Management Accounting Report: Analysis of Big Bear Food Company

VerifiedAdded on 2020/02/17

|19

|6267

|251

Report

AI Summary

This report delves into the core principles of management accounting, providing a comprehensive analysis of its role in financial planning and decision-making within organizations. It explores the fundamental aspects of management accounting, including explaining the different types of management systems, emphasizing their significance in collecting, arranging, and communicating financial data. The report then transitions to the practical application of management accounting techniques, such as activity-based costing and transfer pricing, illustrated with a case study of Big Bear Food Company. It also examines various planning tools used in management accounting, detailing their advantages and limitations. Furthermore, the report analyzes different methods for preparing management accounting reports, including budget reports, accounts receivable aging reports, job cost reports, and inventory and manufacturing reports. Finally, the report compares the ways organizations react to financial problems using management accounting, providing a conclusion and recommendations for effective financial management.

STUDENT NAME:

STUDENT ID:

SUBJECT CODE:

ASSIGNMENT TITLE: MANAGEMENT ACCOUNTING

STUDENT ID:

SUBJECT CODE:

ASSIGNMENT TITLE: MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1: Explaining management accounting and demonstrating the requirements of various types of

management system.........................................................................................................................1

P2: Different methods for preparing management accounting report.............................................5

Task 2...............................................................................................................................................7

LO 2: Application of a range of management accounting techniques.............................................7

P3: Calculation of costs...................................................................................................................7

Task 3.............................................................................................................................................10

LO 3: Explanation on the ‘planning tools’ used in the field of Management Accounting ...........10

P4: Advantages and limitations of the ‘planning tools’ with respect to the scenario under

consideration..................................................................................................................................10

Task 4.............................................................................................................................................13

LO 4: Comparison of the different ways by which Organizations react to the financial problems

using management accounting.......................................................................................................13

P5: Comparison of the accounting system implemented in companies to tackle the financial

problems ........................................................................................................................................13

Conclusion and Recommendation.................................................................................................15

Reference list.................................................................................................................................16

INTRODUCTION...........................................................................................................................1

Task 1...............................................................................................................................................1

P1: Explaining management accounting and demonstrating the requirements of various types of

management system.........................................................................................................................1

P2: Different methods for preparing management accounting report.............................................5

Task 2...............................................................................................................................................7

LO 2: Application of a range of management accounting techniques.............................................7

P3: Calculation of costs...................................................................................................................7

Task 3.............................................................................................................................................10

LO 3: Explanation on the ‘planning tools’ used in the field of Management Accounting ...........10

P4: Advantages and limitations of the ‘planning tools’ with respect to the scenario under

consideration..................................................................................................................................10

Task 4.............................................................................................................................................13

LO 4: Comparison of the different ways by which Organizations react to the financial problems

using management accounting.......................................................................................................13

P5: Comparison of the accounting system implemented in companies to tackle the financial

problems ........................................................................................................................................13

Conclusion and Recommendation.................................................................................................15

Reference list.................................................................................................................................16

INTRODUCTION

Management accounting refer to the method in which organisation store financial data for

systematic planning of business and it also helps management body of an organisation to take

financial and non-financial decision relating to the firm. The process measures, identify,

interpret and communicate information throughout the business environment to achieve goals of

organisation. Alternatively, the role accounting plays to supply information, which will assist

management in planning economical structure, controlling cost, decision making, and to increase

profitability of business is termed as Management accounting. The user of accounting

information who will be benefited from management accounting can be divided into two groups.

The groups are internal manager and external parties. Internal managers group are divided into

two part again one who makes short-run planning and another who make decisions to formulate

policies. External parties refer to shareholders, investors, associate partners and others. Here in

the study a manufacturing organisation Big Bear (Food Company) has been selected to interpret

management accounting system of the company which will give clear concept of fundamental of

Management accounting.

Overview of company

Big bear Limited supply foods, it is situated at Leicester, London and owned brands of different

company such as XXX mints, Sugar Puffs and others. The company was established in 2011 by

Raisio Group and specialised the brands which is unknown or have household names. The

company operate small-size business by producing different food products.

Task 1

P1: Explaining management accounting and demonstrating the requirements

of various types of management system

Management accounting focuses areas of accounting which help management in financial

planning and they prepared principles by interpreting financial data available in business sectors.

Management accounting gives information to management body which will assist them to take

decisions and fulfil objectives of business (Kaplan and Atkinson, 2015, p.47). The basic

objective of management accounting are discussed below-

formulate policy related to financial management

plan for future events to cooperate with internal and external changes of business

1

Management accounting refer to the method in which organisation store financial data for

systematic planning of business and it also helps management body of an organisation to take

financial and non-financial decision relating to the firm. The process measures, identify,

interpret and communicate information throughout the business environment to achieve goals of

organisation. Alternatively, the role accounting plays to supply information, which will assist

management in planning economical structure, controlling cost, decision making, and to increase

profitability of business is termed as Management accounting. The user of accounting

information who will be benefited from management accounting can be divided into two groups.

The groups are internal manager and external parties. Internal managers group are divided into

two part again one who makes short-run planning and another who make decisions to formulate

policies. External parties refer to shareholders, investors, associate partners and others. Here in

the study a manufacturing organisation Big Bear (Food Company) has been selected to interpret

management accounting system of the company which will give clear concept of fundamental of

Management accounting.

Overview of company

Big bear Limited supply foods, it is situated at Leicester, London and owned brands of different

company such as XXX mints, Sugar Puffs and others. The company was established in 2011 by

Raisio Group and specialised the brands which is unknown or have household names. The

company operate small-size business by producing different food products.

Task 1

P1: Explaining management accounting and demonstrating the requirements

of various types of management system

Management accounting focuses areas of accounting which help management in financial

planning and they prepared principles by interpreting financial data available in business sectors.

Management accounting gives information to management body which will assist them to take

decisions and fulfil objectives of business (Kaplan and Atkinson, 2015, p.47). The basic

objective of management accounting are discussed below-

formulate policy related to financial management

plan for future events to cooperate with internal and external changes of business

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

monitoring performance to use resources efficiently and control daily activities of firm

comparing between alternative scenarios of business to assess growth and implement new

methods to improve quality of product

solving financial problems and achieving business targets

Considering behavioural factors that can affect business activities

An accounting system always provide various ways to collect, arrange and communicate

information related to financial activities of firm to organise different elements of firm

systematically (Zimmerman and Yahya-Zadeh, 2011, p.258). Management accounting is

different from actual accounting system, it basically focused on collecting information about

product or cost of specific operation at detail level which will help higher authority to take

decision especially financial decision. The work of management accounting involves around

identifying different types of resolution management will need to carry on business activities

(Ward, 2012, p.36). The decisions which are concerned with management accounting are of two

types, output decision and input decision. Output decision relates with quantity, quality and price

of goods or product supplied by company and Input decision deals with production elements

such as labour, raw materials, capital investments and equipments.

Both the decision discussed above are interconnected thus, for management accounting

managerial planning is necessary which involves seven stages. These stages are also appropriate

for small enterprises as selected above Big Bear (Food Company) for efficient management

accounting system in their manufacturing company. Management accounting has responsibility,

which includes:

Planning: By planning, the accounting manager gets ready for application of the structured

process as per the raised budget of the overall business.

Implementation: After planning the activities the factors essential for implementation are

performed on the workforce is done as an activity as per the raised situation.

Controlling: The workforce of the concerned firm is controlled in order to stabilize the

increasing budget of the firm.

2

comparing between alternative scenarios of business to assess growth and implement new

methods to improve quality of product

solving financial problems and achieving business targets

Considering behavioural factors that can affect business activities

An accounting system always provide various ways to collect, arrange and communicate

information related to financial activities of firm to organise different elements of firm

systematically (Zimmerman and Yahya-Zadeh, 2011, p.258). Management accounting is

different from actual accounting system, it basically focused on collecting information about

product or cost of specific operation at detail level which will help higher authority to take

decision especially financial decision. The work of management accounting involves around

identifying different types of resolution management will need to carry on business activities

(Ward, 2012, p.36). The decisions which are concerned with management accounting are of two

types, output decision and input decision. Output decision relates with quantity, quality and price

of goods or product supplied by company and Input decision deals with production elements

such as labour, raw materials, capital investments and equipments.

Both the decision discussed above are interconnected thus, for management accounting

managerial planning is necessary which involves seven stages. These stages are also appropriate

for small enterprises as selected above Big Bear (Food Company) for efficient management

accounting system in their manufacturing company. Management accounting has responsibility,

which includes:

Planning: By planning, the accounting manager gets ready for application of the structured

process as per the raised budget of the overall business.

Implementation: After planning the activities the factors essential for implementation are

performed on the workforce is done as an activity as per the raised situation.

Controlling: The workforce of the concerned firm is controlled in order to stabilize the

increasing budget of the firm.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Monitoring performance: The performance of the employees is then monitored in order to

avoid flaws that may be faced in the long run of the firm.

Motivating employee: The employees must be motivated in order to gain quality goods and

services for their customers. Therefore, the concerned organization makes effort to motivate their

employees in terms of satisfactory salary and rewarding them as per their capabilities and

performances.

Communicating information: The communication process is again well maintained in order to

keep both the organization and their employees connected to their target audiences.

Different types of management accounting

Management accountings are of different types such as Activity-Based costing, Resource

consumption accounting, Throughput accounting, Transfer pricing and Lean accounting. Here

two types of management accounting related with manufacturing industries are discussed below

briefly to understand the concept of management accounting.

Activity based costing (ABC)

The concept of Activity based costing was explained clearly by Robert S. Kalpan and W. Bruns

in 1987. This method identifies the activities to be followed by an organisation to produce goods

or service and then the cost of each activity are allocated according to cost of production

(Needles et al. 2013, p.27). Activity-Based costing focus on two common aspects of

manufacturing activities, firstly it set up production machine to run batches of product and

secondly it focuses on actual production levels.

Transfer pricing

Transfer pricing deals with the fundamental concept of assigning value to the produced product

by specifying functions and also attribute revenue to different business units, in another way it

can be said the price at which departments of an organisation transacts within organization is

termed as transfer pricing, the departments may be labour and supplier or others. It often

involves transfer of intangible and tangible assets. In addition to above, the cost accounting

system has been marked as a framework that is utilized by the companies in order to acquire an

estimated cost price for the product. Moreover, buy acquiring the estimate costs, the concerned

3

avoid flaws that may be faced in the long run of the firm.

Motivating employee: The employees must be motivated in order to gain quality goods and

services for their customers. Therefore, the concerned organization makes effort to motivate their

employees in terms of satisfactory salary and rewarding them as per their capabilities and

performances.

Communicating information: The communication process is again well maintained in order to

keep both the organization and their employees connected to their target audiences.

Different types of management accounting

Management accountings are of different types such as Activity-Based costing, Resource

consumption accounting, Throughput accounting, Transfer pricing and Lean accounting. Here

two types of management accounting related with manufacturing industries are discussed below

briefly to understand the concept of management accounting.

Activity based costing (ABC)

The concept of Activity based costing was explained clearly by Robert S. Kalpan and W. Bruns

in 1987. This method identifies the activities to be followed by an organisation to produce goods

or service and then the cost of each activity are allocated according to cost of production

(Needles et al. 2013, p.27). Activity-Based costing focus on two common aspects of

manufacturing activities, firstly it set up production machine to run batches of product and

secondly it focuses on actual production levels.

Transfer pricing

Transfer pricing deals with the fundamental concept of assigning value to the produced product

by specifying functions and also attribute revenue to different business units, in another way it

can be said the price at which departments of an organisation transacts within organization is

termed as transfer pricing, the departments may be labour and supplier or others. It often

involves transfer of intangible and tangible assets. In addition to above, the cost accounting

system has been marked as a framework that is utilized by the companies in order to acquire an

estimated cost price for the product. Moreover, buy acquiring the estimate costs, the concerned

3

origanisation would be able to analyse the profitability, inventory along with cost measurable for

the raised situations. Therefore, by application of the cost accounting system, the overall cist

price of the served products and services are estimated more evenly by the job order costing

along with the process costing.

Different kinds of management accounting systems which are used under the Big Bear

business entity of the food processing industry are such as follows:

Cost accounting system: The method in which several kinds of the costs and expenses

come into consideration at the workplace are to be included and analysed is called the

cost accounting system. By using this particular approach of management accounting the

selected food processing company can assess that, how much cost is incurred under the

different business processes like administration, operation, production etc. Hence, the

pricing decisions also can be taken in fruitful manner.

Job costing system: The system where expenses of each and every job of the firm under

the production process are analysed in proper direction is considered as the job costing

(Kaplan and Atkinson, 2015). In the Big Bear company there are different range of the

food items are cooked and served up to the customers. Further, in order to know total

production cost of every job, the mentioned system of management accounting is

undertaken by the manager.

Batch costing system: Moreover, in the cited firm of food industry, different types of

batches are included where several numbers of the products are cooked up to the greater

extent. In every batch, food items differ with each other and level of expenditures as well.

Due to the occurring difference in such all the things cost of the products and services

cannot determine by the company. Therefore, in order to resolve this particular problem

the batch costing system is one of the best and appropriate tool for the chosen company.

Inventory management system: Within working environment, if level of stock or

inventory is higher, then productivity and revenue generation capability affects in

negative direction up to the larger extent. In order to resolve this particular problem, the

mentioned management accounting system is supportive and helps to manage the stock.

Further, it includes basically three methods by which available inventory can be valued

4

the raised situations. Therefore, by application of the cost accounting system, the overall cist

price of the served products and services are estimated more evenly by the job order costing

along with the process costing.

Different kinds of management accounting systems which are used under the Big Bear

business entity of the food processing industry are such as follows:

Cost accounting system: The method in which several kinds of the costs and expenses

come into consideration at the workplace are to be included and analysed is called the

cost accounting system. By using this particular approach of management accounting the

selected food processing company can assess that, how much cost is incurred under the

different business processes like administration, operation, production etc. Hence, the

pricing decisions also can be taken in fruitful manner.

Job costing system: The system where expenses of each and every job of the firm under

the production process are analysed in proper direction is considered as the job costing

(Kaplan and Atkinson, 2015). In the Big Bear company there are different range of the

food items are cooked and served up to the customers. Further, in order to know total

production cost of every job, the mentioned system of management accounting is

undertaken by the manager.

Batch costing system: Moreover, in the cited firm of food industry, different types of

batches are included where several numbers of the products are cooked up to the greater

extent. In every batch, food items differ with each other and level of expenditures as well.

Due to the occurring difference in such all the things cost of the products and services

cannot determine by the company. Therefore, in order to resolve this particular problem

the batch costing system is one of the best and appropriate tool for the chosen company.

Inventory management system: Within working environment, if level of stock or

inventory is higher, then productivity and revenue generation capability affects in

negative direction up to the larger extent. In order to resolve this particular problem, the

mentioned management accounting system is supportive and helps to manage the stock.

Further, it includes basically three methods by which available inventory can be valued

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Hall, 2012). Such stock valuation techniques are like FIFO (first in first out), Weighted

average method (WAM) as well as LIFO (last in first out).

Price optimisation system: Apart from the above all management accounting systems,

other is price optimisation by which the Big Bear enterprise able to take pricing decisions

of its food products and services in profitable way. When the firm charges different

selling prices then number of customers also differ. Moreover, a specific pricing level at

which more consumers attract that will be selected by the management of cited firm for

selling further goods and services.

P2: Different methods for preparing management accounting report

Management accounting reports assist management body and owners of small enterprises to

assess the performance of company. It is prepared frequently in the accounting period as required

depending on the activities of business (Weil, et al. 2013, p.38). There are specifically four types

of methods for preparing management accounting report such as Budget report, Accounts

Receivable Aging, Job Cost reports and Inventory & manufacturing report. These methods are

described below-

Budget report

Budget report is type of internal report which is utilized by management to compare growth of

business with actual performance and estimate cost of production. If organisations are big then

different department of organisation prepare budget report to evaluate their performance. Again

if organisation is small the budget of whole organisation is considered to measure performance

of business. Manager can use budget report to provide incentive and bonus to staff if they

analysed that their performance is enhancing the growth of business. The steps to prepare budget

report are as follows-

Update assumption

Evaluate the capacity of firm to generate sales

Allocate funds required for activities

Step costing points

Create and issue budget package

Obtain department budgets and their request for capital budget

Prepare budget model

Review and issue the budget

5

average method (WAM) as well as LIFO (last in first out).

Price optimisation system: Apart from the above all management accounting systems,

other is price optimisation by which the Big Bear enterprise able to take pricing decisions

of its food products and services in profitable way. When the firm charges different

selling prices then number of customers also differ. Moreover, a specific pricing level at

which more consumers attract that will be selected by the management of cited firm for

selling further goods and services.

P2: Different methods for preparing management accounting report

Management accounting reports assist management body and owners of small enterprises to

assess the performance of company. It is prepared frequently in the accounting period as required

depending on the activities of business (Weil, et al. 2013, p.38). There are specifically four types

of methods for preparing management accounting report such as Budget report, Accounts

Receivable Aging, Job Cost reports and Inventory & manufacturing report. These methods are

described below-

Budget report

Budget report is type of internal report which is utilized by management to compare growth of

business with actual performance and estimate cost of production. If organisations are big then

different department of organisation prepare budget report to evaluate their performance. Again

if organisation is small the budget of whole organisation is considered to measure performance

of business. Manager can use budget report to provide incentive and bonus to staff if they

analysed that their performance is enhancing the growth of business. The steps to prepare budget

report are as follows-

Update assumption

Evaluate the capacity of firm to generate sales

Allocate funds required for activities

Step costing points

Create and issue budget package

Obtain department budgets and their request for capital budget

Prepare budget model

Review and issue the budget

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

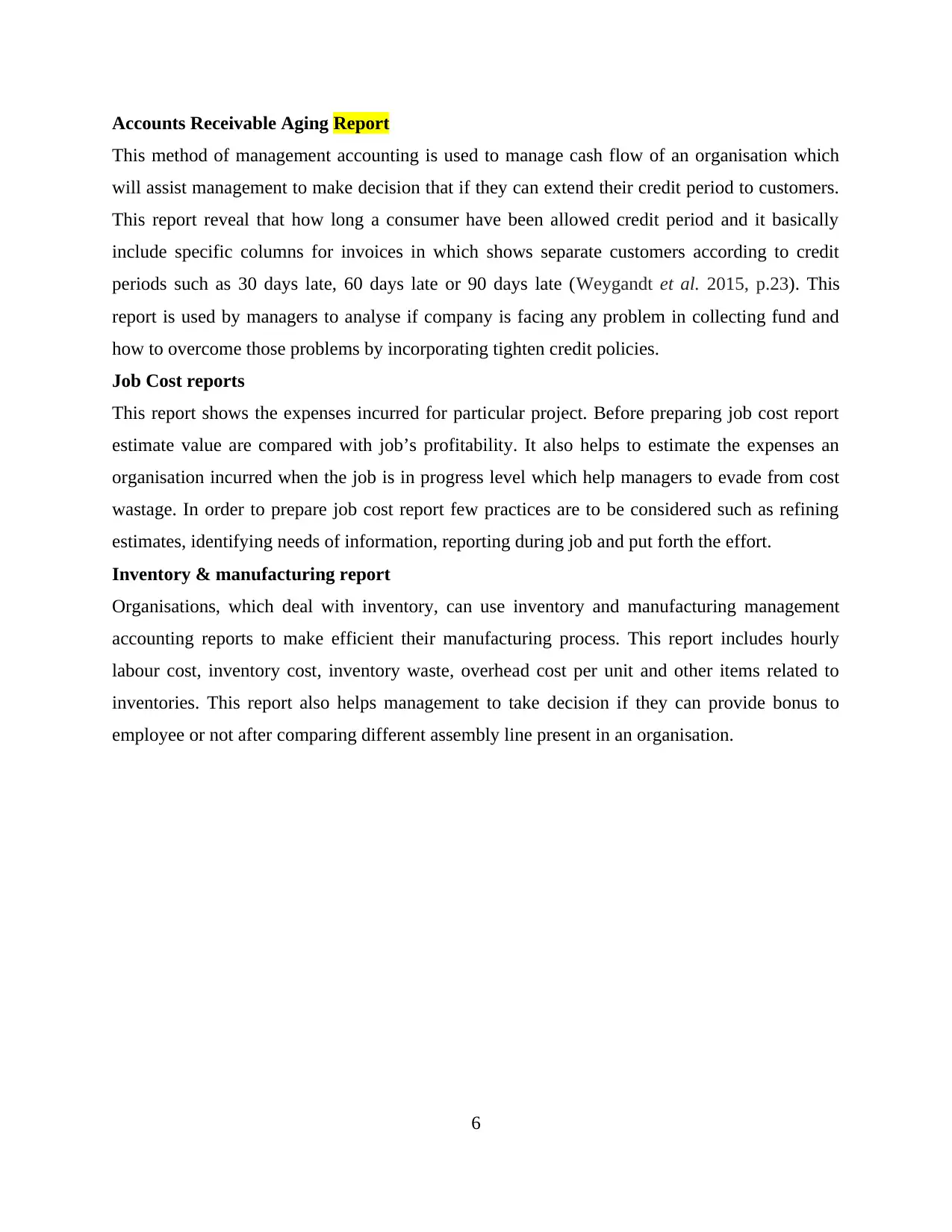

Accounts Receivable Aging Report

This method of management accounting is used to manage cash flow of an organisation which

will assist management to make decision that if they can extend their credit period to customers.

This report reveal that how long a consumer have been allowed credit period and it basically

include specific columns for invoices in which shows separate customers according to credit

periods such as 30 days late, 60 days late or 90 days late (Weygandt et al. 2015, p.23). This

report is used by managers to analyse if company is facing any problem in collecting fund and

how to overcome those problems by incorporating tighten credit policies.

Job Cost reports

This report shows the expenses incurred for particular project. Before preparing job cost report

estimate value are compared with job’s profitability. It also helps to estimate the expenses an

organisation incurred when the job is in progress level which help managers to evade from cost

wastage. In order to prepare job cost report few practices are to be considered such as refining

estimates, identifying needs of information, reporting during job and put forth the effort.

Inventory & manufacturing report

Organisations, which deal with inventory, can use inventory and manufacturing management

accounting reports to make efficient their manufacturing process. This report includes hourly

labour cost, inventory cost, inventory waste, overhead cost per unit and other items related to

inventories. This report also helps management to take decision if they can provide bonus to

employee or not after comparing different assembly line present in an organisation.

6

This method of management accounting is used to manage cash flow of an organisation which

will assist management to make decision that if they can extend their credit period to customers.

This report reveal that how long a consumer have been allowed credit period and it basically

include specific columns for invoices in which shows separate customers according to credit

periods such as 30 days late, 60 days late or 90 days late (Weygandt et al. 2015, p.23). This

report is used by managers to analyse if company is facing any problem in collecting fund and

how to overcome those problems by incorporating tighten credit policies.

Job Cost reports

This report shows the expenses incurred for particular project. Before preparing job cost report

estimate value are compared with job’s profitability. It also helps to estimate the expenses an

organisation incurred when the job is in progress level which help managers to evade from cost

wastage. In order to prepare job cost report few practices are to be considered such as refining

estimates, identifying needs of information, reporting during job and put forth the effort.

Inventory & manufacturing report

Organisations, which deal with inventory, can use inventory and manufacturing management

accounting reports to make efficient their manufacturing process. This report includes hourly

labour cost, inventory cost, inventory waste, overhead cost per unit and other items related to

inventories. This report also helps management to take decision if they can provide bonus to

employee or not after comparing different assembly line present in an organisation.

6

Task 2

LO 2: Application of a range of management accounting techniques

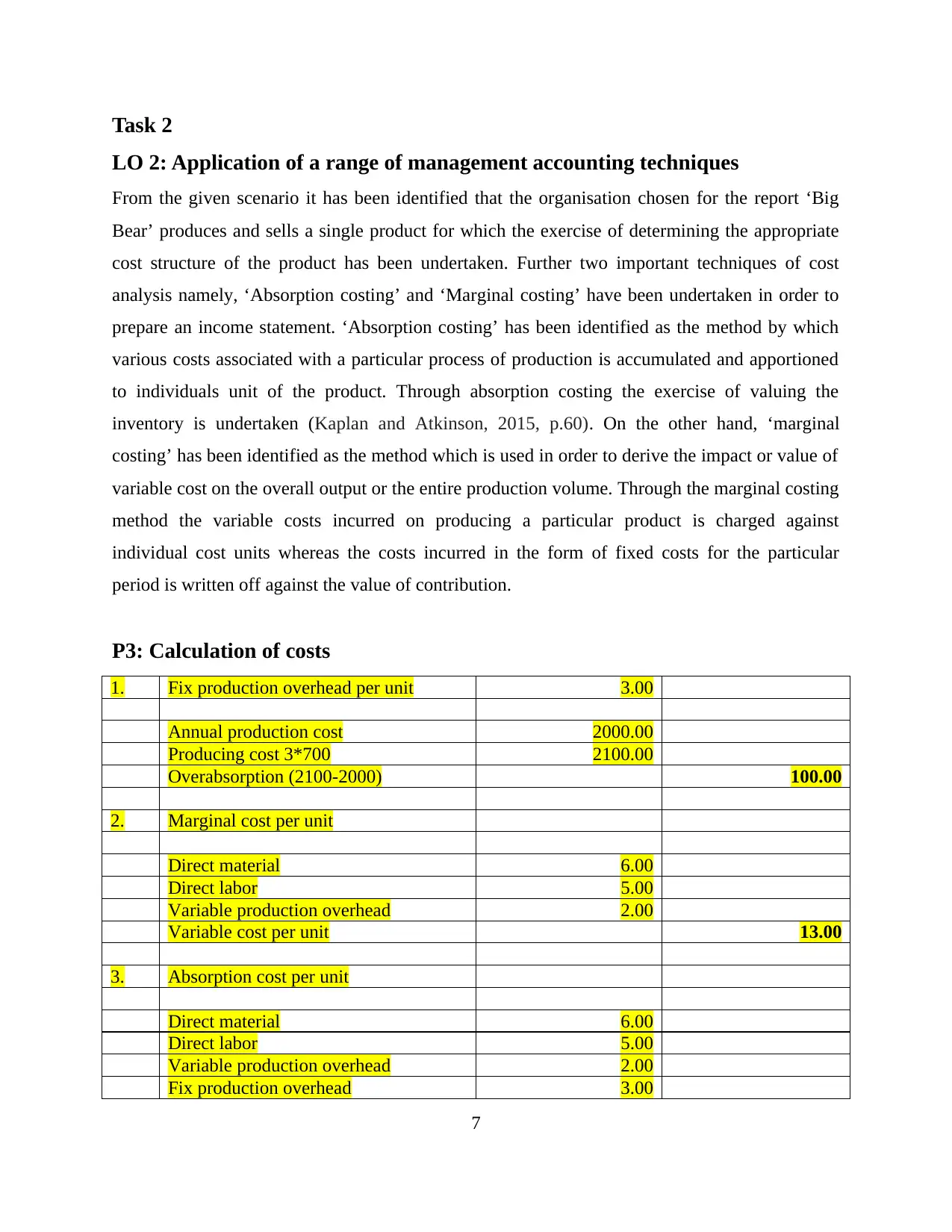

From the given scenario it has been identified that the organisation chosen for the report ‘Big

Bear’ produces and sells a single product for which the exercise of determining the appropriate

cost structure of the product has been undertaken. Further two important techniques of cost

analysis namely, ‘Absorption costing’ and ‘Marginal costing’ have been undertaken in order to

prepare an income statement. ‘Absorption costing’ has been identified as the method by which

various costs associated with a particular process of production is accumulated and apportioned

to individuals unit of the product. Through absorption costing the exercise of valuing the

inventory is undertaken (Kaplan and Atkinson, 2015, p.60). On the other hand, ‘marginal

costing’ has been identified as the method which is used in order to derive the impact or value of

variable cost on the overall output or the entire production volume. Through the marginal costing

method the variable costs incurred on producing a particular product is charged against

individual cost units whereas the costs incurred in the form of fixed costs for the particular

period is written off against the value of contribution.

P3: Calculation of costs

1. Fix production overhead per unit 3.00

Annual production cost 2000.00

Producing cost 3*700 2100.00

Overabsorption (2100-2000) 100.00

2. Marginal cost per unit

Direct material 6.00

Direct labor 5.00

Variable production overhead 2.00

Variable cost per unit 13.00

3. Absorption cost per unit

Direct material 6.00

Direct labor 5.00

Variable production overhead 2.00

Fix production overhead 3.00

7

LO 2: Application of a range of management accounting techniques

From the given scenario it has been identified that the organisation chosen for the report ‘Big

Bear’ produces and sells a single product for which the exercise of determining the appropriate

cost structure of the product has been undertaken. Further two important techniques of cost

analysis namely, ‘Absorption costing’ and ‘Marginal costing’ have been undertaken in order to

prepare an income statement. ‘Absorption costing’ has been identified as the method by which

various costs associated with a particular process of production is accumulated and apportioned

to individuals unit of the product. Through absorption costing the exercise of valuing the

inventory is undertaken (Kaplan and Atkinson, 2015, p.60). On the other hand, ‘marginal

costing’ has been identified as the method which is used in order to derive the impact or value of

variable cost on the overall output or the entire production volume. Through the marginal costing

method the variable costs incurred on producing a particular product is charged against

individual cost units whereas the costs incurred in the form of fixed costs for the particular

period is written off against the value of contribution.

P3: Calculation of costs

1. Fix production overhead per unit 3.00

Annual production cost 2000.00

Producing cost 3*700 2100.00

Overabsorption (2100-2000) 100.00

2. Marginal cost per unit

Direct material 6.00

Direct labor 5.00

Variable production overhead 2.00

Variable cost per unit 13.00

3. Absorption cost per unit

Direct material 6.00

Direct labor 5.00

Variable production overhead 2.00

Fix production overhead 3.00

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

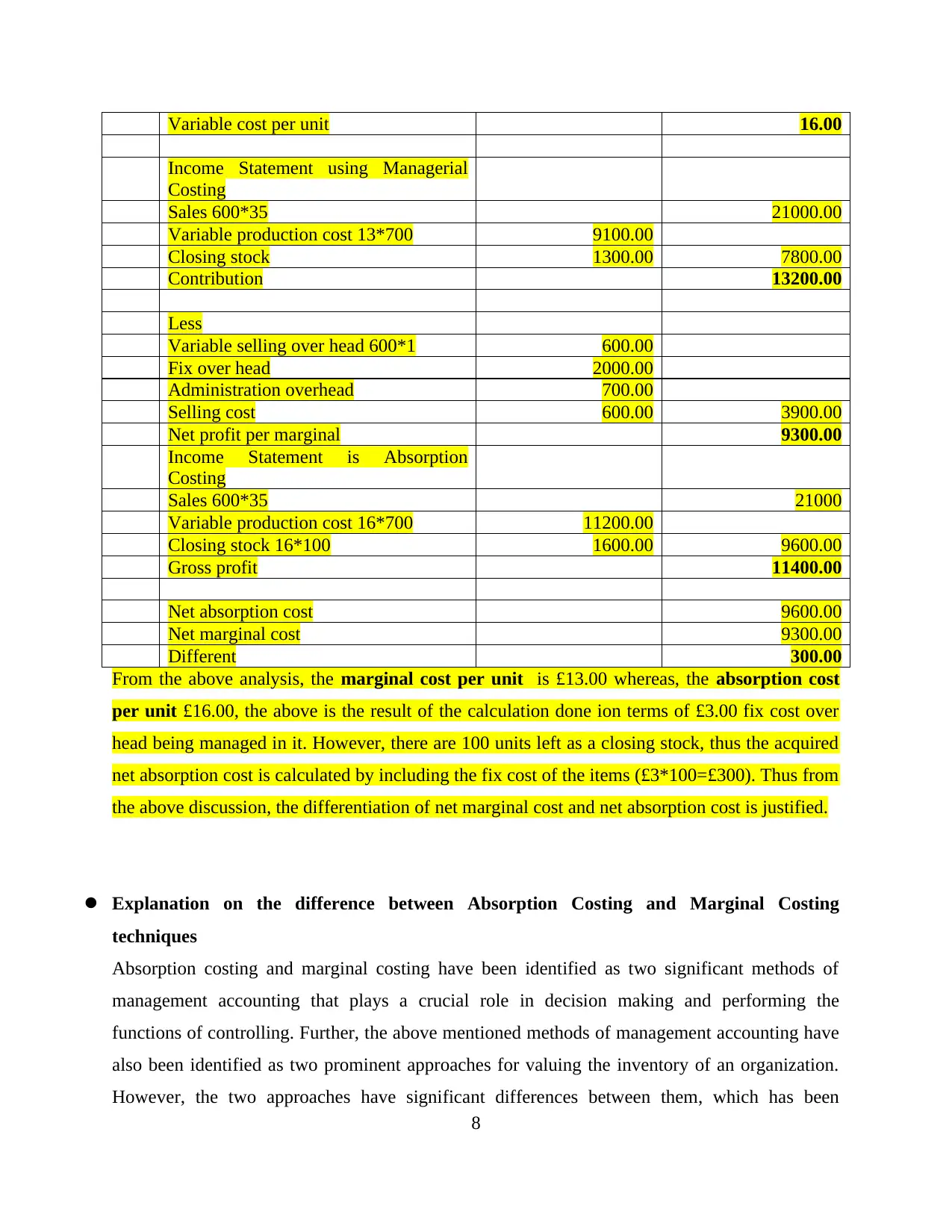

Variable cost per unit 16.00

Income Statement using Managerial

Costing

Sales 600*35 21000.00

Variable production cost 13*700 9100.00

Closing stock 1300.00 7800.00

Contribution 13200.00

Less

Variable selling over head 600*1 600.00

Fix over head 2000.00

Administration overhead 700.00

Selling cost 600.00 3900.00

Net profit per marginal 9300.00

Income Statement is Absorption

Costing

Sales 600*35 21000

Variable production cost 16*700 11200.00

Closing stock 16*100 1600.00 9600.00

Gross profit 11400.00

Net absorption cost 9600.00

Net marginal cost 9300.00

Different 300.00

From the above analysis, the marginal cost per unit is £13.00 whereas, the absorption cost

per unit £16.00, the above is the result of the calculation done ion terms of £3.00 fix cost over

head being managed in it. However, there are 100 units left as a closing stock, thus the acquired

net absorption cost is calculated by including the fix cost of the items (£3*100=£300). Thus from

the above discussion, the differentiation of net marginal cost and net absorption cost is justified.

Explanation on the difference between Absorption Costing and Marginal Costing

techniques

Absorption costing and marginal costing have been identified as two significant methods of

management accounting that plays a crucial role in decision making and performing the

functions of controlling. Further, the above mentioned methods of management accounting have

also been identified as two prominent approaches for valuing the inventory of an organization.

However, the two approaches have significant differences between them, which has been

8

Income Statement using Managerial

Costing

Sales 600*35 21000.00

Variable production cost 13*700 9100.00

Closing stock 1300.00 7800.00

Contribution 13200.00

Less

Variable selling over head 600*1 600.00

Fix over head 2000.00

Administration overhead 700.00

Selling cost 600.00 3900.00

Net profit per marginal 9300.00

Income Statement is Absorption

Costing

Sales 600*35 21000

Variable production cost 16*700 11200.00

Closing stock 16*100 1600.00 9600.00

Gross profit 11400.00

Net absorption cost 9600.00

Net marginal cost 9300.00

Different 300.00

From the above analysis, the marginal cost per unit is £13.00 whereas, the absorption cost

per unit £16.00, the above is the result of the calculation done ion terms of £3.00 fix cost over

head being managed in it. However, there are 100 units left as a closing stock, thus the acquired

net absorption cost is calculated by including the fix cost of the items (£3*100=£300). Thus from

the above discussion, the differentiation of net marginal cost and net absorption cost is justified.

Explanation on the difference between Absorption Costing and Marginal Costing

techniques

Absorption costing and marginal costing have been identified as two significant methods of

management accounting that plays a crucial role in decision making and performing the

functions of controlling. Further, the above mentioned methods of management accounting have

also been identified as two prominent approaches for valuing the inventory of an organization.

However, the two approaches have significant differences between them, which has been

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

discussed hereafter. Primarily, marginal costing method have been chosen as the best decision

making tool over absorption costing.

Marginal costing is a technique for undertaking significant decisions in order to ascertain the

total or overall cost involved in production process whereas absorption costing undertakes the

processes of apportioning the total cost incurred over the cost centres for the purpose of

determining the total or actual cost involved in production (Zimmerman and Yahya-Zadeh, 2011,

p.258). Under the technique of marginal costing the product cost is identified to be the ‘variable

cost’ while the fixed cost involved in producing a product is considered as the ‘period cost’. On

the other hand, under the absorption costing technique, the ‘product cost’ is calculated

considering both the costs namely, fixed cost and variable cost.

The overheads of marginal costing method has been identified as fixed overheads and variable

overheads while the overheads of absorption costing technique have been classified as,

production overhead, selling and distribution overhead and administration overhead.

Through marginal costing data is presented in a manner which helps in highlighting the

contribution made from each product along with the total contribution (Syverson, 2011, p.135).

On the other hand, in absorption costing the data of the cost structure is presented in such a

manner that follows a conventional mechanism or pattern.

As marginal costing technique do not consider the fixed costs therefore the cost attributed to per

unit of production does not appear to be affected due to any kind of difference arising in the

value of opening inventory and closing inventory (Zimmerman and Yahya-Zadeh, 2011, p.258).

In comparison, the per unit cost of production determined using the absorption costing method is

expected to be affected due to the impact created by the fixed overheads as a result of the

difference in its value of opening and closing inventory.

In the method of ‘absorption costing’ for the purpose of valuing the inventory both fixed and

variable costs incurred during the production process are undertaken. Whereas, for the purpose

of valuing the inventory under marginal costing only the costs incurred in the form of variable

costs are considered.

In order to derive the profitability structure under absorption costing two components are

considered namely, revenue generated from sales and the total cost incurred. The decisions made

by the management depending on the absorption data is based on the difference derived from the

figures with respect to sales and total cost (Weygandt et al. 2015, p.112). On the other hand, the

9

making tool over absorption costing.

Marginal costing is a technique for undertaking significant decisions in order to ascertain the

total or overall cost involved in production process whereas absorption costing undertakes the

processes of apportioning the total cost incurred over the cost centres for the purpose of

determining the total or actual cost involved in production (Zimmerman and Yahya-Zadeh, 2011,

p.258). Under the technique of marginal costing the product cost is identified to be the ‘variable

cost’ while the fixed cost involved in producing a product is considered as the ‘period cost’. On

the other hand, under the absorption costing technique, the ‘product cost’ is calculated

considering both the costs namely, fixed cost and variable cost.

The overheads of marginal costing method has been identified as fixed overheads and variable

overheads while the overheads of absorption costing technique have been classified as,

production overhead, selling and distribution overhead and administration overhead.

Through marginal costing data is presented in a manner which helps in highlighting the

contribution made from each product along with the total contribution (Syverson, 2011, p.135).

On the other hand, in absorption costing the data of the cost structure is presented in such a

manner that follows a conventional mechanism or pattern.

As marginal costing technique do not consider the fixed costs therefore the cost attributed to per

unit of production does not appear to be affected due to any kind of difference arising in the

value of opening inventory and closing inventory (Zimmerman and Yahya-Zadeh, 2011, p.258).

In comparison, the per unit cost of production determined using the absorption costing method is

expected to be affected due to the impact created by the fixed overheads as a result of the

difference in its value of opening and closing inventory.

In the method of ‘absorption costing’ for the purpose of valuing the inventory both fixed and

variable costs incurred during the production process are undertaken. Whereas, for the purpose

of valuing the inventory under marginal costing only the costs incurred in the form of variable

costs are considered.

In order to derive the profitability structure under absorption costing two components are

considered namely, revenue generated from sales and the total cost incurred. The decisions made

by the management depending on the absorption data is based on the difference derived from the

figures with respect to sales and total cost (Weygandt et al. 2015, p.112). On the other hand, the

9

decisions of the management depending on the data of marginal costing are based on the figures

derived with respect to ‘contribution’. ‘Contribution’ is a term that is used to denote the excess

value of revenue generated in the form of sales over the marginal cost.

Task 3

LO 3: Explanation on the ‘planning tools’ used in the field of Management

Accounting

P4: Advantages and limitations of the ‘planning tools’ with respect to the

scenario under consideration

Advantages of the ‘planning tools’ implemented in the chosen scenario

Management accounting encompasses various accounting techniques and planning tools that

help the organizations in performing efficient decision-making exercises. The process of

budgeting and the functions performed by the techniques of budgetary control helps in

increasing the efficiency of an organization. Various other tools of management accounting

namely, variance analysis and performance indicators helps in undertaking effective decision

making strategies within an organization. Through the techniques of budgetary control, the

estimations are made on the financial needs of an organization to be incorporated in the

future. The planning tool incorporated in the method of budgetary control helps in controlling

the financial performance of an organization and helps the entity in achieving the desired

results (Hiebl et al. 2013, p.122). Since the budget of an organization is perceived to be an

instrument of control therefore it helps in controlling and measuring the deviations attained

while performing various activities in the organization with respect to planning production

and sales. Various advantages of budgetary control as a planning technique have been

perceived which is enumerated hereafter. Preparation and presentation of the of budgets

which is one of the important planning tools as a part of the budgetary control mechanism

helps the financial manager or the budget coordinator of the organization in coordinating the

resources appropriately ensuring optimum utilization of the resources. Further, the budget

helps in defining the benchmarks or the standards required across different controlling

systems implemented within the organization.

10

derived with respect to ‘contribution’. ‘Contribution’ is a term that is used to denote the excess

value of revenue generated in the form of sales over the marginal cost.

Task 3

LO 3: Explanation on the ‘planning tools’ used in the field of Management

Accounting

P4: Advantages and limitations of the ‘planning tools’ with respect to the

scenario under consideration

Advantages of the ‘planning tools’ implemented in the chosen scenario

Management accounting encompasses various accounting techniques and planning tools that

help the organizations in performing efficient decision-making exercises. The process of

budgeting and the functions performed by the techniques of budgetary control helps in

increasing the efficiency of an organization. Various other tools of management accounting

namely, variance analysis and performance indicators helps in undertaking effective decision

making strategies within an organization. Through the techniques of budgetary control, the

estimations are made on the financial needs of an organization to be incorporated in the

future. The planning tool incorporated in the method of budgetary control helps in controlling

the financial performance of an organization and helps the entity in achieving the desired

results (Hiebl et al. 2013, p.122). Since the budget of an organization is perceived to be an

instrument of control therefore it helps in controlling and measuring the deviations attained

while performing various activities in the organization with respect to planning production

and sales. Various advantages of budgetary control as a planning technique have been

perceived which is enumerated hereafter. Preparation and presentation of the of budgets

which is one of the important planning tools as a part of the budgetary control mechanism

helps the financial manager or the budget coordinator of the organization in coordinating the

resources appropriately ensuring optimum utilization of the resources. Further, the budget

helps in defining the benchmarks or the standards required across different controlling

systems implemented within the organization.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.