Comprehensive Management Accounting Report: Tech (UK) Analysis

VerifiedAdded on 2020/12/09

|15

|4002

|385

Report

AI Summary

This report provides a comprehensive overview of management accounting practices, focusing on the UK-based manufacturing company, Tech (UK). It begins by introducing the core concepts of management accounting, highlighting its role in providing valuable information for effective decision-making, differentiating it from financial accounting, and emphasizing its importance in enhancing organizational value. The report delves into various management accounting systems, including cost management (marginal, absorption, and normal costing), inventory management (FIFO, LIFO, and AVCO), and job costing. It also covers different types of managerial accounting reports, such as budget, accounts receivable, performance, and inventory management reports, along with their benefits. Furthermore, the report includes practical applications through cost calculations and income statement preparation using both marginal and absorption costing methods, providing detailed financial analysis relevant to Tech (UK)'s operations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

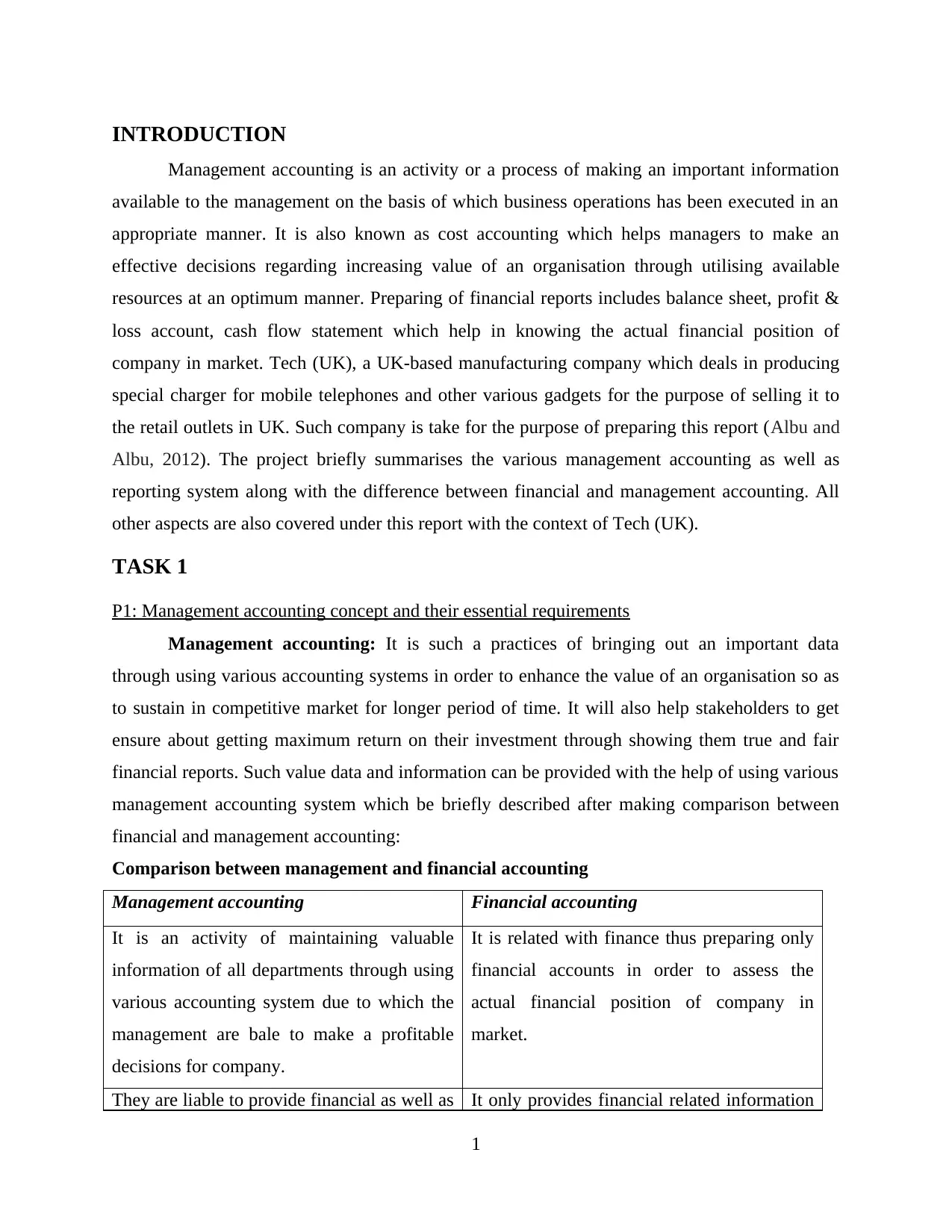

INTRODUCTION

Management accounting is an activity or a process of making an important information

available to the management on the basis of which business operations has been executed in an

appropriate manner. It is also known as cost accounting which helps managers to make an

effective decisions regarding increasing value of an organisation through utilising available

resources at an optimum manner. Preparing of financial reports includes balance sheet, profit &

loss account, cash flow statement which help in knowing the actual financial position of

company in market. Tech (UK), a UK-based manufacturing company which deals in producing

special charger for mobile telephones and other various gadgets for the purpose of selling it to

the retail outlets in UK. Such company is take for the purpose of preparing this report (Albu and

Albu, 2012). The project briefly summarises the various management accounting as well as

reporting system along with the difference between financial and management accounting. All

other aspects are also covered under this report with the context of Tech (UK).

TASK 1

P1: Management accounting concept and their essential requirements

Management accounting: It is such a practices of bringing out an important data

through using various accounting systems in order to enhance the value of an organisation so as

to sustain in competitive market for longer period of time. It will also help stakeholders to get

ensure about getting maximum return on their investment through showing them true and fair

financial reports. Such value data and information can be provided with the help of using various

management accounting system which be briefly described after making comparison between

financial and management accounting:

Comparison between management and financial accounting

Management accounting Financial accounting

It is an activity of maintaining valuable

information of all departments through using

various accounting system due to which the

management are bale to make a profitable

decisions for company.

It is related with finance thus preparing only

financial accounts in order to assess the

actual financial position of company in

market.

They are liable to provide financial as well as It only provides financial related information

1

Management accounting is an activity or a process of making an important information

available to the management on the basis of which business operations has been executed in an

appropriate manner. It is also known as cost accounting which helps managers to make an

effective decisions regarding increasing value of an organisation through utilising available

resources at an optimum manner. Preparing of financial reports includes balance sheet, profit &

loss account, cash flow statement which help in knowing the actual financial position of

company in market. Tech (UK), a UK-based manufacturing company which deals in producing

special charger for mobile telephones and other various gadgets for the purpose of selling it to

the retail outlets in UK. Such company is take for the purpose of preparing this report (Albu and

Albu, 2012). The project briefly summarises the various management accounting as well as

reporting system along with the difference between financial and management accounting. All

other aspects are also covered under this report with the context of Tech (UK).

TASK 1

P1: Management accounting concept and their essential requirements

Management accounting: It is such a practices of bringing out an important data

through using various accounting systems in order to enhance the value of an organisation so as

to sustain in competitive market for longer period of time. It will also help stakeholders to get

ensure about getting maximum return on their investment through showing them true and fair

financial reports. Such value data and information can be provided with the help of using various

management accounting system which be briefly described after making comparison between

financial and management accounting:

Comparison between management and financial accounting

Management accounting Financial accounting

It is an activity of maintaining valuable

information of all departments through using

various accounting system due to which the

management are bale to make a profitable

decisions for company.

It is related with finance thus preparing only

financial accounts in order to assess the

actual financial position of company in

market.

They are liable to provide financial as well as It only provides financial related information

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

non-financial data so as to make an effective

plans and policies.

thus tool less time as compared to Financial

accounts.

It helps in preparing accounts of all

department in order to provide sufficient

information to internal management of

company.

They are wholly liable to prepare financial

accounts which help stakeholders and

investors to make investment decision in

order to get profitable income in return.

Such management accounting, documents are

prepared only when there is need to

requirements of an organisation.

Finance department is liable to make decision

regarding preparation of financial report on

annual basis.

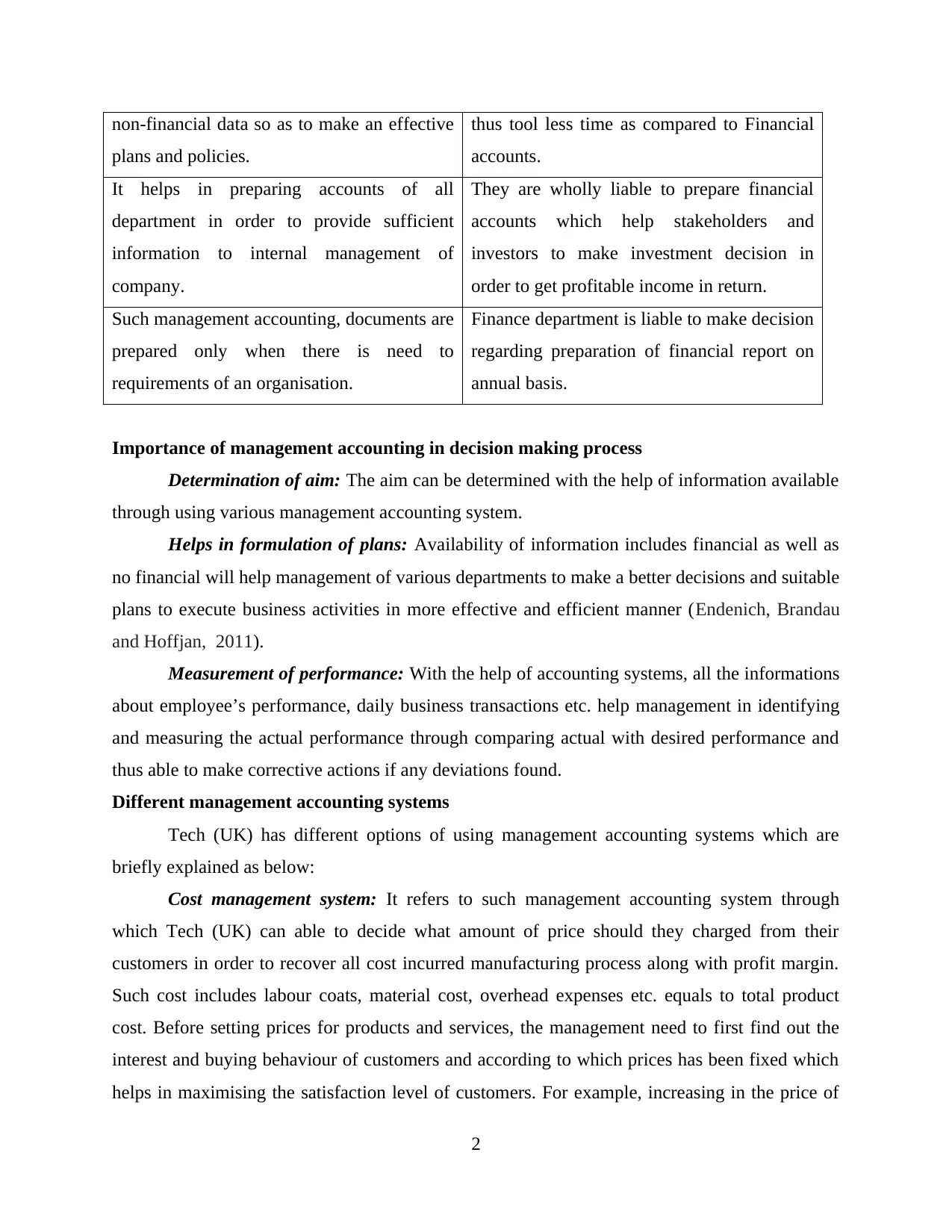

Importance of management accounting in decision making process

Determination of aim: The aim can be determined with the help of information available

through using various management accounting system.

Helps in formulation of plans: Availability of information includes financial as well as

no financial will help management of various departments to make a better decisions and suitable

plans to execute business activities in more effective and efficient manner (Endenich, Brandau

and Hoffjan, 2011).

Measurement of performance: With the help of accounting systems, all the informations

about employee’s performance, daily business transactions etc. help management in identifying

and measuring the actual performance through comparing actual with desired performance and

thus able to make corrective actions if any deviations found.

Different management accounting systems

Tech (UK) has different options of using management accounting systems which are

briefly explained as below:

Cost management system: It refers to such management accounting system through

which Tech (UK) can able to decide what amount of price should they charged from their

customers in order to recover all cost incurred manufacturing process along with profit margin.

Such cost includes labour coats, material cost, overhead expenses etc. equals to total product

cost. Before setting prices for products and services, the management need to first find out the

interest and buying behaviour of customers and according to which prices has been fixed which

helps in maximising the satisfaction level of customers. For example, increasing in the price of

2

plans and policies.

thus tool less time as compared to Financial

accounts.

It helps in preparing accounts of all

department in order to provide sufficient

information to internal management of

company.

They are wholly liable to prepare financial

accounts which help stakeholders and

investors to make investment decision in

order to get profitable income in return.

Such management accounting, documents are

prepared only when there is need to

requirements of an organisation.

Finance department is liable to make decision

regarding preparation of financial report on

annual basis.

Importance of management accounting in decision making process

Determination of aim: The aim can be determined with the help of information available

through using various management accounting system.

Helps in formulation of plans: Availability of information includes financial as well as

no financial will help management of various departments to make a better decisions and suitable

plans to execute business activities in more effective and efficient manner (Endenich, Brandau

and Hoffjan, 2011).

Measurement of performance: With the help of accounting systems, all the informations

about employee’s performance, daily business transactions etc. help management in identifying

and measuring the actual performance through comparing actual with desired performance and

thus able to make corrective actions if any deviations found.

Different management accounting systems

Tech (UK) has different options of using management accounting systems which are

briefly explained as below:

Cost management system: It refers to such management accounting system through

which Tech (UK) can able to decide what amount of price should they charged from their

customers in order to recover all cost incurred manufacturing process along with profit margin.

Such cost includes labour coats, material cost, overhead expenses etc. equals to total product

cost. Before setting prices for products and services, the management need to first find out the

interest and buying behaviour of customers and according to which prices has been fixed which

helps in maximising the satisfaction level of customers. For example, increasing in the price of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

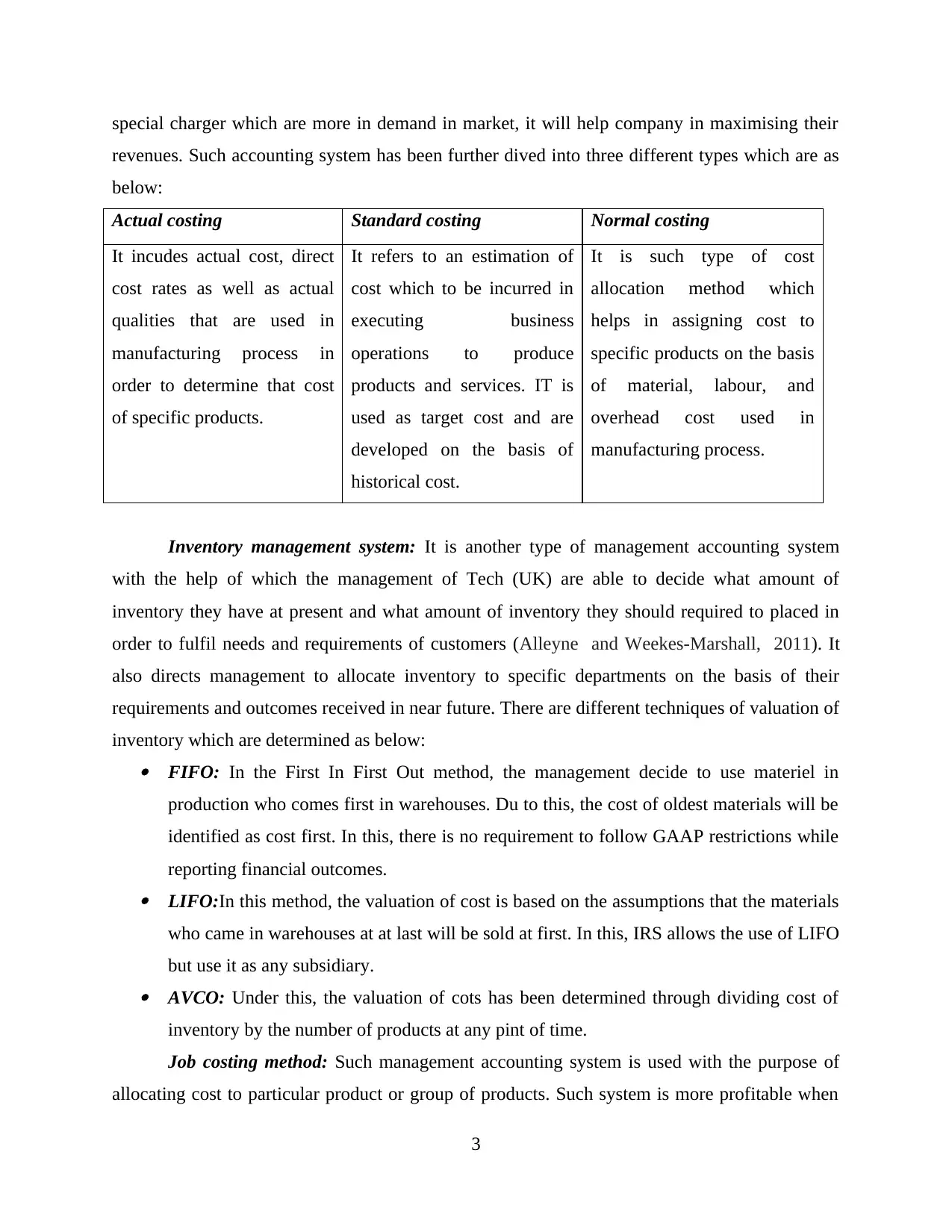

special charger which are more in demand in market, it will help company in maximising their

revenues. Such accounting system has been further dived into three different types which are as

below:

Actual costing Standard costing Normal costing

It incudes actual cost, direct

cost rates as well as actual

qualities that are used in

manufacturing process in

order to determine that cost

of specific products.

It refers to an estimation of

cost which to be incurred in

executing business

operations to produce

products and services. IT is

used as target cost and are

developed on the basis of

historical cost.

It is such type of cost

allocation method which

helps in assigning cost to

specific products on the basis

of material, labour, and

overhead cost used in

manufacturing process.

Inventory management system: It is another type of management accounting system

with the help of which the management of Tech (UK) are able to decide what amount of

inventory they have at present and what amount of inventory they should required to placed in

order to fulfil needs and requirements of customers (Alleyne and Weekes-Marshall, 2011). It

also directs management to allocate inventory to specific departments on the basis of their

requirements and outcomes received in near future. There are different techniques of valuation of

inventory which are determined as below: FIFO: In the First In First Out method, the management decide to use materiel in

production who comes first in warehouses. Du to this, the cost of oldest materials will be

identified as cost first. In this, there is no requirement to follow GAAP restrictions while

reporting financial outcomes. LIFO:In this method, the valuation of cost is based on the assumptions that the materials

who came in warehouses at at last will be sold at first. In this, IRS allows the use of LIFO

but use it as any subsidiary. AVCO: Under this, the valuation of cots has been determined through dividing cost of

inventory by the number of products at any pint of time.

Job costing method: Such management accounting system is used with the purpose of

allocating cost to particular product or group of products. Such system is more profitable when

3

revenues. Such accounting system has been further dived into three different types which are as

below:

Actual costing Standard costing Normal costing

It incudes actual cost, direct

cost rates as well as actual

qualities that are used in

manufacturing process in

order to determine that cost

of specific products.

It refers to an estimation of

cost which to be incurred in

executing business

operations to produce

products and services. IT is

used as target cost and are

developed on the basis of

historical cost.

It is such type of cost

allocation method which

helps in assigning cost to

specific products on the basis

of material, labour, and

overhead cost used in

manufacturing process.

Inventory management system: It is another type of management accounting system

with the help of which the management of Tech (UK) are able to decide what amount of

inventory they have at present and what amount of inventory they should required to placed in

order to fulfil needs and requirements of customers (Alleyne and Weekes-Marshall, 2011). It

also directs management to allocate inventory to specific departments on the basis of their

requirements and outcomes received in near future. There are different techniques of valuation of

inventory which are determined as below: FIFO: In the First In First Out method, the management decide to use materiel in

production who comes first in warehouses. Du to this, the cost of oldest materials will be

identified as cost first. In this, there is no requirement to follow GAAP restrictions while

reporting financial outcomes. LIFO:In this method, the valuation of cost is based on the assumptions that the materials

who came in warehouses at at last will be sold at first. In this, IRS allows the use of LIFO

but use it as any subsidiary. AVCO: Under this, the valuation of cots has been determined through dividing cost of

inventory by the number of products at any pint of time.

Job costing method: Such management accounting system is used with the purpose of

allocating cost to particular product or group of products. Such system is more profitable when

3

the company produce products of different nature. Through such system, the management are

able to track cost which includes material, labour cost etc. which are incurred in production

process. Allocation of cost is based on the future outcomes from particular products. For

example, if Tech (UK) produce chargers of two and three pin then such systems becomes more

profitable to company (Gond and et. al., 2012).

P2: Different types of managerial accounting reports along with their importance

The management of Tech (UK) should able to make an effective plans and policies on the

basis of information available through using various types of management accounting reports.

Such types of reports includes:

Budget report: It includes all important information regarding the aspects and elements

which are required to produce quality products and services for the customers. Such kind of

reports helps management in allocation of cost to specific business activities after analysing the

outcomes that may received in future. It is prepared on the basis of previous year budget in order

to avoid any discrepancies occurred in executing business activities in previous years.

Account receivable report: Such reports is prepared to record all information about the

unpaid debtors of an organisation with an aim of recovering unpaid amount from them on

particular data. In order to assess the unpaid amount, the management need to make

segmentation of bill invoices according to their due date. This wilt direct managers to make

changes in their credit polices so that debtors should not delay in making payments to company.

Performance report: It is such kind of reports which is prepared to record the

performance of each departments of an organisation so as to confirm whether they are performed

according to the pre-determined plans or not. It helps management in finding out the deviations if

any which restricts employees to give their best. For example, to main financial performance of

Tech (UK), the management can use various financial tools such as Key Performance Indicators,

Balance Scorecard Approach etc.

Inventory management report: Such reports helps in updating management about the

inventory level the company have at present and on the basis of which they took decision

whether need to placed order of inventory to suppliers or not in order to meet needs and demands

of market. This will help in supplying adequate level of stock in market so as to avoid situation

of shortage (Nixon and Burns, 2012).

Benefits or importance of management accounting reports

4

able to track cost which includes material, labour cost etc. which are incurred in production

process. Allocation of cost is based on the future outcomes from particular products. For

example, if Tech (UK) produce chargers of two and three pin then such systems becomes more

profitable to company (Gond and et. al., 2012).

P2: Different types of managerial accounting reports along with their importance

The management of Tech (UK) should able to make an effective plans and policies on the

basis of information available through using various types of management accounting reports.

Such types of reports includes:

Budget report: It includes all important information regarding the aspects and elements

which are required to produce quality products and services for the customers. Such kind of

reports helps management in allocation of cost to specific business activities after analysing the

outcomes that may received in future. It is prepared on the basis of previous year budget in order

to avoid any discrepancies occurred in executing business activities in previous years.

Account receivable report: Such reports is prepared to record all information about the

unpaid debtors of an organisation with an aim of recovering unpaid amount from them on

particular data. In order to assess the unpaid amount, the management need to make

segmentation of bill invoices according to their due date. This wilt direct managers to make

changes in their credit polices so that debtors should not delay in making payments to company.

Performance report: It is such kind of reports which is prepared to record the

performance of each departments of an organisation so as to confirm whether they are performed

according to the pre-determined plans or not. It helps management in finding out the deviations if

any which restricts employees to give their best. For example, to main financial performance of

Tech (UK), the management can use various financial tools such as Key Performance Indicators,

Balance Scorecard Approach etc.

Inventory management report: Such reports helps in updating management about the

inventory level the company have at present and on the basis of which they took decision

whether need to placed order of inventory to suppliers or not in order to meet needs and demands

of market. This will help in supplying adequate level of stock in market so as to avoid situation

of shortage (Nixon and Burns, 2012).

Benefits or importance of management accounting reports

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reduction of cost: It helps management in identifying the aspects which may affect the

business operations due to which the cost of company may increased. Such reports directs

management to make a suitable plans to eliminate such aspects in order to run business more

successful and execute as per the standards so as to reduce cost of operations.

Decision making: It helps management in getting information about financial and non-

financial transactions due to which management can easily able to find out the actual financial

position of company. It further help in formulating an effective plans, enhancing performance of

employees, and handle risk factors which makes positive impact on company’s productivity and

profitability (Renz, 2016).

TASK 2

P3: Calculation of cost and preparation of income statement

Cost: It may be defined as value of money which is to acquire or produce something in

standard quality in order to maximise satisfaction level of customers. Thus, irt may be increased

as per the requirements in production process. Example, labour cost cost, material cost, overhead

cost etc. which are incurred in manufacturing quality products.

Marginal costing: It refers to an increment cost which is used to produce one additional

unit of products item. Such cost in considered as variable costs which includes labour and

materiel cost. Using marginal cost method, the fixed cost should be ignore and only variable cost

has been taken into account. Through this, the profit of Tech (UK) may goes up.

Absorption costing: It includes all cost and expenses associated with manufacturing a

specific product will be taken into account thus includes fixed as well as variable cost while

calculating cost for products. Such kind of costing are generally required by the accounting

standards in order to generate inventory valuations which is stated in balance sheet of an

organisation (Macintosh and Quattrone, 2010).

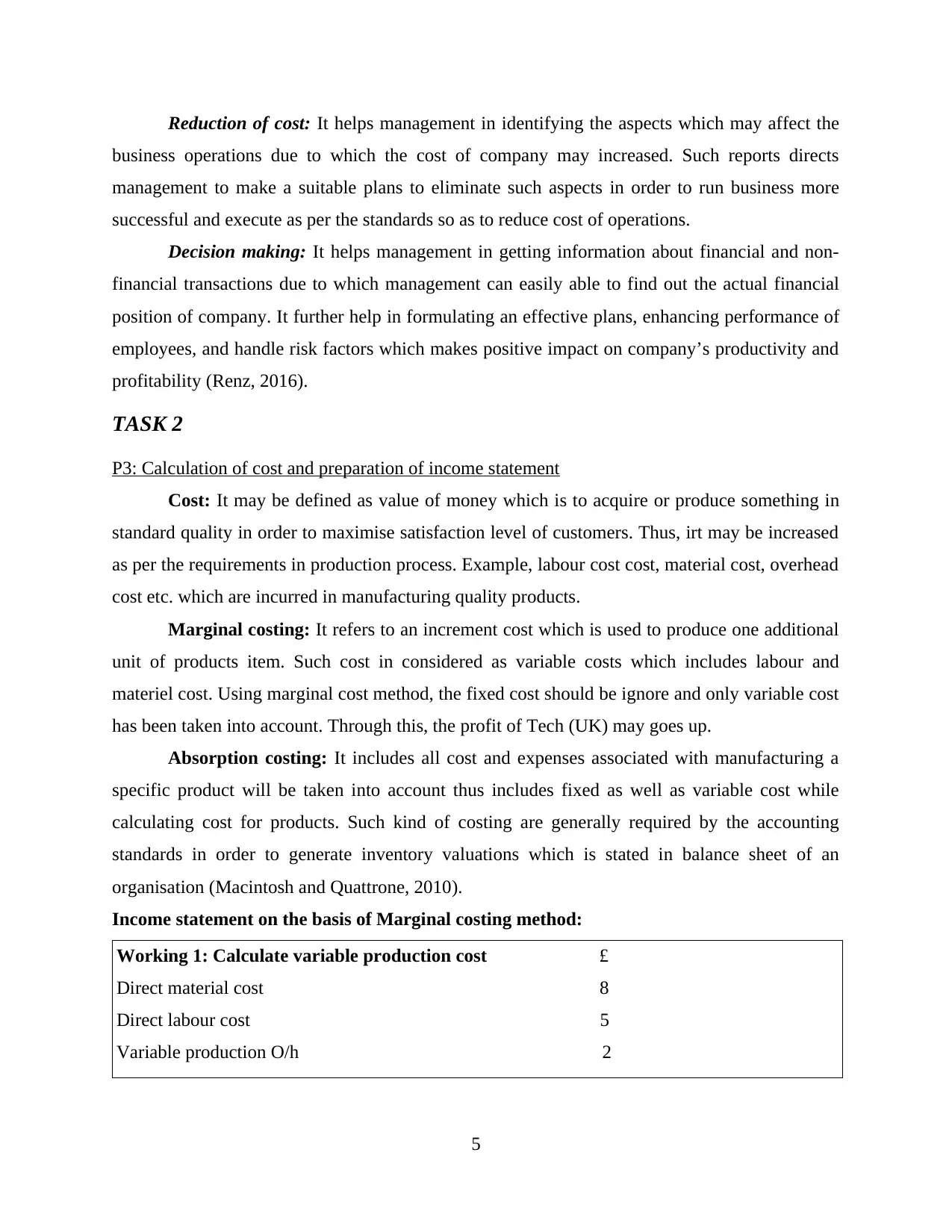

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

5

business operations due to which the cost of company may increased. Such reports directs

management to make a suitable plans to eliminate such aspects in order to run business more

successful and execute as per the standards so as to reduce cost of operations.

Decision making: It helps management in getting information about financial and non-

financial transactions due to which management can easily able to find out the actual financial

position of company. It further help in formulating an effective plans, enhancing performance of

employees, and handle risk factors which makes positive impact on company’s productivity and

profitability (Renz, 2016).

TASK 2

P3: Calculation of cost and preparation of income statement

Cost: It may be defined as value of money which is to acquire or produce something in

standard quality in order to maximise satisfaction level of customers. Thus, irt may be increased

as per the requirements in production process. Example, labour cost cost, material cost, overhead

cost etc. which are incurred in manufacturing quality products.

Marginal costing: It refers to an increment cost which is used to produce one additional

unit of products item. Such cost in considered as variable costs which includes labour and

materiel cost. Using marginal cost method, the fixed cost should be ignore and only variable cost

has been taken into account. Through this, the profit of Tech (UK) may goes up.

Absorption costing: It includes all cost and expenses associated with manufacturing a

specific product will be taken into account thus includes fixed as well as variable cost while

calculating cost for products. Such kind of costing are generally required by the accounting

standards in order to generate inventory valuations which is stated in balance sheet of an

organisation (Macintosh and Quattrone, 2010).

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

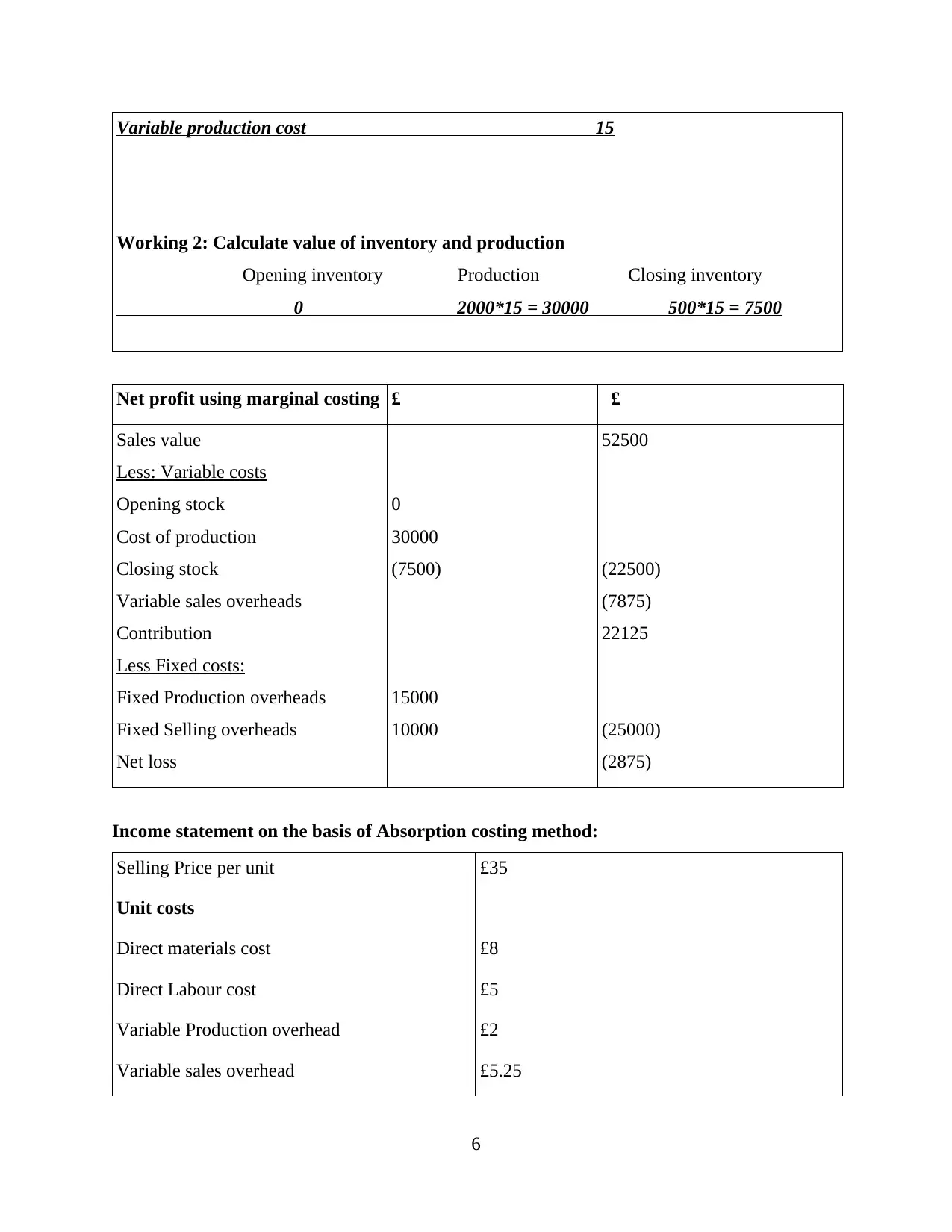

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

6

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Cost of production

Closing stock

Variable sales overheads

Contribution

Less Fixed costs:

Fixed Production overheads

Fixed Selling overheads

Net loss

0

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

(2875)

Income statement on the basis of Absorption costing method:

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

6

Budgeted production for the period is 3000

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000 and Actual cost is £7875

7

units

Fixed cost for a month:

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000 and Actual cost is £7875

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

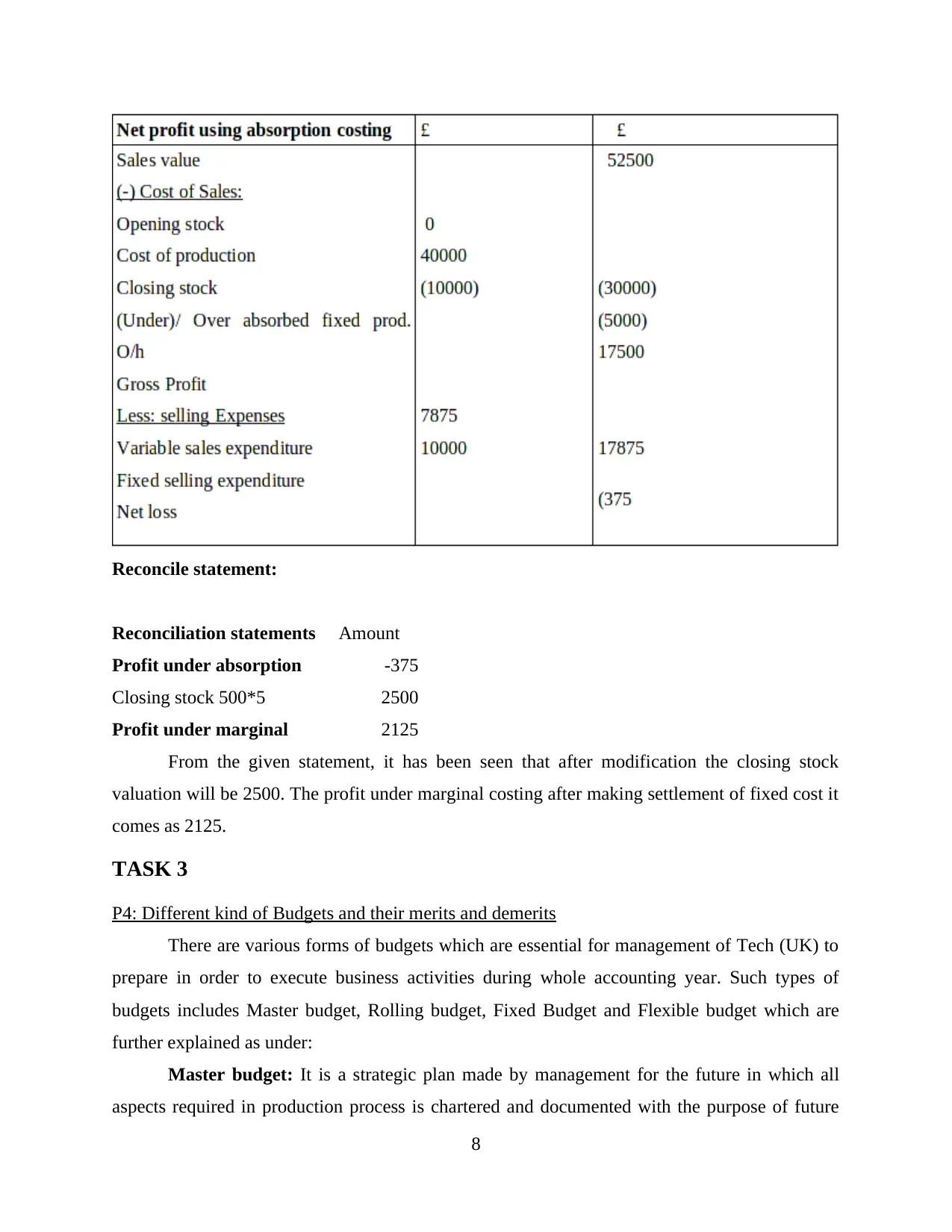

Reconcile statement:

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

From the given statement, it has been seen that after modification the closing stock

valuation will be 2500. The profit under marginal costing after making settlement of fixed cost it

comes as 2125.

TASK 3

P4: Different kind of Budgets and their merits and demerits

There are various forms of budgets which are essential for management of Tech (UK) to

prepare in order to execute business activities during whole accounting year. Such types of

budgets includes Master budget, Rolling budget, Fixed Budget and Flexible budget which are

further explained as under:

Master budget: It is a strategic plan made by management for the future in which all

aspects required in production process is chartered and documented with the purpose of future

8

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

From the given statement, it has been seen that after modification the closing stock

valuation will be 2500. The profit under marginal costing after making settlement of fixed cost it

comes as 2125.

TASK 3

P4: Different kind of Budgets and their merits and demerits

There are various forms of budgets which are essential for management of Tech (UK) to

prepare in order to execute business activities during whole accounting year. Such types of

budgets includes Master budget, Rolling budget, Fixed Budget and Flexible budget which are

further explained as under:

Master budget: It is a strategic plan made by management for the future in which all

aspects required in production process is chartered and documented with the purpose of future

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

predications. It includes cash forecast, budgeted financial statements and a financial plan. Thus,

such kind of budget is prepared in either monthly or quality basis and cover company;s whole

fiscal year (Fullerton, Kennedy and Widener, 2013). Advantage: It helps in coordinating all other budget and to decide short term goals of

company. Te conflicts can also be resolved among the departments as it is consolidation

of all the functional budgets.

Disadvantage: It is prepared on the basis of forecasting thus they are weak to uncertainty

in the environment.

Rolling Budget: Such budget is newly prepared after revising the financial plans for the

upcoming accounting period replacing the previous one so as to continuing the budgeting

system. Advantage: Budgets are reassessed on regular basis thus should be more reliable and

accurate. Along with this, Uncertainty are also get reduce due to revising financial plans.

Disadvantage: Such budget requires more time and money due to preparing number of

budget during the fiscal year.

Fixed Budget: It is one which is prepared on the basis of specific criteria without any

provision for any changes at any point during the time covered by the budget. It directs

management not take make changes in budget on the basis of contingent situation and execute

business operation as per the predetermined plans. Advantage: With the help of such budget, the small sized company such as Tech (UK)

can able to achieve growth and success within shorter period of time (Nixon and Burns,

2012). Disadvantage: Sometimes due to rigidity of budget, the complex situation arises in the

process of execution of business activity may affected the result in adverse manner.

Flexible budget: It is such kind of budget which allows management to make changes

according to the changes in production and sale volume. Due to this, the management can able to

control cost of company. Advantage: It helps in analysing the performance of each department of an organisation

and also also helps in evaluating the impact of changing volume of activities on profit

and cash position.

9

such kind of budget is prepared in either monthly or quality basis and cover company;s whole

fiscal year (Fullerton, Kennedy and Widener, 2013). Advantage: It helps in coordinating all other budget and to decide short term goals of

company. Te conflicts can also be resolved among the departments as it is consolidation

of all the functional budgets.

Disadvantage: It is prepared on the basis of forecasting thus they are weak to uncertainty

in the environment.

Rolling Budget: Such budget is newly prepared after revising the financial plans for the

upcoming accounting period replacing the previous one so as to continuing the budgeting

system. Advantage: Budgets are reassessed on regular basis thus should be more reliable and

accurate. Along with this, Uncertainty are also get reduce due to revising financial plans.

Disadvantage: Such budget requires more time and money due to preparing number of

budget during the fiscal year.

Fixed Budget: It is one which is prepared on the basis of specific criteria without any

provision for any changes at any point during the time covered by the budget. It directs

management not take make changes in budget on the basis of contingent situation and execute

business operation as per the predetermined plans. Advantage: With the help of such budget, the small sized company such as Tech (UK)

can able to achieve growth and success within shorter period of time (Nixon and Burns,

2012). Disadvantage: Sometimes due to rigidity of budget, the complex situation arises in the

process of execution of business activity may affected the result in adverse manner.

Flexible budget: It is such kind of budget which allows management to make changes

according to the changes in production and sale volume. Due to this, the management can able to

control cost of company. Advantage: It helps in analysing the performance of each department of an organisation

and also also helps in evaluating the impact of changing volume of activities on profit

and cash position.

9

Disadvantage: It requires extra amount of money to spend on business activities this

increasing cost of company.

Different pricing systems:

Price skimming: Through adopting such pricing strategy, the management first increases

the price of newly product in market and later on lowering the price due to giving tough

completion to their rivals.

Economy pricing: Through adopting of such strategy, the management always keep the

price of product lower with a motive of influencing buying behaviour of customers.

Cost plus pricing: Such strategy is made with the purpose of fixing an effective price of

product after considering total cost cost incurred in production which includes labour, material

and overhead cost (Ahadiat, 2013).

Full cost pricing: Such strategy includes direct cost incurred in production process so as

to setting up an effective price for products and services.

Marginal cost pricing: It includes additional cost incurred in manufacturing extra units

of items to the price of products.

Benefits of budget for planning and control:

It gives suitable direction to workers engaged in manufacturing activities to execute will

in order to achieve profitable outcomes.

It helps in educating employees about the importance of utilising available resources in

an optimum manner so as to produce quality products.

It helps in preparing management to face future difficulties so to execute pre-decided

future business activities without any interruptions or breakdowns.

TASK 4

P5: Contribution of management accounting systems to respond financial issues

It has been clearly seen from the given case study that Tech (UK) has suffering huge

losses in previous accounting year which may due to poor quality, insufficient support from co-

workers, ineffective strategies etc.

The major reason which are determined behind the loss of organisation includes low

quality of charger, lack of management etc. Advised by the financial manger of organisation is to

use the approach of Balance Scorecard which helps to to overcome from the issues. In

10

increasing cost of company.

Different pricing systems:

Price skimming: Through adopting such pricing strategy, the management first increases

the price of newly product in market and later on lowering the price due to giving tough

completion to their rivals.

Economy pricing: Through adopting of such strategy, the management always keep the

price of product lower with a motive of influencing buying behaviour of customers.

Cost plus pricing: Such strategy is made with the purpose of fixing an effective price of

product after considering total cost cost incurred in production which includes labour, material

and overhead cost (Ahadiat, 2013).

Full cost pricing: Such strategy includes direct cost incurred in production process so as

to setting up an effective price for products and services.

Marginal cost pricing: It includes additional cost incurred in manufacturing extra units

of items to the price of products.

Benefits of budget for planning and control:

It gives suitable direction to workers engaged in manufacturing activities to execute will

in order to achieve profitable outcomes.

It helps in educating employees about the importance of utilising available resources in

an optimum manner so as to produce quality products.

It helps in preparing management to face future difficulties so to execute pre-decided

future business activities without any interruptions or breakdowns.

TASK 4

P5: Contribution of management accounting systems to respond financial issues

It has been clearly seen from the given case study that Tech (UK) has suffering huge

losses in previous accounting year which may due to poor quality, insufficient support from co-

workers, ineffective strategies etc.

The major reason which are determined behind the loss of organisation includes low

quality of charger, lack of management etc. Advised by the financial manger of organisation is to

use the approach of Balance Scorecard which helps to to overcome from the issues. In

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.