Zylla Ltd: Management Accounting, Reporting, and Costing Analysis

VerifiedAdded on 2020/07/23

|17

|5071

|467

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within an organization, focusing on financial reporting systems, costing techniques, and budgetary control. It examines various types of accounting systems, including single-entry, cost accounting, inventory management, job costing, and price optimization, emphasizing their role in recording financial transactions and supporting decision-making. Different accounting reporting methods, such as budget reports, bills receivable reports, job cost reports, and inventory/manufacturing reports, are evaluated for their relevance in providing insights into company performance and risk management. The benefits of management accounting systems, including cost reduction and improved financial returns, are discussed, along with a critical analysis of reporting systems and their impact on profitability and efficiency. The report also explores costing techniques like marginal costing, absorption costing, and activity-based costing for determining net profit and addresses the use of planning tools in budgetary control and the resolution of financial issues, with specific reference to Zylla Ltd.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION..........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Various types of accounting system and its necessary requirements...............................1

P2: Different method of accounting reporting system ..........................................................3

M1: Benefits of management accounting systems and their application...............................4

D1: Critical analysis of reporting system ..............................................................................5

TASK 2............................................................................................................................................5

P3: Various costing techniques used to determine net profit ................................................5

M2: Utilisation of accounting techniques...............................................................................6

D2: Critical evaluation of income statement ........................................................................7

TASK 3............................................................................................................................................7

P4. Use of planning tools in budgetary control......................................................................7

M3: Evaluation of planning tools.........................................................................................10

D3: Tools used for resolving financial issues.......................................................................10

TASK 4..........................................................................................................................................10

P5: Various measures to resolve financial problems............................................................10

M4: Analysis of financial problems.....................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION..........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Various types of accounting system and its necessary requirements...............................1

P2: Different method of accounting reporting system ..........................................................3

M1: Benefits of management accounting systems and their application...............................4

D1: Critical analysis of reporting system ..............................................................................5

TASK 2............................................................................................................................................5

P3: Various costing techniques used to determine net profit ................................................5

M2: Utilisation of accounting techniques...............................................................................6

D2: Critical evaluation of income statement ........................................................................7

TASK 3............................................................................................................................................7

P4. Use of planning tools in budgetary control......................................................................7

M3: Evaluation of planning tools.........................................................................................10

D3: Tools used for resolving financial issues.......................................................................10

TASK 4..........................................................................................................................................10

P5: Various measures to resolve financial problems............................................................10

M4: Analysis of financial problems.....................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is an important measure use by an organisation in order to

analyse financial statements of the company. Various reports related with financial data as well

as other parts of information are intendant as primarily to assist accountant in attaining objectives

of an organisation (Arjaliès and Mundy, 2013). Generally, a accounting system is an essential

facet those are helpful in controlling operations that are being perform on regular basis. Some

accountant describe MA to be the perfect application that is based on certain principles in order

to create, control, protect and enhance value for shareholder.

It needs identification, preparation and interpretation of useful data in order to take

valuable decision making. Use of accounting and reporting system as important tools are more

effective for the company. In order to analyse net profit during the year are generated by using

specific costing method. Understanding of planning tools those are helpful at the time of

budgetary control. Further, this report will examine certain financial issues those are arises in an

organisation and measure to rectify them are clearly explain under this particular project report.

TASK 1

P1: Various types of accounting system and its necessary requirements

In every business organisation whether small or medium size needs to have specific

accounting systems. This will be helpful in order to maintain their every day financial transaction

in more systematic manner. Management accounting system is one of the types of systems which

is use to record financial data. A single entry system under which only one entry is recorded for

every financial transaction which is the most simplest form of accounting. This is mainly said to

be perfect techniques for mid size organisation such as Zylla Ltd (Bebbington, Unerman and

O'Dwyer, 2014). Because there is very less amount of transaction and assets to be recorded. It is

crucial for the purpose of making future forecasting of estimated profits.

It has been seen that managing the accounting data and reports in such perfect manner is

the primary aim of accounts managers in order to make crucial decision regarding future

sustainability of Zylla operations. If company is using corrective system to record transaction

they are at very good position to operate business in more effective and efficient manner. All

these are primarily essential for make proper balance among past and previous year

performances. It is the responsibility of managers to contribute their valuable efforts in proper

1

Management accounting is an important measure use by an organisation in order to

analyse financial statements of the company. Various reports related with financial data as well

as other parts of information are intendant as primarily to assist accountant in attaining objectives

of an organisation (Arjaliès and Mundy, 2013). Generally, a accounting system is an essential

facet those are helpful in controlling operations that are being perform on regular basis. Some

accountant describe MA to be the perfect application that is based on certain principles in order

to create, control, protect and enhance value for shareholder.

It needs identification, preparation and interpretation of useful data in order to take

valuable decision making. Use of accounting and reporting system as important tools are more

effective for the company. In order to analyse net profit during the year are generated by using

specific costing method. Understanding of planning tools those are helpful at the time of

budgetary control. Further, this report will examine certain financial issues those are arises in an

organisation and measure to rectify them are clearly explain under this particular project report.

TASK 1

P1: Various types of accounting system and its necessary requirements

In every business organisation whether small or medium size needs to have specific

accounting systems. This will be helpful in order to maintain their every day financial transaction

in more systematic manner. Management accounting system is one of the types of systems which

is use to record financial data. A single entry system under which only one entry is recorded for

every financial transaction which is the most simplest form of accounting. This is mainly said to

be perfect techniques for mid size organisation such as Zylla Ltd (Bebbington, Unerman and

O'Dwyer, 2014). Because there is very less amount of transaction and assets to be recorded. It is

crucial for the purpose of making future forecasting of estimated profits.

It has been seen that managing the accounting data and reports in such perfect manner is

the primary aim of accounts managers in order to make crucial decision regarding future

sustainability of Zylla operations. If company is using corrective system to record transaction

they are at very good position to operate business in more effective and efficient manner. All

these are primarily essential for make proper balance among past and previous year

performances. It is the responsibility of managers to contribute their valuable efforts in proper

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

allocation of resources. They need to analyse and monitoring every accounting data in order to

minimise risk of uncertainty and make plan for incurring maximum profitability. However, role

of accountant is to make use of proper accounting systems in order to make success of Zylla

company in order to attain long term objectives for an organisation. In order to take decision-

making for the purpose of controlling cost and all those expenses which are incur by company

during the period of time. It is necessary for managers to make financial reports on the basis of

selected information. It will be crucial for making certain improvement in current technologies

and implement modified techniques in accordance to get better results in coming times.

Purpose of management accounting is to make use of accounting system while recording

of various financial transactions those are incur by the company during the time (Cadez and

Guilding, 2012). The information collected by managers can helpful in order to make crucial

decision-making regarding enhancement of performance and growth of the company.

Types of accounting system: There are certain accounting system which is helpful in

recording of financial transaction of the cited company. Likewise, managers needs to make use

of those while recording of entries into accounts statements. Some of them are:

Cost accounting system: It is known as a systematic design used by an organisation in

order to estimate total cost of their goods for the purpose of profitability analysis. According to

this particular system, managers use to record all those income and cost that are incur by Zylla

company during production of product and services. In this accounting system, accurate cost of

products is analyse and recorded in order to determine total gain from the operations.

Inventory management system: According to this particular system which is use for the

purpose of keeping proper record of stock level in the company. The primary objectives of

managers is to control and maintain total cost of stock for the purpose of incurring high

profitability. It the managers who look all the records whether to order extra stock and total cost

of ordering. By the help of this, excess of wastage and cost can be control up to an extent.

Job costing system: Under this particular accounting system Zylla company use to

analyse total cost of manufacturing each units are determine. It is the primary role of managers to

develop a job cost which is use only when the products that produce are entirely different from

each other. It is mainly use for the purpose of allocating costs to an individual projects of a

company.

2

minimise risk of uncertainty and make plan for incurring maximum profitability. However, role

of accountant is to make use of proper accounting systems in order to make success of Zylla

company in order to attain long term objectives for an organisation. In order to take decision-

making for the purpose of controlling cost and all those expenses which are incur by company

during the period of time. It is necessary for managers to make financial reports on the basis of

selected information. It will be crucial for making certain improvement in current technologies

and implement modified techniques in accordance to get better results in coming times.

Purpose of management accounting is to make use of accounting system while recording

of various financial transactions those are incur by the company during the time (Cadez and

Guilding, 2012). The information collected by managers can helpful in order to make crucial

decision-making regarding enhancement of performance and growth of the company.

Types of accounting system: There are certain accounting system which is helpful in

recording of financial transaction of the cited company. Likewise, managers needs to make use

of those while recording of entries into accounts statements. Some of them are:

Cost accounting system: It is known as a systematic design used by an organisation in

order to estimate total cost of their goods for the purpose of profitability analysis. According to

this particular system, managers use to record all those income and cost that are incur by Zylla

company during production of product and services. In this accounting system, accurate cost of

products is analyse and recorded in order to determine total gain from the operations.

Inventory management system: According to this particular system which is use for the

purpose of keeping proper record of stock level in the company. The primary objectives of

managers is to control and maintain total cost of stock for the purpose of incurring high

profitability. It the managers who look all the records whether to order extra stock and total cost

of ordering. By the help of this, excess of wastage and cost can be control up to an extent.

Job costing system: Under this particular accounting system Zylla company use to

analyse total cost of manufacturing each units are determine. It is the primary role of managers to

develop a job cost which is use only when the products that produce are entirely different from

each other. It is mainly use for the purpose of allocating costs to an individual projects of a

company.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimisation system: It is the use of numerical analysis done by company in order

to determine about various prices those are charge by company for their particular products. It is

use to analyse about customers responses about various prices those are being charge for various

products and services. It is also essential for the managers to analyse best suitable price which is

being charge by Zylla company in order to maximise operating profit.

P2: Different method of accounting reporting system

It is necessary for every business entity to making valuable report on the basis of data

collected by managers from various sources. Every report is essential for the company in order to

make curial decision-making about future growth and sustainability. The role of financial

accountant is to make necessary report that is submitted to the shareholder and higher authorities

for making investment decision. Management accounting reports are important tools which

provides the information regarding different important aspects of company (Fourie and et. al.,

2015). These reports have the large number of importance for the manager of Zylla company as

it provides basic information regarding preparation of important policies and plans. These

different reporting methods are also considered as the important risk management tool which

helps in continuous monitoring of the transaction of employees and removal of the problems

faced by them. This will contributes in improvement of the performance of employees and

productivity of the company. All these reports are prepared in frequent intervals depends upon

the requirement of the management (Management Accounting Research Interest Group, 2017).

The different reports which are prepared by the accounting officer of Zylla company and their

relevance for management are mentioned below:

Budget report: This report includes the process of preparation of different budgets

which helps the managers in appraisal of the performance of different departments and

control the unnecessary costs which are incurred on wasteful products. These budgets are

prepared by accounting officer on the basis of the prior information. These budgets helps

ion determination of the objectives and disbursement of the roles and duties to each and

every employee. Budgets are like standards which helps in comparison of the actual

performance of employees and determination of deviations. Financial budget helps in

efficiently allocation of the funds to different departments as per their needs. This helps

in reduction of the cost and accomplishment of their targets.

3

to determine about various prices those are charge by company for their particular products. It is

use to analyse about customers responses about various prices those are being charge for various

products and services. It is also essential for the managers to analyse best suitable price which is

being charge by Zylla company in order to maximise operating profit.

P2: Different method of accounting reporting system

It is necessary for every business entity to making valuable report on the basis of data

collected by managers from various sources. Every report is essential for the company in order to

make curial decision-making about future growth and sustainability. The role of financial

accountant is to make necessary report that is submitted to the shareholder and higher authorities

for making investment decision. Management accounting reports are important tools which

provides the information regarding different important aspects of company (Fourie and et. al.,

2015). These reports have the large number of importance for the manager of Zylla company as

it provides basic information regarding preparation of important policies and plans. These

different reporting methods are also considered as the important risk management tool which

helps in continuous monitoring of the transaction of employees and removal of the problems

faced by them. This will contributes in improvement of the performance of employees and

productivity of the company. All these reports are prepared in frequent intervals depends upon

the requirement of the management (Management Accounting Research Interest Group, 2017).

The different reports which are prepared by the accounting officer of Zylla company and their

relevance for management are mentioned below:

Budget report: This report includes the process of preparation of different budgets

which helps the managers in appraisal of the performance of different departments and

control the unnecessary costs which are incurred on wasteful products. These budgets are

prepared by accounting officer on the basis of the prior information. These budgets helps

ion determination of the objectives and disbursement of the roles and duties to each and

every employee. Budgets are like standards which helps in comparison of the actual

performance of employees and determination of deviations. Financial budget helps in

efficiently allocation of the funds to different departments as per their needs. This helps

in reduction of the cost and accomplishment of their targets.

3

Bills receivable report: It is important report which provides the information regarding

the debtors to whom the company is to collect outstanding amount. It is effective tool

which helps in managing the flow of cash and changing their credit policies which is

more beneficial for them. The information provide by this report is used by the manager

of Zyalla company to examine the current collection process of company. It contributes

in preparation of the effective strategies which helps in collection of the amount on time

and reduction on the account of NPA's. This also provides the opportunity regarding to

give focus on their old debts and adopt the measures to recover them.

Job cost report: It is considered as the important report which helps in identification of

the cost which is incurred in the completion of specific project. Such identification of

cost is compared with the revenue which is going to earn by organisation from such

specific project (Hülle, Kaspar and Möller, 2011). This helps in determination of the

profitability which is earned by company through particular job. Using of these report

provide the opportunity to the management of Zyalla company to find out the such areas

which are more profitable. This helps in focusing on such areas which provides more

return to company and improves their profitability. It contributes to removal of costs from

such processes which are not beneficial and saves their important time and money.

Evaluation of this report helps in correction of the area where the waste activities are

prevail before the increment of cost. It has maximum benefits derived by organisation is

on their operation and functions by optimum utilisation of existing resources.

Inventory and manufacturing report: This report has large number of importance in

managing the physical inventory of zyalla company. This provides the opportunity

regarding make their manufacturing processes more effective and efficient. This will

have large importance in accomplishment of their objectives and targets. Effective

management of inventory helps in providence of materials to different departments and

improves their productivity.

M1: Benefits of management accounting systems and their application

The large number of benefits are derived by the management of Zyalla company due to

the adoption of management accounting systems are mentioned below:

4

the debtors to whom the company is to collect outstanding amount. It is effective tool

which helps in managing the flow of cash and changing their credit policies which is

more beneficial for them. The information provide by this report is used by the manager

of Zyalla company to examine the current collection process of company. It contributes

in preparation of the effective strategies which helps in collection of the amount on time

and reduction on the account of NPA's. This also provides the opportunity regarding to

give focus on their old debts and adopt the measures to recover them.

Job cost report: It is considered as the important report which helps in identification of

the cost which is incurred in the completion of specific project. Such identification of

cost is compared with the revenue which is going to earn by organisation from such

specific project (Hülle, Kaspar and Möller, 2011). This helps in determination of the

profitability which is earned by company through particular job. Using of these report

provide the opportunity to the management of Zyalla company to find out the such areas

which are more profitable. This helps in focusing on such areas which provides more

return to company and improves their profitability. It contributes to removal of costs from

such processes which are not beneficial and saves their important time and money.

Evaluation of this report helps in correction of the area where the waste activities are

prevail before the increment of cost. It has maximum benefits derived by organisation is

on their operation and functions by optimum utilisation of existing resources.

Inventory and manufacturing report: This report has large number of importance in

managing the physical inventory of zyalla company. This provides the opportunity

regarding make their manufacturing processes more effective and efficient. This will

have large importance in accomplishment of their objectives and targets. Effective

management of inventory helps in providence of materials to different departments and

improves their productivity.

M1: Benefits of management accounting systems and their application

The large number of benefits are derived by the management of Zyalla company due to

the adoption of management accounting systems are mentioned below:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reduction of cost: Different costing system helps in identification of important

information. This provides opportunity regarding reduction of cost by adoption of

appropriate strategies.

Improved financial return: Such accounting system provides the information regarding

the tastes of customers and the strategies adopt by competitors. This helps in

improvement of their production process and increase their financial return.

D1: Critical analysis of reporting system

In has been seen that without having proper reporting system no any decision can be

analysed. It is necessary for the company's to make use of financial transaction from various

sources of the department. It is more effective techniques which is useful for Zylla company to

record daily transaction. With the use of reporting system profitability and efficiency can be

enhance and future impacts can be control in more effective manner. By this, aims of the

company can be attain more easily without making any extra costs.

TASK 2

P3: Various costing techniques used to determine net profit

Cost accounting and management systems is one of the branch of management

accounting. There are various type of organisation engaged in producing product and services.

Cost method are used to ascertain the cost of product and services subject to increasing the

profitability (Quagli, 2011). Unit costing, job costing, contract costing, batch costing, operating

costing, multiple costing, uniform costing are the types of cost methods used in manufacturing

and service providing organisation. Below are the major cost methods are defined in subject to

evaluating profitability.

Marginal Costing

Marginal costing is defined to be a tool of costing in accounting. It generally refers to the

cost which has been incurred as per units of cost. The total cost incurred by a business is

categorised on grounds of Fixed and variable cost. The fixed costs remains same whereas

variable cost of varies with amount of units to be produced. The amount which has been incurred

by business to produce an additional commodity is referred to as marginal cost. The concept of

Marginal costing have been helpful in determining price and profitability of the product.

Absorption Costing

5

information. This provides opportunity regarding reduction of cost by adoption of

appropriate strategies.

Improved financial return: Such accounting system provides the information regarding

the tastes of customers and the strategies adopt by competitors. This helps in

improvement of their production process and increase their financial return.

D1: Critical analysis of reporting system

In has been seen that without having proper reporting system no any decision can be

analysed. It is necessary for the company's to make use of financial transaction from various

sources of the department. It is more effective techniques which is useful for Zylla company to

record daily transaction. With the use of reporting system profitability and efficiency can be

enhance and future impacts can be control in more effective manner. By this, aims of the

company can be attain more easily without making any extra costs.

TASK 2

P3: Various costing techniques used to determine net profit

Cost accounting and management systems is one of the branch of management

accounting. There are various type of organisation engaged in producing product and services.

Cost method are used to ascertain the cost of product and services subject to increasing the

profitability (Quagli, 2011). Unit costing, job costing, contract costing, batch costing, operating

costing, multiple costing, uniform costing are the types of cost methods used in manufacturing

and service providing organisation. Below are the major cost methods are defined in subject to

evaluating profitability.

Marginal Costing

Marginal costing is defined to be a tool of costing in accounting. It generally refers to the

cost which has been incurred as per units of cost. The total cost incurred by a business is

categorised on grounds of Fixed and variable cost. The fixed costs remains same whereas

variable cost of varies with amount of units to be produced. The amount which has been incurred

by business to produce an additional commodity is referred to as marginal cost. The concept of

Marginal costing have been helpful in determining price and profitability of the product.

Absorption Costing

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

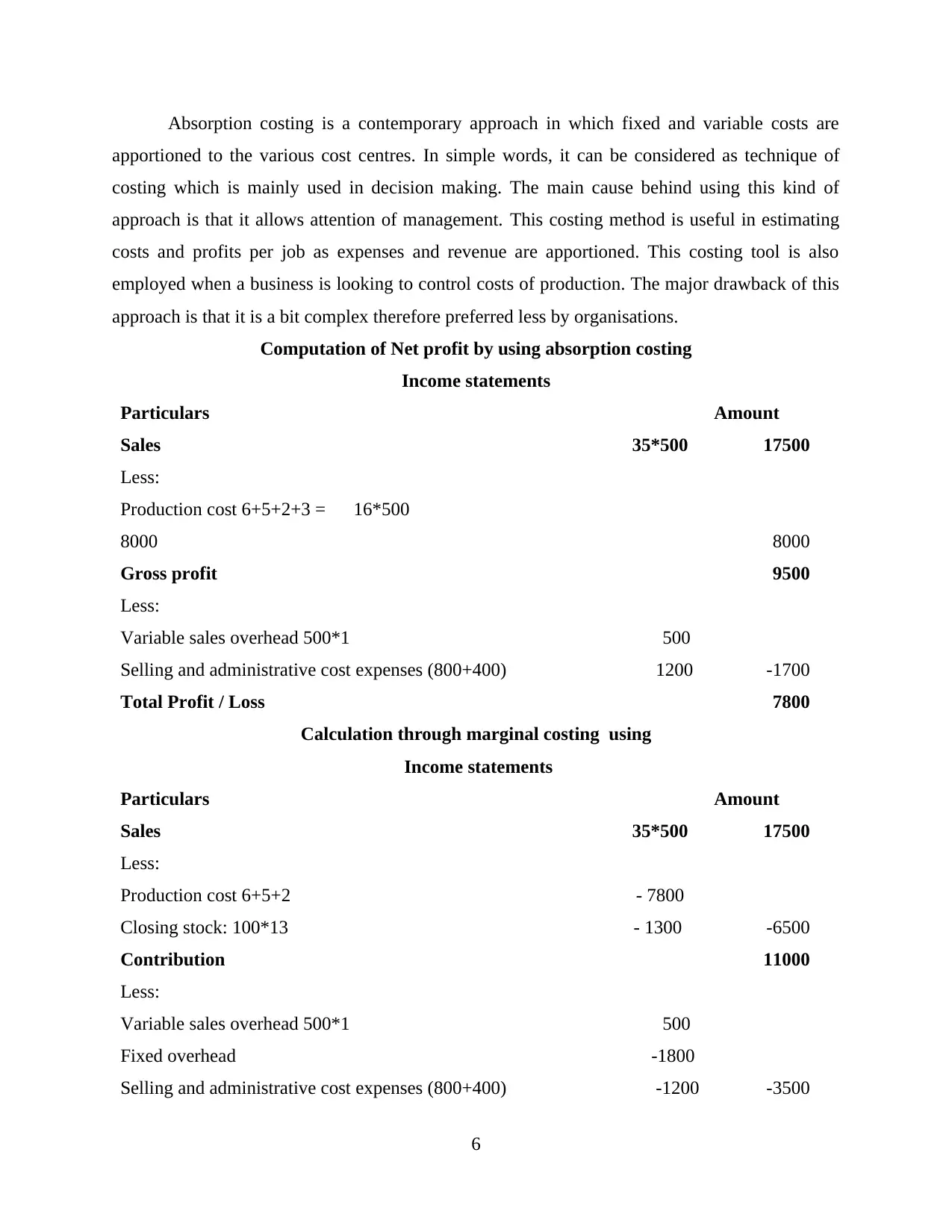

Absorption costing is a contemporary approach in which fixed and variable costs are

apportioned to the various cost centres. In simple words, it can be considered as technique of

costing which is mainly used in decision making. The main cause behind using this kind of

approach is that it allows attention of management. This costing method is useful in estimating

costs and profits per job as expenses and revenue are apportioned. This costing tool is also

employed when a business is looking to control costs of production. The major drawback of this

approach is that it is a bit complex therefore preferred less by organisations.

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

6

apportioned to the various cost centres. In simple words, it can be considered as technique of

costing which is mainly used in decision making. The main cause behind using this kind of

approach is that it allows attention of management. This costing method is useful in estimating

costs and profits per job as expenses and revenue are apportioned. This costing tool is also

employed when a business is looking to control costs of production. The major drawback of this

approach is that it is a bit complex therefore preferred less by organisations.

Computation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation through marginal costing using

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

6

Total Profit / Loss 7500

M2: Utilisation of accounting techniques

There are certain factors which are affecting the financial position of Zylla company.

Some of factors those are related with internal and external department. However, manages

require to implement various accounting tools in order to reduce financial mistake and errors

those are crucial for the purpose of making effective decision-making.

D2: Critical evaluation of income statement

In order to make generate more better results in coming time for zylla company. There

are two effective methods of costing which is helpful in evaluating net profit of the company.

The difference of 300 is arises because of fixed expenses adjustments.

TASK 3

P4. Use of planning tools in budgetary control

Budget: It is a financial plan which is prepared on the basis on forecasting the income

and expenditure incurred in future business activities of an organisation. The manager of

company is held responsible to fix certain amount of money for specific business activities that

will help them in getting positive outcomes (Renz, 2016). Thus, budget preparation help

company in reducing wastage and utilising available financial resources at an optimum manner.

Budgetary control: It is a process of controlling and monitoring the financial resources

used for future planned activities in such an effective manner that will help company in getting

positive result. The manager of company is liable to make comparison actual result with

expected result in order to determine the future profitability (Kotas, 2014). Through budgetary

control system the manager can easily find out the deviations and problems that may arise while

future business activities and accordingly take corrective measures to overcome such problems

which help in reducing the excessive usage of financial resources in different business activities.

Planning tools: It refers to effective tools and techniques which is required to manage

and control budget in order to achieve expected desired result. Some planning tools are as

follows:

Budgeting methods:

7

M2: Utilisation of accounting techniques

There are certain factors which are affecting the financial position of Zylla company.

Some of factors those are related with internal and external department. However, manages

require to implement various accounting tools in order to reduce financial mistake and errors

those are crucial for the purpose of making effective decision-making.

D2: Critical evaluation of income statement

In order to make generate more better results in coming time for zylla company. There

are two effective methods of costing which is helpful in evaluating net profit of the company.

The difference of 300 is arises because of fixed expenses adjustments.

TASK 3

P4. Use of planning tools in budgetary control

Budget: It is a financial plan which is prepared on the basis on forecasting the income

and expenditure incurred in future business activities of an organisation. The manager of

company is held responsible to fix certain amount of money for specific business activities that

will help them in getting positive outcomes (Renz, 2016). Thus, budget preparation help

company in reducing wastage and utilising available financial resources at an optimum manner.

Budgetary control: It is a process of controlling and monitoring the financial resources

used for future planned activities in such an effective manner that will help company in getting

positive result. The manager of company is liable to make comparison actual result with

expected result in order to determine the future profitability (Kotas, 2014). Through budgetary

control system the manager can easily find out the deviations and problems that may arise while

future business activities and accordingly take corrective measures to overcome such problems

which help in reducing the excessive usage of financial resources in different business activities.

Planning tools: It refers to effective tools and techniques which is required to manage

and control budget in order to achieve expected desired result. Some planning tools are as

follows:

Budgeting methods:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incremental budgeting: It is known as one of the crucial budget which is prepared by

using last period's budget or actual performances as a basis with incremental costs included for

new budgeted period (Strumickas and Valanciene, 2015). There are some useful aspects those

are associated with this types of budgets are mention underneath:

The proper allocation of resources is relies upon allocation from the last year.

By the help of this approaches manager cannot recommended as they fails to explain to

takes into account changing situations.

It would encourages total spendings up to the budget to make reasonable allocation in

next period.

Advantages:

It is more stable and constant but it change gradually.

Managers would operate their departments on a regular basis.

The system is relatively more easy to operate and understand every aspects those are

helpful in detecting any issues regarding future planning.

This system is more helpful in solving conflicts if arises in departments that can seen to

be treated similarly.

Disadvantages:

It assume activities and techniques of working that will be continues in same common

way.

No changes of any incentive for formulating new ideas of improvement.

The budget can become out dated and it will no longer associated to the level of activities

or different types of work being formulated during the period of time.

The priority for resources can be changed thus, budgets were set at real costs.

There is no any incentives provided to reduce costs.

It increase spending up to the budget so that the budgets is more next year accordingly.

Zero based budgeting: It is known as budgeting techniques that allocate funds based on

program efficiency and its necessity those are rather than budget history. As its opposed to

traditional budgeting no items is automatically consists in the next budgets. Under this, person

use to make reviews of every program and expenses at the beginning of each budgeted period. It

must be justify that each items in order to retain funding. Budgeting can utilize ZBB to any kind

8

using last period's budget or actual performances as a basis with incremental costs included for

new budgeted period (Strumickas and Valanciene, 2015). There are some useful aspects those

are associated with this types of budgets are mention underneath:

The proper allocation of resources is relies upon allocation from the last year.

By the help of this approaches manager cannot recommended as they fails to explain to

takes into account changing situations.

It would encourages total spendings up to the budget to make reasonable allocation in

next period.

Advantages:

It is more stable and constant but it change gradually.

Managers would operate their departments on a regular basis.

The system is relatively more easy to operate and understand every aspects those are

helpful in detecting any issues regarding future planning.

This system is more helpful in solving conflicts if arises in departments that can seen to

be treated similarly.

Disadvantages:

It assume activities and techniques of working that will be continues in same common

way.

No changes of any incentive for formulating new ideas of improvement.

The budget can become out dated and it will no longer associated to the level of activities

or different types of work being formulated during the period of time.

The priority for resources can be changed thus, budgets were set at real costs.

There is no any incentives provided to reduce costs.

It increase spending up to the budget so that the budgets is more next year accordingly.

Zero based budgeting: It is known as budgeting techniques that allocate funds based on

program efficiency and its necessity those are rather than budget history. As its opposed to

traditional budgeting no items is automatically consists in the next budgets. Under this, person

use to make reviews of every program and expenses at the beginning of each budgeted period. It

must be justify that each items in order to retain funding. Budgeting can utilize ZBB to any kind

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of cost, capital expenses and operation expenditure and administrative costs or COGS

(Vakalfotis, Ballantine and Wall, 2013).

Advantages

It results budgets in well justified and aligned to strategic planning.

This would catalyses broader cooperation across the organisation.

It would help to improve operational efficiency by facing various challenging of

assumptions.

This budgets activity would cost reduction by avoiding automatic budgets can enhance

that are often resulting in savings.

Disadvantages:

It is to costly and complex as well as time consuming because budget is rebuilt from

scratch annually, whereas more faster traditional budgeting can requires proper

justification which can only applicable for incremental costs.

It may be cost-prohibitive for every organisations with specific funding.

The execution challenges related to budget period timing is more constraints.

Activity based budgeting: It is one of the crucial method of budgeting under which the

activities that incur in every functional areas of an organisation those are recorded. There is a

relationships which defined and analysed accordingly. It does not simply adjust prior budgeting

to account for inflation and other business developments (Ward, 2012).

Advantages:

It is followed for better degrees of control over the budgeting process.

Revenue and expenditure planning can occurs at a finer level that would provide valuable

information regarding project examination.

Disadvantages:

It is more costly, if it has been compared to as traditional budgeting techniques. It needed

more information and time for management.

It require more assumptions and insight from administrations.

Process of budget controlling:

Discuss with managers of different departments: It is required for managers of different

departments of company to communicate with each other and discuss about the relevant facts

and informations which will be helpful in performing future business activities.

9

(Vakalfotis, Ballantine and Wall, 2013).

Advantages

It results budgets in well justified and aligned to strategic planning.

This would catalyses broader cooperation across the organisation.

It would help to improve operational efficiency by facing various challenging of

assumptions.

This budgets activity would cost reduction by avoiding automatic budgets can enhance

that are often resulting in savings.

Disadvantages:

It is to costly and complex as well as time consuming because budget is rebuilt from

scratch annually, whereas more faster traditional budgeting can requires proper

justification which can only applicable for incremental costs.

It may be cost-prohibitive for every organisations with specific funding.

The execution challenges related to budget period timing is more constraints.

Activity based budgeting: It is one of the crucial method of budgeting under which the

activities that incur in every functional areas of an organisation those are recorded. There is a

relationships which defined and analysed accordingly. It does not simply adjust prior budgeting

to account for inflation and other business developments (Ward, 2012).

Advantages:

It is followed for better degrees of control over the budgeting process.

Revenue and expenditure planning can occurs at a finer level that would provide valuable

information regarding project examination.

Disadvantages:

It is more costly, if it has been compared to as traditional budgeting techniques. It needed

more information and time for management.

It require more assumptions and insight from administrations.

Process of budget controlling:

Discuss with managers of different departments: It is required for managers of different

departments of company to communicate with each other and discuss about the relevant facts

and informations which will be helpful in performing future business activities.

9

Make proper assumptions and declaration: In order to perform planned activities

without facing any problems the manager should make assumptions related to cost incurred in

future production process through which they can ready with abundant financial resources to

face such challenges.

Set systematic information for budget to achieve objectives: It is the responsibility of

manager to collect information and data from each department which is required in preparing

budget for future business activities.

Measurement of actual with standard: Manager need to measure actual performance by

comparing actual data with the expected data which help them in identifying deviations and

problems that may occurred during performing planned activities (Herzig and et.al. 2012).

Review stages: It is the last and final stage where the managers review and analyse the

budget and check whether any changes made or not to complete business activities.

M3: Evaluation of planning tools

It is important for the Zylla to analyse performance of company through using master

budget, cash budgets etc. and accordingly adopt an effective planning tool among various

planning tools which help them to achieve positive result. Operating budget is very useful for

company in analysing total revenue and cost expenditure incurred in production process of each

units. The company can achieve huge profit only when the manger prepare cash budget and static

budget which also help them in managing the financial resources and controlling the irrelevant

cost incurred in future business activities.

D3: Tools used for resolving financial issues

An organisation who faces financial crisis will need to implement effective and efficient

tools and methods which help them to compete with their competitors. The survival of company

may comes in danger if the manager fail to manage and control financial risk. Thus it is

important for company to maintain and check accounting and financial reports on regular basis

and identify the chances of the facing financial losses with a motive of eliminating them in an

organised manner.

10

without facing any problems the manager should make assumptions related to cost incurred in

future production process through which they can ready with abundant financial resources to

face such challenges.

Set systematic information for budget to achieve objectives: It is the responsibility of

manager to collect information and data from each department which is required in preparing

budget for future business activities.

Measurement of actual with standard: Manager need to measure actual performance by

comparing actual data with the expected data which help them in identifying deviations and

problems that may occurred during performing planned activities (Herzig and et.al. 2012).

Review stages: It is the last and final stage where the managers review and analyse the

budget and check whether any changes made or not to complete business activities.

M3: Evaluation of planning tools

It is important for the Zylla to analyse performance of company through using master

budget, cash budgets etc. and accordingly adopt an effective planning tool among various

planning tools which help them to achieve positive result. Operating budget is very useful for

company in analysing total revenue and cost expenditure incurred in production process of each

units. The company can achieve huge profit only when the manger prepare cash budget and static

budget which also help them in managing the financial resources and controlling the irrelevant

cost incurred in future business activities.

D3: Tools used for resolving financial issues

An organisation who faces financial crisis will need to implement effective and efficient

tools and methods which help them to compete with their competitors. The survival of company

may comes in danger if the manager fail to manage and control financial risk. Thus it is

important for company to maintain and check accounting and financial reports on regular basis

and identify the chances of the facing financial losses with a motive of eliminating them in an

organised manner.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.