Analysis of Management Accounting Systems

VerifiedAdded on 2020/10/22

|14

|4196

|283

AI Summary

The assignment provides a comprehensive overview of management accounting systems, discussing the role of cost and management accounting in addressing financial problems. It also examines the impact of total quality management adoption on small and medium enterprises' financial performance and reviews public sector budgeting practices. The document includes references to various books and journals that support the analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different type of management accounting system................................................................3

P2 Different type of management accounting reports.................................................................5

TASK 2............................................................................................................................................6

P3. Range of management accounting techniques.......................................................................6

TASK 3............................................................................................................................................9

P4.Planning tools used in management accounting.....................................................................9

P5. Comparison of organisations adapting management accounting to respond to financial

problems. ...................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different type of management accounting system................................................................3

P2 Different type of management accounting reports.................................................................5

TASK 2............................................................................................................................................6

P3. Range of management accounting techniques.......................................................................6

TASK 3............................................................................................................................................9

P4.Planning tools used in management accounting.....................................................................9

P5. Comparison of organisations adapting management accounting to respond to financial

problems. ...................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

In the today's present business scenario, there is an essential need of appropriate a skilled

management system that help to control the valuable operation of company in order to increase

the efficiency of business (Collis and Hussey, 2017). Management accounting is a procedure

related with analysing, controlling, managing useful financial information within a business firm

in order to make meaningful decision by the top level manager for growing and developing

profitability in specific period of time. The entire process of cost or managerial accounting start

by gathering, reporting, calculating, measuring, analysing and transferring valuable financial

information of company that are helpful to accomplish the desired goals in predefined time

period. To better understand the importance of management accounting KEF LTD is selected

that is a manufacturing company.

In this report, understanding of various system and reports are demonstrated, by applying

valuable accounting techniques production cost per unit, budgeted P&L statements etc. are

calculated. In addition, report also discuss the use of different planning tool that are used in

management accounting and the ways different system help to respond financial problems.

TASK 1

P1. Different type of management accounting system

In the business context, the concept of management accounting is consider to be an

internal befitting system that support to calculate or measure the overall performance of assorted

units within business firm. Manager usually set standard for evaluating performance, examining

various strategies which support in accomplishing defined goals also aid to make out actual

reasons in deviations for current objective (Schaltegger, Burritt and Petersen, 2017). In business

term, management accounting usually deliver the non-financial and financial data to the manager

and other employees of firm that help to make best effective decision in order to increase the

profitability, productivity and attain goals. There are various useful system of management

accounting that help the management of KEF Ltd that are defined below:

Inventory management system: This system helps to manage inventory of business firm

in form of raw material, goods in transact and finished goods. There are various methods for

controlling stock of company like FIFO, LIFO and Average method that provide the strength to

supply chain of company. In KEF Ltd FIFO method is applied as with this method they are able

In the today's present business scenario, there is an essential need of appropriate a skilled

management system that help to control the valuable operation of company in order to increase

the efficiency of business (Collis and Hussey, 2017). Management accounting is a procedure

related with analysing, controlling, managing useful financial information within a business firm

in order to make meaningful decision by the top level manager for growing and developing

profitability in specific period of time. The entire process of cost or managerial accounting start

by gathering, reporting, calculating, measuring, analysing and transferring valuable financial

information of company that are helpful to accomplish the desired goals in predefined time

period. To better understand the importance of management accounting KEF LTD is selected

that is a manufacturing company.

In this report, understanding of various system and reports are demonstrated, by applying

valuable accounting techniques production cost per unit, budgeted P&L statements etc. are

calculated. In addition, report also discuss the use of different planning tool that are used in

management accounting and the ways different system help to respond financial problems.

TASK 1

P1. Different type of management accounting system

In the business context, the concept of management accounting is consider to be an

internal befitting system that support to calculate or measure the overall performance of assorted

units within business firm. Manager usually set standard for evaluating performance, examining

various strategies which support in accomplishing defined goals also aid to make out actual

reasons in deviations for current objective (Schaltegger, Burritt and Petersen, 2017). In business

term, management accounting usually deliver the non-financial and financial data to the manager

and other employees of firm that help to make best effective decision in order to increase the

profitability, productivity and attain goals. There are various useful system of management

accounting that help the management of KEF Ltd that are defined below:

Inventory management system: This system helps to manage inventory of business firm

in form of raw material, goods in transact and finished goods. There are various methods for

controlling stock of company like FIFO, LIFO and Average method that provide the strength to

supply chain of company. In KEF Ltd FIFO method is applied as with this method they are able

to remove old goods and also reduces losses due to obsolescence. First in First out help KEF Ltd

to produced product as per the trends in market and customer preferences this help to grow

profit.

Cost accounting system: It is used to determine the cost of total production of various

goods manufacture by company. It basically includes total cost at several level and also include

fixed cost that help to determine the profit. There are useful method of accounting cost such as,

marginal and absorption costing, lean costing, activity and standard costing method. In

respective company Activity based costing method is used that basically assigns total cost to

goods which are related with producing goods (Humphrey, C. and Miller, 2012).

Job Coasting system: This method mainly record the cost which are related with

producing good job within an organisation. It assist to delegate manufacturing cost to each good

and product director and accountant have evidence of cost of each product. This system also

support in calculating cost of various product that are manufacture by company in same period of

time. Thus, in KEF Ltd this system help to evaluate and measure the cost of various useful

product that are produced by company in order to meet the customer needs.

Price optimisation system: This is considered to be most important system for company

as it help to determine the customer reaction on prices set by company for manufacture product.

Manager use to fix decent price of goods that will make customer happy and profit can be

maximised. So in KEF Ltd this system support to get the best prices for produced goods in order

to reduce the chances of overpricing and attain the desired profit by satisfying customer.

Benefits of different system

Different accounting

systems

Benefits

Inventory management

system

It aid company in utilising available goods and raw

material so that desired goals can be attained.

This system support to keep a proper track of entire stock

and of any request from supplier so that profit can be

increased ( Holsapple, 2013).

Job Costing system This system assist to provide decent steadiness in

examining and decreasing cost relevant to specific job

to produced product as per the trends in market and customer preferences this help to grow

profit.

Cost accounting system: It is used to determine the cost of total production of various

goods manufacture by company. It basically includes total cost at several level and also include

fixed cost that help to determine the profit. There are useful method of accounting cost such as,

marginal and absorption costing, lean costing, activity and standard costing method. In

respective company Activity based costing method is used that basically assigns total cost to

goods which are related with producing goods (Humphrey, C. and Miller, 2012).

Job Coasting system: This method mainly record the cost which are related with

producing good job within an organisation. It assist to delegate manufacturing cost to each good

and product director and accountant have evidence of cost of each product. This system also

support in calculating cost of various product that are manufacture by company in same period of

time. Thus, in KEF Ltd this system help to evaluate and measure the cost of various useful

product that are produced by company in order to meet the customer needs.

Price optimisation system: This is considered to be most important system for company

as it help to determine the customer reaction on prices set by company for manufacture product.

Manager use to fix decent price of goods that will make customer happy and profit can be

maximised. So in KEF Ltd this system support to get the best prices for produced goods in order

to reduce the chances of overpricing and attain the desired profit by satisfying customer.

Benefits of different system

Different accounting

systems

Benefits

Inventory management

system

It aid company in utilising available goods and raw

material so that desired goals can be attained.

This system support to keep a proper track of entire stock

and of any request from supplier so that profit can be

increased ( Holsapple, 2013).

Job Costing system This system assist to provide decent steadiness in

examining and decreasing cost relevant to specific job

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

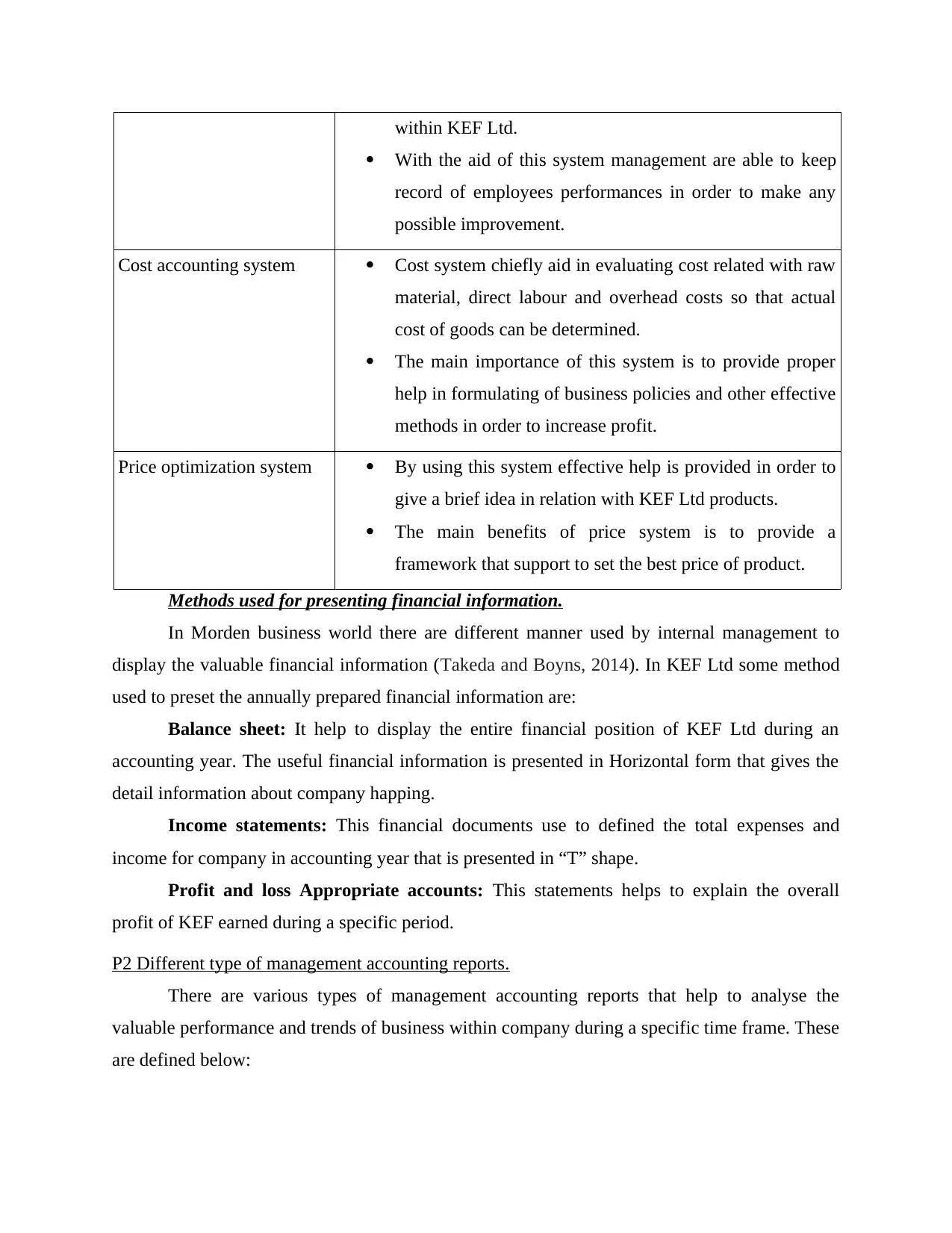

within KEF Ltd.

With the aid of this system management are able to keep

record of employees performances in order to make any

possible improvement.

Cost accounting system Cost system chiefly aid in evaluating cost related with raw

material, direct labour and overhead costs so that actual

cost of goods can be determined.

The main importance of this system is to provide proper

help in formulating of business policies and other effective

methods in order to increase profit.

Price optimization system By using this system effective help is provided in order to

give a brief idea in relation with KEF Ltd products.

The main benefits of price system is to provide a

framework that support to set the best price of product.

Methods used for presenting financial information.

In Morden business world there are different manner used by internal management to

display the valuable financial information (Takeda and Boyns, 2014). In KEF Ltd some method

used to preset the annually prepared financial information are:

Balance sheet: It help to display the entire financial position of KEF Ltd during an

accounting year. The useful financial information is presented in Horizontal form that gives the

detail information about company happing.

Income statements: This financial documents use to defined the total expenses and

income for company in accounting year that is presented in “T” shape.

Profit and loss Appropriate accounts: This statements helps to explain the overall

profit of KEF earned during a specific period.

P2 Different type of management accounting reports.

There are various types of management accounting reports that help to analyse the

valuable performance and trends of business within company during a specific time frame. These

are defined below:

With the aid of this system management are able to keep

record of employees performances in order to make any

possible improvement.

Cost accounting system Cost system chiefly aid in evaluating cost related with raw

material, direct labour and overhead costs so that actual

cost of goods can be determined.

The main importance of this system is to provide proper

help in formulating of business policies and other effective

methods in order to increase profit.

Price optimization system By using this system effective help is provided in order to

give a brief idea in relation with KEF Ltd products.

The main benefits of price system is to provide a

framework that support to set the best price of product.

Methods used for presenting financial information.

In Morden business world there are different manner used by internal management to

display the valuable financial information (Takeda and Boyns, 2014). In KEF Ltd some method

used to preset the annually prepared financial information are:

Balance sheet: It help to display the entire financial position of KEF Ltd during an

accounting year. The useful financial information is presented in Horizontal form that gives the

detail information about company happing.

Income statements: This financial documents use to defined the total expenses and

income for company in accounting year that is presented in “T” shape.

Profit and loss Appropriate accounts: This statements helps to explain the overall

profit of KEF earned during a specific period.

P2 Different type of management accounting reports.

There are various types of management accounting reports that help to analyse the

valuable performance and trends of business within company during a specific time frame. These

are defined below:

Budget Report: This report help to make a better prediction about the upcoming income

and revenues from total business operation of company. In context of KEF Ltd the report support

manager to determine the future and present issues that can impact the income and budgets

exceeds its prediction. With the aid of Budget report, manager are able to develop valuable

reserve and relevant funds that can be used to meet contingencies (Zoni, Dossi and Morelli,

2012).

Performance Report: These reports are mainly prepared for the purpose to record and

measure the performance of employees and business process within an organisation. Manager

basically set target and measure the performance that help in making any possible improvement.

In respective company, management use to assign task and set the deadline for completing

specific work in order to measure the performance of employees and in case if any shortage are

found than necessary steps are taken to increase performance level.

Account receivable report: This reports help to display the present financial position of

KEF Ltd and it holds the detail information about the net inflows and outflows of cash during a

year. It also support to improve the credit policy of company as company have proper record of

each customer from whom money is to be collected on specific date. As per this report the KEF

Ltd are able to make effective decision so the financial status, profitability and market share can

be increased.

TASK 2

P3. Range of management accounting techniques.

Absorption costing: This simply means, to acquire or absorb something relevant to a

specific objective. It mainly includes all those cost that are involved in producing a specific unit

of good. The main drawback of this system is that is gives the total cost of production but do not

support in decision making process (Grabner and Moers, 2013).

Marginal costing: It is defined as the extra cost implemented by companies in order to

get an extra unit of output that help to increase production level. This system of costing only

includes variable cost because fixed cost are already treated against contribution.

1.Production cost per unit.

Amount Details

Direct Material 12

Direct Labor 20

and revenues from total business operation of company. In context of KEF Ltd the report support

manager to determine the future and present issues that can impact the income and budgets

exceeds its prediction. With the aid of Budget report, manager are able to develop valuable

reserve and relevant funds that can be used to meet contingencies (Zoni, Dossi and Morelli,

2012).

Performance Report: These reports are mainly prepared for the purpose to record and

measure the performance of employees and business process within an organisation. Manager

basically set target and measure the performance that help in making any possible improvement.

In respective company, management use to assign task and set the deadline for completing

specific work in order to measure the performance of employees and in case if any shortage are

found than necessary steps are taken to increase performance level.

Account receivable report: This reports help to display the present financial position of

KEF Ltd and it holds the detail information about the net inflows and outflows of cash during a

year. It also support to improve the credit policy of company as company have proper record of

each customer from whom money is to be collected on specific date. As per this report the KEF

Ltd are able to make effective decision so the financial status, profitability and market share can

be increased.

TASK 2

P3. Range of management accounting techniques.

Absorption costing: This simply means, to acquire or absorb something relevant to a

specific objective. It mainly includes all those cost that are involved in producing a specific unit

of good. The main drawback of this system is that is gives the total cost of production but do not

support in decision making process (Grabner and Moers, 2013).

Marginal costing: It is defined as the extra cost implemented by companies in order to

get an extra unit of output that help to increase production level. This system of costing only

includes variable cost because fixed cost are already treated against contribution.

1.Production cost per unit.

Amount Details

Direct Material 12

Direct Labor 20

Variable production overheads 8

Total fixed production overhead cost = £120000

Use standard volume of 20000 units to absorb

the fixed production overhead cost

Selling price = £60

Absorption cost = £46

Absorption Costing = £46/unit {12+20+8+120000/20000=46}

2.Total production cost

Budget: Absorption Costing

technique Sep 2018

Production Cost

Per Unit Total

£ £

Direct Material 12 18000*12 216000

Direct Labor 20 18000*20 360000

Variable production overheads 8 18000*8 144000

Fixed overheads 6 18000*6 108000

46 18000*46 828000

3.Cost of sales for June.

BUDGETED COST Amount

£

Cost of production 828000

Opening Inventory 0

Closing inventory -92000

COST OF SALES 736000

4. Profit and loss statement by using techniques

ABSORPTION COSTING: BUDGETED PROFIT

OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 60 10800000

COST OF PRODUCTION

DM 12 216000

DL 20 360000

VOH 8 144000

FOH 6 108000

46 828000

OPENING INVENTORY 0

Total fixed production overhead cost = £120000

Use standard volume of 20000 units to absorb

the fixed production overhead cost

Selling price = £60

Absorption cost = £46

Absorption Costing = £46/unit {12+20+8+120000/20000=46}

2.Total production cost

Budget: Absorption Costing

technique Sep 2018

Production Cost

Per Unit Total

£ £

Direct Material 12 18000*12 216000

Direct Labor 20 18000*20 360000

Variable production overheads 8 18000*8 144000

Fixed overheads 6 18000*6 108000

46 18000*46 828000

3.Cost of sales for June.

BUDGETED COST Amount

£

Cost of production 828000

Opening Inventory 0

Closing inventory -92000

COST OF SALES 736000

4. Profit and loss statement by using techniques

ABSORPTION COSTING: BUDGETED PROFIT

OR LOSS STATEMENT

PER UNIT TOTAL

£ £ £ £

SALES 60 10800000

COST OF PRODUCTION

DM 12 216000

DL 20 360000

VOH 8 144000

FOH 6 108000

46 828000

OPENING INVENTORY 0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

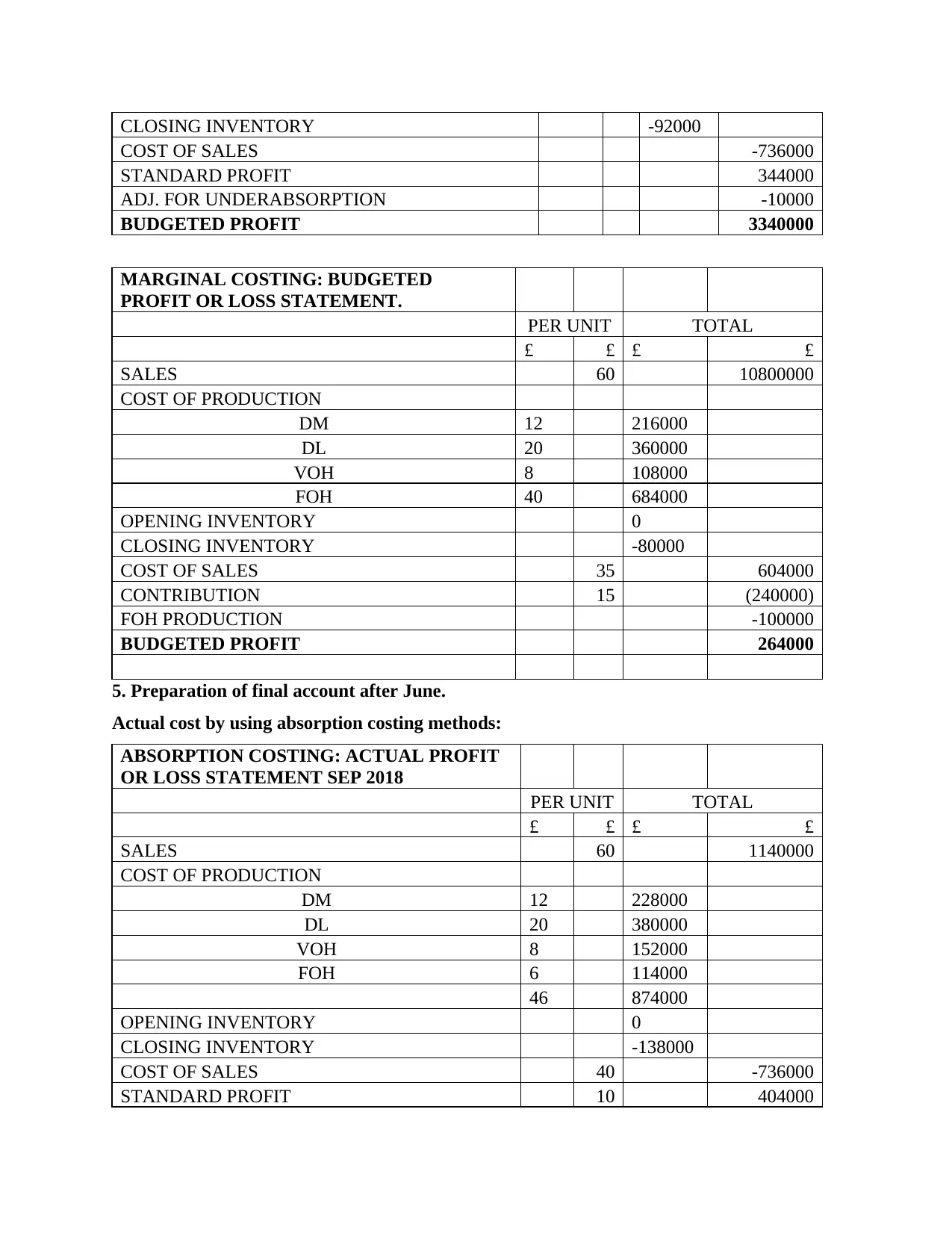

CLOSING INVENTORY -92000

COST OF SALES -736000

STANDARD PROFIT 344000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 3340000

MARGINAL COSTING: BUDGETED

PROFIT OR LOSS STATEMENT.

PER UNIT TOTAL

£ £ £ £

SALES 60 10800000

COST OF PRODUCTION

DM 12 216000

DL 20 360000

VOH 8 108000

FOH 40 684000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES 35 604000

CONTRIBUTION 15 (240000)

FOH PRODUCTION -100000

BUDGETED PROFIT 264000

5. Preparation of final account after June.

Actual cost by using absorption costing methods:

ABSORPTION COSTING: ACTUAL PROFIT

OR LOSS STATEMENT SEP 2018

PER UNIT TOTAL

£ £ £ £

SALES 60 1140000

COST OF PRODUCTION

DM 12 228000

DL 20 380000

VOH 8 152000

FOH 6 114000

46 874000

OPENING INVENTORY 0

CLOSING INVENTORY -138000

COST OF SALES 40 -736000

STANDARD PROFIT 10 404000

COST OF SALES -736000

STANDARD PROFIT 344000

ADJ. FOR UNDERABSORPTION -10000

BUDGETED PROFIT 3340000

MARGINAL COSTING: BUDGETED

PROFIT OR LOSS STATEMENT.

PER UNIT TOTAL

£ £ £ £

SALES 60 10800000

COST OF PRODUCTION

DM 12 216000

DL 20 360000

VOH 8 108000

FOH 40 684000

OPENING INVENTORY 0

CLOSING INVENTORY -80000

COST OF SALES 35 604000

CONTRIBUTION 15 (240000)

FOH PRODUCTION -100000

BUDGETED PROFIT 264000

5. Preparation of final account after June.

Actual cost by using absorption costing methods:

ABSORPTION COSTING: ACTUAL PROFIT

OR LOSS STATEMENT SEP 2018

PER UNIT TOTAL

£ £ £ £

SALES 60 1140000

COST OF PRODUCTION

DM 12 228000

DL 20 380000

VOH 8 152000

FOH 6 114000

46 874000

OPENING INVENTORY 0

CLOSING INVENTORY -138000

COST OF SALES 40 -736000

STANDARD PROFIT 10 404000

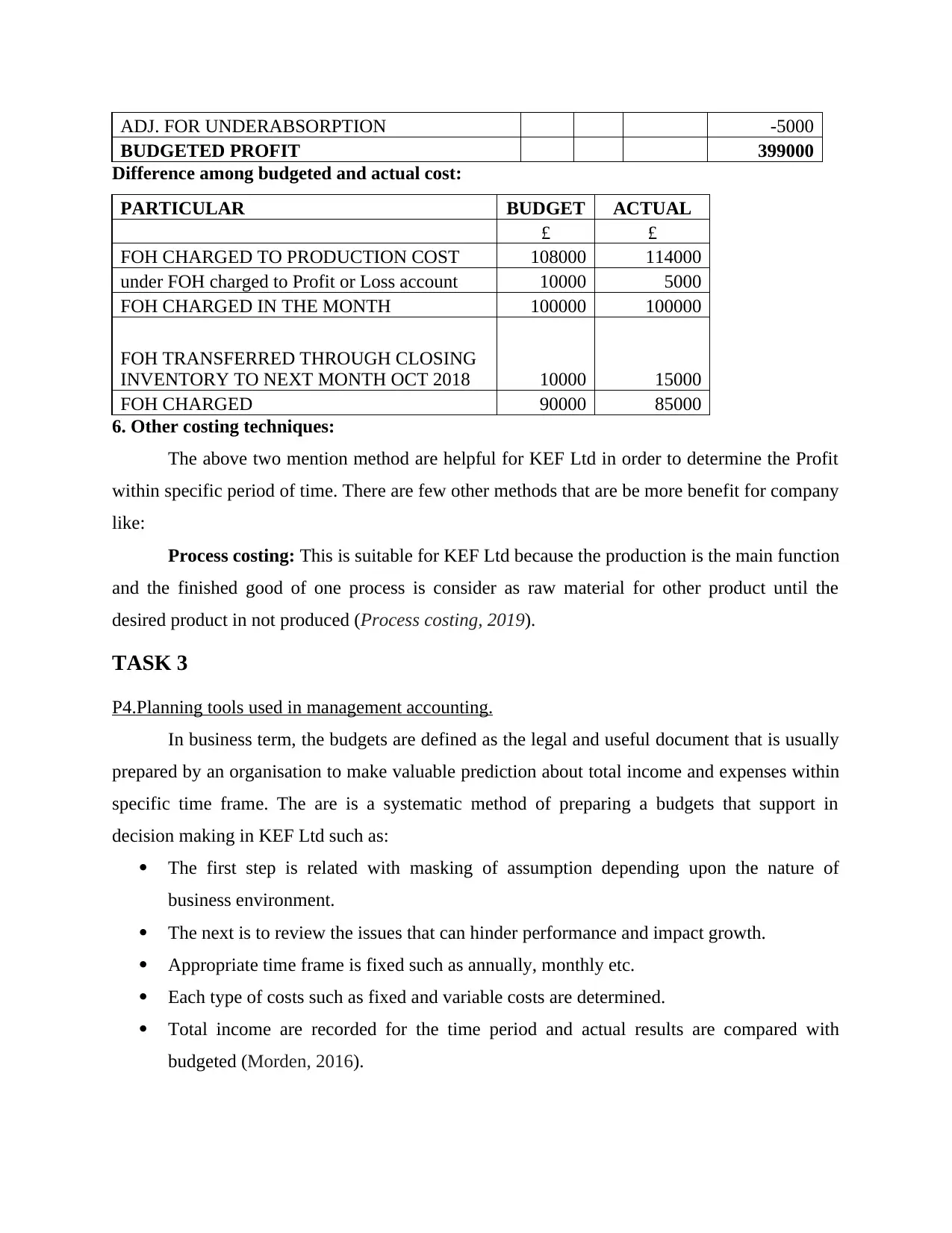

ADJ. FOR UNDERABSORPTION -5000

BUDGETED PROFIT 399000

Difference among budgeted and actual cost:

PARTICULAR BUDGET ACTUAL

£ £

FOH CHARGED TO PRODUCTION COST 108000 114000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

6. Other costing techniques:

The above two mention method are helpful for KEF Ltd in order to determine the Profit

within specific period of time. There are few other methods that are be more benefit for company

like:

Process costing: This is suitable for KEF Ltd because the production is the main function

and the finished good of one process is consider as raw material for other product until the

desired product in not produced (Process costing, 2019).

TASK 3

P4.Planning tools used in management accounting.

In business term, the budgets are defined as the legal and useful document that is usually

prepared by an organisation to make valuable prediction about total income and expenses within

specific time frame. The are is a systematic method of preparing a budgets that support in

decision making in KEF Ltd such as:

The first step is related with masking of assumption depending upon the nature of

business environment.

The next is to review the issues that can hinder performance and impact growth.

Appropriate time frame is fixed such as annually, monthly etc.

Each type of costs such as fixed and variable costs are determined.

Total income are recorded for the time period and actual results are compared with

budgeted (Morden, 2016).

BUDGETED PROFIT 399000

Difference among budgeted and actual cost:

PARTICULAR BUDGET ACTUAL

£ £

FOH CHARGED TO PRODUCTION COST 108000 114000

under FOH charged to Profit or Loss account 10000 5000

FOH CHARGED IN THE MONTH 100000 100000

FOH TRANSFERRED THROUGH CLOSING

INVENTORY TO NEXT MONTH OCT 2018 10000 15000

FOH CHARGED 90000 85000

6. Other costing techniques:

The above two mention method are helpful for KEF Ltd in order to determine the Profit

within specific period of time. There are few other methods that are be more benefit for company

like:

Process costing: This is suitable for KEF Ltd because the production is the main function

and the finished good of one process is consider as raw material for other product until the

desired product in not produced (Process costing, 2019).

TASK 3

P4.Planning tools used in management accounting.

In business term, the budgets are defined as the legal and useful document that is usually

prepared by an organisation to make valuable prediction about total income and expenses within

specific time frame. The are is a systematic method of preparing a budgets that support in

decision making in KEF Ltd such as:

The first step is related with masking of assumption depending upon the nature of

business environment.

The next is to review the issues that can hinder performance and impact growth.

Appropriate time frame is fixed such as annually, monthly etc.

Each type of costs such as fixed and variable costs are determined.

Total income are recorded for the time period and actual results are compared with

budgeted (Morden, 2016).

In order to make more authentic future budgets analysis are made to fix the issues and

drawbacks.

It is stated that main reason for preparing budgets is to reduce the possibilities of risks for

company that may arises due to differences in results of actual and standard budgets. There are

various types of budgets that are used as planning tool in KEF Ltd to ease the process of

budgetary control. These are defined below:

Flexible Budgets: This budget are helpful in modifying the actual budgets of company

due to some emergency or uncertainty that unable to work according to old budgets. In KEF Ltd

this budget helps to involve new expenditure that can be generated by any future situation and

also help to make a systematic record of new ways for increasing revenue during an accounting

year. Flexible budget of KEF Ltd is founded on modification that arises with the changes in

semi-variable, variable cost and fixed cost There are different advantages and disadvantage of

this budget that are defined below:

Advantages:

It enable internal mangers to make best cost control measures because it is basically

prepared with latests trends of market (Siverbo, 2014).

This budget support the management of KEF Ltd to make possible adjustment and

changes in the total cost and so that profit margin can be increased.

Disadvantage:

This type of budgets are confusing and complex in nature that require skilled labour.

It requires extra efforts and time, it also lacks discipline and can be altered at any time.

Zero based budgeting: It is consider to be most effective management accounting tool

that ease the procedure of making new budgets without considering previous budgets. The

process of ZBB mainly includes re evaluation of each product within cash flow and also justify

the different expenses that are spent by various units. In KEF Ltd this budget is helpful in

estimating the entire cost used in producing valuable goods that is incurred depending upon the

actual expenses in-fact of old data. There are various advantages and disadvantage that are

defined below:

Advantages:

Helps to give efficiency and accuracy and in results because it re-evaluate each elements

of cash flow.

drawbacks.

It is stated that main reason for preparing budgets is to reduce the possibilities of risks for

company that may arises due to differences in results of actual and standard budgets. There are

various types of budgets that are used as planning tool in KEF Ltd to ease the process of

budgetary control. These are defined below:

Flexible Budgets: This budget are helpful in modifying the actual budgets of company

due to some emergency or uncertainty that unable to work according to old budgets. In KEF Ltd

this budget helps to involve new expenditure that can be generated by any future situation and

also help to make a systematic record of new ways for increasing revenue during an accounting

year. Flexible budget of KEF Ltd is founded on modification that arises with the changes in

semi-variable, variable cost and fixed cost There are different advantages and disadvantage of

this budget that are defined below:

Advantages:

It enable internal mangers to make best cost control measures because it is basically

prepared with latests trends of market (Siverbo, 2014).

This budget support the management of KEF Ltd to make possible adjustment and

changes in the total cost and so that profit margin can be increased.

Disadvantage:

This type of budgets are confusing and complex in nature that require skilled labour.

It requires extra efforts and time, it also lacks discipline and can be altered at any time.

Zero based budgeting: It is consider to be most effective management accounting tool

that ease the procedure of making new budgets without considering previous budgets. The

process of ZBB mainly includes re evaluation of each product within cash flow and also justify

the different expenses that are spent by various units. In KEF Ltd this budget is helpful in

estimating the entire cost used in producing valuable goods that is incurred depending upon the

actual expenses in-fact of old data. There are various advantages and disadvantage that are

defined below:

Advantages:

Helps to give efficiency and accuracy and in results because it re-evaluate each elements

of cash flow.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ZBB basically provides better coordination communication between various departments

so that decision are made more accurately (Booth, 2018).

The main important this budget helps in reducing the extra activities of KEF Ltd in order

to increase profit.

Disadvantage:

The major disadvantage is that it requires skilled manpower and used more time in

predicting results.

This Budgets also lack the expertise required in preparing a budget.

P5. Comparison of organisations adapting management accounting to respond to financial

problems.

In business world, each type of organisation faces different types of problems due to

which entire functioning and business operation can be reduced. The situation of financial issues

gives various drawbacks such as they are not able to generate enough funds, increase production,

satisfy employees and so on. There are few financial problem that are faced by KEF Ltd that are

defined below:

Lack of Money Management: This financial problem impact the business operation of

respective company in greater manner as they do not have skilled person to manage the funds in

proper manner. There is more spending on different promotion activity and company is not able

to increase sales due to which there is requirement of skilled management (Lachmann, Knauer

and Trapp, 2013).

Special order: Basically company is lacking in producing extra special unit of goods on

customer demands due to which overall profitability is increasing day by day. In case if

management are taking initiative to produce special order than actual production for day is

reducing due to which employees are not happy. This reduces the customer base and gives

advantage to competitors.

In order to determine the different financial problem management of KEF Ltd uses

various crucial management accounting tool that help to deliver the best results. Basic

accounting tool that support to determine the provide solution to financial problem are defined

underneath:

KPI: This support to measure the overall performance of worker within company and

make valuable decision for improving profitability. Hence, performance indicator aids in

so that decision are made more accurately (Booth, 2018).

The main important this budget helps in reducing the extra activities of KEF Ltd in order

to increase profit.

Disadvantage:

The major disadvantage is that it requires skilled manpower and used more time in

predicting results.

This Budgets also lack the expertise required in preparing a budget.

P5. Comparison of organisations adapting management accounting to respond to financial

problems.

In business world, each type of organisation faces different types of problems due to

which entire functioning and business operation can be reduced. The situation of financial issues

gives various drawbacks such as they are not able to generate enough funds, increase production,

satisfy employees and so on. There are few financial problem that are faced by KEF Ltd that are

defined below:

Lack of Money Management: This financial problem impact the business operation of

respective company in greater manner as they do not have skilled person to manage the funds in

proper manner. There is more spending on different promotion activity and company is not able

to increase sales due to which there is requirement of skilled management (Lachmann, Knauer

and Trapp, 2013).

Special order: Basically company is lacking in producing extra special unit of goods on

customer demands due to which overall profitability is increasing day by day. In case if

management are taking initiative to produce special order than actual production for day is

reducing due to which employees are not happy. This reduces the customer base and gives

advantage to competitors.

In order to determine the different financial problem management of KEF Ltd uses

various crucial management accounting tool that help to deliver the best results. Basic

accounting tool that support to determine the provide solution to financial problem are defined

underneath:

KPI: This support to measure the overall performance of worker within company and

make valuable decision for improving profitability. Hence, performance indicator aids in

characteristic the entire expenditure and total return from investment made on specific project. In

context of KEF Ltd, key performance indicator is implemented to find out the financial issues

related with lack of money management. As it consider all those business operation that are

helpful to get best possible results in future.

Benchmarking: It is one of the most beneficial management tool that support company

to fix standard in order to measure the performance against competition. This tool is used in KEF

Ltd to resolve the issue of special order due to which customer demands are not satisfying and

they are losing their interest day by day (Kober, Subraamanniam and Watson, 2012).

Financial governance:

The concept of financial governance is defined as the best management tool that help to

develop the best resolution of various problems that are faced by company and due to which

performance get reduced. It is a descriptive method related with collecting useful information,

controlling and managing financial resources and workforce in order to get best authentic results.

It help to resolve the problem of misuse of money has it enable management of KEF Ltd to keep

a systematic record of each financial dealing incurred in company in order to increase sales. Thus

it help to reduce the mismanagement of money and increase profitability of business. In KEF Ltd

this tool also aid managers in determining the trends in market and hire skilled workforce to

produce the special order on demand of customer.

Comparison:

ABC Ltd KEF LTD

The company use to manufacture car and thus

faces financial problem related with pricing.

Therefore customer are not satisfied with

company policies.

This respective company aspect various

financial issues like lack of money

management and special order.

In order to develop solutions for financial

problem manager of respective company uses

price optimization system to fix the best price of

their product in order to increase the

profitability.

In order to overcome the issue of special

order company uses inventory management

system so that supply of special goods are

meet with the demands.

context of KEF Ltd, key performance indicator is implemented to find out the financial issues

related with lack of money management. As it consider all those business operation that are

helpful to get best possible results in future.

Benchmarking: It is one of the most beneficial management tool that support company

to fix standard in order to measure the performance against competition. This tool is used in KEF

Ltd to resolve the issue of special order due to which customer demands are not satisfying and

they are losing their interest day by day (Kober, Subraamanniam and Watson, 2012).

Financial governance:

The concept of financial governance is defined as the best management tool that help to

develop the best resolution of various problems that are faced by company and due to which

performance get reduced. It is a descriptive method related with collecting useful information,

controlling and managing financial resources and workforce in order to get best authentic results.

It help to resolve the problem of misuse of money has it enable management of KEF Ltd to keep

a systematic record of each financial dealing incurred in company in order to increase sales. Thus

it help to reduce the mismanagement of money and increase profitability of business. In KEF Ltd

this tool also aid managers in determining the trends in market and hire skilled workforce to

produce the special order on demand of customer.

Comparison:

ABC Ltd KEF LTD

The company use to manufacture car and thus

faces financial problem related with pricing.

Therefore customer are not satisfied with

company policies.

This respective company aspect various

financial issues like lack of money

management and special order.

In order to develop solutions for financial

problem manager of respective company uses

price optimization system to fix the best price of

their product in order to increase the

profitability.

In order to overcome the issue of special

order company uses inventory management

system so that supply of special goods are

meet with the demands.

CONCLUSION

The above project report concluded that, management is consider to be valuable

components for an organisation that support in systematic analysing, interpretation and decision

making at managerial level. Different system and reports aid an accountant to record every

business transaction in order to attain the predetermined goals. Moreover it also conclude, use of

costing method to calculate total net profit and determine the cost of production per unit.

Planning tools and its advantage and disadvantage that help in controlling budgets are analyzed

in good order to reach at definite solution. Measure of different financial issues that are happen

inside a firm and management accounting system reposed to these problems are shown. It will be

deciding to get over those problem to maintain entire growth and sustainability in future time

frame.

The above project report concluded that, management is consider to be valuable

components for an organisation that support in systematic analysing, interpretation and decision

making at managerial level. Different system and reports aid an accountant to record every

business transaction in order to attain the predetermined goals. Moreover it also conclude, use of

costing method to calculate total net profit and determine the cost of production per unit.

Planning tools and its advantage and disadvantage that help in controlling budgets are analyzed

in good order to reach at definite solution. Measure of different financial issues that are happen

inside a firm and management accounting system reposed to these problems are shown. It will be

deciding to get over those problem to maintain entire growth and sustainability in future time

frame.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and journals:

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Humphrey, C. and Miller, P., 2012. Rethinking impact and redefining responsibility: The

parameters and coordinates of accounting and public management reforms. Accounting,

Auditing & Accountability Journal. 25(2). pp.295-327.

Holsapple, C. ed., 2013. Handbook on knowledge management 1: Knowledge matters (Vol. 1).

Springer Science & Business Media.

Takeda, H. and Boyns, T., 2014. Management, accounting and philosophy: The development of

management accounting at Kyocera, 1959-2013. Accounting, Auditing & Accountability

Journal. 27(2). pp.317-356.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Morden, T., 2016. Principles of strategic management. Routledge.

Siverbo, S., 2014. The implementation and use of benchmarking in local government: a case

study of the translation of a management accounting innovation. Financial

Accountability & Management. 30(2). pp.121-149.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Lachmann, M., Knauer, T. and Trapp, R., 2013. Strategic management accounting practices in

hospitals: Empirical evidence on their dissemination under competitive market

environments. Journal of Accounting & Organizational Change. 9(3). pp.336-369.

Kober, R., Subraamanniam, T. and Watson, J., 2012. The impact of total quality management

adoption on small and medium enterprises’ financial performance. Accounting &

Finance. 52(2). pp.421-438.

Anessi-Pessina and et.al., 2016. Public sector budgeting: a European review of accounting and

public management journals. Accounting, Auditing & Accountability Journal. 29(3).

pp.491-519.

Online

Process costing. 2019. [Online] Available Through: <https://www.edupristine.com/blog/costing-

methods>.

Books and journals:

Collis, J. and Hussey, R., 2017. Cost and management accounting. Macmillan International

Higher Education.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Humphrey, C. and Miller, P., 2012. Rethinking impact and redefining responsibility: The

parameters and coordinates of accounting and public management reforms. Accounting,

Auditing & Accountability Journal. 25(2). pp.295-327.

Holsapple, C. ed., 2013. Handbook on knowledge management 1: Knowledge matters (Vol. 1).

Springer Science & Business Media.

Takeda, H. and Boyns, T., 2014. Management, accounting and philosophy: The development of

management accounting at Kyocera, 1959-2013. Accounting, Auditing & Accountability

Journal. 27(2). pp.317-356.

Zoni, L., Dossi, A. and Morelli, M., 2012. Management accounting system (MAS) change: field

evidence. Asia-Pacific Journal of Accounting & Economics. 19(1). pp.119-138.

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6-7). pp.407-419.

Morden, T., 2016. Principles of strategic management. Routledge.

Siverbo, S., 2014. The implementation and use of benchmarking in local government: a case

study of the translation of a management accounting innovation. Financial

Accountability & Management. 30(2). pp.121-149.

Booth, P., 2018. Management control in a voluntary organization: accounting and accountants

in organizational context. Routledge.

Lachmann, M., Knauer, T. and Trapp, R., 2013. Strategic management accounting practices in

hospitals: Empirical evidence on their dissemination under competitive market

environments. Journal of Accounting & Organizational Change. 9(3). pp.336-369.

Kober, R., Subraamanniam, T. and Watson, J., 2012. The impact of total quality management

adoption on small and medium enterprises’ financial performance. Accounting &

Finance. 52(2). pp.421-438.

Anessi-Pessina and et.al., 2016. Public sector budgeting: a European review of accounting and

public management journals. Accounting, Auditing & Accountability Journal. 29(3).

pp.491-519.

Online

Process costing. 2019. [Online] Available Through: <https://www.edupristine.com/blog/costing-

methods>.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.