Management Accounting Report: Analysis for Oak Cash & Carry Ltd

VerifiedAdded on 2020/11/12

|16

|5299

|231

Report

AI Summary

This report provides a comprehensive analysis of the management accounting practices at Oak Cash & Carry Ltd, a grocery wholesaler. It explores various management accounting systems, including cost accounting, price optimization, inventory management, and job costing, and their applications within the company. The report details different methods used for management accounting reporting, such as performance reports, account receivable reports, inventory management reports, and job cost reports, evaluating their benefits and integration within the organizational process. Furthermore, it delves into the calculation of costs using appropriate techniques like marginal costing, and discusses the advantages and disadvantages of planning tools used for budgetary control, along with management's responses to financial problems. The report concludes by highlighting how management accounting can lead to sustainable success in addressing financial challenges, providing a thorough overview of financial planning and control within the organization.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types of management accounting systems........................1

P2: Different methods used for management accounting reporting............................................3

M1: Evaluate the benefits of management accounting system and its applications...................4

D1: Management accounting system and its reporting are integrated within organisational

process.........................................................................................................................................5

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate technique..............................................................5

M2 Various types of accounting techniques...............................................................................8

D2 Data interpretation.................................................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used for budgetary control........8

M3 Uses and applications of planning tools for preparing and forecasting budgets................10

P5 Responses of management accounting system to deal with financial problems.................10

M4 Management accounting can lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3 Planning tools respond appropriately to resolve financial problems..................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types of management accounting systems........................1

P2: Different methods used for management accounting reporting............................................3

M1: Evaluate the benefits of management accounting system and its applications...................4

D1: Management accounting system and its reporting are integrated within organisational

process.........................................................................................................................................5

TASK 2............................................................................................................................................5

P3: Calculation of cost using an appropriate technique..............................................................5

M2 Various types of accounting techniques...............................................................................8

D2 Data interpretation.................................................................................................................8

TASK 3............................................................................................................................................8

P4 Advantages and disadvantages of different planning tools used for budgetary control........8

M3 Uses and applications of planning tools for preparing and forecasting budgets................10

P5 Responses of management accounting system to deal with financial problems.................10

M4 Management accounting can lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3 Planning tools respond appropriately to resolve financial problems..................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is the procedure of preparing management reports and accounts

which provide correct and timely financial and statistical data to managers which helps in

making short and long term decision. Management accounting plays an important role in

identifying, analysis, measurement and interpretation and communication of financial data which

management used in planning, evaluating and controlling of information within organisation.

Company follows four basic function of management process that are planning, organising,

controlling and decision making. Management accounting plays a essential role in these

managerial functions performed by all managers at different level of departments (Abdel-

Maksoud, Cheffi and Ghoudi, 2016).

Oak Cash & Carry Ltd is a grocery wholesalers with the registered office located in

Banbury, Oxfordshire UK. In this report company works on various management accounting

systems and its reporting techniques to evaluate company's performance. Cost accountant uses

various costing tools for evaluating its net profit. Oak Cash & Carry Ltd applies several planning

tools that are used in budget controlling and forecasting. Management adopt various accounting

systems to respond its financial issues that assist manager in leading Oak Cash & Carry Ltd to

achieve profitability.

TASK 1

P1: Management accounting and its types of management accounting systems

Management accounting is an essential part of every organisation working. Management

accountant of company develops information which help managers identify the more profitable

products. Company can use management accounting systems such as cost accounting, job

costing, inventory management and price optimisation system that are deployed to render

information for favourable decisions. Oak Cash & Carry Ltd is a grocery wholesalers and offers

a wide range of products in bulk for retailers, offices, caterers and other local businesses. So, it is

important for company to opt various management accounting systems in order to prepare

effective plans and decision to achieve it's objectives.

Types of management accounting systems are explained below:

Cost Accounting Systems: It is a form of management accounting systems, which helps

management to analyse its product's cost. Oak Cash & Carry Ltd purpose of following this

accounting system is to avoid moving over budget so that management can hold their revenues

1

Management accounting is the procedure of preparing management reports and accounts

which provide correct and timely financial and statistical data to managers which helps in

making short and long term decision. Management accounting plays an important role in

identifying, analysis, measurement and interpretation and communication of financial data which

management used in planning, evaluating and controlling of information within organisation.

Company follows four basic function of management process that are planning, organising,

controlling and decision making. Management accounting plays a essential role in these

managerial functions performed by all managers at different level of departments (Abdel-

Maksoud, Cheffi and Ghoudi, 2016).

Oak Cash & Carry Ltd is a grocery wholesalers with the registered office located in

Banbury, Oxfordshire UK. In this report company works on various management accounting

systems and its reporting techniques to evaluate company's performance. Cost accountant uses

various costing tools for evaluating its net profit. Oak Cash & Carry Ltd applies several planning

tools that are used in budget controlling and forecasting. Management adopt various accounting

systems to respond its financial issues that assist manager in leading Oak Cash & Carry Ltd to

achieve profitability.

TASK 1

P1: Management accounting and its types of management accounting systems

Management accounting is an essential part of every organisation working. Management

accountant of company develops information which help managers identify the more profitable

products. Company can use management accounting systems such as cost accounting, job

costing, inventory management and price optimisation system that are deployed to render

information for favourable decisions. Oak Cash & Carry Ltd is a grocery wholesalers and offers

a wide range of products in bulk for retailers, offices, caterers and other local businesses. So, it is

important for company to opt various management accounting systems in order to prepare

effective plans and decision to achieve it's objectives.

Types of management accounting systems are explained below:

Cost Accounting Systems: It is a form of management accounting systems, which helps

management to analyse its product's cost. Oak Cash & Carry Ltd purpose of following this

accounting system is to avoid moving over budget so that management can hold their revenues

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as much of possible. It will help management in determining the costs of products, processes to

ensure that financial statements and reports are as accurate as possible. It is used to identify

closing value of inventory that helps in preparing financial statements. It also assist Oak Cash &

Carry Ltd managers and authorised members of management in forming the most informed

decisions in company's financial planning. Because it provides accurate cost information related

to business. Actual, normal and standard costing are the examples of cost accounting in

determining product actual, budget and normal cost of material, labour and manufacturing

overhead. Company uses this method in identifying where it is earning and losing money (Brock,

Hinings and Powell, 2012).

Price Optimisation Systems: This system refers to customer's demand and the price of

the products is decided according to customer's preference at different price levels which will

help to attract customers and increase future profits. Company follow this system for determine

its initial, promotional and discount pricing. Oak Cash & Carry Ltd uses this system for setting

appropriate pricing strategy and enhance product value among customers that will affect its

profitability. This system consists various information related to operating costs, inventories and

past prices and sales. With the aid of price optimisation system Oak Cash & Carry analysis of

information that anticipate the behaviour of potential buyers at different prices. It also helps to

improve profitability and productivity of the company in order to attain its goals.

Inventory Management System: This system is used as inventory control system where

management can tracks two main functions of company's warehouse i.e. incoming and outgoing

of inventory. This system is important because it determine accurate level of inventory that

automatically minimize under and overstock conditions. First in first out, last in last out,

weighted average are the examples of inventory management. Oak Cash & Carry Ltd adopt this

management system for tracking inventory quantities efficiently across stocking locations and

also assist in making smarter inventory decisions. In order to maintain inventory levels

management uses functions of this system such as creating purchase and sales orders, physical

stock counts by using of FIFO method. This method helps in identify stock level. Oak Cash &

Carry Ltd use this system for improving its bottom line, inventory accuracy and

workflow(Christner and Strömsten, 2015).

Job Costing System: It is system that involves the procedure of accumulating data about

the costs linked with a specific production or service. Process, contract and standard costing are

2

ensure that financial statements and reports are as accurate as possible. It is used to identify

closing value of inventory that helps in preparing financial statements. It also assist Oak Cash &

Carry Ltd managers and authorised members of management in forming the most informed

decisions in company's financial planning. Because it provides accurate cost information related

to business. Actual, normal and standard costing are the examples of cost accounting in

determining product actual, budget and normal cost of material, labour and manufacturing

overhead. Company uses this method in identifying where it is earning and losing money (Brock,

Hinings and Powell, 2012).

Price Optimisation Systems: This system refers to customer's demand and the price of

the products is decided according to customer's preference at different price levels which will

help to attract customers and increase future profits. Company follow this system for determine

its initial, promotional and discount pricing. Oak Cash & Carry Ltd uses this system for setting

appropriate pricing strategy and enhance product value among customers that will affect its

profitability. This system consists various information related to operating costs, inventories and

past prices and sales. With the aid of price optimisation system Oak Cash & Carry analysis of

information that anticipate the behaviour of potential buyers at different prices. It also helps to

improve profitability and productivity of the company in order to attain its goals.

Inventory Management System: This system is used as inventory control system where

management can tracks two main functions of company's warehouse i.e. incoming and outgoing

of inventory. This system is important because it determine accurate level of inventory that

automatically minimize under and overstock conditions. First in first out, last in last out,

weighted average are the examples of inventory management. Oak Cash & Carry Ltd adopt this

management system for tracking inventory quantities efficiently across stocking locations and

also assist in making smarter inventory decisions. In order to maintain inventory levels

management uses functions of this system such as creating purchase and sales orders, physical

stock counts by using of FIFO method. This method helps in identify stock level. Oak Cash &

Carry Ltd use this system for improving its bottom line, inventory accuracy and

workflow(Christner and Strömsten, 2015).

Job Costing System: It is system that involves the procedure of accumulating data about

the costs linked with a specific production or service. Process, contract and standard costing are

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the examples of this costing system. Oak Cash & Carry Ltd is a grocery wholesalers and supply

products in bulk to several retailers, caterers etc. for this it need to follow this system for

acquiring information at various jobs. These details may be required in a way to submit the cost

information to retailers under a contract where costs are refund. Direct material, labour and

overhead costs are the three types of information that accumulate in this system. Oak Cash &

Carry Ltd follow standard costing system for comparing its estimated cost with actual used in

performing its operations (C.R. and Powell, 2012).

P2: Different methods used for management accounting reporting

Management accounting reporting consist accounting information which are derived

from the accounting records of a company. Oak Cash & Carry Ltd is small scale wholesaler

distributor to various retailers and trying to expand their business in future. So, it is essential for

company to prepare management accounting reports so that they maintain their statements on

continuous basis like monthly, quarterly for evaluating their performance. Except financial

reports, Oak Cash & Carry Ltd also need additional reports like budgets, performance and cost

reports of products in analysing its information. Management accounting reporting assist in

maintaining various types of reports such as performance, inventory management, account

receivable and job cost reports that provides necessary information in creating effective plans

and strategies.

Types of management accounting reporting are described below:

Performance Report: It is part of multiple layered report which company's prepare for

evaluating its performance at different levels and forecast for future growth. This report mention

a particular process which is consist of actual collection and transmission of overall performance

information in respect of the project to all related parties. Oak Cash & Carry Ltd prepare this

report for analysing its current status and compare with past for measuring the performance

progress as well as forecast some elements such as workers ability to perform tasks and market

potential of business at all levels. This report set guidelines for all level of managers in

maximizing their department performance which impact on company's overall performance and

also attract stakeholders. It is important for the company to analyse the performance of

employees and its business in market.(Cooper, 2017).

Account Receivable Report: It is one of the simplest methods for analysing the state of

organisation's accounts receivable and print an aging report that is a standard report of every

3

products in bulk to several retailers, caterers etc. for this it need to follow this system for

acquiring information at various jobs. These details may be required in a way to submit the cost

information to retailers under a contract where costs are refund. Direct material, labour and

overhead costs are the three types of information that accumulate in this system. Oak Cash &

Carry Ltd follow standard costing system for comparing its estimated cost with actual used in

performing its operations (C.R. and Powell, 2012).

P2: Different methods used for management accounting reporting

Management accounting reporting consist accounting information which are derived

from the accounting records of a company. Oak Cash & Carry Ltd is small scale wholesaler

distributor to various retailers and trying to expand their business in future. So, it is essential for

company to prepare management accounting reports so that they maintain their statements on

continuous basis like monthly, quarterly for evaluating their performance. Except financial

reports, Oak Cash & Carry Ltd also need additional reports like budgets, performance and cost

reports of products in analysing its information. Management accounting reporting assist in

maintaining various types of reports such as performance, inventory management, account

receivable and job cost reports that provides necessary information in creating effective plans

and strategies.

Types of management accounting reporting are described below:

Performance Report: It is part of multiple layered report which company's prepare for

evaluating its performance at different levels and forecast for future growth. This report mention

a particular process which is consist of actual collection and transmission of overall performance

information in respect of the project to all related parties. Oak Cash & Carry Ltd prepare this

report for analysing its current status and compare with past for measuring the performance

progress as well as forecast some elements such as workers ability to perform tasks and market

potential of business at all levels. This report set guidelines for all level of managers in

maximizing their department performance which impact on company's overall performance and

also attract stakeholders. It is important for the company to analyse the performance of

employees and its business in market.(Cooper, 2017).

Account Receivable Report: It is one of the simplest methods for analysing the state of

organisation's accounts receivable and print an aging report that is a standard report of every

3

organisation. Oak Cash & Carry Ltd prepares this aging report for identifying the amounts

owned by its customers including time duration at which the amounts have been unpaid and

demerits of forecasting tools outstanding. This report consist a list of non paying customers, their

invoices and credit notes which helps in characterising the average collection cycle. Oak Cash &

Carry Ltd also prepare this report for often increasing collection cycle so that company deals

with healthy sales practices. Company identify the list of unpaid creditors and recovery that

amount as soon as possible.

Inventory Management Report: This report display the level of inventory in company

processes. If company inventory is out of stock that may result in loss of customers and if it is

overstock that leads to production loss because of poor management and slow movement in

inventory. Therefore it is necessary for Oak Cash and Carry Ltd to maintain inventory

management report on regular basis. Company is distributor of grocery to various retailers and it

is important to maintain sufficient inventory level by balancing its under and overstock, so that it

meet demand on time. This the reason company find this reporting method very precious (Creel,

2012).

Job Cost reporting: It is a best practices of maintaining job cost reports which every

organisation should keep for identifying and evaluating job expenses so that company track their

efficiency and profitability. Oak Cash & Carry Ltd find this reporting for determining the cost of

several job orders. This reporting method provide a decisive information about current status of

job that assist in estimating the cost and revenue of final job. It also evaluate the investment

recovery amount which is spend on product and that will positively influence on its overall

performance.

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system Oak Cash & Carry Ltd now easily

control their expenses.

It helps in measuring and improving

cost efficiency.

Price optimisation system It assist Oak Cash & Carry Ltd in

setting price according to its product

4

owned by its customers including time duration at which the amounts have been unpaid and

demerits of forecasting tools outstanding. This report consist a list of non paying customers, their

invoices and credit notes which helps in characterising the average collection cycle. Oak Cash &

Carry Ltd also prepare this report for often increasing collection cycle so that company deals

with healthy sales practices. Company identify the list of unpaid creditors and recovery that

amount as soon as possible.

Inventory Management Report: This report display the level of inventory in company

processes. If company inventory is out of stock that may result in loss of customers and if it is

overstock that leads to production loss because of poor management and slow movement in

inventory. Therefore it is necessary for Oak Cash and Carry Ltd to maintain inventory

management report on regular basis. Company is distributor of grocery to various retailers and it

is important to maintain sufficient inventory level by balancing its under and overstock, so that it

meet demand on time. This the reason company find this reporting method very precious (Creel,

2012).

Job Cost reporting: It is a best practices of maintaining job cost reports which every

organisation should keep for identifying and evaluating job expenses so that company track their

efficiency and profitability. Oak Cash & Carry Ltd find this reporting for determining the cost of

several job orders. This reporting method provide a decisive information about current status of

job that assist in estimating the cost and revenue of final job. It also evaluate the investment

recovery amount which is spend on product and that will positively influence on its overall

performance.

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system Oak Cash & Carry Ltd now easily

control their expenses.

It helps in measuring and improving

cost efficiency.

Price optimisation system It assist Oak Cash & Carry Ltd in

setting price according to its product

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

demand.

It helps in determining customer based

pricing strategies.

Inventory management system It helps in identifying sales trend and

customer needs.

It reduces liabilities and loss created by

overstock of Oak Cash and Carry Ltd.

Job costing system It determines company's profitability of each

job individually.

It gives a basis for estimating cost of similar

job in future.

D1: Management accounting system and its reporting are integrated within organisational

process

Oak Cash and Carry Ltd uses several management accounting systems, reporting

methods for evaluating its internal information in order to maximize performance efficiency.

Management accounting systems benefit in organisation's inventory controlling processes by

using inventory management reporting. Job costing system helps in determining its profitability

at individual job levels and cost accounting system assist in measuring cost efficiency.

Performance reports help in evaluating performance at different level of organisation and

account receivable reports identify its average collection period. Therefore above systems and

reporting method evaluate company process that help in improving its performance and

profitability (Flamholtz, 2012).

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is a valuation in terms of money for efforts, materials, resources, time consumed,

risks incurred and opportunity foregone in manufacture and delivery of product or services. Cost

is the total money which an organisation consume in producing the product. Oak Cash & Carry

Ltd set a favourable cost of its product so that it achieving maximum profits. It also identify the

right cost that retailers pay for its grocery at the time of purchase and that cost is satisfactory for

new as well as existing customers.

5

It helps in determining customer based

pricing strategies.

Inventory management system It helps in identifying sales trend and

customer needs.

It reduces liabilities and loss created by

overstock of Oak Cash and Carry Ltd.

Job costing system It determines company's profitability of each

job individually.

It gives a basis for estimating cost of similar

job in future.

D1: Management accounting system and its reporting are integrated within organisational

process

Oak Cash and Carry Ltd uses several management accounting systems, reporting

methods for evaluating its internal information in order to maximize performance efficiency.

Management accounting systems benefit in organisation's inventory controlling processes by

using inventory management reporting. Job costing system helps in determining its profitability

at individual job levels and cost accounting system assist in measuring cost efficiency.

Performance reports help in evaluating performance at different level of organisation and

account receivable reports identify its average collection period. Therefore above systems and

reporting method evaluate company process that help in improving its performance and

profitability (Flamholtz, 2012).

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is a valuation in terms of money for efforts, materials, resources, time consumed,

risks incurred and opportunity foregone in manufacture and delivery of product or services. Cost

is the total money which an organisation consume in producing the product. Oak Cash & Carry

Ltd set a favourable cost of its product so that it achieving maximum profits. It also identify the

right cost that retailers pay for its grocery at the time of purchase and that cost is satisfactory for

new as well as existing customers.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing: It is a costing approach where marginal cost is charged to per unit of

cost while the fixed cost for the period is entirely written off against the contribution. Marginal

cost is also known as variable cost which includes extra units cost of material, labour. It shows

the effects on profit of changes in output by distinguishing between fixed and marginal costs

(Järvenpää and Länsiluoto, 2016).

Absorption costing: It costing method identify the importance of standard costs involved

in production. Oak Cash and Carry Ltd uses this costing technique in identifying its

manufacturing costs that includes in production activities absorbed by sales of the similar

product.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is point where company's total cost is equal to its revenue. It

assist Oak Cash and Carry Ltd in determining the state of no profit or loss. Here company's

opportunity costs have been paid and capital receive expected return.

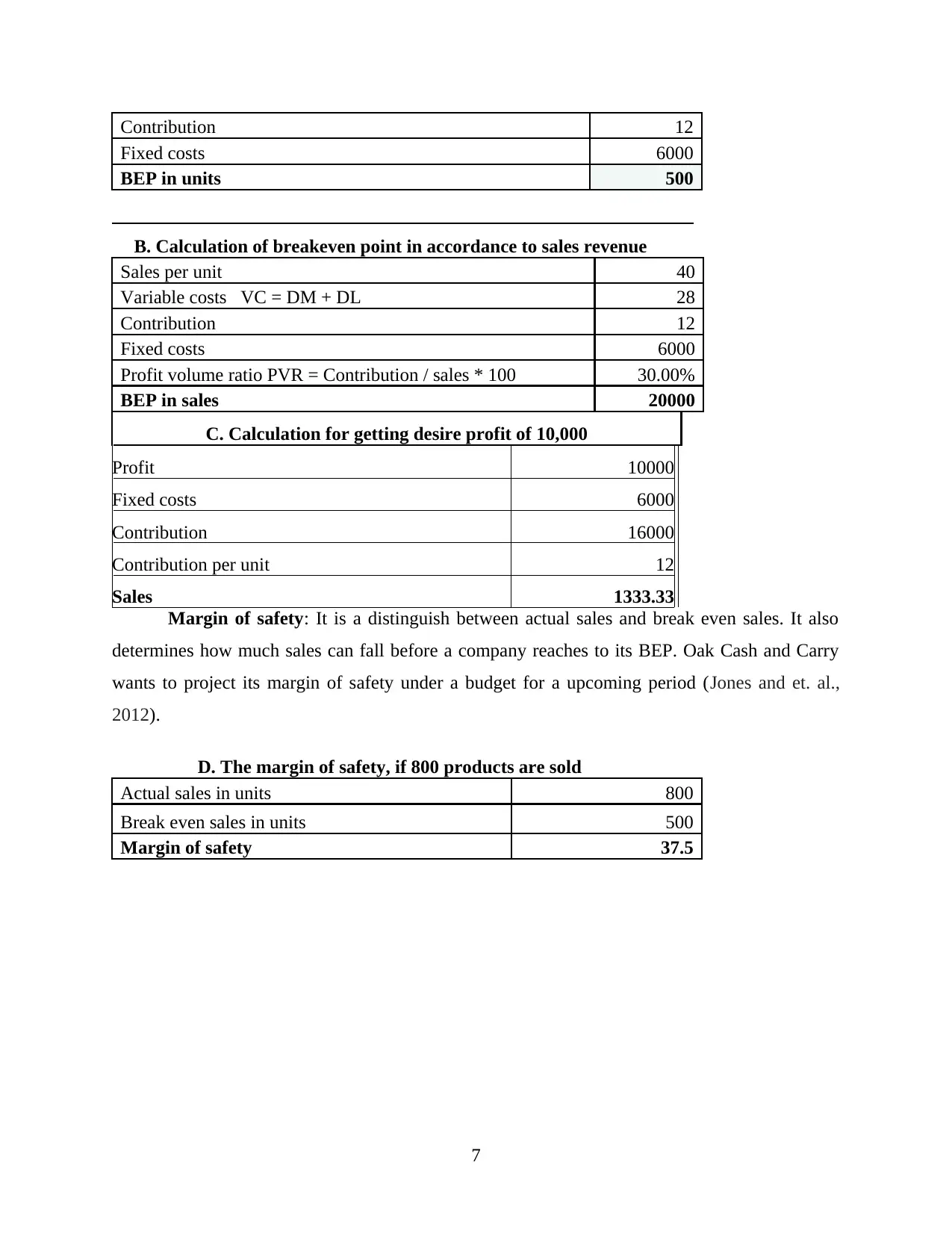

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

6

cost while the fixed cost for the period is entirely written off against the contribution. Marginal

cost is also known as variable cost which includes extra units cost of material, labour. It shows

the effects on profit of changes in output by distinguishing between fixed and marginal costs

(Järvenpää and Länsiluoto, 2016).

Absorption costing: It costing method identify the importance of standard costs involved

in production. Oak Cash and Carry Ltd uses this costing technique in identifying its

manufacturing costs that includes in production activities absorbed by sales of the similar

product.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is point where company's total cost is equal to its revenue. It

assist Oak Cash and Carry Ltd in determining the state of no profit or loss. Here company's

opportunity costs have been paid and capital receive expected return.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

6

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is a distinguish between actual sales and break even sales. It also

determines how much sales can fall before a company reaches to its BEP. Oak Cash and Carry

wants to project its margin of safety under a budget for a upcoming period (Jones and et. al.,

2012).

D. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

7

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is a distinguish between actual sales and break even sales. It also

determines how much sales can fall before a company reaches to its BEP. Oak Cash and Carry

wants to project its margin of safety under a budget for a upcoming period (Jones and et. al.,

2012).

D. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2 Various types of accounting techniques

Standard, marginal and historical costing are the several accounting techniques that are

adopted by Oak Cash and Carry Ltd to determine its net operating income. These techniques are

explained below:

Standard costing: It is used by the managers of Oak Cash and Carry Ltd to determine

the differences between actual cost and budgeted cost. This technique show the deviation in

actual and standard cost.

Marginal costing: This technique is used to analyse extra cost which occurs when

company is producing additional units in production. It determines the opportunity cost that

arises when the quantity produced is increased by extra units (Jordan, Jørgensen and Mitterhofer,

2013).

Historical costing: It is the original cost on the asset, that is recorded in the financial

statements of the company. It can be easily verified by assessing the source acquired and trade

documents.

D2 Data interpretation

As per the above calculation, it is cleared that marginal costing technique is more

beneficial for Oak Cash and Carry Ltd as compare to absorption costing method. It is because it

shows more profit. While computing net profits by marginal costing technique it shows £17500

as profits and absorption costing techniques shows £15675 as profit. When break even point is

calculated, the total numbers of units sold are 500 and total BEP sales is £20000. If the company

want to earn minimum profit of £10000 then it have to sale 1333.33 units. Margin of safety is

37.5 when 800 units are sold by the company.

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

Budgetary control is used to determine various results with the help of forecasted figures

of the company. It is a method that is implemented to control cost which includes preparation of

budgets, coordinating and distributing responsibilities to the departments, comparison of actual

and forecasted performance. It helps to maintain proper workforce that result to achieve

maximum profitability(Lee, Matsunaga and Park, 2012). Budgetary control process involve

various steps such as assigning responsibilities, preparing budget manual, forming budget

committee, setting budget period etc. Oak Cash and Carry Ltd. is a grocery wholesale company it

8

Standard, marginal and historical costing are the several accounting techniques that are

adopted by Oak Cash and Carry Ltd to determine its net operating income. These techniques are

explained below:

Standard costing: It is used by the managers of Oak Cash and Carry Ltd to determine

the differences between actual cost and budgeted cost. This technique show the deviation in

actual and standard cost.

Marginal costing: This technique is used to analyse extra cost which occurs when

company is producing additional units in production. It determines the opportunity cost that

arises when the quantity produced is increased by extra units (Jordan, Jørgensen and Mitterhofer,

2013).

Historical costing: It is the original cost on the asset, that is recorded in the financial

statements of the company. It can be easily verified by assessing the source acquired and trade

documents.

D2 Data interpretation

As per the above calculation, it is cleared that marginal costing technique is more

beneficial for Oak Cash and Carry Ltd as compare to absorption costing method. It is because it

shows more profit. While computing net profits by marginal costing technique it shows £17500

as profits and absorption costing techniques shows £15675 as profit. When break even point is

calculated, the total numbers of units sold are 500 and total BEP sales is £20000. If the company

want to earn minimum profit of £10000 then it have to sale 1333.33 units. Margin of safety is

37.5 when 800 units are sold by the company.

TASK 3

P4 Advantages and disadvantages of different planning tools used for budgetary control

Budgetary control is used to determine various results with the help of forecasted figures

of the company. It is a method that is implemented to control cost which includes preparation of

budgets, coordinating and distributing responsibilities to the departments, comparison of actual

and forecasted performance. It helps to maintain proper workforce that result to achieve

maximum profitability(Lee, Matsunaga and Park, 2012). Budgetary control process involve

various steps such as assigning responsibilities, preparing budget manual, forming budget

committee, setting budget period etc. Oak Cash and Carry Ltd. is a grocery wholesale company it

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

uses three types of planning tools, Forecasting, contingency and scenario tools. These are

explained below:

Forecasting tools: It is a fundamental setup that is used to figure out the deals and

income chart of business. It is used by Oak Cash and Carry Ltd. to forecast internal and external

factors affecting its business, to plan active strategies that helps to grow the business and

increase the sales and profits. These tools are used to forecast future situations with the help of

past reports and current trends (Lindholm, Laine and Suomala, 2017).

Advantages Disadvantages

It helps to evaluate possible outcomes for the

company.

It provide valuable information to the company

for better decision making.

Not possible to forecast the accurate future.

The reports are generated with the help of these

tools are based on past events.

Contingency tools: These tools are used by Oak Cash and Carry Ltd to determine the

event or consequence that might happen in future. It is basically related to negative events and

help the company to be prepare fro that particular risk or uncertainty. These tools are used to

respond appropriately to the negative event that might happen.

Advantages Disadvantages

It help to minimize the loss or production by

estimating the uncertainty.

It helps the company to be ready in advance to

face any consequences in future.

If any risk doesn't occur then the money

invested for the plan is wasted.

The implementation of this process is very

complex for small companies like Oak

Cash and Carry Ltd.

Scenario tools: These tools are used by Oak Cash and Carry Ltd to evaluate the

effectiveness of strategies, plans and decisions that are taken by the management. These tools are

very effective and are used in strategic planning to make long term flexible plans to increase the

profit level of the organisation (Rieckhof, Bergmann and Guenther, 2015).

Advantages Disadvantages

It helps to to understand the possible

implications and benefits of different

It is not useful while making short term

9

explained below:

Forecasting tools: It is a fundamental setup that is used to figure out the deals and

income chart of business. It is used by Oak Cash and Carry Ltd. to forecast internal and external

factors affecting its business, to plan active strategies that helps to grow the business and

increase the sales and profits. These tools are used to forecast future situations with the help of

past reports and current trends (Lindholm, Laine and Suomala, 2017).

Advantages Disadvantages

It helps to evaluate possible outcomes for the

company.

It provide valuable information to the company

for better decision making.

Not possible to forecast the accurate future.

The reports are generated with the help of these

tools are based on past events.

Contingency tools: These tools are used by Oak Cash and Carry Ltd to determine the

event or consequence that might happen in future. It is basically related to negative events and

help the company to be prepare fro that particular risk or uncertainty. These tools are used to

respond appropriately to the negative event that might happen.

Advantages Disadvantages

It help to minimize the loss or production by

estimating the uncertainty.

It helps the company to be ready in advance to

face any consequences in future.

If any risk doesn't occur then the money

invested for the plan is wasted.

The implementation of this process is very

complex for small companies like Oak

Cash and Carry Ltd.

Scenario tools: These tools are used by Oak Cash and Carry Ltd to evaluate the

effectiveness of strategies, plans and decisions that are taken by the management. These tools are

very effective and are used in strategic planning to make long term flexible plans to increase the

profit level of the organisation (Rieckhof, Bergmann and Guenther, 2015).

Advantages Disadvantages

It helps to to understand the possible

implications and benefits of different

It is not useful while making short term

9

approaches.

These tools are very helpful for the

management to make good decisions.

decisions.

It requires controlled monitoring,

analysis and communication process.

M3 Uses and applications of planning tools for preparing and forecasting budgets

Oak Cash and Carry Ltd use three types of planning tools to prepare and forecast

budgets. Those planning tools are forecasting, contingency and scenario tools. These planning

tools are helpful in determining future risks and uncertainties. These tools provide various

information to the management to make appropriate decisions. It helps the managers to be

prepare for the events that might happen in future and reserve resources to deal with the same.

Management can make long term plan by using these tools and it will enhance the productivity

and increase profits for the company. It also help to reduce the production loss by estimating

possible events.

P5 Responses of management accounting system to deal with financial problems

Facing financial problems is a state, in which an organisation have to deal with money

related problems. These problems occur when an organisation is not able to properly maintain its

monetary resources. Oak Cash and Carry Ltd is facing various types of financial problems. The

problems are explained below:

Late payments by clients: The main financial problem that is faced by Oak Cash and

Carry Ltd is receiving late payments from debtors. If they don't make payments on time then

company will have to face the problem of lesser monetary resources to fulfil their requirements.

Late payments from clients will also create higher debts because if company is not having proper

finance then it has to buy goods on credit.

Improper money management system: Improper money management also creates

financial issues for Oak Cash and Carry Ltd. When the system is not properly maintained then it

cannot show the accurate financial reports and then managers are not able to get the exact

information of finance. Incorrect information of finance will guide the managers to take wrong

decision related to monetary resources (Spraakman, 2015).

Sudden expenses: It refers to those expense which are not planned by the managers and

suddenly occur. The managers of Oak Cash and Carry Ltd have to deal with such type of

problems and have to spend money. The managers have to use monetary resources for these

expenses and it create the deficiency of resources that converts to financial problem.

10

These tools are very helpful for the

management to make good decisions.

decisions.

It requires controlled monitoring,

analysis and communication process.

M3 Uses and applications of planning tools for preparing and forecasting budgets

Oak Cash and Carry Ltd use three types of planning tools to prepare and forecast

budgets. Those planning tools are forecasting, contingency and scenario tools. These planning

tools are helpful in determining future risks and uncertainties. These tools provide various

information to the management to make appropriate decisions. It helps the managers to be

prepare for the events that might happen in future and reserve resources to deal with the same.

Management can make long term plan by using these tools and it will enhance the productivity

and increase profits for the company. It also help to reduce the production loss by estimating

possible events.

P5 Responses of management accounting system to deal with financial problems

Facing financial problems is a state, in which an organisation have to deal with money

related problems. These problems occur when an organisation is not able to properly maintain its

monetary resources. Oak Cash and Carry Ltd is facing various types of financial problems. The

problems are explained below:

Late payments by clients: The main financial problem that is faced by Oak Cash and

Carry Ltd is receiving late payments from debtors. If they don't make payments on time then

company will have to face the problem of lesser monetary resources to fulfil their requirements.

Late payments from clients will also create higher debts because if company is not having proper

finance then it has to buy goods on credit.

Improper money management system: Improper money management also creates

financial issues for Oak Cash and Carry Ltd. When the system is not properly maintained then it

cannot show the accurate financial reports and then managers are not able to get the exact

information of finance. Incorrect information of finance will guide the managers to take wrong

decision related to monetary resources (Spraakman, 2015).

Sudden expenses: It refers to those expense which are not planned by the managers and

suddenly occur. The managers of Oak Cash and Carry Ltd have to deal with such type of

problems and have to spend money. The managers have to use monetary resources for these

expenses and it create the deficiency of resources that converts to financial problem.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.