Managerial Accounting Techniques for Tech UK

VerifiedAdded on 2020/06/06

|13

|3590

|186

AI Summary

This assignment delves into the application of managerial accounting techniques within Tech UK Limited. It examines various costing methods like marginal and absorption costing, alongside budgeting practices. The report emphasizes how these techniques can assist in balancing internal operations and achieving financial stability for the company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Management accounting and requirements of management accounting..........................1

Difference between financial accounting and management accounting................................1

Importance of management accounting information to departmental managers for decision-

making....................................................................................................................................2

Various Cost Accounting Systems.........................................................................................2

Inventory management system...............................................................................................1

Job Costing System................................................................................................................1

B) Producing financial information........................................................................................2

Types of management accounting reports..............................................................................2

Information to be presented in understandable manner.........................................................3

TASK 2............................................................................................................................................3

Preparation of income statements using Marginal and Absorption Costing..........................3

TASK 3............................................................................................................................................5

Kinds of budgets and advantages and disadvantages.............................................................5

Budget preparation process and various costing systems.......................................................7

TASK 4............................................................................................................................................7

Comparison of management approach of one organisation with other company..................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Management accounting and requirements of management accounting..........................1

Difference between financial accounting and management accounting................................1

Importance of management accounting information to departmental managers for decision-

making....................................................................................................................................2

Various Cost Accounting Systems.........................................................................................2

Inventory management system...............................................................................................1

Job Costing System................................................................................................................1

B) Producing financial information........................................................................................2

Types of management accounting reports..............................................................................2

Information to be presented in understandable manner.........................................................3

TASK 2............................................................................................................................................3

Preparation of income statements using Marginal and Absorption Costing..........................3

TASK 3............................................................................................................................................5

Kinds of budgets and advantages and disadvantages.............................................................5

Budget preparation process and various costing systems.......................................................7

TASK 4............................................................................................................................................7

Comparison of management approach of one organisation with other company..................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................8

INTRODUCTION

Management accounting is much beneficial to managers so that they are able to take

better decisions. Present report deals with importance of management accounting information in

Tech (UK) Limited which is engaged in production of special chargers for mobile, telephone and

carry-on gadgets for retail outlets. Requirements of such accounting, various managerial reports

are explained. Moreover, marginal and absorption costing methods are used to prepare income

statements. Furthermore, kinds of planning tools are discussed along with advantages and

disadvantages. Use of management accounting systems is explained for resolving financial

problems. Thus, such information is helpful for management to take enhanced decisions.

TASK 1

A) Management accounting and requirements of management accounting

Managers are quite benefited by implementing this type of accounting as it helps them to

take structured decisions in the best possible manner. Financial information is provided to the

managerial personnel so that they may analyse financial performance and take better decision so

that organisation may be strengthened internally and desired outcome can be generated in the

market by garnering profits .(Ahadiat, 2013).

Difference between financial accounting and management accounting

Financial Accounting Management Accounting

1. It is a branch of accounting which takes

monetary transactions and final accounts are

prepared.

1. This accounting not only takes information

of monetary transactions but non-monetary

aspects are also taken into account and

managerial reports are formulated.

2. Financial statements are to be prepared in

accordance to the format provided by

Companies Act 2006

2. No format is prescribed by professional

body and a firm can prepare reports of any

format as per their requirements.

3. Financial accounting imparts detailed

financials of company on various operational

segments (Bennett, Schaltegger and Zvezdov,

3. Managerial reports are summarised ones

about financial health of firm.

1

Management accounting is much beneficial to managers so that they are able to take

better decisions. Present report deals with importance of management accounting information in

Tech (UK) Limited which is engaged in production of special chargers for mobile, telephone and

carry-on gadgets for retail outlets. Requirements of such accounting, various managerial reports

are explained. Moreover, marginal and absorption costing methods are used to prepare income

statements. Furthermore, kinds of planning tools are discussed along with advantages and

disadvantages. Use of management accounting systems is explained for resolving financial

problems. Thus, such information is helpful for management to take enhanced decisions.

TASK 1

A) Management accounting and requirements of management accounting

Managers are quite benefited by implementing this type of accounting as it helps them to

take structured decisions in the best possible manner. Financial information is provided to the

managerial personnel so that they may analyse financial performance and take better decision so

that organisation may be strengthened internally and desired outcome can be generated in the

market by garnering profits .(Ahadiat, 2013).

Difference between financial accounting and management accounting

Financial Accounting Management Accounting

1. It is a branch of accounting which takes

monetary transactions and final accounts are

prepared.

1. This accounting not only takes information

of monetary transactions but non-monetary

aspects are also taken into account and

managerial reports are formulated.

2. Financial statements are to be prepared in

accordance to the format provided by

Companies Act 2006

2. No format is prescribed by professional

body and a firm can prepare reports of any

format as per their requirements.

3. Financial accounting imparts detailed

financials of company on various operational

segments (Bennett, Schaltegger and Zvezdov,

3. Managerial reports are summarised ones

about financial health of firm.

1

2013).

4. The financials are prepared usually at the

end of accounting period.

4. There is no specific period to prepare

managerial reports. It is formulated as when

need arises for the same by management.

Importance of management accounting information to departmental managers for decision-

making

The management accounting information is quite significant of departmental managers so

that they may be able to assess performance of units and take better decisions in order to improve

upon the same if deviations exist. On the other hand, there are various departments in Tech (UK)

Limited which are integrated with one another and required to perform well to inject overall

efficiency (Chenhall and Smith, 2011). Finance, marketing, operations, production and HR are

some departments of an organisation. A production unit provides reports in which amount of

inventory needed is listed. This is then provided to finance department to evaluate whether

resources are available to buy raw materials or not. Thus, all the units are interrelated with each

other and performance is measured with much ease and as such, management accounting

information assists departmental managers of Tech (UK) Limited to take enhanced decisions.

Various Cost Accounting Systems

Cost accounting is essentially required in the organisation so that costs can be controlled

in a better way by reducing expenditures up to a high extent. Cost accounting is helpful to Tech

(UK) Limited as it helps to minimise costs incurred in manufacturing mobile chargers and other

carry-on gadgets in effective manner. The various cost accounting systems are listed below-

2

4. The financials are prepared usually at the

end of accounting period.

4. There is no specific period to prepare

managerial reports. It is formulated as when

need arises for the same by management.

Importance of management accounting information to departmental managers for decision-

making

The management accounting information is quite significant of departmental managers so

that they may be able to assess performance of units and take better decisions in order to improve

upon the same if deviations exist. On the other hand, there are various departments in Tech (UK)

Limited which are integrated with one another and required to perform well to inject overall

efficiency (Chenhall and Smith, 2011). Finance, marketing, operations, production and HR are

some departments of an organisation. A production unit provides reports in which amount of

inventory needed is listed. This is then provided to finance department to evaluate whether

resources are available to buy raw materials or not. Thus, all the units are interrelated with each

other and performance is measured with much ease and as such, management accounting

information assists departmental managers of Tech (UK) Limited to take enhanced decisions.

Various Cost Accounting Systems

Cost accounting is essentially required in the organisation so that costs can be controlled

in a better way by reducing expenditures up to a high extent. Cost accounting is helpful to Tech

(UK) Limited as it helps to minimise costs incurred in manufacturing mobile chargers and other

carry-on gadgets in effective manner. The various cost accounting systems are listed below-

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1. Actual costing-

As the name suggests, actual costs incurred on manufacturing items are recorded in this

system. The costs such as raw materials, labour and quantities used in production is effectively

assessed by the manager and as such, actual cost can be ascertained (Laudon and Laudon, 2016).

2. Standard costing-

Standard costs on various manufacturing activities are ascertained by the organisation. It

is used to compare planned costs with actual costs so that deviations may be analysed in periodic

basis.

3. Normal costing-

Normal costing is another effective method used to assess cost of production. Normal

costs incurred such as materials, overheads costs, labour are ascertained in effective manner.

Inventory management system

Inventory is required by Tech (UK) Limited in order to achieve desired production in the

best possible manner. Organisation uses such system so that inventory can be managed in

effective way and spoilage may be observed. On the other hand, if stock is ordered ion excess,

additional handling cost is incurred for keeping the same in warehouse (Quattrone, 2016). To

overcome this, inventory report is prepared by production department in which requirements are

listed down and provided to top management. Thus, desired stock is purchased to meet demand

of department and hence, no spoilage occurs. Types of inventory management systems are

tracking with barcode and RFID (Radio Frequency Identification). Tracking with barcode system

implies that stock gets updated as soon as it is scanned. Thus, level of inventory available to

company is clarified quite effectually. On the other hand, RFID implies that when stock is

availed, the software recognises it and the same is recorded. Hence, organisation is benefited by

such systems.

Job Costing System

Job costing is a way to assess cost incurred on various manufacturing jobs which are

engaged in generating desired level of production. In simple words, cost of manufacturing is

assigned to particular product. Three types of information are accumulated by job costing system

such as direct labour, direct materials and overheads. Thus, Tech (UK) Limited may be able to

1

As the name suggests, actual costs incurred on manufacturing items are recorded in this

system. The costs such as raw materials, labour and quantities used in production is effectively

assessed by the manager and as such, actual cost can be ascertained (Laudon and Laudon, 2016).

2. Standard costing-

Standard costs on various manufacturing activities are ascertained by the organisation. It

is used to compare planned costs with actual costs so that deviations may be analysed in periodic

basis.

3. Normal costing-

Normal costing is another effective method used to assess cost of production. Normal

costs incurred such as materials, overheads costs, labour are ascertained in effective manner.

Inventory management system

Inventory is required by Tech (UK) Limited in order to achieve desired production in the

best possible manner. Organisation uses such system so that inventory can be managed in

effective way and spoilage may be observed. On the other hand, if stock is ordered ion excess,

additional handling cost is incurred for keeping the same in warehouse (Quattrone, 2016). To

overcome this, inventory report is prepared by production department in which requirements are

listed down and provided to top management. Thus, desired stock is purchased to meet demand

of department and hence, no spoilage occurs. Types of inventory management systems are

tracking with barcode and RFID (Radio Frequency Identification). Tracking with barcode system

implies that stock gets updated as soon as it is scanned. Thus, level of inventory available to

company is clarified quite effectually. On the other hand, RFID implies that when stock is

availed, the software recognises it and the same is recorded. Hence, organisation is benefited by

such systems.

Job Costing System

Job costing is a way to assess cost incurred on various manufacturing jobs which are

engaged in generating desired level of production. In simple words, cost of manufacturing is

assigned to particular product. Three types of information are accumulated by job costing system

such as direct labour, direct materials and overheads. Thus, Tech (UK) Limited may be able to

1

analyse manufacturing jobs and efforts can be made to minimise expenditures on various jobs

which are unproductive. Hence, more production may be achieved in an effective manner.

B) Producing financial information

Types of management accounting reports

The different types of management accounting reports are described below-

1. Segmental Report-

This report provides a way to analyse information regarding various operational segments

of the company (Broccardo, 2014). It is attached in the financial statement and provides clarity

about the performance of segments whether they are performing good or not. This helps to

evaluate overall financial condition of firm and as such, stakeholders can easily access

information and they can take enhanced decisions by relying on this information.

2. Performance Report-

It is prepared to analyse employee's performance in effective manner. Tech (UK) Limited

can easily assess whether workers are highly productive or not. If deviations are analysed in the

actual output with that of planned one, corrective actions can be taken so that productivity can be

enhanced in a better way. Thus, this report is helpful in analysing performance and taking

corrective action to improve upon the same.

3. Accounts Receivables Ageing Report-

Sales are made by company on cash or credit basis. The payment is paid afterwards by

the debtors on goods purchased by them on credit. In relation to this, accounts receivables ageing

report is prepared in effective manner which lists down unpaid invoices of credit customers.

Along with this, names of customers and outstanding amount are listed in such report. Thus,

pending amount can be analysed in a better way and customers may be contacted to make

payments. If outstanding amount is more, then it is required to implement strict credit policies to

avail payment from debtors within stipulated time.

4. Inventory Management Report-

It is prepared by the production department which lists down requirement of inventory

for achieving desired production. The report is forwarded to top management which scrutinises

this report and orders desired stock as per needs of production department and customer's orders

2

which are unproductive. Hence, more production may be achieved in an effective manner.

B) Producing financial information

Types of management accounting reports

The different types of management accounting reports are described below-

1. Segmental Report-

This report provides a way to analyse information regarding various operational segments

of the company (Broccardo, 2014). It is attached in the financial statement and provides clarity

about the performance of segments whether they are performing good or not. This helps to

evaluate overall financial condition of firm and as such, stakeholders can easily access

information and they can take enhanced decisions by relying on this information.

2. Performance Report-

It is prepared to analyse employee's performance in effective manner. Tech (UK) Limited

can easily assess whether workers are highly productive or not. If deviations are analysed in the

actual output with that of planned one, corrective actions can be taken so that productivity can be

enhanced in a better way. Thus, this report is helpful in analysing performance and taking

corrective action to improve upon the same.

3. Accounts Receivables Ageing Report-

Sales are made by company on cash or credit basis. The payment is paid afterwards by

the debtors on goods purchased by them on credit. In relation to this, accounts receivables ageing

report is prepared in effective manner which lists down unpaid invoices of credit customers.

Along with this, names of customers and outstanding amount are listed in such report. Thus,

pending amount can be analysed in a better way and customers may be contacted to make

payments. If outstanding amount is more, then it is required to implement strict credit policies to

avail payment from debtors within stipulated time.

4. Inventory Management Report-

It is prepared by the production department which lists down requirement of inventory

for achieving desired production. The report is forwarded to top management which scrutinises

this report and orders desired stock as per needs of production department and customer's orders

2

are effectively met. Moreover, it reduces wastage of inventory and as such, maximum production

can be accomplished.

Information to be presented in understandable manner

The information should be presented to financial users so that they may analyse financial

statements and take better decisions. Understand ability concept states that information must be

easily understandable by external users of accounting information and all the disclosures and

accounting treatments must be understood by them. Thus, reliable information can be

accomplished by them and as such, stakeholders can take enhanced decisions.

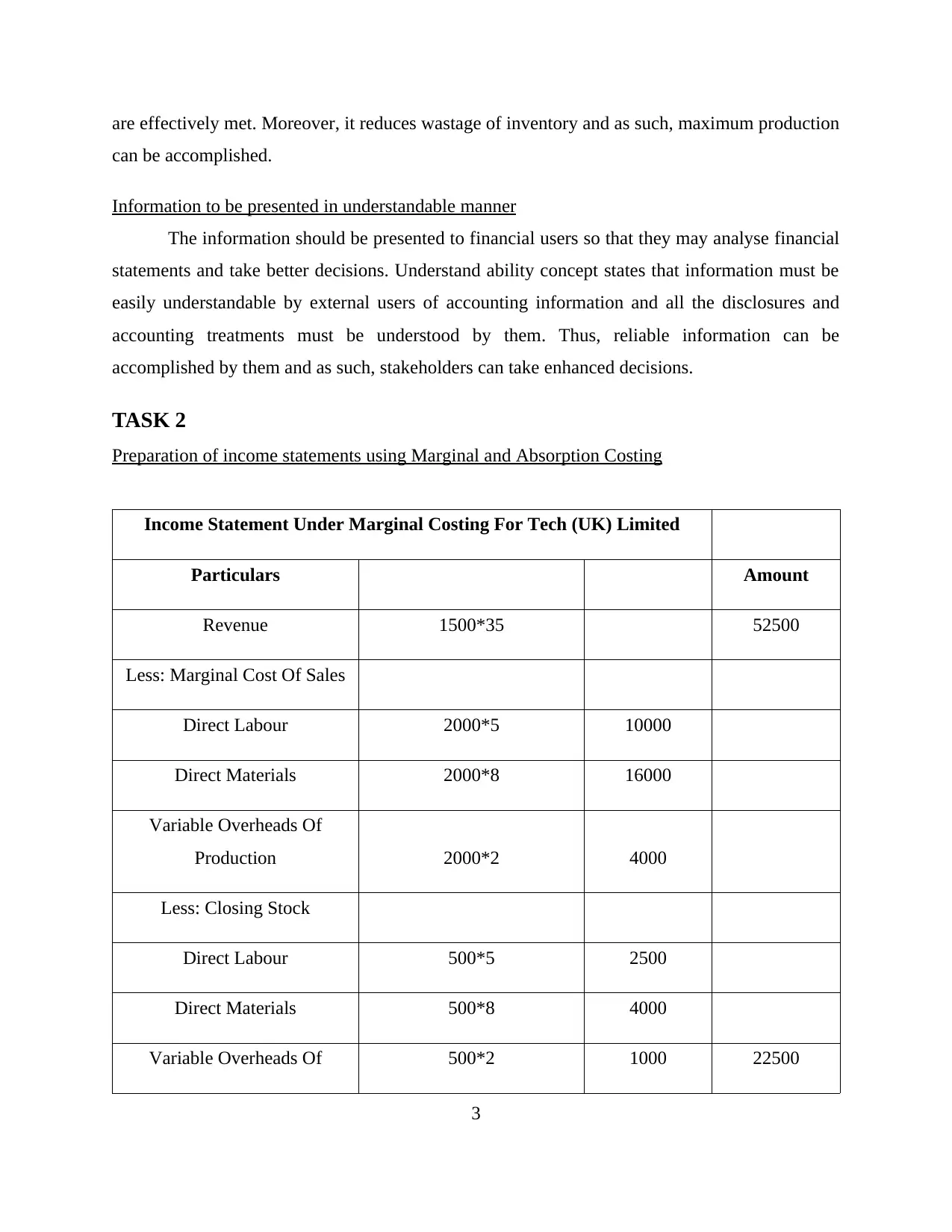

TASK 2

Preparation of income statements using Marginal and Absorption Costing

Income Statement Under Marginal Costing For Tech (UK) Limited

Particulars Amount

Revenue 1500*35 52500

Less: Marginal Cost Of Sales

Direct Labour 2000*5 10000

Direct Materials 2000*8 16000

Variable Overheads Of

Production 2000*2 4000

Less: Closing Stock

Direct Labour 500*5 2500

Direct Materials 500*8 4000

Variable Overheads Of 500*2 1000 22500

3

can be accomplished.

Information to be presented in understandable manner

The information should be presented to financial users so that they may analyse financial

statements and take better decisions. Understand ability concept states that information must be

easily understandable by external users of accounting information and all the disclosures and

accounting treatments must be understood by them. Thus, reliable information can be

accomplished by them and as such, stakeholders can take enhanced decisions.

TASK 2

Preparation of income statements using Marginal and Absorption Costing

Income Statement Under Marginal Costing For Tech (UK) Limited

Particulars Amount

Revenue 1500*35 52500

Less: Marginal Cost Of Sales

Direct Labour 2000*5 10000

Direct Materials 2000*8 16000

Variable Overheads Of

Production 2000*2 4000

Less: Closing Stock

Direct Labour 500*5 2500

Direct Materials 500*8 4000

Variable Overheads Of 500*2 1000 22500

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Production

30000

Less: Other Variable Expenses 52500*15% 7875

Contribution Per Unit 22125

Less: Fixed Costs

Selling Expenses 15000

Administrative Expenses 10000 25000

Net Loss -2875

Marginal Costing is computed for an organisation. It can be interpreted that revenue

generated by firm is 52500, having 1500 units sold at price of 35. Various costs of labour,

materials and variable production of overheads are computed and deducted to get contribution

per unit of 22125. After carrying out variable expenditures, fixed costs like selling and

administrative expenses collectively 25000 is deducted. Finally, net loss is arrived amounting to

2875. It can be analysed that firm is not able to initiate control on fixed and variable costs by

which loss is computed. Thus, it is required to reduce expenditure to earn profit.

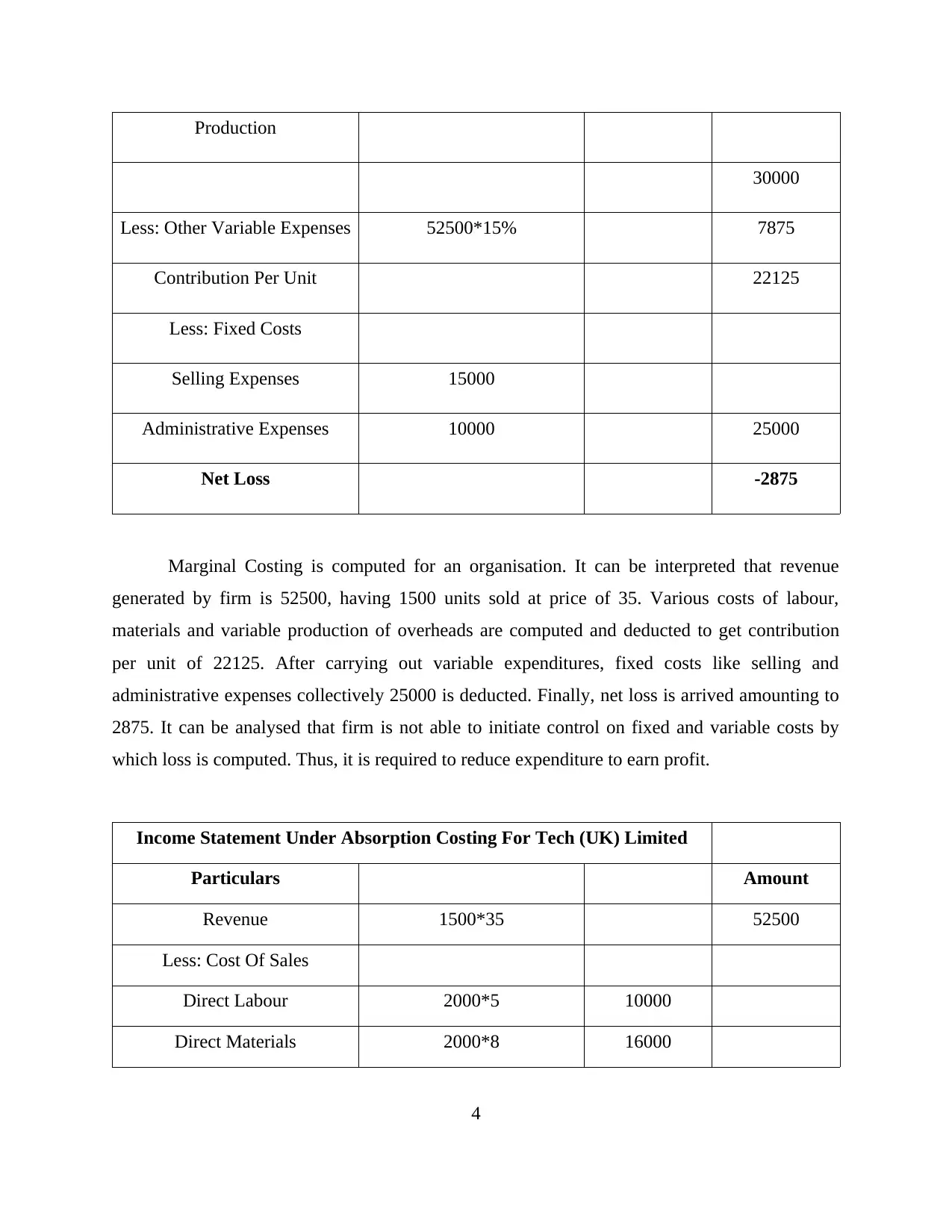

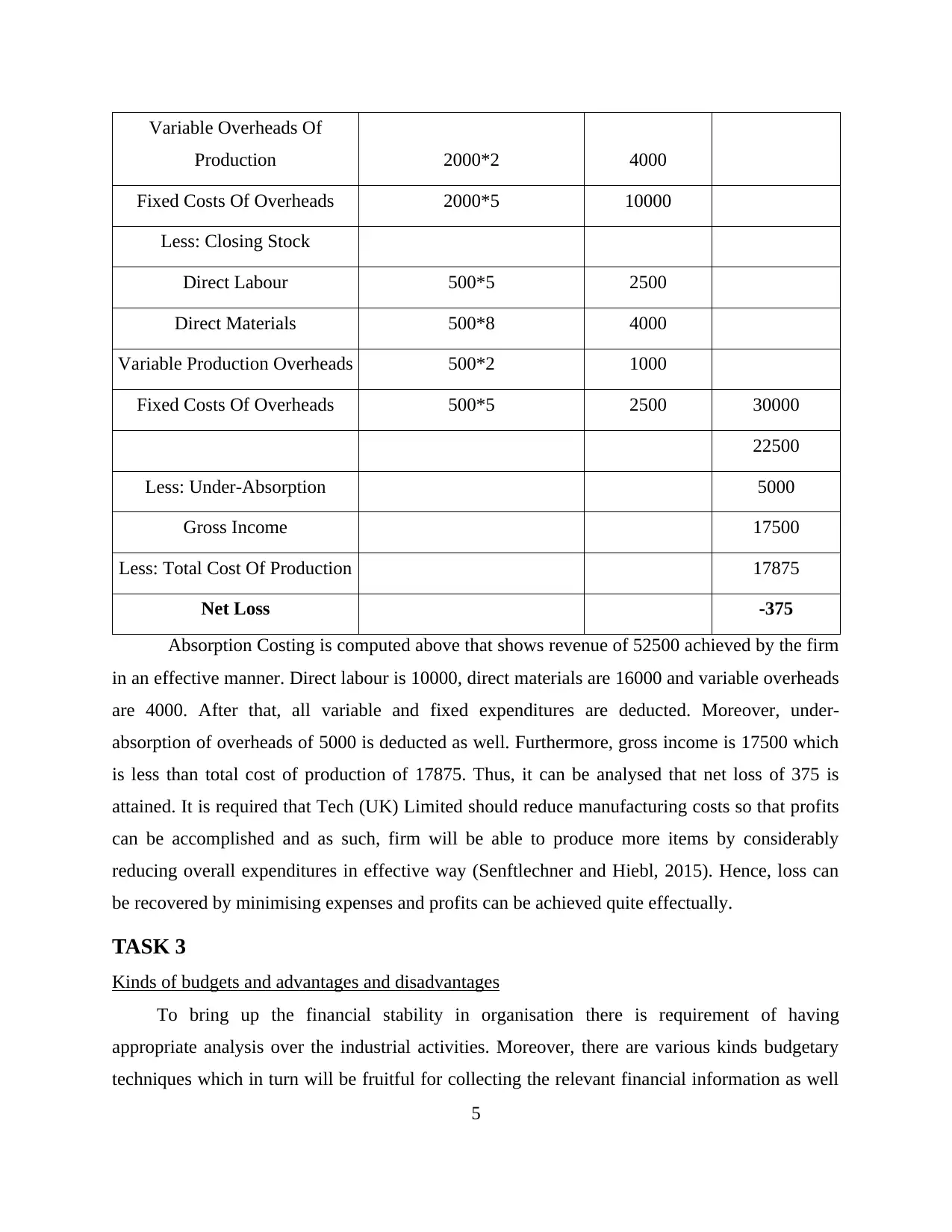

Income Statement Under Absorption Costing For Tech (UK) Limited

Particulars Amount

Revenue 1500*35 52500

Less: Cost Of Sales

Direct Labour 2000*5 10000

Direct Materials 2000*8 16000

4

30000

Less: Other Variable Expenses 52500*15% 7875

Contribution Per Unit 22125

Less: Fixed Costs

Selling Expenses 15000

Administrative Expenses 10000 25000

Net Loss -2875

Marginal Costing is computed for an organisation. It can be interpreted that revenue

generated by firm is 52500, having 1500 units sold at price of 35. Various costs of labour,

materials and variable production of overheads are computed and deducted to get contribution

per unit of 22125. After carrying out variable expenditures, fixed costs like selling and

administrative expenses collectively 25000 is deducted. Finally, net loss is arrived amounting to

2875. It can be analysed that firm is not able to initiate control on fixed and variable costs by

which loss is computed. Thus, it is required to reduce expenditure to earn profit.

Income Statement Under Absorption Costing For Tech (UK) Limited

Particulars Amount

Revenue 1500*35 52500

Less: Cost Of Sales

Direct Labour 2000*5 10000

Direct Materials 2000*8 16000

4

Variable Overheads Of

Production 2000*2 4000

Fixed Costs Of Overheads 2000*5 10000

Less: Closing Stock

Direct Labour 500*5 2500

Direct Materials 500*8 4000

Variable Production Overheads 500*2 1000

Fixed Costs Of Overheads 500*5 2500 30000

22500

Less: Under-Absorption 5000

Gross Income 17500

Less: Total Cost Of Production 17875

Net Loss -375

Absorption Costing is computed above that shows revenue of 52500 achieved by the firm

in an effective manner. Direct labour is 10000, direct materials are 16000 and variable overheads

are 4000. After that, all variable and fixed expenditures are deducted. Moreover, under-

absorption of overheads of 5000 is deducted as well. Furthermore, gross income is 17500 which

is less than total cost of production of 17875. Thus, it can be analysed that net loss of 375 is

attained. It is required that Tech (UK) Limited should reduce manufacturing costs so that profits

can be accomplished and as such, firm will be able to produce more items by considerably

reducing overall expenditures in effective way (Senftlechner and Hiebl, 2015). Hence, loss can

be recovered by minimising expenses and profits can be achieved quite effectually.

TASK 3

Kinds of budgets and advantages and disadvantages

To bring up the financial stability in organisation there is requirement of having

appropriate analysis over the industrial activities. Moreover, there are various kinds budgetary

techniques which in turn will be fruitful for collecting the relevant financial information as well

5

Production 2000*2 4000

Fixed Costs Of Overheads 2000*5 10000

Less: Closing Stock

Direct Labour 500*5 2500

Direct Materials 500*8 4000

Variable Production Overheads 500*2 1000

Fixed Costs Of Overheads 500*5 2500 30000

22500

Less: Under-Absorption 5000

Gross Income 17500

Less: Total Cost Of Production 17875

Net Loss -375

Absorption Costing is computed above that shows revenue of 52500 achieved by the firm

in an effective manner. Direct labour is 10000, direct materials are 16000 and variable overheads

are 4000. After that, all variable and fixed expenditures are deducted. Moreover, under-

absorption of overheads of 5000 is deducted as well. Furthermore, gross income is 17500 which

is less than total cost of production of 17875. Thus, it can be analysed that net loss of 375 is

attained. It is required that Tech (UK) Limited should reduce manufacturing costs so that profits

can be accomplished and as such, firm will be able to produce more items by considerably

reducing overall expenditures in effective way (Senftlechner and Hiebl, 2015). Hence, loss can

be recovered by minimising expenses and profits can be achieved quite effectually.

TASK 3

Kinds of budgets and advantages and disadvantages

To bring up the financial stability in organisation there is requirement of having

appropriate analysis over the industrial activities. Moreover, there are various kinds budgetary

techniques which in turn will be fruitful for collecting the relevant financial information as well

5

as present the appropriate outcomes. Such derived analysis will be summative to bring accurate

changes in the operational activities of business. Therefore, there will be analysis of veracious

budgetary techniques on the basis of their advantages and disadvantages.

Incremental budgeting: This budgetary technique comprises with the methods that it

considers the past transaction as well as pat records of the business which in turn will have

effective and incremental costs in the current time. Moreover, it will be assumed by the

professionals that the costs as well as revenue of the operational activities will be increased in the

coming time. Therefore, they increase the costs or funds of budgets which will be bring them the

favourable returns in the coming time. Tech UK Limited will be helpful to the business as the

managerial professionals analyse the merits and demerits of this budgetary system.

Advantages:

It has the increment in the funds for operation on a constant level while changes incurred

in the operations is gradual.

It is not complex for the managerial professionals to understand the main reasoning

behind the budgets.

It will be easy to develop the co-ordination among the budgets of various departments.

Disadvantages:

It only focuses on increasing the funds for operations while the level of activities remains

content. Moreover, there are no changes into the operational level of entity as there will

be no implication of any technique of strategies to make improvements.

It does not make reduction in the costs and a fund implies in each industrial units.

The irrelevant application of costs will be over useless activities.

Zero based budgeting: these are the budgets which are variable in nature as there will be

flexibility in the costs implied in each activity. Thus, there are various operations which in turn

will be effective as well as helpful to the firm as to have favourable gains. This starts with the

zero balance of budgets as there will be no influences form the past and previous year budgets

for the operations. Thus, it will be very easy and promptly prepared by the professionals.

Similarly, there are various merits and demerits to this budgeting technique which will be helpful

to the managerial personnel of Tech UK Limited.

Advantages:

6

changes in the operational activities of business. Therefore, there will be analysis of veracious

budgetary techniques on the basis of their advantages and disadvantages.

Incremental budgeting: This budgetary technique comprises with the methods that it

considers the past transaction as well as pat records of the business which in turn will have

effective and incremental costs in the current time. Moreover, it will be assumed by the

professionals that the costs as well as revenue of the operational activities will be increased in the

coming time. Therefore, they increase the costs or funds of budgets which will be bring them the

favourable returns in the coming time. Tech UK Limited will be helpful to the business as the

managerial professionals analyse the merits and demerits of this budgetary system.

Advantages:

It has the increment in the funds for operation on a constant level while changes incurred

in the operations is gradual.

It is not complex for the managerial professionals to understand the main reasoning

behind the budgets.

It will be easy to develop the co-ordination among the budgets of various departments.

Disadvantages:

It only focuses on increasing the funds for operations while the level of activities remains

content. Moreover, there are no changes into the operational level of entity as there will

be no implication of any technique of strategies to make improvements.

It does not make reduction in the costs and a fund implies in each industrial units.

The irrelevant application of costs will be over useless activities.

Zero based budgeting: these are the budgets which are variable in nature as there will be

flexibility in the costs implied in each activity. Thus, there are various operations which in turn

will be effective as well as helpful to the firm as to have favourable gains. This starts with the

zero balance of budgets as there will be no influences form the past and previous year budgets

for the operations. Thus, it will be very easy and promptly prepared by the professionals.

Similarly, there are various merits and demerits to this budgeting technique which will be helpful

to the managerial personnel of Tech UK Limited.

Advantages:

6

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

These are the most flexible and variable budgetary techniques which in turn will be

helpful to the business as to have satisfactory amount of funds for the activities at the

time of requirements.

It is the easiest method as it starts form zero balance and no records of past will help in

favourable preparation of the data set.

Disadvantages:

In accordance with the flexible nature of this budgeting technique there will be chances

of having huge manipulation of funds.

No records of past activities and costs would not bring accurate estimation as well as

analysis to auditors in determining the level of funds requires in job.

Activity based budgeting: this method insists the process that it comprises with the past

records of all the business activities. Thus, information relevant with revenue, costs, profits and

losses incurred in operations. There is mainly ascertainment of the expense incurred in activities

like manufacturing, branding etc. Therefore, the outcomes bound professionals to re-think and

make strategic plans to alter the costs of activities. Moreover, this budgeting will help in

managing the operational activities as well as costs incurred in them.

Advantages:

It allocates costs to each business activities which will be helpful and beneficial as to

bring appropriate efficiency and ability to perform the tasks.

Disadvantages:

It will require much time and consideration of accounting professionals to analyse the

past records and plan the new budgets for the period.

Budget preparation process and various costing systems

To plan the financial structure and costing methods for Tech UK Limited there will need to

have proper information relevant with the process of preparing the forecast table. However, there

are various techniques which in turn will be helpful to the managerial professionals as well as

accountant of the entity in terms of analysing the costs incurred in business activities and the

allocation of capital funds in a suitable manner.

7

helpful to the business as to have satisfactory amount of funds for the activities at the

time of requirements.

It is the easiest method as it starts form zero balance and no records of past will help in

favourable preparation of the data set.

Disadvantages:

In accordance with the flexible nature of this budgeting technique there will be chances

of having huge manipulation of funds.

No records of past activities and costs would not bring accurate estimation as well as

analysis to auditors in determining the level of funds requires in job.

Activity based budgeting: this method insists the process that it comprises with the past

records of all the business activities. Thus, information relevant with revenue, costs, profits and

losses incurred in operations. There is mainly ascertainment of the expense incurred in activities

like manufacturing, branding etc. Therefore, the outcomes bound professionals to re-think and

make strategic plans to alter the costs of activities. Moreover, this budgeting will help in

managing the operational activities as well as costs incurred in them.

Advantages:

It allocates costs to each business activities which will be helpful and beneficial as to

bring appropriate efficiency and ability to perform the tasks.

Disadvantages:

It will require much time and consideration of accounting professionals to analyse the

past records and plan the new budgets for the period.

Budget preparation process and various costing systems

To plan the financial structure and costing methods for Tech UK Limited there will need to

have proper information relevant with the process of preparing the forecast table. However, there

are various techniques which in turn will be helpful to the managerial professionals as well as

accountant of the entity in terms of analysing the costs incurred in business activities and the

allocation of capital funds in a suitable manner.

7

TASK 4

Comparison of management approach of one organisation with other company

The use of various management accounting techniques which in turn help in overcoming with

the financial drawbacks in the organisation. Tech UK Limited needed to implicate such

techniques and approaches which in turn bring them the ability to improve the financial strength

of the business.

Balanced scorecard: this the strategic implication of the targets which will encourage

the workforce to make productive efforts in attaining the business targets in the right time

(Balanced Scorecard Basics, 2018). Thus, it ensures that the proposed work will be managed by

the professionals in the required time and manner. Therefore, it will be helpful and beneficial to

overcome with the financial problems in the business.

Variance analysis: the difference between actual and budgeted costs of the business is

known as variance. Moreover, this analysis will bring the adequate determination of the factors

such as the costs implied in each business activities will requires attention of professionals to

make qualitative decision.

Key performance indicators: These are the performance categories of the business

which records all the efforts made by employees in elation wit attaining the industrial goals. On

the other side, it will be motivating and encouraging the professionals as they will have

monetary benefits in return as well as revenue gains against their efforts.

Financial governance: assigning the duties to the most talented and skilled personnel in

relation with handling the accounting operations in the entities. It comprises with the activities

like allocation of funds, capital utilisation, managing the investments, dividend payments as

well as balance between trade payables and receivables. Thus, such implication will lead the

firm in resolving any financial issues.

CONCLUSION

On the basis of above report which comprises with the managerial accounting tactics and

concepts. Therefore, implication of such techniques which will be assistive and helpful in

balancing the internal activities of entities. The report emphasis various costing and budgeting

techniques which will be helpful in manage the operation in Tech UK Limited. There has been

8

Comparison of management approach of one organisation with other company

The use of various management accounting techniques which in turn help in overcoming with

the financial drawbacks in the organisation. Tech UK Limited needed to implicate such

techniques and approaches which in turn bring them the ability to improve the financial strength

of the business.

Balanced scorecard: this the strategic implication of the targets which will encourage

the workforce to make productive efforts in attaining the business targets in the right time

(Balanced Scorecard Basics, 2018). Thus, it ensures that the proposed work will be managed by

the professionals in the required time and manner. Therefore, it will be helpful and beneficial to

overcome with the financial problems in the business.

Variance analysis: the difference between actual and budgeted costs of the business is

known as variance. Moreover, this analysis will bring the adequate determination of the factors

such as the costs implied in each business activities will requires attention of professionals to

make qualitative decision.

Key performance indicators: These are the performance categories of the business

which records all the efforts made by employees in elation wit attaining the industrial goals. On

the other side, it will be motivating and encouraging the professionals as they will have

monetary benefits in return as well as revenue gains against their efforts.

Financial governance: assigning the duties to the most talented and skilled personnel in

relation with handling the accounting operations in the entities. It comprises with the activities

like allocation of funds, capital utilisation, managing the investments, dividend payments as

well as balance between trade payables and receivables. Thus, such implication will lead the

firm in resolving any financial issues.

CONCLUSION

On the basis of above report which comprises with the managerial accounting tactics and

concepts. Therefore, implication of such techniques which will be assistive and helpful in

balancing the internal activities of entities. The report emphasis various costing and budgeting

techniques which will be helpful in manage the operation in Tech UK Limited. There has been

8

measurement of marginal and an absorption costing technique which helps brings the accurate

outcomes to the proposed data base.

REFERENCES

Books and Journals

Ahadiat, N., 2013. In search of practice-based topics for management accounting

education. Available at SSRN 2355853.

Bennett, M. D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices in

management accounting for sustainability (pp. 1-56). London: ICAEW.

Broccardo, L., 2014. Management Accounting System in Italian Smes: Some Evidences and

Implications1. Advances in Management and Applied Economics. 4(4). p.1.

Chenhall, R.H. and Smith, D., 2011. A review of Australian management accounting research:

1980–2009. Accounting & Finance. 51(1). pp.173-206.

Laudon, K. C. and Laudon, J. P., 2016. Management information system. Pearson Education

India.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Senftlechner, D. and Hiebl, M. R., 2015. Management accounting and management control in

family businesses: past accomplishments and future opportunities. Journal of Accounting

& Organizational Change. 11(4). pp.573-606.

Online

9

outcomes to the proposed data base.

REFERENCES

Books and Journals

Ahadiat, N., 2013. In search of practice-based topics for management accounting

education. Available at SSRN 2355853.

Bennett, M. D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices in

management accounting for sustainability (pp. 1-56). London: ICAEW.

Broccardo, L., 2014. Management Accounting System in Italian Smes: Some Evidences and

Implications1. Advances in Management and Applied Economics. 4(4). p.1.

Chenhall, R.H. and Smith, D., 2011. A review of Australian management accounting research:

1980–2009. Accounting & Finance. 51(1). pp.173-206.

Laudon, K. C. and Laudon, J. P., 2016. Management information system. Pearson Education

India.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research. 31. pp.118-122.

Senftlechner, D. and Hiebl, M. R., 2015. Management accounting and management control in

family businesses: past accomplishments and future opportunities. Journal of Accounting

& Organizational Change. 11(4). pp.573-606.

Online

9

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.