Review of Management Accounting Research Studies

VerifiedAdded on 2020/10/05

|17

|5365

|289

AI Summary

The assignment provided is a review of management accounting research studies. It includes a list of references to various articles and books on management accounting practices in different countries and industries. The references are from reputable journals such as Accounting Perspectives, Management: Journal of Contemporary Management Issues, and Industrial Management & Data Systems. The studies cover topics such as activity-based costing, open-book accounting, lean manufacturing, and carbon accounting for sustainability and management. The review aims to provide an overview of the current state of management accounting research and identify potential areas for further study.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirement of its systems..................................................1

M1 Benefits of different management accounting systems...................................................3

P2 Management accounting reporting and its types...............................................................3

D1 Integration of management accounting system and its reports in organisational process5

TASK 2............................................................................................................................................5

P3 Different costing techniques..............................................................................................5

M2: Different types of accounting tools and techniques........................................................7

D2: Analysis of data collected from income statement..........................................................7

TASK 3............................................................................................................................................7

P4 Advantage and Disadvantages of different types of planning tools used for Budgetary

Control....................................................................................................................................7

M3 Use of planning tools while forecasting and estimating budgets...................................10

TASK 4..........................................................................................................................................10

P5 How organisation is dealing with financial problems.....................................................10

D3 Planning tools for solving financial issues.....................................................................12

CONCLUSIONS............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and requirement of its systems..................................................1

M1 Benefits of different management accounting systems...................................................3

P2 Management accounting reporting and its types...............................................................3

D1 Integration of management accounting system and its reports in organisational process5

TASK 2............................................................................................................................................5

P3 Different costing techniques..............................................................................................5

M2: Different types of accounting tools and techniques........................................................7

D2: Analysis of data collected from income statement..........................................................7

TASK 3............................................................................................................................................7

P4 Advantage and Disadvantages of different types of planning tools used for Budgetary

Control....................................................................................................................................7

M3 Use of planning tools while forecasting and estimating budgets...................................10

TASK 4..........................................................................................................................................10

P5 How organisation is dealing with financial problems.....................................................10

D3 Planning tools for solving financial issues.....................................................................12

CONCLUSIONS............................................................................................................................13

REFERENCES .............................................................................................................................14

INTRODUCTION

Management accounting is a process of generating reports that may provide actual

information of business to internal stakeholder of an organisation. It help to get exact knowledge

of that how a business is operating and performing its activities (Management accounting, 2018).

Managers of an organisation are liable to record information in different reports so that this

information may be used to analyse actual position of company. It helps in decision making and

planning for future, by estimating possible future consequences. Management of a company

generate reports to record information of cost, inventory, activities and budgets. The company

chosen for this project report is Oak Cash and Carry Ltd, it is a retail company which is based in

Banbury, United Kingdom. Main objective of this report is to analyse use of management

accounting in a business.

In this project report various topics are discussed, that are management accounting, its

systems, reports, benefits, various costing techniques to calculate operating profits of the

company, advantages and disadvantages of different planning tools that are used in budgetary

control and how organisation use management accounting system to resolve financial problems.

TASK 1

P1 Management accounting and requirement of its systems

Accounting: It is a process of recording data of financial transactions in to books. It

includes assessing, summarising, analysing and reporting these transactions to supervise

administration, regulatory bodies and tax collection authority (Amidu, Effah and Abor, 2011). It

is a function which is followed by the organisations. There are two different types of accounting,

that are as followed:

Financial accounting: It refers to the formulation of financial statements such as income

statement, balance sheet and cash flow statements. These are mainly generated for external

stakeholders like customers, suppliers, government and investors of company to analyse

financial position in the market (Carlsson-Wall, Kraus and Lind, 2015). In Oak Cash and Carry

Ltd financial accounting is followed to generate reports that may reflect financial status of the

organisation.

Management accounting: It is a process in which managers prepare management

reports that reflects the performance of a company. These reports are generated for internal

1

Management accounting is a process of generating reports that may provide actual

information of business to internal stakeholder of an organisation. It help to get exact knowledge

of that how a business is operating and performing its activities (Management accounting, 2018).

Managers of an organisation are liable to record information in different reports so that this

information may be used to analyse actual position of company. It helps in decision making and

planning for future, by estimating possible future consequences. Management of a company

generate reports to record information of cost, inventory, activities and budgets. The company

chosen for this project report is Oak Cash and Carry Ltd, it is a retail company which is based in

Banbury, United Kingdom. Main objective of this report is to analyse use of management

accounting in a business.

In this project report various topics are discussed, that are management accounting, its

systems, reports, benefits, various costing techniques to calculate operating profits of the

company, advantages and disadvantages of different planning tools that are used in budgetary

control and how organisation use management accounting system to resolve financial problems.

TASK 1

P1 Management accounting and requirement of its systems

Accounting: It is a process of recording data of financial transactions in to books. It

includes assessing, summarising, analysing and reporting these transactions to supervise

administration, regulatory bodies and tax collection authority (Amidu, Effah and Abor, 2011). It

is a function which is followed by the organisations. There are two different types of accounting,

that are as followed:

Financial accounting: It refers to the formulation of financial statements such as income

statement, balance sheet and cash flow statements. These are mainly generated for external

stakeholders like customers, suppliers, government and investors of company to analyse

financial position in the market (Carlsson-Wall, Kraus and Lind, 2015). In Oak Cash and Carry

Ltd financial accounting is followed to generate reports that may reflect financial status of the

organisation.

Management accounting: It is a process in which managers prepare management

reports that reflects the performance of a company. These reports are generated for internal

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

stakeholders to provide them actual information about operational and executional activities that

are performed by an organisation. In Oak Cash and Carry Ltd managers use management

accounting to analyse that how organisation is performing in market. It helps managers in

strategic decision making so that they may plan in advance for possible uncertainty. In Oak Cash

and Carry Ltd three management accounting systems are followed that are as follows:

Cost accounting system: It is used to analyse actual cost of products that are sold by a

company. It help managers to estimate profitability of firm by analyse most profitable products

(Dražić Lutilsky and Dragija, 2012). In Oak Cash and Carry Ltd cost accounting system is

followed by the managers to record actual cost involved in distribution, sales and supply chain of

products. Management of organisation may estimate actual cost with help of their system. There

are three types of cost accounting system that are used by the company. That are as followed:

Actual costing: It is a method in which actual costs like labour and overheads are

recorded in books that are related with the product. For example managers of Oak Cash

and Carry Ltd determine direct costs that are concerned with distribution of products.

Normal costing: It refers to the allotment of costs to products according to their

requirement. For example in Oak Cash and Carry Ltd managers use this system to set

selling prices for their products after analysing costs that are concerned with the same

products.

Standard costing: It is a method which is used to analyse different between actual cost

and budgeted cost of products. For example in Oak Cash and Carry Ltd management use

standard costing to determine the variances in their actual cost and forecasted or standard

cost.

Inventory management system: This is used by organisation to keep a track record of

their inventory. It help managers to get exact information of stock, whether goods are in transit

or delivered to client (Granlund, 2011). Three different types of inventory is used by organisation

like raw material, work in progress and finished goods. In Oak Cash and Carry Ltd this system

is used by managers to keep detailed information of inventory. The managers of company use

FIFO (First In First Out) method in inventory management system, in which recently received

inventory is used for sale or distribution by the company. LIFO, JIT, Perpetual inventory and

periodic inventory are other methods that can be used by companies in inventory management

system.

2

are performed by an organisation. In Oak Cash and Carry Ltd managers use management

accounting to analyse that how organisation is performing in market. It helps managers in

strategic decision making so that they may plan in advance for possible uncertainty. In Oak Cash

and Carry Ltd three management accounting systems are followed that are as follows:

Cost accounting system: It is used to analyse actual cost of products that are sold by a

company. It help managers to estimate profitability of firm by analyse most profitable products

(Dražić Lutilsky and Dragija, 2012). In Oak Cash and Carry Ltd cost accounting system is

followed by the managers to record actual cost involved in distribution, sales and supply chain of

products. Management of organisation may estimate actual cost with help of their system. There

are three types of cost accounting system that are used by the company. That are as followed:

Actual costing: It is a method in which actual costs like labour and overheads are

recorded in books that are related with the product. For example managers of Oak Cash

and Carry Ltd determine direct costs that are concerned with distribution of products.

Normal costing: It refers to the allotment of costs to products according to their

requirement. For example in Oak Cash and Carry Ltd managers use this system to set

selling prices for their products after analysing costs that are concerned with the same

products.

Standard costing: It is a method which is used to analyse different between actual cost

and budgeted cost of products. For example in Oak Cash and Carry Ltd management use

standard costing to determine the variances in their actual cost and forecasted or standard

cost.

Inventory management system: This is used by organisation to keep a track record of

their inventory. It help managers to get exact information of stock, whether goods are in transit

or delivered to client (Granlund, 2011). Three different types of inventory is used by organisation

like raw material, work in progress and finished goods. In Oak Cash and Carry Ltd this system

is used by managers to keep detailed information of inventory. The managers of company use

FIFO (First In First Out) method in inventory management system, in which recently received

inventory is used for sale or distribution by the company. LIFO, JIT, Perpetual inventory and

periodic inventory are other methods that can be used by companies in inventory management

system.

2

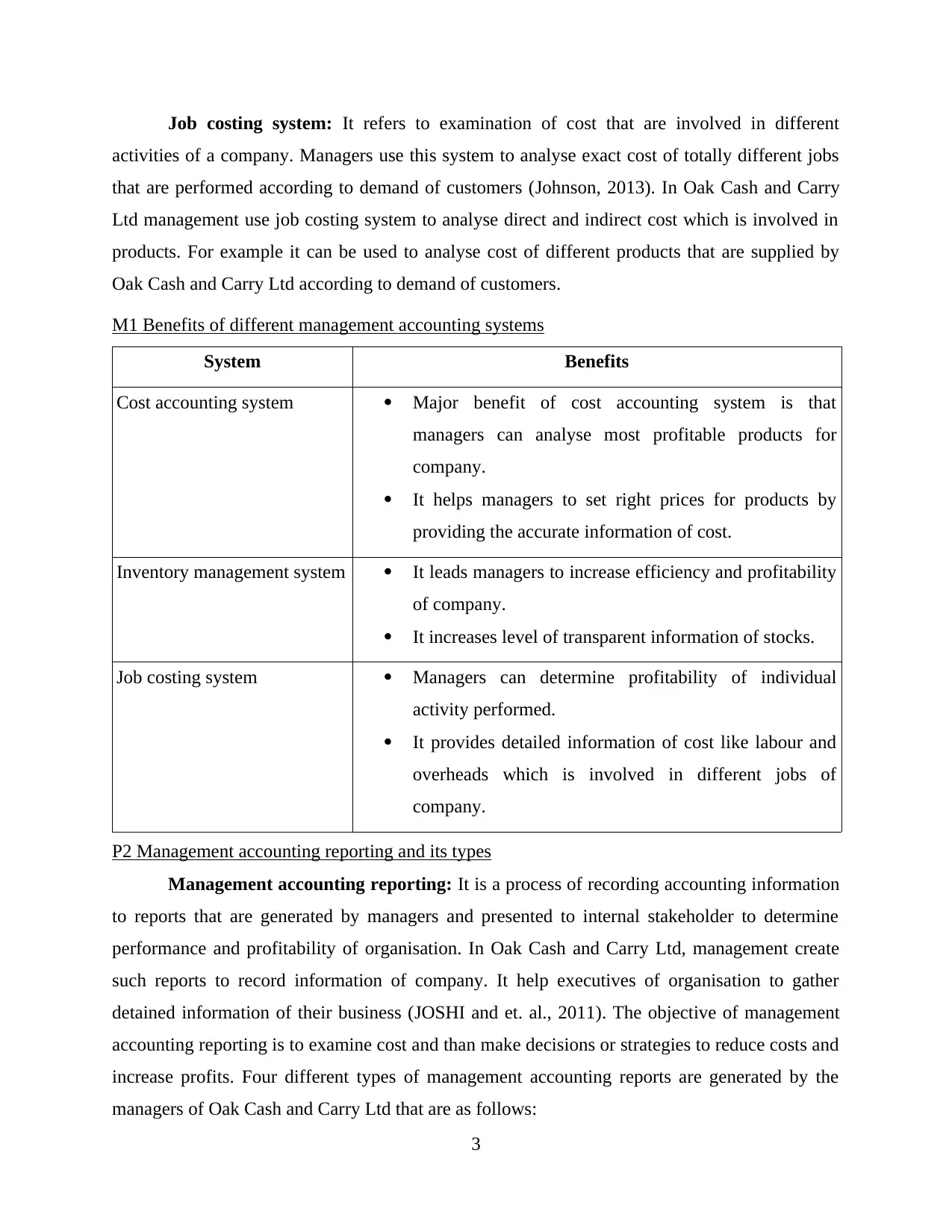

Job costing system: It refers to examination of cost that are involved in different

activities of a company. Managers use this system to analyse exact cost of totally different jobs

that are performed according to demand of customers (Johnson, 2013). In Oak Cash and Carry

Ltd management use job costing system to analyse direct and indirect cost which is involved in

products. For example it can be used to analyse cost of different products that are supplied by

Oak Cash and Carry Ltd according to demand of customers.

M1 Benefits of different management accounting systems

System Benefits

Cost accounting system Major benefit of cost accounting system is that

managers can analyse most profitable products for

company.

It helps managers to set right prices for products by

providing the accurate information of cost.

Inventory management system It leads managers to increase efficiency and profitability

of company.

It increases level of transparent information of stocks.

Job costing system Managers can determine profitability of individual

activity performed.

It provides detailed information of cost like labour and

overheads which is involved in different jobs of

company.

P2 Management accounting reporting and its types

Management accounting reporting: It is a process of recording accounting information

to reports that are generated by managers and presented to internal stakeholder to determine

performance and profitability of organisation. In Oak Cash and Carry Ltd, management create

such reports to record information of company. It help executives of organisation to gather

detained information of their business (JOSHI and et. al., 2011). The objective of management

accounting reporting is to examine cost and than make decisions or strategies to reduce costs and

increase profits. Four different types of management accounting reports are generated by the

managers of Oak Cash and Carry Ltd that are as follows:

3

activities of a company. Managers use this system to analyse exact cost of totally different jobs

that are performed according to demand of customers (Johnson, 2013). In Oak Cash and Carry

Ltd management use job costing system to analyse direct and indirect cost which is involved in

products. For example it can be used to analyse cost of different products that are supplied by

Oak Cash and Carry Ltd according to demand of customers.

M1 Benefits of different management accounting systems

System Benefits

Cost accounting system Major benefit of cost accounting system is that

managers can analyse most profitable products for

company.

It helps managers to set right prices for products by

providing the accurate information of cost.

Inventory management system It leads managers to increase efficiency and profitability

of company.

It increases level of transparent information of stocks.

Job costing system Managers can determine profitability of individual

activity performed.

It provides detailed information of cost like labour and

overheads which is involved in different jobs of

company.

P2 Management accounting reporting and its types

Management accounting reporting: It is a process of recording accounting information

to reports that are generated by managers and presented to internal stakeholder to determine

performance and profitability of organisation. In Oak Cash and Carry Ltd, management create

such reports to record information of company. It help executives of organisation to gather

detained information of their business (JOSHI and et. al., 2011). The objective of management

accounting reporting is to examine cost and than make decisions or strategies to reduce costs and

increase profits. Four different types of management accounting reports are generated by the

managers of Oak Cash and Carry Ltd that are as follows:

3

Inventory management report: It is generated to record information of inventory

related activities. It helps to make supply chain more efficient by properly maintaining

information. In Oak Cash and Carry Ltd, inventory management reports are generated to

compare different distribution channels of company to find best way to supply its products.

Managers can keep a detailed information of inventory with help of these reports.

Importance: Major importance of this system is that it help managers to keep a track

record of stock while buying or supplying (Klychova, Faskhutdinova and Sadrieva, 2014). It

directs owners of business that what is quantity of products in warehouses and when to order

inventory before warehouses go empty.

Budget report: This report is generated by managers to compare estimated output and

actual performance of a company. In Oak Cash and Carry Ltd, such reports are created by

management to control and understand costs of products. It helps to estimate future expenses in

prior years so that managers may formulate strategies to deal with or resolve same.

Importance: It helps to analyse financial health and provide overview of activities that

are performed by company in whole year. Managers may monitor revenues with help of budget

reports by keeping exact information about activities that are performed.

Account receivable report: These reports are mainly generated by companies who are

providing goods or products on credit to customers and clients. It assist in getting accurate

outstanding amount of debtors (Mistry, Sharma and Low, 2014). In Oak Cash and Carry Ltd,

account receivable reports are created to calculate actual owed amount which needs to be

recovered from clients. It is mainly prepared for those clients who are not able to pay whole

amount at time of purchase but willing to pay amount later.

Importance: It is very important for company because it helps to find errors in credit

policy. It will lead managers to tighten credit policies of the company.

Financial report: Financial reports are mainly concerned with statements that may show

actual status of company and provide financial strength. It help managers to analyse that what are

the total revenues and expenses of an organisation. In Oak Cash and Carry Ltd, these reports are

generated to analyse position of company in market.

Importance: This is very important for companies because it help stakeholders to

analyse actual performance and its profitability. It is also beneficial for mangers while making

strategic decisions.

4

related activities. It helps to make supply chain more efficient by properly maintaining

information. In Oak Cash and Carry Ltd, inventory management reports are generated to

compare different distribution channels of company to find best way to supply its products.

Managers can keep a detailed information of inventory with help of these reports.

Importance: Major importance of this system is that it help managers to keep a track

record of stock while buying or supplying (Klychova, Faskhutdinova and Sadrieva, 2014). It

directs owners of business that what is quantity of products in warehouses and when to order

inventory before warehouses go empty.

Budget report: This report is generated by managers to compare estimated output and

actual performance of a company. In Oak Cash and Carry Ltd, such reports are created by

management to control and understand costs of products. It helps to estimate future expenses in

prior years so that managers may formulate strategies to deal with or resolve same.

Importance: It helps to analyse financial health and provide overview of activities that

are performed by company in whole year. Managers may monitor revenues with help of budget

reports by keeping exact information about activities that are performed.

Account receivable report: These reports are mainly generated by companies who are

providing goods or products on credit to customers and clients. It assist in getting accurate

outstanding amount of debtors (Mistry, Sharma and Low, 2014). In Oak Cash and Carry Ltd,

account receivable reports are created to calculate actual owed amount which needs to be

recovered from clients. It is mainly prepared for those clients who are not able to pay whole

amount at time of purchase but willing to pay amount later.

Importance: It is very important for company because it helps to find errors in credit

policy. It will lead managers to tighten credit policies of the company.

Financial report: Financial reports are mainly concerned with statements that may show

actual status of company and provide financial strength. It help managers to analyse that what are

the total revenues and expenses of an organisation. In Oak Cash and Carry Ltd, these reports are

generated to analyse position of company in market.

Importance: This is very important for companies because it help stakeholders to

analyse actual performance and its profitability. It is also beneficial for mangers while making

strategic decisions.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1 Integration of management accounting system and its reports in organisational process

Management accounting system and its reports help managers and internal stakeholder to

analyse performance of organisation. It provides information of cost which is involved in

distribution activities, actual owed amount by customers, financial position of company etc.

Account receivable reports can help managers to tighten credit policies by providing them

information of those customers who are not able to pay their outstanding amounts. Inventory

management reports is also assisting in management to track inventory in whole supply chain.

TASK 2

P3 Different costing techniques

Cost: Cost is the monetary value of a product that includes cost of material, overheads,

labour etc. Companies set their selling prices according to their cost because it will help them to

earn more profits (Moser, 2012). A customer who is willing to buy a product will always try to

find out that what is actual cost of that product so company should set appropriate cost for their

products, it will help them to attract more and more customers.

Oak Cash and Carry Ltd is a retail company so managers of company should set such

cost or selling prices for products that may attract more customers and help company to acquire

more market share. Cost of products include different direct and indirect expenses. Here, the

mentioned techniques are followed by managers of Oak Cash and Carry Ltd to calculate their net

profits:

Marginal costing: It is a technique which is used by companies to estimate cost of

additional unit which is added by managers in distribution channel or supply chain of company.

It includes variable cost which is going to be absorbed from sales of additional units.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

5

Management accounting system and its reports help managers and internal stakeholder to

analyse performance of organisation. It provides information of cost which is involved in

distribution activities, actual owed amount by customers, financial position of company etc.

Account receivable reports can help managers to tighten credit policies by providing them

information of those customers who are not able to pay their outstanding amounts. Inventory

management reports is also assisting in management to track inventory in whole supply chain.

TASK 2

P3 Different costing techniques

Cost: Cost is the monetary value of a product that includes cost of material, overheads,

labour etc. Companies set their selling prices according to their cost because it will help them to

earn more profits (Moser, 2012). A customer who is willing to buy a product will always try to

find out that what is actual cost of that product so company should set appropriate cost for their

products, it will help them to attract more and more customers.

Oak Cash and Carry Ltd is a retail company so managers of company should set such

cost or selling prices for products that may attract more customers and help company to acquire

more market share. Cost of products include different direct and indirect expenses. Here, the

mentioned techniques are followed by managers of Oak Cash and Carry Ltd to calculate their net

profits:

Marginal costing: It is a technique which is used by companies to estimate cost of

additional unit which is added by managers in distribution channel or supply chain of company.

It includes variable cost which is going to be absorbed from sales of additional units.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

5

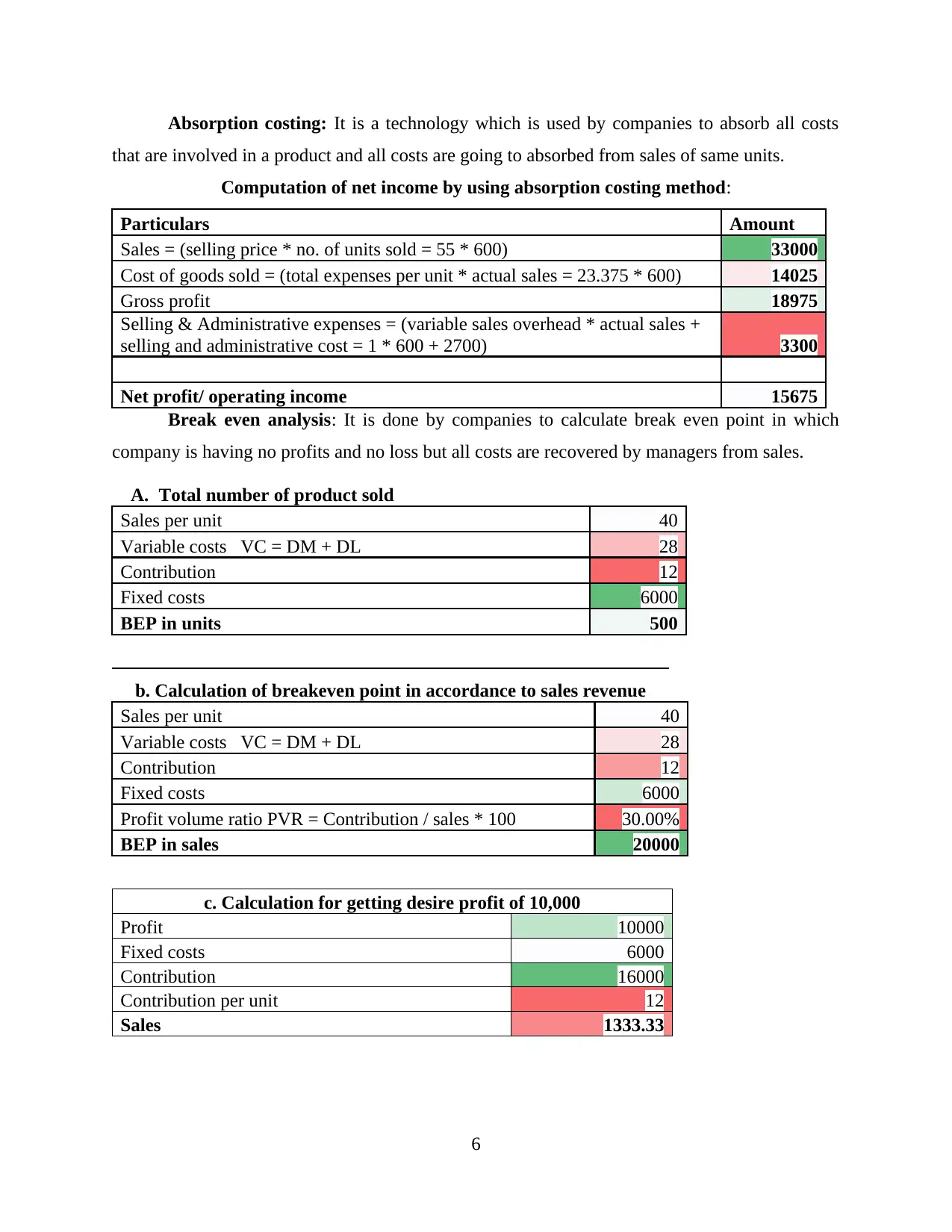

Absorption costing: It is a technology which is used by companies to absorb all costs

that are involved in a product and all costs are going to absorbed from sales of same units.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is done by companies to calculate break even point in which

company is having no profits and no loss but all costs are recovered by managers from sales.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

6

that are involved in a product and all costs are going to absorbed from sales of same units.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is done by companies to calculate break even point in which

company is having no profits and no loss but all costs are recovered by managers from sales.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

6

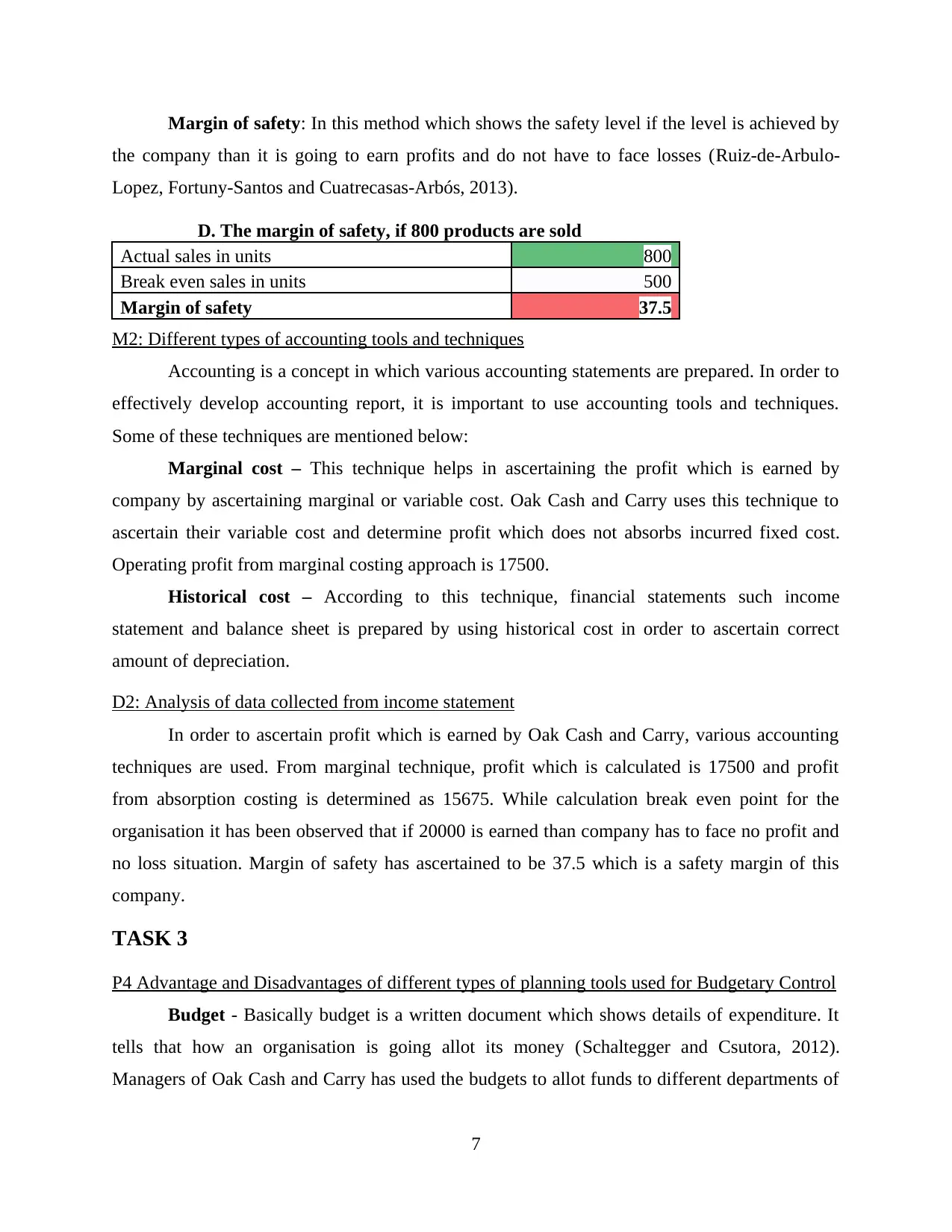

Margin of safety: In this method which shows the safety level if the level is achieved by

the company than it is going to earn profits and do not have to face losses (Ruiz-de-Arbulo-

Lopez, Fortuny-Santos and Cuatrecasas-Arbós, 2013).

D. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Different types of accounting tools and techniques

Accounting is a concept in which various accounting statements are prepared. In order to

effectively develop accounting report, it is important to use accounting tools and techniques.

Some of these techniques are mentioned below:

Marginal cost – This technique helps in ascertaining the profit which is earned by

company by ascertaining marginal or variable cost. Oak Cash and Carry uses this technique to

ascertain their variable cost and determine profit which does not absorbs incurred fixed cost.

Operating profit from marginal costing approach is 17500.

Historical cost – According to this technique, financial statements such income

statement and balance sheet is prepared by using historical cost in order to ascertain correct

amount of depreciation.

D2: Analysis of data collected from income statement

In order to ascertain profit which is earned by Oak Cash and Carry, various accounting

techniques are used. From marginal technique, profit which is calculated is 17500 and profit

from absorption costing is determined as 15675. While calculation break even point for the

organisation it has been observed that if 20000 is earned than company has to face no profit and

no loss situation. Margin of safety has ascertained to be 37.5 which is a safety margin of this

company.

TASK 3

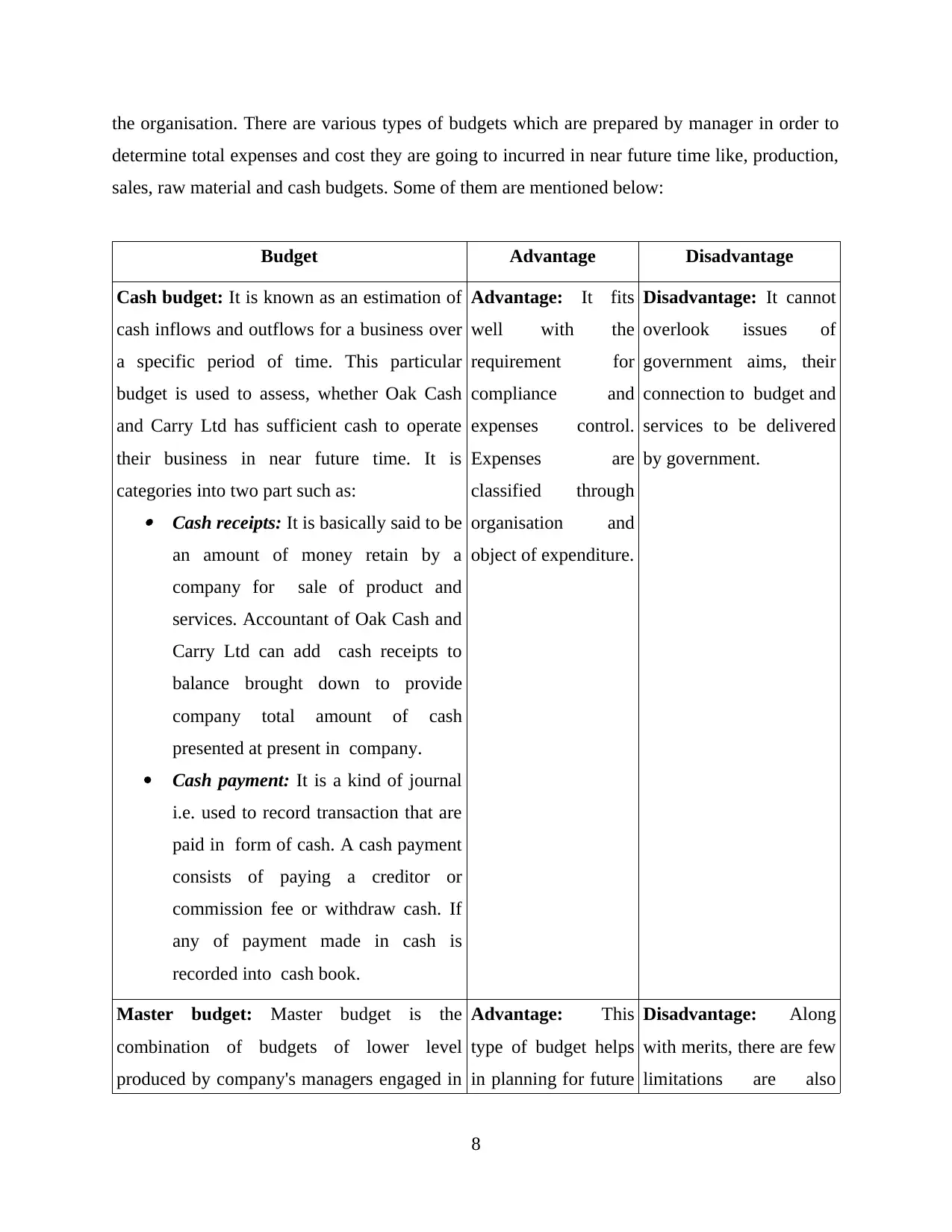

P4 Advantage and Disadvantages of different types of planning tools used for Budgetary Control

Budget - Basically budget is a written document which shows details of expenditure. It

tells that how an organisation is going allot its money (Schaltegger and Csutora, 2012).

Managers of Oak Cash and Carry has used the budgets to allot funds to different departments of

7

the company than it is going to earn profits and do not have to face losses (Ruiz-de-Arbulo-

Lopez, Fortuny-Santos and Cuatrecasas-Arbós, 2013).

D. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2: Different types of accounting tools and techniques

Accounting is a concept in which various accounting statements are prepared. In order to

effectively develop accounting report, it is important to use accounting tools and techniques.

Some of these techniques are mentioned below:

Marginal cost – This technique helps in ascertaining the profit which is earned by

company by ascertaining marginal or variable cost. Oak Cash and Carry uses this technique to

ascertain their variable cost and determine profit which does not absorbs incurred fixed cost.

Operating profit from marginal costing approach is 17500.

Historical cost – According to this technique, financial statements such income

statement and balance sheet is prepared by using historical cost in order to ascertain correct

amount of depreciation.

D2: Analysis of data collected from income statement

In order to ascertain profit which is earned by Oak Cash and Carry, various accounting

techniques are used. From marginal technique, profit which is calculated is 17500 and profit

from absorption costing is determined as 15675. While calculation break even point for the

organisation it has been observed that if 20000 is earned than company has to face no profit and

no loss situation. Margin of safety has ascertained to be 37.5 which is a safety margin of this

company.

TASK 3

P4 Advantage and Disadvantages of different types of planning tools used for Budgetary Control

Budget - Basically budget is a written document which shows details of expenditure. It

tells that how an organisation is going allot its money (Schaltegger and Csutora, 2012).

Managers of Oak Cash and Carry has used the budgets to allot funds to different departments of

7

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

the organisation. There are various types of budgets which are prepared by manager in order to

determine total expenses and cost they are going to incurred in near future time like, production,

sales, raw material and cash budgets. Some of them are mentioned below:

Budget Advantage Disadvantage

Cash budget: It is known as an estimation of

cash inflows and outflows for a business over

a specific period of time. This particular

budget is used to assess, whether Oak Cash

and Carry Ltd has sufficient cash to operate

their business in near future time. It is

categories into two part such as: Cash receipts: It is basically said to be

an amount of money retain by a

company for sale of product and

services. Accountant of Oak Cash and

Carry Ltd can add cash receipts to

balance brought down to provide

company total amount of cash

presented at present in company.

Cash payment: It is a kind of journal

i.e. used to record transaction that are

paid in form of cash. A cash payment

consists of paying a creditor or

commission fee or withdraw cash. If

any of payment made in cash is

recorded into cash book.

Advantage: It fits

well with the

requirement for

compliance and

expenses control.

Expenses are

classified through

organisation and

object of expenditure.

Disadvantage: It cannot

overlook issues of

government aims, their

connection to budget and

services to be delivered

by government.

Master budget: Master budget is the

combination of budgets of lower level

produced by company's managers engaged in

Advantage: This

type of budget helps

in planning for future

Disadvantage: Along

with merits, there are few

limitations are also

8

determine total expenses and cost they are going to incurred in near future time like, production,

sales, raw material and cash budgets. Some of them are mentioned below:

Budget Advantage Disadvantage

Cash budget: It is known as an estimation of

cash inflows and outflows for a business over

a specific period of time. This particular

budget is used to assess, whether Oak Cash

and Carry Ltd has sufficient cash to operate

their business in near future time. It is

categories into two part such as: Cash receipts: It is basically said to be

an amount of money retain by a

company for sale of product and

services. Accountant of Oak Cash and

Carry Ltd can add cash receipts to

balance brought down to provide

company total amount of cash

presented at present in company.

Cash payment: It is a kind of journal

i.e. used to record transaction that are

paid in form of cash. A cash payment

consists of paying a creditor or

commission fee or withdraw cash. If

any of payment made in cash is

recorded into cash book.

Advantage: It fits

well with the

requirement for

compliance and

expenses control.

Expenses are

classified through

organisation and

object of expenditure.

Disadvantage: It cannot

overlook issues of

government aims, their

connection to budget and

services to be delivered

by government.

Master budget: Master budget is the

combination of budgets of lower level

produced by company's managers engaged in

Advantage: This

type of budget helps

in planning for future

Disadvantage: Along

with merits, there are few

limitations are also

8

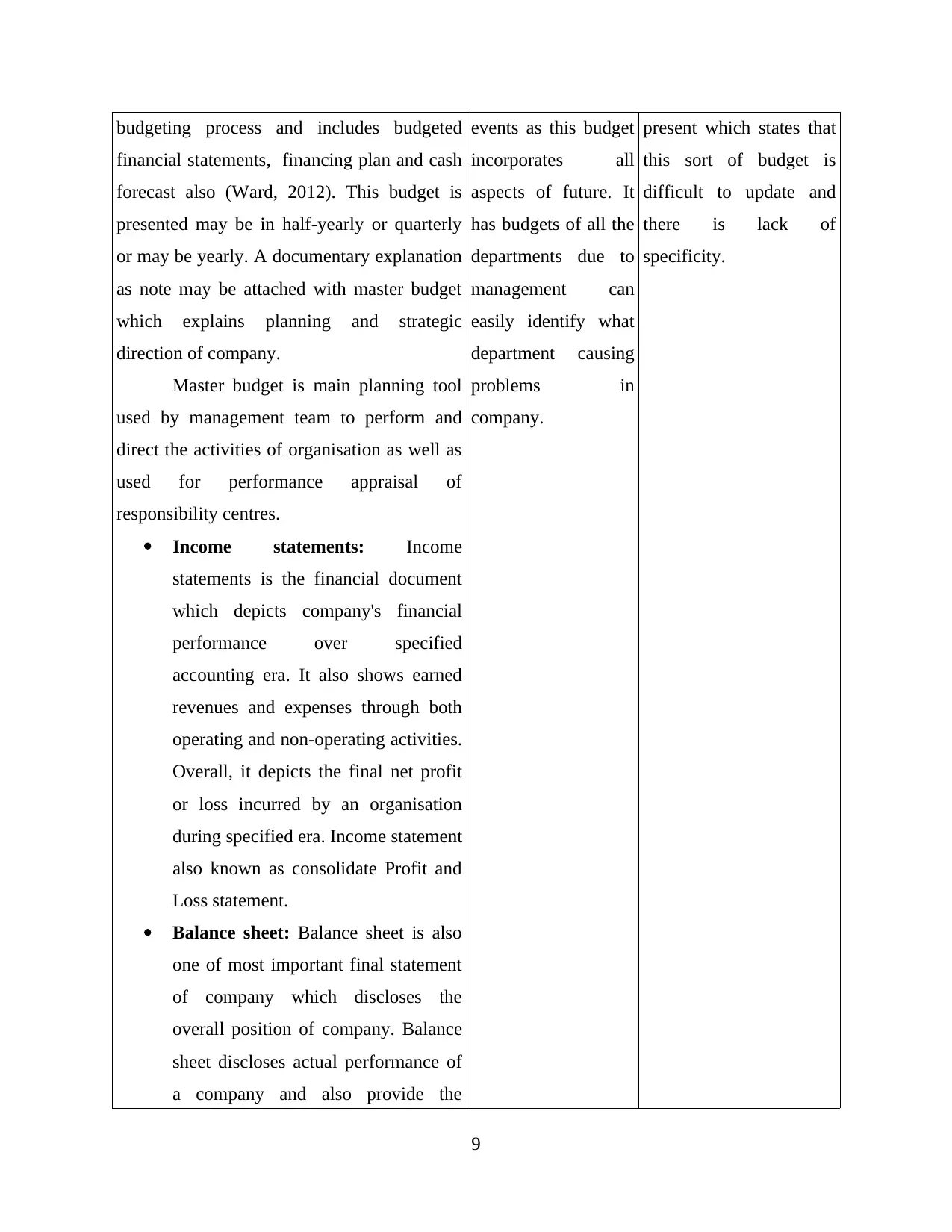

budgeting process and includes budgeted

financial statements, financing plan and cash

forecast also (Ward, 2012). This budget is

presented may be in half-yearly or quarterly

or may be yearly. A documentary explanation

as note may be attached with master budget

which explains planning and strategic

direction of company.

Master budget is main planning tool

used by management team to perform and

direct the activities of organisation as well as

used for performance appraisal of

responsibility centres.

Income statements: Income

statements is the financial document

which depicts company's financial

performance over specified

accounting era. It also shows earned

revenues and expenses through both

operating and non-operating activities.

Overall, it depicts the final net profit

or loss incurred by an organisation

during specified era. Income statement

also known as consolidate Profit and

Loss statement.

Balance sheet: Balance sheet is also

one of most important final statement

of company which discloses the

overall position of company. Balance

sheet discloses actual performance of

a company and also provide the

events as this budget

incorporates all

aspects of future. It

has budgets of all the

departments due to

management can

easily identify what

department causing

problems in

company.

present which states that

this sort of budget is

difficult to update and

there is lack of

specificity.

9

financial statements, financing plan and cash

forecast also (Ward, 2012). This budget is

presented may be in half-yearly or quarterly

or may be yearly. A documentary explanation

as note may be attached with master budget

which explains planning and strategic

direction of company.

Master budget is main planning tool

used by management team to perform and

direct the activities of organisation as well as

used for performance appraisal of

responsibility centres.

Income statements: Income

statements is the financial document

which depicts company's financial

performance over specified

accounting era. It also shows earned

revenues and expenses through both

operating and non-operating activities.

Overall, it depicts the final net profit

or loss incurred by an organisation

during specified era. Income statement

also known as consolidate Profit and

Loss statement.

Balance sheet: Balance sheet is also

one of most important final statement

of company which discloses the

overall position of company. Balance

sheet discloses actual performance of

a company and also provide the

events as this budget

incorporates all

aspects of future. It

has budgets of all the

departments due to

management can

easily identify what

department causing

problems in

company.

present which states that

this sort of budget is

difficult to update and

there is lack of

specificity.

9

information of available financial

resources. There are two parts of

balance sheet one is assets part which

shows the values of total current

assets and total non- current assets.

Second part shows information about

liabilities as well as total shareholders

equity.

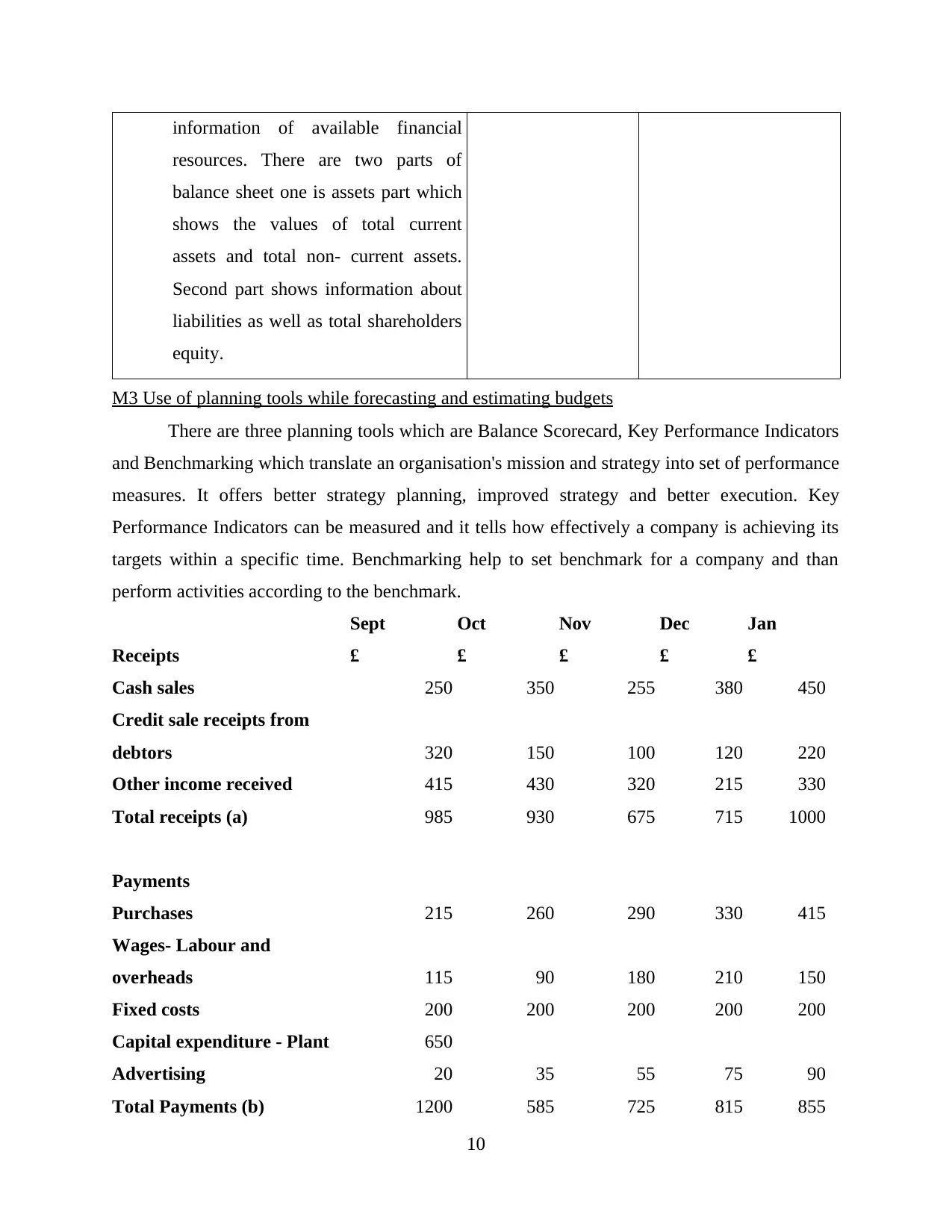

M3 Use of planning tools while forecasting and estimating budgets

There are three planning tools which are Balance Scorecard, Key Performance Indicators

and Benchmarking which translate an organisation's mission and strategy into set of performance

measures. It offers better strategy planning, improved strategy and better execution. Key

Performance Indicators can be measured and it tells how effectively a company is achieving its

targets within a specific time. Benchmarking help to set benchmark for a company and than

perform activities according to the benchmark.

Sept Oct Nov Dec Jan

Receipts £ £ £ £ £

Cash sales 250 350 255 380 450

Credit sale receipts from

debtors 320 150 100 120 220

Other income received 415 430 320 215 330

Total receipts (a) 985 930 675 715 1000

Payments

Purchases 215 260 290 330 415

Wages- Labour and

overheads 115 90 180 210 150

Fixed costs 200 200 200 200 200

Capital expenditure - Plant 650

Advertising 20 35 55 75 90

Total Payments (b) 1200 585 725 815 855

10

resources. There are two parts of

balance sheet one is assets part which

shows the values of total current

assets and total non- current assets.

Second part shows information about

liabilities as well as total shareholders

equity.

M3 Use of planning tools while forecasting and estimating budgets

There are three planning tools which are Balance Scorecard, Key Performance Indicators

and Benchmarking which translate an organisation's mission and strategy into set of performance

measures. It offers better strategy planning, improved strategy and better execution. Key

Performance Indicators can be measured and it tells how effectively a company is achieving its

targets within a specific time. Benchmarking help to set benchmark for a company and than

perform activities according to the benchmark.

Sept Oct Nov Dec Jan

Receipts £ £ £ £ £

Cash sales 250 350 255 380 450

Credit sale receipts from

debtors 320 150 100 120 220

Other income received 415 430 320 215 330

Total receipts (a) 985 930 675 715 1000

Payments

Purchases 215 260 290 330 415

Wages- Labour and

overheads 115 90 180 210 150

Fixed costs 200 200 200 200 200

Capital expenditure - Plant 650

Advertising 20 35 55 75 90

Total Payments (b) 1200 585 725 815 855

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

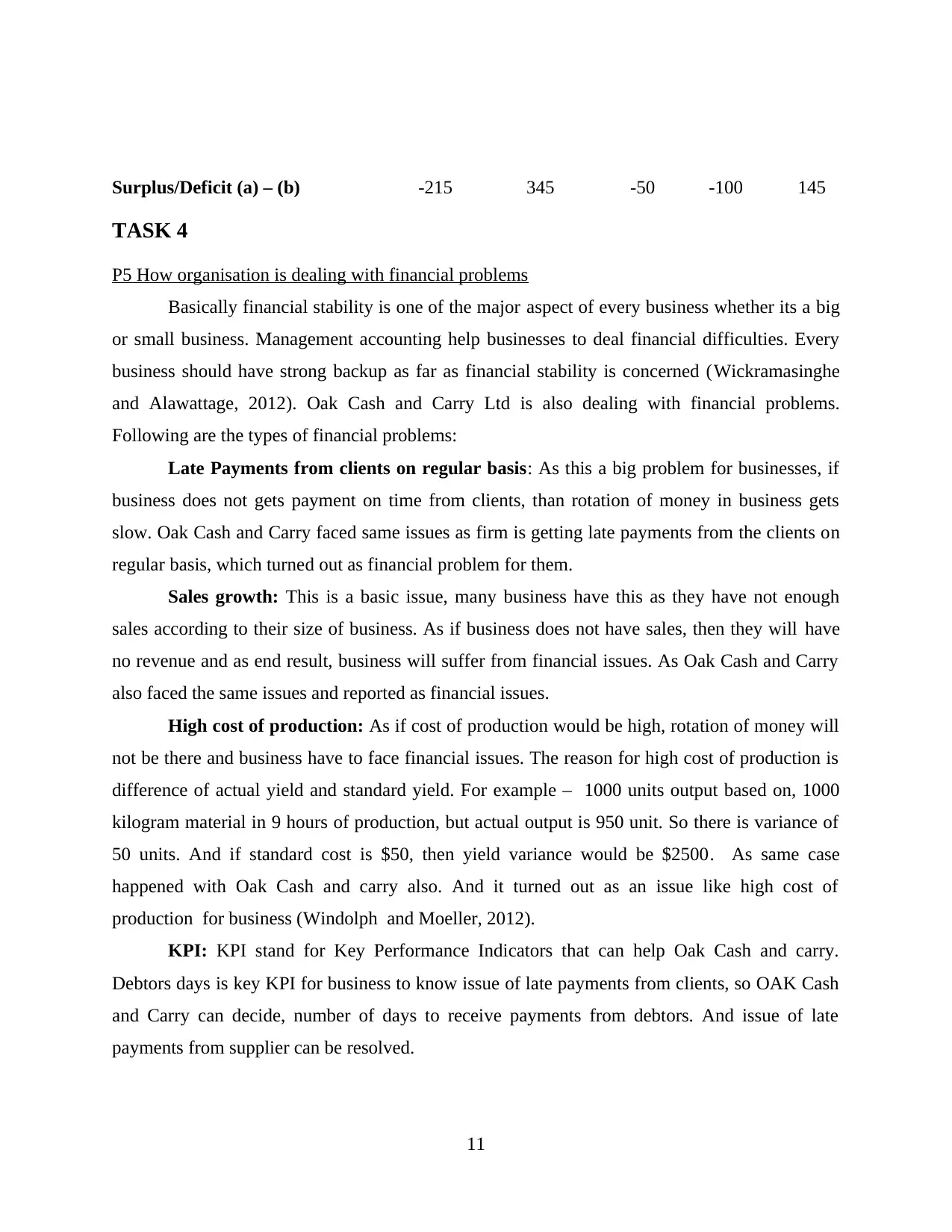

Surplus/Deficit (a) – (b) -215 345 -50 -100 145

TASK 4

P5 How organisation is dealing with financial problems

Basically financial stability is one of the major aspect of every business whether its a big

or small business. Management accounting help businesses to deal financial difficulties. Every

business should have strong backup as far as financial stability is concerned (Wickramasinghe

and Alawattage, 2012). Oak Cash and Carry Ltd is also dealing with financial problems.

Following are the types of financial problems:

Late Payments from clients on regular basis: As this a big problem for businesses, if

business does not gets payment on time from clients, than rotation of money in business gets

slow. Oak Cash and Carry faced same issues as firm is getting late payments from the clients on

regular basis, which turned out as financial problem for them.

Sales growth: This is a basic issue, many business have this as they have not enough

sales according to their size of business. As if business does not have sales, then they will have

no revenue and as end result, business will suffer from financial issues. As Oak Cash and Carry

also faced the same issues and reported as financial issues.

High cost of production: As if cost of production would be high, rotation of money will

not be there and business have to face financial issues. The reason for high cost of production is

difference of actual yield and standard yield. For example – 1000 units output based on, 1000

kilogram material in 9 hours of production, but actual output is 950 unit. So there is variance of

50 units. And if standard cost is $50, then yield variance would be $2500. As same case

happened with Oak Cash and carry also. And it turned out as an issue like high cost of

production for business (Windolph and Moeller, 2012).

KPI: KPI stand for Key Performance Indicators that can help Oak Cash and carry.

Debtors days is key KPI for business to know issue of late payments from clients, so OAK Cash

and Carry can decide, number of days to receive payments from debtors. And issue of late

payments from supplier can be resolved.

11

TASK 4

P5 How organisation is dealing with financial problems

Basically financial stability is one of the major aspect of every business whether its a big

or small business. Management accounting help businesses to deal financial difficulties. Every

business should have strong backup as far as financial stability is concerned (Wickramasinghe

and Alawattage, 2012). Oak Cash and Carry Ltd is also dealing with financial problems.

Following are the types of financial problems:

Late Payments from clients on regular basis: As this a big problem for businesses, if

business does not gets payment on time from clients, than rotation of money in business gets

slow. Oak Cash and Carry faced same issues as firm is getting late payments from the clients on

regular basis, which turned out as financial problem for them.

Sales growth: This is a basic issue, many business have this as they have not enough

sales according to their size of business. As if business does not have sales, then they will have

no revenue and as end result, business will suffer from financial issues. As Oak Cash and Carry

also faced the same issues and reported as financial issues.

High cost of production: As if cost of production would be high, rotation of money will

not be there and business have to face financial issues. The reason for high cost of production is

difference of actual yield and standard yield. For example – 1000 units output based on, 1000

kilogram material in 9 hours of production, but actual output is 950 unit. So there is variance of

50 units. And if standard cost is $50, then yield variance would be $2500. As same case

happened with Oak Cash and carry also. And it turned out as an issue like high cost of

production for business (Windolph and Moeller, 2012).

KPI: KPI stand for Key Performance Indicators that can help Oak Cash and carry.

Debtors days is key KPI for business to know issue of late payments from clients, so OAK Cash

and Carry can decide, number of days to receive payments from debtors. And issue of late

payments from supplier can be resolved.

11

Balance scorecard: Balance Score Card can help Oak Cash and Carry to grow their

sales. Financial perspective of Balance Scorecard depicts that if any business work on lower cost,

more sales policy (Zainun Tuanmat and Smith, 2011). It can help business to grow sales and if

sales will be more, then similarly revenue will be more. And issue of sales growth can be solve.

Benchmarking: Benchmarking is best solution for issues of high cost of production. As

a standard quantity is set for production, in actual yield if it goes below from set benchmark then

cost of production for per unit will be high, because yield is not according to set benchmark. As

for example – 1000 units output based on, 1000 kilogram material in 9 hours of production, but

actual output is 950 unit. So there is variance of 50 units. And if standard cost is $50, then yield

variance would be $2500. And if benchmark would used there, then material would be used

according to 950 units. So there would not be any yield variance.

Oak Cash and Carry Agmet Chemical

As this company used Key Performance

Indicators tools to solve issue of late payments

from clients. As through this they set specific

time for debtors to make payments in given

time.

This spend less money on raw materials, they

just buy enough resources to make ordered

products.

As this use Balance Scorecard for the boosting

sales, as Balance Scorecard financial

prospective say, low more, more revenue.

This use Just in Time, according to them, one

should focus on primary task like making

goods to interacting with customers, rather

than stocking the material

To avoid high cost of product, they use

Benchmarking as it sets standard before

production and then it compare to actual yield.

Through comparison of actual and standard

yield, difference would be known to company.

As company does not need to store raw

material for production, as Just In Time

concept tells to order material when it needed.

So company does not need to keep material in

warehouses, so cost warehousing can be

minimized through this concept.

M4 How planning tools help to deal financial problems

Planning tools like cash budget and master budget help Oak Cash and Carry Ltd to

resolve financial issues by properly maintaining its monetary funds so that there is not lack of

12

sales. Financial perspective of Balance Scorecard depicts that if any business work on lower cost,

more sales policy (Zainun Tuanmat and Smith, 2011). It can help business to grow sales and if

sales will be more, then similarly revenue will be more. And issue of sales growth can be solve.

Benchmarking: Benchmarking is best solution for issues of high cost of production. As

a standard quantity is set for production, in actual yield if it goes below from set benchmark then

cost of production for per unit will be high, because yield is not according to set benchmark. As

for example – 1000 units output based on, 1000 kilogram material in 9 hours of production, but

actual output is 950 unit. So there is variance of 50 units. And if standard cost is $50, then yield

variance would be $2500. And if benchmark would used there, then material would be used

according to 950 units. So there would not be any yield variance.

Oak Cash and Carry Agmet Chemical

As this company used Key Performance

Indicators tools to solve issue of late payments

from clients. As through this they set specific

time for debtors to make payments in given

time.

This spend less money on raw materials, they

just buy enough resources to make ordered

products.

As this use Balance Scorecard for the boosting

sales, as Balance Scorecard financial

prospective say, low more, more revenue.

This use Just in Time, according to them, one

should focus on primary task like making

goods to interacting with customers, rather

than stocking the material

To avoid high cost of product, they use

Benchmarking as it sets standard before

production and then it compare to actual yield.

Through comparison of actual and standard

yield, difference would be known to company.

As company does not need to store raw

material for production, as Just In Time

concept tells to order material when it needed.

So company does not need to keep material in

warehouses, so cost warehousing can be

minimized through this concept.

M4 How planning tools help to deal financial problems

Planning tools like cash budget and master budget help Oak Cash and Carry Ltd to

resolve financial issues by properly maintaining its monetary funds so that there is not lack of

12

such resources. It will help company to possibility of financial problems. In this way, it will help

to respond financial problems appropriately, with help of planning tools like cash budget and

master budget.

D3 Planning tools for solving financial issues

The managers of Oak Cash and Carry have used three different tools to resolve financial

issues which are balance scorecard, benchmarking and KPI. Key performance Indicators helps to

financial issues of business of Oak Cash and Carry Ltd used to eliminate late payments from

clients. As Oak Cash and carry Ltd used Benchmarking to removes high cost of production

through setting up benchmarks.

CONCLUSIONS

From above project report it has been concluded that management accounting can help

managers while dealing with financial problems. It can help internal stakeholder to analyse

actual performance of company as well as level of operational activities of a company. Planning

tools can help to forecast and estimate budgets by analysing possible future expenses.

Management accounting help internal stakeholders to analyse performance and position of the

company.

13

to respond financial problems appropriately, with help of planning tools like cash budget and

master budget.

D3 Planning tools for solving financial issues

The managers of Oak Cash and Carry have used three different tools to resolve financial

issues which are balance scorecard, benchmarking and KPI. Key performance Indicators helps to

financial issues of business of Oak Cash and Carry Ltd used to eliminate late payments from

clients. As Oak Cash and carry Ltd used Benchmarking to removes high cost of production

through setting up benchmarks.

CONCLUSIONS

From above project report it has been concluded that management accounting can help

managers while dealing with financial problems. It can help internal stakeholder to analyse

actual performance of company as well as level of operational activities of a company. Planning

tools can help to forecast and estimate budgets by analysing possible future expenses.

Management accounting help internal stakeholders to analyse performance and position of the

company.

13

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journal:

Amidu, M., Effah, J. and Abor, J., 2011. E-accounting practices among small and medium

enterprises in Ghana. Journal of Management Policy and Practice. 12(4). pp.146-155.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Dražić Lutilsky, I. and Dragija, M., 2012. Activity based costing as a means to full costing–

possibilities and constraints for European universities. Management: Journal of

contemporary management issues. 17(1). pp.33-57.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Johnson, H. T., 2013. A New Approach to Management Accounting History (RLE Accounting).

Routledge.

JOSHI, P. L. and et. al., 2011. Diffusion of management accounting practices in gulf cooperation

council countries. Accounting Perspectives. 10(1). pp.23-53.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E.R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences. 5(24). p.79.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Moser, D. V., 2012. Is accounting research stagnant ?. Accounting Horizons. 26(4). pp.845-850.

Ruiz-de-Arbulo-Lopez, P., Fortuny-Santos, J. and Cuatrecasas-Arbós, L., 2013. Lean

manufacturing: costing the value stream. Industrial Management & Data

Systems. 113(5). pp.647-668.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Zainun Tuanmat, T. and Smith, M., 2011. Changes in management accounting practices in

Malaysia. Asian Review of Accounting. 19(3). pp.221-242.

Online

Management accounting. 2018. [Online]. Available through:

<https://www.invensis.net/blog/finance-and-accounting/what-is-management-accounting-

and-its-importance/>

14

Books and Journal:

Amidu, M., Effah, J. and Abor, J., 2011. E-accounting practices among small and medium

enterprises in Ghana. Journal of Management Policy and Practice. 12(4). pp.146-155.

Carlsson-Wall, M., Kraus, K. and Lind, J., 2015. Strategic management accounting in close

inter-organisational relationships. Accounting and Business Research. 45(1). pp.27-54.

Dražić Lutilsky, I. and Dragija, M., 2012. Activity based costing as a means to full costing–

possibilities and constraints for European universities. Management: Journal of

contemporary management issues. 17(1). pp.33-57.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Johnson, H. T., 2013. A New Approach to Management Accounting History (RLE Accounting).

Routledge.

JOSHI, P. L. and et. al., 2011. Diffusion of management accounting practices in gulf cooperation

council countries. Accounting Perspectives. 10(1). pp.23-53.

Klychova, G. S., Faskhutdinova, М. S. and Sadrieva, E.R., 2014. Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences. 5(24). p.79.

Mistry, V., Sharma, U. and Low, M., 2014. Management accountants' perception of their role in

accounting for sustainable development: An exploratory study. Pacific Accounting

Review. 26(1/2). pp.112-133.

Moser, D. V., 2012. Is accounting research stagnant ?. Accounting Horizons. 26(4). pp.845-850.

Ruiz-de-Arbulo-Lopez, P., Fortuny-Santos, J. and Cuatrecasas-Arbós, L., 2013. Lean

manufacturing: costing the value stream. Industrial Management & Data

Systems. 113(5). pp.647-668.

Schaltegger, S. and Csutora, M., 2012. Carbon accounting for sustainability and management.

Status quo and challenges. Journal of Cleaner Production. 36. pp.1-16.

Ward, K., 2012. Strategic management accounting. Routledge.

Wickramasinghe, D. and Alawattage, C., 2012. Management accounting change: approaches

and perspectives. Routledge.

Windolph, M. and Moeller, K., 2012. Open-book accounting: Reason for failure of inter-firm

cooperation?. Management Accounting Research. 23(1). pp.47-60.

Zainun Tuanmat, T. and Smith, M., 2011. Changes in management accounting practices in

Malaysia. Asian Review of Accounting. 19(3). pp.221-242.

Online

Management accounting. 2018. [Online]. Available through:

<https://www.invensis.net/blog/finance-and-accounting/what-is-management-accounting-

and-its-importance/>

14

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.