Management Accounting Case Study: Voltus Overhead Allocation Analysis

VerifiedAdded on 2022/11/19

|12

|2903

|500

Homework Assignment

AI Summary

This document provides a comprehensive solution to a management accounting case study focused on Voltus. It begins by explaining prime costs, overhead, and the traditional volume-based overhead allocation method, calculating a predetermined overhead rate of $45 per machine hour. T...

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................7

Answer to question 6:.................................................................................................................8

References and bibliography:...................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................7

Answer to question 6:.................................................................................................................8

References and bibliography:...................................................................................................10

2MANAGEMENT ACCOUNTING

Answer to question 1:

Production of any goods or rendering of any service require certain inputs. All the

costs related to the prime input factors constitute the prime cost of the product or services. In

other words, all the direct expenses are the part of prime costs and all the indirect expenses

are collectively called overhead. Therefore, indirect materials used in production, indirect

labour incurred in relation to the production or manufacturing of goods and any other indirect

expenses are collectively called manufacturing overhead. In the same way, indirect materials

indirect labour and indirect expenses related to selling and distribution of goods are known as

selling and distribution overhead. Similarly all the period expenses related to the office and

administration are known as office and administrative overhead (Anderson and Dekker

2014).

Overhead expenses are those expenses which cannot be directly linked with the

production unit and hence, it needs to be allocated or absorbed to the production unit using

certain appropriate basis. The system of allocation of overhead to the production unit is called

the overhead allocation or overhead absorption. There are various methods of overhead

allocation or overhead absorption. The traditional method of overhead allocation uses a single

base for allocation of all the overhead expenses and that is why it is called the volume based

overhead allocation system (Kaplan and Atkinson 2015). There are various disadvantages of

overhead allocation using a single base which makes it an unscientific and inappropriate

method of overhead allocation in the modern revolutionary business era. In this system, a

predetermined overhead rate is computed based on the estimated total overhead and total use

of a single activity. Using that rate all the overhead is allocated to the production units

(Kamal 2015).

Answer to question 1:

Production of any goods or rendering of any service require certain inputs. All the

costs related to the prime input factors constitute the prime cost of the product or services. In

other words, all the direct expenses are the part of prime costs and all the indirect expenses

are collectively called overhead. Therefore, indirect materials used in production, indirect

labour incurred in relation to the production or manufacturing of goods and any other indirect

expenses are collectively called manufacturing overhead. In the same way, indirect materials

indirect labour and indirect expenses related to selling and distribution of goods are known as

selling and distribution overhead. Similarly all the period expenses related to the office and

administration are known as office and administrative overhead (Anderson and Dekker

2014).

Overhead expenses are those expenses which cannot be directly linked with the

production unit and hence, it needs to be allocated or absorbed to the production unit using

certain appropriate basis. The system of allocation of overhead to the production unit is called

the overhead allocation or overhead absorption. There are various methods of overhead

allocation or overhead absorption. The traditional method of overhead allocation uses a single

base for allocation of all the overhead expenses and that is why it is called the volume based

overhead allocation system (Kaplan and Atkinson 2015). There are various disadvantages of

overhead allocation using a single base which makes it an unscientific and inappropriate

method of overhead allocation in the modern revolutionary business era. In this system, a

predetermined overhead rate is computed based on the estimated total overhead and total use

of a single activity. Using that rate all the overhead is allocated to the production units

(Kamal 2015).

You're viewing a preview

Unlock full access by subscribing today!

3MANAGEMENT ACCOUNTING

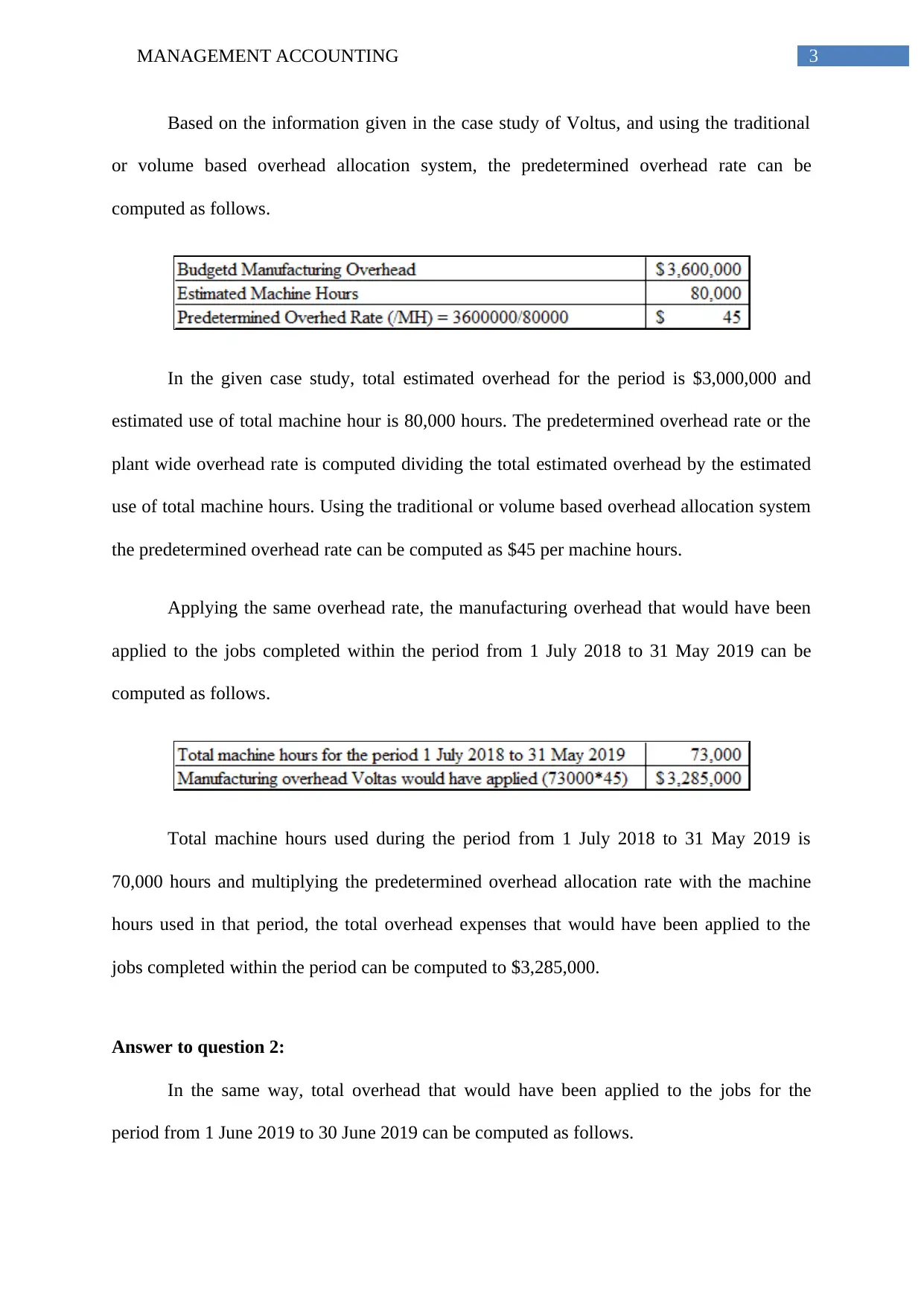

Based on the information given in the case study of Voltus, and using the traditional

or volume based overhead allocation system, the predetermined overhead rate can be

computed as follows.

In the given case study, total estimated overhead for the period is $3,000,000 and

estimated use of total machine hour is 80,000 hours. The predetermined overhead rate or the

plant wide overhead rate is computed dividing the total estimated overhead by the estimated

use of total machine hours. Using the traditional or volume based overhead allocation system

the predetermined overhead rate can be computed as $45 per machine hours.

Applying the same overhead rate, the manufacturing overhead that would have been

applied to the jobs completed within the period from 1 July 2018 to 31 May 2019 can be

computed as follows.

Total machine hours used during the period from 1 July 2018 to 31 May 2019 is

70,000 hours and multiplying the predetermined overhead allocation rate with the machine

hours used in that period, the total overhead expenses that would have been applied to the

jobs completed within the period can be computed to $3,285,000.

Answer to question 2:

In the same way, total overhead that would have been applied to the jobs for the

period from 1 June 2019 to 30 June 2019 can be computed as follows.

Based on the information given in the case study of Voltus, and using the traditional

or volume based overhead allocation system, the predetermined overhead rate can be

computed as follows.

In the given case study, total estimated overhead for the period is $3,000,000 and

estimated use of total machine hour is 80,000 hours. The predetermined overhead rate or the

plant wide overhead rate is computed dividing the total estimated overhead by the estimated

use of total machine hours. Using the traditional or volume based overhead allocation system

the predetermined overhead rate can be computed as $45 per machine hours.

Applying the same overhead rate, the manufacturing overhead that would have been

applied to the jobs completed within the period from 1 July 2018 to 31 May 2019 can be

computed as follows.

Total machine hours used during the period from 1 July 2018 to 31 May 2019 is

70,000 hours and multiplying the predetermined overhead allocation rate with the machine

hours used in that period, the total overhead expenses that would have been applied to the

jobs completed within the period can be computed to $3,285,000.

Answer to question 2:

In the same way, total overhead that would have been applied to the jobs for the

period from 1 June 2019 to 30 June 2019 can be computed as follows.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

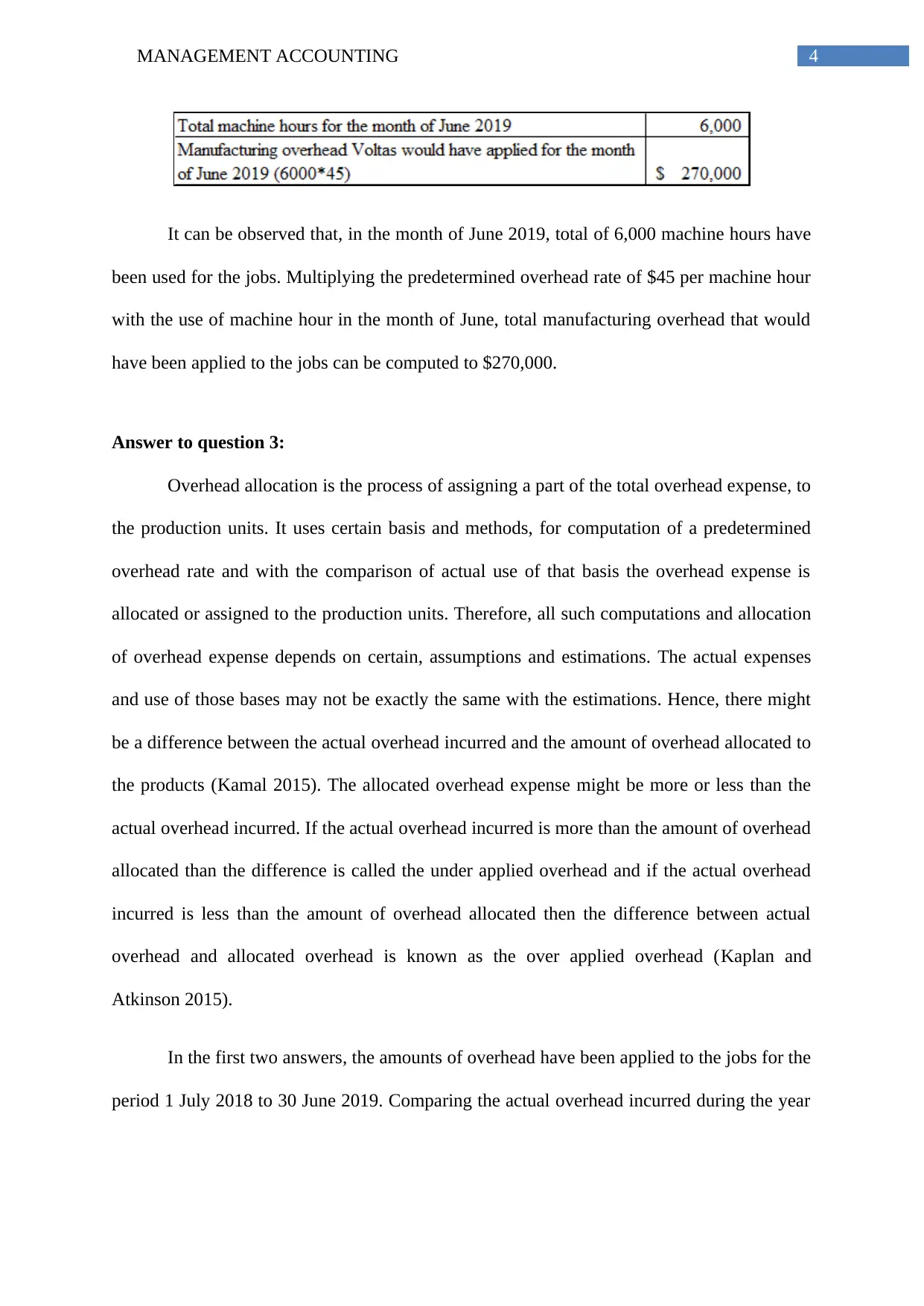

It can be observed that, in the month of June 2019, total of 6,000 machine hours have

been used for the jobs. Multiplying the predetermined overhead rate of $45 per machine hour

with the use of machine hour in the month of June, total manufacturing overhead that would

have been applied to the jobs can be computed to $270,000.

Answer to question 3:

Overhead allocation is the process of assigning a part of the total overhead expense, to

the production units. It uses certain basis and methods, for computation of a predetermined

overhead rate and with the comparison of actual use of that basis the overhead expense is

allocated or assigned to the production units. Therefore, all such computations and allocation

of overhead expense depends on certain, assumptions and estimations. The actual expenses

and use of those bases may not be exactly the same with the estimations. Hence, there might

be a difference between the actual overhead incurred and the amount of overhead allocated to

the products (Kamal 2015). The allocated overhead expense might be more or less than the

actual overhead incurred. If the actual overhead incurred is more than the amount of overhead

allocated than the difference is called the under applied overhead and if the actual overhead

incurred is less than the amount of overhead allocated then the difference between actual

overhead and allocated overhead is known as the over applied overhead (Kaplan and

Atkinson 2015).

In the first two answers, the amounts of overhead have been applied to the jobs for the

period 1 July 2018 to 30 June 2019. Comparing the actual overhead incurred during the year

It can be observed that, in the month of June 2019, total of 6,000 machine hours have

been used for the jobs. Multiplying the predetermined overhead rate of $45 per machine hour

with the use of machine hour in the month of June, total manufacturing overhead that would

have been applied to the jobs can be computed to $270,000.

Answer to question 3:

Overhead allocation is the process of assigning a part of the total overhead expense, to

the production units. It uses certain basis and methods, for computation of a predetermined

overhead rate and with the comparison of actual use of that basis the overhead expense is

allocated or assigned to the production units. Therefore, all such computations and allocation

of overhead expense depends on certain, assumptions and estimations. The actual expenses

and use of those bases may not be exactly the same with the estimations. Hence, there might

be a difference between the actual overhead incurred and the amount of overhead allocated to

the products (Kamal 2015). The allocated overhead expense might be more or less than the

actual overhead incurred. If the actual overhead incurred is more than the amount of overhead

allocated than the difference is called the under applied overhead and if the actual overhead

incurred is less than the amount of overhead allocated then the difference between actual

overhead and allocated overhead is known as the over applied overhead (Kaplan and

Atkinson 2015).

In the first two answers, the amounts of overhead have been applied to the jobs for the

period 1 July 2018 to 30 June 2019. Comparing the actual overhead incurred during the year

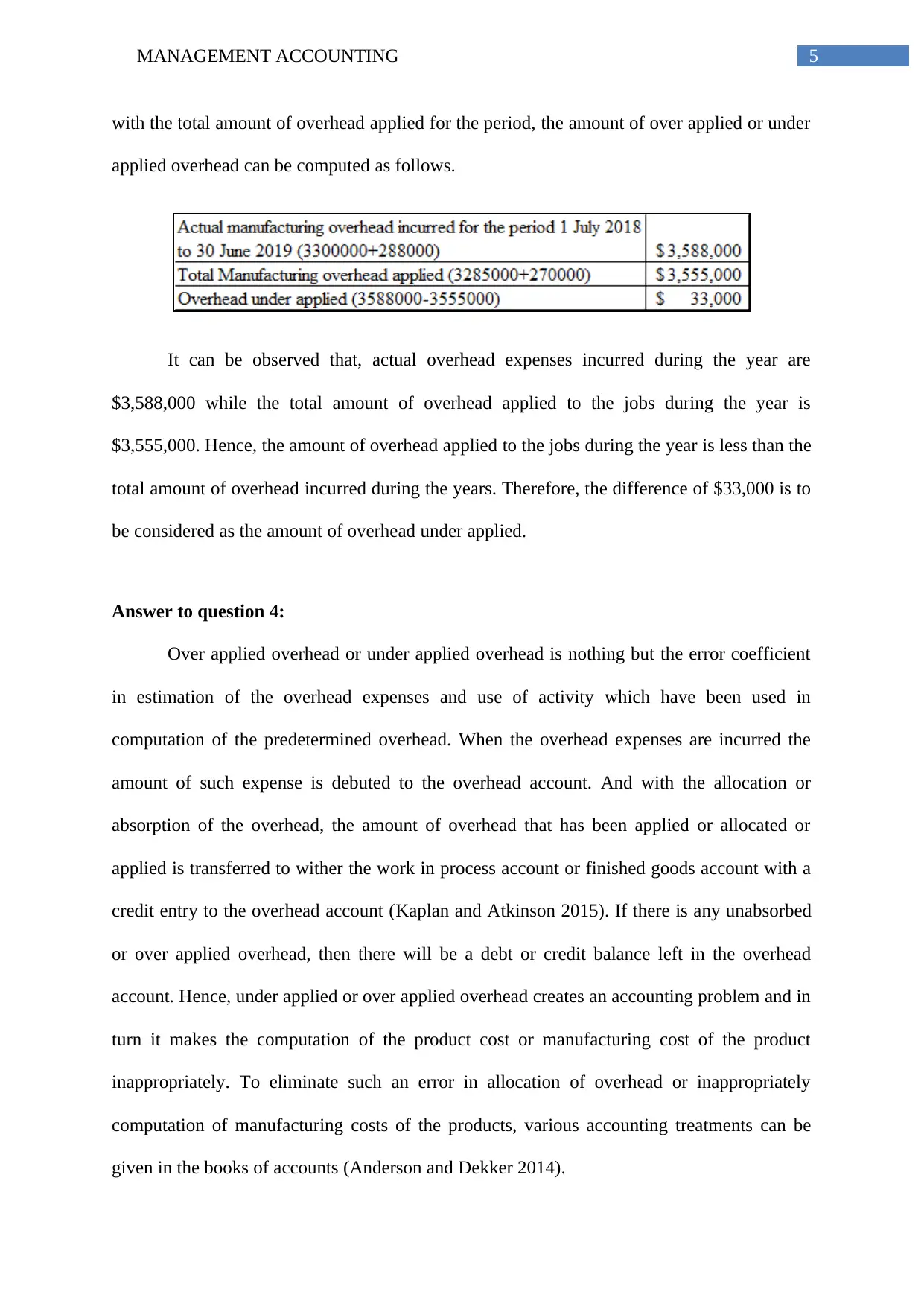

5MANAGEMENT ACCOUNTING

with the total amount of overhead applied for the period, the amount of over applied or under

applied overhead can be computed as follows.

It can be observed that, actual overhead expenses incurred during the year are

$3,588,000 while the total amount of overhead applied to the jobs during the year is

$3,555,000. Hence, the amount of overhead applied to the jobs during the year is less than the

total amount of overhead incurred during the years. Therefore, the difference of $33,000 is to

be considered as the amount of overhead under applied.

Answer to question 4:

Over applied overhead or under applied overhead is nothing but the error coefficient

in estimation of the overhead expenses and use of activity which have been used in

computation of the predetermined overhead. When the overhead expenses are incurred the

amount of such expense is debuted to the overhead account. And with the allocation or

absorption of the overhead, the amount of overhead that has been applied or allocated or

applied is transferred to wither the work in process account or finished goods account with a

credit entry to the overhead account (Kaplan and Atkinson 2015). If there is any unabsorbed

or over applied overhead, then there will be a debt or credit balance left in the overhead

account. Hence, under applied or over applied overhead creates an accounting problem and in

turn it makes the computation of the product cost or manufacturing cost of the product

inappropriately. To eliminate such an error in allocation of overhead or inappropriately

computation of manufacturing costs of the products, various accounting treatments can be

given in the books of accounts (Anderson and Dekker 2014).

with the total amount of overhead applied for the period, the amount of over applied or under

applied overhead can be computed as follows.

It can be observed that, actual overhead expenses incurred during the year are

$3,588,000 while the total amount of overhead applied to the jobs during the year is

$3,555,000. Hence, the amount of overhead applied to the jobs during the year is less than the

total amount of overhead incurred during the years. Therefore, the difference of $33,000 is to

be considered as the amount of overhead under applied.

Answer to question 4:

Over applied overhead or under applied overhead is nothing but the error coefficient

in estimation of the overhead expenses and use of activity which have been used in

computation of the predetermined overhead. When the overhead expenses are incurred the

amount of such expense is debuted to the overhead account. And with the allocation or

absorption of the overhead, the amount of overhead that has been applied or allocated or

applied is transferred to wither the work in process account or finished goods account with a

credit entry to the overhead account (Kaplan and Atkinson 2015). If there is any unabsorbed

or over applied overhead, then there will be a debt or credit balance left in the overhead

account. Hence, under applied or over applied overhead creates an accounting problem and in

turn it makes the computation of the product cost or manufacturing cost of the product

inappropriately. To eliminate such an error in allocation of overhead or inappropriately

computation of manufacturing costs of the products, various accounting treatments can be

given in the books of accounts (Anderson and Dekker 2014).

You're viewing a preview

Unlock full access by subscribing today!

6MANAGEMENT ACCOUNTING

Under applied overhead implies computation of less amount of production cost for the

products. On the other hand, over applied overhead implies computation of higher amount of

production costs for the product (Henri, Boiral and Roy 2016). Therefore, to adjust the cost of

products and to eliminate the effect of over applied or under applied overhead expense, the

cost of the finished goods or work in process need to be adjusted by an appropriate

accounting entry. If the production process is still in progress and the amount incurred is still

in work in process, then the amount of over applied or under applied overhead needs to be

adjusted with the amount of work in process inventory and if the jobs are completed and

transferred to the finished goods inventory, then the amount of over applied or under applied

overhead needs to be adjusted with the amount of finished goods inventory (Kamal 2015). If

the goods which have been manufactured and to which such overhead expenses were

incurred is already sold, then the complications arises. Though there are certain ways and

accounting treatments through which the under applied and over applied overhead can be

adjusted.

If the is an under applied overhead and the goods are still in process, then the

overhead account is credited with the amount of under applied overhead and the work in

process inventory is debited with the same amount. On the other hand, if there is an over

applied overhead and the goods are still in process, then the amount of over applied overhead

is debited to the overhead account and the same is credited to the work in process inventory

account (Henri, Boiral and Roy 2016). When the goods are completely processed and the

goods are transferred to the finished goods inventory and there is an under applied overhead,

then the amount of under applied overhead is to be debited to the finished goods inventory

and the same amount is to be credited to the overhead account. If there is any over applied

overhead and the goods are still in the finished goods inventory then the overhead account is

Under applied overhead implies computation of less amount of production cost for the

products. On the other hand, over applied overhead implies computation of higher amount of

production costs for the product (Henri, Boiral and Roy 2016). Therefore, to adjust the cost of

products and to eliminate the effect of over applied or under applied overhead expense, the

cost of the finished goods or work in process need to be adjusted by an appropriate

accounting entry. If the production process is still in progress and the amount incurred is still

in work in process, then the amount of over applied or under applied overhead needs to be

adjusted with the amount of work in process inventory and if the jobs are completed and

transferred to the finished goods inventory, then the amount of over applied or under applied

overhead needs to be adjusted with the amount of finished goods inventory (Kamal 2015). If

the goods which have been manufactured and to which such overhead expenses were

incurred is already sold, then the complications arises. Though there are certain ways and

accounting treatments through which the under applied and over applied overhead can be

adjusted.

If the is an under applied overhead and the goods are still in process, then the

overhead account is credited with the amount of under applied overhead and the work in

process inventory is debited with the same amount. On the other hand, if there is an over

applied overhead and the goods are still in process, then the amount of over applied overhead

is debited to the overhead account and the same is credited to the work in process inventory

account (Henri, Boiral and Roy 2016). When the goods are completely processed and the

goods are transferred to the finished goods inventory and there is an under applied overhead,

then the amount of under applied overhead is to be debited to the finished goods inventory

and the same amount is to be credited to the overhead account. If there is any over applied

overhead and the goods are still in the finished goods inventory then the overhead account is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

debited with the amount of over applied overhead amount and a credit entry is given to the

finished goods inventory account with the same amount (Kaplan and Atkinson 2015).

If the goods are already sold and subsequently the over applied or under applied

overhead is detected, then the amount of over applied overhead is credited to the cost of

goods sold with a similar credit entry to the overhead account (Henri, Boiral and Roy 2016).

If there is any under applied overhead and the goods are already sold, then the amount of

under applied overhead is to the credited to the overhead account and a similar debit entry is

to be given to the cost of goods sold account. It can be clearly understood from the above

discussions, that the allocation and absorption of overhead increases the cost of products,

under applied overhead implies less cost of production and over applied overhead implies

more cost of production. Therefore, the cost of production needs to the adjusted accordingly

and an appropriate entry needs to be given to the appropriate account where the inventory

have been accounted for (Kaplan and Atkinson 2015).

Answer to question 5:

There are various methods of overhead allocation which uses different bases and

estimation for such an overhead allocation. Allocation and absorption of overhead using a

single base or using the volume of the production is known as traditional system of overhead

allocation or volume based overhead allocation system. In this system a single base is

considered for the allocation of the total overhead expense. It has various inefficiencies and

disadvantages (Kamal 2015). Components of overhead expenses may not depend on a single

base or activity. There might be more than one activity which leads the overhead costs. Each

jobs or products might not be consuming or using those activities evenly. Hence, there is a

need for considering those activities which drives the overhead costs (Anderson and Dekker

2014).

debited with the amount of over applied overhead amount and a credit entry is given to the

finished goods inventory account with the same amount (Kaplan and Atkinson 2015).

If the goods are already sold and subsequently the over applied or under applied

overhead is detected, then the amount of over applied overhead is credited to the cost of

goods sold with a similar credit entry to the overhead account (Henri, Boiral and Roy 2016).

If there is any under applied overhead and the goods are already sold, then the amount of

under applied overhead is to the credited to the overhead account and a similar debit entry is

to be given to the cost of goods sold account. It can be clearly understood from the above

discussions, that the allocation and absorption of overhead increases the cost of products,

under applied overhead implies less cost of production and over applied overhead implies

more cost of production. Therefore, the cost of production needs to the adjusted accordingly

and an appropriate entry needs to be given to the appropriate account where the inventory

have been accounted for (Kaplan and Atkinson 2015).

Answer to question 5:

There are various methods of overhead allocation which uses different bases and

estimation for such an overhead allocation. Allocation and absorption of overhead using a

single base or using the volume of the production is known as traditional system of overhead

allocation or volume based overhead allocation system. In this system a single base is

considered for the allocation of the total overhead expense. It has various inefficiencies and

disadvantages (Kamal 2015). Components of overhead expenses may not depend on a single

base or activity. There might be more than one activity which leads the overhead costs. Each

jobs or products might not be consuming or using those activities evenly. Hence, there is a

need for considering those activities which drives the overhead costs (Anderson and Dekker

2014).

8MANAGEMENT ACCOUNTING

To eliminate the disadvantages of the traditional or volume based overhead allocation

system, the activity based system of overhead allocation has been developed. In this system

the total overhead expenses is identified with some key activities which drives the amount of

overhead expenses. Based on the use of each such activity the total overhead amount is

allocated to the products or jobs. The activity based overhead allocation system is more

scientific as it considers all those activities which drive the overhead costs and allocates the

overhead on the basis of use of such activities (Kamal 2015). In this system the overhead is

efficiently allocated to the products or jobs, hence, it helps in computation of cost of products

correctly.

In the given case study, there are four components of the overhead expenses, but the

activities leading those expenses could not be identified. Hence, in this case the activity based

costing system could not be applied. If the activities behind such overhead expenses could

have been identified, then the activity based costing system could have been applied

successfully, to allocate the total overhead expenses to the jobs (Anderson and Dekker 2014).

Answer to question 6:

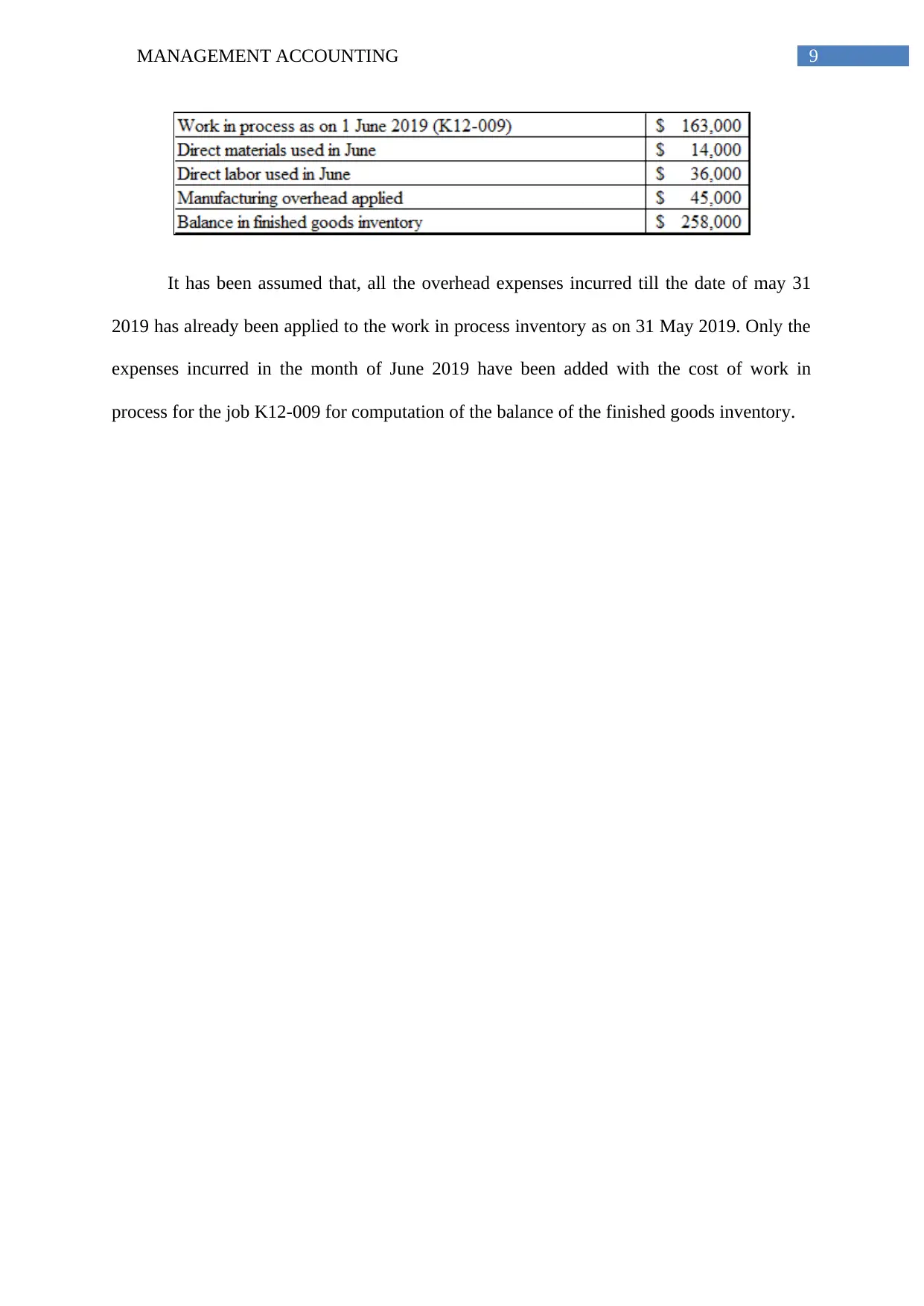

Computation of value of finished goods inventory requires identification of the jobs

which have been completed and transferred to the finished goods inventory but are still left

with the finished goods and not already sold to the market. It can be observed from the given

case study that, the job number K12-009 is only left with the finished goods inventory.

Hence, the manufacturing cost of job number K12-009 would be the balance of finished

goods inventory as on the closing date. Therefore, the amount of balance in finished goods

inventory as on 30 June 2019 can be computed as follows.

To eliminate the disadvantages of the traditional or volume based overhead allocation

system, the activity based system of overhead allocation has been developed. In this system

the total overhead expenses is identified with some key activities which drives the amount of

overhead expenses. Based on the use of each such activity the total overhead amount is

allocated to the products or jobs. The activity based overhead allocation system is more

scientific as it considers all those activities which drive the overhead costs and allocates the

overhead on the basis of use of such activities (Kamal 2015). In this system the overhead is

efficiently allocated to the products or jobs, hence, it helps in computation of cost of products

correctly.

In the given case study, there are four components of the overhead expenses, but the

activities leading those expenses could not be identified. Hence, in this case the activity based

costing system could not be applied. If the activities behind such overhead expenses could

have been identified, then the activity based costing system could have been applied

successfully, to allocate the total overhead expenses to the jobs (Anderson and Dekker 2014).

Answer to question 6:

Computation of value of finished goods inventory requires identification of the jobs

which have been completed and transferred to the finished goods inventory but are still left

with the finished goods and not already sold to the market. It can be observed from the given

case study that, the job number K12-009 is only left with the finished goods inventory.

Hence, the manufacturing cost of job number K12-009 would be the balance of finished

goods inventory as on the closing date. Therefore, the amount of balance in finished goods

inventory as on 30 June 2019 can be computed as follows.

You're viewing a preview

Unlock full access by subscribing today!

9MANAGEMENT ACCOUNTING

It has been assumed that, all the overhead expenses incurred till the date of may 31

2019 has already been applied to the work in process inventory as on 31 May 2019. Only the

expenses incurred in the month of June 2019 have been added with the cost of work in

process for the job K12-009 for computation of the balance of the finished goods inventory.

It has been assumed that, all the overhead expenses incurred till the date of may 31

2019 has already been applied to the work in process inventory as on 31 May 2019. Only the

expenses incurred in the month of June 2019 have been added with the cost of work in

process for the job K12-009 for computation of the balance of the finished goods inventory.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

References and bibliography:

Anderson, S.W. and Dekker, H.C., 2014. The role of management controls in transforming

firm boundaries and sustaining hybrid organizational forms. Foundations and Trends® in

Accounting, 8(2), pp.75-141.

Balakrishnan, R., Labro, E. and Soderstrom, N.S., 2014. Cost structure and sticky

costs. Journal of management accounting research, 26(2), pp.91-116.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial

accounting. McGraw-Hill Education.

Cooper, R., 2017. Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

Debnath, S. and Bose, S.K., 2014. Exploring full cost accounting approach to evaluate cost of

MSW services in India. Resources, Conservation and Recycling, 83, pp.87-95.

D'Onza, G., Greco, G. and Allegrini, M., 2016. Full cost accounting in the analysis of

separated waste collection efficiency: A methodological proposal. Journal of environmental

management, 167, pp.59-65.

Fayard, D., Lee, L.S., Leitch, R.A. and Kettinger, W.J., 2014. Interorganizational cost

management in supply chains: Practices and payoffs. Management accounting

quarterly, 15(3), pp.1-9.

Fleischman, R.K. and Parker, L.D., 2017. What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

References and bibliography:

Anderson, S.W. and Dekker, H.C., 2014. The role of management controls in transforming

firm boundaries and sustaining hybrid organizational forms. Foundations and Trends® in

Accounting, 8(2), pp.75-141.

Balakrishnan, R., Labro, E. and Soderstrom, N.S., 2014. Cost structure and sticky

costs. Journal of management accounting research, 26(2), pp.91-116.

Brewer, P.C., Garrison, R.H. and Noreen, E.W., 2015. Introduction to managerial

accounting. McGraw-Hill Education.

Cooper, R., 2017. Supply chain development for the lean enterprise: interorganizational cost

management. Routledge.

Debnath, S. and Bose, S.K., 2014. Exploring full cost accounting approach to evaluate cost of

MSW services in India. Resources, Conservation and Recycling, 83, pp.87-95.

D'Onza, G., Greco, G. and Allegrini, M., 2016. Full cost accounting in the analysis of

separated waste collection efficiency: A methodological proposal. Journal of environmental

management, 167, pp.59-65.

Fayard, D., Lee, L.S., Leitch, R.A. and Kettinger, W.J., 2014. Interorganizational cost

management in supply chains: Practices and payoffs. Management accounting

quarterly, 15(3), pp.1-9.

Fleischman, R.K. and Parker, L.D., 2017. What is Past is Prologue: Cost Accounting in the

British Industrial Revolution, 1760-1850. Routledge.

11MANAGEMENT ACCOUNTING

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Henri, J.F., Boiral, O. and Roy, M.J., 2016. Strategic cost management and performance: The

case of environmental costs. The British Accounting Review, 48(2), pp.269-282.

Kamal, S., 2015. Historical evolution of management accounting. The cost and

management, 43(4), pp.12-19.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Klychova, G.S., Faskhutdinova, М.S. and Sadrieva, E.R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), p.79.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Nakajima, M., Kimura, A. and Wagner, B., 2015. Introduction of material flow cost

accounting (MFCA) to the supply chain: a questionnaire study on the challenges of

constructing a low-carbon supply chain to promote resource efficiency. Journal of Cleaner

Production, 108, pp.1302-1309.

Nørreklit, H., 2014. Quality in qualitative management accounting research. Qualitative

Research in Accounting & Management, 11(1), pp.29-39.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Henri, J.F., Boiral, O. and Roy, M.J., 2016. Strategic cost management and performance: The

case of environmental costs. The British Accounting Review, 48(2), pp.269-282.

Kamal, S., 2015. Historical evolution of management accounting. The cost and

management, 43(4), pp.12-19.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Klychova, G.S., Faskhutdinova, М.S. and Sadrieva, E.R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), p.79.

Maskell, B.H., Baggaley, B. and Grasso, L., 2017. Practical lean accounting: a proven

system for measuring and managing the lean enterprise. Productivity Press.

Nakajima, M., Kimura, A. and Wagner, B., 2015. Introduction of material flow cost

accounting (MFCA) to the supply chain: a questionnaire study on the challenges of

constructing a low-carbon supply chain to promote resource efficiency. Journal of Cleaner

Production, 108, pp.1302-1309.

Nørreklit, H., 2014. Quality in qualitative management accounting research. Qualitative

Research in Accounting & Management, 11(1), pp.29-39.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

You're viewing a preview

Unlock full access by subscribing today!

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.