Comparison of Manufacturing and Purchasing the Product

VerifiedAdded on 2019/11/26

|11

|2601

|2077

Report

AI Summary

The analysis concludes that purchasing the product instead of manufacturing it would be more economical for Water World Ltd. The company's employees are not satisfied with their salaries and there is a lack of coordination between workers, which affects productivity. To improve motivation, regular communication and feedback should be shared with employees. Additionally, recognizing employee efforts and providing rewards can encourage them to work efficiently. In the long run, efficient management will lead to better profits.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Part A.....................................................................................................................................3

Part B......................................................................................................................................3

Part C......................................................................................................................................3

Question 2..................................................................................................................................3

References..................................................................................................................................4

Question 1..................................................................................................................................3

Part A.....................................................................................................................................3

Part B......................................................................................................................................3

Part C......................................................................................................................................3

Question 2..................................................................................................................................3

References..................................................................................................................................4

QUESTION 1

Introduction

Present part of the study is based on analysis of case situation of Nestle regarding the

evaluation of budgetary slack. It will include a description of budgetary slack and its

consequence regarding the performance of the business. Further, the recommendation will be

providing regarding the development of effective bonus plan to motivate managers for

providing better performance in an ethical manner.

Part A

Budgetary slack:

It refers to an allowance adjusted deliberately in expectation of future cash flow. It can take

either of two forms:

Underestimation of income or revenue generated in a certain period.

Overestimation of expenses to be paid for a certain period.

In other words, it can be said that Budgetary slack is the practice of underestimating

revenues or overestimating expenses while preparing a budget. This helps the managers

mainly in improving their financial performance (Sallis, 2014). For example, this practice is

primarily used in performance appraisals and bonuses which are according to the

achievement of these budgeted numbers.

Consequence:

Employees get a very low incentive for meeting their budgeted goals thus the

performance of the organisation falls or is interfered. Companies having stretch goals

perform much better as compare to the companies having constant budgetary slack for a

number of consecutive years (Kerzner, 2013). Hence, this budgetary slack has a negative

consequence on the business. It also affects the profits and competitive position of the

company for long term.

If the managers of the Nestle who can set expectations very high are allowed input

into the budget model, then the chances of budgetary slack to occur is very low. Further, in

the cited case of Nestle there is no relation in performance, and bonus plans due to which

slack is very less likely to occur (Hill, Jones and Schilling, 2014). In a situation where there is

uncertainty about the results to be expected for a period of time the chances of budgetary

Introduction

Present part of the study is based on analysis of case situation of Nestle regarding the

evaluation of budgetary slack. It will include a description of budgetary slack and its

consequence regarding the performance of the business. Further, the recommendation will be

providing regarding the development of effective bonus plan to motivate managers for

providing better performance in an ethical manner.

Part A

Budgetary slack:

It refers to an allowance adjusted deliberately in expectation of future cash flow. It can take

either of two forms:

Underestimation of income or revenue generated in a certain period.

Overestimation of expenses to be paid for a certain period.

In other words, it can be said that Budgetary slack is the practice of underestimating

revenues or overestimating expenses while preparing a budget. This helps the managers

mainly in improving their financial performance (Sallis, 2014). For example, this practice is

primarily used in performance appraisals and bonuses which are according to the

achievement of these budgeted numbers.

Consequence:

Employees get a very low incentive for meeting their budgeted goals thus the

performance of the organisation falls or is interfered. Companies having stretch goals

perform much better as compare to the companies having constant budgetary slack for a

number of consecutive years (Kerzner, 2013). Hence, this budgetary slack has a negative

consequence on the business. It also affects the profits and competitive position of the

company for long term.

If the managers of the Nestle who can set expectations very high are allowed input

into the budget model, then the chances of budgetary slack to occur is very low. Further, in

the cited case of Nestle there is no relation in performance, and bonus plans due to which

slack is very less likely to occur (Hill, Jones and Schilling, 2014). In a situation where there is

uncertainty about the results to be expected for a period of time the chances of budgetary

slack increases. As a result, under such conditions managers while creating budgets become

more conservative. If there is no source of reliability, as no historical records for possible

results and the budget are created for new product line then also budgetary slack prevails.

Part B

The organization put a significant level of trust into their management. From CEO to

employees, managers contain the full responsibility to ensure that their behaviours and

attitude is ethical and have the best of interest of primary as well as secondary stakeholders

(Gallani and et al., 2015). Being a manager, it is significant to consider ethical behaviours so

as to experience, company’s desires for conduct, ensuring right behaviours of subordinates,

and to reduce vagueness that mostly arrive while practising ethics.

Thus, it vital to consider codes of conduct and ethics, set of regulations and to achieve

and maintain records of linked documentation placed for the expectations and framework

purposely for ethical behaviour. It is also a responsibility of the manager to certify that those

who are responsible for reporting are required to understand these rules.

A manager working on ethical behaviour is also duty-bound to set the prospect, and

all ethically unsafe practices are disallowed. Any of the members conducting this type act has

the duty to report it to an appropriate channel (Douthit and et al., 2016). Managers that

continuously make use of Code of Conduct of company or any other same program with the

other recognized and expected behaviour offer a base of ethical conduct and belief in their

relationship with the stakeholders.

Part C

Managers have the position in the company to assist the management in

accomplishing its strategic goals and objectives. The major thing to consider is the incentive

plan is the objective to motivate their team members, and this plays a vital role in the success

and growth of the company. There is the existence of a broad range of incentive plans, to

assist managers in being focused on activities and drive great opportunities (Daumoser, Sohn

and Hirsch, 2016). A mix of incentive plans must be taken by Nestle into account to create a

great reward package so it can assist in achievements and retentions. A business entity can

make a reduction in budgeting problem in many ways, primarily, it must prevent dependence

on budgets as an obstructive and evaluative tool. Next, managers must be provided incentives

for attaining their projects on budgets as well as to offer proper and correct projections

through adopting Zero based budgeting and by applying these following tools:

more conservative. If there is no source of reliability, as no historical records for possible

results and the budget are created for new product line then also budgetary slack prevails.

Part B

The organization put a significant level of trust into their management. From CEO to

employees, managers contain the full responsibility to ensure that their behaviours and

attitude is ethical and have the best of interest of primary as well as secondary stakeholders

(Gallani and et al., 2015). Being a manager, it is significant to consider ethical behaviours so

as to experience, company’s desires for conduct, ensuring right behaviours of subordinates,

and to reduce vagueness that mostly arrive while practising ethics.

Thus, it vital to consider codes of conduct and ethics, set of regulations and to achieve

and maintain records of linked documentation placed for the expectations and framework

purposely for ethical behaviour. It is also a responsibility of the manager to certify that those

who are responsible for reporting are required to understand these rules.

A manager working on ethical behaviour is also duty-bound to set the prospect, and

all ethically unsafe practices are disallowed. Any of the members conducting this type act has

the duty to report it to an appropriate channel (Douthit and et al., 2016). Managers that

continuously make use of Code of Conduct of company or any other same program with the

other recognized and expected behaviour offer a base of ethical conduct and belief in their

relationship with the stakeholders.

Part C

Managers have the position in the company to assist the management in

accomplishing its strategic goals and objectives. The major thing to consider is the incentive

plan is the objective to motivate their team members, and this plays a vital role in the success

and growth of the company. There is the existence of a broad range of incentive plans, to

assist managers in being focused on activities and drive great opportunities (Daumoser, Sohn

and Hirsch, 2016). A mix of incentive plans must be taken by Nestle into account to create a

great reward package so it can assist in achievements and retentions. A business entity can

make a reduction in budgeting problem in many ways, primarily, it must prevent dependence

on budgets as an obstructive and evaluative tool. Next, managers must be provided incentives

for attaining their projects on budgets as well as to offer proper and correct projections

through adopting Zero based budgeting and by applying these following tools:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Pay-for-Performance

A knowledgeable management company, APQC made use of researchers in order to

identify that paying according to their performance at all levels is the best way in an entity, as

this tool is unbiased and by this managers and employees stay motivated and will focus on

giving the best performance (Nouri and Kyj, 2014). This model usually includes a paying rate

combined with a variable rate which is particularly knotted to the performance of an

individual. Best performing managers are normally familiar and amendable to this model; it

is because it introduces a precise connection between individual’s performance and

attainment toward company goals.

Stock Options

In 2001, more than 30000 diverse options of stocks were used by firms in and around

the US. Stock options are formerly an incentive provided especially to a company’s best

performers. Stock options are generally provided by an employer as an incentive of employee

retention (De Baerdemaeker and Bruggeman, 2014). This concept for the stock option is to

add value in a specific time period so that employees can be able to sell their stock at

proceeds when the designated period of waiting expires. These incentives can inspire and

motivate managers to surpass their goals along with the expectation to positively drive the

stock value of the company.

Recognition

Business entities who deeply rely on knowing their achievement of leading managers,

often forgot the influences have on impacting performance made by managers. Managers

performing at Mid-level might be particularly ignored, as their performance is not visible to

upper management (Fullerton, Kennedy and Widener, 2014). Every employee in the

management team must be compensated, publicly as well as privately for their performance

that goes beyond the expectations. This incentive plan can also include bonus like gifts,

certificates, additional vacation days and trophies.

Conclusion

By considering above description company is required to develop an effective bonus

plan for managers by including factors such as Pay-for-Performance, stock options and

recognition to motivate them to operate ethically for attaining goals and objectives of

business.

A knowledgeable management company, APQC made use of researchers in order to

identify that paying according to their performance at all levels is the best way in an entity, as

this tool is unbiased and by this managers and employees stay motivated and will focus on

giving the best performance (Nouri and Kyj, 2014). This model usually includes a paying rate

combined with a variable rate which is particularly knotted to the performance of an

individual. Best performing managers are normally familiar and amendable to this model; it

is because it introduces a precise connection between individual’s performance and

attainment toward company goals.

Stock Options

In 2001, more than 30000 diverse options of stocks were used by firms in and around

the US. Stock options are formerly an incentive provided especially to a company’s best

performers. Stock options are generally provided by an employer as an incentive of employee

retention (De Baerdemaeker and Bruggeman, 2014). This concept for the stock option is to

add value in a specific time period so that employees can be able to sell their stock at

proceeds when the designated period of waiting expires. These incentives can inspire and

motivate managers to surpass their goals along with the expectation to positively drive the

stock value of the company.

Recognition

Business entities who deeply rely on knowing their achievement of leading managers,

often forgot the influences have on impacting performance made by managers. Managers

performing at Mid-level might be particularly ignored, as their performance is not visible to

upper management (Fullerton, Kennedy and Widener, 2014). Every employee in the

management team must be compensated, publicly as well as privately for their performance

that goes beyond the expectations. This incentive plan can also include bonus like gifts,

certificates, additional vacation days and trophies.

Conclusion

By considering above description company is required to develop an effective bonus

plan for managers by including factors such as Pay-for-Performance, stock options and

recognition to motivate them to operate ethically for attaining goals and objectives of

business.

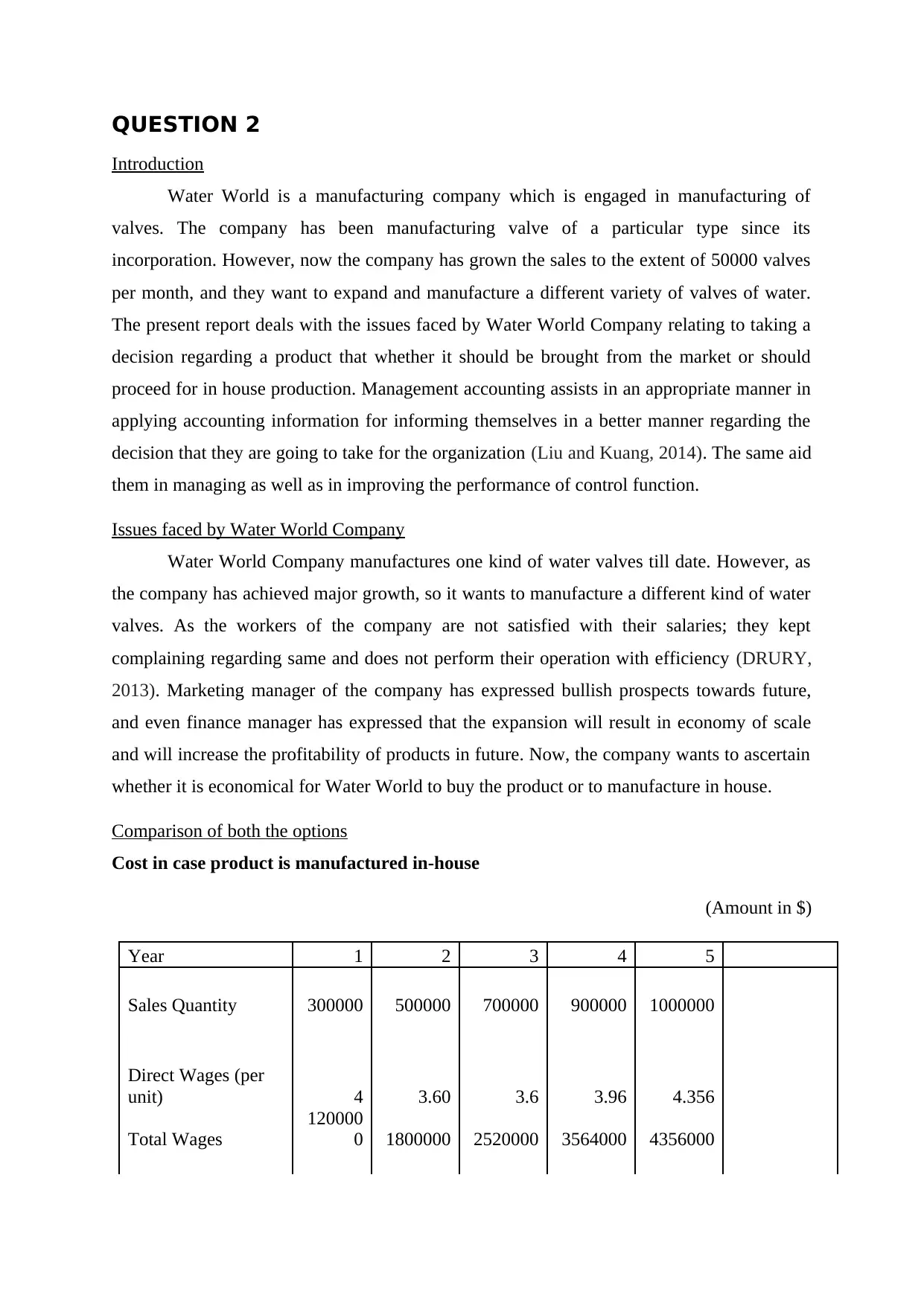

QUESTION 2

Introduction

Water World is a manufacturing company which is engaged in manufacturing of

valves. The company has been manufacturing valve of a particular type since its

incorporation. However, now the company has grown the sales to the extent of 50000 valves

per month, and they want to expand and manufacture a different variety of valves of water.

The present report deals with the issues faced by Water World Company relating to taking a

decision regarding a product that whether it should be brought from the market or should

proceed for in house production. Management accounting assists in an appropriate manner in

applying accounting information for informing themselves in a better manner regarding the

decision that they are going to take for the organization (Liu and Kuang, 2014). The same aid

them in managing as well as in improving the performance of control function.

Issues faced by Water World Company

Water World Company manufactures one kind of water valves till date. However, as

the company has achieved major growth, so it wants to manufacture a different kind of water

valves. As the workers of the company are not satisfied with their salaries; they kept

complaining regarding same and does not perform their operation with efficiency (DRURY,

2013). Marketing manager of the company has expressed bullish prospects towards future,

and even finance manager has expressed that the expansion will result in economy of scale

and will increase the profitability of products in future. Now, the company wants to ascertain

whether it is economical for Water World to buy the product or to manufacture in house.

Comparison of both the options

Cost in case product is manufactured in-house

(Amount in $)

Year 1 2 3 4 5

Sales Quantity 300000 500000 700000 900000 1000000

Direct Wages (per

unit) 4 3.60 3.6 3.96 4.356

Total Wages

120000

0 1800000 2520000 3564000 4356000

Introduction

Water World is a manufacturing company which is engaged in manufacturing of

valves. The company has been manufacturing valve of a particular type since its

incorporation. However, now the company has grown the sales to the extent of 50000 valves

per month, and they want to expand and manufacture a different variety of valves of water.

The present report deals with the issues faced by Water World Company relating to taking a

decision regarding a product that whether it should be brought from the market or should

proceed for in house production. Management accounting assists in an appropriate manner in

applying accounting information for informing themselves in a better manner regarding the

decision that they are going to take for the organization (Liu and Kuang, 2014). The same aid

them in managing as well as in improving the performance of control function.

Issues faced by Water World Company

Water World Company manufactures one kind of water valves till date. However, as

the company has achieved major growth, so it wants to manufacture a different kind of water

valves. As the workers of the company are not satisfied with their salaries; they kept

complaining regarding same and does not perform their operation with efficiency (DRURY,

2013). Marketing manager of the company has expressed bullish prospects towards future,

and even finance manager has expressed that the expansion will result in economy of scale

and will increase the profitability of products in future. Now, the company wants to ascertain

whether it is economical for Water World to buy the product or to manufacture in house.

Comparison of both the options

Cost in case product is manufactured in-house

(Amount in $)

Year 1 2 3 4 5

Sales Quantity 300000 500000 700000 900000 1000000

Direct Wages (per

unit) 4 3.60 3.6 3.96 4.356

Total Wages

120000

0 1800000 2520000 3564000 4356000

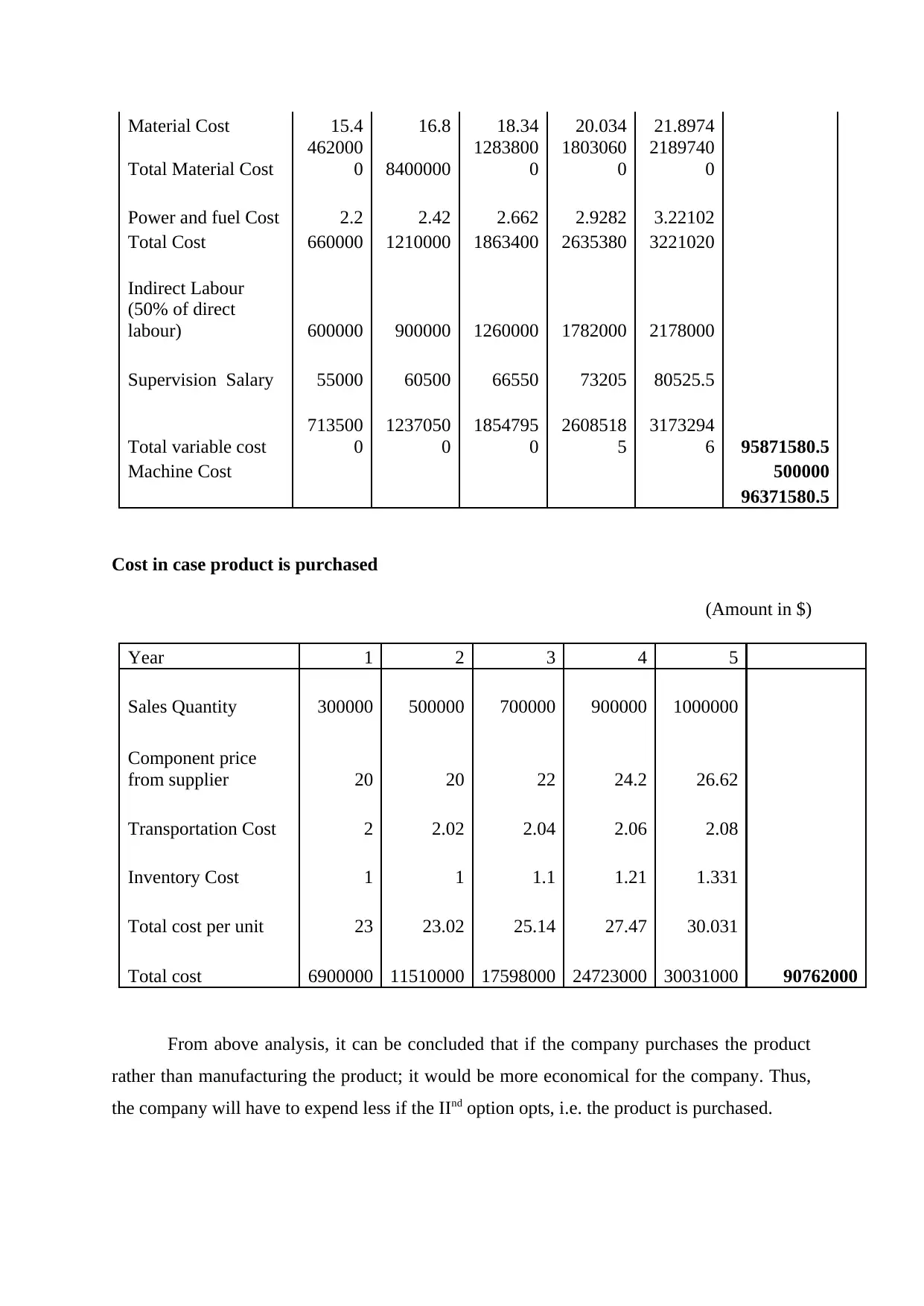

Material Cost 15.4 16.8 18.34 20.034 21.8974

Total Material Cost

462000

0 8400000

1283800

0

1803060

0

2189740

0

Power and fuel Cost 2.2 2.42 2.662 2.9282 3.22102

Total Cost 660000 1210000 1863400 2635380 3221020

Indirect Labour

(50% of direct

labour) 600000 900000 1260000 1782000 2178000

Supervision Salary 55000 60500 66550 73205 80525.5

Total variable cost

713500

0

1237050

0

1854795

0

2608518

5

3173294

6 95871580.5

Machine Cost 500000

96371580.5

Cost in case product is purchased

(Amount in $)

Year 1 2 3 4 5

Sales Quantity 300000 500000 700000 900000 1000000

Component price

from supplier 20 20 22 24.2 26.62

Transportation Cost 2 2.02 2.04 2.06 2.08

Inventory Cost 1 1 1.1 1.21 1.331

Total cost per unit 23 23.02 25.14 27.47 30.031

Total cost 6900000 11510000 17598000 24723000 30031000 90762000

From above analysis, it can be concluded that if the company purchases the product

rather than manufacturing the product; it would be more economical for the company. Thus,

the company will have to expend less if the IInd option opts, i.e. the product is purchased.

Total Material Cost

462000

0 8400000

1283800

0

1803060

0

2189740

0

Power and fuel Cost 2.2 2.42 2.662 2.9282 3.22102

Total Cost 660000 1210000 1863400 2635380 3221020

Indirect Labour

(50% of direct

labour) 600000 900000 1260000 1782000 2178000

Supervision Salary 55000 60500 66550 73205 80525.5

Total variable cost

713500

0

1237050

0

1854795

0

2608518

5

3173294

6 95871580.5

Machine Cost 500000

96371580.5

Cost in case product is purchased

(Amount in $)

Year 1 2 3 4 5

Sales Quantity 300000 500000 700000 900000 1000000

Component price

from supplier 20 20 22 24.2 26.62

Transportation Cost 2 2.02 2.04 2.06 2.08

Inventory Cost 1 1 1.1 1.21 1.331

Total cost per unit 23 23.02 25.14 27.47 30.031

Total cost 6900000 11510000 17598000 24723000 30031000 90762000

From above analysis, it can be concluded that if the company purchases the product

rather than manufacturing the product; it would be more economical for the company. Thus,

the company will have to expend less if the IInd option opts, i.e. the product is purchased.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other factors to be considered

In a situation where a company wants to make a profit for the long term than it is

necessary that efficient management should exist in the company. In the present case of

Water World Ltd; the employees are not satisfied with the salaries which have been provided

to them and no appropriate management among workers regarding the time they spent on

working exist. In these situations, it is impossible to attain predetermined goals. It is

necessary that company manager should make efforts to maintain coordination between

employees and higher authority (Shields, 2015).

Employee motivation is considered to be the constant challenge on the workplace

been faced by company. Especially at a workplace where there is no emphasizing of

employee satisfaction, and not considering it as a part of a cling and supported business

strategy as whole (Liu and Kuang, 2014). On the other hand, they make out their authority in

drawing on the best employees have to offer; however, they experience themselves as

unsupported, satisfied or familiar on their work to develop motivation further to contributee

employees.

Regular communication with employees by scheduling staff meeting in order to

update them any of the information of company that can influence their work. Feedbacks and

reviews of customers, changing of due dates, improvements in commodities, guidance and

training and updates on divisions reporting on communicating structures are the significant

factors that must be shared with employees (Douthit and et.al. 2016). Communicating and

meeting is most significant aspect in any business management.

Regular communication with each and every employee is important as it develops

more motivation in them, even though a polite good morning can allow the employee to

engage with them. Ensuring that the employees are clear about their job, objectives time,

efforts and decisions. Organization must pause or stop in those areas which are specially

impacted by changes.

Further, they should be encouraged for making an efficient effort and should assure

that they will be awarded appropriately for the same. In situation where company wants that

employees work hard than it is necessary that appropriate award should be rewarded to them

in return. By making small changes in organization and payment methods, the company will

be able to satisfy employees as well as earn more profits.

In a situation where a company wants to make a profit for the long term than it is

necessary that efficient management should exist in the company. In the present case of

Water World Ltd; the employees are not satisfied with the salaries which have been provided

to them and no appropriate management among workers regarding the time they spent on

working exist. In these situations, it is impossible to attain predetermined goals. It is

necessary that company manager should make efforts to maintain coordination between

employees and higher authority (Shields, 2015).

Employee motivation is considered to be the constant challenge on the workplace

been faced by company. Especially at a workplace where there is no emphasizing of

employee satisfaction, and not considering it as a part of a cling and supported business

strategy as whole (Liu and Kuang, 2014). On the other hand, they make out their authority in

drawing on the best employees have to offer; however, they experience themselves as

unsupported, satisfied or familiar on their work to develop motivation further to contributee

employees.

Regular communication with employees by scheduling staff meeting in order to

update them any of the information of company that can influence their work. Feedbacks and

reviews of customers, changing of due dates, improvements in commodities, guidance and

training and updates on divisions reporting on communicating structures are the significant

factors that must be shared with employees (Douthit and et.al. 2016). Communicating and

meeting is most significant aspect in any business management.

Regular communication with each and every employee is important as it develops

more motivation in them, even though a polite good morning can allow the employee to

engage with them. Ensuring that the employees are clear about their job, objectives time,

efforts and decisions. Organization must pause or stop in those areas which are specially

impacted by changes.

Further, they should be encouraged for making an efficient effort and should assure

that they will be awarded appropriately for the same. In situation where company wants that

employees work hard than it is necessary that appropriate award should be rewarded to them

in return. By making small changes in organization and payment methods, the company will

be able to satisfy employees as well as earn more profits.

Conclusion and recommendations

Cited part of study shows that in decision making process it is important for managers

to consider financial as well as non-financial factors to ensure its viability and impact on

business activities. With this approach sound decisions can be taken by managerial

authorities through which better opportunities for growth and high profitability can be

attained. Further, human resources is the most crucial asset for business thus managers should

be focused to create better work environment for them to keep them motivated so they can

contribute for value creation.

Cited part of study shows that in decision making process it is important for managers

to consider financial as well as non-financial factors to ensure its viability and impact on

business activities. With this approach sound decisions can be taken by managerial

authorities through which better opportunities for growth and high profitability can be

attained. Further, human resources is the most crucial asset for business thus managers should

be focused to create better work environment for them to keep them motivated so they can

contribute for value creation.

REFERENCES

Sallis, E., 2014. Total quality management in education. Routledge.'

Kerzner, H., 2013. Project management: a systems approach to planning, scheduling, and

controlling. John Wiley & Sons.

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management: theory: an

integrated approach. Cengage Learning.

Gallani, S., Krishnan, R., Marinich, E.J. and Shields, M.D., 2015. Budgeting, Psychological

Contracts, and Budgetary Slack.

Douthit, J., Schwartz, S.T., Stevens, D.E. and Young, R.A., 2016. The Effect of Endogenous

Contract Selection on Budgetary Slack: An Experimental Examination of Trust, Distrust, and

Trustworthiness.

Daumoser, C., Sohn, M. and Hirsch, B., 2016. Honesty in Budgeting: A Review of Budgetary

Slack.

Nouri, H. and Kyj, L., 2014. An Experimental Examination of the Combined Effects of

Normative and Instrumental Commitments on Budgetary Slack Creation: Comparing

Individuals versus Group Members. In Advances in Management Accounting (pp. 225-260).

Emerald Group Publishing Limited.

De Baerdemaeker, J. and Bruggeman, W., 2014. How participation in the strategy

development process impacts managers' creation of budgetary slack. In European Accounting

Association 37th Annual Congress (p. 168).

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7), pp.414-428.

Liu, Y. and Kuang, Y., 2014. The Establishment of Management Accounting System in

Administrative Institutions. Journal of Accounting and Economics,2, p.003.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Shields, M.D., 2015. Established management accounting knowledge.Journal of

Management Accounting Research, 27(1), pp.123-132.

Sallis, E., 2014. Total quality management in education. Routledge.'

Kerzner, H., 2013. Project management: a systems approach to planning, scheduling, and

controlling. John Wiley & Sons.

Hill, C.W., Jones, G.R. and Schilling, M.A., 2014. Strategic management: theory: an

integrated approach. Cengage Learning.

Gallani, S., Krishnan, R., Marinich, E.J. and Shields, M.D., 2015. Budgeting, Psychological

Contracts, and Budgetary Slack.

Douthit, J., Schwartz, S.T., Stevens, D.E. and Young, R.A., 2016. The Effect of Endogenous

Contract Selection on Budgetary Slack: An Experimental Examination of Trust, Distrust, and

Trustworthiness.

Daumoser, C., Sohn, M. and Hirsch, B., 2016. Honesty in Budgeting: A Review of Budgetary

Slack.

Nouri, H. and Kyj, L., 2014. An Experimental Examination of the Combined Effects of

Normative and Instrumental Commitments on Budgetary Slack Creation: Comparing

Individuals versus Group Members. In Advances in Management Accounting (pp. 225-260).

Emerald Group Publishing Limited.

De Baerdemaeker, J. and Bruggeman, W., 2014. How participation in the strategy

development process impacts managers' creation of budgetary slack. In European Accounting

Association 37th Annual Congress (p. 168).

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7), pp.414-428.

Liu, Y. and Kuang, Y., 2014. The Establishment of Management Accounting System in

Administrative Institutions. Journal of Accounting and Economics,2, p.003.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Shields, M.D., 2015. Established management accounting knowledge.Journal of

Management Accounting Research, 27(1), pp.123-132.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.