets- This is a kinds of problem which occurs in

business entities because of lack of effective control over assets (Arnaboldi and

Cuganesan, 2017). Due to ineffective control over assets, it becomes difficult to

companies in order to make better utilisation of their resources in an effective manner. In

the context of British American Tobacco plc, they are facing this financial issue and as a

result they are not able to take proper advantage from their assets.

Error in accounting records- It is a type of financial issue that is related with making

error in accounting records. Due to this issue, it becomes difficult for managers in order

to take suitable decisions because of wrong financial information.

Accounting methods to respond the financial issues :

Benchmarking – It is an approach that is widely used by companies in order to make

compare actual financial position with rest of other business entities that operates in same

operations (Saeidi, 2018). In broad sense, under this technique companies' track the

variances of different aspects with other companies. By help of this approach, it becomes

easier for managers to assess actual monetary issue and as per it they find alternatives. In

the aspect of above British American Tobacco Plc, they are applying this approach in

order to assess actual monetary issue and as accordance search possible alternatives.

Financial governance – Under this approach all types of monetary outcomes of

businesses are recorded in a systematic way. Due to this managers of companies focus on

those activities which are causing as lose in terms of lower revenues. Basically, this

approach is suitable for those business entities wherein large number of monetary

transactions are done on a daily basis.

Herein, below key techniques are mentioned that are as followings:

Balance scorecard - A balanced scorecard is a measurable statistic of management used

to classify and enhance various important business processes and their external results.

Balanced scorecards are being used to assess institutions and to provide input. In order to

provide quantitative results, data gathering is essential as managers and directors gather

and define the data and use it to make better choices for the institution. In the aspect of

above company's financial issue of inadequate protection of assets is sort out by help of

this technique. It became become possible because by help of this, they evaluated their

actual level of performance and implemented strategies accordingly.

Activity based costing- Activity-based costing (ABC) is a method of costing associated

goods and services with overhead and indirect costs. This costing accounting method

acknowledges the connection respectively costs, overhead practices, and products,

allocating administrative costs less arbitrarily to goods than classical cost methods. In the

above company, they are applying this technique in order to find out variation between

actual and estimated costs.

MAS to solve financial issues.

Benchmarking – It is an approach that is widely used by companies in order to make

compare actual financial position with rest of other business entities that operates in same

operations (Saeidi, 2018). In broad sense, under this technique companies' track the

variances of different aspects with other companies. By help of this approach, it becomes

easier for managers to assess actual monetary issue and as per it they find alternatives. In

the aspect of above British American Tobacco Plc, they are applying this approach in

order to assess actual monetary issue and as accordance search possible alternatives.

Financial governance – Under this approach all types of monetary outcomes of

businesses are recorded in a systematic way. Due to this managers of companies focus on

those activities which are causing as lose in terms of lower revenues. Basically, this

approach is suitable for those business entities wherein large number of monetary

transactions are done on a daily basis.

Herein, below key techniques are mentioned that are as followings:

Balance scorecard - A balanced scorecard is a measurable statistic of management used

to classify and enhance various important business processes and their external results.

Balanced scorecards are being used to assess institutions and to provide input. In order to

provide quantitative results, data gathering is essential as managers and directors gather

and define the data and use it to make better choices for the institution. In the aspect of

above company's financial issue of inadequate protection of assets is sort out by help of

this technique. It became become possible because by help of this, they evaluated their

actual level of performance and implemented strategies accordingly.

Activity based costing- Activity-based costing (ABC) is a method of costing associated

goods and services with overhead and indirect costs. This costing accounting method

acknowledges the connection respectively costs, overhead practices, and products,

allocating administrative costs less arbitrarily to goods than classical cost methods. In the

above company, they are applying this technique in order to find out variation between

actual and estimated costs.

MAS to solve financial issues.

There are different kind of monetary issues which are faced by companies in their

operations and activities (Hemmer and Labro, 2017). Such as in the above British American

Tobacco Plc, their issue is regards to decreasing total amount of sales which has been sorted out

by “Price optimisation system”. Thus, it can be stated that MAS are useful for solving issues.

Planning tools to solve monetary issues.

Along with the MAS, the planning tools are also beneficial for solving the monetary

issues. Like in the above British American Tobacco Plc, they are using a variety of budgets in

order to access financial transactions and to sort the issues. Their financial managers are mainly

based on production budget, sales budget for getting accurate data of financial transactions.

CONCLUSION

As accordance of above detailed project report it can be articulated that in present

business scenario the role of MAS is increasing as companies are moving towards globalisation.

The report concludes about different types of MAS like cost accounting system, price

optimisation system and many more. As well as MA reports such as performance report, stock

report etc. are mentioned. In further part of project report income statements are produced by

help of absorption and marginal costing on assumption based data. In addition role of planning

tools and MAS in aspect of sorting monetary issues is concluded in the last part of project report.

operations and activities (Hemmer and Labro, 2017). Such as in the above British American

Tobacco Plc, their issue is regards to decreasing total amount of sales which has been sorted out

by “Price optimisation system”. Thus, it can be stated that MAS are useful for solving issues.

Planning tools to solve monetary issues.

Along with the MAS, the planning tools are also beneficial for solving the monetary

issues. Like in the above British American Tobacco Plc, they are using a variety of budgets in

order to access financial transactions and to sort the issues. Their financial managers are mainly

based on production budget, sales budget for getting accurate data of financial transactions.

CONCLUSION

As accordance of above detailed project report it can be articulated that in present

business scenario the role of MAS is increasing as companies are moving towards globalisation.

The report concludes about different types of MAS like cost accounting system, price

optimisation system and many more. As well as MA reports such as performance report, stock

report etc. are mentioned. In further part of project report income statements are produced by

help of absorption and marginal costing on assumption based data. In addition role of planning

tools and MAS in aspect of sorting monetary issues is concluded in the last part of project report.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and journals:

Fleischman, R. K. and Parker, L. D., 2017. What is Past is Prologue: Cost Accounting in the

British Industrial Revolution. 1760-1850. Routledge.

Gurarda, S., 2015. Environmental management accounting. In Handbook of research on

developing sustainable value in economics, finance, and marketing (pp. 278-296). IGI

Global.

Verma, M., 2015. Inventory management accounting for obsolete inventory. IUP Journal of

Accounting Research & Audit Practices. 14(1). p.55.

Baumann, S., Lehner, O.M. and Losbichler, H., 2015. A push-and-pull factor model for

environmental management accounting: a contingency perspective. Journal of

Sustainable Finance & Investment. 5(3). pp.155-177.

Oldroyd, D., 2017. Estates, enterprise and investment at the dawn of the industrial revolution:

estate management and accounting in the North-East of England, c. 1700-1780.

Routledge.

Busco, C. and Quattrone, P., 2015. Exploring how the balanced scorecard engages and unfolds:

Articulating the visual power of accounting inscriptions. Contemporary Accounting

Research. 32(3). pp.1236-1262.

Grace, M. F., Leverty, J .T., Phillips, R .D. and Shimpi, P., 2015. The value of investing in

enterprise risk management. Journal of Risk and Insurance. 82(2). pp.289-316.

Sithole, S., Chandler, P., Abeysekera, I. and Paas, F., 2017. Benefits of guided self-management

of attention on learning accounting. Journal of Educational Psychology. 109(2). p.220.

Burritt, R .L. and Christ, K. L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management. 201. pp.72-81.

Arnaboldi, M., Busco, C. and Cuganesan, S., 2017. Accounting, accountability, social media and

big data: revolution or hype?. Accounting, auditing & accountability journal. 30(4).

pp.762-776.

Saeidi, S .P., Othman, M .S. H., Saeidi, P. and Saeidi, S. P., 2018. The moderating role of

environmental management accounting between environmental innovation and firm

financial performance. International Journal of Business Performance Management.

19(3). pp.326-348.

Hemmer, T. and Labro, E., 2017. Management Accounting and Operations Management. In The

Routledge Companion to Production and Operations Management (pp. 345-359).

Routledge.

Flamholtz, E .G., Baiserkeyev, O., Brzezinski, D., Dimitrova, A., Feng, D., Iliev, I., Milman, F.

and Rudnik, P., 2016. Overcoming Management Accounting Myopia: Broadening the

Strategic Focus . In☆ Advances in Management Accounting(pp. 73-121). Emerald

Group Publishing Limited.

Seal, W. and Mattimoe, R., 2016. The role of narrative in developing management control

knowledge from fieldwork: A pragmatic constructivist perspective. Qualitative

Research in Accounting & Management. 13(3). pp.330-349.

Jacobs, K., 2016. Theorising interdisciplinary public sector accounting research. Financial

Accountability & Management. 32(4). pp.469-488.

Books and journals:

Fleischman, R. K. and Parker, L. D., 2017. What is Past is Prologue: Cost Accounting in the

British Industrial Revolution. 1760-1850. Routledge.

Gurarda, S., 2015. Environmental management accounting. In Handbook of research on

developing sustainable value in economics, finance, and marketing (pp. 278-296). IGI

Global.

Verma, M., 2015. Inventory management accounting for obsolete inventory. IUP Journal of

Accounting Research & Audit Practices. 14(1). p.55.

Baumann, S., Lehner, O.M. and Losbichler, H., 2015. A push-and-pull factor model for

environmental management accounting: a contingency perspective. Journal of

Sustainable Finance & Investment. 5(3). pp.155-177.

Oldroyd, D., 2017. Estates, enterprise and investment at the dawn of the industrial revolution:

estate management and accounting in the North-East of England, c. 1700-1780.

Routledge.

Busco, C. and Quattrone, P., 2015. Exploring how the balanced scorecard engages and unfolds:

Articulating the visual power of accounting inscriptions. Contemporary Accounting

Research. 32(3). pp.1236-1262.

Grace, M. F., Leverty, J .T., Phillips, R .D. and Shimpi, P., 2015. The value of investing in

enterprise risk management. Journal of Risk and Insurance. 82(2). pp.289-316.

Sithole, S., Chandler, P., Abeysekera, I. and Paas, F., 2017. Benefits of guided self-management

of attention on learning accounting. Journal of Educational Psychology. 109(2). p.220.

Burritt, R .L. and Christ, K. L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management. 201. pp.72-81.

Arnaboldi, M., Busco, C. and Cuganesan, S., 2017. Accounting, accountability, social media and

big data: revolution or hype?. Accounting, auditing & accountability journal. 30(4).

pp.762-776.

Saeidi, S .P., Othman, M .S. H., Saeidi, P. and Saeidi, S. P., 2018. The moderating role of

environmental management accounting between environmental innovation and firm

financial performance. International Journal of Business Performance Management.

19(3). pp.326-348.

Hemmer, T. and Labro, E., 2017. Management Accounting and Operations Management. In The

Routledge Companion to Production and Operations Management (pp. 345-359).

Routledge.

Flamholtz, E .G., Baiserkeyev, O., Brzezinski, D., Dimitrova, A., Feng, D., Iliev, I., Milman, F.

and Rudnik, P., 2016. Overcoming Management Accounting Myopia: Broadening the

Strategic Focus . In☆ Advances in Management Accounting(pp. 73-121). Emerald

Group Publishing Limited.

Seal, W. and Mattimoe, R., 2016. The role of narrative in developing management control

knowledge from fieldwork: A pragmatic constructivist perspective. Qualitative

Research in Accounting & Management. 13(3). pp.330-349.

Jacobs, K., 2016. Theorising interdisciplinary public sector accounting research. Financial

Accountability & Management. 32(4). pp.469-488.

Akroyd, C., Biswas, S. S .N. and Chuang, S., 2016. How management control practices enable

strategic alignment during the product development process. In Advances in

management accounting. (pp. 99-138). Emerald Group Publishing Limited.

strategic alignment during the product development process. In Advances in

management accounting. (pp. 99-138). Emerald Group Publishing Limited.

APPENDIX

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.