Management Accounting Practices and Trends

VerifiedAdded on 2020/01/16

|20

|6546

|197

Essay

AI Summary

This assignment delves into contemporary trends in management accounting. It examines the impact of lean manufacturing on accounting practices, analyzes the role of management accounting in promoting sustainable development, and investigates its application in safety management within organizations. The analysis draws upon a range of academic sources to provide a comprehensive understanding of current developments and challenges in the field.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................1

M1 Evaluate the benefits of management accounting systems and their application within

Agmet..........................................................................................................................................3

P2 Explanation regarding different methods used for management accounting reporting.........4

D1 Critical evaluation about how management accounting systems and management

accounting reporting is integrated within organisational processes............................................6

TASK 2............................................................................................................................................8

P3 & M2 Preparation of income statements as per the method of absorption and marginal

costing techniques........................................................................................................................8

D2 Interpretation of the data and information which have been calculated above in the

statements of income under absorption and marginal costing techniques.................................11

TASK 3..........................................................................................................................................12

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control........................................................................................................................................12

M3 Analysis over the use of different planning tools and their application for preparing and

forecasting budgets with special reference................................................................................12

D3 & M4 Evaluate how planning tools for accounting respond appropriately to solving

financial problems to lead organisations to sustainable success...............................................14

TASK 4..........................................................................................................................................15

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1Explain management accounting and give the essential requirements of different types of

management accounting systems.................................................................................................1

M1 Evaluate the benefits of management accounting systems and their application within

Agmet..........................................................................................................................................3

P2 Explanation regarding different methods used for management accounting reporting.........4

D1 Critical evaluation about how management accounting systems and management

accounting reporting is integrated within organisational processes............................................6

TASK 2............................................................................................................................................8

P3 & M2 Preparation of income statements as per the method of absorption and marginal

costing techniques........................................................................................................................8

D2 Interpretation of the data and information which have been calculated above in the

statements of income under absorption and marginal costing techniques.................................11

TASK 3..........................................................................................................................................12

P4 Advantages and disadvantages of different types of planning tools used for budgetary

control........................................................................................................................................12

M3 Analysis over the use of different planning tools and their application for preparing and

forecasting budgets with special reference................................................................................12

D3 & M4 Evaluate how planning tools for accounting respond appropriately to solving

financial problems to lead organisations to sustainable success...............................................14

TASK 4..........................................................................................................................................15

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems.....................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting can be considered as a technique though which management of

any enterprise can easily manage their available resources(Renz, 2016). As a small business

enterprise Agmet is having less resources whether in terms of financial or in terms of non

financial sources. Hence it is important for such enterprise to manage their sources for attaining

the objectives of the enterprise which are predetermined by its managerial personnel’s including

top level management. This report has been framed on the case study of Agmet which is a

chemical manufacturing company in United Kingdom (Gibassier, 2017). Its employing less than

50 employees and they are having less £500,000 hence it can be said that they need to employ

techniques of cost and management accounting in its financial and organisational structure. In

this report the concept of cost accounting have been defined with their essential requirements.

Further there are two statements as per the method of absorption and marginal costing and such

statements are presented with there interpretation.

TASK 1

P1Explain management accounting and give the essential requirements of different types of

management accounting systems

Management accounting can be referred as the combination of both financial accounting

concepts and managerial principles. Hence it can be said that Agmet and its management through

optimizing the principles which are there in cost accounting can achieve the goals and objectives

which are there in the organisational structure since from beginning and the short term goals

which are there in current period. As short term goals can only contribute towards the managing

the long term goals and objectives (Quinn, 2011). There are many essential requirements of

management accounting as same as financial accounting hence it can be said that just like

financial reporting frameworks management accounting is also having certain requirements

which needs to be fulfilled so that the users can get the clear image of the company so that they

can make their decisions in respect of it. It have the combination of principles and data which

makes it reliable and the plans which are framed according to it are also ethical and achievable.

Because of it the managers and employees will not get frustrated in achieving the targets which

are determined by the top level management. Agmet can abolish the competitive factors out of

the chemical manufacturing market (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015).

1

Management accounting can be considered as a technique though which management of

any enterprise can easily manage their available resources(Renz, 2016). As a small business

enterprise Agmet is having less resources whether in terms of financial or in terms of non

financial sources. Hence it is important for such enterprise to manage their sources for attaining

the objectives of the enterprise which are predetermined by its managerial personnel’s including

top level management. This report has been framed on the case study of Agmet which is a

chemical manufacturing company in United Kingdom (Gibassier, 2017). Its employing less than

50 employees and they are having less £500,000 hence it can be said that they need to employ

techniques of cost and management accounting in its financial and organisational structure. In

this report the concept of cost accounting have been defined with their essential requirements.

Further there are two statements as per the method of absorption and marginal costing and such

statements are presented with there interpretation.

TASK 1

P1Explain management accounting and give the essential requirements of different types of

management accounting systems

Management accounting can be referred as the combination of both financial accounting

concepts and managerial principles. Hence it can be said that Agmet and its management through

optimizing the principles which are there in cost accounting can achieve the goals and objectives

which are there in the organisational structure since from beginning and the short term goals

which are there in current period. As short term goals can only contribute towards the managing

the long term goals and objectives (Quinn, 2011). There are many essential requirements of

management accounting as same as financial accounting hence it can be said that just like

financial reporting frameworks management accounting is also having certain requirements

which needs to be fulfilled so that the users can get the clear image of the company so that they

can make their decisions in respect of it. It have the combination of principles and data which

makes it reliable and the plans which are framed according to it are also ethical and achievable.

Because of it the managers and employees will not get frustrated in achieving the targets which

are determined by the top level management. Agmet can abolish the competitive factors out of

the chemical manufacturing market (Ibarrondo-Dávila, López-Alonso and Rubio-Gámez, 2015).

1

It allows firm to capture a major market share within the targeted market. The essential

requirements of management accounting techniques are mentioned below:

Traditional Accounting system: This can be defined as the system in which cost is

allocated among the various departments which are accountable for such cost and price. Through

this requirement cost can be easily traced with its responsible department further it can be said

that the revenue of each and every department in the manufacturing units of Agmet can be traced

out easily (Pipan and Czarniawska, 2010).

Lean Accounting System: This system is actually deals with the changes which are

there in management and systems. Hence it can be said that when there is a change in the capital

and organisational structure then lean accounting system can be helpful to cop up with such

changes.

Cost accounting system: It is a system which helps business to evaluate the cost of

goods and services provided by the company in order to measure profits, also known as product

costing system. Agmet can make use of this system and calculate its cost and can evaluate

profits, for preparing financial statement. The company can compute production cost separately

for each operation by the help of such accounting system.

Job costing system: It helps in collecting information about cost related with specific

job. With the help of this system, Agmet can submit required cost information to its customer

under contract where costs are refundable. Business can also keep a check over accuracy of

estimating system, which helps to quotes prices for obtaining targeted profits. This helps

company to evaluate the expenses incurred on direct materials, direct labour and overheads.

Batch costing system: It is specific order costing, which evaluates the cost in batches

also includes fixed and variable costs. Company can compute per unit cost by dividend the total

batch cost by number of units produced. For instance, when company receives order and there

are common products among several orders, the production can be done in batches and with the

help of these system, Agmet can identify total cost on each batch performed.

Inventory management system: It is a software system, which keeps a record of

inventory levels, sales and various orders placed in a reporting year. The company can keep a

record of work orders, bills of material and production to avoid overstock. This will assist

Agment to calculate inventory of raw material, finished products and work in progress to manage

inventory level.

2

requirements of management accounting techniques are mentioned below:

Traditional Accounting system: This can be defined as the system in which cost is

allocated among the various departments which are accountable for such cost and price. Through

this requirement cost can be easily traced with its responsible department further it can be said

that the revenue of each and every department in the manufacturing units of Agmet can be traced

out easily (Pipan and Czarniawska, 2010).

Lean Accounting System: This system is actually deals with the changes which are

there in management and systems. Hence it can be said that when there is a change in the capital

and organisational structure then lean accounting system can be helpful to cop up with such

changes.

Cost accounting system: It is a system which helps business to evaluate the cost of

goods and services provided by the company in order to measure profits, also known as product

costing system. Agmet can make use of this system and calculate its cost and can evaluate

profits, for preparing financial statement. The company can compute production cost separately

for each operation by the help of such accounting system.

Job costing system: It helps in collecting information about cost related with specific

job. With the help of this system, Agmet can submit required cost information to its customer

under contract where costs are refundable. Business can also keep a check over accuracy of

estimating system, which helps to quotes prices for obtaining targeted profits. This helps

company to evaluate the expenses incurred on direct materials, direct labour and overheads.

Batch costing system: It is specific order costing, which evaluates the cost in batches

also includes fixed and variable costs. Company can compute per unit cost by dividend the total

batch cost by number of units produced. For instance, when company receives order and there

are common products among several orders, the production can be done in batches and with the

help of these system, Agmet can identify total cost on each batch performed.

Inventory management system: It is a software system, which keeps a record of

inventory levels, sales and various orders placed in a reporting year. The company can keep a

record of work orders, bills of material and production to avoid overstock. This will assist

Agment to calculate inventory of raw material, finished products and work in progress to manage

inventory level.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Price optimization system: It is a mathematical analysis, price optimization is prediction

of behaviours of buyers to different prices by which company gets to know how buyers will react

to prices of products and services provided by the company. This helps company to decide

pricing in order to maximize their profits with satisfaction of consumers. Pricing strategy of

Agmet can be done by segmenting customers. This can be done by identifying common needs,

common interests, similar lifestyles.

M1 Evaluate the benefits of management accounting systems and their application within Agmet

There are several benefits of management accounting system though which it can be

clearly observed that such techniques can be utilized in responding towards various problems

that may occur during several processes of management has been carried out. Such benefits are

mentioned below:

Improvement in cash flow: These methods and principles can assist an enterprise in

managing the cash flow from various activities. Cash flow statement shows three

sections out of which first one is about operating activities and the second one is about

investing and it is followed by financing activities(Nandan, 2010).

Reduction in expenses: There are lots of expenses in each and every functions and

activities of hence they are required to assist the enterprise in the proper functionality so

that the expenses can be controlled and managed as there is very less revenue earned

through the turnover of Agmet. So managerial personnels should implement these

methods and principles for coordinating with the expenses. Through reduction which is

made in negative cash flow efficiency at its best level and high productivity rate can be

achieved. Hence it can be said that the enterprise should implement the methods so as to

become an effective firm with high annual turnover and less operating and non operating

expenses.

Framing managerial decisions: Management should implement better decisions so as to

achieve the organisational structure which comprises of each and every activity and

elements which may lead to success and positive results so that the organisation can

achieve the results which are positive And they will get what their strategies are aimed

at. Managerial decisions should be based on some ethical and credible data and

information so that the decisions will lead the Agmet into the right path towards

successful destinations(Macintoshand and Quattrone, 2010).

3

of behaviours of buyers to different prices by which company gets to know how buyers will react

to prices of products and services provided by the company. This helps company to decide

pricing in order to maximize their profits with satisfaction of consumers. Pricing strategy of

Agmet can be done by segmenting customers. This can be done by identifying common needs,

common interests, similar lifestyles.

M1 Evaluate the benefits of management accounting systems and their application within Agmet

There are several benefits of management accounting system though which it can be

clearly observed that such techniques can be utilized in responding towards various problems

that may occur during several processes of management has been carried out. Such benefits are

mentioned below:

Improvement in cash flow: These methods and principles can assist an enterprise in

managing the cash flow from various activities. Cash flow statement shows three

sections out of which first one is about operating activities and the second one is about

investing and it is followed by financing activities(Nandan, 2010).

Reduction in expenses: There are lots of expenses in each and every functions and

activities of hence they are required to assist the enterprise in the proper functionality so

that the expenses can be controlled and managed as there is very less revenue earned

through the turnover of Agmet. So managerial personnels should implement these

methods and principles for coordinating with the expenses. Through reduction which is

made in negative cash flow efficiency at its best level and high productivity rate can be

achieved. Hence it can be said that the enterprise should implement the methods so as to

become an effective firm with high annual turnover and less operating and non operating

expenses.

Framing managerial decisions: Management should implement better decisions so as to

achieve the organisational structure which comprises of each and every activity and

elements which may lead to success and positive results so that the organisation can

achieve the results which are positive And they will get what their strategies are aimed

at. Managerial decisions should be based on some ethical and credible data and

information so that the decisions will lead the Agmet into the right path towards

successful destinations(Macintoshand and Quattrone, 2010).

3

Financial Planning : through implementation of the techniques and methods of financial

and cost accounting, management can introduce better cost structure which can be

considered as the optimum capital composition. In optimum capital structure the

financial resources are having less obligations but they are capable enough to generate

high returns in accordance with the plans and strategies which were previously

determined by the top level management of the cited firm.

P2 Explanation regarding different methods used for management accounting reporting

There are several methods which can be used by the cited enterprise for the management

of business affairs and to get the right return which have been estimated and observed by the top

level management of Agmet. Finally it can be said that the different methods which are used for

the financial reporting can help the management and other team who are responsible and

accountable for the preparation of the financial statements. As these methods presents the results

which are more credible and reliable hence they can predict the future image of enterprise and it

is the basic objective of financial reporting and its framework. There are several methods of

financial paling and reporting and these methods are mentioned below in detail with their

detailed features.

Job cost report: It is used to evaluate incur cost of organization from particular jobs. It

also compares actual cost and estimated cost in order to show profit margins. Agmet’s

manager can maintain these reports to avoid waste of resources and allocating resources.

It also helps to keep an eye on sales recovery, work in progress, value added and profit

summary.

Sales reports: A data maintained of calls made and sale of products and services during

specific period of time by manager or sales person. Daily check over sales cycle is a long

and complicated process that is why Agmet's sales manager can maintain sales report to

keep a track of customers interested, success rate, campaigning and closing rate.

Accounts receivable reports (AR): It is account receivable aging, data that file unpaid

customer invoices and unused credit memos according to dates. The company can use

this as an indicator to determine financial health of its customers. With the help of AR,

manager can maintain a snap shot of outstanding money due from the consumer and

create right credit extending decisions.

4

and cost accounting, management can introduce better cost structure which can be

considered as the optimum capital composition. In optimum capital structure the

financial resources are having less obligations but they are capable enough to generate

high returns in accordance with the plans and strategies which were previously

determined by the top level management of the cited firm.

P2 Explanation regarding different methods used for management accounting reporting

There are several methods which can be used by the cited enterprise for the management

of business affairs and to get the right return which have been estimated and observed by the top

level management of Agmet. Finally it can be said that the different methods which are used for

the financial reporting can help the management and other team who are responsible and

accountable for the preparation of the financial statements. As these methods presents the results

which are more credible and reliable hence they can predict the future image of enterprise and it

is the basic objective of financial reporting and its framework. There are several methods of

financial paling and reporting and these methods are mentioned below in detail with their

detailed features.

Job cost report: It is used to evaluate incur cost of organization from particular jobs. It

also compares actual cost and estimated cost in order to show profit margins. Agmet’s

manager can maintain these reports to avoid waste of resources and allocating resources.

It also helps to keep an eye on sales recovery, work in progress, value added and profit

summary.

Sales reports: A data maintained of calls made and sale of products and services during

specific period of time by manager or sales person. Daily check over sales cycle is a long

and complicated process that is why Agmet's sales manager can maintain sales report to

keep a track of customers interested, success rate, campaigning and closing rate.

Accounts receivable reports (AR): It is account receivable aging, data that file unpaid

customer invoices and unused credit memos according to dates. The company can use

this as an indicator to determine financial health of its customers. With the help of AR,

manager can maintain a snap shot of outstanding money due from the consumer and

create right credit extending decisions.

4

Inventory management reports: It is a synopsis of items belonging to an organization

inclusive account of stock and supply. Manager should maintain inventory reports in

order to improve productivity in store and also enables Agmet to improve efficiency of

ordering and delivery through proper inventory management.

Ratio Analysis: ratio analysis can be presented as the techniques which in fact consist of

ratios and other calculative tasks(Lukkaand and Modell, 2010). These calculations and

task are scientific and universally accepted hence it can be said that through using the

ratio analysis the management can lead to organisational benefits and they can frame

better strategies and reporting framework through optimizing the profitability, efficiency

and turnover ratios. As through it they can easily estimate that whether they are capable

enough to pay off the debts of the enterprise so that goodwill of Agmet in chemical

market can be maintained.

Fund Flow Analysis: This analysis is done on a statement which contain the working over

the working capital and it also consists of the tools through which the sources and

application of funds can be targeted and calculated easily so that the managerial

personnels can control over the different areas in which the sources have been utilized.

So far as the matter of sources from where the finance and funding is acquired then it can

said that better steps can be taken by the top managerial and middle level managerial

personnels for acquiring the finance as well as they can get better sources through which

they can acquire the funds(Luftand and Shields, 2010).

Cash flow analysis: Cash flow analysis and its controls can be applied in the top

managerial activities as through it they can manage the cash inflow and cash out flow. As

the cash flow statement consists of three sections hence it can be said that there are three

segments through which the managerial personnel’s can observe that how much fund or

cash is utilized in which activity. Further they can observe that how much cash is in

category of inflow and how much is in the category of outflow (Kihn and Ihantola, 2015).

Operating activities and its cash flow can assist them to make strategies and decisions

regarding the operational activities and through investing activities they can find out the

total cash used or generated through investing activities. Further the third section of cash

flow is all about the financing activity so the cash flow which is generated from the

activities of finance can lead to take decisions in reference of financial planning. Hence

5

inclusive account of stock and supply. Manager should maintain inventory reports in

order to improve productivity in store and also enables Agmet to improve efficiency of

ordering and delivery through proper inventory management.

Ratio Analysis: ratio analysis can be presented as the techniques which in fact consist of

ratios and other calculative tasks(Lukkaand and Modell, 2010). These calculations and

task are scientific and universally accepted hence it can be said that through using the

ratio analysis the management can lead to organisational benefits and they can frame

better strategies and reporting framework through optimizing the profitability, efficiency

and turnover ratios. As through it they can easily estimate that whether they are capable

enough to pay off the debts of the enterprise so that goodwill of Agmet in chemical

market can be maintained.

Fund Flow Analysis: This analysis is done on a statement which contain the working over

the working capital and it also consists of the tools through which the sources and

application of funds can be targeted and calculated easily so that the managerial

personnels can control over the different areas in which the sources have been utilized.

So far as the matter of sources from where the finance and funding is acquired then it can

said that better steps can be taken by the top managerial and middle level managerial

personnels for acquiring the finance as well as they can get better sources through which

they can acquire the funds(Luftand and Shields, 2010).

Cash flow analysis: Cash flow analysis and its controls can be applied in the top

managerial activities as through it they can manage the cash inflow and cash out flow. As

the cash flow statement consists of three sections hence it can be said that there are three

segments through which the managerial personnel’s can observe that how much fund or

cash is utilized in which activity. Further they can observe that how much cash is in

category of inflow and how much is in the category of outflow (Kihn and Ihantola, 2015).

Operating activities and its cash flow can assist them to make strategies and decisions

regarding the operational activities and through investing activities they can find out the

total cash used or generated through investing activities. Further the third section of cash

flow is all about the financing activity so the cash flow which is generated from the

activities of finance can lead to take decisions in reference of financial planning. Hence

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

it can be said that cash flow analysis techniques can be used for can be said that the

management should utilize the methods of financial and cost accounting for getting better

results (Lowe and De Loo, 2014).

D1 Critical evaluation about how management accounting systems and management accounting

reporting is integrated within organisational processes

Management accounting system can be integrated into the the organisation for managing

the operations of business entity. As Agmet is a small business enterprise which is in fact dealing

in chemical productionj(Kaplan and Atkinson, 2015). As it is having a high competitive market

just because of this they are required to make a brief plan in which the techniques and methods

of management accounting should be integrated in order to manage the activities so that the

management can get effective results with appropriate line up of different principles. They

should make an organisational composition in which each accountable person from each and

every department should work upon their operations effectively through optimizing the

proficiencies of cost accounting. As managerial decisions can be taken only by the managers due

to which it can be proved that management accounting and its tools cannot replace the

managerial personnels. But they can assist them in taking the right decisions and to frame right

conclusion towards the targets and goals. Reporting should be integrated in the accounting

system so that the stakeholders can get right information and they can achieve better decision

making so that management can get the right targets and they can also get the right objectives

which can allow them to survive in the competitive market of the UK. They should utilize the

tools for planning and forecasting like budgetary control for managing the expenditures in

different areas. As they can prepare the sales budget through which they can decide that how

much they have to sale in a given time period and through which what return or revenue they can

get. Other than sales budget they can also utilize the tool of production budget through which

they can clearly estimate that how much quantity of chemicals they are required to produce for

meeting the level of requirement of chemical as per the buyer behaviour in the open market of

UK and other markets at which the cited enterprise is dealing(Jansen, 2011). Financial budget

and cash flow budget shows two different areas in which this can be integrated. First one shows

the finance department of company so it can be clearly observed and advised to use financial

budget in the finance department of Agmet so that they can calculate that how much fund is to be

deposited or invested at which responsibility centres. Further through cash flow budget they can

6

management should utilize the methods of financial and cost accounting for getting better

results (Lowe and De Loo, 2014).

D1 Critical evaluation about how management accounting systems and management accounting

reporting is integrated within organisational processes

Management accounting system can be integrated into the the organisation for managing

the operations of business entity. As Agmet is a small business enterprise which is in fact dealing

in chemical productionj(Kaplan and Atkinson, 2015). As it is having a high competitive market

just because of this they are required to make a brief plan in which the techniques and methods

of management accounting should be integrated in order to manage the activities so that the

management can get effective results with appropriate line up of different principles. They

should make an organisational composition in which each accountable person from each and

every department should work upon their operations effectively through optimizing the

proficiencies of cost accounting. As managerial decisions can be taken only by the managers due

to which it can be proved that management accounting and its tools cannot replace the

managerial personnels. But they can assist them in taking the right decisions and to frame right

conclusion towards the targets and goals. Reporting should be integrated in the accounting

system so that the stakeholders can get right information and they can achieve better decision

making so that management can get the right targets and they can also get the right objectives

which can allow them to survive in the competitive market of the UK. They should utilize the

tools for planning and forecasting like budgetary control for managing the expenditures in

different areas. As they can prepare the sales budget through which they can decide that how

much they have to sale in a given time period and through which what return or revenue they can

get. Other than sales budget they can also utilize the tool of production budget through which

they can clearly estimate that how much quantity of chemicals they are required to produce for

meeting the level of requirement of chemical as per the buyer behaviour in the open market of

UK and other markets at which the cited enterprise is dealing(Jansen, 2011). Financial budget

and cash flow budget shows two different areas in which this can be integrated. First one shows

the finance department of company so it can be clearly observed and advised to use financial

budget in the finance department of Agmet so that they can calculate that how much fund is to be

deposited or invested at which responsibility centres. Further through cash flow budget they can

6

clearly estimate that how much investment is tob be made by the cited enterprise in the

operating, investing and financing activities.

TASK 2

P3 & M2 Preparation of income statements as per the method of absorption and marginal costing

techniques

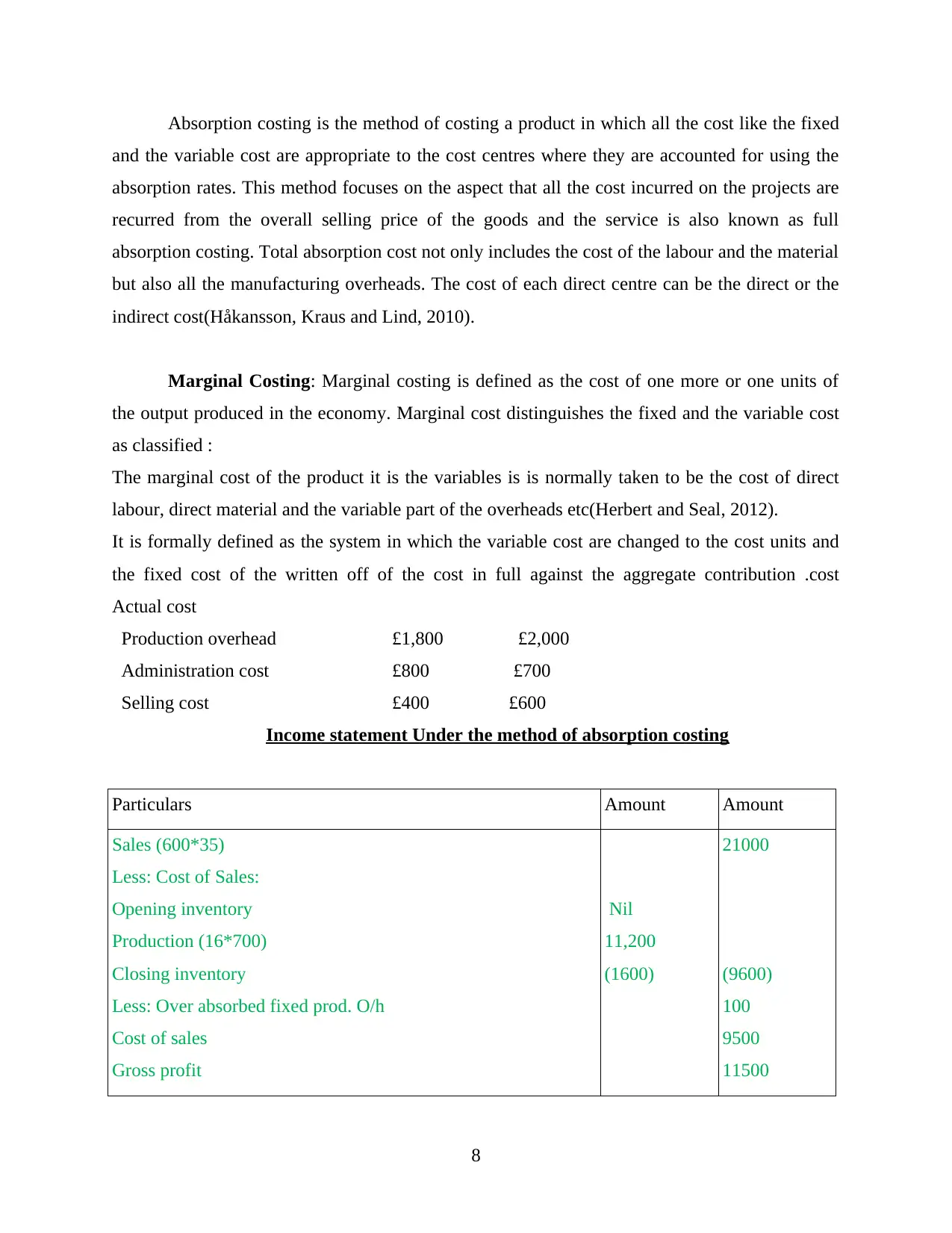

Absorption Costing:

Absorption costing is the method of costing a product in which all the cost like the fixed

and the variable cost are appropriate to the cost centres where they are accounted for using the

absorption rates. This method focuses on the aspect that all the cost incurred on the projects are

recurred from the overall selling price of the goods and the service is also known as full

absorption costing. Total absorption cost not only includes the cost of the labour and the material

but also all the manufacturing overheads. The cost of each direct centre can be the direct or the

indirect cost.

Marginal Costing: Marginal costing is defined as the cost of one more or one units of the

output produced in the economy(Hiebl, 2014). Marginal cost distinguishes the fixed and

the variable cost as classified: The marginal cost of the product it is the variables is is

normally taken to be the cost of direct labour, direct material and the variable part of the

overheads etc. It is formally defined as the system in which the variable cost are changed

to the cost units and the fixed cost of the written off of the cost in full against the

aggregate contribution .

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted Absorption Costing:

7

operating, investing and financing activities.

TASK 2

P3 & M2 Preparation of income statements as per the method of absorption and marginal costing

techniques

Absorption Costing:

Absorption costing is the method of costing a product in which all the cost like the fixed

and the variable cost are appropriate to the cost centres where they are accounted for using the

absorption rates. This method focuses on the aspect that all the cost incurred on the projects are

recurred from the overall selling price of the goods and the service is also known as full

absorption costing. Total absorption cost not only includes the cost of the labour and the material

but also all the manufacturing overheads. The cost of each direct centre can be the direct or the

indirect cost.

Marginal Costing: Marginal costing is defined as the cost of one more or one units of the

output produced in the economy(Hiebl, 2014). Marginal cost distinguishes the fixed and

the variable cost as classified: The marginal cost of the product it is the variables is is

normally taken to be the cost of direct labour, direct material and the variable part of the

overheads etc. It is formally defined as the system in which the variable cost are changed

to the cost units and the fixed cost of the written off of the cost in full against the

aggregate contribution .

Selling price £35

Unit costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted Absorption Costing:

7

Absorption costing is the method of costing a product in which all the cost like the fixed

and the variable cost are appropriate to the cost centres where they are accounted for using the

absorption rates. This method focuses on the aspect that all the cost incurred on the projects are

recurred from the overall selling price of the goods and the service is also known as full

absorption costing. Total absorption cost not only includes the cost of the labour and the material

but also all the manufacturing overheads. The cost of each direct centre can be the direct or the

indirect cost(Håkansson, Kraus and Lind, 2010).

Marginal Costing: Marginal costing is defined as the cost of one more or one units of

the output produced in the economy. Marginal cost distinguishes the fixed and the variable cost

as classified :

The marginal cost of the product it is the variables is is normally taken to be the cost of direct

labour, direct material and the variable part of the overheads etc(Herbert and Seal, 2012).

It is formally defined as the system in which the variable cost are changed to the cost units and

the fixed cost of the written off of the cost in full against the aggregate contribution .cost

Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Income statement Under the method of absorption costing

Particulars Amount Amount

Sales (600*35)

Less: Cost of Sales:

Opening inventory

Production (16*700)

Closing inventory

Less: Over absorbed fixed prod. O/h

Cost of sales

Gross profit

Nil

11,200

(1600)

21000

(9600)

100

9500

11500

8

and the variable cost are appropriate to the cost centres where they are accounted for using the

absorption rates. This method focuses on the aspect that all the cost incurred on the projects are

recurred from the overall selling price of the goods and the service is also known as full

absorption costing. Total absorption cost not only includes the cost of the labour and the material

but also all the manufacturing overheads. The cost of each direct centre can be the direct or the

indirect cost(Håkansson, Kraus and Lind, 2010).

Marginal Costing: Marginal costing is defined as the cost of one more or one units of

the output produced in the economy. Marginal cost distinguishes the fixed and the variable cost

as classified :

The marginal cost of the product it is the variables is is normally taken to be the cost of direct

labour, direct material and the variable part of the overheads etc(Herbert and Seal, 2012).

It is formally defined as the system in which the variable cost are changed to the cost units and

the fixed cost of the written off of the cost in full against the aggregate contribution .cost

Actual cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling cost £400 £600

Income statement Under the method of absorption costing

Particulars Amount Amount

Sales (600*35)

Less: Cost of Sales:

Opening inventory

Production (16*700)

Closing inventory

Less: Over absorbed fixed prod. O/h

Cost of sales

Gross profit

Nil

11,200

(1600)

21000

(9600)

100

9500

11500

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

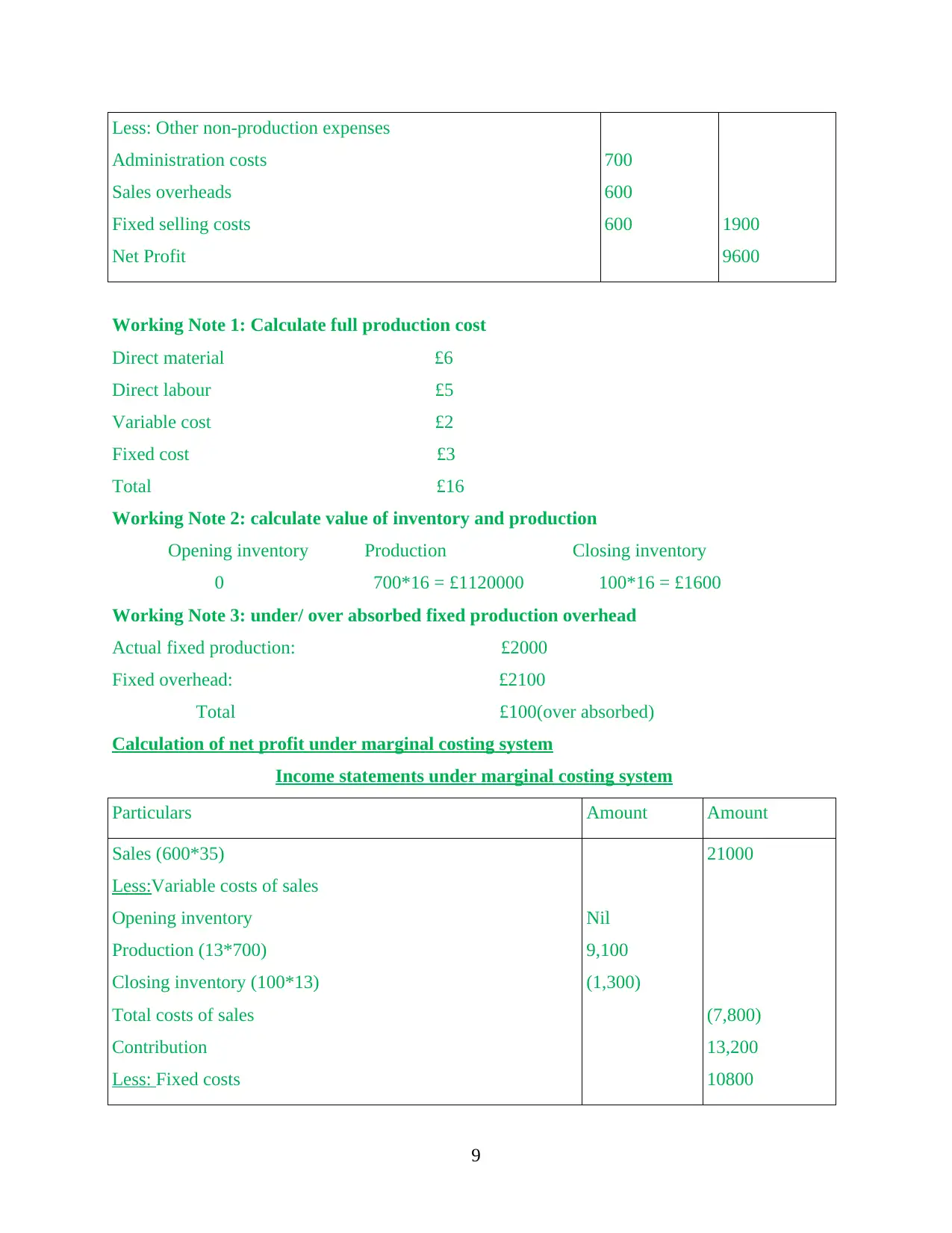

Less: Other non-production expenses

Administration costs

Sales overheads

Fixed selling costs

Net Profit

700

600

600 1900

9600

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*16 = £1120000 100*16 = £1600

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £2000

Fixed overhead: £2100

Total £100(over absorbed)

Calculation of net profit under marginal costing system

Income statements under marginal costing system

Particulars Amount Amount

Sales (600*35)

Less:Variable costs of sales

Opening inventory

Production (13*700)

Closing inventory (100*13)

Total costs of sales

Contribution

Less: Fixed costs

Nil

9,100

(1,300)

21000

(7,800)

13,200

10800

9

Administration costs

Sales overheads

Fixed selling costs

Net Profit

700

600

600 1900

9600

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*16 = £1120000 100*16 = £1600

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £2000

Fixed overhead: £2100

Total £100(over absorbed)

Calculation of net profit under marginal costing system

Income statements under marginal costing system

Particulars Amount Amount

Sales (600*35)

Less:Variable costs of sales

Opening inventory

Production (13*700)

Closing inventory (100*13)

Total costs of sales

Contribution

Less: Fixed costs

Nil

9,100

(1,300)

21000

(7,800)

13,200

10800

9

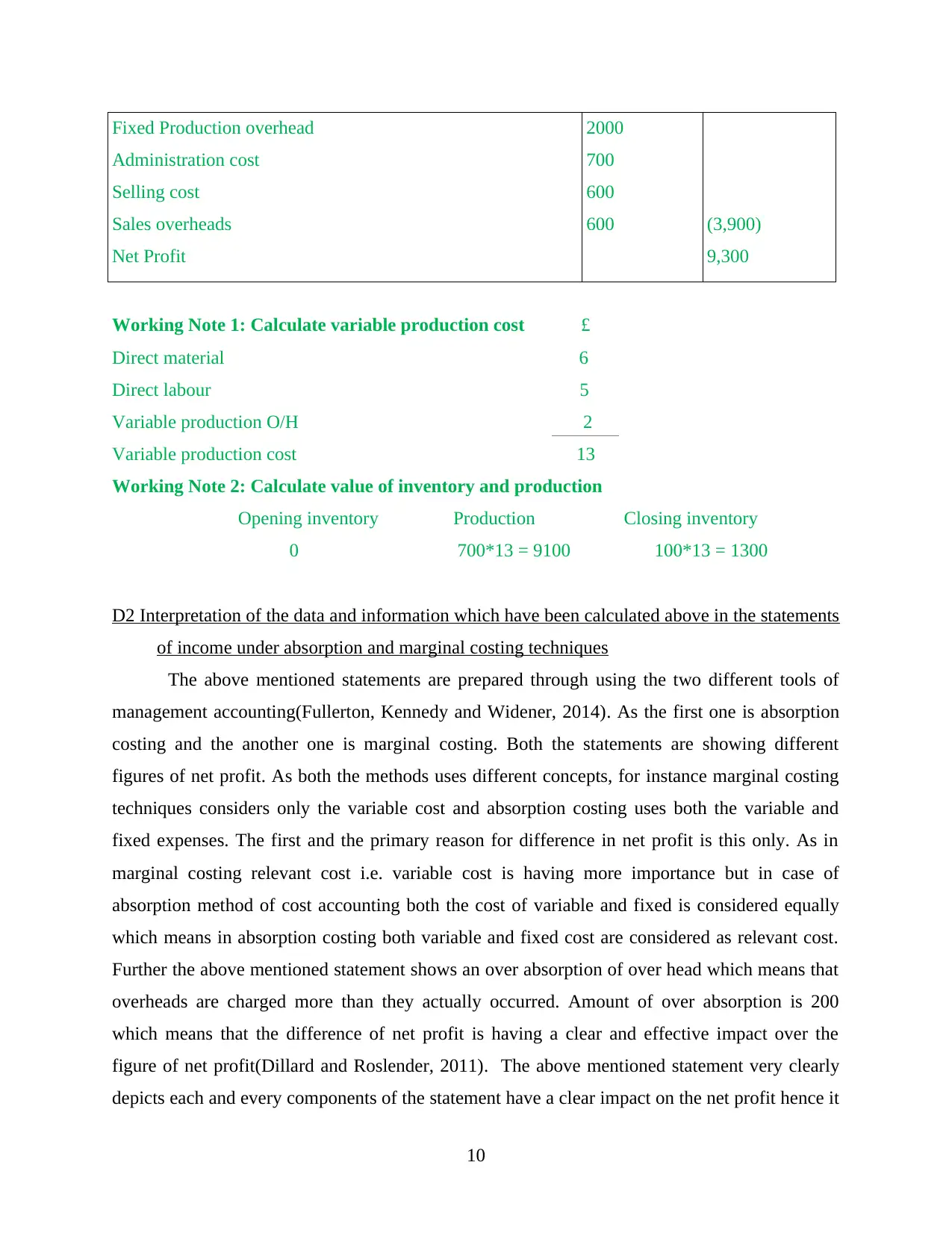

Fixed Production overhead

Administration cost

Selling cost

Sales overheads

Net Profit

2000

700

600

600 (3,900)

9,300

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 2

Variable production cost 13

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*13 = 9100 100*13 = 1300

D2 Interpretation of the data and information which have been calculated above in the statements

of income under absorption and marginal costing techniques

The above mentioned statements are prepared through using the two different tools of

management accounting(Fullerton, Kennedy and Widener, 2014). As the first one is absorption

costing and the another one is marginal costing. Both the statements are showing different

figures of net profit. As both the methods uses different concepts, for instance marginal costing

techniques considers only the variable cost and absorption costing uses both the variable and

fixed expenses. The first and the primary reason for difference in net profit is this only. As in

marginal costing relevant cost i.e. variable cost is having more importance but in case of

absorption method of cost accounting both the cost of variable and fixed is considered equally

which means in absorption costing both variable and fixed cost are considered as relevant cost.

Further the above mentioned statement shows an over absorption of over head which means that

overheads are charged more than they actually occurred. Amount of over absorption is 200

which means that the difference of net profit is having a clear and effective impact over the

figure of net profit(Dillard and Roslender, 2011). The above mentioned statement very clearly

depicts each and every components of the statement have a clear impact on the net profit hence it

10

Administration cost

Selling cost

Sales overheads

Net Profit

2000

700

600

600 (3,900)

9,300

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 2

Variable production cost 13

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*13 = 9100 100*13 = 1300

D2 Interpretation of the data and information which have been calculated above in the statements

of income under absorption and marginal costing techniques

The above mentioned statements are prepared through using the two different tools of

management accounting(Fullerton, Kennedy and Widener, 2014). As the first one is absorption

costing and the another one is marginal costing. Both the statements are showing different

figures of net profit. As both the methods uses different concepts, for instance marginal costing

techniques considers only the variable cost and absorption costing uses both the variable and

fixed expenses. The first and the primary reason for difference in net profit is this only. As in

marginal costing relevant cost i.e. variable cost is having more importance but in case of

absorption method of cost accounting both the cost of variable and fixed is considered equally

which means in absorption costing both variable and fixed cost are considered as relevant cost.

Further the above mentioned statement shows an over absorption of over head which means that

overheads are charged more than they actually occurred. Amount of over absorption is 200

which means that the difference of net profit is having a clear and effective impact over the

figure of net profit(Dillard and Roslender, 2011). The above mentioned statement very clearly

depicts each and every components of the statement have a clear impact on the net profit hence it

10

can be said that each and every components should be managed so that the ultimate net profit or

revenue can be managed as per the predetermined targets.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

There are several advantages and disadvantages of the planning tiools which can be used

by the Agmet for managing its financial and non financial resources. As through these planning

tools they can implement better planning and strategies through which they can frame a image of

itself in the targeted market(Contrafatto and Burns, 2013). They can optimize their financial

resources in a way through which they can frame strategies and plans for getting the clear cut

estimation about the future projects. Certain advantages and disadvantages of planning tools are

mentioned below:

Advantages

It helps in determining plans and fixes the way through which any particular target

could be achieved.

It helps in getting better coordination and better team work through which the

employees at all the three levels can achieve the targets by introducing team work and

effective strategy making.

It secures better understanding and improved coordination between the employees of

enterprise sop that the management can get objectives and goals.

Disadvantages

There are certain disadvantages also of budgetary control system as it is rigid in nature

hence in case of there is change in situation of enterprise then there may be chances

where

M3 Analysis over the use of different planning tools and their application for preparing and

forecasting budgets with special reference

Tools and technique used for planning budgets: There are different types of tools and

techniques that are used for planning the budget which are classified as:

Cost Aggregation: Cost aggregation is the calculation of the single cost based on work

breakdown structure. The work breakdown structure calculates the cost of each and every

item and thus it helps in planning the budgets for future(Cinquini and Tenucci, 2010).

The work package cost are than aggregated to achieve the higher competent level in the

11

revenue can be managed as per the predetermined targets.

TASK 3

P4 Advantages and disadvantages of different types of planning tools used for budgetary control

There are several advantages and disadvantages of the planning tiools which can be used

by the Agmet for managing its financial and non financial resources. As through these planning

tools they can implement better planning and strategies through which they can frame a image of

itself in the targeted market(Contrafatto and Burns, 2013). They can optimize their financial

resources in a way through which they can frame strategies and plans for getting the clear cut

estimation about the future projects. Certain advantages and disadvantages of planning tools are

mentioned below:

Advantages

It helps in determining plans and fixes the way through which any particular target

could be achieved.

It helps in getting better coordination and better team work through which the

employees at all the three levels can achieve the targets by introducing team work and

effective strategy making.

It secures better understanding and improved coordination between the employees of

enterprise sop that the management can get objectives and goals.

Disadvantages

There are certain disadvantages also of budgetary control system as it is rigid in nature

hence in case of there is change in situation of enterprise then there may be chances

where

M3 Analysis over the use of different planning tools and their application for preparing and

forecasting budgets with special reference

Tools and technique used for planning budgets: There are different types of tools and

techniques that are used for planning the budget which are classified as:

Cost Aggregation: Cost aggregation is the calculation of the single cost based on work

breakdown structure. The work breakdown structure calculates the cost of each and every

item and thus it helps in planning the budgets for future(Cinquini and Tenucci, 2010).

The work package cost are than aggregated to achieve the higher competent level in the

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

economy of the work breakdown structure and ultimately the entire project for the

economy.

Reserve Analysis: Reserve analysis is a technique that involves review of the project

management and the project plans. It is also used to determine the total budget of a

project. During reserve analysis a project is analysed from the cost overruns point and the

buffers are placed at their initial place and these buffers are called as contingency or

management reserves.

Contingency and Management Reserves: Contingency reserves are the buffers that

account for the risk factors that will occur .Example-Contingency reserves for the for the

lack of skills and human Resources in certain technological aspects. By looking at the

risk breakdown structure one will be able to get more categories that requires a

contingency reserve. Management reserve are used for the risk that have not been

identified. Every project is hit by the unidentified risk. The management reserve saves the

project from these critter. Regardless of the type of the reserve the amount of the buffer is

equal to the cost risk foreseen in the project or the activities at the individual level. The

norms of the organisation may also tell about the level of buffering. There is no particular

method to perform contingency reserves however there are certain guidelines that one

should made buffer according to the risk levels identified for the project or the individual

level activities

Expert judgement technique: Expert judgement technique refers to the technique in

which the judgement is based on the specific criteria or by the experts that have been

acquired in a specific knowledge area or product or a particular industry(Christ and

Burritt, 2013). Effective results can be ascertained through making judgement in

reference of organisational structure and towards the financial planning so that experts

can implement better techniques for managing the processes. This knowledge can be

provided by the members of the project teams or multiple members of the team or by the

team leaders. Expert judgement requires an expertise that is not present within the

project team and it is common for an external group of person with relevant skill and

knowledge based brought in for consultation. Judgement can be made through analysing

the techniques and the results of such techniques.

12

economy.

Reserve Analysis: Reserve analysis is a technique that involves review of the project

management and the project plans. It is also used to determine the total budget of a

project. During reserve analysis a project is analysed from the cost overruns point and the

buffers are placed at their initial place and these buffers are called as contingency or

management reserves.

Contingency and Management Reserves: Contingency reserves are the buffers that

account for the risk factors that will occur .Example-Contingency reserves for the for the

lack of skills and human Resources in certain technological aspects. By looking at the

risk breakdown structure one will be able to get more categories that requires a

contingency reserve. Management reserve are used for the risk that have not been

identified. Every project is hit by the unidentified risk. The management reserve saves the

project from these critter. Regardless of the type of the reserve the amount of the buffer is

equal to the cost risk foreseen in the project or the activities at the individual level. The

norms of the organisation may also tell about the level of buffering. There is no particular

method to perform contingency reserves however there are certain guidelines that one

should made buffer according to the risk levels identified for the project or the individual

level activities

Expert judgement technique: Expert judgement technique refers to the technique in

which the judgement is based on the specific criteria or by the experts that have been

acquired in a specific knowledge area or product or a particular industry(Christ and

Burritt, 2013). Effective results can be ascertained through making judgement in

reference of organisational structure and towards the financial planning so that experts

can implement better techniques for managing the processes. This knowledge can be

provided by the members of the project teams or multiple members of the team or by the

team leaders. Expert judgement requires an expertise that is not present within the

project team and it is common for an external group of person with relevant skill and

knowledge based brought in for consultation. Judgement can be made through analysing

the techniques and the results of such techniques.

12

Historical facts and data : Historical facts and data means that the facts are taken from

the past record for the present work project(Baldvinsdottir, Mitchell and Nørreklit, 2010).

Historical data is helpful in predicting the future of the company and the market as when

conducing predictive analysis

D3 & M4 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success

Sustainable success can be achieve through getting the right objectives at the right time so that

organisation could achieve the best alternatives. Organisation are adapting management

accounting system to solve financial problems:

The organisation are adapting the management system to solve the financial problems

because in management accounting the mangers uses the accounting information in order to

solve the problems and to decide about the matters of the organisation which aids their

management and t6he performance of the control functions(Bennett, Schaltegger and Zvezdov,

2013).

The financial problems of the organisation are discussed as:

Cash Flow: Every business has the problem of cash flow where the bills for the goods and

services are generated. The revenues just looks good only on the paper but the bank account

looks terrible. The business can run well if there is track of all the goods sold and received for

the proper growth of the organisation.

Funding: When the business is getting at the growth stage that the funds can be generated easily.

The proper decisions has to be taken about how the funds will be generated for the overall

activities of the organisation.

Economic cycles: When there is proper management system the right product or the service can

be the best sales method which will be struggling because of the outsides forces. Sometimes the

business or the economy can go into crises because the customer habits, taste and preferences

might change, changes in the demands of the product by the customers and the demand for the

product can fall or grow

13

the past record for the present work project(Baldvinsdottir, Mitchell and Nørreklit, 2010).

Historical data is helpful in predicting the future of the company and the market as when

conducing predictive analysis

D3 & M4 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success

Sustainable success can be achieve through getting the right objectives at the right time so that

organisation could achieve the best alternatives. Organisation are adapting management

accounting system to solve financial problems:

The organisation are adapting the management system to solve the financial problems

because in management accounting the mangers uses the accounting information in order to

solve the problems and to decide about the matters of the organisation which aids their

management and t6he performance of the control functions(Bennett, Schaltegger and Zvezdov,

2013).

The financial problems of the organisation are discussed as:

Cash Flow: Every business has the problem of cash flow where the bills for the goods and

services are generated. The revenues just looks good only on the paper but the bank account

looks terrible. The business can run well if there is track of all the goods sold and received for

the proper growth of the organisation.

Funding: When the business is getting at the growth stage that the funds can be generated easily.

The proper decisions has to be taken about how the funds will be generated for the overall

activities of the organisation.

Economic cycles: When there is proper management system the right product or the service can

be the best sales method which will be struggling because of the outsides forces. Sometimes the

business or the economy can go into crises because the customer habits, taste and preferences

might change, changes in the demands of the product by the customers and the demand for the

product can fall or grow

13

TASK 4

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems

Financial problems should be managed and controlled in order top achieve the targets

which have been set by the enterprise and its top level management. Sustainable success of the

organisation

Planning tools leads to the success of the organisation because planning helps to develop the

activities for the future growth and the development of the organisation. Sustainable success

leads to secure the resources for the future generations because they need a set of strategies to

develop the plans and the procedures for the future. It forms a set of strategies that build a solid

financial foundation for the economy(Busco and Scapens, 2011). The strategic plans should be

needed to achieve the goals of the organization and to fulfil its objectives. All the process of the

strategic planning should be designed in such a way that the value of the exercise lies in the

process itself. Strategic planning affords stakeholders in the organisation, the opportunities to

learn more about the organisation to share their perception of their strengths.

Key performance indicators (KPI): It is a measure which is used to measure the growth

of organizations, company, business according to goals and performance through profitability

measurement, analysis of solvency & liquidity position and others. Agemet can evaluate their

business efficiency through various KPIs and make better planning and prudent decisions for

maximizing their performance in later period.

Bench-marking: It is setting a ultimate goal or objective for business or organization by

measuring competition, uncertainties and likewise all the dimensions. Agmet need to identify all

the companies performing similar activities and compare their own profitability with that of

competitive organization. Manager can use this tool to measure performance using specific

indicator i.e. cost, sales, net return and others and make well plans and strategies to reach the idle

position.

Budgetary control: It is used to control cost and monitor operations by manager in a

financial year. For this Agment’s manager needs to create budget and have to set a plan to reach

company's financial goals that management need to complete within the year. Budget report

helps manager to keep an eye on unfavourable variances which must be removed by tight

controlling, regular administration and monitoring & cost-rationalized measures.

14

P5 Compare how organisations are adapting management accounting systems to respond to

financial problems

Financial problems should be managed and controlled in order top achieve the targets

which have been set by the enterprise and its top level management. Sustainable success of the

organisation

Planning tools leads to the success of the organisation because planning helps to develop the

activities for the future growth and the development of the organisation. Sustainable success

leads to secure the resources for the future generations because they need a set of strategies to

develop the plans and the procedures for the future. It forms a set of strategies that build a solid

financial foundation for the economy(Busco and Scapens, 2011). The strategic plans should be

needed to achieve the goals of the organization and to fulfil its objectives. All the process of the

strategic planning should be designed in such a way that the value of the exercise lies in the

process itself. Strategic planning affords stakeholders in the organisation, the opportunities to

learn more about the organisation to share their perception of their strengths.

Key performance indicators (KPI): It is a measure which is used to measure the growth

of organizations, company, business according to goals and performance through profitability

measurement, analysis of solvency & liquidity position and others. Agemet can evaluate their

business efficiency through various KPIs and make better planning and prudent decisions for

maximizing their performance in later period.

Bench-marking: It is setting a ultimate goal or objective for business or organization by

measuring competition, uncertainties and likewise all the dimensions. Agmet need to identify all

the companies performing similar activities and compare their own profitability with that of

competitive organization. Manager can use this tool to measure performance using specific

indicator i.e. cost, sales, net return and others and make well plans and strategies to reach the idle

position.

Budgetary control: It is used to control cost and monitor operations by manager in a

financial year. For this Agment’s manager needs to create budget and have to set a plan to reach

company's financial goals that management need to complete within the year. Budget report

helps manager to keep an eye on unfavourable variances which must be removed by tight

controlling, regular administration and monitoring & cost-rationalized measures.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial governance: It is a set of rules and regulations that company needs to follow

for accountability requirements. Finance manager need to focus on strategic resource plan and

annual budget in order to maintain governance on financial matters. It helps manager in risk

assessment, controlling activities, information and communication, monitoring.

CONCLUSION

From all the above report it can be concluded that the management accounting helps to

the organisation to taking the managerial decisions. Agmet company adapting the accounting

management and helps in solve the financial problems. With the help of management

accounting the information efficiency would not suffer and helps in taking the effective

decisions. There is a some difference in the income statement as per marginal cost and the

absorption techniques. And the accounting management helps and manage the finance . And to

control the and manage the finance is very important for the company. Through the accounting

management it is easy to planning, designing , implementing and controlling the financial data

for the good decision making process. From this the cash flow and the financial statements are

maintained. From all this it will easy to the managers of this company to preparing accurate

financial report on a particular time period. In this report various techniques and methods of

management accounting have been mentioned with their advantages and disadvantages.

15

for accountability requirements. Finance manager need to focus on strategic resource plan and

annual budget in order to maintain governance on financial matters. It helps manager in risk

assessment, controlling activities, information and communication, monitoring.

CONCLUSION

From all the above report it can be concluded that the management accounting helps to

the organisation to taking the managerial decisions. Agmet company adapting the accounting

management and helps in solve the financial problems. With the help of management

accounting the information efficiency would not suffer and helps in taking the effective

decisions. There is a some difference in the income statement as per marginal cost and the

absorption techniques. And the accounting management helps and manage the finance . And to

control the and manage the finance is very important for the company. Through the accounting

management it is easy to planning, designing , implementing and controlling the financial data

for the good decision making process. From this the cash flow and the financial statements are

maintained. From all this it will easy to the managers of this company to preparing accurate

financial report on a particular time period. In this report various techniques and methods of

management accounting have been mentioned with their advantages and disadvantages.

15

REFERENCES

Books and Journals

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Bhimani, A. and et. al., 2013. Introduction to Management Accounting. Pearson Higher Ed.

Bodie, Z., Kane, A. and Marcus, A. J., 2014. Investments, 10e. McGraw-Hill Education.

Boyns, T. and Edwards, J. R., 2013. A history of management accounting: The British

experience (Vol. 12). Routledge.

Breuer, A., Frumusanu, M. L. and Manciu, A., 2013. The role of management accounting in the

decision making process: Case study caras severin county. Annales Universitatis

Apulensis: Series Oeconomica. 15(2). p.355.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Chan, H.K., Wang, X. and Raffoni, A., 2014. An integrated approach for green design: Life-

cycle, fuzzy AHP and environmental management accounting. The British Accounting

Review. 46(4). pp.344-360.

Cleary, P., 2015. An empirical investigation of the impact of management accounting on

structural capital and business performance. Journal of Intellectual Capital. 16(3).

pp.566-586.

Cooper, D.J., Ezzamel, M. and Qu, S., 2016. Popularizing a management accounting idea: The

case of the balanced scorecard.

Dobroszek, J. and Szychta, A., 2015. Indicators as an Instrument of Measurement in

Management Accounting in Logistics Enterprises in Poland.Management and Business

Administration. 23(4). pp.11-33.

16

Books and Journals

Bebbington, J., Unerman, J. and O'Dwyer, B., 2014. Sustainability accounting and

accountability. Routledge.

Bhimani, A. and et. al., 2013. Introduction to Management Accounting. Pearson Higher Ed.

Bodie, Z., Kane, A. and Marcus, A. J., 2014. Investments, 10e. McGraw-Hill Education.

Boyns, T. and Edwards, J. R., 2013. A history of management accounting: The British

experience (Vol. 12). Routledge.

Breuer, A., Frumusanu, M. L. and Manciu, A., 2013. The role of management accounting in the

decision making process: Case study caras severin county. Annales Universitatis

Apulensis: Series Oeconomica. 15(2). p.355.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Chan, H.K., Wang, X. and Raffoni, A., 2014. An integrated approach for green design: Life-

cycle, fuzzy AHP and environmental management accounting. The British Accounting

Review. 46(4). pp.344-360.

Cleary, P., 2015. An empirical investigation of the impact of management accounting on

structural capital and business performance. Journal of Intellectual Capital. 16(3).

pp.566-586.

Cooper, D.J., Ezzamel, M. and Qu, S., 2016. Popularizing a management accounting idea: The

case of the balanced scorecard.

Dobroszek, J. and Szychta, A., 2015. Indicators as an Instrument of Measurement in

Management Accounting in Logistics Enterprises in Poland.Management and Business

Administration. 23(4). pp.11-33.

16

Fayard, D. and et. al., 2014. Interorganizational cost management in supply chains: Practices and

payoffs.Management Accounting Quarterly. 15(3). pp.1.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment.Accounting, Organizations and Society.

38(1). pp.50-71.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment.Accounting, Organizations and Society.

38(1). pp.50-71.