Evaluation of Costing Methods and Systems: Connectta Ltd Report

VerifiedAdded on 2023/04/03

|14

|2537

|207

Report

AI Summary

This report provides a detailed analysis of the costing system employed by Connectta Limited, focusing on the job costing method. The report evaluates the suitability of job costing, examines the balance of work-in-process inventory, and calculates the cost of finished goods. It addresses the treatment of over-applied or under-applied overhead, exploring alternative accounting methods. Furthermore, the report highlights the benefits of activity-based costing over job costing, emphasizing its ability to create separate cost pools for service activities and assign overhead costs more accurately using cost drivers. The analysis includes a comparison of cost assignment, two-stage assignment, and the utilization of historical costs in both costing systems, concluding with recommendations for Connectta Limited to mitigate deficiencies in its current system by adopting activity-based costing.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Executive Summary:

The current report would focus on analysing the costing system for conducting its business

operations by Connectta Limited. From the case information, it has been identified that the firm

follows job costing system in order to make sound disclosure of business costs. In case of job

costing system, the overhead costs related to the service departments are assigned to the

production departments and hence, there is limitation of cost pools in the system. However, the

activity-based costing procedure assists in creating separate cost pools for the service activities

along with overhead costs associated with service activities, which are apportioned directly to the

specific products by applying the rates of cost drivers.

Executive Summary:

The current report would focus on analysing the costing system for conducting its business

operations by Connectta Limited. From the case information, it has been identified that the firm

follows job costing system in order to make sound disclosure of business costs. In case of job

costing system, the overhead costs related to the service departments are assigned to the

production departments and hence, there is limitation of cost pools in the system. However, the

activity-based costing procedure assists in creating separate cost pools for the service activities

along with overhead costs associated with service activities, which are apportioned directly to the

specific products by applying the rates of cost drivers.

2MANAGEMENT ACCOUNTING

Table of Contents

Introduction:....................................................................................................................................3

1. Suitability of using job costing system for an organisation:........................................................3

2. Balance of work-in-process inventory account of Connectta Limited:.......................................4

3. Cost of the chairs in finished goods inventory:...........................................................................5

4. Over-applied or under-applied overhead for the year:................................................................6

5. Alternative accounting treatments under job costing system for under-applied or over-applied

overhead balances:...........................................................................................................................6

6. Benefits of activity-based costing over job costing system:........................................................7

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

Table of Contents

Introduction:....................................................................................................................................3

1. Suitability of using job costing system for an organisation:........................................................3

2. Balance of work-in-process inventory account of Connectta Limited:.......................................4

3. Cost of the chairs in finished goods inventory:...........................................................................5

4. Over-applied or under-applied overhead for the year:................................................................6

5. Alternative accounting treatments under job costing system for under-applied or over-applied

overhead balances:...........................................................................................................................6

6. Benefits of activity-based costing over job costing system:........................................................7

Conclusion:....................................................................................................................................10

References:....................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Introduction:

The current report would focus on analysing the costing system for conducting its

business operations by Connectta Limited. From the case information, it has been identified that

the firm follows job costing system in order to make sound disclosure of business costs. The

paper would focus on evaluating the costing methods, which are available to the organisation and

the possible ways through improvements could be made. Different costs are calculated for

Connectta Limited. Moreover, the alternative accounting treatments in relation to overhead costs

and their likely effects have been discussed adequately in this paper. The analysis would be

performed for under-applied or over-applied overhead costs and the ways of treating them from

the cost accounting perspective. The report would shed light on the role performed by activity-

based costing system and the techniques through which the management of the firm could be

assisted to make decisions for ensuring economic growth in future. In other words, the benefits

of activity-based costing system would be discussed for mitigating the deficiencies inherent in

traditional costing system.

1. Suitability of using job costing system for an organisation:

The section has laid stress on different aspects related to the cost accounting reporting

framework and the framework that is followed by Connectta Limited. In the existing market

situation, a firm is required determining the appropriate project costs in order to estimate profits

and product prices that would be offered to the customers (Balakrishnan, Labro & Soderstrom,

2014). Job costing system is described as the system that a firm uses for meeting the orders made

by the customers. From the viewpoint of the business, the management of Connectta Limited

applies job costing technique for controlling the use of raw materials. The customer orders are

Introduction:

The current report would focus on analysing the costing system for conducting its

business operations by Connectta Limited. From the case information, it has been identified that

the firm follows job costing system in order to make sound disclosure of business costs. The

paper would focus on evaluating the costing methods, which are available to the organisation and

the possible ways through improvements could be made. Different costs are calculated for

Connectta Limited. Moreover, the alternative accounting treatments in relation to overhead costs

and their likely effects have been discussed adequately in this paper. The analysis would be

performed for under-applied or over-applied overhead costs and the ways of treating them from

the cost accounting perspective. The report would shed light on the role performed by activity-

based costing system and the techniques through which the management of the firm could be

assisted to make decisions for ensuring economic growth in future. In other words, the benefits

of activity-based costing system would be discussed for mitigating the deficiencies inherent in

traditional costing system.

1. Suitability of using job costing system for an organisation:

The section has laid stress on different aspects related to the cost accounting reporting

framework and the framework that is followed by Connectta Limited. In the existing market

situation, a firm is required determining the appropriate project costs in order to estimate profits

and product prices that would be offered to the customers (Balakrishnan, Labro & Soderstrom,

2014). Job costing system is described as the system that a firm uses for meeting the orders made

by the customers. From the viewpoint of the business, the management of Connectta Limited

applies job costing technique for controlling the use of raw materials. The customer orders are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

taken into account by the organisations so that the overall demand could be met accordingly. By

considering the significant business activities, the management has a number of alternatives

regarding the selection of the appropriate costing system, which requires application depending

on business operations. The reason behind the use of job costing system is to estimate the total

cost of the manufacturing overheads and the firms depending more on customers for fulfilling

the production requirements coupled with generating operating revenue (Banker & Byzalov,

2014).

The method is viable for those firms functioning in the manufacturing industry and the

costs are disclosed in the costing reports, which are formulated by complying with the job

costing method principles. Various firms are identified to be using the job costing system for

effective presentation of business expenses and they mainly include hospitals, manufacturers and

other businesses (Brewer, Garrison & Noreen, 2015). Hence, job costing method is a procedure

of determining cost for only one cost unit, which is for a specific job. This system is considered

to be beneficial under certain circumstances, which are discussed mainly as follows:

Job costing system is used when any firm is providing any particular product depending

on specific needs of the customers.

Another situation where this system is applied is when a firm produces a variety of

identical or alike products (Christ & Burritt, 2015).

2. Balance of work-in-process inventory account of Connectta Limited:

taken into account by the organisations so that the overall demand could be met accordingly. By

considering the significant business activities, the management has a number of alternatives

regarding the selection of the appropriate costing system, which requires application depending

on business operations. The reason behind the use of job costing system is to estimate the total

cost of the manufacturing overheads and the firms depending more on customers for fulfilling

the production requirements coupled with generating operating revenue (Banker & Byzalov,

2014).

The method is viable for those firms functioning in the manufacturing industry and the

costs are disclosed in the costing reports, which are formulated by complying with the job

costing method principles. Various firms are identified to be using the job costing system for

effective presentation of business expenses and they mainly include hospitals, manufacturers and

other businesses (Brewer, Garrison & Noreen, 2015). Hence, job costing method is a procedure

of determining cost for only one cost unit, which is for a specific job. This system is considered

to be beneficial under certain circumstances, which are discussed mainly as follows:

Job costing system is used when any firm is providing any particular product depending

on specific needs of the customers.

Another situation where this system is applied is when a firm produces a variety of

identical or alike products (Christ & Burritt, 2015).

2. Balance of work-in-process inventory account of Connectta Limited:

5MANAGEMENT ACCOUNTING

Woking note:

3. Cost of the chairs in finished goods inventory:

Working notes:

It has been identified that Job CH 291 is engaged in chair production, which mandates the

need to determine the cost of the specified job.

The firm is identified to be using the First-In-First-Out (FIFO) method of inventory

system. Hence, the finished goods inventory units constitute of the units completed during the

December month.

Woking note:

3. Cost of the chairs in finished goods inventory:

Working notes:

It has been identified that Job CH 291 is engaged in chair production, which mandates the

need to determine the cost of the specified job.

The firm is identified to be using the First-In-First-Out (FIFO) method of inventory

system. Hence, the finished goods inventory units constitute of the units completed during the

December month.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

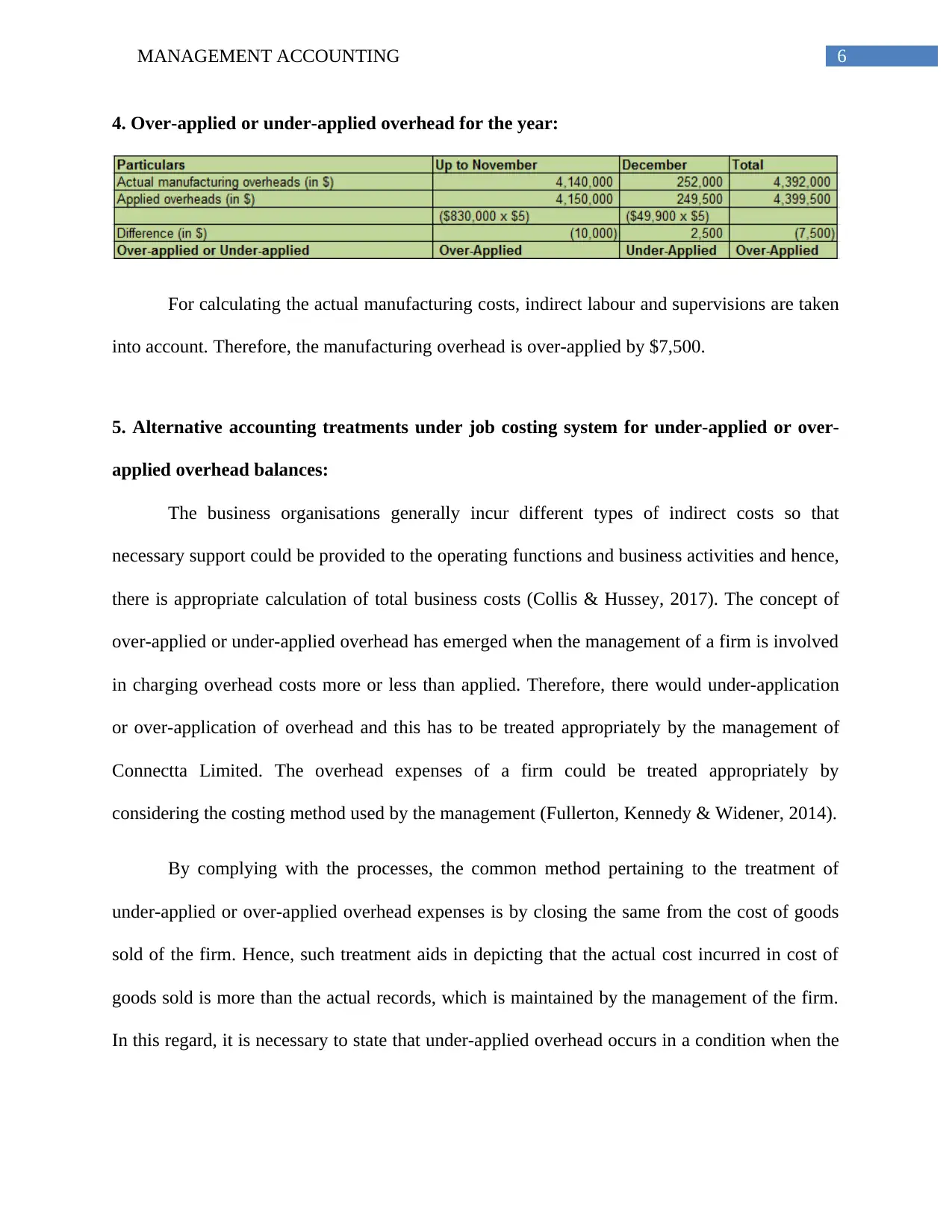

4. Over-applied or under-applied overhead for the year:

For calculating the actual manufacturing costs, indirect labour and supervisions are taken

into account. Therefore, the manufacturing overhead is over-applied by $7,500.

5. Alternative accounting treatments under job costing system for under-applied or over-

applied overhead balances:

The business organisations generally incur different types of indirect costs so that

necessary support could be provided to the operating functions and business activities and hence,

there is appropriate calculation of total business costs (Collis & Hussey, 2017). The concept of

over-applied or under-applied overhead has emerged when the management of a firm is involved

in charging overhead costs more or less than applied. Therefore, there would under-application

or over-application of overhead and this has to be treated appropriately by the management of

Connectta Limited. The overhead expenses of a firm could be treated appropriately by

considering the costing method used by the management (Fullerton, Kennedy & Widener, 2014).

By complying with the processes, the common method pertaining to the treatment of

under-applied or over-applied overhead expenses is by closing the same from the cost of goods

sold of the firm. Hence, such treatment aids in depicting that the actual cost incurred in cost of

goods sold is more than the actual records, which is maintained by the management of the firm.

In this regard, it is necessary to state that under-applied overhead occurs in a condition when the

4. Over-applied or under-applied overhead for the year:

For calculating the actual manufacturing costs, indirect labour and supervisions are taken

into account. Therefore, the manufacturing overhead is over-applied by $7,500.

5. Alternative accounting treatments under job costing system for under-applied or over-

applied overhead balances:

The business organisations generally incur different types of indirect costs so that

necessary support could be provided to the operating functions and business activities and hence,

there is appropriate calculation of total business costs (Collis & Hussey, 2017). The concept of

over-applied or under-applied overhead has emerged when the management of a firm is involved

in charging overhead costs more or less than applied. Therefore, there would under-application

or over-application of overhead and this has to be treated appropriately by the management of

Connectta Limited. The overhead expenses of a firm could be treated appropriately by

considering the costing method used by the management (Fullerton, Kennedy & Widener, 2014).

By complying with the processes, the common method pertaining to the treatment of

under-applied or over-applied overhead expenses is by closing the same from the cost of goods

sold of the firm. Hence, such treatment aids in depicting that the actual cost incurred in cost of

goods sold is more than the actual records, which is maintained by the management of the firm.

In this regard, it is necessary to state that under-applied overhead occurs in a condition when the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

cost of applied overhead goes below the actual overhead expenses of the firm (Hopper & Bui,

2016).

When there is under-application or over-application of overhead cost and if the same

does not have important nature, treatment would be made as period costs and it would be closed

with the cost of goods sold account of the firm. However, if over-applied or under-applied

overhead costs are found to be significant, it mandates the need of incorporating the same within

the pertinent accounts. The pertinent accounts have to be considered from the perspective of the

costing system of the concerned entity.

By considering the above-discussed aspects, it could be said that under-applied or over-

applied disposal of manufacturing expenses could be formulated in two ways. One method is to

charge manufacturing overhead to the cost of goods sold account or the same is possible to be

applied on finished goods inventory, cost of goods sold and work-in-process inventory in the

cost percentage carried by the pertinent accounts (Kamal, 2015). However, the final treatment

would be similar for both alternatives.

6. Benefits of activity-based costing over job costing system:

Activity-based costing system is an accounting procedure, which is utilised by an

organisation for sound cost identification pertaining to business operations and they are assigned

to the overhead expenses appropriately. With the help of this method, it becomes possible to

realise the association among costs, overhead expenses and activities produced by the company

(Kaplan & Atkinson, 2015). The system is considered as the most popular costing procedure in

terms of cost identification, since it could be connected with the essential business activities. The

cost of applied overhead goes below the actual overhead expenses of the firm (Hopper & Bui,

2016).

When there is under-application or over-application of overhead cost and if the same

does not have important nature, treatment would be made as period costs and it would be closed

with the cost of goods sold account of the firm. However, if over-applied or under-applied

overhead costs are found to be significant, it mandates the need of incorporating the same within

the pertinent accounts. The pertinent accounts have to be considered from the perspective of the

costing system of the concerned entity.

By considering the above-discussed aspects, it could be said that under-applied or over-

applied disposal of manufacturing expenses could be formulated in two ways. One method is to

charge manufacturing overhead to the cost of goods sold account or the same is possible to be

applied on finished goods inventory, cost of goods sold and work-in-process inventory in the

cost percentage carried by the pertinent accounts (Kamal, 2015). However, the final treatment

would be similar for both alternatives.

6. Benefits of activity-based costing over job costing system:

Activity-based costing system is an accounting procedure, which is utilised by an

organisation for sound cost identification pertaining to business operations and they are assigned

to the overhead expenses appropriately. With the help of this method, it becomes possible to

realise the association among costs, overhead expenses and activities produced by the company

(Kaplan & Atkinson, 2015). The system is considered as the most popular costing procedure in

terms of cost identification, since it could be connected with the essential business activities. The

8MANAGEMENT ACCOUNTING

overhead costs of the entity assign the indirect costs appropriately when they are contrasted with

the conventional methods of costing such as the job costing system.

The manufacturing companies mainly use the system because there is improvement in the

reliability of cost data and hence, sound presentation of business expenses could be conducted

accordingly. Due to this, the management of the firm could make effective decisions regarding

the cost components (Klychova, Faskhutdinova & Sadrieva, 2014). Certain ways are inherent by

which activity-based costing system could mitigate the loopholes in the job costing procedure of

Connectta Limited, which are elaborated below:

Assignment of cost:

Both activity-based costing and job costing system conduct costing related to a cost

object; however, there are differences in the methodologies of both the systems. For example, it

is estimated that any particular job of Connectta Limited consumes significant amount of labour

and materials, which could be measured appropriately. Hence, it is possible to conduct the

costing of the two systems similarly like the job costing system, which is made by multiplying

the labour hours utilised by the component by the per hour labour rate (Lavia López & Hiebl,

2014). In addition, the overhead portion of the form would be added, which has been consumed

on the part of the component.

Under the traditional costing technique, this procedure is conducted by loading a

percentage of the total overhead cost of the company to the component. However, in case of

activity-based costing procedure, the actual activities of overhead have to be determined, which

are performed on the component. The cost drivers are used for measurement of overhead

activities. Per unit cost of each activity is calculated by dividing the overhead cost pool of that

overhead costs of the entity assign the indirect costs appropriately when they are contrasted with

the conventional methods of costing such as the job costing system.

The manufacturing companies mainly use the system because there is improvement in the

reliability of cost data and hence, sound presentation of business expenses could be conducted

accordingly. Due to this, the management of the firm could make effective decisions regarding

the cost components (Klychova, Faskhutdinova & Sadrieva, 2014). Certain ways are inherent by

which activity-based costing system could mitigate the loopholes in the job costing procedure of

Connectta Limited, which are elaborated below:

Assignment of cost:

Both activity-based costing and job costing system conduct costing related to a cost

object; however, there are differences in the methodologies of both the systems. For example, it

is estimated that any particular job of Connectta Limited consumes significant amount of labour

and materials, which could be measured appropriately. Hence, it is possible to conduct the

costing of the two systems similarly like the job costing system, which is made by multiplying

the labour hours utilised by the component by the per hour labour rate (Lavia López & Hiebl,

2014). In addition, the overhead portion of the form would be added, which has been consumed

on the part of the component.

Under the traditional costing technique, this procedure is conducted by loading a

percentage of the total overhead cost of the company to the component. However, in case of

activity-based costing procedure, the actual activities of overhead have to be determined, which

are performed on the component. The cost drivers are used for measurement of overhead

activities. Per unit cost of each activity is calculated by dividing the overhead cost pool of that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

activity by the units of cost drivers at the firm level (Lukka & Vinnari, 2014). After the process,

it is necessary to multiply the units of cost drivers used actually by the component with the cost

driver rate. By using the same, the actual overhead activity cost has to be ascertained, which is

conducted on the component. This results in better assignment of overhead expense in activity-

based costing system when it is contrasted with the job costing system.

Two-stage assignment:

In case of job costing system, the overhead costs related to the service departments are

assigned to the production departments and hence, there is limitation of cost pools in the system.

However, the activity-based costing procedure assists in creating separate cost pools for the

service activities along with overhead costs associated with service activities, which are

apportioned directly to the specific products by applying the rates of cost drivers (Otley, 2016).

Hence, by utilising the activity-based costing procedure, there is no need to assign or reapportion

overheads associated with the service departments.

Utilisation of historical costs:

The historical orientation between job costing system and activity-based costing system

differs from each other. Generally, any entity uses the actual historical cost for formulating the

manufacturing cost standards (Parker & Fleischman, 2017). Such costs generally take into

consideration rework, inefficiency, duplication, waste and redundancy. By accepting historical

costs and depicting the costs on standards do not provide support to the continuous improvement.

Under any competitive situation where the competitors are found to be proactive in activity and

waste elimination improvements, an organisation could move out of its standards for effective

fulfilment of the same (Shields, 2015).

activity by the units of cost drivers at the firm level (Lukka & Vinnari, 2014). After the process,

it is necessary to multiply the units of cost drivers used actually by the component with the cost

driver rate. By using the same, the actual overhead activity cost has to be ascertained, which is

conducted on the component. This results in better assignment of overhead expense in activity-

based costing system when it is contrasted with the job costing system.

Two-stage assignment:

In case of job costing system, the overhead costs related to the service departments are

assigned to the production departments and hence, there is limitation of cost pools in the system.

However, the activity-based costing procedure assists in creating separate cost pools for the

service activities along with overhead costs associated with service activities, which are

apportioned directly to the specific products by applying the rates of cost drivers (Otley, 2016).

Hence, by utilising the activity-based costing procedure, there is no need to assign or reapportion

overheads associated with the service departments.

Utilisation of historical costs:

The historical orientation between job costing system and activity-based costing system

differs from each other. Generally, any entity uses the actual historical cost for formulating the

manufacturing cost standards (Parker & Fleischman, 2017). Such costs generally take into

consideration rework, inefficiency, duplication, waste and redundancy. By accepting historical

costs and depicting the costs on standards do not provide support to the continuous improvement.

Under any competitive situation where the competitors are found to be proactive in activity and

waste elimination improvements, an organisation could move out of its standards for effective

fulfilment of the same (Shields, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

Although historical resource costs are used in the calculations of activity-based costing

system, the orientation in activity-based costing system is not similar to that of job costing

system. It has been identified that some proponents of activity-based costing system lays

additional emphasis on the future competitive positions and historical cost is used only as a

baseline for improvement in business operations and activities (Tappura et al., 2015).

By taking into account the above analysis, Connectta Limited would be able to mitigate

the deficiencies in the current costing system by using the activity-based costing system within

the firm.

Conclusion:

The above discussion makes it evident that the management of Connectta Limited applies

job costing technique for controlling the use of raw materials. The customer orders are taken into

account by the organisations so that the overall demand could be met accordingly. By

considering the significant business activities, the management has a number of alternatives

regarding the selection of the appropriate costing system, which requires application depending

on business operations. The reason behind the use of job costing system is to estimate the total

cost of the manufacturing overheads and the firms depending more on customers for fulfilling

the production requirements coupled with generating operating revenue.

Under-applied or over-applied disposal of manufacturing expenses could be formulated

in two ways. One method is to charge manufacturing overhead to the cost of goods sold account

or the same is possible to be applied on finished goods inventory, cost of goods sold and work-

in-process inventory in the cost percentage carried by the pertinent accounts. In case of job

costing system, the overhead costs related to the service departments are assigned to the

Although historical resource costs are used in the calculations of activity-based costing

system, the orientation in activity-based costing system is not similar to that of job costing

system. It has been identified that some proponents of activity-based costing system lays

additional emphasis on the future competitive positions and historical cost is used only as a

baseline for improvement in business operations and activities (Tappura et al., 2015).

By taking into account the above analysis, Connectta Limited would be able to mitigate

the deficiencies in the current costing system by using the activity-based costing system within

the firm.

Conclusion:

The above discussion makes it evident that the management of Connectta Limited applies

job costing technique for controlling the use of raw materials. The customer orders are taken into

account by the organisations so that the overall demand could be met accordingly. By

considering the significant business activities, the management has a number of alternatives

regarding the selection of the appropriate costing system, which requires application depending

on business operations. The reason behind the use of job costing system is to estimate the total

cost of the manufacturing overheads and the firms depending more on customers for fulfilling

the production requirements coupled with generating operating revenue.

Under-applied or over-applied disposal of manufacturing expenses could be formulated

in two ways. One method is to charge manufacturing overhead to the cost of goods sold account

or the same is possible to be applied on finished goods inventory, cost of goods sold and work-

in-process inventory in the cost percentage carried by the pertinent accounts. In case of job

costing system, the overhead costs related to the service departments are assigned to the

11MANAGEMENT ACCOUNTING

production departments and hence, there is limitation of cost pools in the system. However, the

activity-based costing procedure assists in creating separate cost pools for the service activities

along with overhead costs associated with service activities, which are apportioned directly to the

specific products by applying the rates of cost drivers.

production departments and hence, there is limitation of cost pools in the system. However, the

activity-based costing procedure assists in creating separate cost pools for the service activities

along with overhead costs associated with service activities, which are apportioned directly to the

specific products by applying the rates of cost drivers.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.