Management Accounting: Cost Analysis, Budgetary Control Methods

VerifiedAdded on 2023/06/18

|14

|3784

|59

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its definition, requirements, and differences from financial accounting. It explores various management accounting systems like cost accounting, job costing, inventory management, and price optimization. The report also analyzes methods for management accounting reporting, including budget reports, accounts receivable aging, inventory reports, job cost reports, operating budget reports, profit and loss statements, and performance reports. Furthermore, it calculates costs using marginal and absorption costing techniques to prepare income statements. The advantages and disadvantages of planning tools for budgetary control, such as activity-based budgeting, are discussed. Finally, it examines how organizations use management accounting systems to address financial challenges. Desklib is a platform where students can find similar solved assignments and study tools.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Definition of management accounting and provide requirements of different types of

management accounting systems.................................................................................................3

Various methods used for management accounting reporting.....................................................5

Calculating costs using techniques of cost analysis to make income statement using absorption

and marginal costs........................................................................................................................7

Advantages and disadvantages of various planning tools which can be used for budgetary

control..........................................................................................................................................9

Organisations are adopting management accounting systems to respond to various financial

problems.....................................................................................................................................11

Conclusion ....................................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

Definition of management accounting and provide requirements of different types of

management accounting systems.................................................................................................3

Various methods used for management accounting reporting.....................................................5

Calculating costs using techniques of cost analysis to make income statement using absorption

and marginal costs........................................................................................................................7

Advantages and disadvantages of various planning tools which can be used for budgetary

control..........................................................................................................................................9

Organisations are adopting management accounting systems to respond to various financial

problems.....................................................................................................................................11

Conclusion ....................................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is the process or procedure to identify, measures, evaluate and

use and communicate financial information to the leaders or managers of the company in order to

fulfil goals or objectives of the organisation. It is different from financial accounting because the

aim of managerial accounting is to help internal users of the organisation so that they can make

better decisions (Allain, Lemaire and Lux, 2021). Marks and Spenser is the multinational

company and is famous across the globe. Company deals in clothing, footwear, accessories,

perfumes, bags etc. this company is famous for its good quality of products and have good

financial position. It has good market reputation. this report will discuss the concept of

management accounting and the requirement of different management accounting system.

Further it will analyse methods used for management accounting reporting and calculate costs to

make income statements using absorption and marginal costs. It will also discuss advantages and

disadvantages of various types of planning tools used for budgetary control and how organisation

is helpful in solving financial problems.

MAIN BODY

Definition of management accounting and provide requirements of different types of

management accounting systems.

Management accounting:

It is the process so that various information of the organisation can be used like variance

analysis, budget reporting, inventory reports etc so that financial data can be generated which

helps in the decision making process of the business so that they can successfully run its

Management accounting is the process or procedure to identify, measures, evaluate and

use and communicate financial information to the leaders or managers of the company in order to

fulfil goals or objectives of the organisation. It is different from financial accounting because the

aim of managerial accounting is to help internal users of the organisation so that they can make

better decisions (Allain, Lemaire and Lux, 2021). Marks and Spenser is the multinational

company and is famous across the globe. Company deals in clothing, footwear, accessories,

perfumes, bags etc. this company is famous for its good quality of products and have good

financial position. It has good market reputation. this report will discuss the concept of

management accounting and the requirement of different management accounting system.

Further it will analyse methods used for management accounting reporting and calculate costs to

make income statements using absorption and marginal costs. It will also discuss advantages and

disadvantages of various types of planning tools used for budgetary control and how organisation

is helpful in solving financial problems.

MAIN BODY

Definition of management accounting and provide requirements of different types of

management accounting systems.

Management accounting:

It is the process so that various information of the organisation can be used like variance

analysis, budget reporting, inventory reports etc so that financial data can be generated which

helps in the decision making process of the business so that they can successfully run its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operational activities. The main users of management accounting involve management

employees, shareholders, workforce of the company, investors etc.

Principle of management accounting:

The first principle is the data which is related to accounting, statements or reports are collected

on the basis of past and present information of the company so that future can be forecast.

Second principle is it helps organisation to present its information in an structural manner

(Johnstone, 2020). With the help of management accounting return of investment can be easily

calculated. Third principle is all the necessary or essential information which is required so that

management of the organisation can be run are easily incorporated via management accounting.

Difference of management accounting and financial accounting:

Financial accounting which consists of financial data which is used by the external stakeholders

like investors so that they can know the company's financial position before investing. While

management accounting consists of all kinds of information which can be used by both external

as well as internal stakeholders and it also derived from financial reports. When profitability of

the business has to check than financial accounting is used and the role of management

accounting is to make budget and do conduct variance analysis etc. with the help of balance sheet

or income statement or profit and loss account financial reports can be made whereas

management reports can be made by forecasting future, funds flow statements, budgetary

statements etc.

Management accounting systems are given below:

Cost accounting system:

This system is majorly used by the manufacturing industries so that flow of inventory can be

tracked via different production stages. Cost accounting is used by Marks and Spenser so that

records related to manufacturing operations can be maintained. While doing cost accounting,

accountants has to consider the direct and indirect costs related to manufacturing unit. The

advantage of this system is that it is helpful in finding out per unit production cost of the

company on the basis of the price. This accounting system is uses by managers for controlling

cost, valuation of inventory and doing profitability analysis etc. it is also helpful in doing cost

optimization.

Job costing system:

employees, shareholders, workforce of the company, investors etc.

Principle of management accounting:

The first principle is the data which is related to accounting, statements or reports are collected

on the basis of past and present information of the company so that future can be forecast.

Second principle is it helps organisation to present its information in an structural manner

(Johnstone, 2020). With the help of management accounting return of investment can be easily

calculated. Third principle is all the necessary or essential information which is required so that

management of the organisation can be run are easily incorporated via management accounting.

Difference of management accounting and financial accounting:

Financial accounting which consists of financial data which is used by the external stakeholders

like investors so that they can know the company's financial position before investing. While

management accounting consists of all kinds of information which can be used by both external

as well as internal stakeholders and it also derived from financial reports. When profitability of

the business has to check than financial accounting is used and the role of management

accounting is to make budget and do conduct variance analysis etc. with the help of balance sheet

or income statement or profit and loss account financial reports can be made whereas

management reports can be made by forecasting future, funds flow statements, budgetary

statements etc.

Management accounting systems are given below:

Cost accounting system:

This system is majorly used by the manufacturing industries so that flow of inventory can be

tracked via different production stages. Cost accounting is used by Marks and Spenser so that

records related to manufacturing operations can be maintained. While doing cost accounting,

accountants has to consider the direct and indirect costs related to manufacturing unit. The

advantage of this system is that it is helpful in finding out per unit production cost of the

company on the basis of the price. This accounting system is uses by managers for controlling

cost, valuation of inventory and doing profitability analysis etc. it is also helpful in doing cost

optimization.

Job costing system:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This system is used calculation the costs of manufacturing job and not the process. The data or

information related to production cost of the company can be easily identified (Cescon,

Costantini and Grassetti, 2019). So the information can be used by marks and Spenser to check

the accuracy of the procedure, setting price of products and reimbursement for customers which

is the biggest advantage for the system. With the help of this system project manager can easily

record the cost of every job and maintaining data is important to run business operations

effectively.

Inventory management system:

This system guides companies that how much stock has to order so that company needs can

satisfied and also at what time. This system is used for doing valuation of the material under

inventory by using processes like LIFO, FIFO etc. there are many benefits which marks and

Spenser can get through this management system which includes loss of products, selling price

and products requirements can be measured easily. This system is helpful in checking that there

should be enough stock so that customers order can be fulfilled and also provide warning at the

time of shortage.

Price optimization system:

This system is used by the organisation to check the customers demand and the probabilities of

paying more in order to get the products. marks and Spenser can increase the price of the

products so that they can get more profit margin on its products. More profit margin will help

company in their expansion and growth.

Various methods used for management accounting reporting

Management accounting process helpful to manage company's performance. Marks and

Spenser should use various management accounting process to make smooth their business

operations. This accounting process will help the organisation within various procedure through

which managerial function can be done in an effective manner. Various management accounting

methods are given below:

budget report-

This report is one of the important report because it helps company in determining the budgetary

control for the organisation and also helps company to know about their future performance.

Budget helps company to create plan regarding how much money will get spend on which

business activity and also make sure that money should be spend within the given time period.

information related to production cost of the company can be easily identified (Cescon,

Costantini and Grassetti, 2019). So the information can be used by marks and Spenser to check

the accuracy of the procedure, setting price of products and reimbursement for customers which

is the biggest advantage for the system. With the help of this system project manager can easily

record the cost of every job and maintaining data is important to run business operations

effectively.

Inventory management system:

This system guides companies that how much stock has to order so that company needs can

satisfied and also at what time. This system is used for doing valuation of the material under

inventory by using processes like LIFO, FIFO etc. there are many benefits which marks and

Spenser can get through this management system which includes loss of products, selling price

and products requirements can be measured easily. This system is helpful in checking that there

should be enough stock so that customers order can be fulfilled and also provide warning at the

time of shortage.

Price optimization system:

This system is used by the organisation to check the customers demand and the probabilities of

paying more in order to get the products. marks and Spenser can increase the price of the

products so that they can get more profit margin on its products. More profit margin will help

company in their expansion and growth.

Various methods used for management accounting reporting

Management accounting process helpful to manage company's performance. Marks and

Spenser should use various management accounting process to make smooth their business

operations. This accounting process will help the organisation within various procedure through

which managerial function can be done in an effective manner. Various management accounting

methods are given below:

budget report-

This report is one of the important report because it helps company in determining the budgetary

control for the organisation and also helps company to know about their future performance.

Budget helps company to create plan regarding how much money will get spend on which

business activity and also make sure that money should be spend within the given time period.

This report is the fundamental report in the accounting. It is very helpful for business owners to

control costs for the business (Berg and Madsen, 2020). If company will evaluate the expenses

for previous year then for them it becomes easy to estimate budgets for the future years and can

also estimate that where they have to do cost cutting.

Accounting receivable ageing-

This report is mainly used by those companies which gives credit to their customers. This report

is used to check unpaid invoice of customers like the credit memos which are not used as per the

date along with the contract information. With the help of this report marks and Spenser can

check effectiveness of credit functions within customers. This report provide guidance to adjust

credit policies in order to align with payment capabilities of the customers.

Inventory report-

this report is used by the organisation to find out the number of stock, loss of products and sales

rate etc. so that company can find that there is the requirements for manufacturing more products

or not. This report is more valuable for those companies which manufacture physical products.

As with the help of this report they will get complete information regarding inventory. Through

this data centralization is done on labour or on different overheads which are includes in

production process etc.

Job cost reports-

This report consists of job lists and the costs related to it in previous time which includes

material cost, labour costs, field overhead etc. so organisation can use such report to calculate

expenditure relating to every activity so that planning can be made in order to complete it. This

report gives review of total cost which is happened for single product as compared to the

expected revenue extracted by the project (Hadid and Al-Sayed, 2021). Managers can use this

report to analyse profitability for particular jobs and concentrating on such jobs which provides

major profits to the company.

Operating budget report-

This report is very helpful in calculating the expenditure and income within the time period and

it is made with the help of forecasted sales. Sales budget can use marks and Spenser to develop

this. This budget exclude capital heads because it is the short term budget.

Profit and loss statements-

control costs for the business (Berg and Madsen, 2020). If company will evaluate the expenses

for previous year then for them it becomes easy to estimate budgets for the future years and can

also estimate that where they have to do cost cutting.

Accounting receivable ageing-

This report is mainly used by those companies which gives credit to their customers. This report

is used to check unpaid invoice of customers like the credit memos which are not used as per the

date along with the contract information. With the help of this report marks and Spenser can

check effectiveness of credit functions within customers. This report provide guidance to adjust

credit policies in order to align with payment capabilities of the customers.

Inventory report-

this report is used by the organisation to find out the number of stock, loss of products and sales

rate etc. so that company can find that there is the requirements for manufacturing more products

or not. This report is more valuable for those companies which manufacture physical products.

As with the help of this report they will get complete information regarding inventory. Through

this data centralization is done on labour or on different overheads which are includes in

production process etc.

Job cost reports-

This report consists of job lists and the costs related to it in previous time which includes

material cost, labour costs, field overhead etc. so organisation can use such report to calculate

expenditure relating to every activity so that planning can be made in order to complete it. This

report gives review of total cost which is happened for single product as compared to the

expected revenue extracted by the project (Hadid and Al-Sayed, 2021). Managers can use this

report to analyse profitability for particular jobs and concentrating on such jobs which provides

major profits to the company.

Operating budget report-

This report is very helpful in calculating the expenditure and income within the time period and

it is made with the help of forecasted sales. Sales budget can use marks and Spenser to develop

this. This budget exclude capital heads because it is the short term budget.

Profit and loss statements-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is also the kind of report and it can be said that it is most important report for every company

because this statement shows that what profits company is making and where they are incurring

loss. Marks and Spenser make this report to identify its expenditure and various costs or

revenues within specified time period which can be year or a quarter.

Performance report-

This report shows result of the activity or the work which is done by an individual. This report

compares actual outcomes with the standard of the budget and also compares variance within

two numbers (Alsharari, 2019).

Calculating costs using techniques of cost analysis to make income statement using absorption

and marginal costs.

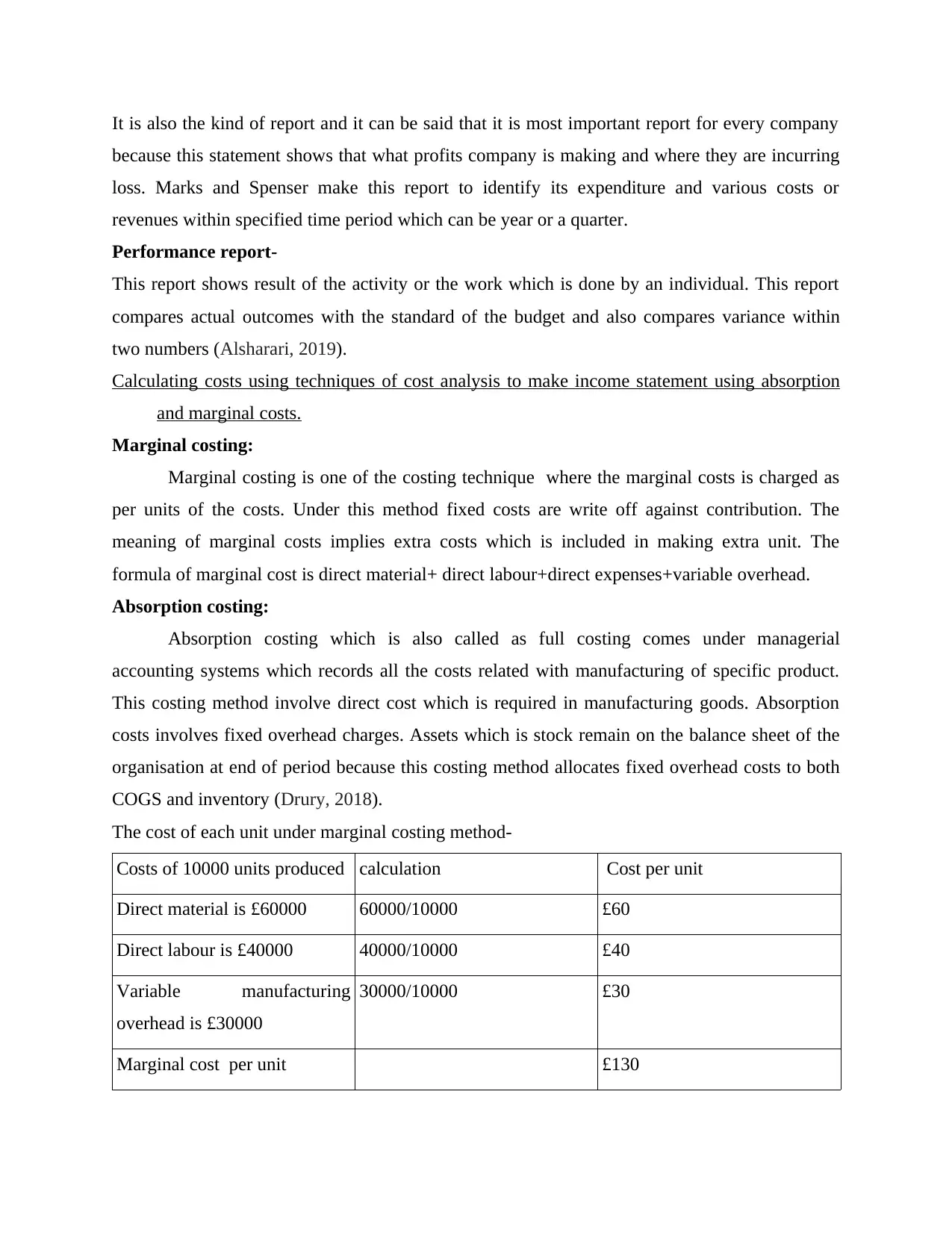

Marginal costing:

Marginal costing is one of the costing technique where the marginal costs is charged as

per units of the costs. Under this method fixed costs are write off against contribution. The

meaning of marginal costs implies extra costs which is included in making extra unit. The

formula of marginal cost is direct material+ direct labour+direct expenses+variable overhead.

Absorption costing:

Absorption costing which is also called as full costing comes under managerial

accounting systems which records all the costs related with manufacturing of specific product.

This costing method involve direct cost which is required in manufacturing goods. Absorption

costs involves fixed overhead charges. Assets which is stock remain on the balance sheet of the

organisation at end of period because this costing method allocates fixed overhead costs to both

COGS and inventory (Drury, 2018).

The cost of each unit under marginal costing method-

Costs of 10000 units produced calculation Cost per unit

Direct material is £60000 60000/10000 £60

Direct labour is £40000 40000/10000 £40

Variable manufacturing

overhead is £30000

30000/10000 £30

Marginal cost per unit £130

because this statement shows that what profits company is making and where they are incurring

loss. Marks and Spenser make this report to identify its expenditure and various costs or

revenues within specified time period which can be year or a quarter.

Performance report-

This report shows result of the activity or the work which is done by an individual. This report

compares actual outcomes with the standard of the budget and also compares variance within

two numbers (Alsharari, 2019).

Calculating costs using techniques of cost analysis to make income statement using absorption

and marginal costs.

Marginal costing:

Marginal costing is one of the costing technique where the marginal costs is charged as

per units of the costs. Under this method fixed costs are write off against contribution. The

meaning of marginal costs implies extra costs which is included in making extra unit. The

formula of marginal cost is direct material+ direct labour+direct expenses+variable overhead.

Absorption costing:

Absorption costing which is also called as full costing comes under managerial

accounting systems which records all the costs related with manufacturing of specific product.

This costing method involve direct cost which is required in manufacturing goods. Absorption

costs involves fixed overhead charges. Assets which is stock remain on the balance sheet of the

organisation at end of period because this costing method allocates fixed overhead costs to both

COGS and inventory (Drury, 2018).

The cost of each unit under marginal costing method-

Costs of 10000 units produced calculation Cost per unit

Direct material is £60000 60000/10000 £60

Direct labour is £40000 40000/10000 £40

Variable manufacturing

overhead is £30000

30000/10000 £30

Marginal cost per unit £130

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The cost of each unit under absorption costing method-

Costs of 10000 units produced calculation Cost per unit

Direct material is £60000 60000/10000 £60

Direct labour is £40000 40000/10000 £40

Variable manufacturing

overhead is £30000

30000/10000 £30

Fixed manufacturing overhead

is £50000

50000/10000 £50

Cost per unit £180

Income statement of XYZ ltd.

particulars units Selling price £ per unit Value in £

sales 10000 30 3000000

Less: marginal costs of

products

Direct material 10000*60= 600000

Direct labour 10000*40=400000

Variable

manufacturing

overhead

10000*30= 300000

Total marginal cost 1300000 1300000

Gross contribution 1700000

Less: variable and

administration

expenses

200000

Net contribution 1500000

Costs of 10000 units produced calculation Cost per unit

Direct material is £60000 60000/10000 £60

Direct labour is £40000 40000/10000 £40

Variable manufacturing

overhead is £30000

30000/10000 £30

Fixed manufacturing overhead

is £50000

50000/10000 £50

Cost per unit £180

Income statement of XYZ ltd.

particulars units Selling price £ per unit Value in £

sales 10000 30 3000000

Less: marginal costs of

products

Direct material 10000*60= 600000

Direct labour 10000*40=400000

Variable

manufacturing

overhead

10000*30= 300000

Total marginal cost 1300000 1300000

Gross contribution 1700000

Less: variable and

administration

expenses

200000

Net contribution 1500000

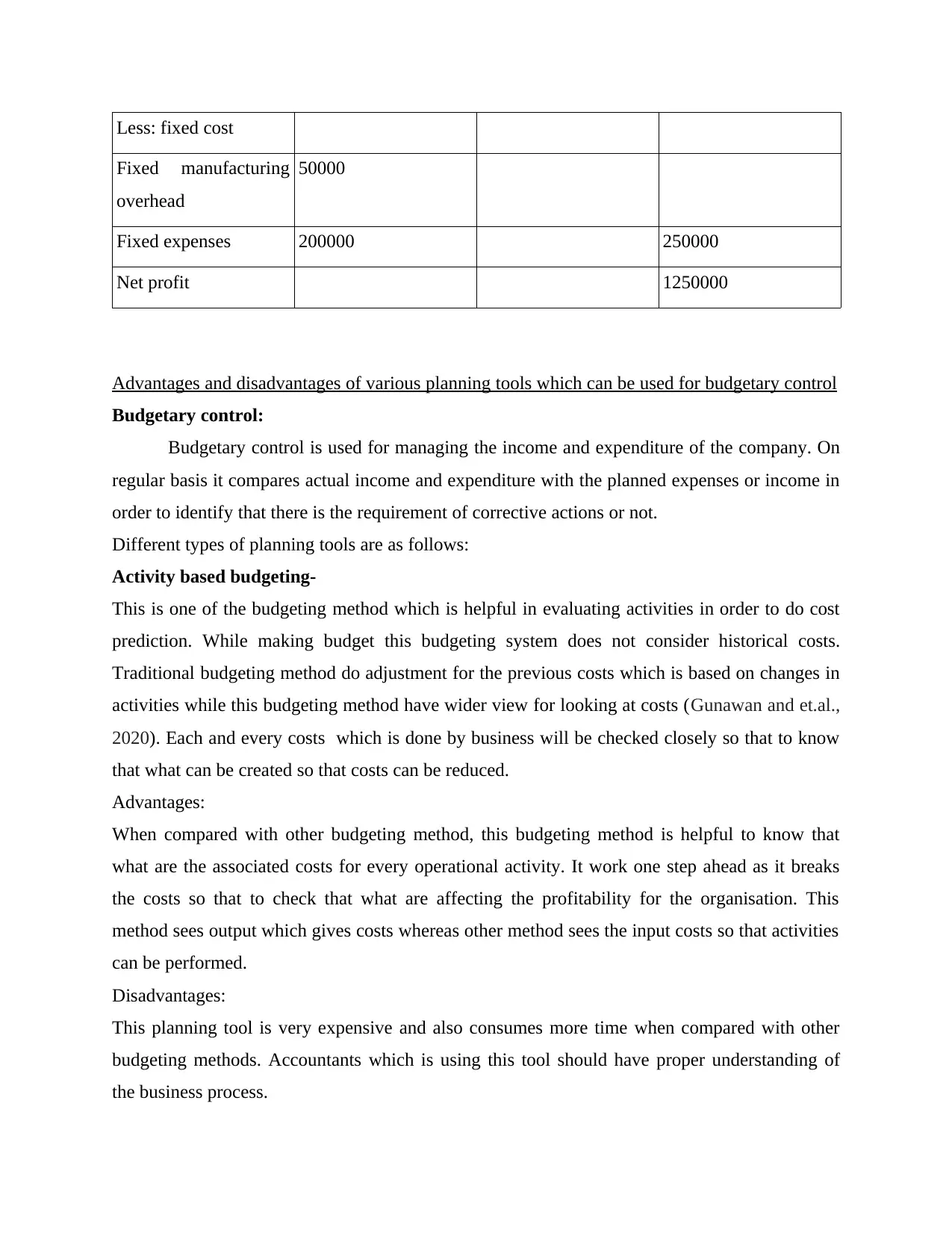

Less: fixed cost

Fixed manufacturing

overhead

50000

Fixed expenses 200000 250000

Net profit 1250000

Advantages and disadvantages of various planning tools which can be used for budgetary control

Budgetary control:

Budgetary control is used for managing the income and expenditure of the company. On

regular basis it compares actual income and expenditure with the planned expenses or income in

order to identify that there is the requirement of corrective actions or not.

Different types of planning tools are as follows:

Activity based budgeting-

This is one of the budgeting method which is helpful in evaluating activities in order to do cost

prediction. While making budget this budgeting system does not consider historical costs.

Traditional budgeting method do adjustment for the previous costs which is based on changes in

activities while this budgeting method have wider view for looking at costs (Gunawan and et.al.,

2020). Each and every costs which is done by business will be checked closely so that to know

that what can be created so that costs can be reduced.

Advantages:

When compared with other budgeting method, this budgeting method is helpful to know that

what are the associated costs for every operational activity. It work one step ahead as it breaks

the costs so that to check that what are affecting the profitability for the organisation. This

method sees output which gives costs whereas other method sees the input costs so that activities

can be performed.

Disadvantages:

This planning tool is very expensive and also consumes more time when compared with other

budgeting methods. Accountants which is using this tool should have proper understanding of

the business process.

Fixed manufacturing

overhead

50000

Fixed expenses 200000 250000

Net profit 1250000

Advantages and disadvantages of various planning tools which can be used for budgetary control

Budgetary control:

Budgetary control is used for managing the income and expenditure of the company. On

regular basis it compares actual income and expenditure with the planned expenses or income in

order to identify that there is the requirement of corrective actions or not.

Different types of planning tools are as follows:

Activity based budgeting-

This is one of the budgeting method which is helpful in evaluating activities in order to do cost

prediction. While making budget this budgeting system does not consider historical costs.

Traditional budgeting method do adjustment for the previous costs which is based on changes in

activities while this budgeting method have wider view for looking at costs (Gunawan and et.al.,

2020). Each and every costs which is done by business will be checked closely so that to know

that what can be created so that costs can be reduced.

Advantages:

When compared with other budgeting method, this budgeting method is helpful to know that

what are the associated costs for every operational activity. It work one step ahead as it breaks

the costs so that to check that what are affecting the profitability for the organisation. This

method sees output which gives costs whereas other method sees the input costs so that activities

can be performed.

Disadvantages:

This planning tool is very expensive and also consumes more time when compared with other

budgeting methods. Accountants which is using this tool should have proper understanding of

the business process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Zero based budgeting-

It is the tool which is used in budgeting where income substracts with the expenses should be

equals to zero. Under this budgeting method it is important to ensure that expenses should be

always match with income of the month. It is difficult to start budget from zero but is helps

organisation to make best decision which they can use in long run. Marks and Spenser can also

use this tool to attain sustainability.

Advantages:

This tool make sure that managers think that how to spend money within every budgeting period.

It is also helpful in keeping legacy expenses checked as these expenses are not checked until

some economic shock arises.

Disadvantages:

The biggest challenge of this tool is that it can enhance short term thinking by moving resources

within those field of company which will generate profits over the budgeting period. It is also

time consuming because it takes time in review and justifying the element of budget rather than

doing modification in an existing budget (Alam and Alam, 2020).

Cash budget-

Cash budget is one of the most famous budgeting. This budget define the term cash budget

because cash is used in order to make purchase and not credit cards.

Advantages:

it is helpful in preventing overspending. By using cash budget one can only use what they have

with them. So hat is why it provides better perspective of how to utilize money. It incur no extra

costs.

Disadvantages:

it can be steal very easily. If the money is stolen once then it is difficult that an individual will

get money back whereas this does not happens with credit cards. Credit cards are easily get

tracked whereas it cannot be easily tracked.

Operating budget-

This tool is used to show the projected revenue of the company and also to show the expenses for

the estimated period. It is shown in the form of income statements and also it write down the

expected expenses and incomes within the fiscal year of the organisation. Marks and Spenser

It is the tool which is used in budgeting where income substracts with the expenses should be

equals to zero. Under this budgeting method it is important to ensure that expenses should be

always match with income of the month. It is difficult to start budget from zero but is helps

organisation to make best decision which they can use in long run. Marks and Spenser can also

use this tool to attain sustainability.

Advantages:

This tool make sure that managers think that how to spend money within every budgeting period.

It is also helpful in keeping legacy expenses checked as these expenses are not checked until

some economic shock arises.

Disadvantages:

The biggest challenge of this tool is that it can enhance short term thinking by moving resources

within those field of company which will generate profits over the budgeting period. It is also

time consuming because it takes time in review and justifying the element of budget rather than

doing modification in an existing budget (Alam and Alam, 2020).

Cash budget-

Cash budget is one of the most famous budgeting. This budget define the term cash budget

because cash is used in order to make purchase and not credit cards.

Advantages:

it is helpful in preventing overspending. By using cash budget one can only use what they have

with them. So hat is why it provides better perspective of how to utilize money. It incur no extra

costs.

Disadvantages:

it can be steal very easily. If the money is stolen once then it is difficult that an individual will

get money back whereas this does not happens with credit cards. Credit cards are easily get

tracked whereas it cannot be easily tracked.

Operating budget-

This tool is used to show the projected revenue of the company and also to show the expenses for

the estimated period. It is shown in the form of income statements and also it write down the

expected expenses and incomes within the fiscal year of the organisation. Marks and Spenser

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

uses this budget to ascertain the revenue of the company (Bada Olaran, Goudie Pujals and

Leporati, 2019).

Advantages:

this is one of most useful tool for every company. It is used by every company whether it is small

or big or have any business structure.

Disadvantages:

this budget is not that much accurate just like other budgets. This takes place when company

does not met targets.

Organisations are adopting management accounting systems to respond to various financial

problems.

Organisations in today's world are using various business models or strategies to respond

to various challenges while creating value for the shareholders. Company can identify financial

issues through various methods which are as follows:

benchmarking:

This is the tool which is used for measuring performance so that business processes can be

compared. Other metrics also lean them to benchmarking (What is benchmarking? What are the

pros and cons., 2021). Benchmark also varies with the nature of industry and its purpose. Marks

and Spenser are using benchmarking to find out the internal expectations and also comparing

their progress with the competitors.

Pros:

it is helpful in improving the performance and solving various financial problems. It encourages

creativity. As it helps business in achieving its goals and objectives. It is easy to do and also cost

effective.

Cons:

it is not able to use for measuring effectiveness of the business process. It is not consider as solo

activity. Although benchmarking is important but it cannot be only use to bring institute change.

Key performance indicator:

KPI or Key performance indicator is the performance measurement tool which is also called as

performance indicator which marks and Spenser uses so that its process can be tracked and also

get awareness of the success rate of the company. This tool set achievable goals for the

department of the organisation. So with the help of KPI goals can be attain easily.

Leporati, 2019).

Advantages:

this is one of most useful tool for every company. It is used by every company whether it is small

or big or have any business structure.

Disadvantages:

this budget is not that much accurate just like other budgets. This takes place when company

does not met targets.

Organisations are adopting management accounting systems to respond to various financial

problems.

Organisations in today's world are using various business models or strategies to respond

to various challenges while creating value for the shareholders. Company can identify financial

issues through various methods which are as follows:

benchmarking:

This is the tool which is used for measuring performance so that business processes can be

compared. Other metrics also lean them to benchmarking (What is benchmarking? What are the

pros and cons., 2021). Benchmark also varies with the nature of industry and its purpose. Marks

and Spenser are using benchmarking to find out the internal expectations and also comparing

their progress with the competitors.

Pros:

it is helpful in improving the performance and solving various financial problems. It encourages

creativity. As it helps business in achieving its goals and objectives. It is easy to do and also cost

effective.

Cons:

it is not able to use for measuring effectiveness of the business process. It is not consider as solo

activity. Although benchmarking is important but it cannot be only use to bring institute change.

Key performance indicator:

KPI or Key performance indicator is the performance measurement tool which is also called as

performance indicator which marks and Spenser uses so that its process can be tracked and also

get awareness of the success rate of the company. This tool set achievable goals for the

department of the organisation. So with the help of KPI goals can be attain easily.

Pros:

it provides measurable results. As it tracks the success rate so that is why it provides accurate

outcomes in the form of statistics, numbers etc. KPI provides daily, weekly, monthly or yearly

outcomes as per the requirement of the objectives.

Cons:

it shows results for short term goals so there are higher chances that employees can lose

concentration from the high quality work.

Corporate governance:

This tool deals with the management of the organisation. It is strategy which provides guidance

and control to the organisation. It is important that company should operate as per the decisions

of its shareholders. It balances individual objectives with social or economic goals (Oladele and

Longlong, 2019).

Pros:

when company will bring good corporate performance then it will help in improving

performance and economic development. With good corporate governance the trust of investors

are also maintained. Business gets opportunity to raise its capital effectively.

Cons:

it increase illegal trading. Corporate insiders are done by corporate executives, managers and

workforce because they can use sensitive information of the company which can even influence

the share value of the company. There are many process through which financial statements can

be presented which mislead investors. And through this way investors discourage and does not

invest in the company (Pedroso and Gomes, 2020).

So organisation can use above management accounting system to solve financial problems.

Conclusion

Through this report it can concluded that management accounting system plays important

role in every company in order to evaluate both type of data financial and non financial to

forecast future and make strategies. Different management accounting systems like inventory

management system, price optimization system etc are used at different levels in the

organisation. Report has also evaluated planning tool which are activity based budgeting, cash

budget, zero based budgeting etc. with advantages and disadvantages. nowadays companies are

it provides measurable results. As it tracks the success rate so that is why it provides accurate

outcomes in the form of statistics, numbers etc. KPI provides daily, weekly, monthly or yearly

outcomes as per the requirement of the objectives.

Cons:

it shows results for short term goals so there are higher chances that employees can lose

concentration from the high quality work.

Corporate governance:

This tool deals with the management of the organisation. It is strategy which provides guidance

and control to the organisation. It is important that company should operate as per the decisions

of its shareholders. It balances individual objectives with social or economic goals (Oladele and

Longlong, 2019).

Pros:

when company will bring good corporate performance then it will help in improving

performance and economic development. With good corporate governance the trust of investors

are also maintained. Business gets opportunity to raise its capital effectively.

Cons:

it increase illegal trading. Corporate insiders are done by corporate executives, managers and

workforce because they can use sensitive information of the company which can even influence

the share value of the company. There are many process through which financial statements can

be presented which mislead investors. And through this way investors discourage and does not

invest in the company (Pedroso and Gomes, 2020).

So organisation can use above management accounting system to solve financial problems.

Conclusion

Through this report it can concluded that management accounting system plays important

role in every company in order to evaluate both type of data financial and non financial to

forecast future and make strategies. Different management accounting systems like inventory

management system, price optimization system etc are used at different levels in the

organisation. Report has also evaluated planning tool which are activity based budgeting, cash

budget, zero based budgeting etc. with advantages and disadvantages. nowadays companies are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.