Management Accounting: Methods, Systems, and Cost Analysis

VerifiedAdded on 2023/06/08

|17

|4674

|183

AI Summary

This report discusses the role and principles of management accounting, its systems, and different methods of management accounting reporting. It also evaluates costs using marginal and absorption costing methods and elaborates on the merits and demerits of various planning tools used for budgetary control. The report includes a case study of Airdri Group's financial problems and how management accounting can help.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

accounting

accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1 Define management accounting and also give important requirements of various kinds of

management accounting system.............................................................................................3

P2. Different methods that are exploited for the purposes of management accounting

reporting.................................................................................................................................5

P3 Evaluate costs by using adequate methods of cost analysis to prepare an income statement

using marginal and absorption costs.......................................................................................6

P4 Elaborate the merits and demerits of various types of planning tools used for budgetary

control...................................................................................................................................10

P5. Comparing how organisations adapts management accounting systems to respond to

financial problems................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1 Define management accounting and also give important requirements of various kinds of

management accounting system.............................................................................................3

P2. Different methods that are exploited for the purposes of management accounting

reporting.................................................................................................................................5

P3 Evaluate costs by using adequate methods of cost analysis to prepare an income statement

using marginal and absorption costs.......................................................................................6

P4 Elaborate the merits and demerits of various types of planning tools used for budgetary

control...................................................................................................................................10

P5. Comparing how organisations adapts management accounting systems to respond to

financial problems................................................................................................................12

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a concept which is preferred by each and every organisation

in order to make a number of reports by accessing the financial information of the organisation

(Bagherzadegan, and Khanmohammadi, 2019). Airdri Group was established in 1974 by two

mechanical and electrical engineers. Today, it is a family owned organisation operating in UK,

US and China. Stability in environment is main objective to Airdri's continuing product

development. By initiating best practices and performing with honesty Airdri Group try to

accomplish duties towards the environment, providing dependable and innovative commodities

that represents commitment of Airdri group towards wastage, energy saving , reduction in level

of noise and purify air. In the year 2020, Airdri has introduced SteraSpace, a variety of best in

class air and sanitisers for surface, that are build in such a that ensures effective elimination up to

99.6% of harmful bacteria and viruses. The report consists of two parts. The first part includes

the role and principle of management accounting and its systems which are explained in detail

using the techniques and method of marginal and absorption costing. Further, the part is summed

up by describing the integration and benefits of it in the entity. The second part takes into

consideration the different planning tools. Also the financial problems of Airdri Group are

discussed in the following report.

MAIN BODY

P1 Define management accounting and also give important requirements of various kinds of

management accounting system.

Management Accounting

It is also termed as managerial accounting. It is a technique of accounting that assist in

creation of statements, reports and documents that aid management in the process of decision

making which are related to the performance of business. It is mainly utilised for internal

operations of an organisation. It assists the management to perform all its functions including

planning, organizing, staffing, directing and controlling (Baxter, and Chua, 2019).

Role of management accounting and its systems.

It refers to an process that usually centres about observing and evaluating stratified

objectives to refer distinctive monetary and non-monetary data to higher governing body of

organisation. Administrators can uses this information for making various financial plans and

Management accounting is a concept which is preferred by each and every organisation

in order to make a number of reports by accessing the financial information of the organisation

(Bagherzadegan, and Khanmohammadi, 2019). Airdri Group was established in 1974 by two

mechanical and electrical engineers. Today, it is a family owned organisation operating in UK,

US and China. Stability in environment is main objective to Airdri's continuing product

development. By initiating best practices and performing with honesty Airdri Group try to

accomplish duties towards the environment, providing dependable and innovative commodities

that represents commitment of Airdri group towards wastage, energy saving , reduction in level

of noise and purify air. In the year 2020, Airdri has introduced SteraSpace, a variety of best in

class air and sanitisers for surface, that are build in such a that ensures effective elimination up to

99.6% of harmful bacteria and viruses. The report consists of two parts. The first part includes

the role and principle of management accounting and its systems which are explained in detail

using the techniques and method of marginal and absorption costing. Further, the part is summed

up by describing the integration and benefits of it in the entity. The second part takes into

consideration the different planning tools. Also the financial problems of Airdri Group are

discussed in the following report.

MAIN BODY

P1 Define management accounting and also give important requirements of various kinds of

management accounting system.

Management Accounting

It is also termed as managerial accounting. It is a technique of accounting that assist in

creation of statements, reports and documents that aid management in the process of decision

making which are related to the performance of business. It is mainly utilised for internal

operations of an organisation. It assists the management to perform all its functions including

planning, organizing, staffing, directing and controlling (Baxter, and Chua, 2019).

Role of management accounting and its systems.

It refers to an process that usually centres about observing and evaluating stratified

objectives to refer distinctive monetary and non-monetary data to higher governing body of

organisation. Administrators can uses this information for making various financial plans and

implementation of reports. The executive accounting is surely have more unpredicted content as

compared to organised summaries of budget. Main difference between them is that the prior one

is ready in affiliation with inner cycles on the contrary the last one is brought up for outsiders

such as investors. It generally assist in predicting future patterns and incomes of company

function which also advises in making plans related to spending.

The accounting framework is a tool of supervising and effecting employees just as

various costs which are primary for accomplishing important goals. Compulsory implementation

of the accounting framework in Airdri Group is beneficial as it provides different experiences

which helps in direction and organising procedures (Boyle, Boyle, and Hermanson, 2020).

Certain Management accounting systems are as follows:

Cost accounting model is a strategic scheme which assists organisation in estimating

product cost for performing advantageous analysis and valuation of stock. It is beneficial

for Airdri Group as it assists in recognition of items that are advantageous for operations

of business. This system in addition of these also aid accountants of foundation in making

fiscal report. It consists of job request and cycle costing strategies.

Stock administration system is concerned about valuing and accounting changes in stock

at any level of business. Airdri Group includes this model to expand its deals and increase

net revenues. Stock of business are of three types, to be particular, unprocessed

components, work underway and accomplished commodities. Its action is usually

required in organisations to increase operational ability and duration of business projects.

It assists Airdri Group in differentiating direct costs related with acquiring and troughing

away interactivity. It also assists entity in holding additional stock which aids in

happening of inadequacy (Campbell, Mauler, and Pierce, 2019).

Cost streamlining system is a numeral model which assists an organisation in falling

down and evaluating how request vary with respect to the change in level of value of item

or administration. Data collected by this model is adjoined with cost and stock at

recommendations of costs that advises in further development of the productivity. Airdri

includes this system for collecting information regarding trends of market, demands of

clients and propensity to work its operations effectively.

Job costing model is a process of collecting different information regarding subsequent

and disjoining cost with designated work or task. It requires to occupy differential data in

compared to organised summaries of budget. Main difference between them is that the prior one

is ready in affiliation with inner cycles on the contrary the last one is brought up for outsiders

such as investors. It generally assist in predicting future patterns and incomes of company

function which also advises in making plans related to spending.

The accounting framework is a tool of supervising and effecting employees just as

various costs which are primary for accomplishing important goals. Compulsory implementation

of the accounting framework in Airdri Group is beneficial as it provides different experiences

which helps in direction and organising procedures (Boyle, Boyle, and Hermanson, 2020).

Certain Management accounting systems are as follows:

Cost accounting model is a strategic scheme which assists organisation in estimating

product cost for performing advantageous analysis and valuation of stock. It is beneficial

for Airdri Group as it assists in recognition of items that are advantageous for operations

of business. This system in addition of these also aid accountants of foundation in making

fiscal report. It consists of job request and cycle costing strategies.

Stock administration system is concerned about valuing and accounting changes in stock

at any level of business. Airdri Group includes this model to expand its deals and increase

net revenues. Stock of business are of three types, to be particular, unprocessed

components, work underway and accomplished commodities. Its action is usually

required in organisations to increase operational ability and duration of business projects.

It assists Airdri Group in differentiating direct costs related with acquiring and troughing

away interactivity. It also assists entity in holding additional stock which aids in

happening of inadequacy (Campbell, Mauler, and Pierce, 2019).

Cost streamlining system is a numeral model which assists an organisation in falling

down and evaluating how request vary with respect to the change in level of value of item

or administration. Data collected by this model is adjoined with cost and stock at

recommendations of costs that advises in further development of the productivity. Airdri

includes this system for collecting information regarding trends of market, demands of

clients and propensity to work its operations effectively.

Job costing model is a process of collecting different information regarding subsequent

and disjoining cost with designated work or task. It requires to occupy differential data in

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

respect of direct material, cost and upward. Airdri Group includes this system in order to

conclude accuracy of its evaluating system which assists in giving estimations of items of

cost. It also assists organisation in creation of a reasonable advantage. Primary

requirement of this model is an organisation is consistent observation of creation

procedure which assists with identification of issues and making adaption in order to try

not to damage any situations (Chung, and Cho, 2018).

P2. Different methods that are exploited for the purposes of management accounting reporting.

It is used for designing, controlling, decision making purpose and measurement of

performance. These reports are consistently created through the accounting and auditing period

according to necessities. The outcomes of management accounting is in form of periodic reports

for the organisation's department managers and CEO. For instance, current creation of sales

revenue, the recent position or condition of the entity's accounts payable and accounts

receivables etc. Management reporting looks in the business in a more elaborated manner and

represents outcomes from different sections. Instead on focusing on the entire organisation,

management reports emphasis on a specific job, department or team.

Methods used for management accounting reporting are:

Cost report: While doing business in Airdri Group, management accounting examines a

number of costs of producing commodities. On this base, cost report is execute in Airdri Group,

as it analyse all labour costs, raw material besides any form of extra cost in order to maintain

reporting of management accounting. The whole information is then adequately combined with

the cost report. And hence, the technique assists in supervising and planning profit margins.

Performance report: It can be refer to as a descriptive statement which evaluates results

of specific operations which is incidental to the development of company in given time frame.

Management accountants of Airdri Group, making best usage of budgets for comparing real

expenses with revenues which are dependent on budgeted variables and them list or updating

data on basis of performance of report. When a report is prepared, managers design the demand

of its future for consumers and the requirement of a product in market and according to that

makes variations in prices (Lehner, and Harrer, 2019).

Inventory management report: It is an extract of unfinished stock and data of such

amount of stock is approachable, commodities that are sold the most and quickest, category

performance etc. connected to status collectively with demonstration of merchandise. For fruitful

conclude accuracy of its evaluating system which assists in giving estimations of items of

cost. It also assists organisation in creation of a reasonable advantage. Primary

requirement of this model is an organisation is consistent observation of creation

procedure which assists with identification of issues and making adaption in order to try

not to damage any situations (Chung, and Cho, 2018).

P2. Different methods that are exploited for the purposes of management accounting reporting.

It is used for designing, controlling, decision making purpose and measurement of

performance. These reports are consistently created through the accounting and auditing period

according to necessities. The outcomes of management accounting is in form of periodic reports

for the organisation's department managers and CEO. For instance, current creation of sales

revenue, the recent position or condition of the entity's accounts payable and accounts

receivables etc. Management reporting looks in the business in a more elaborated manner and

represents outcomes from different sections. Instead on focusing on the entire organisation,

management reports emphasis on a specific job, department or team.

Methods used for management accounting reporting are:

Cost report: While doing business in Airdri Group, management accounting examines a

number of costs of producing commodities. On this base, cost report is execute in Airdri Group,

as it analyse all labour costs, raw material besides any form of extra cost in order to maintain

reporting of management accounting. The whole information is then adequately combined with

the cost report. And hence, the technique assists in supervising and planning profit margins.

Performance report: It can be refer to as a descriptive statement which evaluates results

of specific operations which is incidental to the development of company in given time frame.

Management accountants of Airdri Group, making best usage of budgets for comparing real

expenses with revenues which are dependent on budgeted variables and them list or updating

data on basis of performance of report. When a report is prepared, managers design the demand

of its future for consumers and the requirement of a product in market and according to that

makes variations in prices (Lehner, and Harrer, 2019).

Inventory management report: It is an extract of unfinished stock and data of such

amount of stock is approachable, commodities that are sold the most and quickest, category

performance etc. connected to status collectively with demonstration of merchandise. For fruitful

growth of Airdri Group, it is essential for management inventory level in accurate and ideally

ways as possible. It is power of purchase manager of the company to make sure that accurate

stock levels are continued in accordance for producing and marketing of various types of

products. The revealing technique that records all kinds of deals which are related to

diversification of inventory to different compartments and their end results.

Budget report: This specific technique plays a important role in management accounting

in Airdri Group for communicating as it emphasis on formulation and diverging the budgets

with different sections of company. The report of budget focuses on execution of Airdri, firm

and is preserved in an entity. Report demonstrate administrator the way to reorganised terms

with suppliers and marketer, better employee incentives and cutting down the cost on

commodities. Directors also operate for up surging the demand in sales and reducing the

expenditure which results in saving of money (Li, 2018).

P3 Evaluate costs by using adequate methods of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost: It can be referred as an amount which can be paid instead of getting product or service.

According to business, cost is evaluation of money with sources, risk obtained, opportunities

forgone, materials, consumption of time and utilities in producing with product delivery or any

services. For examining cost of formulation of income statement, financial analysts utilises

different kinds of techniques and methods.

Absorption Costing: In this method, managers utilises a technique for making external financial

as well as recording of income tax also. Examining of techniques incidental to cost acquires all

cost which is accompanied with production or selling a product (Li, 2022,May).

Profit and loss as per absorption costing method:

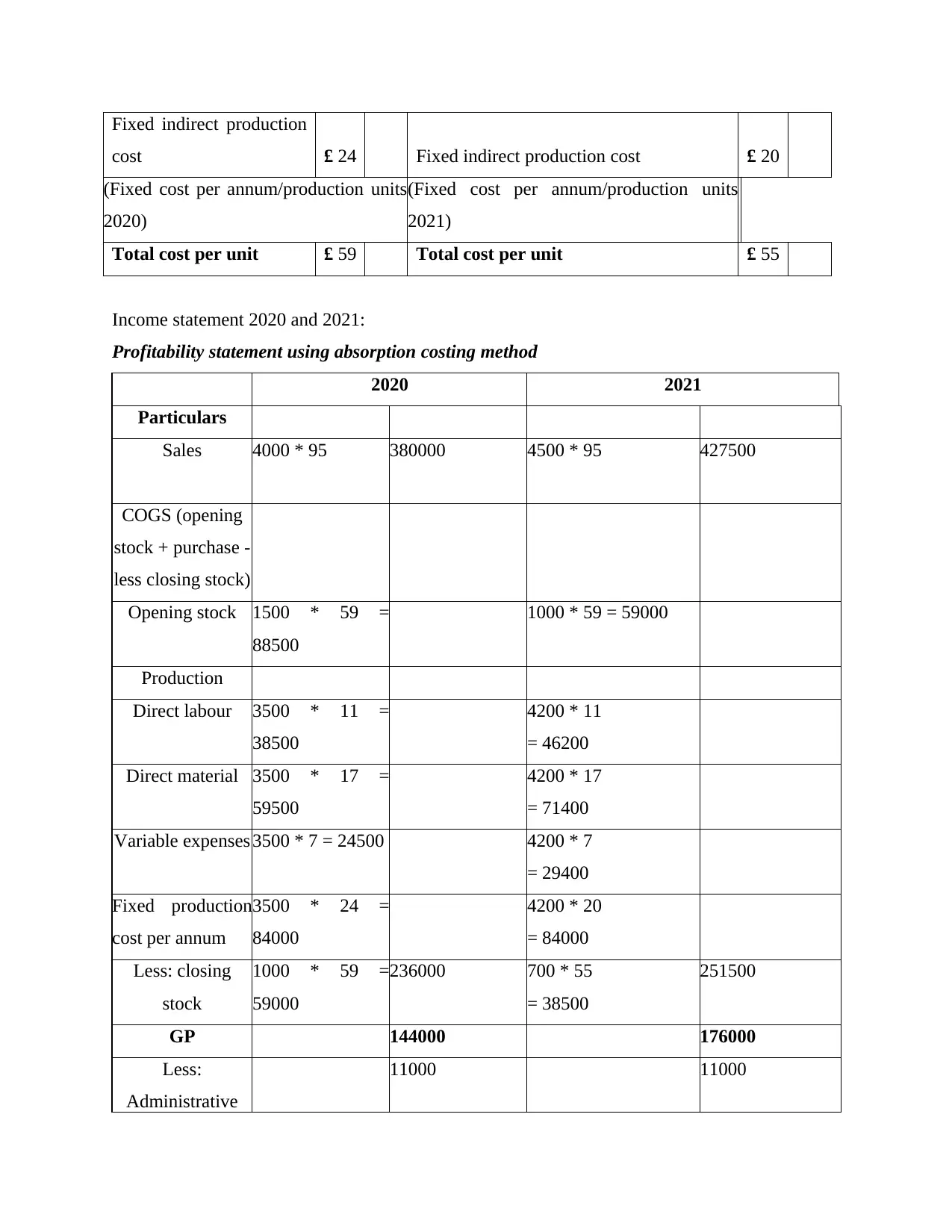

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per

unit(B) Absorption cost per unit (C)

Direct Labour cost £ 11 Direct Labour cost £ 11

Direct material cost £ 17 Direct material cost £ 17

variable expenses £ 7 variable expenses £ 7

ways as possible. It is power of purchase manager of the company to make sure that accurate

stock levels are continued in accordance for producing and marketing of various types of

products. The revealing technique that records all kinds of deals which are related to

diversification of inventory to different compartments and their end results.

Budget report: This specific technique plays a important role in management accounting

in Airdri Group for communicating as it emphasis on formulation and diverging the budgets

with different sections of company. The report of budget focuses on execution of Airdri, firm

and is preserved in an entity. Report demonstrate administrator the way to reorganised terms

with suppliers and marketer, better employee incentives and cutting down the cost on

commodities. Directors also operate for up surging the demand in sales and reducing the

expenditure which results in saving of money (Li, 2018).

P3 Evaluate costs by using adequate methods of cost analysis to prepare an income statement

using marginal and absorption costs.

Cost: It can be referred as an amount which can be paid instead of getting product or service.

According to business, cost is evaluation of money with sources, risk obtained, opportunities

forgone, materials, consumption of time and utilities in producing with product delivery or any

services. For examining cost of formulation of income statement, financial analysts utilises

different kinds of techniques and methods.

Absorption Costing: In this method, managers utilises a technique for making external financial

as well as recording of income tax also. Examining of techniques incidental to cost acquires all

cost which is accompanied with production or selling a product (Li, 2022,May).

Profit and loss as per absorption costing method:

Cost per unit -Absorption costing approach

2020 2021

Absorption cost per

unit(B) Absorption cost per unit (C)

Direct Labour cost £ 11 Direct Labour cost £ 11

Direct material cost £ 17 Direct material cost £ 17

variable expenses £ 7 variable expenses £ 7

Fixed indirect production

cost £ 24 Fixed indirect production cost £ 20

(Fixed cost per annum/production units

2020)

(Fixed cost per annum/production units

2021)

Total cost per unit £ 59 Total cost per unit £ 55

Income statement 2020 and 2021:

Profitability statement using absorption costing method

2020 2021

Particulars

Sales 4000 * 95 380000 4500 * 95 427500

COGS (opening

stock + purchase -

less closing stock)

Opening stock 1500 * 59 =

88500

1000 * 59 = 59000

Production

Direct labour 3500 * 11 =

38500

4200 * 11

= 46200

Direct material 3500 * 17 =

59500

4200 * 17

= 71400

Variable expenses 3500 * 7 = 24500 4200 * 7

= 29400

Fixed production

cost per annum

3500 * 24 =

84000

4200 * 20

= 84000

Less: closing

stock

1000 * 59 =

59000

236000 700 * 55

= 38500

251500

GP 144000 176000

Less:

Administrative

11000 11000

cost £ 24 Fixed indirect production cost £ 20

(Fixed cost per annum/production units

2020)

(Fixed cost per annum/production units

2021)

Total cost per unit £ 59 Total cost per unit £ 55

Income statement 2020 and 2021:

Profitability statement using absorption costing method

2020 2021

Particulars

Sales 4000 * 95 380000 4500 * 95 427500

COGS (opening

stock + purchase -

less closing stock)

Opening stock 1500 * 59 =

88500

1000 * 59 = 59000

Production

Direct labour 3500 * 11 =

38500

4200 * 11

= 46200

Direct material 3500 * 17 =

59500

4200 * 17

= 71400

Variable expenses 3500 * 7 = 24500 4200 * 7

= 29400

Fixed production

cost per annum

3500 * 24 =

84000

4200 * 20

= 84000

Less: closing

stock

1000 * 59 =

59000

236000 700 * 55

= 38500

251500

GP 144000 176000

Less:

Administrative

11000 11000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

overhead

Net Profit 133000 165000

Marginal costing: The cost analyse technique in which fixed costs of period and variable cost

are forced on units, cost are changed in complete manner in opposed to offering is referred as to

marginal costing. This method is used for analysing conditions wherein break even point is

equals with fixed costs. It implied additional costs that are part in production of extra output

units(Ling, 2021, April).

Profit and loss as per marginal costing method:

Calculation of opening and closing inventory units

2020 2021

Opening stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock

(Closing stock = opening

stock + production – Sales ) 1000 700

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

Direct Labour cost £ 11

Direct material cost £ 17

variable expenses £ 7

Total cost per unit £ 35

Income statement 2020:

Sales (4000 X 95) 380000

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1500 x 35) 52500

Net Profit 133000 165000

Marginal costing: The cost analyse technique in which fixed costs of period and variable cost

are forced on units, cost are changed in complete manner in opposed to offering is referred as to

marginal costing. This method is used for analysing conditions wherein break even point is

equals with fixed costs. It implied additional costs that are part in production of extra output

units(Ling, 2021, April).

Profit and loss as per marginal costing method:

Calculation of opening and closing inventory units

2020 2021

Opening stock 1,500.00 1000

production 3,500.00 4,200.00

sales 4,000.00 4,500.00

closing stock

(Closing stock = opening

stock + production – Sales ) 1000 700

Cost per unit -Marginal costing approach

2020/2021

Marginal cost per unit (A)

Direct Labour cost £ 11

Direct material cost £ 17

variable expenses £ 7

Total cost per unit £ 35

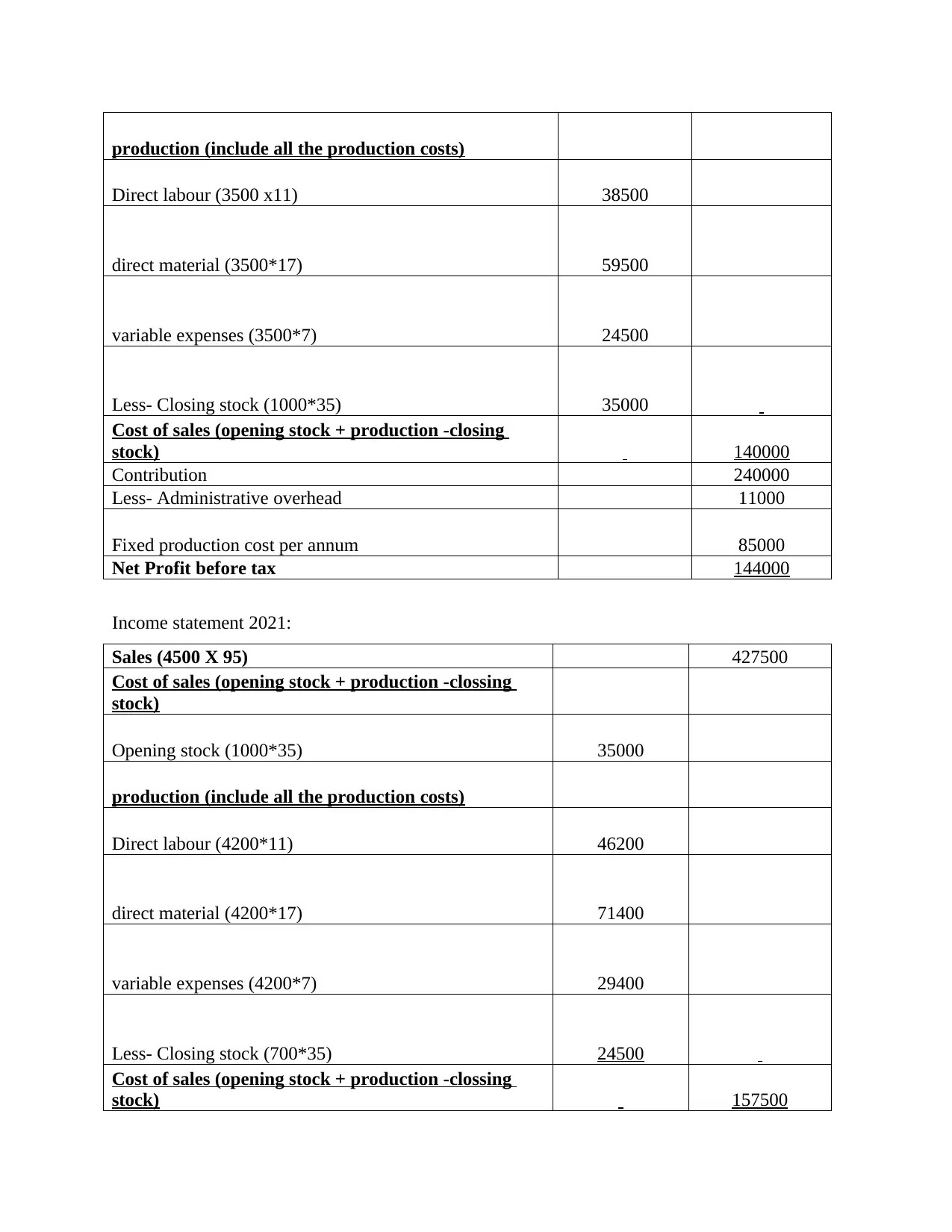

Income statement 2020:

Sales (4000 X 95) 380000

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1500 x 35) 52500

production (include all the production costs)

Direct labour (3500 x11) 38500

direct material (3500*17) 59500

variable expenses (3500*7) 24500

Less- Closing stock (1000*35) 35000

Cost of sales (opening stock + production -closing

stock) 140000

Contribution 240000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 144000

Income statement 2021:

Sales (4500 X 95) 427500

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1000*35) 35000

production (include all the production costs)

Direct labour (4200*11) 46200

direct material (4200*17) 71400

variable expenses (4200*7) 29400

Less- Closing stock (700*35) 24500

Cost of sales (opening stock + production -clossing

stock) 157500

Direct labour (3500 x11) 38500

direct material (3500*17) 59500

variable expenses (3500*7) 24500

Less- Closing stock (1000*35) 35000

Cost of sales (opening stock + production -closing

stock) 140000

Contribution 240000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 144000

Income statement 2021:

Sales (4500 X 95) 427500

Cost of sales (opening stock + production -clossing

stock)

Opening stock (1000*35) 35000

production (include all the production costs)

Direct labour (4200*11) 46200

direct material (4200*17) 71400

variable expenses (4200*7) 29400

Less- Closing stock (700*35) 24500

Cost of sales (opening stock + production -clossing

stock) 157500

Contribution 270000

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 174000

P4 Elaborate the merits and demerits of various types of planning tools used for budgetary

control.

Budgetary control process

The finance department of the organisation incorporates a variety of budgets for different

activities. On basis of which it takes corrective and directive actions for the company. A

responsibility centres are identified for a operational unit which is lead by a team leader who is

held responsible. In simple words it is a technique where actual results are being compared with

budgeted result (Montenegro, and Rodrigues, 2020).There are a number of methods, techniques,

planning tools, used in budgetary control which can effect the result in economical and effectual

operations of a business. There are many benefit and demerits which are connected with

budgetary control which assists the organisation to develop, expand and which can also create

hurdles in the path. Budgetary control is the utilisation of actual expenditure with some levels

which are strictly set up the organisation. Planning tools are the instruments which provides

measurement and following up the operations for implementing a specific plan or project.

Executives of Airdri Group are using various kinds of planning tools for the adequate control of

the budgeting system. Some planning tools are discussed below:

Operating budget: It can be termed as a budget which is in accordance with all the

operating revenues and activities related to expense as well. Supervisors of Airdri Group

use this budget for managing and controlling expense related activities in relation to

business. It also assists in forecasting of issues which are incidental to future happenings,

expenses and take preventive course of actions in advance(Narayanan, and Boyce,

2019). There are three major elements of operating budget which can be termed as

revenue, variable costs, fixed costs. There are some benefits and demerits for Airdri

Group:

Advantages Disadvantages

Less- Administrative overhead 11000

Fixed production cost per annum 85000

Net Profit before tax 174000

P4 Elaborate the merits and demerits of various types of planning tools used for budgetary

control.

Budgetary control process

The finance department of the organisation incorporates a variety of budgets for different

activities. On basis of which it takes corrective and directive actions for the company. A

responsibility centres are identified for a operational unit which is lead by a team leader who is

held responsible. In simple words it is a technique where actual results are being compared with

budgeted result (Montenegro, and Rodrigues, 2020).There are a number of methods, techniques,

planning tools, used in budgetary control which can effect the result in economical and effectual

operations of a business. There are many benefit and demerits which are connected with

budgetary control which assists the organisation to develop, expand and which can also create

hurdles in the path. Budgetary control is the utilisation of actual expenditure with some levels

which are strictly set up the organisation. Planning tools are the instruments which provides

measurement and following up the operations for implementing a specific plan or project.

Executives of Airdri Group are using various kinds of planning tools for the adequate control of

the budgeting system. Some planning tools are discussed below:

Operating budget: It can be termed as a budget which is in accordance with all the

operating revenues and activities related to expense as well. Supervisors of Airdri Group

use this budget for managing and controlling expense related activities in relation to

business. It also assists in forecasting of issues which are incidental to future happenings,

expenses and take preventive course of actions in advance(Narayanan, and Boyce,

2019). There are three major elements of operating budget which can be termed as

revenue, variable costs, fixed costs. There are some benefits and demerits for Airdri

Group:

Advantages Disadvantages

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

It can have a fruitful result in Airdri

Group for calculating costs and

management on expenses of the

business functional activities for

accomplishing the main motive of

business in the long period of time. This

method can assists in making the best

available possibility to enlarge business.

It is not suitable for Airdri Group as it do not

encourage any assistance for evaluating the difference

between standard and actual costs. This method is not

considered suitable and is not flexible in nature and

working. Modifications cannot be made in policies

which are formed during the year.

Zero based budgeting: Zero based budgeting is a method which explains the reasons of

the expenses which are incurred in the financial year (Ng, 2018). It is used by Airdri

Group for examining the best possible usage of resources distributed at different places.

There are certain merits and demerits for Airdri Group:

Advantage Disadvantages

This method assists Airdri Group in

determining the areas which aid in creation of

profits and the operational activities in which it

utilized. This provides a better, clearer and

more applicable data for understanding the

working of company and analysing of business

performance that would assists in management

of the budgets and have a proper control over

them.

It is understood as a challenging, time

consuming and an pricey process. It is

considered as tough task to detailed the usage

of expenses and creation of profit in budgets.

Any decrement in the profit margin or revenue

of the company can effect the brand image of

the company.

Capital budgeting: It is an assessment acknowledged by an organisation for the

determination and estimation of potential for essential projects and investments. For

instance, planning for investing a huge amount in machinery and new technology for long

term success of operations of entity (Padovani, and Iacuzzi, 2021). This technique

assists Airdri Group in researching and selection of beneficial decisions for

Group for calculating costs and

management on expenses of the

business functional activities for

accomplishing the main motive of

business in the long period of time. This

method can assists in making the best

available possibility to enlarge business.

It is not suitable for Airdri Group as it do not

encourage any assistance for evaluating the difference

between standard and actual costs. This method is not

considered suitable and is not flexible in nature and

working. Modifications cannot be made in policies

which are formed during the year.

Zero based budgeting: Zero based budgeting is a method which explains the reasons of

the expenses which are incurred in the financial year (Ng, 2018). It is used by Airdri

Group for examining the best possible usage of resources distributed at different places.

There are certain merits and demerits for Airdri Group:

Advantage Disadvantages

This method assists Airdri Group in

determining the areas which aid in creation of

profits and the operational activities in which it

utilized. This provides a better, clearer and

more applicable data for understanding the

working of company and analysing of business

performance that would assists in management

of the budgets and have a proper control over

them.

It is understood as a challenging, time

consuming and an pricey process. It is

considered as tough task to detailed the usage

of expenses and creation of profit in budgets.

Any decrement in the profit margin or revenue

of the company can effect the brand image of

the company.

Capital budgeting: It is an assessment acknowledged by an organisation for the

determination and estimation of potential for essential projects and investments. For

instance, planning for investing a huge amount in machinery and new technology for long

term success of operations of entity (Padovani, and Iacuzzi, 2021). This technique

assists Airdri Group in researching and selection of beneficial decisions for

accomplishing long term success of organisation. Its merits and demerits in context

Airdri Group are:

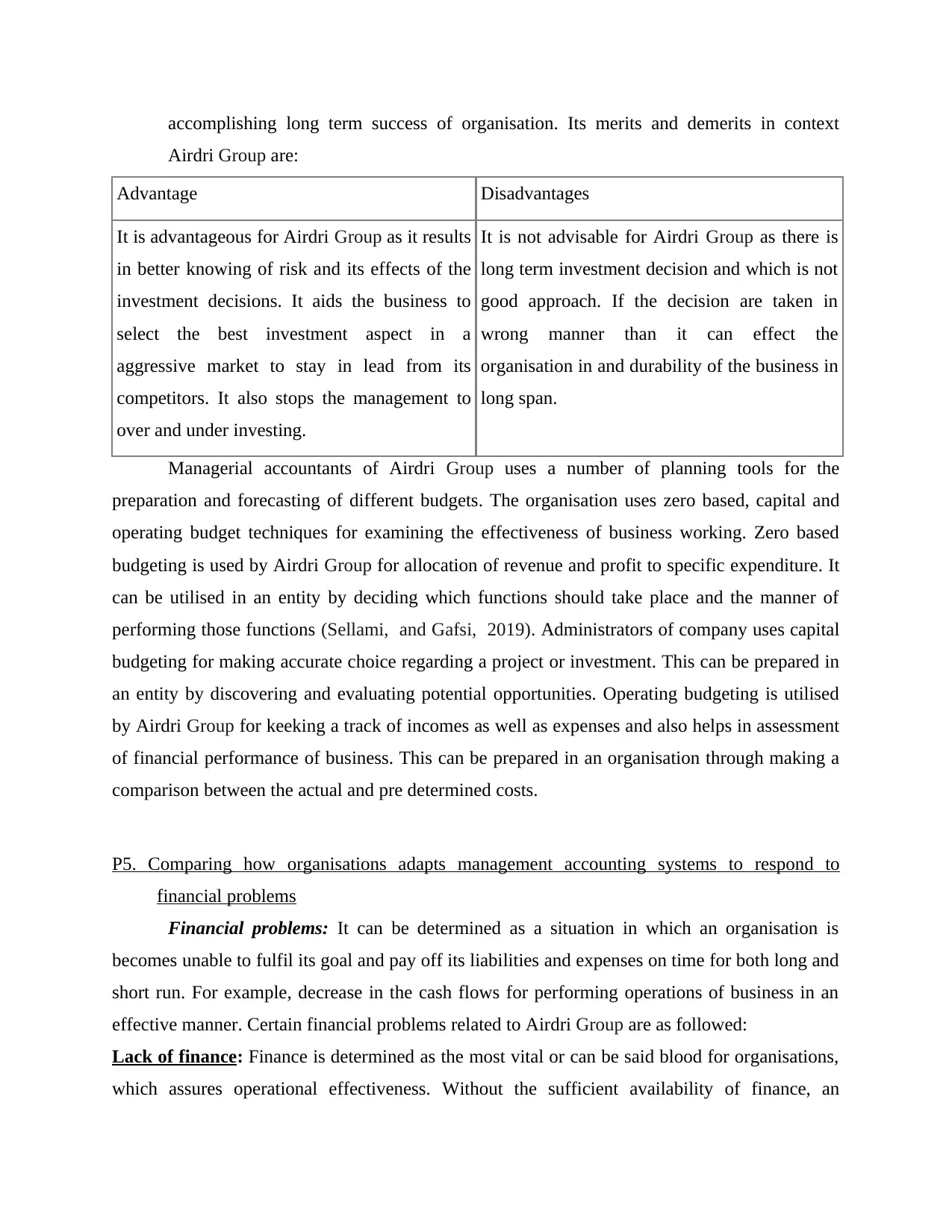

Advantage Disadvantages

It is advantageous for Airdri Group as it results

in better knowing of risk and its effects of the

investment decisions. It aids the business to

select the best investment aspect in a

aggressive market to stay in lead from its

competitors. It also stops the management to

over and under investing.

It is not advisable for Airdri Group as there is

long term investment decision and which is not

good approach. If the decision are taken in

wrong manner than it can effect the

organisation in and durability of the business in

long span.

Managerial accountants of Airdri Group uses a number of planning tools for the

preparation and forecasting of different budgets. The organisation uses zero based, capital and

operating budget techniques for examining the effectiveness of business working. Zero based

budgeting is used by Airdri Group for allocation of revenue and profit to specific expenditure. It

can be utilised in an entity by deciding which functions should take place and the manner of

performing those functions (Sellami, and Gafsi, 2019). Administrators of company uses capital

budgeting for making accurate choice regarding a project or investment. This can be prepared in

an entity by discovering and evaluating potential opportunities. Operating budgeting is utilised

by Airdri Group for keeking a track of incomes as well as expenses and also helps in assessment

of financial performance of business. This can be prepared in an organisation through making a

comparison between the actual and pre determined costs.

P5. Comparing how organisations adapts management accounting systems to respond to

financial problems

Financial problems: It can be determined as a situation in which an organisation is

becomes unable to fulfil its goal and pay off its liabilities and expenses on time for both long and

short run. For example, decrease in the cash flows for performing operations of business in an

effective manner. Certain financial problems related to Airdri Group are as followed:

Lack of finance: Finance is determined as the most vital or can be said blood for organisations,

which assures operational effectiveness. Without the sufficient availability of finance, an

Airdri Group are:

Advantage Disadvantages

It is advantageous for Airdri Group as it results

in better knowing of risk and its effects of the

investment decisions. It aids the business to

select the best investment aspect in a

aggressive market to stay in lead from its

competitors. It also stops the management to

over and under investing.

It is not advisable for Airdri Group as there is

long term investment decision and which is not

good approach. If the decision are taken in

wrong manner than it can effect the

organisation in and durability of the business in

long span.

Managerial accountants of Airdri Group uses a number of planning tools for the

preparation and forecasting of different budgets. The organisation uses zero based, capital and

operating budget techniques for examining the effectiveness of business working. Zero based

budgeting is used by Airdri Group for allocation of revenue and profit to specific expenditure. It

can be utilised in an entity by deciding which functions should take place and the manner of

performing those functions (Sellami, and Gafsi, 2019). Administrators of company uses capital

budgeting for making accurate choice regarding a project or investment. This can be prepared in

an entity by discovering and evaluating potential opportunities. Operating budgeting is utilised

by Airdri Group for keeking a track of incomes as well as expenses and also helps in assessment

of financial performance of business. This can be prepared in an organisation through making a

comparison between the actual and pre determined costs.

P5. Comparing how organisations adapts management accounting systems to respond to

financial problems

Financial problems: It can be determined as a situation in which an organisation is

becomes unable to fulfil its goal and pay off its liabilities and expenses on time for both long and

short run. For example, decrease in the cash flows for performing operations of business in an

effective manner. Certain financial problems related to Airdri Group are as followed:

Lack of finance: Finance is determined as the most vital or can be said blood for organisations,

which assures operational effectiveness. Without the sufficient availability of finance, an

organisation cannot think of its expansion and further development. Even inadequate finance

can create issues in day to day operations of Airdri Group.

Mismanagement of cash flow: This method can lead Airdri Group towards the path of

inefficiency and diversification of activities in various areas. Improper management of cash flow

can results in confusion and default in reporting of operations of business. It is a important

financial problem which seriously effects performance of business.

Excessive Debts: It can create a great financial problem to entity. Highly indebtedness of funds

can lead limits Airdri Group in keeping its short as well as long run liabilities and even creates a

situation of bankruptcy. This financial issue can also create obstacle in meeting daily operations

of an organisation.

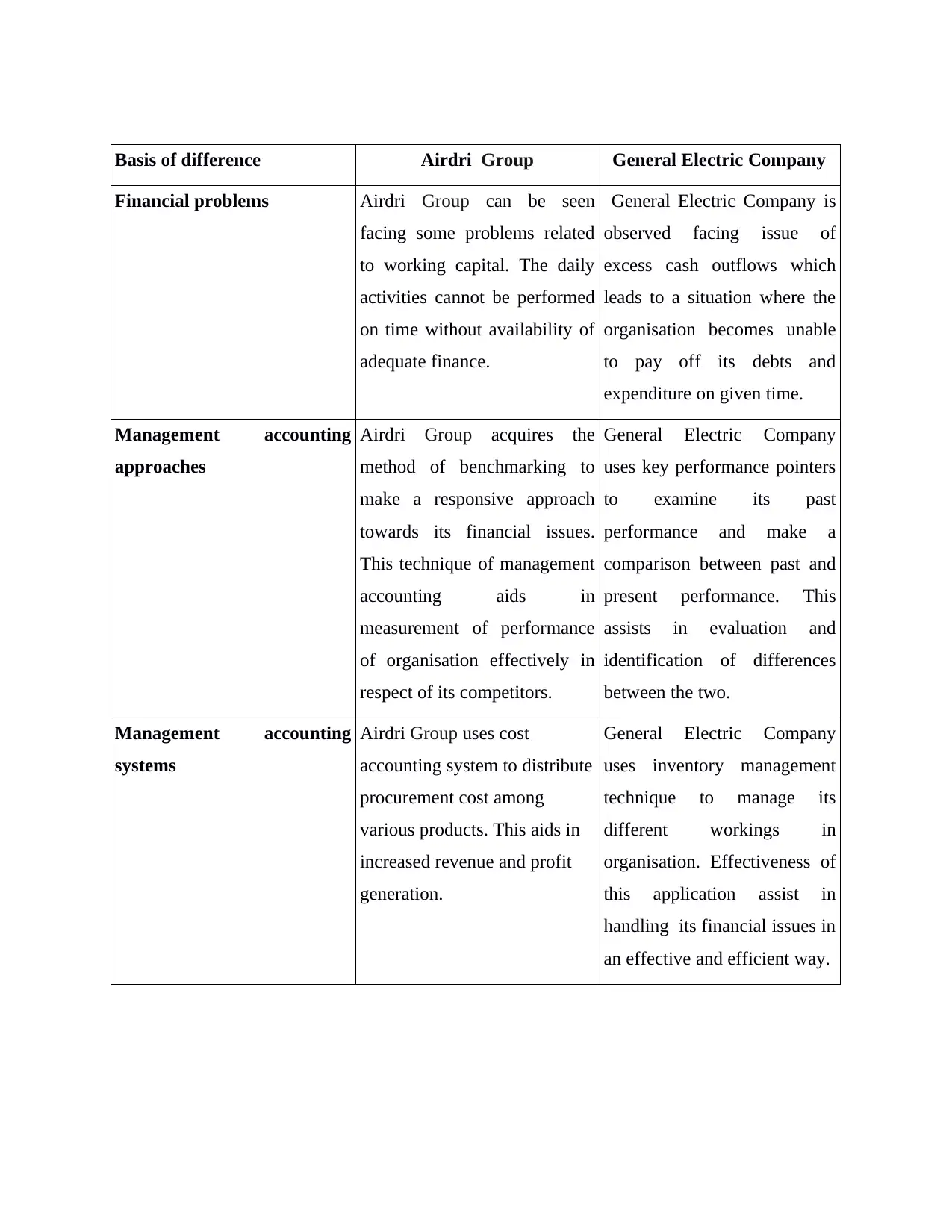

Approaches of management accounting used by Airdri Group are as follows:

1. Financial governance: This includes the policies and processes that assists an entity in

keeping track of financial transactions and vents, performance of management and ,

monitoring of different operations. Ineffectiveness of this methods limits Airdri Group in

examining and gathering correct information about the financial transactions. Risk can be

identifies at a faster pace as compared to its competitors if this approach is approach is

implemented in an effective manner (Triantafillou, 2022).

2. Key performance pointers: This indicates the set of quantifiable techniques that assists

an enterprise in measurement of its overall performance. These are traced by automatic

software's and various analytical techniques. It is advantageous for Airdri Group as it

assists in formulation of organisations goals and also evaluates execution in operations.

3. Benchmarking: It is expressed as an method of making comparison between products,

services and strategies of company those organisations who are determined as leaders in

the industry. Airdri Group utilises this technique in their workings as it assists in reducing

performance gaps which leads to identification of areas which are required to have

modifications in them.

Comparison of different entities for applying management accounting system in resolving

a number of financial issues.

can create issues in day to day operations of Airdri Group.

Mismanagement of cash flow: This method can lead Airdri Group towards the path of

inefficiency and diversification of activities in various areas. Improper management of cash flow

can results in confusion and default in reporting of operations of business. It is a important

financial problem which seriously effects performance of business.

Excessive Debts: It can create a great financial problem to entity. Highly indebtedness of funds

can lead limits Airdri Group in keeping its short as well as long run liabilities and even creates a

situation of bankruptcy. This financial issue can also create obstacle in meeting daily operations

of an organisation.

Approaches of management accounting used by Airdri Group are as follows:

1. Financial governance: This includes the policies and processes that assists an entity in

keeping track of financial transactions and vents, performance of management and ,

monitoring of different operations. Ineffectiveness of this methods limits Airdri Group in

examining and gathering correct information about the financial transactions. Risk can be

identifies at a faster pace as compared to its competitors if this approach is approach is

implemented in an effective manner (Triantafillou, 2022).

2. Key performance pointers: This indicates the set of quantifiable techniques that assists

an enterprise in measurement of its overall performance. These are traced by automatic

software's and various analytical techniques. It is advantageous for Airdri Group as it

assists in formulation of organisations goals and also evaluates execution in operations.

3. Benchmarking: It is expressed as an method of making comparison between products,

services and strategies of company those organisations who are determined as leaders in

the industry. Airdri Group utilises this technique in their workings as it assists in reducing

performance gaps which leads to identification of areas which are required to have

modifications in them.

Comparison of different entities for applying management accounting system in resolving

a number of financial issues.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Basis of difference Airdri Group General Electric Company

Financial problems Airdri Group can be seen

facing some problems related

to working capital. The daily

activities cannot be performed

on time without availability of

adequate finance.

General Electric Company is

observed facing issue of

excess cash outflows which

leads to a situation where the

organisation becomes unable

to pay off its debts and

expenditure on given time.

Management accounting

approaches

Airdri Group acquires the

method of benchmarking to

make a responsive approach

towards its financial issues.

This technique of management

accounting aids in

measurement of performance

of organisation effectively in

respect of its competitors.

General Electric Company

uses key performance pointers

to examine its past

performance and make a

comparison between past and

present performance. This

assists in evaluation and

identification of differences

between the two.

Management accounting

systems

Airdri Group uses cost

accounting system to distribute

procurement cost among

various products. This aids in

increased revenue and profit

generation.

General Electric Company

uses inventory management

technique to manage its

different workings in

organisation. Effectiveness of

this application assist in

handling its financial issues in

an effective and efficient way.

Financial problems Airdri Group can be seen

facing some problems related

to working capital. The daily

activities cannot be performed

on time without availability of

adequate finance.

General Electric Company is

observed facing issue of

excess cash outflows which

leads to a situation where the

organisation becomes unable

to pay off its debts and

expenditure on given time.

Management accounting

approaches

Airdri Group acquires the

method of benchmarking to

make a responsive approach

towards its financial issues.

This technique of management

accounting aids in

measurement of performance

of organisation effectively in

respect of its competitors.

General Electric Company

uses key performance pointers

to examine its past

performance and make a

comparison between past and

present performance. This

assists in evaluation and

identification of differences

between the two.

Management accounting

systems

Airdri Group uses cost

accounting system to distribute

procurement cost among

various products. This aids in

increased revenue and profit

generation.

General Electric Company

uses inventory management

technique to manage its

different workings in

organisation. Effectiveness of

this application assist in

handling its financial issues in

an effective and efficient way.

CONCLUSION

The above prepared report concludes a brief discussion of Airdri Group, the meaning of

management accounting and need of various kinds of man accounting systems in Airdri Group.

It also consists of different techniques used in the process of management accounting reporting.

It also discloses the techniques of cost analysis like marginal costing and absorption costing used

in the preparation of income statement. The following report also contains the advantages and

disadvantages of various types of planning tools applied in budgetary control. It also represents a

comparison on the way organisations adopts management accounting systems to overcome

financial problems.

The above prepared report concludes a brief discussion of Airdri Group, the meaning of

management accounting and need of various kinds of man accounting systems in Airdri Group.

It also consists of different techniques used in the process of management accounting reporting.

It also discloses the techniques of cost analysis like marginal costing and absorption costing used

in the preparation of income statement. The following report also contains the advantages and

disadvantages of various types of planning tools applied in budgetary control. It also represents a

comparison on the way organisations adopts management accounting systems to overcome

financial problems.

REFERENCES

Books and Journals

Bagherzadegan, R. and Khanmohammadi, M.H., 2019. Investigate the relationship between the

quality of accounting information and corporate governance by investing in the main

operations of the company. Management Accounting, 12(40). pp.1-14.

Baxter, J. and Chua, W.F., 2019. Using critical realism in critical accounting research–a

commentary by two ANTs. Accounting, Auditing & Accountability Journal, 33(3).

pp.655-665.

Boyle, D.M., Boyle, J.F. and Hermanson, D.R., 2020. How to publish in peer-reviewed

practitioner accounting journals. Issues in Accounting Education, 35(2). pp.19-30.

Campbell, J.L., Mauler, L.M. and Pierce, S.R., 2019. A review of derivatives research in

accounting and suggestions for future work. Journal of Accounting Literature.

Chung, J. and Cho, C.H., 2018. Current trends within social and environmental accounting

research: a literature review. Accounting Perspectives, 17(2). pp.207-239.

Lehner, O.M. and Harrer, T., 2019. Accounting for economic sustainability: environmental,

social and governance perspectives. Journal of applied accounting research.

Li, H., 2018. Unconditional accounting conservatism and real earnings

management. International journal of financial research, 9(2). pp.203-215.

Li, S., 2022, May. Construction of Accounting Technology Block Analysis System Under the

Background of Big Data Cloud Computing. In 2022 International Conference on

Applied Artificial Intelligence and Computing (ICAAIC) (pp. 767-770). IEEE.

Ling, J., 2021, April. Exploring the Role of Accounting Review in Financial Management.

In 2021 2nd Asia-Pacific Conference on Image Processing, Electronics and

Computers (pp. 695-698).

Montenegro, T.M. and Rodrigues, L.L., 2020. Determinants of the attitudes of Portuguese

accounting students and professionals towards earnings management. Journal of

Academic Ethics, 18(3). pp.301-332.

Narayanan, V. and Boyce, G., 2019. Exploring the transformative potential of management

control systems in organisational change towards sustainability. Accounting, Auditing

& Accountability Journal.

Ng, A.W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of cleaner

production, 195. pp.585-592.

Padovani, E. and Iacuzzi, S., 2021. Real-time crisis management: Testing the role of accounting

in local governments. Journal of Accounting and Public Policy, 40(3). p.106854.

Sellami, Y.M. and Gafsi, Y., 2019. Public management systems, accounting education, and

compliance with international public sector accounting standards in sub-Saharan

Africa. International Journal of Public Sector Management.

Triantafillou, P., 2022. Accounting for value-based management of healthcare services:

challenging neoliberal government from within?. Public Money & Management, 42(3).

pp.199-208.

(Bagherzadegan, and Khanmohammadi, 2019) (Baxter, and Chua, 2019) (Boyle, Boyle, and

Hermanson, 2020) (Campbell, Mauler, and Pierce, 2019) (Chung, and Cho, 2018)

Books and Journals

Bagherzadegan, R. and Khanmohammadi, M.H., 2019. Investigate the relationship between the

quality of accounting information and corporate governance by investing in the main

operations of the company. Management Accounting, 12(40). pp.1-14.

Baxter, J. and Chua, W.F., 2019. Using critical realism in critical accounting research–a

commentary by two ANTs. Accounting, Auditing & Accountability Journal, 33(3).

pp.655-665.

Boyle, D.M., Boyle, J.F. and Hermanson, D.R., 2020. How to publish in peer-reviewed

practitioner accounting journals. Issues in Accounting Education, 35(2). pp.19-30.

Campbell, J.L., Mauler, L.M. and Pierce, S.R., 2019. A review of derivatives research in

accounting and suggestions for future work. Journal of Accounting Literature.

Chung, J. and Cho, C.H., 2018. Current trends within social and environmental accounting

research: a literature review. Accounting Perspectives, 17(2). pp.207-239.

Lehner, O.M. and Harrer, T., 2019. Accounting for economic sustainability: environmental,

social and governance perspectives. Journal of applied accounting research.

Li, H., 2018. Unconditional accounting conservatism and real earnings

management. International journal of financial research, 9(2). pp.203-215.

Li, S., 2022, May. Construction of Accounting Technology Block Analysis System Under the

Background of Big Data Cloud Computing. In 2022 International Conference on

Applied Artificial Intelligence and Computing (ICAAIC) (pp. 767-770). IEEE.

Ling, J., 2021, April. Exploring the Role of Accounting Review in Financial Management.

In 2021 2nd Asia-Pacific Conference on Image Processing, Electronics and

Computers (pp. 695-698).

Montenegro, T.M. and Rodrigues, L.L., 2020. Determinants of the attitudes of Portuguese

accounting students and professionals towards earnings management. Journal of

Academic Ethics, 18(3). pp.301-332.

Narayanan, V. and Boyce, G., 2019. Exploring the transformative potential of management

control systems in organisational change towards sustainability. Accounting, Auditing

& Accountability Journal.

Ng, A.W., 2018. From sustainability accounting to a green financing system: Institutional

legitimacy and market heterogeneity in a global financial centre. Journal of cleaner

production, 195. pp.585-592.

Padovani, E. and Iacuzzi, S., 2021. Real-time crisis management: Testing the role of accounting

in local governments. Journal of Accounting and Public Policy, 40(3). p.106854.

Sellami, Y.M. and Gafsi, Y., 2019. Public management systems, accounting education, and

compliance with international public sector accounting standards in sub-Saharan

Africa. International Journal of Public Sector Management.

Triantafillou, P., 2022. Accounting for value-based management of healthcare services:

challenging neoliberal government from within?. Public Money & Management, 42(3).

pp.199-208.

(Bagherzadegan, and Khanmohammadi, 2019) (Baxter, and Chua, 2019) (Boyle, Boyle, and

Hermanson, 2020) (Campbell, Mauler, and Pierce, 2019) (Chung, and Cho, 2018)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(Lehner, and Harrer, 2019) (Li, 2018) (Li, 2022,May) (Ling, 2021, April)

(Montenegro, and Rodrigues, 2020) (Narayanan, and Boyce, 2019) (Ng, 2018)

(Padovani, and Iacuzzi, 2021) (Sellami, and Gafsi, 2019) (Triantafillou, 2022)

(Montenegro, and Rodrigues, 2020) (Narayanan, and Boyce, 2019) (Ng, 2018)

(Padovani, and Iacuzzi, 2021) (Sellami, and Gafsi, 2019) (Triantafillou, 2022)

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.