Management Accounting Solutions for Bizdaq

VerifiedAdded on 2020/06/06

|21

|5528

|197

AI Summary

This assignment explores the financial difficulties encountered by a company named Bizdaq, which include excessive debt, poor purchasing decisions, and ineffective investment choices. The focus is on how management accounting tools can help Bizdaq improve sales revenue, return on capital invested, and overall financial performance. The solution proposes using Key Performance Indicators (KPIs), benchmarking against competitors, and implementing robust budgetary control measures to address these issues.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Concept of management accounting and their kinds to company.....................................3

P2 Report to the General manager concerning to methods of management accounting reports 6

TASK 2..........................................................................................................................................10

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:........................................................................................10

TASK 3..........................................................................................................................................14

P4 Advantages and disadvantage of various kinds of planning tools for the budgetary control

..............................................................................................................................................14

P5 Management accounting system use in solving financial problems...............................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

.......................................................................................................................................................19

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Concept of management accounting and their kinds to company.....................................3

P2 Report to the General manager concerning to methods of management accounting reports 6

TASK 2..........................................................................................................................................10

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:........................................................................................10

TASK 3..........................................................................................................................................14

P4 Advantages and disadvantage of various kinds of planning tools for the budgetary control

..............................................................................................................................................14

P5 Management accounting system use in solving financial problems...............................17

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

.......................................................................................................................................................19

INTRODUCTION

In management accounting, managers uses regulations data accounting to get support in

decision-making process of an organisation (Banerjee, 2010). Management accounting is a

provision of financial and non-financial decision-making informations to top management.

According to Chenhall, 2012 “Management accounting is a process that contains involvement in

decision making, allocation planning and performance management systems and it also provides

proficiency in financial reporting to support management in implementing organisation's

strategies”.

Bizdaq was established in 2015, it is in Business sales sectors. Company gives a

marketplace for sale. It's annual turnover is £100,000.

This assignment consists of various types of management accounting systems and their

methods. To enlighten the features of budget control, advantages and disadvantages of various

types of budgetary control tool is discussed. Base case study is dependent on two scenario's. First

scenario, contains a report which focuses on implementation of accounting techniques for the

business (Otley and Emmanuel, 2013). In second scenario, resolution techniques for financial

problem or issues has been explained through report to General manager.

The main objective of this report is to discuss on techniques management accounting

which is marginal costs and absorption costs and profit analysis. Making of Income statement at

the end of the year with two different techniques will shows basic difference between Marginal

costing and also Absorption costing.

TASK 1

P1 Concept of management accounting and their kinds to company

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report consists of concept of management accounting system, its different types which is

required for a company are also being discussed. Some of its different types are Traditional,

Lean, Throughput and Transfer accounting. This report is based on explaining the features of

management accounting system, to help management in understanding how it can support top

In management accounting, managers uses regulations data accounting to get support in

decision-making process of an organisation (Banerjee, 2010). Management accounting is a

provision of financial and non-financial decision-making informations to top management.

According to Chenhall, 2012 “Management accounting is a process that contains involvement in

decision making, allocation planning and performance management systems and it also provides

proficiency in financial reporting to support management in implementing organisation's

strategies”.

Bizdaq was established in 2015, it is in Business sales sectors. Company gives a

marketplace for sale. It's annual turnover is £100,000.

This assignment consists of various types of management accounting systems and their

methods. To enlighten the features of budget control, advantages and disadvantages of various

types of budgetary control tool is discussed. Base case study is dependent on two scenario's. First

scenario, contains a report which focuses on implementation of accounting techniques for the

business (Otley and Emmanuel, 2013). In second scenario, resolution techniques for financial

problem or issues has been explained through report to General manager.

The main objective of this report is to discuss on techniques management accounting

which is marginal costs and absorption costs and profit analysis. Making of Income statement at

the end of the year with two different techniques will shows basic difference between Marginal

costing and also Absorption costing.

TASK 1

P1 Concept of management accounting and their kinds to company

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting system

This report consists of concept of management accounting system, its different types which is

required for a company are also being discussed. Some of its different types are Traditional,

Lean, Throughput and Transfer accounting. This report is based on explaining the features of

management accounting system, to help management in understanding how it can support top

management in decision-making process.

Management Accounting System:

This accounting system consists of all provisions that gives essential informations to a

managers. The data of these systems supports top management in finding resolutions for

financial issues like failure in budgeting, overestimation and underestimation of funds, waste of

resources, etc. (Bebbington, Unerman and O'Dwyer, 2014). The main stakeholders of

management accounting systems are Investors, Creditors, operational managers and company's

business analysts.

Below is the diagram of different types of Management accounting system:

Explanation of all these types of Management accounting system has been done below:

Traditional Accounting: In this accounting method, data's related to costs is recorded.

Traditional Transfer

ThroughputLean

Illustration 1: Management accounting

Management Accounting System:

This accounting system consists of all provisions that gives essential informations to a

managers. The data of these systems supports top management in finding resolutions for

financial issues like failure in budgeting, overestimation and underestimation of funds, waste of

resources, etc. (Bebbington, Unerman and O'Dwyer, 2014). The main stakeholders of

management accounting systems are Investors, Creditors, operational managers and company's

business analysts.

Below is the diagram of different types of Management accounting system:

Explanation of all these types of Management accounting system has been done below:

Traditional Accounting: In this accounting method, data's related to costs is recorded.

Traditional Transfer

ThroughputLean

Illustration 1: Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

These data's are recorded by applying job order and process costing methods. Big

projects are normally refers job order costing methods because in individual projects,

recording of costs through this method becomes easy (Bennett, Schaltegger and

Zvezdov, 2013). On the other hand, process costing method is used by those companies

which are into production of homogeneous products. Bizdaq is required Traditional

accounting because it could determine how to allocate its funds into different

departments after application of this tool. For instance, this method will makes easy in

recording data's related to purchase, supply and selling department separately which

would support company in deciding proper allocation of funds into these departments.

Lean Accounting: This accounting system, applies new techniques to reduce costs of

production. It mainly consists of all steps which eliminates wastes at each process

through which company could manage to control its costs (Bodie, Kane and Marcus,

2014). This accounting system gives informations to accounting managers to support

them in decision-making.

Bizdaq could use this method, in reducing costs of production and in eliminating

wastes. Company has Cost of goods sold of more than 90%, which indicates that there are lots

of fund consumes in this activity. Reason may be unnecessary use of resources which raises the

overall cost of production (Bodie, 2013). Therefore, company could use this method in

minimizing costs and elimination of wastage through tracking the operational process.

Throughput accounting: This type of accounting is neither cost accounting nor costing

because it's only considers cash based transactions. It doesn't distributes all types of

costs like variable and fixed costs to products or services made by a company.

Throughput accounting is a technique which uses performance measure in Theory of

Constraints.

Bizdaq would be benefited from the application of these techniques because

Throughput accounting could support company in maximising profits, cost cutting and reducing

expenses. This accounting methods usually focused on generating more throughput from

operational process of a company.

Transfer pricing methods: This method also known as traditional transactions

methods, in this technique price of a company is compared with third-party prices. In

managerial accounting, transfer price supports in knowing price at which upstream

projects are normally refers job order costing methods because in individual projects,

recording of costs through this method becomes easy (Bennett, Schaltegger and

Zvezdov, 2013). On the other hand, process costing method is used by those companies

which are into production of homogeneous products. Bizdaq is required Traditional

accounting because it could determine how to allocate its funds into different

departments after application of this tool. For instance, this method will makes easy in

recording data's related to purchase, supply and selling department separately which

would support company in deciding proper allocation of funds into these departments.

Lean Accounting: This accounting system, applies new techniques to reduce costs of

production. It mainly consists of all steps which eliminates wastes at each process

through which company could manage to control its costs (Bodie, Kane and Marcus,

2014). This accounting system gives informations to accounting managers to support

them in decision-making.

Bizdaq could use this method, in reducing costs of production and in eliminating

wastes. Company has Cost of goods sold of more than 90%, which indicates that there are lots

of fund consumes in this activity. Reason may be unnecessary use of resources which raises the

overall cost of production (Bodie, 2013). Therefore, company could use this method in

minimizing costs and elimination of wastage through tracking the operational process.

Throughput accounting: This type of accounting is neither cost accounting nor costing

because it's only considers cash based transactions. It doesn't distributes all types of

costs like variable and fixed costs to products or services made by a company.

Throughput accounting is a technique which uses performance measure in Theory of

Constraints.

Bizdaq would be benefited from the application of these techniques because

Throughput accounting could support company in maximising profits, cost cutting and reducing

expenses. This accounting methods usually focused on generating more throughput from

operational process of a company.

Transfer pricing methods: This method also known as traditional transactions

methods, in this technique price of a company is compared with third-party prices. In

managerial accounting, transfer price supports in knowing price at which upstream

division of a company sold goods to downstream divisions. These goods and services

are labour, components and equipments used in production process of a company. It

could be identified through market-based, cost-based or negotiated method.

It could help Bizdaq, determining costs and revenues among various divisions and

it also affects performance evaluation of these divisions. It is essentially required at the time of

selling of products across international borders.

Apart from this there are other types of Management Accounting systems, which is discussed

below:

Cost Accounting System: A cost accounting system (also called product cost system or

cost system) is a framework used by companies to estimate the cost of their products for

profitability analysis, inventory evaluation and cost control.

Job Costing: This is defined as a method of recording the cost of a manufacturing job

rather than the process. With a job-cost system, a project manager or accountant can

track the cost of every job, maintains data which is often more relevant to the operation

of the business.

Inventory: The list includes raw materials, methodology, and finished goods, which a

company receives for its production processes or for sale to customers (Lukka and

Modell, 2010). Inventory is considered to be a property, so the accountant must use a

valid method to specify the costs for the inventory.

Price Optimization: Price optimization models are mathematical programs that

calculate how demand differs at different price levels and then combines the data with

information about prices and inventory levels, from which prices can be recommended,

which in profit Will bring improvement.

P2 Report to the General manager concerning to methods of management accounting reports

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting report

This report consists different methods of reporting in the management accounting. Uses of these

various reports to help Bizdaq in decision-making process is also mentioned.

Management accounting report

are labour, components and equipments used in production process of a company. It

could be identified through market-based, cost-based or negotiated method.

It could help Bizdaq, determining costs and revenues among various divisions and

it also affects performance evaluation of these divisions. It is essentially required at the time of

selling of products across international borders.

Apart from this there are other types of Management Accounting systems, which is discussed

below:

Cost Accounting System: A cost accounting system (also called product cost system or

cost system) is a framework used by companies to estimate the cost of their products for

profitability analysis, inventory evaluation and cost control.

Job Costing: This is defined as a method of recording the cost of a manufacturing job

rather than the process. With a job-cost system, a project manager or accountant can

track the cost of every job, maintains data which is often more relevant to the operation

of the business.

Inventory: The list includes raw materials, methodology, and finished goods, which a

company receives for its production processes or for sale to customers (Lukka and

Modell, 2010). Inventory is considered to be a property, so the accountant must use a

valid method to specify the costs for the inventory.

Price Optimization: Price optimization models are mathematical programs that

calculate how demand differs at different price levels and then combines the data with

information about prices and inventory levels, from which prices can be recommended,

which in profit Will bring improvement.

P2 Report to the General manager concerning to methods of management accounting reports

From: Management accounting officer

To: General manager of Bizdaq

Sub: Management accounting report

This report consists different methods of reporting in the management accounting. Uses of these

various reports to help Bizdaq in decision-making process is also mentioned.

Management accounting report

These reports of management accounting supports business in analysing company's

performance (Boyns and Edwards, 2013). These type of reports usually generated at the end of

every year. Top management usually requires it to know their financial status in the market. It

helps managers in identifying their company's performance over past years. Managers requires

these types of reports during every week, month, quarterly, half-yearly and yearly.

Management accounting reports are very important for Bizdaq because it supports business

in forecasting the future, Make or buy decisions, understanding the variance in performance of

labour, materials and assets and analysing necessary return rate to run business.

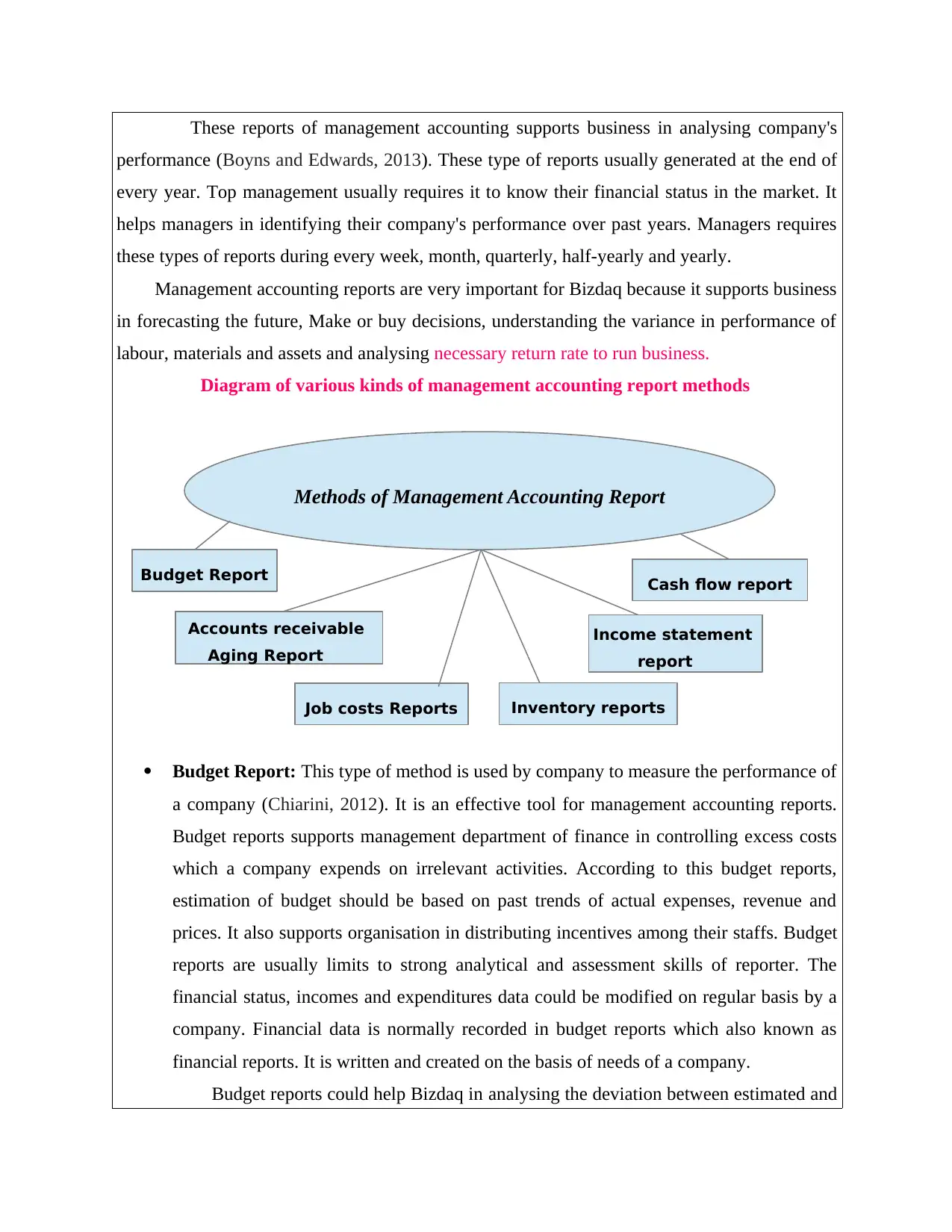

Diagram of various kinds of management accounting report methods

Budget Report: This type of method is used by company to measure the performance of

a company (Chiarini, 2012). It is an effective tool for management accounting reports.

Budget reports supports management department of finance in controlling excess costs

which a company expends on irrelevant activities. According to this budget reports,

estimation of budget should be based on past trends of actual expenses, revenue and

prices. It also supports organisation in distributing incentives among their staffs. Budget

reports are usually limits to strong analytical and assessment skills of reporter. The

financial status, incomes and expenditures data could be modified on regular basis by a

company. Financial data is normally recorded in budget reports which also known as

financial reports. It is written and created on the basis of needs of a company.

Budget reports could help Bizdaq in analysing the deviation between estimated and

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow report

Budget Report

Inventory reports

performance (Boyns and Edwards, 2013). These type of reports usually generated at the end of

every year. Top management usually requires it to know their financial status in the market. It

helps managers in identifying their company's performance over past years. Managers requires

these types of reports during every week, month, quarterly, half-yearly and yearly.

Management accounting reports are very important for Bizdaq because it supports business

in forecasting the future, Make or buy decisions, understanding the variance in performance of

labour, materials and assets and analysing necessary return rate to run business.

Diagram of various kinds of management accounting report methods

Budget Report: This type of method is used by company to measure the performance of

a company (Chiarini, 2012). It is an effective tool for management accounting reports.

Budget reports supports management department of finance in controlling excess costs

which a company expends on irrelevant activities. According to this budget reports,

estimation of budget should be based on past trends of actual expenses, revenue and

prices. It also supports organisation in distributing incentives among their staffs. Budget

reports are usually limits to strong analytical and assessment skills of reporter. The

financial status, incomes and expenditures data could be modified on regular basis by a

company. Financial data is normally recorded in budget reports which also known as

financial reports. It is written and created on the basis of needs of a company.

Budget reports could help Bizdaq in analysing the deviation between estimated and

Methods of Management Accounting Report

Accounts receivable

Aging Report

Job costs Reports

Income statement

report

Cash flow report

Budget Report

Inventory reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

actual figures. More variance reflects inefficiency of a company in managing its price where

minimum discrepancy implies which an organisation use efficiently utilising its all resources

without debility resources (Ward, 2012). For instance, let's assume Bizdaq's budgeted sales is

450 units while its actual sales if 600 units. It is under budgeted sales, because actual sales is

more than budgeted one. This situation might impact business in facing difficulties in fulfilling

the demands on time.

Accounts receivable aging report: Accounts receivable aging is a periodic report that

receives accounts of a company from time to time, which is an invoice outstanding. It is

used as a gauge to determine the financial health of the company's customers (DRURY,

2013). If the account receives an eligible age, indicating that receipts of an organistaion

are being gathered very slowly than the unsual, it is warning sign from which business

can be slow down or firm is vulnerable to its sales related practices Is picking up.

Bizdaq would know about the tenure taken by its debtors to pay back to company.

For example any increase in debtors from previous year, can affect companies efficiency of

working capital (Baldvinsdottir, Mitchell and Nørrekli, 2010). Due to less cash available to a

business. Hence, this report could be applied to control excess obstruction of cash among

debtors.

Job costs Reports: To support the cost of a job for an accounting system, it should be

assigned job numbers and different items of revenue. Job can be explained that special

project for consumer or unit of produced goods of units of similar kind which are

developed together. Reports related to job costing consists of collection of the costs of

materials, labour, and overhead for a specific job. Job Cost Report is also used to

examine expenses of work-in-progress task to eliminate wastes before completing it.

With the application of this method, Bizdaq might determine which activity

consumes how much cash. For instance, company has production, selling and distribution costs.

These different costs would be generate job costing reports for the Bizdaq.

Inventory and manufacturing reports: Inventory reports inventory supervisors help in

an inventory management, tracking the movement of an inventory inside the warehouse

as well as inventory of various categories,like for an instance hold inventory and

visibility (Håkansson, Kraus and Lind, 2010). These types of reports can be used to

categorize list which is based on the cost. In addition to this production reports analysis,

minimum discrepancy implies which an organisation use efficiently utilising its all resources

without debility resources (Ward, 2012). For instance, let's assume Bizdaq's budgeted sales is

450 units while its actual sales if 600 units. It is under budgeted sales, because actual sales is

more than budgeted one. This situation might impact business in facing difficulties in fulfilling

the demands on time.

Accounts receivable aging report: Accounts receivable aging is a periodic report that

receives accounts of a company from time to time, which is an invoice outstanding. It is

used as a gauge to determine the financial health of the company's customers (DRURY,

2013). If the account receives an eligible age, indicating that receipts of an organistaion

are being gathered very slowly than the unsual, it is warning sign from which business

can be slow down or firm is vulnerable to its sales related practices Is picking up.

Bizdaq would know about the tenure taken by its debtors to pay back to company.

For example any increase in debtors from previous year, can affect companies efficiency of

working capital (Baldvinsdottir, Mitchell and Nørrekli, 2010). Due to less cash available to a

business. Hence, this report could be applied to control excess obstruction of cash among

debtors.

Job costs Reports: To support the cost of a job for an accounting system, it should be

assigned job numbers and different items of revenue. Job can be explained that special

project for consumer or unit of produced goods of units of similar kind which are

developed together. Reports related to job costing consists of collection of the costs of

materials, labour, and overhead for a specific job. Job Cost Report is also used to

examine expenses of work-in-progress task to eliminate wastes before completing it.

With the application of this method, Bizdaq might determine which activity

consumes how much cash. For instance, company has production, selling and distribution costs.

These different costs would be generate job costing reports for the Bizdaq.

Inventory and manufacturing reports: Inventory reports inventory supervisors help in

an inventory management, tracking the movement of an inventory inside the warehouse

as well as inventory of various categories,like for an instance hold inventory and

visibility (Håkansson, Kraus and Lind, 2010). These types of reports can be used to

categorize list which is based on the cost. In addition to this production reports analysis,

how much manufacturing is done and how much has to produced during a year. Both

reports are interlinked to each other.

Application of inventory and manufacturing reports would help Bizdaq in identifying

opportunities for consolidation. This report could provide cycle count variance informations to a

company on daily, monthly or weekly basis. SKUs or Stock Keeping Units report provides

informations about the locations which are still remained unused by the company in various

time buckets.

Income statement report: These types of management accounting reports is considered

by management to identify how much profit is earned by a company during financial

year. These profits are calculated by deducting all types of taxes and expenses from it. It

helps company in measuring performance of it by comparing form previous years

performance.

Bizdaq could calculate its financial profit or net earnings during a year with Income

statement reports. It could also determine how many expenses are outstanding by the company

and how much it has paid in advance to its suppliers or landlords for rents and prepaid

payments.

Cash Flow statement report: In management accounting, a cash flow statement, also

known as the statement of cash flow, it is a financial statement that shows how changes

in the balance sheet account and income affects cash and cash equivalents (Hopwood,

Unerman and Fries, 2010). It breaks the analysis under operating, investment and

analysis Financial activities.

Bizdaq could apply this method to find liquidity of its business through analysing cash

flow statement reports (Simons, 2013). For example, Company's net profit is £9300 calculated

through Marginal costing, which is accrued which means it is not actually earned by business in

exchange of cash. So, Cash flow reports supports in identifying how much actual cash is left

with the company.

Conclusion

On the basis of above report, it can be concluded that, Bizdaq requires to prepare all

different methods of reporting because different functions of its business requires different

methods of reporting. Such as Cash related activities requires Inventory management functions,

cash flow reports requires Manufacturing and Inventory methods of reporting. Cash flow

reports are interlinked to each other.

Application of inventory and manufacturing reports would help Bizdaq in identifying

opportunities for consolidation. This report could provide cycle count variance informations to a

company on daily, monthly or weekly basis. SKUs or Stock Keeping Units report provides

informations about the locations which are still remained unused by the company in various

time buckets.

Income statement report: These types of management accounting reports is considered

by management to identify how much profit is earned by a company during financial

year. These profits are calculated by deducting all types of taxes and expenses from it. It

helps company in measuring performance of it by comparing form previous years

performance.

Bizdaq could calculate its financial profit or net earnings during a year with Income

statement reports. It could also determine how many expenses are outstanding by the company

and how much it has paid in advance to its suppliers or landlords for rents and prepaid

payments.

Cash Flow statement report: In management accounting, a cash flow statement, also

known as the statement of cash flow, it is a financial statement that shows how changes

in the balance sheet account and income affects cash and cash equivalents (Hopwood,

Unerman and Fries, 2010). It breaks the analysis under operating, investment and

analysis Financial activities.

Bizdaq could apply this method to find liquidity of its business through analysing cash

flow statement reports (Simons, 2013). For example, Company's net profit is £9300 calculated

through Marginal costing, which is accrued which means it is not actually earned by business in

exchange of cash. So, Cash flow reports supports in identifying how much actual cash is left

with the company.

Conclusion

On the basis of above report, it can be concluded that, Bizdaq requires to prepare all

different methods of reporting because different functions of its business requires different

methods of reporting. Such as Cash related activities requires Inventory management functions,

cash flow reports requires Manufacturing and Inventory methods of reporting. Cash flow

statement report is useful to analyse solvency of a business. Income statement reports supports

business in determining how much profits left with an organisation to re-invest in order to

elaboration activities as well as maintenance of business. Budget reports are the forecasts which

is based on the estimation. It requires for a Bizdaq to allocate its funds among different

department accordingly.

TASK 2

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:

Marginal Costing: Increase or decrease the total cost of production to make an

additional unit of an item (Islam and Hu, 2012). The calculation is done in those conditions

where breakaway has reached point: the prices already determined by the previously

manufactured goods have already been contained and only the cost of direct variable costs is to

be accounted for.

Marginal cost, coupled with cost of labour and material costs, plus the estimated portion

of fixed cost such as administration overheads and sales expenses. In the companies where the

average cost is quite stable, the marginal cost is usually equal to the average cost. However,

industries require heavy capital investments like auto-mobile plant, airline, mine and higher

average costs, it is relatively low.

Absorption Costing: In this type of income statement method, all types of

manufacturing costs absorbed or socked by the units produced in operational process of a

company (Kokubu and Kitada, 2015). It can be said that cost of finished goods in inventory is

added to direct materials, direct labour and both variable & fixed manufacturing overheads. In

this method of costing, fixed manufacturing overheads are not divided into the products which is

already manufactured.

Absorption costing is necessary for external financial and income tax reporting. For

example, lets assume that Bizdaq's employees of two departments (Selling and production) eat

their lunch in company's canteen. The cost of canteen is bared by company itself. Hence, the cost

of canteen is not a direct cost but it supports both departments to run a business. Therefore,

absorption methods suggests to distribute canteen expenses among these two departments to get

actual value.

business in determining how much profits left with an organisation to re-invest in order to

elaboration activities as well as maintenance of business. Budget reports are the forecasts which

is based on the estimation. It requires for a Bizdaq to allocate its funds among different

department accordingly.

TASK 2

P3 Difference between Marginal costing and Absorption costing and calculation of Income

statement through these methods:

Marginal Costing: Increase or decrease the total cost of production to make an

additional unit of an item (Islam and Hu, 2012). The calculation is done in those conditions

where breakaway has reached point: the prices already determined by the previously

manufactured goods have already been contained and only the cost of direct variable costs is to

be accounted for.

Marginal cost, coupled with cost of labour and material costs, plus the estimated portion

of fixed cost such as administration overheads and sales expenses. In the companies where the

average cost is quite stable, the marginal cost is usually equal to the average cost. However,

industries require heavy capital investments like auto-mobile plant, airline, mine and higher

average costs, it is relatively low.

Absorption Costing: In this type of income statement method, all types of

manufacturing costs absorbed or socked by the units produced in operational process of a

company (Kokubu and Kitada, 2015). It can be said that cost of finished goods in inventory is

added to direct materials, direct labour and both variable & fixed manufacturing overheads. In

this method of costing, fixed manufacturing overheads are not divided into the products which is

already manufactured.

Absorption costing is necessary for external financial and income tax reporting. For

example, lets assume that Bizdaq's employees of two departments (Selling and production) eat

their lunch in company's canteen. The cost of canteen is bared by company itself. Hence, the cost

of canteen is not a direct cost but it supports both departments to run a business. Therefore,

absorption methods suggests to distribute canteen expenses among these two departments to get

actual value.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

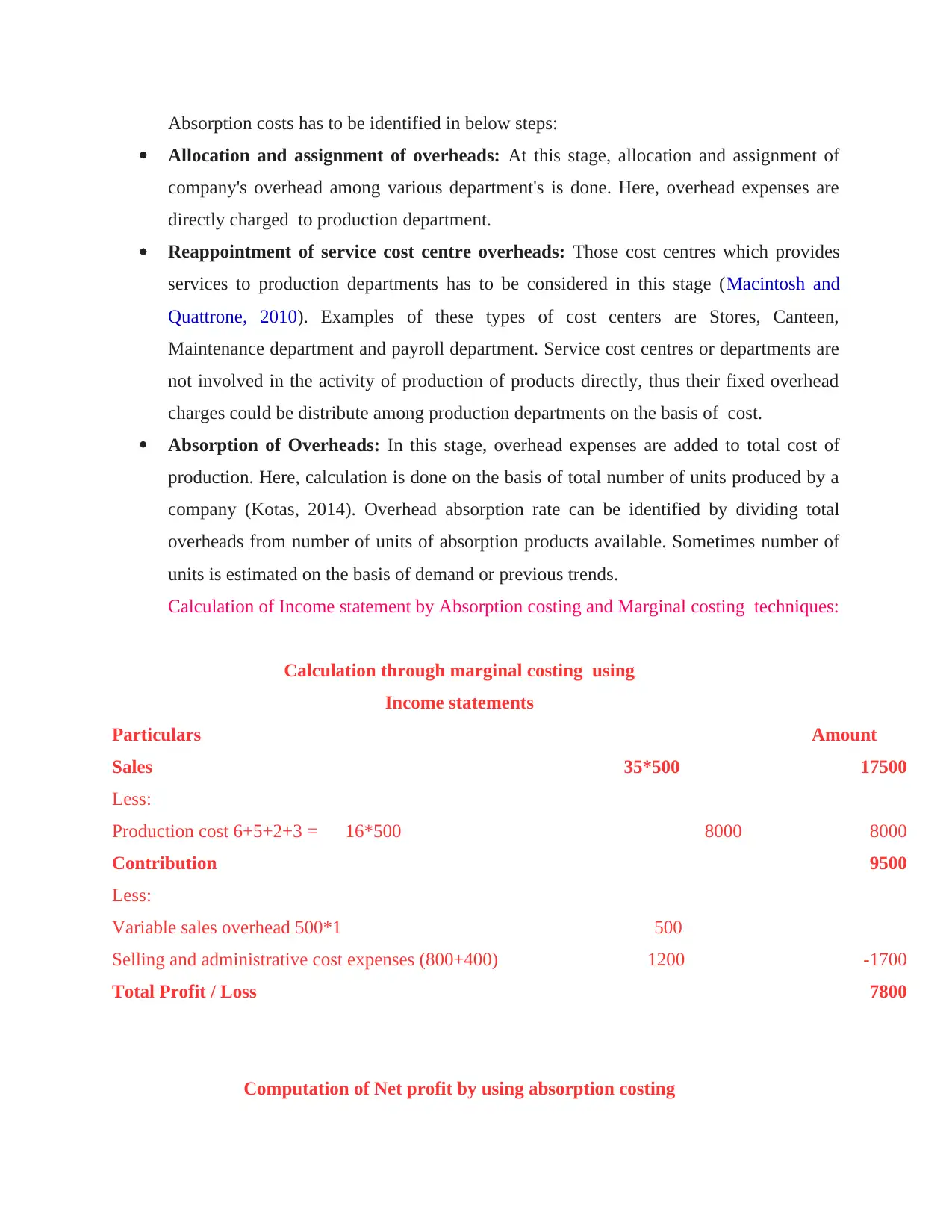

Absorption costs has to be identified in below steps:

Allocation and assignment of overheads: At this stage, allocation and assignment of

company's overhead among various department's is done. Here, overhead expenses are

directly charged to production department.

Reappointment of service cost centre overheads: Those cost centres which provides

services to production departments has to be considered in this stage (Macintosh and

Quattrone, 2010). Examples of these types of cost centers are Stores, Canteen,

Maintenance department and payroll department. Service cost centres or departments are

not involved in the activity of production of products directly, thus their fixed overhead

charges could be distribute among production departments on the basis of cost.

Absorption of Overheads: In this stage, overhead expenses are added to total cost of

production. Here, calculation is done on the basis of total number of units produced by a

company (Kotas, 2014). Overhead absorption rate can be identified by dividing total

overheads from number of units of absorption products available. Sometimes number of

units is estimated on the basis of demand or previous trends.

Calculation of Income statement by Absorption costing and Marginal costing techniques:

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Contribution 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Computation of Net profit by using absorption costing

Allocation and assignment of overheads: At this stage, allocation and assignment of

company's overhead among various department's is done. Here, overhead expenses are

directly charged to production department.

Reappointment of service cost centre overheads: Those cost centres which provides

services to production departments has to be considered in this stage (Macintosh and

Quattrone, 2010). Examples of these types of cost centers are Stores, Canteen,

Maintenance department and payroll department. Service cost centres or departments are

not involved in the activity of production of products directly, thus their fixed overhead

charges could be distribute among production departments on the basis of cost.

Absorption of Overheads: In this stage, overhead expenses are added to total cost of

production. Here, calculation is done on the basis of total number of units produced by a

company (Kotas, 2014). Overhead absorption rate can be identified by dividing total

overheads from number of units of absorption products available. Sometimes number of

units is estimated on the basis of demand or previous trends.

Calculation of Income statement by Absorption costing and Marginal costing techniques:

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000 8000

Contribution 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Computation of Net profit by using absorption costing

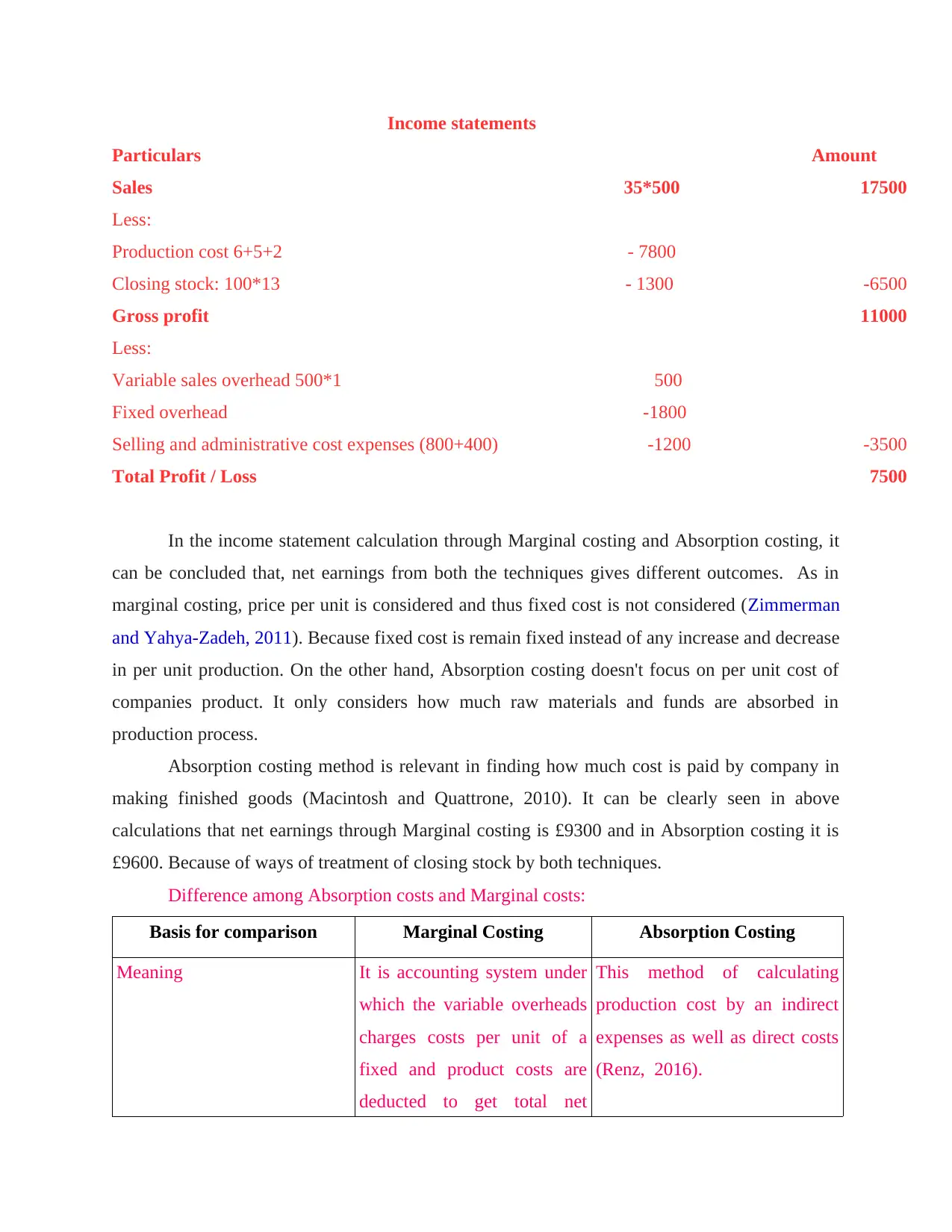

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Gross profit 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

In the income statement calculation through Marginal costing and Absorption costing, it

can be concluded that, net earnings from both the techniques gives different outcomes. As in

marginal costing, price per unit is considered and thus fixed cost is not considered (Zimmerman

and Yahya-Zadeh, 2011). Because fixed cost is remain fixed instead of any increase and decrease

in per unit production. On the other hand, Absorption costing doesn't focus on per unit cost of

companies product. It only considers how much raw materials and funds are absorbed in

production process.

Absorption costing method is relevant in finding how much cost is paid by company in

making finished goods (Macintosh and Quattrone, 2010). It can be clearly seen in above

calculations that net earnings through Marginal costing is £9300 and in Absorption costing it is

£9600. Because of ways of treatment of closing stock by both techniques.

Difference among Absorption costs and Marginal costs:

Basis for comparison Marginal Costing Absorption Costing

Meaning It is accounting system under

which the variable overheads

charges costs per unit of a

fixed and product costs are

deducted to get total net

This method of calculating

production cost by an indirect

expenses as well as direct costs

(Renz, 2016).

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Gross profit 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

In the income statement calculation through Marginal costing and Absorption costing, it

can be concluded that, net earnings from both the techniques gives different outcomes. As in

marginal costing, price per unit is considered and thus fixed cost is not considered (Zimmerman

and Yahya-Zadeh, 2011). Because fixed cost is remain fixed instead of any increase and decrease

in per unit production. On the other hand, Absorption costing doesn't focus on per unit cost of

companies product. It only considers how much raw materials and funds are absorbed in

production process.

Absorption costing method is relevant in finding how much cost is paid by company in

making finished goods (Macintosh and Quattrone, 2010). It can be clearly seen in above

calculations that net earnings through Marginal costing is £9300 and in Absorption costing it is

£9600. Because of ways of treatment of closing stock by both techniques.

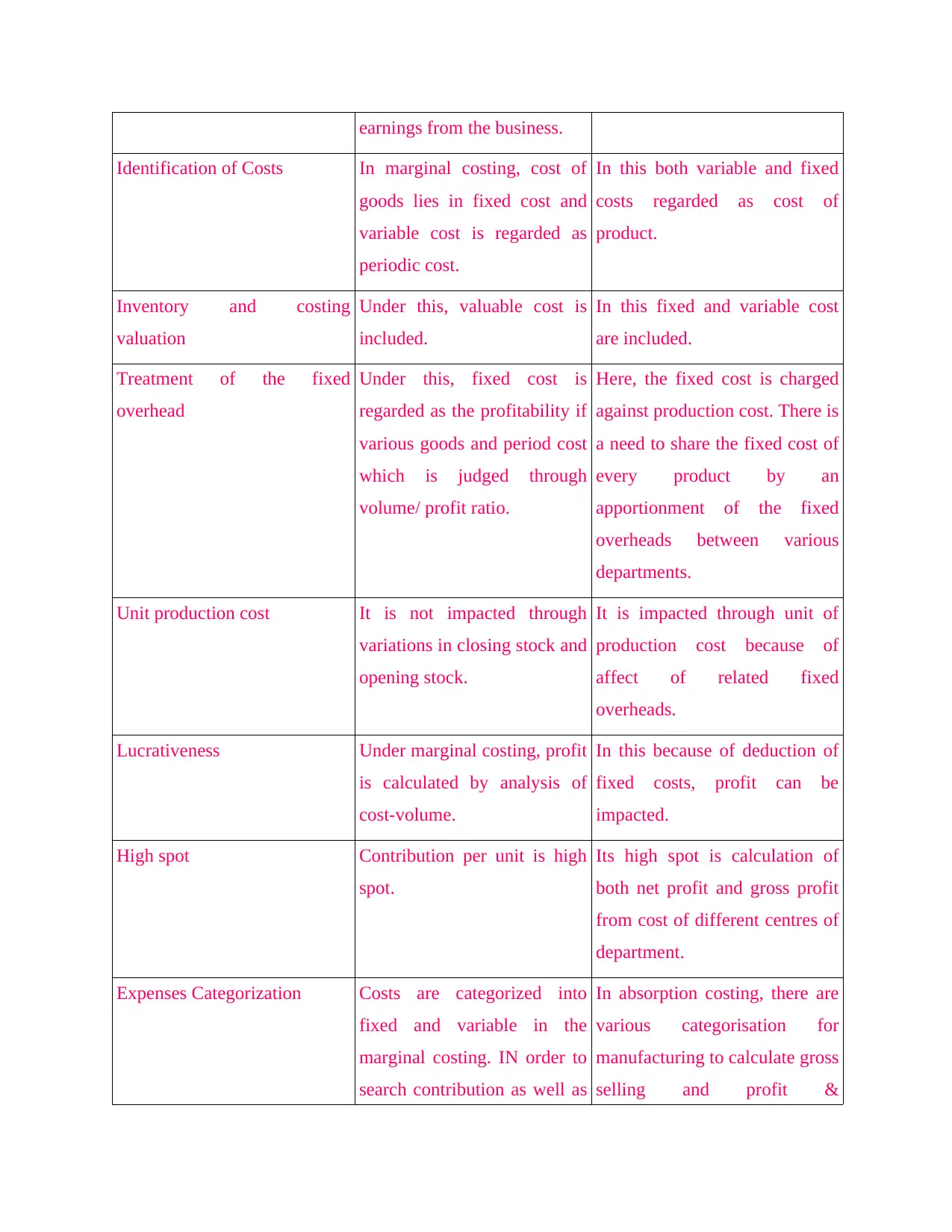

Difference among Absorption costs and Marginal costs:

Basis for comparison Marginal Costing Absorption Costing

Meaning It is accounting system under

which the variable overheads

charges costs per unit of a

fixed and product costs are

deducted to get total net

This method of calculating

production cost by an indirect

expenses as well as direct costs

(Renz, 2016).

earnings from the business.

Identification of Costs In marginal costing, cost of

goods lies in fixed cost and

variable cost is regarded as

periodic cost.

In this both variable and fixed

costs regarded as cost of

product.

Inventory and costing

valuation

Under this, valuable cost is

included.

In this fixed and variable cost

are included.

Treatment of the fixed

overhead

Under this, fixed cost is

regarded as the profitability if

various goods and period cost

which is judged through

volume/ profit ratio.

Here, the fixed cost is charged

against production cost. There is

a need to share the fixed cost of

every product by an

apportionment of the fixed

overheads between various

departments.

Unit production cost It is not impacted through

variations in closing stock and

opening stock.

It is impacted through unit of

production cost because of

affect of related fixed

overheads.

Lucrativeness Under marginal costing, profit

is calculated by analysis of

cost-volume.

In this because of deduction of

fixed costs, profit can be

impacted.

High spot Contribution per unit is high

spot.

Its high spot is calculation of

both net profit and gross profit

from cost of different centres of

department.

Expenses Categorization Costs are categorized into

fixed and variable in the

marginal costing. IN order to

search contribution as well as

In absorption costing, there are

various categorisation for

manufacturing to calculate gross

selling and profit &

Identification of Costs In marginal costing, cost of

goods lies in fixed cost and

variable cost is regarded as

periodic cost.

In this both variable and fixed

costs regarded as cost of

product.

Inventory and costing

valuation

Under this, valuable cost is

included.

In this fixed and variable cost

are included.

Treatment of the fixed

overhead

Under this, fixed cost is

regarded as the profitability if

various goods and period cost

which is judged through

volume/ profit ratio.

Here, the fixed cost is charged

against production cost. There is

a need to share the fixed cost of

every product by an

apportionment of the fixed

overheads between various

departments.

Unit production cost It is not impacted through

variations in closing stock and

opening stock.

It is impacted through unit of

production cost because of

affect of related fixed

overheads.

Lucrativeness Under marginal costing, profit

is calculated by analysis of

cost-volume.

In this because of deduction of

fixed costs, profit can be

impacted.

High spot Contribution per unit is high

spot.

Its high spot is calculation of

both net profit and gross profit

from cost of different centres of

department.

Expenses Categorization Costs are categorized into

fixed and variable in the

marginal costing. IN order to

search contribution as well as

In absorption costing, there are

various categorisation for

manufacturing to calculate gross

selling and profit &

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

net profit both separately. administration costs to know net

profit.

Cost Collection Cost is gathered through

outlining total contribution of

every goods.

Cost is gathered through

customary method in order to

show data cost.

Hence, from the above differentiation it can be concluded that, Marginal costing

considers two types of costs viz. Variable and fixed costs but in absorption costing method, it

considers production and selling & distribution costs which means it doesn't show fixed costs

separately.

TASK 3

P4 Advantages and disadvantage of various kinds of planning tools for the budgetary control

From: Management accounting officer

To: General manager of Bizdaq

Sub: Kinds of accounting tools for budgetary control

This report consists of all advantages and disadvantage of using various types of planning tools

for budgetary control. It would highlight what factors to be considered while choosing particular

tools for making budgets.

Budgetary control

Management control system under which real expenditure and income both are compared

with planned expenditure and income, to see whether schemes are being followed and if those

plans have to be changed to make profit (Shields, 2015). Hence, Budget control shows how

effectively an employer used budget to monitor and control costs and operations during a

financial period. Managemnt of budgetary control have a determining process of performance

and financial goals with budget and comparing the actual results and adjusting performance,

when ever it is required.

profit.

Cost Collection Cost is gathered through

outlining total contribution of

every goods.

Cost is gathered through

customary method in order to

show data cost.

Hence, from the above differentiation it can be concluded that, Marginal costing

considers two types of costs viz. Variable and fixed costs but in absorption costing method, it

considers production and selling & distribution costs which means it doesn't show fixed costs

separately.

TASK 3

P4 Advantages and disadvantage of various kinds of planning tools for the budgetary control

From: Management accounting officer

To: General manager of Bizdaq

Sub: Kinds of accounting tools for budgetary control

This report consists of all advantages and disadvantage of using various types of planning tools

for budgetary control. It would highlight what factors to be considered while choosing particular

tools for making budgets.

Budgetary control

Management control system under which real expenditure and income both are compared

with planned expenditure and income, to see whether schemes are being followed and if those

plans have to be changed to make profit (Shields, 2015). Hence, Budget control shows how

effectively an employer used budget to monitor and control costs and operations during a

financial period. Managemnt of budgetary control have a determining process of performance

and financial goals with budget and comparing the actual results and adjusting performance,

when ever it is required.

(Source: Tools4Management)

There are various kinds of tools which are used by process of budgetary control such as

Financial budgets, Operating budgets, Non- monetary budgets and Fixed and Variable Budgets.

It is explained with the diagram below:

Types planning tools of Budgetary

control

Financial

Budgets

Non-Monetary

Budgets

Operating

Budgets

Fixed and variable

budgets

There are various kinds of tools which are used by process of budgetary control such as

Financial budgets, Operating budgets, Non- monetary budgets and Fixed and Variable Budgets.

It is explained with the diagram below:

Types planning tools of Budgetary

control

Financial

Budgets

Non-Monetary

Budgets

Operating

Budgets

Fixed and variable

budgets

Financial Budgets: These budgets supports companies in allocating its funds on the

basis of financial budgets. Usually these budgets contains various sources and

distribution of cash flows to run business activities. It could help Culina Group in

determining past trends to estimate future trends and budgets for a company.

Advantages: It helps company in knowing its future cash inflows and outflows. It also

supports companies in knowing where to allocate its funds to benefit a business in long run.

Disadvantages: This method estimates future which is uncertain. Floods, strike, changes

in government, regulations and policies can't be predict in advance.

For an example- Master budget, Zero base budgeting.

Operating Budgets: This tool of budget controlling, It supports company in allocation

of funds among its operational process like work-in-progress, working capital,

Assembling, etc. Operating budgets are of three types which is Sales budget, Expense

budget and Project budgets (Otley and Emmanuel, 2013).

Advantages

Company could meet future product demands through this tool. It is also an effective in

facilitating business in a smooth way. It supports business in allocating of its funds.

Disadvantages

It is time consuming because company requires all most a year to make a plan. It is also

requires lots of expertise to make such a plan. Culina Group requires lots of money also to

implement such a plan into business.

Eg- Sales, Purchase, Production etc.

Non-Monetary Budgets: These budgets consists of non-financial sales or revenue

expenses. Company requires a non-monetary budget to track those activities which don't

have any affect on cash, but after expiry of machines value, it can affect the operation of

the business after depreciation.

Advantage:

These budgets are similar to planning as plan and budgets both works on future

estimations. It helps in knowing the strength and weakness of companies financial status.

Disadvantages:

These type of budget is only based future estimation for making budgets. It fully ignores

Innovation, which is an important part of every organisation. It is the major disadvantage of this

basis of financial budgets. Usually these budgets contains various sources and

distribution of cash flows to run business activities. It could help Culina Group in

determining past trends to estimate future trends and budgets for a company.

Advantages: It helps company in knowing its future cash inflows and outflows. It also

supports companies in knowing where to allocate its funds to benefit a business in long run.

Disadvantages: This method estimates future which is uncertain. Floods, strike, changes

in government, regulations and policies can't be predict in advance.

For an example- Master budget, Zero base budgeting.

Operating Budgets: This tool of budget controlling, It supports company in allocation

of funds among its operational process like work-in-progress, working capital,

Assembling, etc. Operating budgets are of three types which is Sales budget, Expense

budget and Project budgets (Otley and Emmanuel, 2013).

Advantages

Company could meet future product demands through this tool. It is also an effective in

facilitating business in a smooth way. It supports business in allocating of its funds.

Disadvantages

It is time consuming because company requires all most a year to make a plan. It is also

requires lots of expertise to make such a plan. Culina Group requires lots of money also to

implement such a plan into business.

Eg- Sales, Purchase, Production etc.

Non-Monetary Budgets: These budgets consists of non-financial sales or revenue

expenses. Company requires a non-monetary budget to track those activities which don't

have any affect on cash, but after expiry of machines value, it can affect the operation of

the business after depreciation.

Advantage:

These budgets are similar to planning as plan and budgets both works on future

estimations. It helps in knowing the strength and weakness of companies financial status.

Disadvantages:

These type of budget is only based future estimation for making budgets. It fully ignores

Innovation, which is an important part of every organisation. It is the major disadvantage of this

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

type of budget.

Fixed and variable budgets: Fixed budget are the future estimatation of business

expansion, change in organisational structures, etc. Fixed expenses are permanent in

nature and it is not affected by any increase or decrease in production of units (Ward,

2012).

Advantage:

Fixed and variable budgets helps in identifying cost per unit and Break even point of

production and sales, which is required by Bizdaq to gain profits.

Disadvantage:

This tools of budgetary-control are rigid in nature because changes in a plan which is

already made can't be change.

For an example- Office rent, insurance etc.

P5 Management accounting system use in solving financial problems

From: Management accounting officer

To: General manager of Bizdaq Group

Sub: Uses of Management Accounting System in solving financial issues

In this report, various problems related to financial category will be discussed. Focus will be on

different alternatives to solve these issues.

Management Accounting Tools

These tools helps management in assessing information of finance to solve issues of

company. Financial issues are all those factors which affects performance of a company

(Monden, 2011). Such as improper budgeting, Borrowing too much debts, Poor purchasing

decisions and error in investing decisions.

Management accounting tools would support Bizdaq in improve its sales revenues and

returns on its capital invested in various projects. In this process, previous data's of a company

helps it in creating a linear trend analysis on the past performance of the business. This linear

trends assists management in estimating future trends by applying regression methods and trend

analysis methods while preparing a budget for a company.

Below is the explanation of three techniques which is alternate solutions for financial

issues arises in a company:

Fixed and variable budgets: Fixed budget are the future estimatation of business

expansion, change in organisational structures, etc. Fixed expenses are permanent in

nature and it is not affected by any increase or decrease in production of units (Ward,

2012).

Advantage:

Fixed and variable budgets helps in identifying cost per unit and Break even point of

production and sales, which is required by Bizdaq to gain profits.

Disadvantage:

This tools of budgetary-control are rigid in nature because changes in a plan which is

already made can't be change.

For an example- Office rent, insurance etc.

P5 Management accounting system use in solving financial problems

From: Management accounting officer

To: General manager of Bizdaq Group

Sub: Uses of Management Accounting System in solving financial issues

In this report, various problems related to financial category will be discussed. Focus will be on

different alternatives to solve these issues.

Management Accounting Tools

These tools helps management in assessing information of finance to solve issues of

company. Financial issues are all those factors which affects performance of a company

(Monden, 2011). Such as improper budgeting, Borrowing too much debts, Poor purchasing

decisions and error in investing decisions.

Management accounting tools would support Bizdaq in improve its sales revenues and

returns on its capital invested in various projects. In this process, previous data's of a company

helps it in creating a linear trend analysis on the past performance of the business. This linear

trends assists management in estimating future trends by applying regression methods and trend

analysis methods while preparing a budget for a company.

Below is the explanation of three techniques which is alternate solutions for financial

issues arises in a company:

Key Performance Indicators (KPI): KPI could support Bizdaq in measuring

performance of its various resources such as inventories, labour, funds, assets, etc. It

measures the performance based on returns received by business after investing in

particular resources (McNeil, Freyand Embrechts, 2015). It could re-solve financial

issues like excess debts and non-performing of assets by application of KPI indicators to

eliminate these issues at beginning stage. Bizdaq could eliminate financial issues of

excess blockage of money in customers through reducing credit amount given to them.

For this company needs to identify whether it is profitable for a company to more sale

foods on credit or not.

Benchmarking: Here, company can measured its annual performance by comparing it

with previous years of different companies. For Example, let's assume Bizdaq's

competitors which is into same business size has more sales than the company. Hence,

company could take their sales as a benchmarking.

Controlling Budgets: It supports companies in meeting with financial issues like over

expenditure of cash on unnecessary events that doesn't have any values to a product.

Bizdaq could use these techniques to control variances between its estimated and actual

sales.

CONCLUSION

From above mentioned assignment it has been comprehended that an organisation has to

minimize their wastage and for this they need to use available resources. It is must for an

organisation to do their task adequately as this will assist them to raise profits. Apart from this, it

is necessary for manager to prepare an effective plan as this will give proper direction to

employees. Several tools and techniques of Budgetary control support company in tracking all

activities and also helps in decision-making process to decide changes required in these

activities.

performance of its various resources such as inventories, labour, funds, assets, etc. It

measures the performance based on returns received by business after investing in

particular resources (McNeil, Freyand Embrechts, 2015). It could re-solve financial

issues like excess debts and non-performing of assets by application of KPI indicators to

eliminate these issues at beginning stage. Bizdaq could eliminate financial issues of

excess blockage of money in customers through reducing credit amount given to them.

For this company needs to identify whether it is profitable for a company to more sale

foods on credit or not.

Benchmarking: Here, company can measured its annual performance by comparing it

with previous years of different companies. For Example, let's assume Bizdaq's

competitors which is into same business size has more sales than the company. Hence,

company could take their sales as a benchmarking.

Controlling Budgets: It supports companies in meeting with financial issues like over

expenditure of cash on unnecessary events that doesn't have any values to a product.

Bizdaq could use these techniques to control variances between its estimated and actual

sales.

CONCLUSION

From above mentioned assignment it has been comprehended that an organisation has to

minimize their wastage and for this they need to use available resources. It is must for an

organisation to do their task adequately as this will assist them to raise profits. Apart from this, it

is necessary for manager to prepare an effective plan as this will give proper direction to

employees. Several tools and techniques of Budgetary control support company in tracking all

activities and also helps in decision-making process to decide changes required in these

activities.

REFERENCES

Books and Journals

Books and Journals

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.