Detailed Management Accounting Report: ABC Ltd Cost Analysis

VerifiedAdded on 2020/07/23

|24

|3875

|21

Report

AI Summary

This report provides a detailed analysis of management accounting principles applied to ABC Ltd. It begins with a classification of costs and explores different costing methods, including job costing, process costing, and batch costing. The report then delves into calculating closing stock using FIFO, LIFO, and average cost methods. Furthermore, it compares marginal and absorption costing techniques and prepares routine costs. The report also discusses key performance indicators, benchmarking, and suggestions for reducing costs, improving value, and enhancing quality. Finally, it covers the purpose and nature of budgeting, different budgeting methods (traditional, zero-based, and fixed budgets), and their importance in an organization. The report uses various tables and calculations to illustrate the concepts, providing a comprehensive overview of cost analysis and budgeting within the context of ABC Ltd.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Index of Tables

Table 1: Closing stock using FIFO..................................................................................................3

Table 2: Closing stock using LIFO..................................................................................................3

Table 3: Closing stock using Average cost......................................................................................4

Table 4: Routine costs......................................................................................................................5

Table 5: sales budget........................................................................................................................7

Table 6: Production budget..............................................................................................................8

Table 7: Material usage budget........................................................................................................8

Table 8: Material purchase budget...................................................................................................8

Table 9: Plastic usage budget...........................................................................................................8

Table 10: Plastic purchase budget....................................................................................................9

Table 11: Cash budget.....................................................................................................................9

Table 12: Calculating sales............................................................................................................10

Table 13: Raw material..................................................................................................................11

Table 14: Production overhead......................................................................................................11

Table 15: Variance analysis...........................................................................................................12

Table 1: Closing stock using FIFO..................................................................................................3

Table 2: Closing stock using LIFO..................................................................................................3

Table 3: Closing stock using Average cost......................................................................................4

Table 4: Routine costs......................................................................................................................5

Table 5: sales budget........................................................................................................................7

Table 6: Production budget..............................................................................................................8

Table 7: Material usage budget........................................................................................................8

Table 8: Material purchase budget...................................................................................................8

Table 9: Plastic usage budget...........................................................................................................8

Table 10: Plastic purchase budget....................................................................................................9

Table 11: Cash budget.....................................................................................................................9

Table 12: Calculating sales............................................................................................................10

Table 13: Raw material..................................................................................................................11

Table 14: Production overhead......................................................................................................11

Table 15: Variance analysis...........................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Role of management accountant of an entity is to minimise the complexities imposed on

an entity. It help to make complete records of each and every transactions so that company will

run effectively. ABC Ltd has been selected in the given report in order to analyse the

performance of the firm in relation to various costs and variances determined. This report is all

about classification of costs, determination of closing stock using different techniques. Current

report emphasises on preparing budgets to forecast the future performance along with the

preparation of variance analysis.

TASK 1

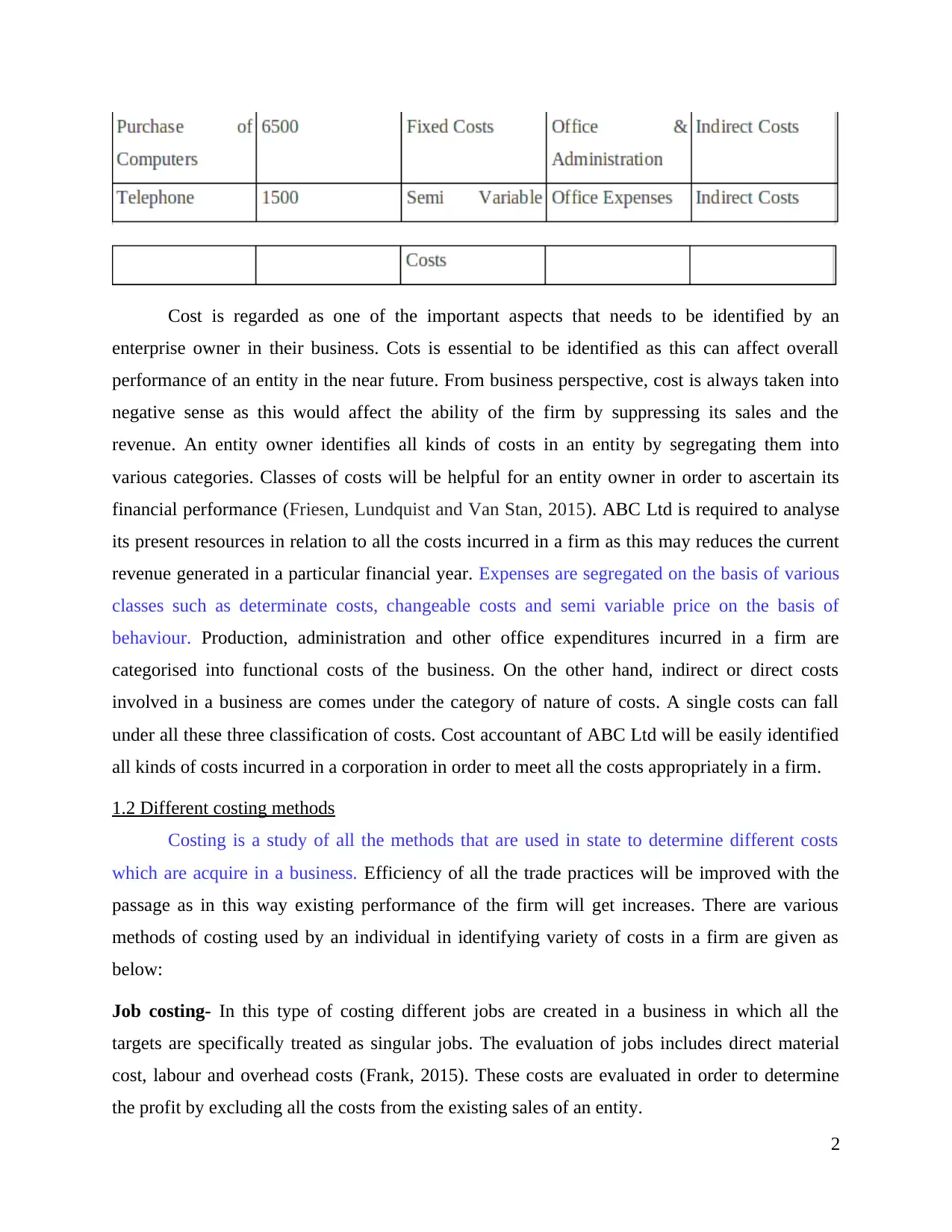

1.1 Classification of costs

1

Role of management accountant of an entity is to minimise the complexities imposed on

an entity. It help to make complete records of each and every transactions so that company will

run effectively. ABC Ltd has been selected in the given report in order to analyse the

performance of the firm in relation to various costs and variances determined. This report is all

about classification of costs, determination of closing stock using different techniques. Current

report emphasises on preparing budgets to forecast the future performance along with the

preparation of variance analysis.

TASK 1

1.1 Classification of costs

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

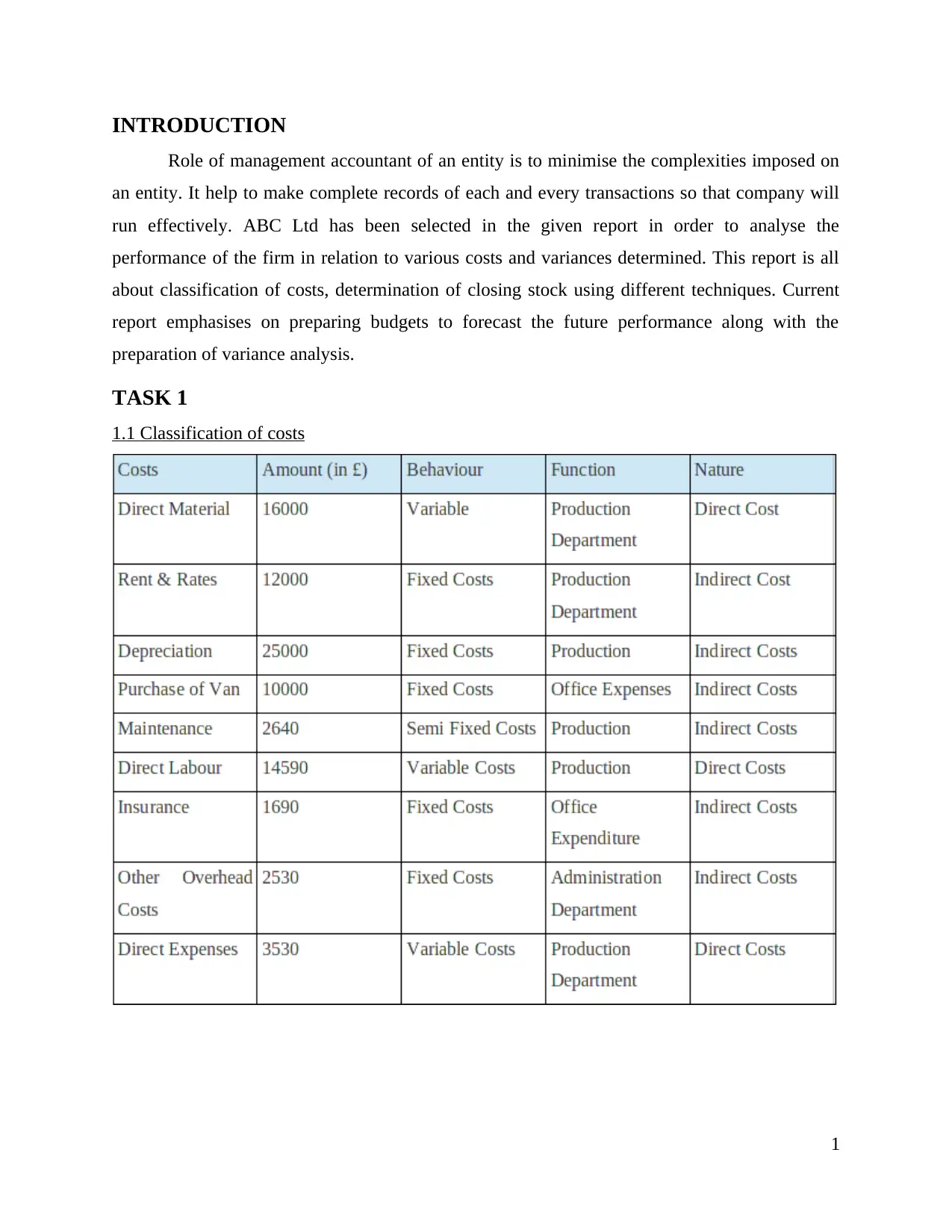

Cost is regarded as one of the important aspects that needs to be identified by an

enterprise owner in their business. Cots is essential to be identified as this can affect overall

performance of an entity in the near future. From business perspective, cost is always taken into

negative sense as this would affect the ability of the firm by suppressing its sales and the

revenue. An entity owner identifies all kinds of costs in an entity by segregating them into

various categories. Classes of costs will be helpful for an entity owner in order to ascertain its

financial performance (Friesen, Lundquist and Van Stan, 2015). ABC Ltd is required to analyse

its present resources in relation to all the costs incurred in a firm as this may reduces the current

revenue generated in a particular financial year. Expenses are segregated on the basis of various

classes such as determinate costs, changeable costs and semi variable price on the basis of

behaviour. Production, administration and other office expenditures incurred in a firm are

categorised into functional costs of the business. On the other hand, indirect or direct costs

involved in a business are comes under the category of nature of costs. A single costs can fall

under all these three classification of costs. Cost accountant of ABC Ltd will be easily identified

all kinds of costs incurred in a corporation in order to meet all the costs appropriately in a firm.

1.2 Different costing methods

Costing is a study of all the methods that are used in state to determine different costs

which are acquire in a business. Efficiency of all the trade practices will be improved with the

passage as in this way existing performance of the firm will get increases. There are various

methods of costing used by an individual in identifying variety of costs in a firm are given as

below:

Job costing- In this type of costing different jobs are created in a business in which all the

targets are specifically treated as singular jobs. The evaluation of jobs includes direct material

cost, labour and overhead costs (Frank, 2015). These costs are evaluated in order to determine

the profit by excluding all the costs from the existing sales of an entity.

2

enterprise owner in their business. Cots is essential to be identified as this can affect overall

performance of an entity in the near future. From business perspective, cost is always taken into

negative sense as this would affect the ability of the firm by suppressing its sales and the

revenue. An entity owner identifies all kinds of costs in an entity by segregating them into

various categories. Classes of costs will be helpful for an entity owner in order to ascertain its

financial performance (Friesen, Lundquist and Van Stan, 2015). ABC Ltd is required to analyse

its present resources in relation to all the costs incurred in a firm as this may reduces the current

revenue generated in a particular financial year. Expenses are segregated on the basis of various

classes such as determinate costs, changeable costs and semi variable price on the basis of

behaviour. Production, administration and other office expenditures incurred in a firm are

categorised into functional costs of the business. On the other hand, indirect or direct costs

involved in a business are comes under the category of nature of costs. A single costs can fall

under all these three classification of costs. Cost accountant of ABC Ltd will be easily identified

all kinds of costs incurred in a corporation in order to meet all the costs appropriately in a firm.

1.2 Different costing methods

Costing is a study of all the methods that are used in state to determine different costs

which are acquire in a business. Efficiency of all the trade practices will be improved with the

passage as in this way existing performance of the firm will get increases. There are various

methods of costing used by an individual in identifying variety of costs in a firm are given as

below:

Job costing- In this type of costing different jobs are created in a business in which all the

targets are specifically treated as singular jobs. The evaluation of jobs includes direct material

cost, labour and overhead costs (Frank, 2015). These costs are evaluated in order to determine

the profit by excluding all the costs from the existing sales of an entity.

2

Process costing- In industry like construction, a process is evaluated from start till the end of the

process to determine the overall movement of goods from one process to another. Process

costing consider both direct and indirect costs which are integral part of an entity. In the end of

every process finished stock will be transferred to the finished stock ledger as the products are

processed with the help of al the processes whose accounting will be done in the current costing

methods.

Batch costing- It is a form of specific order costing. In batch costing items are manufactured for

stock. A finished product may require different components for assembly and may be produced

in economical batch lots. In general the procedures for costing batches are very similar to costing

jobs. The batch would be treated as a job during manufacture. On completion of the batch the

cost per unit can be calculated by dividing the total batch cost by the number of good units

produced.

Examples of products that are best accounted for cost through batch costing include:

Production of engineering components

Radios/television sets

Medicine

Footwear

Clothing manufacturer

The costs included in the batch cost are direct costs of material, labour and direct expenses plus

overheads absorbed into the batch.

1.3 Calculating closing stock

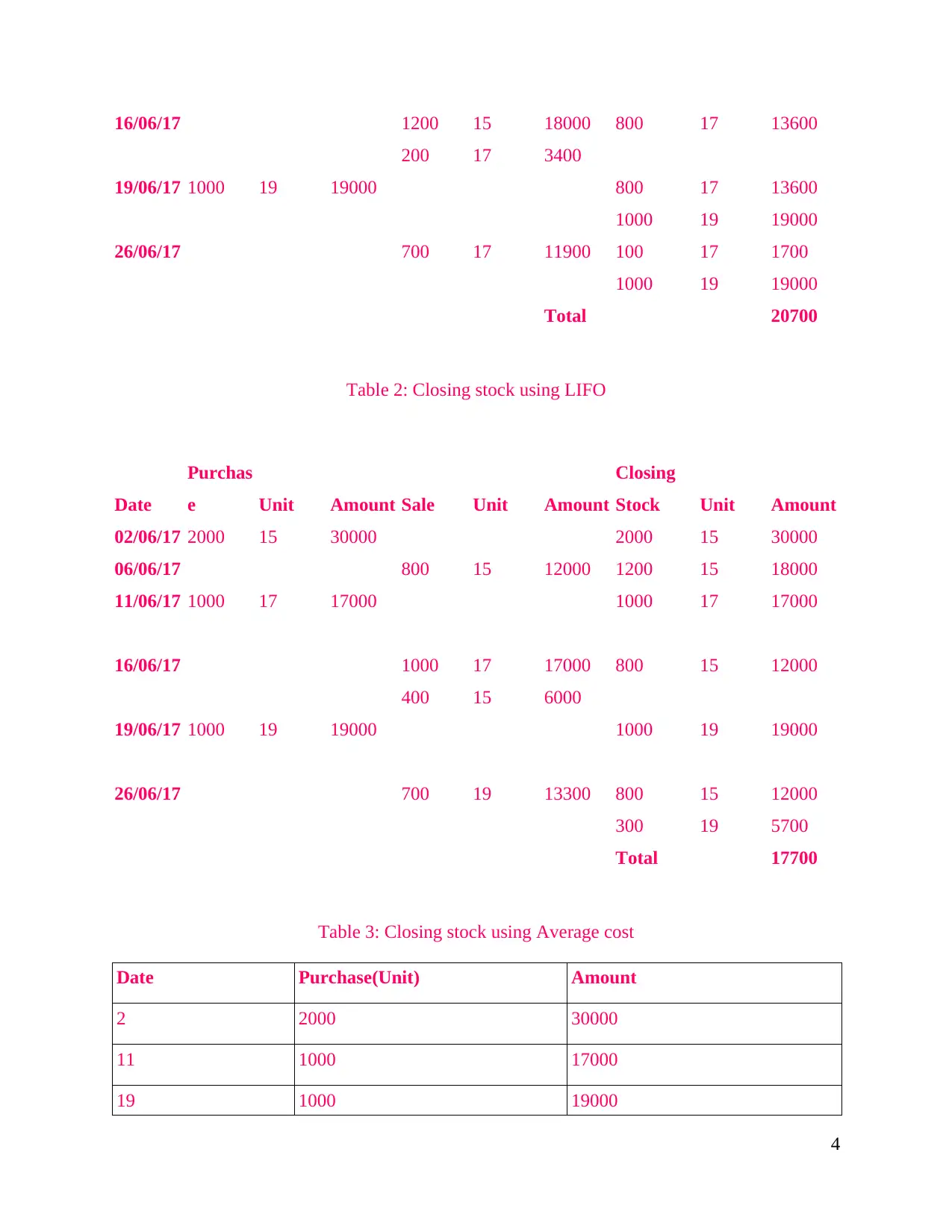

Table 1: Closing stock using FIFO

Date

Purchas

e Unit Amount Sale Unit Amount

Closing

Stock Unit Amount

02/06/17 2000 15 30000 2000 15 30000

06/06/17 800 15 12000 1200 15 18000

11/06/17 1000 17 17000 1200 15 18000

1000 17 17000

3

process to determine the overall movement of goods from one process to another. Process

costing consider both direct and indirect costs which are integral part of an entity. In the end of

every process finished stock will be transferred to the finished stock ledger as the products are

processed with the help of al the processes whose accounting will be done in the current costing

methods.

Batch costing- It is a form of specific order costing. In batch costing items are manufactured for

stock. A finished product may require different components for assembly and may be produced

in economical batch lots. In general the procedures for costing batches are very similar to costing

jobs. The batch would be treated as a job during manufacture. On completion of the batch the

cost per unit can be calculated by dividing the total batch cost by the number of good units

produced.

Examples of products that are best accounted for cost through batch costing include:

Production of engineering components

Radios/television sets

Medicine

Footwear

Clothing manufacturer

The costs included in the batch cost are direct costs of material, labour and direct expenses plus

overheads absorbed into the batch.

1.3 Calculating closing stock

Table 1: Closing stock using FIFO

Date

Purchas

e Unit Amount Sale Unit Amount

Closing

Stock Unit Amount

02/06/17 2000 15 30000 2000 15 30000

06/06/17 800 15 12000 1200 15 18000

11/06/17 1000 17 17000 1200 15 18000

1000 17 17000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

16/06/17 1200 15 18000 800 17 13600

200 17 3400

19/06/17 1000 19 19000 800 17 13600

1000 19 19000

26/06/17 700 17 11900 100 17 1700

1000 19 19000

Total 20700

Table 2: Closing stock using LIFO

Date

Purchas

e Unit Amount Sale Unit Amount

Closing

Stock Unit Amount

02/06/17 2000 15 30000 2000 15 30000

06/06/17 800 15 12000 1200 15 18000

11/06/17 1000 17 17000 1000 17 17000

16/06/17 1000 17 17000 800 15 12000

400 15 6000

19/06/17 1000 19 19000 1000 19 19000

26/06/17 700 19 13300 800 15 12000

300 19 5700

Total 17700

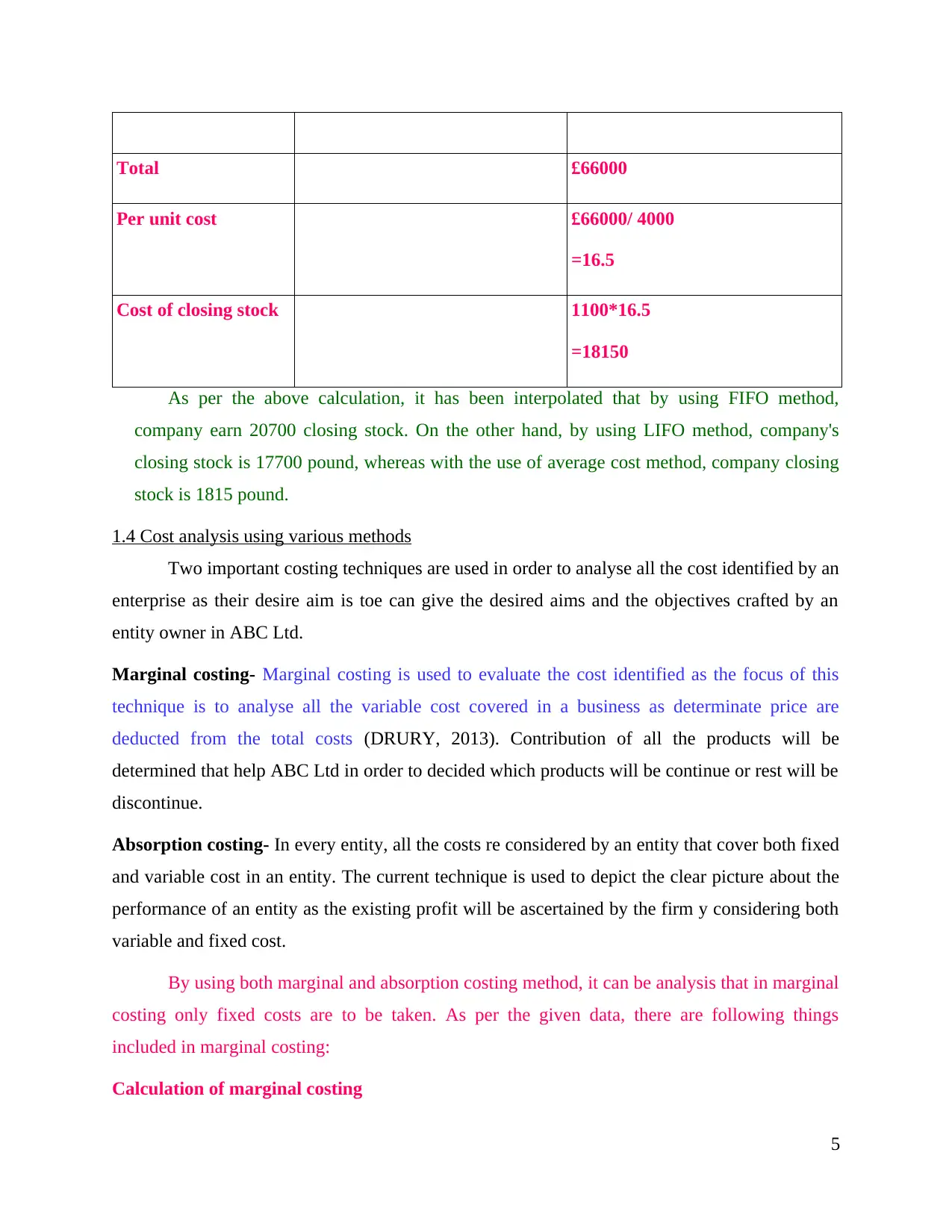

Table 3: Closing stock using Average cost

Date Purchase(Unit) Amount

2 2000 30000

11 1000 17000

19 1000 19000

4

200 17 3400

19/06/17 1000 19 19000 800 17 13600

1000 19 19000

26/06/17 700 17 11900 100 17 1700

1000 19 19000

Total 20700

Table 2: Closing stock using LIFO

Date

Purchas

e Unit Amount Sale Unit Amount

Closing

Stock Unit Amount

02/06/17 2000 15 30000 2000 15 30000

06/06/17 800 15 12000 1200 15 18000

11/06/17 1000 17 17000 1000 17 17000

16/06/17 1000 17 17000 800 15 12000

400 15 6000

19/06/17 1000 19 19000 1000 19 19000

26/06/17 700 19 13300 800 15 12000

300 19 5700

Total 17700

Table 3: Closing stock using Average cost

Date Purchase(Unit) Amount

2 2000 30000

11 1000 17000

19 1000 19000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total £66000

Per unit cost £66000/ 4000

=16.5

Cost of closing stock 1100*16.5

=18150

As per the above calculation, it has been interpolated that by using FIFO method,

company earn 20700 closing stock. On the other hand, by using LIFO method, company's

closing stock is 17700 pound, whereas with the use of average cost method, company closing

stock is 1815 pound.

1.4 Cost analysis using various methods

Two important costing techniques are used in order to analyse all the cost identified by an

enterprise as their desire aim is toe can give the desired aims and the objectives crafted by an

entity owner in ABC Ltd.

Marginal costing- Marginal costing is used to evaluate the cost identified as the focus of this

technique is to analyse all the variable cost covered in a business as determinate price are

deducted from the total costs (DRURY, 2013). Contribution of all the products will be

determined that help ABC Ltd in order to decided which products will be continue or rest will be

discontinue.

Absorption costing- In every entity, all the costs re considered by an entity that cover both fixed

and variable cost in an entity. The current technique is used to depict the clear picture about the

performance of an entity as the existing profit will be ascertained by the firm y considering both

variable and fixed cost.

By using both marginal and absorption costing method, it can be analysis that in marginal

costing only fixed costs are to be taken. As per the given data, there are following things

included in marginal costing:

Calculation of marginal costing

5

Per unit cost £66000/ 4000

=16.5

Cost of closing stock 1100*16.5

=18150

As per the above calculation, it has been interpolated that by using FIFO method,

company earn 20700 closing stock. On the other hand, by using LIFO method, company's

closing stock is 17700 pound, whereas with the use of average cost method, company closing

stock is 1815 pound.

1.4 Cost analysis using various methods

Two important costing techniques are used in order to analyse all the cost identified by an

enterprise as their desire aim is toe can give the desired aims and the objectives crafted by an

entity owner in ABC Ltd.

Marginal costing- Marginal costing is used to evaluate the cost identified as the focus of this

technique is to analyse all the variable cost covered in a business as determinate price are

deducted from the total costs (DRURY, 2013). Contribution of all the products will be

determined that help ABC Ltd in order to decided which products will be continue or rest will be

discontinue.

Absorption costing- In every entity, all the costs re considered by an entity that cover both fixed

and variable cost in an entity. The current technique is used to depict the clear picture about the

performance of an entity as the existing profit will be ascertained by the firm y considering both

variable and fixed cost.

By using both marginal and absorption costing method, it can be analysis that in marginal

costing only fixed costs are to be taken. As per the given data, there are following things

included in marginal costing:

Calculation of marginal costing

5

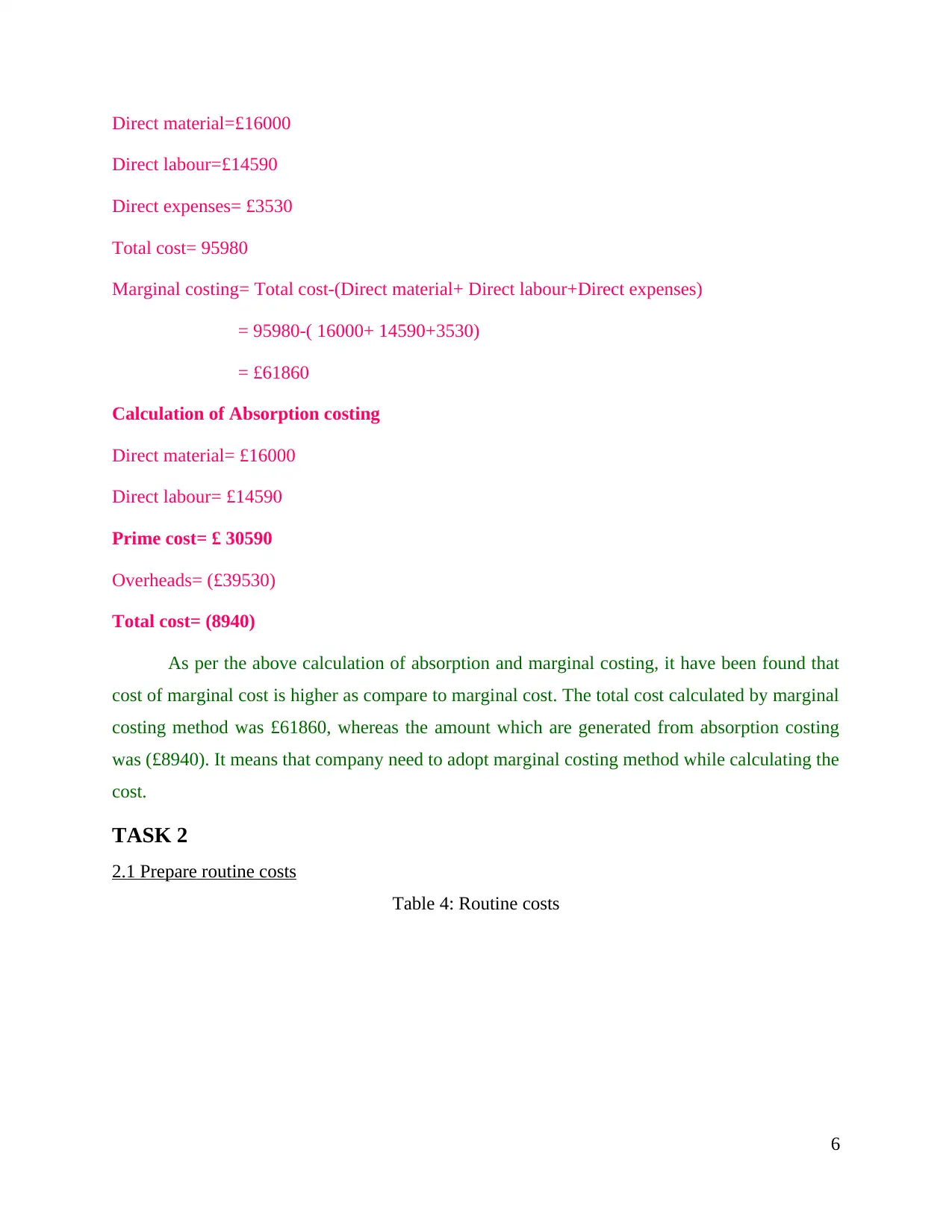

Direct material=£16000

Direct labour=£14590

Direct expenses= £3530

Total cost= 95980

Marginal costing= Total cost-(Direct material+ Direct labour+Direct expenses)

= 95980-( 16000+ 14590+3530)

= £61860

Calculation of Absorption costing

Direct material= £16000

Direct labour= £14590

Prime cost= £ 30590

Overheads= (£39530)

Total cost= (8940)

As per the above calculation of absorption and marginal costing, it have been found that

cost of marginal cost is higher as compare to marginal cost. The total cost calculated by marginal

costing method was £61860, whereas the amount which are generated from absorption costing

was (£8940). It means that company need to adopt marginal costing method while calculating the

cost.

TASK 2

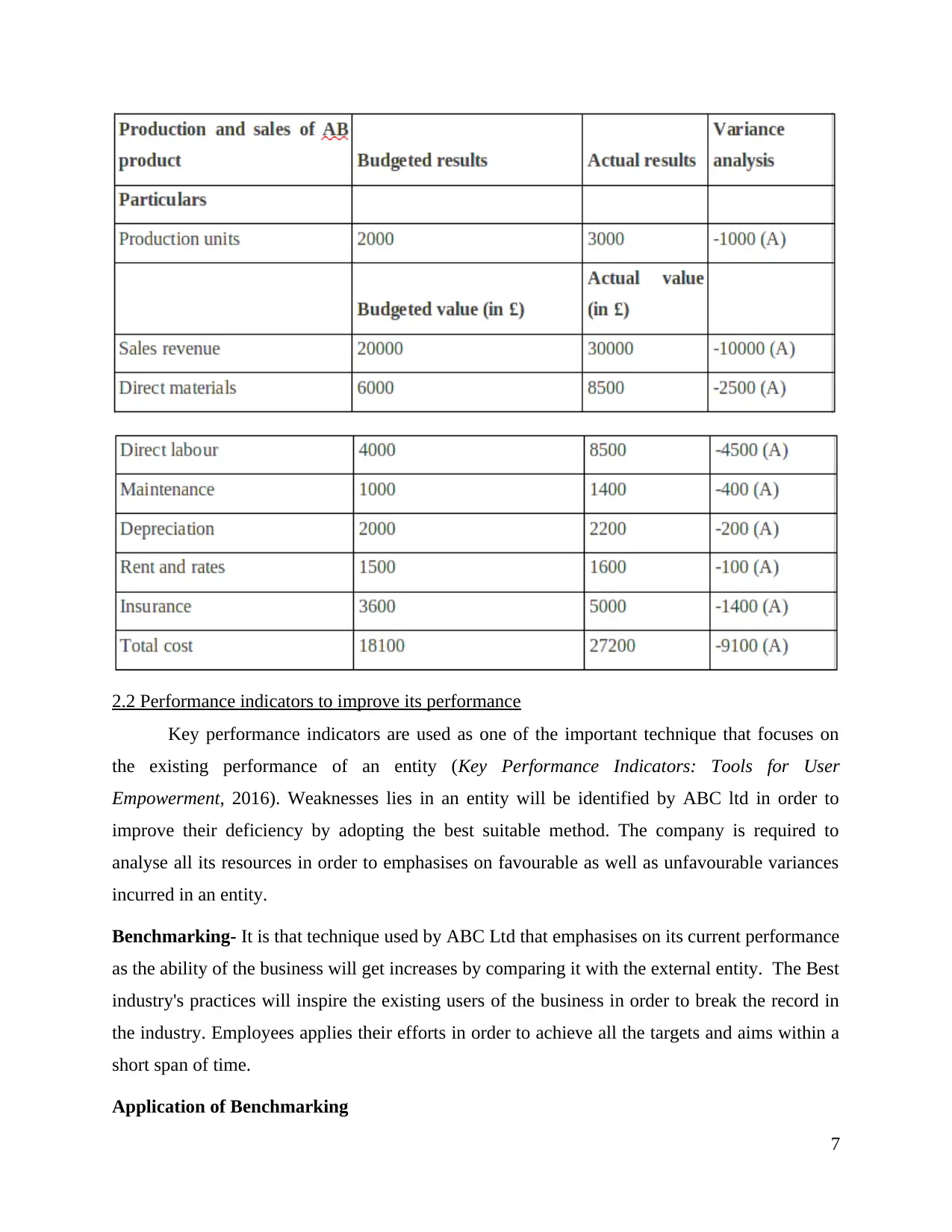

2.1 Prepare routine costs

Table 4: Routine costs

6

Direct labour=£14590

Direct expenses= £3530

Total cost= 95980

Marginal costing= Total cost-(Direct material+ Direct labour+Direct expenses)

= 95980-( 16000+ 14590+3530)

= £61860

Calculation of Absorption costing

Direct material= £16000

Direct labour= £14590

Prime cost= £ 30590

Overheads= (£39530)

Total cost= (8940)

As per the above calculation of absorption and marginal costing, it have been found that

cost of marginal cost is higher as compare to marginal cost. The total cost calculated by marginal

costing method was £61860, whereas the amount which are generated from absorption costing

was (£8940). It means that company need to adopt marginal costing method while calculating the

cost.

TASK 2

2.1 Prepare routine costs

Table 4: Routine costs

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 Performance indicators to improve its performance

Key performance indicators are used as one of the important technique that focuses on

the existing performance of an entity (Key Performance Indicators: Tools for User

Empowerment, 2016). Weaknesses lies in an entity will be identified by ABC ltd in order to

improve their deficiency by adopting the best suitable method. The company is required to

analyse all its resources in order to emphasises on favourable as well as unfavourable variances

incurred in an entity.

Benchmarking- It is that technique used by ABC Ltd that emphasises on its current performance

as the ability of the business will get increases by comparing it with the external entity. The Best

industry's practices will inspire the existing users of the business in order to break the record in

the industry. Employees applies their efforts in order to achieve all the targets and aims within a

short span of time.

Application of Benchmarking

7

Key performance indicators are used as one of the important technique that focuses on

the existing performance of an entity (Key Performance Indicators: Tools for User

Empowerment, 2016). Weaknesses lies in an entity will be identified by ABC ltd in order to

improve their deficiency by adopting the best suitable method. The company is required to

analyse all its resources in order to emphasises on favourable as well as unfavourable variances

incurred in an entity.

Benchmarking- It is that technique used by ABC Ltd that emphasises on its current performance

as the ability of the business will get increases by comparing it with the external entity. The Best

industry's practices will inspire the existing users of the business in order to break the record in

the industry. Employees applies their efforts in order to achieve all the targets and aims within a

short span of time.

Application of Benchmarking

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In terms of financial performance of ABC Ltd, desired rate of return on investment will

help in achieving the desired aims and targets of the business. For instance, benchmarking is

used by ABC Ltd in order increase their ROI of 6% to 8% as achieving higher percentage than

the standards decided by the industry. Favourable or unfavourable variances will be determined

by ABC by comparing their actual results with the standards framed by the experts of the overall

industry. Desired motive of the business is to capture higher share in the external business

environment.

2.3 Suggestion to reduce cost, value and quality

Three important component of the business concern is cost, value and quality that ensure

higher productivity of the business. Aims and objectives developed by an entity will be helpful

for an entity in order to enhance the existing worth of the firm in eyes of all the customers

located in the external business environment.

ABC- Activity based costing technique is used by an enterprise owner in order allocate all kinds

of costs in a business appropriately among all the departments. Efficiency of all the resources

will be maintained that will be helpful in meeting higher complexity. Cost drivers are effectively

used in order to identify various cost incurred in a business as the focus of an entity lies on the

weak areas of the business. Profit generated by an entity gets increases with the passage of time

when the current cost incurred by ABC Ltd gets reduces over certain period.

Balance score card- Quality management approach used by CEO of ABC Ltd in order to

identify the quality of all he resources used by them in delivering all the services. Quality of all

the services are required to be maintained by the business firm by emphasises on the existing

gaols and the objectives of firm. It has four different perspectives such as internal business

process, innovation ad creativity, customer experience and financial perspectives. These four

pillars are important for an entity as the overall evaluation of al the business activities is possible

with the help of current technique.

TASK 3

3.1 Purpose and nature of budgeting process

Budgeting is a written statement prepared in a business that cover income and

expenditure equally the main motto of the employer is to identify its existing performance

(Jobson, 2012). Costs are identified with the budget in order to manage its performance by

8

help in achieving the desired aims and targets of the business. For instance, benchmarking is

used by ABC Ltd in order increase their ROI of 6% to 8% as achieving higher percentage than

the standards decided by the industry. Favourable or unfavourable variances will be determined

by ABC by comparing their actual results with the standards framed by the experts of the overall

industry. Desired motive of the business is to capture higher share in the external business

environment.

2.3 Suggestion to reduce cost, value and quality

Three important component of the business concern is cost, value and quality that ensure

higher productivity of the business. Aims and objectives developed by an entity will be helpful

for an entity in order to enhance the existing worth of the firm in eyes of all the customers

located in the external business environment.

ABC- Activity based costing technique is used by an enterprise owner in order allocate all kinds

of costs in a business appropriately among all the departments. Efficiency of all the resources

will be maintained that will be helpful in meeting higher complexity. Cost drivers are effectively

used in order to identify various cost incurred in a business as the focus of an entity lies on the

weak areas of the business. Profit generated by an entity gets increases with the passage of time

when the current cost incurred by ABC Ltd gets reduces over certain period.

Balance score card- Quality management approach used by CEO of ABC Ltd in order to

identify the quality of all he resources used by them in delivering all the services. Quality of all

the services are required to be maintained by the business firm by emphasises on the existing

gaols and the objectives of firm. It has four different perspectives such as internal business

process, innovation ad creativity, customer experience and financial perspectives. These four

pillars are important for an entity as the overall evaluation of al the business activities is possible

with the help of current technique.

TASK 3

3.1 Purpose and nature of budgeting process

Budgeting is a written statement prepared in a business that cover income and

expenditure equally the main motto of the employer is to identify its existing performance

(Jobson, 2012). Costs are identified with the budget in order to manage its performance by

8

utilising available resources. Different budgets are used by ABC Ltd in order to forecast their

future by analysing all the present resources in an entity.

Purpose and Nature of budgets

It helps in forecasting future of an entity by analysing the current data of a firm.

Providing significant financial information related t the firm such as income, costs, profit.

Helps management in order to take decisions

Optimum utilization of all the resources in an entity

Delegating responsibilities among all the employees

3.2 Budgeting methods and its need in organisation

Traditional budgeting- It is that kind of budget which is also recognises as incremental

budget in which income increases from previous period are easily identified (Jones and

et.al., 2013). Previous year figures forms base for the new budgets prepared as the

reasons for the increase or decrease in the company's performance can be found out.

Zero based budget- Modernised version of budgeting in which no base is taken into

account as every budget prepared as fresh without carry forwarding past figures.

Efficiency of the firm get increases as new budgets prepared by them will enhance its

skills and the capabilities.

Fixed Budget- A fixed budget, also called a static budget, is financial plan based on the

assumption of selling specific amounts of goods during a period. In other words, fixed

budgets are based on a set volume of sales or revenues. This is an easy way for

management to plan out expenses and operations when they assume that sales volume

and total revenues will be a set amount during a period.

Flexible Budget- A flexible budget is a budget that adjusts or flexes for changes in the

volume of activity. The flexible budget is more sophisticated and useful than a static

budget, which remains at one amount regardless of the volume of activity.

3.3 Different budgets

Table 5: sales budget

9

future by analysing all the present resources in an entity.

Purpose and Nature of budgets

It helps in forecasting future of an entity by analysing the current data of a firm.

Providing significant financial information related t the firm such as income, costs, profit.

Helps management in order to take decisions

Optimum utilization of all the resources in an entity

Delegating responsibilities among all the employees

3.2 Budgeting methods and its need in organisation

Traditional budgeting- It is that kind of budget which is also recognises as incremental

budget in which income increases from previous period are easily identified (Jones and

et.al., 2013). Previous year figures forms base for the new budgets prepared as the

reasons for the increase or decrease in the company's performance can be found out.

Zero based budget- Modernised version of budgeting in which no base is taken into

account as every budget prepared as fresh without carry forwarding past figures.

Efficiency of the firm get increases as new budgets prepared by them will enhance its

skills and the capabilities.

Fixed Budget- A fixed budget, also called a static budget, is financial plan based on the

assumption of selling specific amounts of goods during a period. In other words, fixed

budgets are based on a set volume of sales or revenues. This is an easy way for

management to plan out expenses and operations when they assume that sales volume

and total revenues will be a set amount during a period.

Flexible Budget- A flexible budget is a budget that adjusts or flexes for changes in the

volume of activity. The flexible budget is more sophisticated and useful than a static

budget, which remains at one amount regardless of the volume of activity.

3.3 Different budgets

Table 5: sales budget

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.