Management Accounting: Income Statements, Planning Tools & MAS Role

VerifiedAdded on 2023/01/06

|15

|3221

|33

Report

AI Summary

This management accounting report provides a comprehensive analysis of income statements, planning tools, and the role of Management Accounting Systems (MAS) in solving financial issues. It begins with an overview of microeconomic techniques such as cost-volume-profit analysis and cost variance, then explores different costing methods including absorption and marginal costing. The report further examines budgetary control, cash budgets, and capital budgets, highlighting their benefits and drawbacks. Pricing strategies like penetration and skimming are discussed, along with strategic planning tools like SWOT analysis. The report concludes by addressing common monetary issues faced by businesses and how MAS can be utilized to solve them, emphasizing the importance of accurate accounting records and effective financial management. This student-contributed assignment is available on Desklib, offering valuable insights and examples for understanding key management accounting concepts.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

TASK 2...................................................................................................................................................3

P3. Measurement of income statements...................................................................................................3

M2. Accounting techniques to produce financial statements...................................................................8

D2. Interpretation of prepared financial statements.................................................................................8

TASK 3...................................................................................................................................................8

P4. Benefits and drawbacks of planning tool...........................................................................................8

TASK 4.................................................................................................................................................11

P5. Role of MAS to solve issues............................................................................................................11

M4. MAS to solve financial issue..........................................................................................................13

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

INTRODUCTION.......................................................................................................................................3

MAIN BODY..............................................................................................................................................3

TASK 2...................................................................................................................................................3

P3. Measurement of income statements...................................................................................................3

M2. Accounting techniques to produce financial statements...................................................................8

D2. Interpretation of prepared financial statements.................................................................................8

TASK 3...................................................................................................................................................8

P4. Benefits and drawbacks of planning tool...........................................................................................8

TASK 4.................................................................................................................................................11

P5. Role of MAS to solve issues............................................................................................................11

M4. MAS to solve financial issue..........................................................................................................13

CONCLUSION.........................................................................................................................................14

REFERENCES..........................................................................................................................................15

INTRODUCTION

Management Accounting involves application of expert insight and skills in the framing

and collecting accounting information and data in a specific way as to facilitate managing

personnel in development of policies, guidelines and also in the scheduling and monitoring of the

procedure of enterprise. It presents the processes and concepts sufficient for efficacious planning

for picking among acceptable business actions and for oversight through appraisal and analysis

of performances (Macintosh and Quattrone, 2010). Prime Furniture ltd, a furniture

manufacturer corporation picked for this study-project. The report offers comprehensive

information about various accounting-systems, reporting-tools and planning tools for addressing

financial issues.

MAIN BODY

TASK 2

P3. Measurement of income statements.

Micro economic techniques:

Cost- In terms of accounting aspect, cost pertains to the money value of spending/expenses on

raw-materials, machine, consumables, goods, labour, services, and so on. This is the sum that is

described as expense in the financial reports.

Cost volume analysis- Cost Volume Analysis describes the behaviors patterns of profit figures in

responding to changes in costs and quantity. In other phrases, this is an evaluation of effect of

costs and volume on earnings. Popularly known as the CVP Analysis, a management team could

consider the threshold of sales at which corporation would be in no-profit-no-loss scenario with

this evaluation. This condition is called point of break-even (Otley and Emmanuel, 2013).

Cost variance- When actual costs are different from standard costs, it is termed cost variances.

When actual costs are lower than standard costs or when actual profit is greater than standard

profits, it is termed the positive variance. Also, on opposite, when actual costs are higher

than standard-costs or profits are lower, this is termed adverse variance.

Management Accounting involves application of expert insight and skills in the framing

and collecting accounting information and data in a specific way as to facilitate managing

personnel in development of policies, guidelines and also in the scheduling and monitoring of the

procedure of enterprise. It presents the processes and concepts sufficient for efficacious planning

for picking among acceptable business actions and for oversight through appraisal and analysis

of performances (Macintosh and Quattrone, 2010). Prime Furniture ltd, a furniture

manufacturer corporation picked for this study-project. The report offers comprehensive

information about various accounting-systems, reporting-tools and planning tools for addressing

financial issues.

MAIN BODY

TASK 2

P3. Measurement of income statements.

Micro economic techniques:

Cost- In terms of accounting aspect, cost pertains to the money value of spending/expenses on

raw-materials, machine, consumables, goods, labour, services, and so on. This is the sum that is

described as expense in the financial reports.

Cost volume analysis- Cost Volume Analysis describes the behaviors patterns of profit figures in

responding to changes in costs and quantity. In other phrases, this is an evaluation of effect of

costs and volume on earnings. Popularly known as the CVP Analysis, a management team could

consider the threshold of sales at which corporation would be in no-profit-no-loss scenario with

this evaluation. This condition is called point of break-even (Otley and Emmanuel, 2013).

Cost variance- When actual costs are different from standard costs, it is termed cost variances.

When actual costs are lower than standard costs or when actual profit is greater than standard

profits, it is termed the positive variance. Also, on opposite, when actual costs are higher

than standard-costs or profits are lower, this is termed adverse variance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

There's a crucial range of vital approaches to frame financial statements and reports, like

absorption-method and marginal-method. Application of these techniques allow exploring of

different financial and non-financial aspect. These methods are described as follows:

Absorption costing method- Under this method simply all manufacturing costs are

recognized separately to assess gross profit.

Marginal costing method- Marginal costing method is mainly utilized for internal

monitoring, with aim of enabling supervisors to monitor and coordinate operational

activities. It is a managerial technique for the determination of the marginal costs and the

impacts on profits of variations in quantity or form of outcome by distinguishing the

overall costs into fixed costs as-well-as variable costs (Scapens and Bromwich, 2010).

Product costing:

Fixed cost- These costs are costs that generally not shifts over the near term, even though

the corporation experience shifts in its overall sales volumes or other operation.

Variable cost- These costs are cost which goes up and down in specific ratio to the

quantity of production.

Standard costing- Standard costing is method of calculating the costs of the

manufacturing method. It is a cost accounting component that the producer uses, for

instance, to forecast its expenditures for the upcoming year on different costs, like direct

materials , direct-labor or overheads.

Activity based costing- ABC is technique for more accurate assignment of overhead

expenses through attributing them to operations. After overall costs are allocated

to operations, costs which be allocated to costs items that apply activities. The framework

could be used to minimize overhead costs in a specific target manner.

Role of costing in setting prices- this is worthwhile to perform a part in setting prices as

the business controls the rate in compliance with it. This is because when costs are higher

than estimated than that of values set by the corporations, conversely.

Cost of inventory:

absorption-method and marginal-method. Application of these techniques allow exploring of

different financial and non-financial aspect. These methods are described as follows:

Absorption costing method- Under this method simply all manufacturing costs are

recognized separately to assess gross profit.

Marginal costing method- Marginal costing method is mainly utilized for internal

monitoring, with aim of enabling supervisors to monitor and coordinate operational

activities. It is a managerial technique for the determination of the marginal costs and the

impacts on profits of variations in quantity or form of outcome by distinguishing the

overall costs into fixed costs as-well-as variable costs (Scapens and Bromwich, 2010).

Product costing:

Fixed cost- These costs are costs that generally not shifts over the near term, even though

the corporation experience shifts in its overall sales volumes or other operation.

Variable cost- These costs are cost which goes up and down in specific ratio to the

quantity of production.

Standard costing- Standard costing is method of calculating the costs of the

manufacturing method. It is a cost accounting component that the producer uses, for

instance, to forecast its expenditures for the upcoming year on different costs, like direct

materials , direct-labor or overheads.

Activity based costing- ABC is technique for more accurate assignment of overhead

expenses through attributing them to operations. After overall costs are allocated

to operations, costs which be allocated to costs items that apply activities. The framework

could be used to minimize overhead costs in a specific target manner.

Role of costing in setting prices- this is worthwhile to perform a part in setting prices as

the business controls the rate in compliance with it. This is because when costs are higher

than estimated than that of values set by the corporations, conversely.

Cost of inventory:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

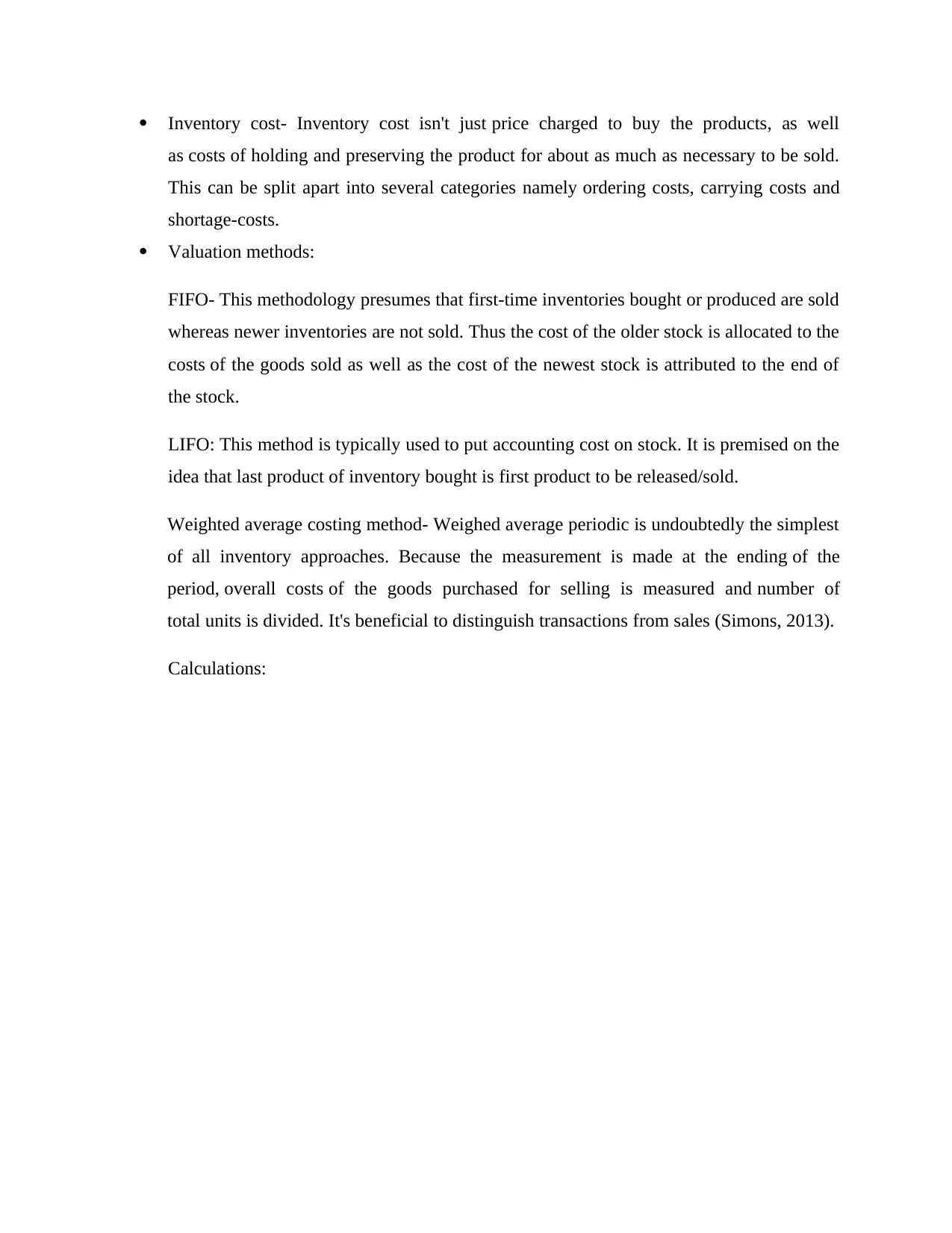

Inventory cost- Inventory cost isn't just price charged to buy the products, as well

as costs of holding and preserving the product for about as much as necessary to be sold.

This can be split apart into several categories namely ordering costs, carrying costs and

shortage-costs.

Valuation methods:

FIFO- This methodology presumes that first-time inventories bought or produced are sold

whereas newer inventories are not sold. Thus the cost of the older stock is allocated to the

costs of the goods sold as well as the cost of the newest stock is attributed to the end of

the stock.

LIFO: This method is typically used to put accounting cost on stock. It is premised on the

idea that last product of inventory bought is first product to be released/sold.

Weighted average costing method- Weighed average periodic is undoubtedly the simplest

of all inventory approaches. Because the measurement is made at the ending of the

period, overall costs of the goods purchased for selling is measured and number of

total units is divided. It's beneficial to distinguish transactions from sales (Simons, 2013).

Calculations:

as costs of holding and preserving the product for about as much as necessary to be sold.

This can be split apart into several categories namely ordering costs, carrying costs and

shortage-costs.

Valuation methods:

FIFO- This methodology presumes that first-time inventories bought or produced are sold

whereas newer inventories are not sold. Thus the cost of the older stock is allocated to the

costs of the goods sold as well as the cost of the newest stock is attributed to the end of

the stock.

LIFO: This method is typically used to put accounting cost on stock. It is premised on the

idea that last product of inventory bought is first product to be released/sold.

Weighted average costing method- Weighed average periodic is undoubtedly the simplest

of all inventory approaches. Because the measurement is made at the ending of the

period, overall costs of the goods purchased for selling is measured and number of

total units is divided. It's beneficial to distinguish transactions from sales (Simons, 2013).

Calculations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2. Accounting techniques to produce financial statements.

In the commercial finance field, often income statements are arranged into absorption-method

and marginal-method systems. As with Prime furniture, profits are reported by absorption as well

as marginal-costing methods. A wide array of methodologies, excluding these, cover the

preparation of financial reporting, including traditional cost system, costing incidents, etc. The

estimation of the possible costs considered for contrast can be shown as connected in contrast to

the standard costing. Operational costs are distributed and measured by increasing activity for

various forms of operations (Soin and Collier, 2013).

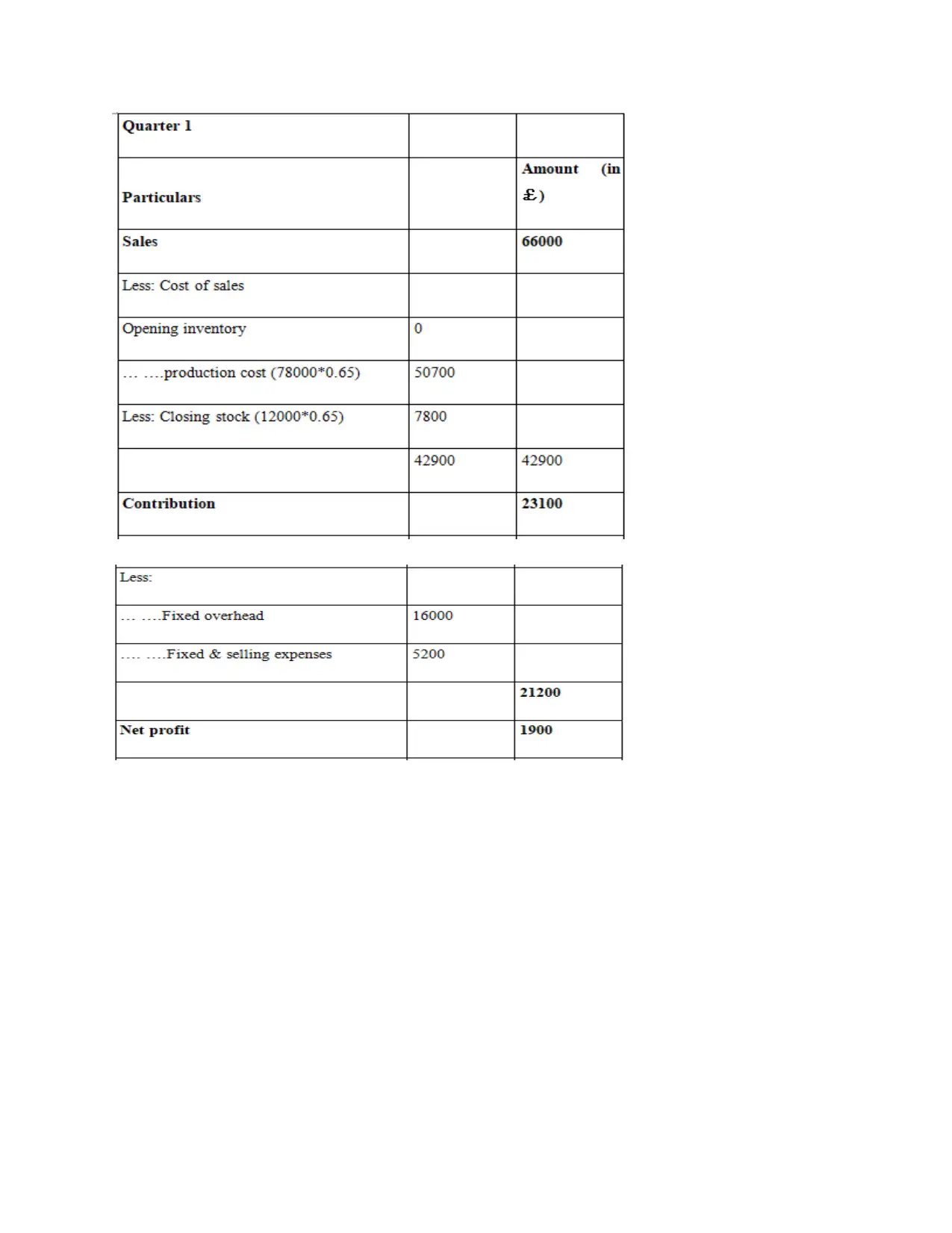

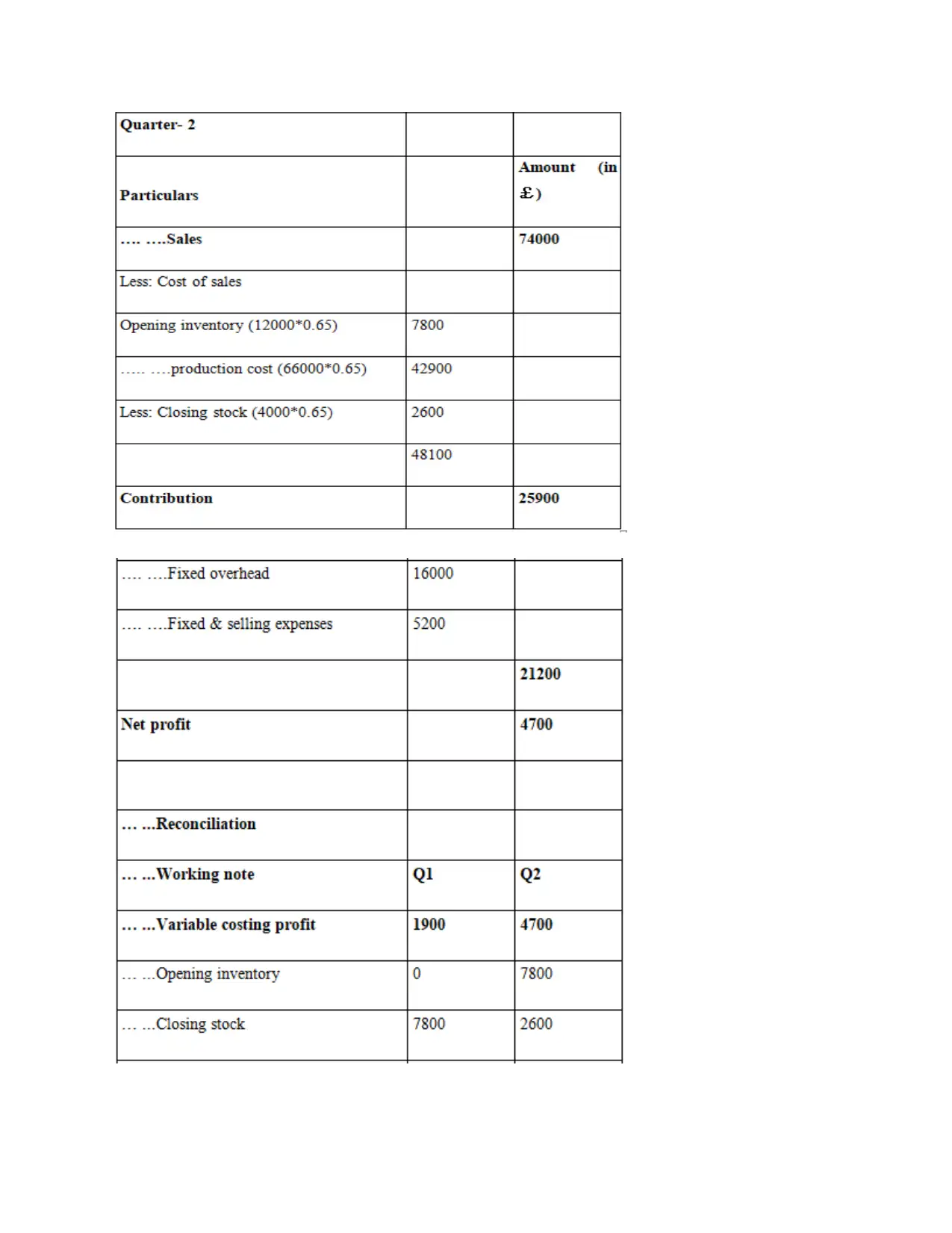

D2. Interpretation of prepared financial statements.

As far as income statement produced above is concerned, it can be said that net

profits figure is 1900 GBP by absorption cost method. Net profits equate to 4 700 pounds,

form marginal cost system. Profit figure differential with these methods is mainly due to under or

over absorption of fixed-costs.

TASK 3.

P4. Benefits and drawbacks of planning tool.

Budgetary control- Budgetary control is budgetary term for controlling revenues and expenses.

In fact, that involves matching the real income or spending on a daily basis with the expected

revenue or expense to assess whether or not preventive measure is needed. Here are certain

aspects of budgetary control as discussed below:

Operational budget- Operating budget is budget anticipated for one or more prospective cycles of

earnings and expenditures predicted. The executive team usually formulates an operating

In the commercial finance field, often income statements are arranged into absorption-method

and marginal-method systems. As with Prime furniture, profits are reported by absorption as well

as marginal-costing methods. A wide array of methodologies, excluding these, cover the

preparation of financial reporting, including traditional cost system, costing incidents, etc. The

estimation of the possible costs considered for contrast can be shown as connected in contrast to

the standard costing. Operational costs are distributed and measured by increasing activity for

various forms of operations (Soin and Collier, 2013).

D2. Interpretation of prepared financial statements.

As far as income statement produced above is concerned, it can be said that net

profits figure is 1900 GBP by absorption cost method. Net profits equate to 4 700 pounds,

form marginal cost system. Profit figure differential with these methods is mainly due to under or

over absorption of fixed-costs.

TASK 3.

P4. Benefits and drawbacks of planning tool.

Budgetary control- Budgetary control is budgetary term for controlling revenues and expenses.

In fact, that involves matching the real income or spending on a daily basis with the expected

revenue or expense to assess whether or not preventive measure is needed. Here are certain

aspects of budgetary control as discussed below:

Operational budget- Operating budget is budget anticipated for one or more prospective cycles of

earnings and expenditures predicted. The executive team usually formulates an operating

budget before the starting of year and indicates expected thresholds of activity throughout the

period. Here are certain major benefit and disadvantage of this budget, as follows:

Benefits- This is advantageous for company to handle their operations effectively by assessing

the actual productivity of different operations as well as forecast them.

Drawbacks- Classification of operations and allocation of costs is time consuming task in this

budget.

Cash budget- The cash budget is report of receipts and cash payment for a set period of time.

This is a report of cash inflows and cash outflows over a certain period. The cash budget shows

the likely revenue and payments of funds. In such cases , effective cash control is applied where

payments are higher than sales. Expenditures is smaller than revenue whenever there's surplus,

so the choice about how to employ surplus is made. Here are several benefit and disadvantages

of this budget, as follows:

Benefits- If cash is scarce and the distance is filled, it is handy in emergencies. A accurate bank

balance lets pay on due dates, which enables managers to reap the incentives of cash-balance.

Drawbacks- This budget only emphasizes on cash aspects and ignores other variables which

decrease the relevancy of this budget in strategic decision making.

Capital budget- It is a kind of budget for the procurement or maintenances of capital assets

like buildings and machinery. This is capital spending strategy for a corporation. Capital

spending is a duration of even more than 1 year of expenditures produced. It is used for

purchasing properties or extending the productive life of established properties; the financing for

a plant is an illustration of capital spending. The capital budgeting of plans concerned must take

care of the possible profitability (Ward, 2012). Two formulas for estimating the capital

expenditure are used for estimating the NPV or the intrinsic return on investment. Here below

are listed certain benefits and disadvantages of this budget, as follows:

Advantages – A comprehensive budget review assesses the budgetary condition

of respective company.

period. Here are certain major benefit and disadvantage of this budget, as follows:

Benefits- This is advantageous for company to handle their operations effectively by assessing

the actual productivity of different operations as well as forecast them.

Drawbacks- Classification of operations and allocation of costs is time consuming task in this

budget.

Cash budget- The cash budget is report of receipts and cash payment for a set period of time.

This is a report of cash inflows and cash outflows over a certain period. The cash budget shows

the likely revenue and payments of funds. In such cases , effective cash control is applied where

payments are higher than sales. Expenditures is smaller than revenue whenever there's surplus,

so the choice about how to employ surplus is made. Here are several benefit and disadvantages

of this budget, as follows:

Benefits- If cash is scarce and the distance is filled, it is handy in emergencies. A accurate bank

balance lets pay on due dates, which enables managers to reap the incentives of cash-balance.

Drawbacks- This budget only emphasizes on cash aspects and ignores other variables which

decrease the relevancy of this budget in strategic decision making.

Capital budget- It is a kind of budget for the procurement or maintenances of capital assets

like buildings and machinery. This is capital spending strategy for a corporation. Capital

spending is a duration of even more than 1 year of expenditures produced. It is used for

purchasing properties or extending the productive life of established properties; the financing for

a plant is an illustration of capital spending. The capital budgeting of plans concerned must take

care of the possible profitability (Ward, 2012). Two formulas for estimating the capital

expenditure are used for estimating the NPV or the intrinsic return on investment. Here below

are listed certain benefits and disadvantages of this budget, as follows:

Advantages – A comprehensive budget review assesses the budgetary condition

of respective company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Drawback: Adjustments are challenging to make the biggest obstacle in this form of budget.

Pricing:

Pricing strategies:

• Penetration pricing strategy: This pricing initiative immediately lowers the prices of an item so

that a large part of the market can be readily accessed. The strategy is effective for consumers

cos of new company's cheaper price.

• Skimming technique- Skimming pricing approach is a pricing method in which a selling firm

initially decides the quality of a goods or services and lowers prices over period. The business

reduces the prices to draw another price-responsive group if the competition of first customers is

surpassed.

Companies assess pricing according to market trends and business operations: corporations

assess price rates according to competition. Prices are contingent on the key operations measured

and taken out.

Considerations of supply and demand – Pricing is economic concept in an environment of

supplies and demands. Units' or even other economic goods, such as labor or financial fluid

goods, are priced at a time where the prices sold (at present rates) is same, and that results in fair

financial output and use. The costs of certain goods would be set.

Strategic planning

SWOT Analysis- SWOT analysis can be initiated by an enterprise, company group, person or

team. In reality, analysis reflects a range of project goals. In order to analyses and externalise a

commodity or business, a transaction or a partnership, the SWOT approach may be utilized.

SWOT analysis can also assist to determine a specific point of origin, loop, demands for

products or technology (van der Steen, 2011).

Benefits- The SWOT analysis could influence an organization, a coordination system, a person

or team. In reality, the research will satisfy a variety of project targets. SWOT approach can, for

instance, be utilized to evaluate and externalization of a service or corporation, a mechanism or a

Pricing:

Pricing strategies:

• Penetration pricing strategy: This pricing initiative immediately lowers the prices of an item so

that a large part of the market can be readily accessed. The strategy is effective for consumers

cos of new company's cheaper price.

• Skimming technique- Skimming pricing approach is a pricing method in which a selling firm

initially decides the quality of a goods or services and lowers prices over period. The business

reduces the prices to draw another price-responsive group if the competition of first customers is

surpassed.

Companies assess pricing according to market trends and business operations: corporations

assess price rates according to competition. Prices are contingent on the key operations measured

and taken out.

Considerations of supply and demand – Pricing is economic concept in an environment of

supplies and demands. Units' or even other economic goods, such as labor or financial fluid

goods, are priced at a time where the prices sold (at present rates) is same, and that results in fair

financial output and use. The costs of certain goods would be set.

Strategic planning

SWOT Analysis- SWOT analysis can be initiated by an enterprise, company group, person or

team. In reality, analysis reflects a range of project goals. In order to analyses and externalise a

commodity or business, a transaction or a partnership, the SWOT approach may be utilized.

SWOT analysis can also assist to determine a specific point of origin, loop, demands for

products or technology (van der Steen, 2011).

Benefits- The SWOT analysis could influence an organization, a coordination system, a person

or team. In reality, the research will satisfy a variety of project targets. SWOT approach can, for

instance, be utilized to evaluate and externalization of a service or corporation, a mechanism or a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

relationship. SWOT evaluation also helps to quantify the precise manufacturing source, sales

cycle, and commodity demands, or technical acceptance.

Drawbacks: The SWOT review is based on four types of assets, weaknesses, prospects and

threats in each area. However, the approach does not provide for a system to assess the

dependent variables over another. The real impact of each aspect on the goal cannot therefore be

measured.

M3. Role of various planning tools.

Companies are using different kinds of budgets to enhance financial choices. Their reports hold a

combination of plans, including the cash prediction, the annual budget and the budget model as

described above (Taschner and Charifzadeh, 2020). Both of these estimates could be used to

properly manage their liquid assets and schedule different tasks. These all expenditures have a

big part to play in the total metric of receipts and expenses. This is likely because the mangers of

this organization, in order to approximate recent operations, assess the measurements taken in

past years. It can thus be argued that the management practices on financial performance

predictive devices are too crucial to precise.

TASK 4

P5. Role of MAS to solve issues.

Monetary issues- Competition is growing and creating monetary problems in the current market

scenario. These challenges are determined by a lack of strategy formulation and management.

Moreover, financial difficulty is created by the lack of business, where companies seek to fulfil

various tasks. These are the few financial problems that most businesses face:

Errors in accounting records- This may be defined as a deliberate or unintended figural

disturbance financial issue resulting to unacceptable money management. Unable to find

major transfer, investment opportunities, and so much more because of another monetary

problem. They face problems with their financial statements in the previously mentioned

Prime furniture limited.

cycle, and commodity demands, or technical acceptance.

Drawbacks: The SWOT review is based on four types of assets, weaknesses, prospects and

threats in each area. However, the approach does not provide for a system to assess the

dependent variables over another. The real impact of each aspect on the goal cannot therefore be

measured.

M3. Role of various planning tools.

Companies are using different kinds of budgets to enhance financial choices. Their reports hold a

combination of plans, including the cash prediction, the annual budget and the budget model as

described above (Taschner and Charifzadeh, 2020). Both of these estimates could be used to

properly manage their liquid assets and schedule different tasks. These all expenditures have a

big part to play in the total metric of receipts and expenses. This is likely because the mangers of

this organization, in order to approximate recent operations, assess the measurements taken in

past years. It can thus be argued that the management practices on financial performance

predictive devices are too crucial to precise.

TASK 4

P5. Role of MAS to solve issues.

Monetary issues- Competition is growing and creating monetary problems in the current market

scenario. These challenges are determined by a lack of strategy formulation and management.

Moreover, financial difficulty is created by the lack of business, where companies seek to fulfil

various tasks. These are the few financial problems that most businesses face:

Errors in accounting records- This may be defined as a deliberate or unintended figural

disturbance financial issue resulting to unacceptable money management. Unable to find

major transfer, investment opportunities, and so much more because of another monetary

problem. They face problems with their financial statements in the previously mentioned

Prime furniture limited.

Inadequate protection of financial assets- The risk of losing capital expenditure is a sort

of problem. This problem is that investment control has been reduced fixed and unfixed.

As a result, companies face other difficulties, such as staff shortages and more.

MA methods to respond financial problems:

Benchmarking- This process includes the relevant indicators of a corporation to identify

adverse variances by competing companies. The institution will therefore realise why the

financial crisis has contributed. In the business sector mentioned above, they use this

framework to address their fundamental monetary hurdle. The other companies are linked

to their financial factors.

Key performance indicator- They can be described as a methodology coherent with the

correct financial and nonfinancial assessment (Doktoralina and Apollo, 2019). The cost

aspect is the productivity, expenses etc. of the corporation, whereas the non-financial

aspects involve employee stress levels, links, etc.

Financial governance- It can be identified as a method that properly records all monetary

operations of the company for a specific period. This review incorporates current money

problems and utilises methodological concepts to resolve them.

Management accountant skills:

Better communication skills- The successful accounting firm must be supplied with

greater effective communication so that financial results can be accessed within the

corporation.

Effective knowledge of accounting concepts- In order to produce financial data, accounts

should also have based systems resources.

Such accounting skills can be used to fix problems with money. It is because, on the basis of this,

companies can fix any kind of scenario and can advisor management consultants to find

solutions.

of problem. This problem is that investment control has been reduced fixed and unfixed.

As a result, companies face other difficulties, such as staff shortages and more.

MA methods to respond financial problems:

Benchmarking- This process includes the relevant indicators of a corporation to identify

adverse variances by competing companies. The institution will therefore realise why the

financial crisis has contributed. In the business sector mentioned above, they use this

framework to address their fundamental monetary hurdle. The other companies are linked

to their financial factors.

Key performance indicator- They can be described as a methodology coherent with the

correct financial and nonfinancial assessment (Doktoralina and Apollo, 2019). The cost

aspect is the productivity, expenses etc. of the corporation, whereas the non-financial

aspects involve employee stress levels, links, etc.

Financial governance- It can be identified as a method that properly records all monetary

operations of the company for a specific period. This review incorporates current money

problems and utilises methodological concepts to resolve them.

Management accountant skills:

Better communication skills- The successful accounting firm must be supplied with

greater effective communication so that financial results can be accessed within the

corporation.

Effective knowledge of accounting concepts- In order to produce financial data, accounts

should also have based systems resources.

Such accounting skills can be used to fix problems with money. It is because, on the basis of this,

companies can fix any kind of scenario and can advisor management consultants to find

solutions.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.