Management Accounting Report: IKEA Financial Problem Solving

VerifiedAdded on 2022/11/29

|26

|6558

|203

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within IKEA. It begins with an introduction to management accounting, differentiating it from financial accounting, and outlining its core principles. The report then delves into various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, highlighting their advantages and relevance to IKEA's operations. Furthermore, it explores different methods of management accounting reporting, such as budget reports, accounts receivable reports, and cost reports, emphasizing their significance in managerial decision-making. The report also examines techniques of cost analysis, including cost-volume-profit analysis, and discusses planning tools for budgetary control. Finally, it addresses how IKEA can adopt management accounting systems to respond to financial problems, leading to sustainable success. The report concludes with a summary of key findings and references to relevant sources.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Management accounting and its different types of system..........................................................3

Methods of management accounting reporting...........................................................................7

Techniques of cost analysis.........................................................................................................9

Types of planning tool for budgetary control............................................................................10

Adoption of management accounting system in response of financial problem.......................12

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................3

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Management accounting and its different types of system..........................................................3

Methods of management accounting reporting...........................................................................7

Techniques of cost analysis.........................................................................................................9

Types of planning tool for budgetary control............................................................................10

Adoption of management accounting system in response of financial problem.......................12

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

APPENDIX......................................................................................................................................3

INTRODUCTION

Management accounting refers to the accounting that is concerned with managerial level and

is also known as decision making accounting. This is the base by which managers can determine

the actual performance of the company and the related activities and operation and on the basis

of that they make decision regarding the company which will assist it to have better dealing with

activities and involvement of operations that may lead to success of company in terms of goal

accomplishment (Kostyukova and et.al., 2018). It is also used in the form of planning tool by

which managers will determine the direction on which company need to work. IKEA is a value

based company that create various items related with making the home even more better in terms

of better experience. It is one of the famous company that produces various home accessories,

home appliances and various other. It was founded on 1943. This report will discuss about the

concept of management accounting along with various system and its reporting frameworks.

This report will also shed light on the concept of planning as a base concept with context of

management accounting. Likewise, it will also discuss that how management accounting and

different approaches enable the company to deal with financial issues. Lastly a practical

application of management accounting costing is also presented in the report.

MAIN BODY

Management accounting and its different types of system

Management accounting:

It is one of the major form of accounting concerned with internal user. Management

accounting is mainly considered withy managers and managerial level of organization. It is also

known as decision making accounting because on the basis of managerial report managers

determine the company’s position and performance and take the adequate decision (Rikhardsson

and Yigitbasioglu, 2018).

Management accounting refers to a process and procedures that will lead to have creation

of documents and reports which will aid management in taking decisions (What is Managerial

Accounting?, 2021).

Management accounting involves compiling information that will allow the managers to

make decision and make planning for future (Kristin, 2019).

Management accounting refers to the accounting that is concerned with managerial level and

is also known as decision making accounting. This is the base by which managers can determine

the actual performance of the company and the related activities and operation and on the basis

of that they make decision regarding the company which will assist it to have better dealing with

activities and involvement of operations that may lead to success of company in terms of goal

accomplishment (Kostyukova and et.al., 2018). It is also used in the form of planning tool by

which managers will determine the direction on which company need to work. IKEA is a value

based company that create various items related with making the home even more better in terms

of better experience. It is one of the famous company that produces various home accessories,

home appliances and various other. It was founded on 1943. This report will discuss about the

concept of management accounting along with various system and its reporting frameworks.

This report will also shed light on the concept of planning as a base concept with context of

management accounting. Likewise, it will also discuss that how management accounting and

different approaches enable the company to deal with financial issues. Lastly a practical

application of management accounting costing is also presented in the report.

MAIN BODY

Management accounting and its different types of system

Management accounting:

It is one of the major form of accounting concerned with internal user. Management

accounting is mainly considered withy managers and managerial level of organization. It is also

known as decision making accounting because on the basis of managerial report managers

determine the company’s position and performance and take the adequate decision (Rikhardsson

and Yigitbasioglu, 2018).

Management accounting refers to a process and procedures that will lead to have creation

of documents and reports which will aid management in taking decisions (What is Managerial

Accounting?, 2021).

Management accounting involves compiling information that will allow the managers to

make decision and make planning for future (Kristin, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is the process of identifying, analysing, interpreting and communicating the information to

managers which will further assist the company to move towards the direction of the its objective

with the required and adequate decisions concerning with management.

Principles:

Designing and compiling:

As per this principle management accounting is considered with the best and relevant

data. This means that the management accounting comprises of all such information by which

details regarding past, present and future can be grabbed (Volkovska, 2017). This will lead to

better decision making.

Management by exception:

This principle is implemented when information is being presented to management. This

means that only information related with budgetary control and standard costing is presented.

This will lead to the comparison of actual performance with the standard (Principles of

Management Accounting, 2021). Here the deviation are found and corrective actions are taken.

Use of return on investment:

It is also called return on capital employed. The rate concerning return indicate the

efficiency of business. This is for the reason capital employed is calculated on the basis of real

money value.

Integration:

Here all the required information is integrated and used in such a way that the cost will be

minimum and the concerned benefits will be maximum.

Controllable and uncontrollable cost:

There is always such cost which is controllable and uncontrollable with regard to

business. Management accounting suggest techniques through which steps can be taken in order

to control the controllable cost.

Forward looking:

Management accounting always works on the forward looking approach. It fix standard

and make plans regarding the future controlling and efficiency.

Difference between management and financial accounting:

Financial accounting Management accounting

managers which will further assist the company to move towards the direction of the its objective

with the required and adequate decisions concerning with management.

Principles:

Designing and compiling:

As per this principle management accounting is considered with the best and relevant

data. This means that the management accounting comprises of all such information by which

details regarding past, present and future can be grabbed (Volkovska, 2017). This will lead to

better decision making.

Management by exception:

This principle is implemented when information is being presented to management. This

means that only information related with budgetary control and standard costing is presented.

This will lead to the comparison of actual performance with the standard (Principles of

Management Accounting, 2021). Here the deviation are found and corrective actions are taken.

Use of return on investment:

It is also called return on capital employed. The rate concerning return indicate the

efficiency of business. This is for the reason capital employed is calculated on the basis of real

money value.

Integration:

Here all the required information is integrated and used in such a way that the cost will be

minimum and the concerned benefits will be maximum.

Controllable and uncontrollable cost:

There is always such cost which is controllable and uncontrollable with regard to

business. Management accounting suggest techniques through which steps can be taken in order

to control the controllable cost.

Forward looking:

Management accounting always works on the forward looking approach. It fix standard

and make plans regarding the future controlling and efficiency.

Difference between management and financial accounting:

Financial accounting Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

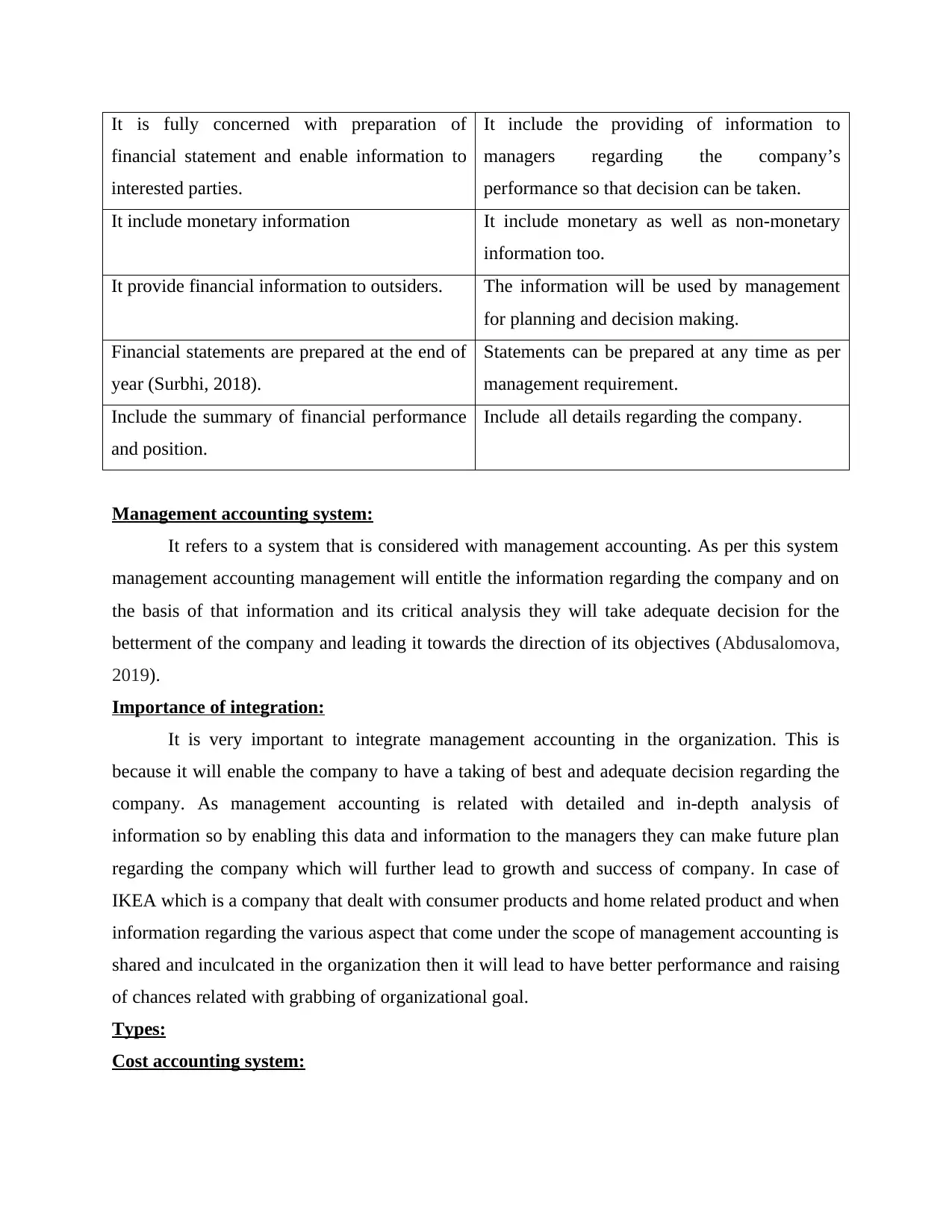

It is fully concerned with preparation of

financial statement and enable information to

interested parties.

It include the providing of information to

managers regarding the company’s

performance so that decision can be taken.

It include monetary information It include monetary as well as non-monetary

information too.

It provide financial information to outsiders. The information will be used by management

for planning and decision making.

Financial statements are prepared at the end of

year (Surbhi, 2018).

Statements can be prepared at any time as per

management requirement.

Include the summary of financial performance

and position.

Include all details regarding the company.

Management accounting system:

It refers to a system that is considered with management accounting. As per this system

management accounting management will entitle the information regarding the company and on

the basis of that information and its critical analysis they will take adequate decision for the

betterment of the company and leading it towards the direction of its objectives (Abdusalomova,

2019).

Importance of integration:

It is very important to integrate management accounting in the organization. This is

because it will enable the company to have a taking of best and adequate decision regarding the

company. As management accounting is related with detailed and in-depth analysis of

information so by enabling this data and information to the managers they can make future plan

regarding the company which will further lead to growth and success of company. In case of

IKEA which is a company that dealt with consumer products and home related product and when

information regarding the various aspect that come under the scope of management accounting is

shared and inculcated in the organization then it will lead to have better performance and raising

of chances related with grabbing of organizational goal.

Types:

Cost accounting system:

financial statement and enable information to

interested parties.

It include the providing of information to

managers regarding the company’s

performance so that decision can be taken.

It include monetary information It include monetary as well as non-monetary

information too.

It provide financial information to outsiders. The information will be used by management

for planning and decision making.

Financial statements are prepared at the end of

year (Surbhi, 2018).

Statements can be prepared at any time as per

management requirement.

Include the summary of financial performance

and position.

Include all details regarding the company.

Management accounting system:

It refers to a system that is considered with management accounting. As per this system

management accounting management will entitle the information regarding the company and on

the basis of that information and its critical analysis they will take adequate decision for the

betterment of the company and leading it towards the direction of its objectives (Abdusalomova,

2019).

Importance of integration:

It is very important to integrate management accounting in the organization. This is

because it will enable the company to have a taking of best and adequate decision regarding the

company. As management accounting is related with detailed and in-depth analysis of

information so by enabling this data and information to the managers they can make future plan

regarding the company which will further lead to growth and success of company. In case of

IKEA which is a company that dealt with consumer products and home related product and when

information regarding the various aspect that come under the scope of management accounting is

shared and inculcated in the organization then it will lead to have better performance and raising

of chances related with grabbing of organizational goal.

Types:

Cost accounting system:

As per this system cost regarding the product is being analysed by the firms. This will

help them to analyse the profitability, valuing inventory and controlling cost. This is an

important system because this will enable the companies to analyse the actual cost and on the

basis of that they can further analyse the profit (Prischenko and Nizovkina, 2017). And in case if

the cost of production is high then by effective controlling it can be maintained too. This system

also enable the company to have a cost-profit analysis which means with the help of this system

profit in association of cost will be analysed and identified.

Advantages:

It is an important system because through this profitable and unprofitable activities can

be identified. It also act as base for future production policies. Here exact cause of declining

profit is also identified.

Inventory management system:

As per this system a watch over the inventory is being performed by the business. This

approach assist the company to monitor the inventory right from making purchase, till transfer to

production and conversion till it will be sold (Chebet and Kitheka, 2019). This will ensure a

check over the inventory. As inventory is a major aspect with regard to company so with an

enabling of inventory management, company can make efficient utilization of it through this

system. This means that with this system not only checking but the problem of over and under

stocking will also be reduced.

Advantages:

It is an essential method because it will keep track inventory and reduced the risk of

wastage and overselling. It will lead to cost saving. It will lead to have better negotiation in

business. It reduces the risk of over and under stork situation.

Job costing system:

It is all related with overhead costing which can be understood as depreciation on

equipment of production and building rent. This is related with one or more cost pool. However,

on the end of every accounting period, the total sum in each cost pool is assigned to various open

jobs. This is based on certain methodology.

Advantages:

help them to analyse the profitability, valuing inventory and controlling cost. This is an

important system because this will enable the companies to analyse the actual cost and on the

basis of that they can further analyse the profit (Prischenko and Nizovkina, 2017). And in case if

the cost of production is high then by effective controlling it can be maintained too. This system

also enable the company to have a cost-profit analysis which means with the help of this system

profit in association of cost will be analysed and identified.

Advantages:

It is an important system because through this profitable and unprofitable activities can

be identified. It also act as base for future production policies. Here exact cause of declining

profit is also identified.

Inventory management system:

As per this system a watch over the inventory is being performed by the business. This

approach assist the company to monitor the inventory right from making purchase, till transfer to

production and conversion till it will be sold (Chebet and Kitheka, 2019). This will ensure a

check over the inventory. As inventory is a major aspect with regard to company so with an

enabling of inventory management, company can make efficient utilization of it through this

system. This means that with this system not only checking but the problem of over and under

stocking will also be reduced.

Advantages:

It is an essential method because it will keep track inventory and reduced the risk of

wastage and overselling. It will lead to cost saving. It will lead to have better negotiation in

business. It reduces the risk of over and under stork situation.

Job costing system:

It is all related with overhead costing which can be understood as depreciation on

equipment of production and building rent. This is related with one or more cost pool. However,

on the end of every accounting period, the total sum in each cost pool is assigned to various open

jobs. This is based on certain methodology.

Advantages:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability regarding each job will be identified individually. It also acts as base for cost

elimination with similar jobs. Here a detailed analysis of the cost regarding material, labour, and

overhead is performed.

Price optimising system:

As per this system the determination of demand variation is calculated with various price

levels. Then this data will be combine with information on cost and inventory level so that the

adequate price will be determined and profit will be raised (Simchi-Levi, 2017). This system also

enable the company to have an adequate determination of the prices as per analysis of the market

demand so that it will ultimately assist the company to grab good percentage of profit.

Advantages:

This system ensure the minimization of possibility of occurrence of any error. It will

enable the companies to make adjustment in prices as per the market trends and situation. This

system enables the companies to secure optimum profits for the business.

However, with respect to IKEA cost accounting, price optimization and inventor control

is usually followed. This is because it enables the IKEA to have adequate availability of

inventory, cost covering with profitability. In the same manner these system also ensure to have

a maintenance of adequate prices so that the company will earn sufficient profits and pricing

strategy.

Presenting financial information:

It is concerned with the financial accounting wherein the financial information is

presented in the form of financial statements. These statements are the base on which the

company’s performance and situation can be analysed and identified. The presented information

is relevant to users including customers, employees, investors, shareholders because it will

enable them to judge and analyse the company’s financial efficiency in terms of its performance.

Information is usually presented in understandable manner because it will enable the user

to understand the company’s financial position. Because if the information is complex then the

user would not be able to understand the complex terms and may not take investment decision.

Thus, it is kept understandable and simple.

elimination with similar jobs. Here a detailed analysis of the cost regarding material, labour, and

overhead is performed.

Price optimising system:

As per this system the determination of demand variation is calculated with various price

levels. Then this data will be combine with information on cost and inventory level so that the

adequate price will be determined and profit will be raised (Simchi-Levi, 2017). This system also

enable the company to have an adequate determination of the prices as per analysis of the market

demand so that it will ultimately assist the company to grab good percentage of profit.

Advantages:

This system ensure the minimization of possibility of occurrence of any error. It will

enable the companies to make adjustment in prices as per the market trends and situation. This

system enables the companies to secure optimum profits for the business.

However, with respect to IKEA cost accounting, price optimization and inventor control

is usually followed. This is because it enables the IKEA to have adequate availability of

inventory, cost covering with profitability. In the same manner these system also ensure to have

a maintenance of adequate prices so that the company will earn sufficient profits and pricing

strategy.

Presenting financial information:

It is concerned with the financial accounting wherein the financial information is

presented in the form of financial statements. These statements are the base on which the

company’s performance and situation can be analysed and identified. The presented information

is relevant to users including customers, employees, investors, shareholders because it will

enable them to judge and analyse the company’s financial efficiency in terms of its performance.

Information is usually presented in understandable manner because it will enable the user

to understand the company’s financial position. Because if the information is complex then the

user would not be able to understand the complex terms and may not take investment decision.

Thus, it is kept understandable and simple.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Methods of management accounting reporting

Management reporting:

It is an essential aspect with regard to management accounting. This is because it enable

the managerial level to have a knowledge regarding the company’s current performance and

requirement. This will also ensure timely taking of decision with regard to company. IKEA also

ensure the inculcation of management accounting reporting so that it can take best decision with

regard to its success.

Methods:

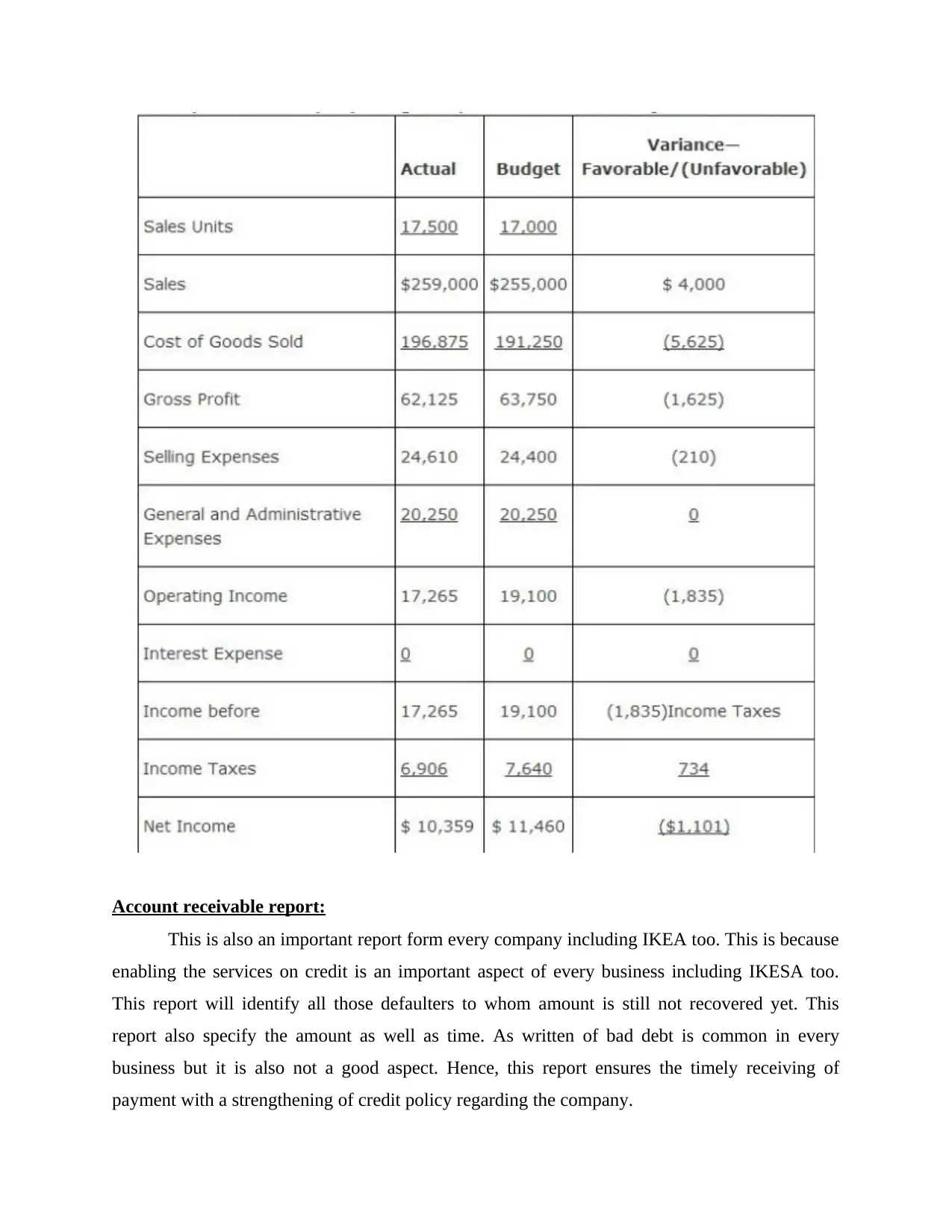

Budget report:

It is an essential type of report concerning managerial accounting. As per this report

estimated budgets regarding the business are prepared and then the activities are plan and

synchronized as per planned budget. Budgets are generally prepared on the basis of past

performance and futuristic plans (Schaltegger, Etxeberria and Ortas, 2017). Various aspects are

being considered while preparing budget. It includes all the sources of income and estimated

expenditure too. This report enable the managers to offer cost cuts, employees incentive,

negotiate terms with vendors and suppliers. This is counted as critical report. IKEA also made

this report and perform its activities within the framework of estimated budget.

This report is significant and relevant because it is made on the basis of past data trends

and analysis. Likewise, this report also include future expected expenses and income so it is

relevant too.

Management reporting:

It is an essential aspect with regard to management accounting. This is because it enable

the managerial level to have a knowledge regarding the company’s current performance and

requirement. This will also ensure timely taking of decision with regard to company. IKEA also

ensure the inculcation of management accounting reporting so that it can take best decision with

regard to its success.

Methods:

Budget report:

It is an essential type of report concerning managerial accounting. As per this report

estimated budgets regarding the business are prepared and then the activities are plan and

synchronized as per planned budget. Budgets are generally prepared on the basis of past

performance and futuristic plans (Schaltegger, Etxeberria and Ortas, 2017). Various aspects are

being considered while preparing budget. It includes all the sources of income and estimated

expenditure too. This report enable the managers to offer cost cuts, employees incentive,

negotiate terms with vendors and suppliers. This is counted as critical report. IKEA also made

this report and perform its activities within the framework of estimated budget.

This report is significant and relevant because it is made on the basis of past data trends

and analysis. Likewise, this report also include future expected expenses and income so it is

relevant too.

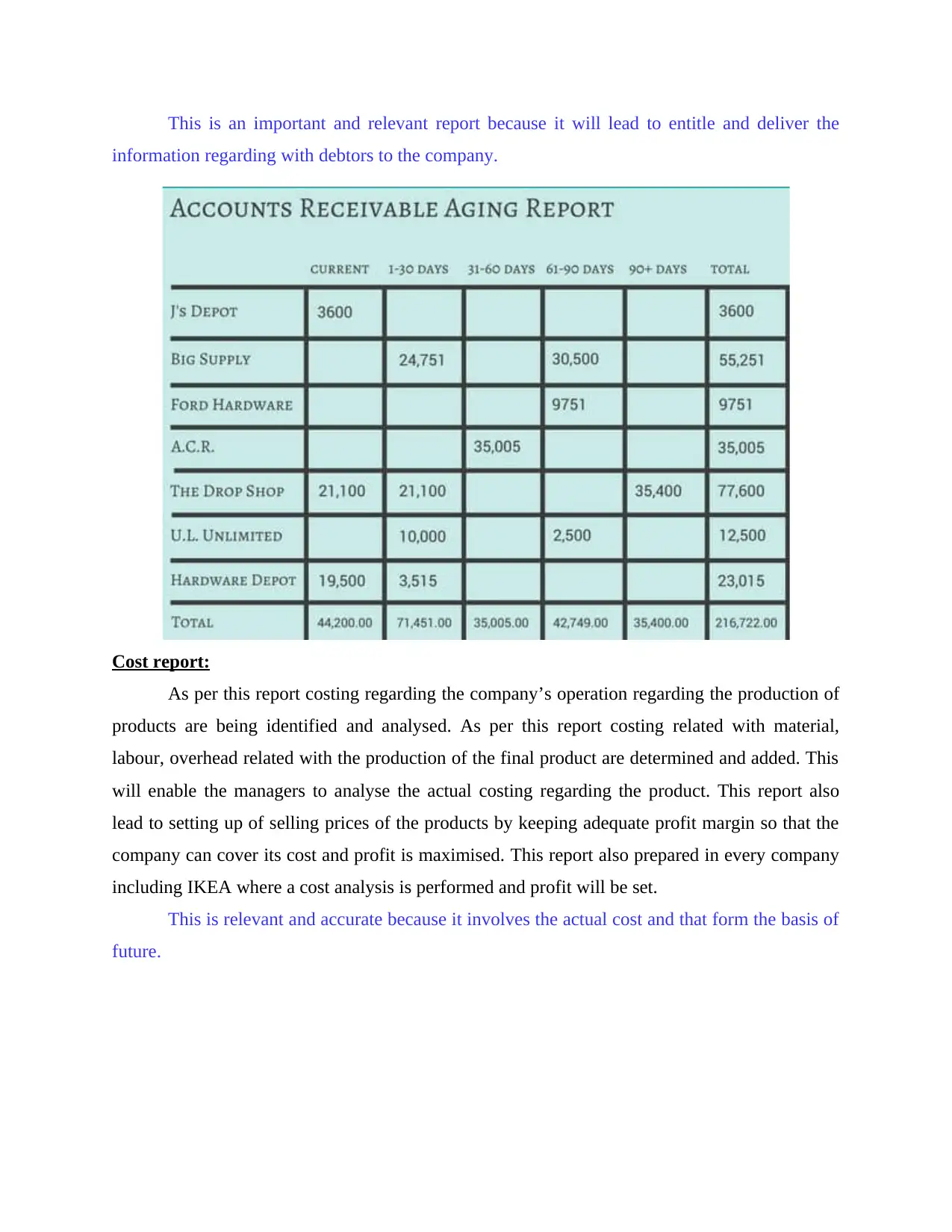

Account receivable report:

This is also an important report form every company including IKEA too. This is because

enabling the services on credit is an important aspect of every business including IKESA too.

This report will identify all those defaulters to whom amount is still not recovered yet. This

report also specify the amount as well as time. As written of bad debt is common in every

business but it is also not a good aspect. Hence, this report ensures the timely receiving of

payment with a strengthening of credit policy regarding the company.

This is also an important report form every company including IKEA too. This is because

enabling the services on credit is an important aspect of every business including IKESA too.

This report will identify all those defaulters to whom amount is still not recovered yet. This

report also specify the amount as well as time. As written of bad debt is common in every

business but it is also not a good aspect. Hence, this report ensures the timely receiving of

payment with a strengthening of credit policy regarding the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is an important and relevant report because it will lead to entitle and deliver the

information regarding with debtors to the company.

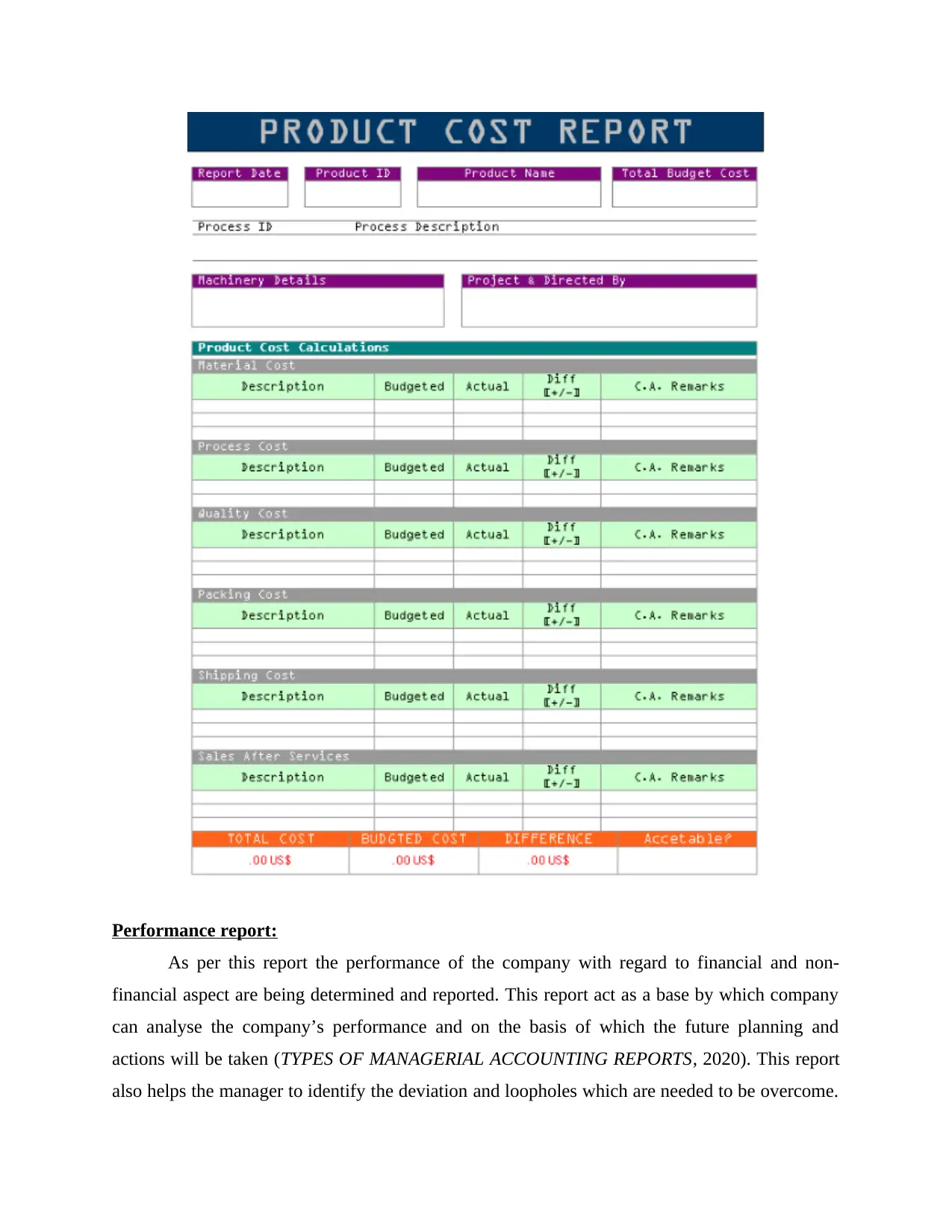

Cost report:

As per this report costing regarding the company’s operation regarding the production of

products are being identified and analysed. As per this report costing related with material,

labour, overhead related with the production of the final product are determined and added. This

will enable the managers to analyse the actual costing regarding the product. This report also

lead to setting up of selling prices of the products by keeping adequate profit margin so that the

company can cover its cost and profit is maximised. This report also prepared in every company

including IKEA where a cost analysis is performed and profit will be set.

This is relevant and accurate because it involves the actual cost and that form the basis of

future.

information regarding with debtors to the company.

Cost report:

As per this report costing regarding the company’s operation regarding the production of

products are being identified and analysed. As per this report costing related with material,

labour, overhead related with the production of the final product are determined and added. This

will enable the managers to analyse the actual costing regarding the product. This report also

lead to setting up of selling prices of the products by keeping adequate profit margin so that the

company can cover its cost and profit is maximised. This report also prepared in every company

including IKEA where a cost analysis is performed and profit will be set.

This is relevant and accurate because it involves the actual cost and that form the basis of

future.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Performance report:

As per this report the performance of the company with regard to financial and non-

financial aspect are being determined and reported. This report act as a base by which company

can analyse the company’s performance and on the basis of which the future planning and

actions will be taken (TYPES OF MANAGERIAL ACCOUNTING REPORTS, 2020). This report

also helps the manager to identify the deviation and loopholes which are needed to be overcome.

As per this report the performance of the company with regard to financial and non-

financial aspect are being determined and reported. This report act as a base by which company

can analyse the company’s performance and on the basis of which the future planning and

actions will be taken (TYPES OF MANAGERIAL ACCOUNTING REPORTS, 2020). This report

also helps the manager to identify the deviation and loopholes which are needed to be overcome.

Preparation of this report at regular interval in IKEA enable the company to have the

determination of future course of action and planning regarding the future activities and business

operations.

This report is accurate and reliable because it is made on the basis of analysis of

company's financial statements and information and as financial statements are the reflection of

company's image so it will lead itself raise its accuracy.

Other managerial report:

Apart from these IKEA also prepare other managerial report including project report,

competitor analysis, information report and various others. And on the basis of the information

regarding reports various decisions are taken by the management of the IKEA that assist it to

perform its operations towards the direction of its objectives. This report including competitor

analysis, information report and various other will lead to have a creation of base that will assist

the organisation to grab and accomplish its goals.

Integration of system and reporting:

An integration of management accounting system and reporting enable the company

including IKEA to have better working of business operation. This can be understood as if the

inventory system will be integrated then it will lead to have full control related with issuing and

dispatching of inventory will take place as it is already being adopted in IKEA too. likewise, an

adoption of management accounting reporting will enable to have better controlling and

monitoring like in case of cost or performance report. These report will enable the IKEA to have

measurement and monitoring of its performance. However, on a critical note it is to be

considered that an execution of these concepts will require a lot of time as well as cost because it

is time consuming as well as costly affair too.

Techniques of cost analysis

Cost:

It refers to the expenses which is being incurred in order to acquire any good or product.

It can also be said that the cost is the financial valuation of resources including material, risk,

time and various other aspects in order to purchase the product (Pope and Mohr, 2017).

Types:

Fixed:

determination of future course of action and planning regarding the future activities and business

operations.

This report is accurate and reliable because it is made on the basis of analysis of

company's financial statements and information and as financial statements are the reflection of

company's image so it will lead itself raise its accuracy.

Other managerial report:

Apart from these IKEA also prepare other managerial report including project report,

competitor analysis, information report and various others. And on the basis of the information

regarding reports various decisions are taken by the management of the IKEA that assist it to

perform its operations towards the direction of its objectives. This report including competitor

analysis, information report and various other will lead to have a creation of base that will assist

the organisation to grab and accomplish its goals.

Integration of system and reporting:

An integration of management accounting system and reporting enable the company

including IKEA to have better working of business operation. This can be understood as if the

inventory system will be integrated then it will lead to have full control related with issuing and

dispatching of inventory will take place as it is already being adopted in IKEA too. likewise, an

adoption of management accounting reporting will enable to have better controlling and

monitoring like in case of cost or performance report. These report will enable the IKEA to have

measurement and monitoring of its performance. However, on a critical note it is to be

considered that an execution of these concepts will require a lot of time as well as cost because it

is time consuming as well as costly affair too.

Techniques of cost analysis

Cost:

It refers to the expenses which is being incurred in order to acquire any good or product.

It can also be said that the cost is the financial valuation of resources including material, risk,

time and various other aspects in order to purchase the product (Pope and Mohr, 2017).

Types:

Fixed:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.