Importance of Management Accounting System and Reports

VerifiedAdded on 2023/02/03

|17

|4767

|60

AI Summary

This document provides an in-depth understanding of the importance of various management accounting systems and reports in organizations. It discusses the techniques of cost analysis and their benefits, such as marginal costing, absorption costing, and break-even analysis. The document also highlights the integration of management accounting systems and reports in organizational processes.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK1.............................................................................................................................................1

P1. Importance of various management accounting system..................................................1

P2. Importance of management accounting report and its type.............................................3

M1 Evaluation of Benefits of various management accounting systems..............................4

D1 Integration of management accounting system and its reports in organisational process.1

TASK2.............................................................................................................................................1

P3. Appropriate techniques of cost analysis..........................................................................1

M2 A range of management accounting techniques..............................................................4

D2 Interpret data for a range of business activities................................................................4

TASK3.............................................................................................................................................4

P4 Advantages and disadvantages of planning tools used in budgetary control....................4

M3 Use of planning tool to prepare budget............................................................................6

TASK4.............................................................................................................................................7

P5 Financial problem and techniques to solve these problem................................................7

D3 Planning tools for solving financial issues.......................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK1.............................................................................................................................................1

P1. Importance of various management accounting system..................................................1

P2. Importance of management accounting report and its type.............................................3

M1 Evaluation of Benefits of various management accounting systems..............................4

D1 Integration of management accounting system and its reports in organisational process.1

TASK2.............................................................................................................................................1

P3. Appropriate techniques of cost analysis..........................................................................1

M2 A range of management accounting techniques..............................................................4

D2 Interpret data for a range of business activities................................................................4

TASK3.............................................................................................................................................4

P4 Advantages and disadvantages of planning tools used in budgetary control....................4

M3 Use of planning tool to prepare budget............................................................................6

TASK4.............................................................................................................................................7

P5 Financial problem and techniques to solve these problem................................................7

D3 Planning tools for solving financial issues.......................................................................8

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting is the practices of collecting useful information related to

business activity and recording of that data in accounting report that help manager to make

effective decision (Management accounting, 2018). Management of companies collect,

reminder, measure, control and examine the collected information that aid them to make policies

and strategies to succeed goal. It is a system which is followed by the management to resolve

various financial issues that may arise with the organisation. To realize the value of direction

accounting Airdri is chosen, it is hand dryer manufacture founded in 1974 and one of the small

enterprises of UK.

In this project report detailed information about management accounting their system and

importance of report is shown. Project focus on different costing method, various planning tool

which are useful in maintaining budgets and important of management accounting approaches to

resolve different financial problem faces by companies.

TASK1

P1. Importance of various management accounting system.

Accounting is a method of recording, maintaining, auditing and analysing important

financial information to the management and advise them on taxation matter. It is useful in

revealing the profit and loss for an accounting year and provides the values and nature of

organisation owner equity, assets and liabilities. Accounting is further divided in two categories

that are financial accounting and management accounting.

Management accounting is defines as the process of identifying, analysing, recording,

and presenting useful financial information which is used by internal manager for making

decision, improving performance, planning for future and controlling operation with an

organisation. This helps them to forecast various future events with the help of past experiences

and develop short and long term effective policies (Amidu, Effah and Abor, 2011).

Financial accounting refers to the tracking of firm's money transaction using centralised

standard to measure the economic performance for an accounting year. It is summarising and

presenting of transaction in financial report or financial statements such as cash flow or income

statements and balance sheet. In Airdri manager used three important accounting system to

1

Management accounting is the practices of collecting useful information related to

business activity and recording of that data in accounting report that help manager to make

effective decision (Management accounting, 2018). Management of companies collect,

reminder, measure, control and examine the collected information that aid them to make policies

and strategies to succeed goal. It is a system which is followed by the management to resolve

various financial issues that may arise with the organisation. To realize the value of direction

accounting Airdri is chosen, it is hand dryer manufacture founded in 1974 and one of the small

enterprises of UK.

In this project report detailed information about management accounting their system and

importance of report is shown. Project focus on different costing method, various planning tool

which are useful in maintaining budgets and important of management accounting approaches to

resolve different financial problem faces by companies.

TASK1

P1. Importance of various management accounting system.

Accounting is a method of recording, maintaining, auditing and analysing important

financial information to the management and advise them on taxation matter. It is useful in

revealing the profit and loss for an accounting year and provides the values and nature of

organisation owner equity, assets and liabilities. Accounting is further divided in two categories

that are financial accounting and management accounting.

Management accounting is defines as the process of identifying, analysing, recording,

and presenting useful financial information which is used by internal manager for making

decision, improving performance, planning for future and controlling operation with an

organisation. This helps them to forecast various future events with the help of past experiences

and develop short and long term effective policies (Amidu, Effah and Abor, 2011).

Financial accounting refers to the tracking of firm's money transaction using centralised

standard to measure the economic performance for an accounting year. It is summarising and

presenting of transaction in financial report or financial statements such as cash flow or income

statements and balance sheet. In Airdri manager used three important accounting system to

1

evaluate and analyse information like cost, performance and inventory. These are explained

below:

Cost accounting system: This system is help small and large company to examine and

improve its real profitability by estimating actual cost of its product. Cost accounting system

helps manager to measure the total cost that is incurred during the production of a particular

product. Airdri produces expensive hand dryer thus it require huge cost in the production so this

system is useful in this company. They use to record all the production related operation and help

them to get exact information cost which is involved in production process. There are mainly

three type of costing system. Actual costing is used to track and record direct costs that are

involved in producing a product (Carlsson-Wall, Kraus and Lind, 2015). For example in Airdri

manager uses to measure the cost of total hour utilised in manufacturing a product. Standard

costing is the analyses of difference between actual and budgeted cost like manager of Airdri

prepare a budgets of cost that is going to be involved in production process and then they

compare it with actual cost involved. Normal costing is used to derive the cost of a product. For

example in Airdri manager uses normal costing to derive the cost of hand dryer.

Inventory management system: This system is used by production organisation to

ascertain the actual information of stock lying with them. Manager track the inventory while it is

in transit, storehouse or in production process. Inventory lies within organisation in three basic

form which is raw material, goods in progress and finished good. In Airdri manager uses this

system to record the total inventory present in there production departments. They also manage

and record the total flow of raw material and finished hand dryer with this system. There are

various techniques of inventory management system to maintain effective report of their stock

such as perpetual and periodic inventory, FIFO, LIFO and JIT. Management of Airdri use FIFO

techniques in which earlier received stock will be used first for production of product (Dražić

Lutilsky and Dragija, 2012).

Job costing system: This system is mainly associated with evaluating and analysing cost

of individual job that is involved in different operation performed within the company. For

example in Airdri manager uses this system to analyse direct and indirect cost that is involved in

the production of hand dryer. So they can further reduce the cost if required and improve the

efficiency of business to increase the profitability of Airdri.

2

below:

Cost accounting system: This system is help small and large company to examine and

improve its real profitability by estimating actual cost of its product. Cost accounting system

helps manager to measure the total cost that is incurred during the production of a particular

product. Airdri produces expensive hand dryer thus it require huge cost in the production so this

system is useful in this company. They use to record all the production related operation and help

them to get exact information cost which is involved in production process. There are mainly

three type of costing system. Actual costing is used to track and record direct costs that are

involved in producing a product (Carlsson-Wall, Kraus and Lind, 2015). For example in Airdri

manager uses to measure the cost of total hour utilised in manufacturing a product. Standard

costing is the analyses of difference between actual and budgeted cost like manager of Airdri

prepare a budgets of cost that is going to be involved in production process and then they

compare it with actual cost involved. Normal costing is used to derive the cost of a product. For

example in Airdri manager uses normal costing to derive the cost of hand dryer.

Inventory management system: This system is used by production organisation to

ascertain the actual information of stock lying with them. Manager track the inventory while it is

in transit, storehouse or in production process. Inventory lies within organisation in three basic

form which is raw material, goods in progress and finished good. In Airdri manager uses this

system to record the total inventory present in there production departments. They also manage

and record the total flow of raw material and finished hand dryer with this system. There are

various techniques of inventory management system to maintain effective report of their stock

such as perpetual and periodic inventory, FIFO, LIFO and JIT. Management of Airdri use FIFO

techniques in which earlier received stock will be used first for production of product (Dražić

Lutilsky and Dragija, 2012).

Job costing system: This system is mainly associated with evaluating and analysing cost

of individual job that is involved in different operation performed within the company. For

example in Airdri manager uses this system to analyse direct and indirect cost that is involved in

the production of hand dryer. So they can further reduce the cost if required and improve the

efficiency of business to increase the profitability of Airdri.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

P2. Importance of management accounting report and its type.

Accounting report are very important that shows the exact picture about the company

performance. It is the systematic recording of every financial transaction to the report by

manager. Later these report are presented to shareholders both internal and external to show the

financial position about the company. These report are maintained at end of every quarter so that

management have the holistic view about the company finance. Management accounting reports

are crucial for small business firm like Airdri, as they derive important strategies to reduce cost

and maximise profit. Manager of Airdri prepare different type of report to ease decision making.

Some of the basic report are described below:

Budget Report: It is most fundamental report of management accounting as it help the

business owner to understand and control across with an organisation. They calculate the cost in

prior year and estimate budgets for the following year and determine the places to reduce cost. In

Airdri, manager prepare cost budgeted report to control expenditure involved in production of

product. They also estimate the future expenses and form strategies with the help of this report.

Importance: This report aid to predict the financial health and give the picture about the

overall operation of company. Management calculate the expense and monitor the revenue

generated during an accounting with the help of budgets report (Granlund, 2011).

Inventory management report: This report is prepared to record detail information

about the inventory laying in an organisation. It aid to make the supply chain more efficient, data

on inventory stock, labour and other expenses involved in production process. Management of

Airdri prepare these report to compare different distribution channels within company to provide

best manner of supply their product. They also maintain record of total stock available, goods in

transit and finished product.

Importance: This report have major importance in management accounting as manager

keep a track record of stock present within the company. Inventory management report aid them

to record all quantity of product in warehouses and maintain proper flow of the product.

Account receivable report: These report are crucial for every organisation that provide

good and services on credit to their buyers. It helps to determine the exact outstanding amount

form debtor and prepare depending on the days of outstanding. Manager of Airdri prepare these

report to evaluate the total amount which is need to be recovered form their client. It keeps the

systematic record of those buyers who have not paid full amount at the time of purchase.

3

Accounting report are very important that shows the exact picture about the company

performance. It is the systematic recording of every financial transaction to the report by

manager. Later these report are presented to shareholders both internal and external to show the

financial position about the company. These report are maintained at end of every quarter so that

management have the holistic view about the company finance. Management accounting reports

are crucial for small business firm like Airdri, as they derive important strategies to reduce cost

and maximise profit. Manager of Airdri prepare different type of report to ease decision making.

Some of the basic report are described below:

Budget Report: It is most fundamental report of management accounting as it help the

business owner to understand and control across with an organisation. They calculate the cost in

prior year and estimate budgets for the following year and determine the places to reduce cost. In

Airdri, manager prepare cost budgeted report to control expenditure involved in production of

product. They also estimate the future expenses and form strategies with the help of this report.

Importance: This report aid to predict the financial health and give the picture about the

overall operation of company. Management calculate the expense and monitor the revenue

generated during an accounting with the help of budgets report (Granlund, 2011).

Inventory management report: This report is prepared to record detail information

about the inventory laying in an organisation. It aid to make the supply chain more efficient, data

on inventory stock, labour and other expenses involved in production process. Management of

Airdri prepare these report to compare different distribution channels within company to provide

best manner of supply their product. They also maintain record of total stock available, goods in

transit and finished product.

Importance: This report have major importance in management accounting as manager

keep a track record of stock present within the company. Inventory management report aid them

to record all quantity of product in warehouses and maintain proper flow of the product.

Account receivable report: These report are crucial for every organisation that provide

good and services on credit to their buyers. It helps to determine the exact outstanding amount

form debtor and prepare depending on the days of outstanding. Manager of Airdri prepare these

report to evaluate the total amount which is need to be recovered form their client. It keeps the

systematic record of those buyers who have not paid full amount at the time of purchase.

3

Importance: This report is also important of manager as they determine total amount of

revenue to be generated in future and help to improve credit policy. With the help of account

receivable report management modify the collection process of Airdri.

Operating report: This report is tools that are used to reiterate the status of a project or

operation. Management distribute these report to experience employee for setting goal and

appraise performance of other worker working in any operation activity. In Airdri manager uses

these report to record the daily functioning of different operation related to production of Hand

dryer. This helps the, top manager to increase the profitability of operation and increase

efficiency of worker. Maintaining a daily operational performance report helps them to inform

other employee about the business condition so they make better decision.

Importance: Major importance of this report is to provide detail information about the

operation of business. So that management of organisation can make a effective decision in

respect if operation are not profitable (Johnson, 2013).

M1 Evaluation of Benefits of various management accounting systems.

System Benefits

Cost accounting system This system helps managers so that they can analyse

most profitable products for company.

It helps managers to ascertain faithful prices for

products by furnish the accurate data of cost.

Inventory management system Managers with the help of this system increase

efficiency and profitability of company by maintaining

stock.

It increases level of transparent information of

inventory.

Job costing system Managers ascertain the profitability of individual job

performed within an organisation.

It provides detailed information of cost like labour and

overheads which is involved in different jobs of

company.

4

revenue to be generated in future and help to improve credit policy. With the help of account

receivable report management modify the collection process of Airdri.

Operating report: This report is tools that are used to reiterate the status of a project or

operation. Management distribute these report to experience employee for setting goal and

appraise performance of other worker working in any operation activity. In Airdri manager uses

these report to record the daily functioning of different operation related to production of Hand

dryer. This helps the, top manager to increase the profitability of operation and increase

efficiency of worker. Maintaining a daily operational performance report helps them to inform

other employee about the business condition so they make better decision.

Importance: Major importance of this report is to provide detail information about the

operation of business. So that management of organisation can make a effective decision in

respect if operation are not profitable (Johnson, 2013).

M1 Evaluation of Benefits of various management accounting systems.

System Benefits

Cost accounting system This system helps managers so that they can analyse

most profitable products for company.

It helps managers to ascertain faithful prices for

products by furnish the accurate data of cost.

Inventory management system Managers with the help of this system increase

efficiency and profitability of company by maintaining

stock.

It increases level of transparent information of

inventory.

Job costing system Managers ascertain the profitability of individual job

performed within an organisation.

It provides detailed information of cost like labour and

overheads which is involved in different jobs of

company.

4

D1 Integration of management accounting system and its reports in organisational process.

Management accounting system and various report are very important for every

organisation to grow as these system and report help to record and measure performance of

company. This provide detail information to control cost, amount owned by debtors and financial

position of company etc. Budget report are useful in estimating total cost, account receivable

reports can help the managers to improve the credit policies and collection process. Inventory

management report is useful to track the stock available in warehouse and inventory in whole

supply business. Whereas, operational report are useful to keep record of daily business activity

performed within an organisation. These all report help them to increase the efficiency of

company and improve performance of business (JOSHI and et. al, 2011).

TASK2

P3. Appropriate techniques of cost analysis.

Cost is that amount which is paid to get something it is usually the movement of money from

buyer to seller. In business, it is the monetary value which is going to be sold by seller that includes

cost of direct material, overheads, labour etc. All expenses are cost, but all cost are not considered as

expenses because some are incurred in the acquisition of income generating assets. Manager of

company have to be able to determine the costs of product or services they offer for sale so that they

can generate more profit. Every organisation wants to earn huge profit so they fir appropriate price

for their product keeping actual cost in mind. Faithful cost of product will attract more number of

customers. There are many types of cost such as direct cost and indirect cost that should be managed

by manager of business to generate more revenue.

Managers in Airdri should fix such cost or selling prices for the hand dryer that may attract

more customers and aid to acquire more market share. Cost of products includes different direct and

indirect expenses. Following techniques are followed by managers of chosen company to calculate

their net profits:

Marginal costing: This is the total cost involved in production on one additional unit of

output. The main purpose of analysing marginal cost is to ascertain the best point for an organisation

so it can achieve maximum profit. Marginal costing is a code whereby variable cost are charged to

cost units and the fixed cost aspects to the applicable period is carved off in full against the input for

that period. So in common bit is known as variable costing also in which only variable cost are

Management accounting system and various report are very important for every

organisation to grow as these system and report help to record and measure performance of

company. This provide detail information to control cost, amount owned by debtors and financial

position of company etc. Budget report are useful in estimating total cost, account receivable

reports can help the managers to improve the credit policies and collection process. Inventory

management report is useful to track the stock available in warehouse and inventory in whole

supply business. Whereas, operational report are useful to keep record of daily business activity

performed within an organisation. These all report help them to increase the efficiency of

company and improve performance of business (JOSHI and et. al, 2011).

TASK2

P3. Appropriate techniques of cost analysis.

Cost is that amount which is paid to get something it is usually the movement of money from

buyer to seller. In business, it is the monetary value which is going to be sold by seller that includes

cost of direct material, overheads, labour etc. All expenses are cost, but all cost are not considered as

expenses because some are incurred in the acquisition of income generating assets. Manager of

company have to be able to determine the costs of product or services they offer for sale so that they

can generate more profit. Every organisation wants to earn huge profit so they fir appropriate price

for their product keeping actual cost in mind. Faithful cost of product will attract more number of

customers. There are many types of cost such as direct cost and indirect cost that should be managed

by manager of business to generate more revenue.

Managers in Airdri should fix such cost or selling prices for the hand dryer that may attract

more customers and aid to acquire more market share. Cost of products includes different direct and

indirect expenses. Following techniques are followed by managers of chosen company to calculate

their net profits:

Marginal costing: This is the total cost involved in production on one additional unit of

output. The main purpose of analysing marginal cost is to ascertain the best point for an organisation

so it can achieve maximum profit. Marginal costing is a code whereby variable cost are charged to

cost units and the fixed cost aspects to the applicable period is carved off in full against the input for

that period. So in common bit is known as variable costing also in which only variable cost are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accumulated and cost accumulated and cost per units is determined depending upon variable cost

(Klychova, Faskhutdinova and Sadrieva, 2014).

2

(Klychova, Faskhutdinova and Sadrieva, 2014).

2

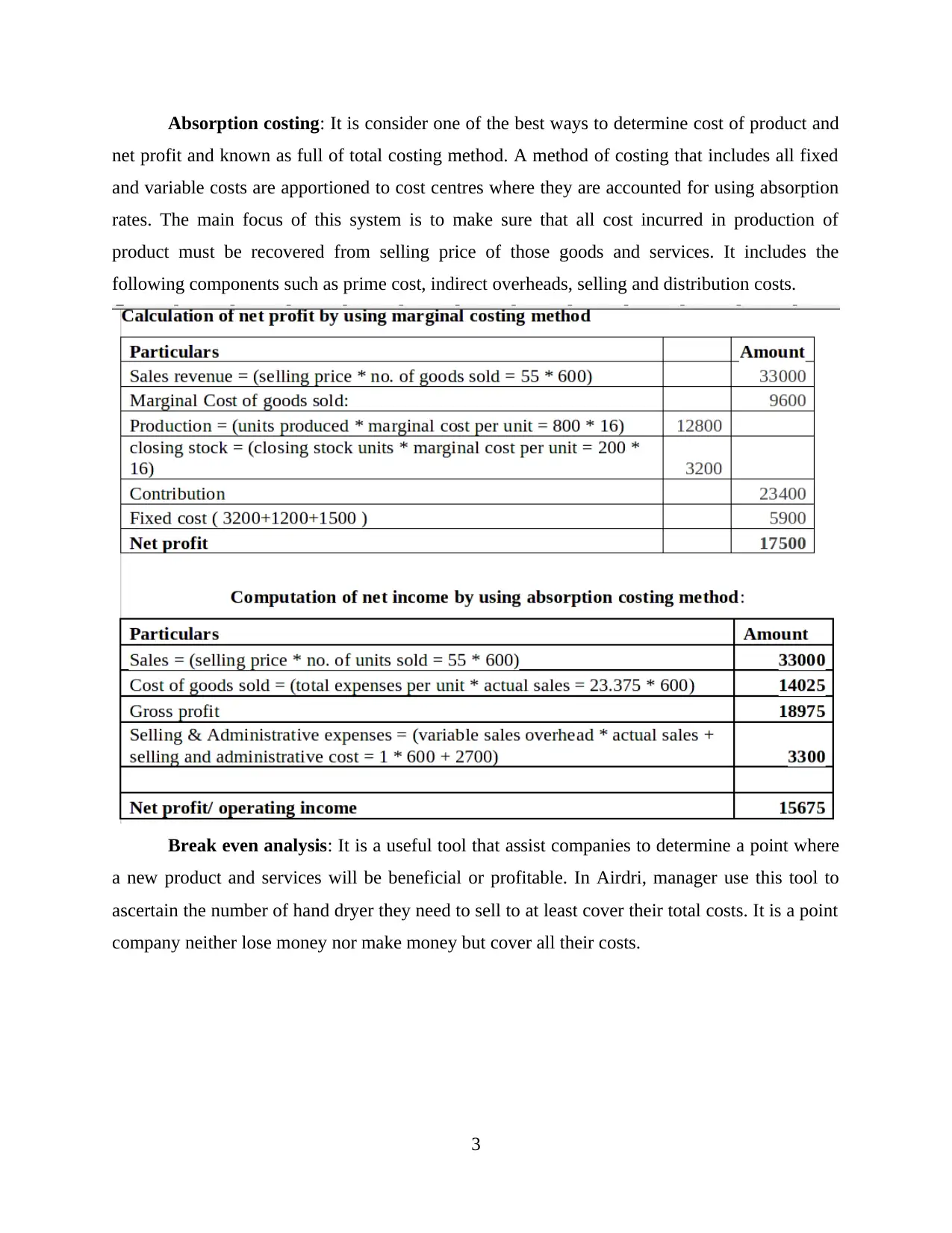

Absorption costing: It is consider one of the best ways to determine cost of product and

net profit and known as full of total costing method. A method of costing that includes all fixed

and variable costs are apportioned to cost centres where they are accounted for using absorption

rates. The main focus of this system is to make sure that all cost incurred in production of

product must be recovered from selling price of those goods and services. It includes the

following components such as prime cost, indirect overheads, selling and distribution costs.

Break even analysis: It is a useful tool that assist companies to determine a point where

a new product and services will be beneficial or profitable. In Airdri, manager use this tool to

ascertain the number of hand dryer they need to sell to at least cover their total costs. It is a point

company neither lose money nor make money but cover all their costs.

3

net profit and known as full of total costing method. A method of costing that includes all fixed

and variable costs are apportioned to cost centres where they are accounted for using absorption

rates. The main focus of this system is to make sure that all cost incurred in production of

product must be recovered from selling price of those goods and services. It includes the

following components such as prime cost, indirect overheads, selling and distribution costs.

Break even analysis: It is a useful tool that assist companies to determine a point where

a new product and services will be beneficial or profitable. In Airdri, manager use this tool to

ascertain the number of hand dryer they need to sell to at least cover their total costs. It is a point

company neither lose money nor make money but cover all their costs.

3

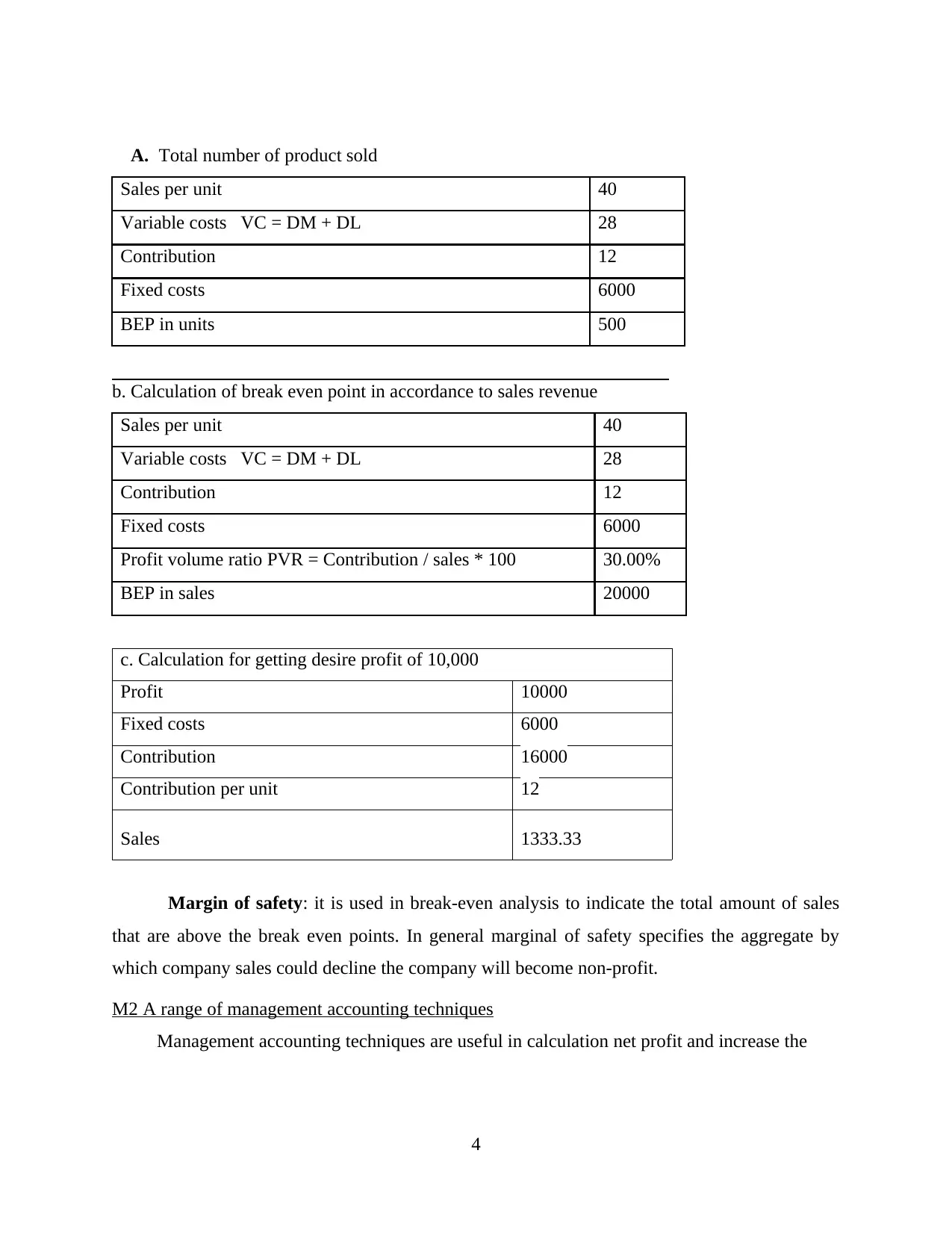

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: it is used in break-even analysis to indicate the total amount of sales

that are above the break even points. In general marginal of safety specifies the aggregate by

which company sales could decline the company will become non-profit.

M2 A range of management accounting techniques

Management accounting techniques are useful in calculation net profit and increase the

4

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: it is used in break-even analysis to indicate the total amount of sales

that are above the break even points. In general marginal of safety specifies the aggregate by

which company sales could decline the company will become non-profit.

M2 A range of management accounting techniques

Management accounting techniques are useful in calculation net profit and increase the

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

efficiency of organisation. In Airdri, manager uses different costing method to calculated net

profit for current accounting year like marginal absorption costing. Management also follows

two types of tool marginal tool and historical tool.

D2 Interpret data for a range of business activities

From the above calculation of marginal and absorption costing it is observed that

management of airdri tries to make best result from these methods. As a result, net profit

generated from marginal costing is $17500 and net margin of Profit Company earned by

using absorption costing techniques is $15675. So it is clear marginal costing is more

benefited for Airdri to calculate net profit. Break-even point of company is determined by

selling 500 units and sales ate $6000. In respect if company wants a desired profit of

$10000 than total units they have to sell is 1333.33.

TASK3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget: It is an estimation of incomes and expenditures for a specific period of time. A

budget is prepared by the managers of a company with the help of previous year data and current

market trends. It is formulated to perform organisational activities and presented to the internal

stakeholders (Mistry, Sharma and Low, 2014).

Cash budget: It is known as an estimation of money inflows and outflows for a business

over a particular timeframe. This specific spending budget is utilized to assess, regardless of

whether Oak Cash and Carry Ltd has adequate money to work their business in not so distant

future time. It is classes into two section, for example,

Cash receipts: It is essentially said to be a measure of cash hold by an organization

available to be purchased of goods and services. Accountant of Oak Cash and Carry Ltd can add

money receipts to be adjust brought down to give organization additional sum of trade current

cast at present organization.

Cash payment: It is a type of journal record i.e. used to record transaction that is paid in

form of money. A cash payment comprises of paying a bank or commission charge or pull back

money. In the activity that any of payment made in real money is recorded into money book.

Advantage: It fits well with the prerequisite for consistence and costs control. Costs are

arranged through association and protest of consumption.

5

profit for current accounting year like marginal absorption costing. Management also follows

two types of tool marginal tool and historical tool.

D2 Interpret data for a range of business activities

From the above calculation of marginal and absorption costing it is observed that

management of airdri tries to make best result from these methods. As a result, net profit

generated from marginal costing is $17500 and net margin of Profit Company earned by

using absorption costing techniques is $15675. So it is clear marginal costing is more

benefited for Airdri to calculate net profit. Break-even point of company is determined by

selling 500 units and sales ate $6000. In respect if company wants a desired profit of

$10000 than total units they have to sell is 1333.33.

TASK3

P4 Advantages and disadvantages of planning tools used in budgetary control

Budget: It is an estimation of incomes and expenditures for a specific period of time. A

budget is prepared by the managers of a company with the help of previous year data and current

market trends. It is formulated to perform organisational activities and presented to the internal

stakeholders (Mistry, Sharma and Low, 2014).

Cash budget: It is known as an estimation of money inflows and outflows for a business

over a particular timeframe. This specific spending budget is utilized to assess, regardless of

whether Oak Cash and Carry Ltd has adequate money to work their business in not so distant

future time. It is classes into two section, for example,

Cash receipts: It is essentially said to be a measure of cash hold by an organization

available to be purchased of goods and services. Accountant of Oak Cash and Carry Ltd can add

money receipts to be adjust brought down to give organization additional sum of trade current

cast at present organization.

Cash payment: It is a type of journal record i.e. used to record transaction that is paid in

form of money. A cash payment comprises of paying a bank or commission charge or pull back

money. In the activity that any of payment made in real money is recorded into money book.

Advantage: It fits well with the prerequisite for consistence and costs control. Costs are

arranged through association and protest of consumption.

5

Disadvantage: It can't neglect issues of government points, their association with

spending plan and administrations to be conveyed by government.

Master budget: It is known as the mixture of spending plans of lower level created by

organization's administrators occupied with planning process and incorporates planned financial

statements, financing plan and cash flows likewise. This financial plan is introduced might be

Fifty-fifty yearly or quarterly or might be yearly. A narrative clarification as note might be

appended with ace spending which clarifies arranging and key course of organization.

As master budget is fundamental arranging instrument utilized by administration group to

perform and coordinate the exercises of association and in addition utilized for execution

examination of financial department of the company (Moser, 2012).

Income statement: It is the money related record which represents organization's

financial performance over specified bookkeeping period. It additionally proves received

incomes and costs through both operating and non-operating activities. However, it represents

the end net profit or losses that are taken about by a management during the period of time.

Income statements are also commonly known as Profit and Loss statements.

Balance sheet: It is additionally one of most critical last financial statements of

organization which provides the entire position of organization. The accounting report

additionally discloses organization’s aggregate resources and liabilities that is mentioned under

the income statement of the company, or helps in determining the financial position of the

company. There are two parts of balance sheet one is assets part which proves the estimates of

total current assets and total non-current assets. Second part indicates data about liabilities and

additionally included into to investors value.

Benefits: This type of spending helps in getting ready for future occasions as this

financial plan consolidates all parts of future. It has spending plans of the considerable number of

offices because of administration can without much of a stretch recognize what office causing

issues in organization.

Limitation: Along with merits, there are couple of constraints are additionally present

which expresses that this kind of spending plan is hard to refresh and there is absence of

specificity (Ruiz-de-Arbulo-Lopez, Fortuny-Santos and Cuatrecasas-Arbós, 2013

).

6

spending plan and administrations to be conveyed by government.

Master budget: It is known as the mixture of spending plans of lower level created by

organization's administrators occupied with planning process and incorporates planned financial

statements, financing plan and cash flows likewise. This financial plan is introduced might be

Fifty-fifty yearly or quarterly or might be yearly. A narrative clarification as note might be

appended with ace spending which clarifies arranging and key course of organization.

As master budget is fundamental arranging instrument utilized by administration group to

perform and coordinate the exercises of association and in addition utilized for execution

examination of financial department of the company (Moser, 2012).

Income statement: It is the money related record which represents organization's

financial performance over specified bookkeeping period. It additionally proves received

incomes and costs through both operating and non-operating activities. However, it represents

the end net profit or losses that are taken about by a management during the period of time.

Income statements are also commonly known as Profit and Loss statements.

Balance sheet: It is additionally one of most critical last financial statements of

organization which provides the entire position of organization. The accounting report

additionally discloses organization’s aggregate resources and liabilities that is mentioned under

the income statement of the company, or helps in determining the financial position of the

company. There are two parts of balance sheet one is assets part which proves the estimates of

total current assets and total non-current assets. Second part indicates data about liabilities and

additionally included into to investors value.

Benefits: This type of spending helps in getting ready for future occasions as this

financial plan consolidates all parts of future. It has spending plans of the considerable number of

offices because of administration can without much of a stretch recognize what office causing

issues in organization.

Limitation: Along with merits, there are couple of constraints are additionally present

which expresses that this kind of spending plan is hard to refresh and there is absence of

specificity (Ruiz-de-Arbulo-Lopez, Fortuny-Santos and Cuatrecasas-Arbós, 2013

).

6

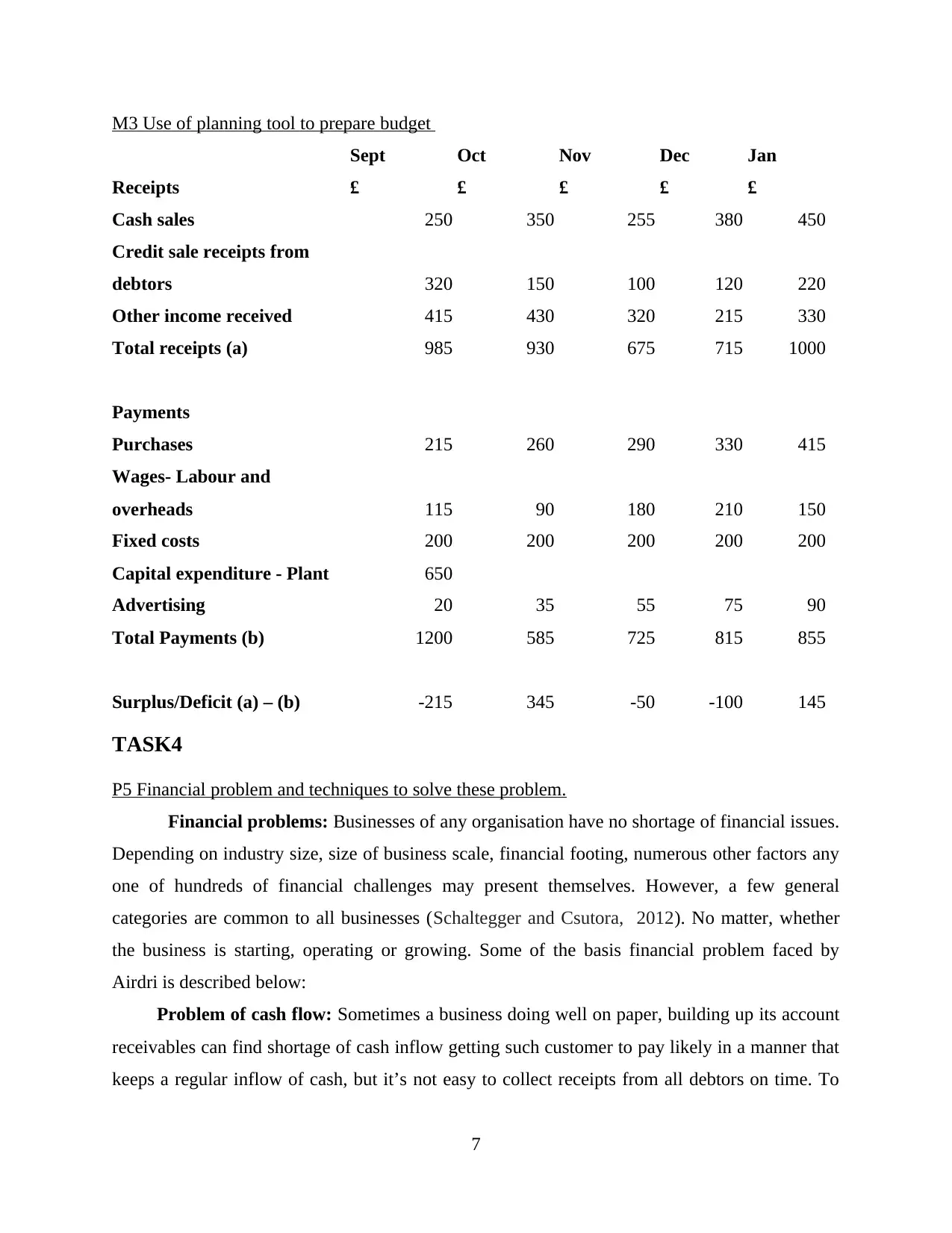

M3 Use of planning tool to prepare budget

Sept Oct Nov Dec Jan

Receipts £ £ £ £ £

Cash sales 250 350 255 380 450

Credit sale receipts from

debtors 320 150 100 120 220

Other income received 415 430 320 215 330

Total receipts (a) 985 930 675 715 1000

Payments

Purchases 215 260 290 330 415

Wages- Labour and

overheads 115 90 180 210 150

Fixed costs 200 200 200 200 200

Capital expenditure - Plant 650

Advertising 20 35 55 75 90

Total Payments (b) 1200 585 725 815 855

Surplus/Deficit (a) – (b) -215 345 -50 -100 145

TASK4

P5 Financial problem and techniques to solve these problem.

Financial problems: Businesses of any organisation have no shortage of financial issues.

Depending on industry size, size of business scale, financial footing, numerous other factors any

one of hundreds of financial challenges may present themselves. However, a few general

categories are common to all businesses (Schaltegger and Csutora, 2012). No matter, whether

the business is starting, operating or growing. Some of the basis financial problem faced by

Airdri is described below:

Problem of cash flow: Sometimes a business doing well on paper, building up its account

receivables can find shortage of cash inflow getting such customer to pay likely in a manner that

keeps a regular inflow of cash, but it’s not easy to collect receipts from all debtors on time. To

7

Sept Oct Nov Dec Jan

Receipts £ £ £ £ £

Cash sales 250 350 255 380 450

Credit sale receipts from

debtors 320 150 100 120 220

Other income received 415 430 320 215 330

Total receipts (a) 985 930 675 715 1000

Payments

Purchases 215 260 290 330 415

Wages- Labour and

overheads 115 90 180 210 150

Fixed costs 200 200 200 200 200

Capital expenditure - Plant 650

Advertising 20 35 55 75 90

Total Payments (b) 1200 585 725 815 855

Surplus/Deficit (a) – (b) -215 345 -50 -100 145

TASK4

P5 Financial problem and techniques to solve these problem.

Financial problems: Businesses of any organisation have no shortage of financial issues.

Depending on industry size, size of business scale, financial footing, numerous other factors any

one of hundreds of financial challenges may present themselves. However, a few general

categories are common to all businesses (Schaltegger and Csutora, 2012). No matter, whether

the business is starting, operating or growing. Some of the basis financial problem faced by

Airdri is described below:

Problem of cash flow: Sometimes a business doing well on paper, building up its account

receivables can find shortage of cash inflow getting such customer to pay likely in a manner that

keeps a regular inflow of cash, but it’s not easy to collect receipts from all debtors on time. To

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

avoid these challenges, maintain good collection methods, set up the payment criteria in written

contracts and screen customers before extending credit or payment.

Lack of money management: In Airdri, manger lacks the skill to manage their funds and

they face the problem of shortage of fund. They do not have proper knowledge to control their

expenses.

More spending than earning: In Airdri, manager spends more revenue on sales promotion

activities to increase their sales. But as a result company is not able to generate income and there

is a chance of new financial problem. Their promotion activities are not able to attract more

customer there low sales for the period (Ward, 2012).

To resolve these financial problem companies follows various management accounting

approaches such as benchmarking and KPI.

Benchmarking: In business world, companies uses benchmarking as appoint of references

as they form reports as a way to compare themselves to the other companies within the same

industry. This is the practice of a business firm comparing key metrics of their operation to the

other similar organisation. In Airdri management uses this approaches to make report that are

followed by other manufacture companies within the same industry. The prepare benchmark

report related to money management that are being used by other companies and improve

efficiency of manager to manage money.

KPI (Key performance indictors): This indicators are consider to be firm metrics by business

associate and other director to path and examine component hold important for future growth and

development (Wickramasinghe, and Alawattage, 2012). In Airdri manager uses this approaches

to comparison and fit accomplished regulation that assist them in resolution commercial

enterprise issue related to more spending than earning. They form standard at every level so that

expenses are monitor and control by the management easily.

Comparison

Airdri Agmet solution

Management of selected firm applies the

approach of benchmark in order to set standard

that support to firmness the business problem

that is of lack of money management. As they

In this organisation the concept benchmarking

has been applied in order to provide valid

solution to the problems of sales but no profit.

8

contracts and screen customers before extending credit or payment.

Lack of money management: In Airdri, manger lacks the skill to manage their funds and

they face the problem of shortage of fund. They do not have proper knowledge to control their

expenses.

More spending than earning: In Airdri, manager spends more revenue on sales promotion

activities to increase their sales. But as a result company is not able to generate income and there

is a chance of new financial problem. Their promotion activities are not able to attract more

customer there low sales for the period (Ward, 2012).

To resolve these financial problem companies follows various management accounting

approaches such as benchmarking and KPI.

Benchmarking: In business world, companies uses benchmarking as appoint of references

as they form reports as a way to compare themselves to the other companies within the same

industry. This is the practice of a business firm comparing key metrics of their operation to the

other similar organisation. In Airdri management uses this approaches to make report that are

followed by other manufacture companies within the same industry. The prepare benchmark

report related to money management that are being used by other companies and improve

efficiency of manager to manage money.

KPI (Key performance indictors): This indicators are consider to be firm metrics by business

associate and other director to path and examine component hold important for future growth and

development (Wickramasinghe, and Alawattage, 2012). In Airdri manager uses this approaches

to comparison and fit accomplished regulation that assist them in resolution commercial

enterprise issue related to more spending than earning. They form standard at every level so that

expenses are monitor and control by the management easily.

Comparison

Airdri Agmet solution

Management of selected firm applies the

approach of benchmark in order to set standard

that support to firmness the business problem

that is of lack of money management. As they

In this organisation the concept benchmarking

has been applied in order to provide valid

solution to the problems of sales but no profit.

8

adopt the policies followed by other companies

within the same industry (Zainun Tuanmat

and Smith, 2011).

In above mention company director resolve

the content of more disbursement than

spending by applying the accounting

approaches of KPI.

In Agmet solution management utilize the

methods of JIT in order to defeat the difficulty

of more payment on promotion activities.

D3 Planning tools for solving financial issues

Manager of respective company prepare effective budgets to estimate and control value

to raise the presentation of worker to improve the productivity. Planning play an important role

to handle in tough circumstances and any kind of fiscal problems that may raised in upcoming

time frame (Windolph, and Moeller, 2012). They applies the techniques of key performance

indicator and benchmarking to provide valuable solution in order to overcome the above

described issues that could hamper the business performance. The different situation such as

money management and control their expenses that help in expansion of business and generate

more profit.

CONCLUSION

From above report it has been concluded that management accounting is very useful in

the context of an organisation. It plays an important role in the internal management of any

business. In addition, management accounting consists various kind of reports like performance

report, budget report etc. Each of these reports are very crucial for managing the business in a

right way.

9

within the same industry (Zainun Tuanmat

and Smith, 2011).

In above mention company director resolve

the content of more disbursement than

spending by applying the accounting

approaches of KPI.

In Agmet solution management utilize the

methods of JIT in order to defeat the difficulty

of more payment on promotion activities.

D3 Planning tools for solving financial issues

Manager of respective company prepare effective budgets to estimate and control value

to raise the presentation of worker to improve the productivity. Planning play an important role

to handle in tough circumstances and any kind of fiscal problems that may raised in upcoming

time frame (Windolph, and Moeller, 2012). They applies the techniques of key performance

indicator and benchmarking to provide valuable solution in order to overcome the above

described issues that could hamper the business performance. The different situation such as

money management and control their expenses that help in expansion of business and generate

more profit.

CONCLUSION

From above report it has been concluded that management accounting is very useful in

the context of an organisation. It plays an important role in the internal management of any

business. In addition, management accounting consists various kind of reports like performance

report, budget report etc. Each of these reports are very crucial for managing the business in a

right way.

9

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journal:

Amidu, M., Effah, J. and Abor, J., 2011. E-accounting practices among small and medium

enterprises in Ghana. Journal of Management Policy and Practice. 12(4). pp.146-155.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Dražić Lutilsky, I. and Dragija, M., 2012. Activity based costing as a means to full costing–

possibilities and constraints for European universities. Management: Journal of

contemporary management issues. 17(1). pp.33-57.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Johnson, H. T., 2013. A New Approach to Management Accounting History (RLE Accounting).

Routledge.

JOSHI, P. L., and et. al., 2011. Diffusion of management accounting practices in gulf

cooperation council countries. Accounting Perspectives. 10(1). pp.23-53.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E.R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences. 5(24). p.79.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Moser, D. V., 2012. Is accounting research stagnant ?. Accounting Horizons. 26(4). pp.845-850.

Ruiz-de-Arbulo-Lopez, P., Fortuny-Santos, J. and Cuatrecasas-Arbós, L., 2013. Lean

manufacturing: costing the value stream. Industrial Management & Data

Systems. 113(5). pp.647-668.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Zainun Tuanmat, T. and Smith, M., 2011. Changes in management accounting practices in

Malaysia. Asian Review of Accounting. 19(3). pp.221-242.

Online

Management accounting. 2018. [Online]. Available through:

<https://www.invensis.net/blog/finance-and-accounting/what-is-management-accounting-

and-its-importance/>

11

Books and Journal:

Amidu, M., Effah, J. and Abor, J., 2011. E-accounting practices among small and medium

enterprises in Ghana. Journal of Management Policy and Practice. 12(4). pp.146-155.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Dražić Lutilsky, I. and Dragija, M., 2012. Activity based costing as a means to full costing–

possibilities and constraints for European universities. Management: Journal of

contemporary management issues. 17(1). pp.33-57.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Johnson, H. T., 2013. A New Approach to Management Accounting History (RLE Accounting).

Routledge.

JOSHI, P. L., and et. al., 2011. Diffusion of management accounting practices in gulf

cooperation council countries. Accounting Perspectives. 10(1). pp.23-53.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E.R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences. 5(24). p.79.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Moser, D. V., 2012. Is accounting research stagnant ?. Accounting Horizons. 26(4). pp.845-850.

Ruiz-de-Arbulo-Lopez, P., Fortuny-Santos, J. and Cuatrecasas-Arbós, L., 2013. Lean

manufacturing: costing the value stream. Industrial Management & Data

Systems. 113(5). pp.647-668.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Zainun Tuanmat, T. and Smith, M., 2011. Changes in management accounting practices in

Malaysia. Asian Review of Accounting. 19(3). pp.221-242.

Online

Management accounting. 2018. [Online]. Available through:

<https://www.invensis.net/blog/finance-and-accounting/what-is-management-accounting-

and-its-importance/>

11

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.