Management Accounting: MAS and Financial Accounting Comparison

VerifiedAdded on 2023/01/19

|18

|5396

|99

AI Summary

This report discusses the comparison between management accounting and financial accounting in terms of legal requirements, types of data used, format, timing, system, and valuation. It also explores different types of management accounting systems such as cost accounting, inventory management, and job costing. The report further evaluates the importance of these systems and their reports in improving business performance. Additionally, it highlights the features of good information and provides an example of calculating the break-even point using absorption costing and marginal costing methods.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................6

TASK 3............................................................................................................................................8

TASK 4..........................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

TASK 2............................................................................................................................................6

TASK 3............................................................................................................................................8

TASK 4..........................................................................................................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

In the business context, the process of accounting that is related with collecting

quantitative financial and business information into separate accounts so that day to day decision

are made is known as management accounting. It is related with gathering, reporting,

formulating of useful business report which enables manager to take valid decision in order to

improve the business performance. By using internal report, internal manager use to identify the

financial performance and profitability of company and make cosine report in order to make

further improvement. To better recognise the importance of MA topic Excite enterprise have

been selected which is located in UK.

In this report, several kind of management accounting system with its main advantages

and reports are discussed. Costing method is also elaborated in this project which help in

preparing annual statements and extract net profit. Apart from this different planning tools with

pros and cons and support in budgetary control is stated. With the support of different system

company is able to resolve the situation of financial problem.

TASK 1

Section A

(a) Assessment between MAS and Financial accounting.

Management accounting: Financial or non-monetary data in corporate reporting is

being used by bookkeepers throughout this type of accounting.

Financial accounting: In this kind of accounting the processing of various financial

reports provided to outside investors so that they can get the financial information about

company within reporting year (Smith, 2015).

Comparison:

Basis Management accounting Financial accounting

Legal

requirement

The preparing of management

accounting documents is not legally

required.

It is a legal requirement in terms of

financial reporting for investors to

formulate financial reports.

Types of data

used

Economic or non-financial information

is used in management reporting.

On the opposite, just financial

information is used to prepare authentic

1

In the business context, the process of accounting that is related with collecting

quantitative financial and business information into separate accounts so that day to day decision

are made is known as management accounting. It is related with gathering, reporting,

formulating of useful business report which enables manager to take valid decision in order to

improve the business performance. By using internal report, internal manager use to identify the

financial performance and profitability of company and make cosine report in order to make

further improvement. To better recognise the importance of MA topic Excite enterprise have

been selected which is located in UK.

In this report, several kind of management accounting system with its main advantages

and reports are discussed. Costing method is also elaborated in this project which help in

preparing annual statements and extract net profit. Apart from this different planning tools with

pros and cons and support in budgetary control is stated. With the support of different system

company is able to resolve the situation of financial problem.

TASK 1

Section A

(a) Assessment between MAS and Financial accounting.

Management accounting: Financial or non-monetary data in corporate reporting is

being used by bookkeepers throughout this type of accounting.

Financial accounting: In this kind of accounting the processing of various financial

reports provided to outside investors so that they can get the financial information about

company within reporting year (Smith, 2015).

Comparison:

Basis Management accounting Financial accounting

Legal

requirement

The preparing of management

accounting documents is not legally

required.

It is a legal requirement in terms of

financial reporting for investors to

formulate financial reports.

Types of data

used

Economic or non-financial information

is used in management reporting.

On the opposite, just financial

information is used to prepare authentic

1

report.

Format of

presentation

The MA documents are not delivered in

any specific format.

Accountant must file financial

statements by considering IFRS

regulated particular format.

Timing In this accounting reports are frequently

issued as manager needs specific

information on each aspect of business

to make proper decision.

This accounting requires financial

statements to be published as the end of

accounting year to determine overall

financial strength.

System In management accounting manager use

to look into the every system of

different operation so that ways can be

made to improve the overall profit of

company.

Manager under financial accounting

consider the system that company used

for making profit.

Valuation This method consider the value of items

that only increase the productivity of

company.

It includes different impairments in

order to address the proper valuation of

assets and liabilities.

Various types of MAS:

(b) Cost accounting system:

This accounting system is associated with the cost forecasting method for different tasks

and procedures within company. Cost system primarily helps to control and decrease

expenditures of companies. Therefore, businesses are primarily expected to distribute the

monetary resources for company according to the projected costs of the various activities

(O’Grady, Morlidge and Rouse, 2016). This system mainly includes various types of costing

like direct, standard costing, etc. Standard expenses involve the absorption costing structure

where both kinds of expenses are assumed to be unit costs.

Whereas, direct costs consider marginal costs in which only the variable costs are considered as

manufacturing costs. This system assists businesses to maintain efficient spending control.

Excite limited is using that accounting system for the purpose of controlling the expenses of

operations in the context of entertainment services For example, absorption costs are valuable in

2

Format of

presentation

The MA documents are not delivered in

any specific format.

Accountant must file financial

statements by considering IFRS

regulated particular format.

Timing In this accounting reports are frequently

issued as manager needs specific

information on each aspect of business

to make proper decision.

This accounting requires financial

statements to be published as the end of

accounting year to determine overall

financial strength.

System In management accounting manager use

to look into the every system of

different operation so that ways can be

made to improve the overall profit of

company.

Manager under financial accounting

consider the system that company used

for making profit.

Valuation This method consider the value of items

that only increase the productivity of

company.

It includes different impairments in

order to address the proper valuation of

assets and liabilities.

Various types of MAS:

(b) Cost accounting system:

This accounting system is associated with the cost forecasting method for different tasks

and procedures within company. Cost system primarily helps to control and decrease

expenditures of companies. Therefore, businesses are primarily expected to distribute the

monetary resources for company according to the projected costs of the various activities

(O’Grady, Morlidge and Rouse, 2016). This system mainly includes various types of costing

like direct, standard costing, etc. Standard expenses involve the absorption costing structure

where both kinds of expenses are assumed to be unit costs.

Whereas, direct costs consider marginal costs in which only the variable costs are considered as

manufacturing costs. This system assists businesses to maintain efficient spending control.

Excite limited is using that accounting system for the purpose of controlling the expenses of

operations in the context of entertainment services For example, absorption costs are valuable in

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

effectively measuring benefit and marginal costs support to control manufacturing costs. There

are different cost related with Excite company such as;

Direct cost: These kind of cost are directly noticeable to the overall cost of the specific

product or services produced by company. Direct cost fluctuate with the level of output but are

the same for each single unit of production, thus must be control and managed by manager of

Excite Ltd.

Standard cost: This method is related with substituting an estimation cost equitable to

actual cost within accounting records, so that differences can be determined between the actual

and expected figures. Manager use to create estimated cost related to different activities in Excite

limited which support to make better decision in future.

(c) Inventory management system:

This accounting system primarily incorporates two practices that track and manage

manufactured inventory in storage. The inventory deposited could be assets of businesses, raw

materials and finished products, etc. Manufacturing divisions need to do that specifically in

businesses to make a smart decision related to output level. Different solutions such as a

perpetual inventory systems, continuous inventory systems and periodic stock systems are part

of this process. Just in time technique means reducing production time and decreased costs. The

permanent inventory plan also monitors the product balance present in factories. The periodic

inventory process results from reviewing the number of items a company holds at the start of

reporting year. This accounting system applies by the management respective firm to keep an

authentic record about inventories, such as LEDs, music system and many more so that decision

can be made regarding setting of price. Furthermore, company also apply the ABC inventory

system such as entertainment booking from customer which are nearest to the date are consider

into A category, booking that are needed to be delivered afterwards are kept in to B category and

in C category booking addressed after some months are recorded.

(d) Job costing system –

This form of accounting method is that which is connected by each task allocated to

different tasks to define expense and profit. This accounting is primarily used in businesses

where the product range is broader. That's because the manufacturing manager could be aware

about each cost for all produced item separately by using this accounting system (Sithole,

Chandler, Abeysekera and Paas, 2017). In principle, it enables executives to calculate profits in a

3

are different cost related with Excite company such as;

Direct cost: These kind of cost are directly noticeable to the overall cost of the specific

product or services produced by company. Direct cost fluctuate with the level of output but are

the same for each single unit of production, thus must be control and managed by manager of

Excite Ltd.

Standard cost: This method is related with substituting an estimation cost equitable to

actual cost within accounting records, so that differences can be determined between the actual

and expected figures. Manager use to create estimated cost related to different activities in Excite

limited which support to make better decision in future.

(c) Inventory management system:

This accounting system primarily incorporates two practices that track and manage

manufactured inventory in storage. The inventory deposited could be assets of businesses, raw

materials and finished products, etc. Manufacturing divisions need to do that specifically in

businesses to make a smart decision related to output level. Different solutions such as a

perpetual inventory systems, continuous inventory systems and periodic stock systems are part

of this process. Just in time technique means reducing production time and decreased costs. The

permanent inventory plan also monitors the product balance present in factories. The periodic

inventory process results from reviewing the number of items a company holds at the start of

reporting year. This accounting system applies by the management respective firm to keep an

authentic record about inventories, such as LEDs, music system and many more so that decision

can be made regarding setting of price. Furthermore, company also apply the ABC inventory

system such as entertainment booking from customer which are nearest to the date are consider

into A category, booking that are needed to be delivered afterwards are kept in to B category and

in C category booking addressed after some months are recorded.

(d) Job costing system –

This form of accounting method is that which is connected by each task allocated to

different tasks to define expense and profit. This accounting is primarily used in businesses

where the product range is broader. That's because the manufacturing manager could be aware

about each cost for all produced item separately by using this accounting system (Sithole,

Chandler, Abeysekera and Paas, 2017). In principle, it enables executives to calculate profits in a

3

certain job, which they allocate in separate business operations. The major benefit of

job accounting system in the Excite Company to know all the work costs associated with various

activities. For example Excite limited organise specific event for promoting business proposal of

newly developed company, thus with the support of this system manager keep the entire record

total employee engage in this activity so that total cost spend on each job can be ascertained and

proper future steps are made to reduce if cost are higher.

(e) Evaluation of MAS and management accounting reports.

In the company, various kinds of MAS and reports are used to make different activities

best and productive. As mentioned above, cost accounting system is associated to Excite's

financial department which help to lower the costs of various events. As well as inventory

control process, aid in managing inventory properly in warehouses (Brown and Dillard, 2015).

For instance, they handle their transactions and suppliers of equipment with this accounting

system which enables to increase sales of different services. In fact, different MA reports like

cost reports that provide specific information regarding the current cost relevant with business

activities. Along with certain other documents, such as the report on the aging of receivables or

the report on performance are connected with different duties of business entity. Therefore, MA

documents and MAS can be claimed to be related to the system of organization.

Benefits of above mentioned MAS:

Importance of cost accounting system: For corporations, it's useful to reduce the costs

from various types of operation. In the business mentioned Excite Company uses this

system to reduce their operating costs. Furthermore, multiple costing schemes, such as

the standard costing model, aid in the identification of real differences between total

expenditure.

Importance of inventory management system: This allows businesses to better

maintain processed materials like raw materials, finished products etc. above-

mentioned business use this accounting system, helps them to reduce storage costs and to

maintain their facilities.

Importance of job costing system: This system is related to the system of recording any

work costs. In the case of Excite company, with the support of this system gives them

with data about total costs incurred on different job engaged in different task.

Section B

4

job accounting system in the Excite Company to know all the work costs associated with various

activities. For example Excite limited organise specific event for promoting business proposal of

newly developed company, thus with the support of this system manager keep the entire record

total employee engage in this activity so that total cost spend on each job can be ascertained and

proper future steps are made to reduce if cost are higher.

(e) Evaluation of MAS and management accounting reports.

In the company, various kinds of MAS and reports are used to make different activities

best and productive. As mentioned above, cost accounting system is associated to Excite's

financial department which help to lower the costs of various events. As well as inventory

control process, aid in managing inventory properly in warehouses (Brown and Dillard, 2015).

For instance, they handle their transactions and suppliers of equipment with this accounting

system which enables to increase sales of different services. In fact, different MA reports like

cost reports that provide specific information regarding the current cost relevant with business

activities. Along with certain other documents, such as the report on the aging of receivables or

the report on performance are connected with different duties of business entity. Therefore, MA

documents and MAS can be claimed to be related to the system of organization.

Benefits of above mentioned MAS:

Importance of cost accounting system: For corporations, it's useful to reduce the costs

from various types of operation. In the business mentioned Excite Company uses this

system to reduce their operating costs. Furthermore, multiple costing schemes, such as

the standard costing model, aid in the identification of real differences between total

expenditure.

Importance of inventory management system: This allows businesses to better

maintain processed materials like raw materials, finished products etc. above-

mentioned business use this accounting system, helps them to reduce storage costs and to

maintain their facilities.

Importance of job costing system: This system is related to the system of recording any

work costs. In the case of Excite company, with the support of this system gives them

with data about total costs incurred on different job engaged in different task.

Section B

4

(a) Various kinds of managerial reports

Management accounting reports - MA reports could be described as documents compelled

according to information gathered from multiple accounting systems. Specific information

regarding financial and non-financial issues is provided in all of these reports. Here are certain

Management accounting reports that are as follows:

Cost accounting reports: The cost report could be described as a sort of document

providing comprehensive information about expense of different activities and

operations• It allows businesses to track certain activities involving higher costs. The

Excite Company produces this document with the help of accountants that allows their

management to assess the annual cost and to target on activities that lead to higher

expenditures. (Burritt and Christ, 2017).

Inventory report: It is an inventory management system-based report. Evidence about

quantity stored in storage facilities is provided in this report. The stock document is

important to businesses as the manufacturing team focuses on the development of new

goods, according to the data provided in that report. Excite entertainment allowed its

auditor to produce this document which enables them to properly manage its products

and provide details regarding the current amount of stock to be purchased to deliver

different services.

Account receivable ageing report: It can be classified as a type of report that

gives details about the total debt level outstanding from borrowers of company. It is

convenient to businesses, as it requires the deadline on which the parties have made an

agreement to make payments. As a result, businesses will work on debtors who have not

make payment even after the deadline has been crossed. The report aims to finance

bodies of company by reminding them about how much debtors owe and gives the name

of debtors whose payment is outstanding. As in the context of Excite limited it is

observed that accountants generate this document to obtain customers data so that

correct amount can be collected.

Budget report: This is a sort of document generated on the framework of different types

of budgets. Details on forecast income and expenditure as well as on final results are also

considering budget report. This document is useful for administrators since it support

to take future decisions by using details regarding the current differences among actual

5

Management accounting reports - MA reports could be described as documents compelled

according to information gathered from multiple accounting systems. Specific information

regarding financial and non-financial issues is provided in all of these reports. Here are certain

Management accounting reports that are as follows:

Cost accounting reports: The cost report could be described as a sort of document

providing comprehensive information about expense of different activities and

operations• It allows businesses to track certain activities involving higher costs. The

Excite Company produces this document with the help of accountants that allows their

management to assess the annual cost and to target on activities that lead to higher

expenditures. (Burritt and Christ, 2017).

Inventory report: It is an inventory management system-based report. Evidence about

quantity stored in storage facilities is provided in this report. The stock document is

important to businesses as the manufacturing team focuses on the development of new

goods, according to the data provided in that report. Excite entertainment allowed its

auditor to produce this document which enables them to properly manage its products

and provide details regarding the current amount of stock to be purchased to deliver

different services.

Account receivable ageing report: It can be classified as a type of report that

gives details about the total debt level outstanding from borrowers of company. It is

convenient to businesses, as it requires the deadline on which the parties have made an

agreement to make payments. As a result, businesses will work on debtors who have not

make payment even after the deadline has been crossed. The report aims to finance

bodies of company by reminding them about how much debtors owe and gives the name

of debtors whose payment is outstanding. As in the context of Excite limited it is

observed that accountants generate this document to obtain customers data so that

correct amount can be collected.

Budget report: This is a sort of document generated on the framework of different types

of budgets. Details on forecast income and expenditure as well as on final results are also

considering budget report. This document is useful for administrators since it support

to take future decisions by using details regarding the current differences among actual

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and estimated results. As with the above Excite entertainment limited manager uses this

study to review evidence on measuring variances from current and expected results,

according to this report plans and policies, manager take more calculated steps while

developing new services and good by making sure that expenses are not higher than

expected income.

Performance report: This report is basically developed by manager of companies to

examine the overall performance of various departments and employees working on

allotted job (Laing and Perrin, 2018). The report includes details on the results generated

by different activities and procedures. The performance report is primarily beneficial for

executives when they make strategic decisions about future of organizations so that any

gap or problem can be removed and performance can be grown. The Excite

Entertainment Limited company auditor publishes the report, which provides a key

decision-making process for staff and activities. In addition, individual employees are

granted for superior performance.

(b) Features of good information.

It is essential that information collected must be good and detailed so that decision are

made easily. Some of the main features of good information are discussed below:

Accuracy: Accounting reliability and accuracy is a key element since organizations fail

to take the necessary actions when financial information is not reliable. It is therefore a

key feature of good information.

Relevancy: The relevance of good information determines the accounting information

must be according different business operations and events. This is critical because

businesses can develop better approaches due to the importance of accounting data. That

will defiantly reduce the chances of error and every plan work resulting to generate more

and more revenue.

Reliable and up to date: It's another feature of useful information which means that

reporting data should contain accuracy and must be up-to-date. Organizations should

retain accurate financial records so that critical organizational decisions can be made to

improve overall performance.

6

study to review evidence on measuring variances from current and expected results,

according to this report plans and policies, manager take more calculated steps while

developing new services and good by making sure that expenses are not higher than

expected income.

Performance report: This report is basically developed by manager of companies to

examine the overall performance of various departments and employees working on

allotted job (Laing and Perrin, 2018). The report includes details on the results generated

by different activities and procedures. The performance report is primarily beneficial for

executives when they make strategic decisions about future of organizations so that any

gap or problem can be removed and performance can be grown. The Excite

Entertainment Limited company auditor publishes the report, which provides a key

decision-making process for staff and activities. In addition, individual employees are

granted for superior performance.

(b) Features of good information.

It is essential that information collected must be good and detailed so that decision are

made easily. Some of the main features of good information are discussed below:

Accuracy: Accounting reliability and accuracy is a key element since organizations fail

to take the necessary actions when financial information is not reliable. It is therefore a

key feature of good information.

Relevancy: The relevance of good information determines the accounting information

must be according different business operations and events. This is critical because

businesses can develop better approaches due to the importance of accounting data. That

will defiantly reduce the chances of error and every plan work resulting to generate more

and more revenue.

Reliable and up to date: It's another feature of useful information which means that

reporting data should contain accuracy and must be up-to-date. Organizations should

retain accurate financial records so that critical organizational decisions can be made to

improve overall performance.

6

Timely presentation of information: In order to allow companies to make

valuable decisions on time, the accounting data must be provided in actual time and

date (Meidell & Kaarbøe, 2017).

TASK 2

Section (A)

The two measure accounting methods are discussed below that help to prepare income

statement to calculate net profit:

Absorption costing method: This could be described as a type of approach where the

value product is calculated by considering fixed and variable cost. Marginal costing method: It is a form of costing approach although in which fixed costs

are viewed as period costs and overhead costs are viewed as product costs.

Contribution = Selling price per unit – Variable cost per unit

Selling price per unit £40

Less: variable cost per unit £10

Contribution per unit £30

Break-even point = Fixed cost / contribution per unit

Fixed cost = £120000

Contribution per unit = 30

So, BEP = 120000 / 30

= 4000 tickets.

Section (B)

There are some main factors that bring changes in the above computed figures such as:

Selling price: The overall selling price modify from £ 40 to upper value which directly impact

contribution to get increased and further modify the BEP point.

Variable cost: Due to the changes in the figure of variable cost the total result from break even

points also gets changed.

Section (C)

BEP to attain desired profit = Fixed cost + desired profit / Contribution per unit

= 120000 + 60000 / 30

= 6000 tickets

Profit at sales of 4000 tickets

7

valuable decisions on time, the accounting data must be provided in actual time and

date (Meidell & Kaarbøe, 2017).

TASK 2

Section (A)

The two measure accounting methods are discussed below that help to prepare income

statement to calculate net profit:

Absorption costing method: This could be described as a type of approach where the

value product is calculated by considering fixed and variable cost. Marginal costing method: It is a form of costing approach although in which fixed costs

are viewed as period costs and overhead costs are viewed as product costs.

Contribution = Selling price per unit – Variable cost per unit

Selling price per unit £40

Less: variable cost per unit £10

Contribution per unit £30

Break-even point = Fixed cost / contribution per unit

Fixed cost = £120000

Contribution per unit = 30

So, BEP = 120000 / 30

= 4000 tickets.

Section (B)

There are some main factors that bring changes in the above computed figures such as:

Selling price: The overall selling price modify from £ 40 to upper value which directly impact

contribution to get increased and further modify the BEP point.

Variable cost: Due to the changes in the figure of variable cost the total result from break even

points also gets changed.

Section (C)

BEP to attain desired profit = Fixed cost + desired profit / Contribution per unit

= 120000 + 60000 / 30

= 6000 tickets

Profit at sales of 4000 tickets

7

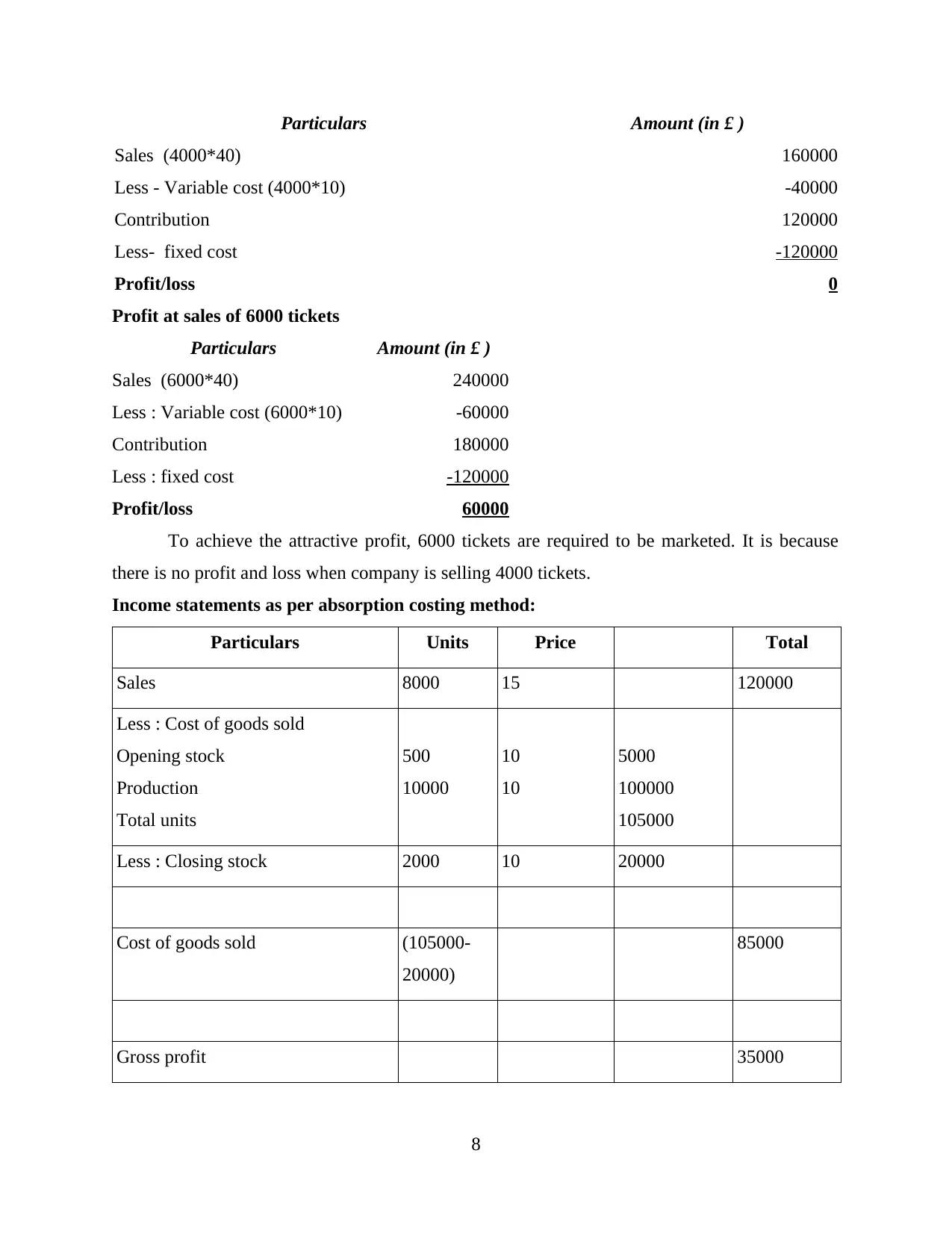

Particulars Amount (in £ )

Sales (4000*40) 160000

Less - Variable cost (4000*10) -40000

Contribution 120000

Less- fixed cost -120000

Profit/loss 0

Profit at sales of 6000 tickets

Particulars Amount (in £ )

Sales (6000*40) 240000

Less : Variable cost (6000*10) -60000

Contribution 180000

Less : fixed cost -120000

Profit/loss 60000

To achieve the attractive profit, 6000 tickets are required to be marketed. It is because

there is no profit and loss when company is selling 4000 tickets.

Income statements as per absorption costing method:

Particulars Units Price Total

Sales 8000 15 120000

Less : Cost of goods sold

Opening stock

Production

Total units

500

10000

10

10

5000

100000

105000

Less : Closing stock 2000 10 20000

Cost of goods sold (105000-

20000)

85000

Gross profit 35000

8

Sales (4000*40) 160000

Less - Variable cost (4000*10) -40000

Contribution 120000

Less- fixed cost -120000

Profit/loss 0

Profit at sales of 6000 tickets

Particulars Amount (in £ )

Sales (6000*40) 240000

Less : Variable cost (6000*10) -60000

Contribution 180000

Less : fixed cost -120000

Profit/loss 60000

To achieve the attractive profit, 6000 tickets are required to be marketed. It is because

there is no profit and loss when company is selling 4000 tickets.

Income statements as per absorption costing method:

Particulars Units Price Total

Sales 8000 15 120000

Less : Cost of goods sold

Opening stock

Production

Total units

500

10000

10

10

5000

100000

105000

Less : Closing stock 2000 10 20000

Cost of goods sold (105000-

20000)

85000

Gross profit 35000

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

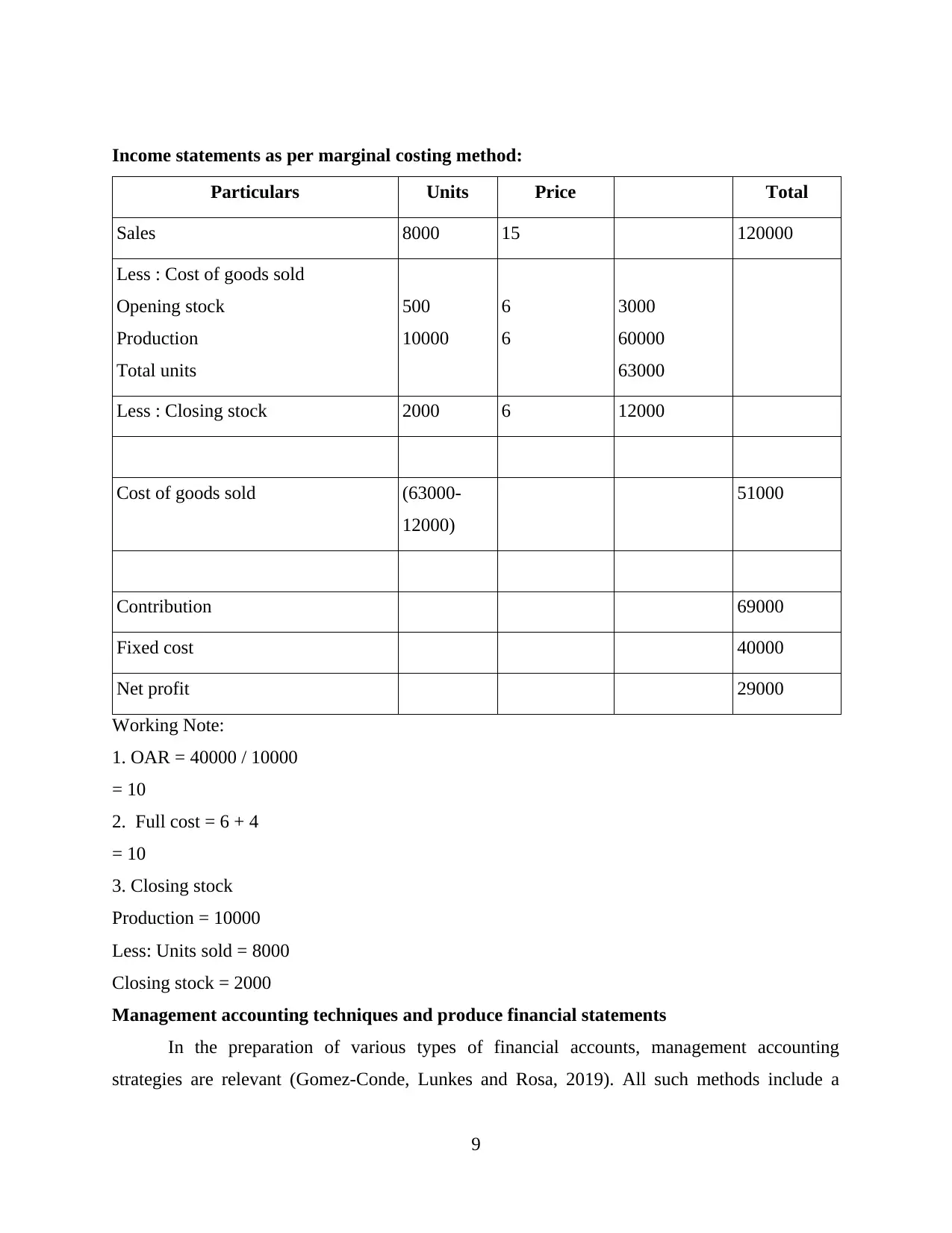

Income statements as per marginal costing method:

Particulars Units Price Total

Sales 8000 15 120000

Less : Cost of goods sold

Opening stock

Production

Total units

500

10000

6

6

3000

60000

63000

Less : Closing stock 2000 6 12000

Cost of goods sold (63000-

12000)

51000

Contribution 69000

Fixed cost 40000

Net profit 29000

Working Note:

1. OAR = 40000 / 10000

= 10

2. Full cost = 6 + 4

= 10

3. Closing stock

Production = 10000

Less: Units sold = 8000

Closing stock = 2000

Management accounting techniques and produce financial statements

In the preparation of various types of financial accounts, management accounting

strategies are relevant (Gomez-Conde, Lunkes and Rosa, 2019). All such methods include a

9

Particulars Units Price Total

Sales 8000 15 120000

Less : Cost of goods sold

Opening stock

Production

Total units

500

10000

6

6

3000

60000

63000

Less : Closing stock 2000 6 12000

Cost of goods sold (63000-

12000)

51000

Contribution 69000

Fixed cost 40000

Net profit 29000

Working Note:

1. OAR = 40000 / 10000

= 10

2. Full cost = 6 + 4

= 10

3. Closing stock

Production = 10000

Less: Units sold = 8000

Closing stock = 2000

Management accounting techniques and produce financial statements

In the preparation of various types of financial accounts, management accounting

strategies are relevant (Gomez-Conde, Lunkes and Rosa, 2019). All such methods include a

9

specific structure for the preparation of financial statements. Like in Excite entertainment limited

company different types of MA methods are used to obtain financial statements,

like marginal and absorption costing schemes. It demonstrates that management reporting

methods for managing the internal managerial reports are beneficial so that annual reports can be

prepared by accountant easily.

TASK 3

Advantages and disadvantages of different types of planning tools used for budgetary

control.

Budget – This could be described as a future revenue and expenditure estimate. Budgets

could be compelled according to requirements for a shorter and longer period of time for a

company. These are important for businesses, since money and resources need not be efficiently

distributed without them. There are various types of budgets planned by the managers to

consider industry and company dynamics, some of these are listed below:

Zero based budget: This is among the most effective and popular budgeting strategies in

companies nowadays which support in for forecasting preferences and alternatives. The ZBB

process begins from zero, as it does not take anything into account from last year's investment or

any operation and therefore all expenditure is valid in the budget. The excite company include

this budget in order to set the expenditure limits on different activities, as manager use to analyse

the market condition and estimate the expenses required to develop required services. This also

support in determining the total revenue that can be generated by firm by delivering the most

possible entertainment services. The benefits and disadvantages of ZBB are discussed below:

Advantages:

It makes for an accurate allocation of funds (departmental), since it does not take historic

figures into account in order to figure out actual numbers.

By eliminating non-productive or routine tasks that support manager of excite limited

company in exploration of new and more cost-effective ways of working which

encouraged to reach the desired exciting outcomes in specific year.

Disadvantages:

This is a moment where administrators need to produce new projections of revenue and

expenses single time.

10

company different types of MA methods are used to obtain financial statements,

like marginal and absorption costing schemes. It demonstrates that management reporting

methods for managing the internal managerial reports are beneficial so that annual reports can be

prepared by accountant easily.

TASK 3

Advantages and disadvantages of different types of planning tools used for budgetary

control.

Budget – This could be described as a future revenue and expenditure estimate. Budgets

could be compelled according to requirements for a shorter and longer period of time for a

company. These are important for businesses, since money and resources need not be efficiently

distributed without them. There are various types of budgets planned by the managers to

consider industry and company dynamics, some of these are listed below:

Zero based budget: This is among the most effective and popular budgeting strategies in

companies nowadays which support in for forecasting preferences and alternatives. The ZBB

process begins from zero, as it does not take anything into account from last year's investment or

any operation and therefore all expenditure is valid in the budget. The excite company include

this budget in order to set the expenditure limits on different activities, as manager use to analyse

the market condition and estimate the expenses required to develop required services. This also

support in determining the total revenue that can be generated by firm by delivering the most

possible entertainment services. The benefits and disadvantages of ZBB are discussed below:

Advantages:

It makes for an accurate allocation of funds (departmental), since it does not take historic

figures into account in order to figure out actual numbers.

By eliminating non-productive or routine tasks that support manager of excite limited

company in exploration of new and more cost-effective ways of working which

encouraged to reach the desired exciting outcomes in specific year.

Disadvantages:

This is a moment where administrators need to produce new projections of revenue and

expenses single time.

10

To engage Professional managers are really a challenging and expensive task for the

business, in order to describe every line item or price.

Program budget: A program schedule or budget is a mechanism whereby the company

allocates the resources to various departments, programs, operations and manages the flow of

money of the company (Saeidi., Othman, Saeidi and Saeidi, 2018). Every budgetary format

contains certain specific project-related costs and profits associated with several other project

profits and costs. In excite company manager use this budget to make proper estimation about

expenses required to run different entertainment services and predict the revenue generated from

these program. The below are some advantages and disadvantages:

Advantages:

This plan lets director to determine the company's main task and program to provide

enough resources in order to achieve the predetermined goals.

This plan in Excite Limited helps find the sustainable business regions which needed

more money for increasing overall productivity.

Disadvantages:

If the budget for a particular system does not work properly, the total cost of the company

would certainly increase. This proposal takes time because extensive information is required to identify the actual

need for the resources to operate different activities in respective company.

Incremental budget- This budget is an important component in management accounts

and relies on the premise that just a little adjustment is made in the current budget to make

produce new budgets. This method of cumulative budgeting starts depending on the

assumption that the costs of the past year are treated at the starting point of the current year. In

excite limited manager make better use of incremental budget for example to increase sales they

consider last year sales budget and make some possible adjustment which could lead to increase

on revenue in current year. The following list of advantages and disadvantages:

Advantages:

This budgeting method is quite easy to accomplish and thus no difficult measurements

are needed. It can be done easily in multiple departments, because there is no need for

comprehensive analysis that benefit to reduce costs and time.

11

business, in order to describe every line item or price.

Program budget: A program schedule or budget is a mechanism whereby the company

allocates the resources to various departments, programs, operations and manages the flow of

money of the company (Saeidi., Othman, Saeidi and Saeidi, 2018). Every budgetary format

contains certain specific project-related costs and profits associated with several other project

profits and costs. In excite company manager use this budget to make proper estimation about

expenses required to run different entertainment services and predict the revenue generated from

these program. The below are some advantages and disadvantages:

Advantages:

This plan lets director to determine the company's main task and program to provide

enough resources in order to achieve the predetermined goals.

This plan in Excite Limited helps find the sustainable business regions which needed

more money for increasing overall productivity.

Disadvantages:

If the budget for a particular system does not work properly, the total cost of the company

would certainly increase. This proposal takes time because extensive information is required to identify the actual

need for the resources to operate different activities in respective company.

Incremental budget- This budget is an important component in management accounts

and relies on the premise that just a little adjustment is made in the current budget to make

produce new budgets. This method of cumulative budgeting starts depending on the

assumption that the costs of the past year are treated at the starting point of the current year. In

excite limited manager make better use of incremental budget for example to increase sales they

consider last year sales budget and make some possible adjustment which could lead to increase

on revenue in current year. The following list of advantages and disadvantages:

Advantages:

This budgeting method is quite easy to accomplish and thus no difficult measurements

are needed. It can be done easily in multiple departments, because there is no need for

comprehensive analysis that benefit to reduce costs and time.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This budget has reduced competition and the increase of value through a year-by-year

reliable budget for Excite Company.

Disadvantages:

This tactic can actually increase the overall spending of Director as the have to

continuously check the previous budget in order to predict about future.

This budgeting method requires more and more time as improper prediction just on

relying on past figures can lead to wrong decision.

Use of planning tools for preparing and forecasting of budgets:

In order to create and forecast best and authentic budgets for company, require different

forms of financial plans such as ZBB, the Program and incremental budgets (Hemmer and Labro,

2017). It's compulsory to included possible financial data in these planning instruments that act

as a legal structure for the preparation of yearly budgets as shown in the respective business,

different kinds of forecasting methods are being used to manage budgets like ZBB, program

budgets. For example incremental budget is beneficial in deciding in advance about the purchase

expenses that is required to meet the future customer demand. It is also supportive to ascertain

the income level that can be generated through these services.

Planning tools to solve financial issues:

Budgetary management planning methods comprise of a critical set of financial

transaction data in company’s process. All different planning tools are beneficial to reduce and

solve the chances of financial problem arising within company process. Such with the support of

zero base budgeting company can resolve the chances of unwanted expenses. On the other side

program budget is helpful in reducing the contingencies related with different operation of excite

company so that productivity can be increased. By using incremental budget manager are able to

resolve the issue of more expenses on those activities that does not providing the better revenue

for company.

TASK 4

Management accounting systems to respond to financial problems.

Financial Governance: Financial governance can be described as an overall process

which includes collection of financial data, management of operations and activities, monitoring

of the performance and control over the data, operations and efforts of the company. Financial

governance provide assistance in resolving financial problems by having internal control,

12

reliable budget for Excite Company.

Disadvantages:

This tactic can actually increase the overall spending of Director as the have to

continuously check the previous budget in order to predict about future.

This budgeting method requires more and more time as improper prediction just on

relying on past figures can lead to wrong decision.

Use of planning tools for preparing and forecasting of budgets:

In order to create and forecast best and authentic budgets for company, require different

forms of financial plans such as ZBB, the Program and incremental budgets (Hemmer and Labro,

2017). It's compulsory to included possible financial data in these planning instruments that act

as a legal structure for the preparation of yearly budgets as shown in the respective business,

different kinds of forecasting methods are being used to manage budgets like ZBB, program

budgets. For example incremental budget is beneficial in deciding in advance about the purchase

expenses that is required to meet the future customer demand. It is also supportive to ascertain

the income level that can be generated through these services.

Planning tools to solve financial issues:

Budgetary management planning methods comprise of a critical set of financial

transaction data in company’s process. All different planning tools are beneficial to reduce and

solve the chances of financial problem arising within company process. Such with the support of

zero base budgeting company can resolve the chances of unwanted expenses. On the other side

program budget is helpful in reducing the contingencies related with different operation of excite

company so that productivity can be increased. By using incremental budget manager are able to

resolve the issue of more expenses on those activities that does not providing the better revenue

for company.

TASK 4

Management accounting systems to respond to financial problems.

Financial Governance: Financial governance can be described as an overall process

which includes collection of financial data, management of operations and activities, monitoring

of the performance and control over the data, operations and efforts of the company. Financial

governance provide assistance in resolving financial problems by having internal control,

12

creating financial policies, conduction internal and external audit, manage work flow, track data

and manage data security. In context with the selected organization, financial governance helps

in solving major financial problems such as late payments from the customers and weak fund

management system. Financial governance helps the management in assessing the effectiveness

of credit terms and policies executing by the company and also suggest solutions to strengthen

the policies if required. This governance system also supports internal audits within the

establishment so that loop holes in the accounting system can be detected and an effective

financial accounting system can be implemented.

Full Compliance Management System: A compliance management system or CMS is a

program or framework that has been designed to keep an organization aware and utilise fair

lending regulations within the organization and be on the right side. Organizations nowadays are

working into a dynamic economic environment which is influence by emerging technology,

financial services and globalized market and industry. In order to remain profitable, financial

institutions have to modify business offerings and manage the compliance with the new

legislations and standards at the same time. A fully compliance management system helps the

managers in implementation of adequate standards, policies and provisions which helps in

identifying and solving various financial problems. Benefits of full compliance are given below:

Full compliance of management system helps in maintaining business procedures

workflow and minimize the risk. It allows restricted or selective access of confidential

data to the employees to ensure that they will receive authenticated information only.

Compliance management also assists to reduce legal conflicts and avoid future costs. It

encourage the administration to practice good data security and avoid a breach altogether

so that establishment do not have to face any legal consequences and long-term losses.

A fully compliance system helps in communicating the task among the employees and

entire organization, track controls and inside standard processes and create strong

customer base.

The management should develop a full compliance management system to avoid the

following consequences:

Non-compliance with certain regulatory laws can impose criminal charges on the board

members or directors.

13

and manage data security. In context with the selected organization, financial governance helps

in solving major financial problems such as late payments from the customers and weak fund

management system. Financial governance helps the management in assessing the effectiveness

of credit terms and policies executing by the company and also suggest solutions to strengthen

the policies if required. This governance system also supports internal audits within the

establishment so that loop holes in the accounting system can be detected and an effective

financial accounting system can be implemented.

Full Compliance Management System: A compliance management system or CMS is a

program or framework that has been designed to keep an organization aware and utilise fair

lending regulations within the organization and be on the right side. Organizations nowadays are

working into a dynamic economic environment which is influence by emerging technology,

financial services and globalized market and industry. In order to remain profitable, financial

institutions have to modify business offerings and manage the compliance with the new

legislations and standards at the same time. A fully compliance management system helps the

managers in implementation of adequate standards, policies and provisions which helps in

identifying and solving various financial problems. Benefits of full compliance are given below:

Full compliance of management system helps in maintaining business procedures

workflow and minimize the risk. It allows restricted or selective access of confidential

data to the employees to ensure that they will receive authenticated information only.

Compliance management also assists to reduce legal conflicts and avoid future costs. It

encourage the administration to practice good data security and avoid a breach altogether

so that establishment do not have to face any legal consequences and long-term losses.

A fully compliance system helps in communicating the task among the employees and

entire organization, track controls and inside standard processes and create strong

customer base.

The management should develop a full compliance management system to avoid the

following consequences:

Non-compliance with certain regulatory laws can impose criminal charges on the board

members or directors.

13

A regular non-compliance can damage the brand image, goodwill and reputation of the

organization. Customer can loose their trust from the establishment.

Non-compliance with the laws and standards can cause a loss of lucrative opportunities

and other corporal owners can deny to derive business from the organization.

Monitoring System: The respective organization utilize financial governance system to

monitor and control the operations and find out the variances or deviations of actual outputs from

targeted goals. An effective compliance with financial governance system helps the management

in setting measurements for achievement of objectives and provide regular check of the

efficiency of activities and people. This helps in performance appraisal and detect deviations.

After identifying variations it helps in implementing standards and guidelines that are must to

control the deviations and make corrections in the procedures and structures.

MAS to solve financial issues:

In an organisation the use of different system is beneficial to reduce the financial problem

that can hinder the overall performance. In the context of above selected company there have

been different financial problem that reduces the functioning of operation and lead to decrease

the complete productivity and performance. It is observed that with the support of cost

accounting system are able to reduce the issue of more spending than earning and making

resources engage in those activities that results better profit. Similarly with the aid of inventory

management system manager of excite limited are able to reduce the cost incurred on managing

extra raw material. As they start giving the order on the specific date to meet the production

requirement without storing in warehouse for long period.

PART B

Calculations:

BEP to attain desired profit = Fixed cost + desired profit / contribution per unit

= 120000+90000

= 210000/30

= 7000 units

Profit of sale of 7000 units

Sales (7000*40) = 280000

- Variable cost = 70000

14

organization. Customer can loose their trust from the establishment.

Non-compliance with the laws and standards can cause a loss of lucrative opportunities

and other corporal owners can deny to derive business from the organization.

Monitoring System: The respective organization utilize financial governance system to

monitor and control the operations and find out the variances or deviations of actual outputs from

targeted goals. An effective compliance with financial governance system helps the management

in setting measurements for achievement of objectives and provide regular check of the

efficiency of activities and people. This helps in performance appraisal and detect deviations.

After identifying variations it helps in implementing standards and guidelines that are must to

control the deviations and make corrections in the procedures and structures.

MAS to solve financial issues:

In an organisation the use of different system is beneficial to reduce the financial problem

that can hinder the overall performance. In the context of above selected company there have

been different financial problem that reduces the functioning of operation and lead to decrease

the complete productivity and performance. It is observed that with the support of cost

accounting system are able to reduce the issue of more spending than earning and making

resources engage in those activities that results better profit. Similarly with the aid of inventory

management system manager of excite limited are able to reduce the cost incurred on managing

extra raw material. As they start giving the order on the specific date to meet the production

requirement without storing in warehouse for long period.

PART B

Calculations:

BEP to attain desired profit = Fixed cost + desired profit / contribution per unit

= 120000+90000

= 210000/30

= 7000 units

Profit of sale of 7000 units

Sales (7000*40) = 280000

- Variable cost = 70000

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contribution = 210000

- Fixed cost = 120000

Profit = 90000

CONCLUSION

The above report concluded that management accounting is mandatory to be used, as it help

internal manager to make valuable decision from internal report in order to maximise

productivity. Different reporting methods, such as performance report, budget and cost report

help in preparing forecasted budgets, analyse the performance of different operation and

maintain a proper record of cost incurred on these activities. With the support of several MA

system Excite limited is able to resolve the financial problem and make each operation to work

in desired manner to attain the goals. In contrast to certain planning methods, such as ZBB,

manager are able to control budgets and make proper estimation so that each business operation

work in the favour to attain main objective.

15

- Fixed cost = 120000

Profit = 90000

CONCLUSION

The above report concluded that management accounting is mandatory to be used, as it help

internal manager to make valuable decision from internal report in order to maximise

productivity. Different reporting methods, such as performance report, budget and cost report

help in preparing forecasted budgets, analyse the performance of different operation and

maintain a proper record of cost incurred on these activities. With the support of several MA

system Excite limited is able to resolve the financial problem and make each operation to work

in desired manner to attain the goals. In contrast to certain planning methods, such as ZBB,

manager are able to control budgets and make proper estimation so that each business operation

work in the favour to attain main objective.

15

REFERENCES

Books and journals:

Elmassri, M .M., Harris, E. P. and Carter, D. B., 2016. Accounting for strategic investment

decision-making under extreme uncertainty. The British Accounting Review. 48(2).

pp.151-168.

Smith, S. S., 2015. Accounting: Evolving for an integrated future. Journal of Accounting,

Finance & Management Strategy. 10(1). p.1.

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and effectiveness

of management control systems with cybernetic tools. Management Accounting

Research. 33. pp.1-15.

Sithole, S., Chandler, P., Abeysekera, I. and Paas, F., 2017. Benefits of guided self-management

of attention on learning accounting. Journal of Educational Psychology. 109(2). p.220.

Brown, J. and Dillard, J., 2015. Opening accounting to critical scrutiny: towards dialogic

accounting for policy analysis and democracy. Journal of Comparative Policy Analysis:

Research and Practice. 17(3). pp.247-268.

Burritt, R .L. and Christ, K .L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management. 201. pp.72-81.

Laing, G .K. and Perrin, R .W., 2018. Management Accounting in the Australian Printing

Industry: A Survey. The Journal of New Business Ideas & Trends. 16(3). pp.13-19.

Meidell, A. and Kaarbøe, K., 2017. How the enterprise risk management function influences

decision-making in the organization–A field study of a large, global oil and gas

company. The British Accounting Review. . 49(1). pp.39-55.

Gomez-Conde, J., Lunkes, R .J. and Rosa, F .S., 2019. Environmental innovation practices and

operational performance. The joint effects of management accounting and control

systems and environmental training. Accounting, Auditing & Accountability Journal.

Saeidi, S. P., Othman, M .S. H., Saeidi, P. and Saeidi, S. P., 2018. The moderating role of

environmental management accounting between environmental innovation and firm

financial performance. International Journal of Business Performance Management.

19(3). pp.326-348.

Hemmer, T. and Labro, E., 2017. Management Accounting and Operations Management. In The

Routledge Companion to Production and Operations Management (pp. 345-359).

Routledge.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Beske-Janssen, P., Johnson, M.P. and Schaltegger, S., 2015. 20 years of performance

measurement in sustainable supply chain management–what has been achieved?. Supply

chain management: An international Journal. 20(6). pp.664-680.

Chandler, J., 2017. Questioning the new public management. Routledge.

Farrell, M. and Gallagher, R., 2015. The valuation implications of enterprise risk management

maturity. Journal of Risk and Insurance. 82(3). pp.625-657.

16

Books and journals:

Elmassri, M .M., Harris, E. P. and Carter, D. B., 2016. Accounting for strategic investment

decision-making under extreme uncertainty. The British Accounting Review. 48(2).

pp.151-168.

Smith, S. S., 2015. Accounting: Evolving for an integrated future. Journal of Accounting,

Finance & Management Strategy. 10(1). p.1.

O’Grady, W., Morlidge, S. and Rouse, P., 2016. Evaluating the completeness and effectiveness

of management control systems with cybernetic tools. Management Accounting

Research. 33. pp.1-15.

Sithole, S., Chandler, P., Abeysekera, I. and Paas, F., 2017. Benefits of guided self-management

of attention on learning accounting. Journal of Educational Psychology. 109(2). p.220.

Brown, J. and Dillard, J., 2015. Opening accounting to critical scrutiny: towards dialogic

accounting for policy analysis and democracy. Journal of Comparative Policy Analysis:

Research and Practice. 17(3). pp.247-268.

Burritt, R .L. and Christ, K .L., 2017. The need for monetary information within corporate water

accounting. Journal of environmental management. 201. pp.72-81.

Laing, G .K. and Perrin, R .W., 2018. Management Accounting in the Australian Printing

Industry: A Survey. The Journal of New Business Ideas & Trends. 16(3). pp.13-19.

Meidell, A. and Kaarbøe, K., 2017. How the enterprise risk management function influences

decision-making in the organization–A field study of a large, global oil and gas

company. The British Accounting Review. . 49(1). pp.39-55.

Gomez-Conde, J., Lunkes, R .J. and Rosa, F .S., 2019. Environmental innovation practices and

operational performance. The joint effects of management accounting and control

systems and environmental training. Accounting, Auditing & Accountability Journal.

Saeidi, S. P., Othman, M .S. H., Saeidi, P. and Saeidi, S. P., 2018. The moderating role of

environmental management accounting between environmental innovation and firm

financial performance. International Journal of Business Performance Management.

19(3). pp.326-348.

Hemmer, T. and Labro, E., 2017. Management Accounting and Operations Management. In The

Routledge Companion to Production and Operations Management (pp. 345-359).

Routledge.

Hoque, Z., 2018. Methodological issues in accounting research. Spiramus Press Ltd.

Beske-Janssen, P., Johnson, M.P. and Schaltegger, S., 2015. 20 years of performance

measurement in sustainable supply chain management–what has been achieved?. Supply

chain management: An international Journal. 20(6). pp.664-680.

Chandler, J., 2017. Questioning the new public management. Routledge.

Farrell, M. and Gallagher, R., 2015. The valuation implications of enterprise risk management

maturity. Journal of Risk and Insurance. 82(3). pp.625-657.

16

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.