Management Accounting Innovations

VerifiedAdded on 2020/01/07

|14

|4358

|149

Essay

AI Summary

This assignment delves into the field of management accounting research, examining recent developments and innovations. It analyzes various perspectives on the topic, including social and environmental accounting, organizational change, and management control practices in lean manufacturing environments. The assignment encourages critical thinking about the roles and effects of paradigms in accounting research and highlights the practical relevance of these findings for management practitioners.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................4

P1 Management accounting and its functions.............................................................................4

P2 Types of management accounting system.............................................................................6

TASK 2............................................................................................................................................7

P3 Income statement using absorption costing and marginal costing methods..........................7

TASK 3............................................................................................................................................9

P4 a) Types of budgets................................................................................................................9

b) Process of budget preparation...............................................................................................10

c) Pricing strategies...................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Explain what a Balance Score Card approach is and its implementation...........................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1 ...........................................................................................................................................4

P1 Management accounting and its functions.............................................................................4

P2 Types of management accounting system.............................................................................6

TASK 2............................................................................................................................................7

P3 Income statement using absorption costing and marginal costing methods..........................7

TASK 3............................................................................................................................................9

P4 a) Types of budgets................................................................................................................9

b) Process of budget preparation...............................................................................................10

c) Pricing strategies...................................................................................................................11

TASK 4..........................................................................................................................................11

P5 Explain what a Balance Score Card approach is and its implementation...........................11

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting can be defined as the allocation of financial data and direction

to a particular company for its use which will also be helpful in the business development.

Finance is the blood of any firm, which helps the entity to grow successfully in the market, and

for the proper management of finance it is necessary to prepare management accounting report

(Ward, 2012). This report is based on the case study of Imda Tech (UK), who are the producers

of mobile phone chargers and other gadgets. In this report various functions of management

accounting, its types and methods, budgeting methods will be discussed. Income statement for

the Imda Tech will be prepared in this report. Income statement can be defined as the financial

statement, that helps in analysing financial performance of the company in a particular

accounting period. Financial performance is analysed with the help of summary, which shows

how business incurs its expenses and revenues through non-operating and operating activities.

TASK 1

P1 Management accounting and its functions

Managerial accounting or management accounting can be referred as the process of

analysing, identifying, presenting and recording financial information which is used by the

internal departments or management for the process of decision making, planning and control. In

contrast to the financial accounting, management accounting is relation with such activities

which provide necessary information and reports to the internal users like entrepreneurs,

managers etc. so that they can plan and control activities of business (Define Management

Accounting. What are its objectives. 2016).

Difference between management accounting and financial accounting

Financial Accounting Management Accounting

It is in a specific format which is given by

international accounting standards, in order to

compare the financial accounts of various

firms.

There is no particular format for the system of

management accounting.

Financial accounting is helpful for decision

making, investment making and in-credit

Management accounting is helpful in planning,

recording and controlling activities in order to

Management accounting can be defined as the allocation of financial data and direction

to a particular company for its use which will also be helpful in the business development.

Finance is the blood of any firm, which helps the entity to grow successfully in the market, and

for the proper management of finance it is necessary to prepare management accounting report

(Ward, 2012). This report is based on the case study of Imda Tech (UK), who are the producers

of mobile phone chargers and other gadgets. In this report various functions of management

accounting, its types and methods, budgeting methods will be discussed. Income statement for

the Imda Tech will be prepared in this report. Income statement can be defined as the financial

statement, that helps in analysing financial performance of the company in a particular

accounting period. Financial performance is analysed with the help of summary, which shows

how business incurs its expenses and revenues through non-operating and operating activities.

TASK 1

P1 Management accounting and its functions

Managerial accounting or management accounting can be referred as the process of

analysing, identifying, presenting and recording financial information which is used by the

internal departments or management for the process of decision making, planning and control. In

contrast to the financial accounting, management accounting is relation with such activities

which provide necessary information and reports to the internal users like entrepreneurs,

managers etc. so that they can plan and control activities of business (Define Management

Accounting. What are its objectives. 2016).

Difference between management accounting and financial accounting

Financial Accounting Management Accounting

It is in a specific format which is given by

international accounting standards, in order to

compare the financial accounts of various

firms.

There is no particular format for the system of

management accounting.

Financial accounting is helpful for decision

making, investment making and in-credit

Management accounting is helpful in planning,

recording and controlling activities in order to

ratings. help in the process of decision making.

Information which is produced by financial

accounting is useful for the external users like

bank, shareholders and creditors (Vaivio and

Sirén, 2010).

Information which is developed by

management accounting is useful for internal

users like employees and mangers.

Main focus of financial accounting is on

history.

Management accounting's main focus is on

future.

Financial accounting reports are prepared by

the department of finance.

Management accounting reports are created

with the coordination of each and every

department in an organisation.

Importance of management accounting in decision making

Management accounting is very helpful in the process of strategic planning. When Imda

Tech is looking for making strategic decisions, for instance, development of the new product,

expansion of business in other countries, acquiring other business, for all such decisions CIMA

trained accountant will help in providing advice. Various tools can also be used which will be

helpful in the process of decision making, these can be like ratio analysis, forecasts (like variance

and cash flows) and budgets. Ratio analysis: It is helpful in the evaluation of the different aspects related to

company's financial and operating performance like liquidity, profitability, efficiency

and solvency. Trends of these ratios are checked from time to time to know whether they

are deteriorating or improving. Forecasts: It can be done with the help of variance analysis and cash flow analysis.

Variance analysis can be defined as the quantitative investigation regarding difference

between planned and actual behaviour. It is also done for maintaining control over

business. Cash flow analysis helps in analysing cash inflow and outflow of the Imda

Tech.

Budgets: It can be termed as the quantitative expression of the financial plan for a

particular time. It includes planned revenues and sales volumes, costs and expenses,

liabilities, cash flows and assets (What is Budgetary control?. 2017).

Functions of management accounting

Information which is produced by financial

accounting is useful for the external users like

bank, shareholders and creditors (Vaivio and

Sirén, 2010).

Information which is developed by

management accounting is useful for internal

users like employees and mangers.

Main focus of financial accounting is on

history.

Management accounting's main focus is on

future.

Financial accounting reports are prepared by

the department of finance.

Management accounting reports are created

with the coordination of each and every

department in an organisation.

Importance of management accounting in decision making

Management accounting is very helpful in the process of strategic planning. When Imda

Tech is looking for making strategic decisions, for instance, development of the new product,

expansion of business in other countries, acquiring other business, for all such decisions CIMA

trained accountant will help in providing advice. Various tools can also be used which will be

helpful in the process of decision making, these can be like ratio analysis, forecasts (like variance

and cash flows) and budgets. Ratio analysis: It is helpful in the evaluation of the different aspects related to

company's financial and operating performance like liquidity, profitability, efficiency

and solvency. Trends of these ratios are checked from time to time to know whether they

are deteriorating or improving. Forecasts: It can be done with the help of variance analysis and cash flow analysis.

Variance analysis can be defined as the quantitative investigation regarding difference

between planned and actual behaviour. It is also done for maintaining control over

business. Cash flow analysis helps in analysing cash inflow and outflow of the Imda

Tech.

Budgets: It can be termed as the quantitative expression of the financial plan for a

particular time. It includes planned revenues and sales volumes, costs and expenses,

liabilities, cash flows and assets (What is Budgetary control?. 2017).

Functions of management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Planning: Management accounting helps in the long term and short term plans of the

Imda Tech, which helps in achieving targets. It helps in planning by giving reports which

helps in estimating impact of alternative actions on firm's ability for achieving goals. Organising: It is process for maintaining organisational framework and giving various

responsibilities to people who are working in an entity. Management accounting helps

managers in the process of organising by providing necessary information and reports

regarding activities and operations. Controlling: It is process of monitoring, evaluating, correcting and measuring results to

make sure that plans and goals are achieved. Management accounting is helpful in the

process of controlling by creating control and performance reports (Ward, 2012).

Decision making: It is the process to make choice among different competing

alternatives. Management accounting contains valuable information which helps in

predicting results regarding different course of action.

P2 Types of management accounting system

Management accounting system helps in the collection of financial data from the various

business operations and activities like sales data, inventory shift and change in the cost of raw

material, and then converts the information into the analysis reports. There are various systems

under the management accounting system, which can be explained as follows: Cost accounting systems: It is the type of framework which is used by Imda Tech, in

order to estimate the products cost for inventory valuation, profitability analysis and cost

control. Mentioned entity must know about their products which are profitable and which

are not. This can be done by estimating correct product cost (Vaivio and Sirén, 2010). A

product costing system also helps in the estimation of the closing value of inventory,

finished goods inventory and work in progress in order to prepare financial statement.

There are two important cost accounting systems which are job order costing and process

costing. Job order costing is that system which accumulates producing cost for each job

separately. It sis necessary for such firms who are engaged in the process of production.

Process costing also involves producing cost separately. It is important for such products,

in which there is an involvement of different departments for the process of production. Inventory management system: It is the type of system which is used by the firms in

order to track level of inventory, sales, deliveries and orders (ter Bogt and van Helden,

Imda Tech, which helps in achieving targets. It helps in planning by giving reports which

helps in estimating impact of alternative actions on firm's ability for achieving goals. Organising: It is process for maintaining organisational framework and giving various

responsibilities to people who are working in an entity. Management accounting helps

managers in the process of organising by providing necessary information and reports

regarding activities and operations. Controlling: It is process of monitoring, evaluating, correcting and measuring results to

make sure that plans and goals are achieved. Management accounting is helpful in the

process of controlling by creating control and performance reports (Ward, 2012).

Decision making: It is the process to make choice among different competing

alternatives. Management accounting contains valuable information which helps in

predicting results regarding different course of action.

P2 Types of management accounting system

Management accounting system helps in the collection of financial data from the various

business operations and activities like sales data, inventory shift and change in the cost of raw

material, and then converts the information into the analysis reports. There are various systems

under the management accounting system, which can be explained as follows: Cost accounting systems: It is the type of framework which is used by Imda Tech, in

order to estimate the products cost for inventory valuation, profitability analysis and cost

control. Mentioned entity must know about their products which are profitable and which

are not. This can be done by estimating correct product cost (Vaivio and Sirén, 2010). A

product costing system also helps in the estimation of the closing value of inventory,

finished goods inventory and work in progress in order to prepare financial statement.

There are two important cost accounting systems which are job order costing and process

costing. Job order costing is that system which accumulates producing cost for each job

separately. It sis necessary for such firms who are engaged in the process of production.

Process costing also involves producing cost separately. It is important for such products,

in which there is an involvement of different departments for the process of production. Inventory management system: It is the type of system which is used by the firms in

order to track level of inventory, sales, deliveries and orders (ter Bogt and van Helden,

2012). It is used by the manufacturing firms so as to make work orders, production

documents and material bills. Inventory management system helps to avoid product

outages and overstock. It is a tool which helps in organising data of inventory. It is

helpful for Imda Tech in order management, service management, asset tracking,

inventory optimization and product identification. Job costing system: It is process used for the accumulation of information regarding cost

which is associated with service job or production. This kind of information may be

required for submitting information related to cost to a customer under the contract where

there is reimbursement of cost. The information also helps in determining accuracy

regarding estimating system of company. It provides necessary information regarding

direct material, direct labor and overhead (Quinn, 2011).

Price optimising systems: It is the kind of mathematical analysis which is being done by

Imda Tech in order to determine how customers are going to respond to several prices

regarding services and products through several channels. It also helps in determining the

prices which are determined by company in order to meet targets like maximisation of

operating profit.

There are various benefits of management accounting which is very helpful for Imda

Tech. It helps in the management of company's financial accounts and statements. It also helps in

the process of decision making, as it assist in short and long term planning. Company can create

accurate and exact financial information with the help of budgeting and forecasting.

According to Merchant (2012), there are four management accounting system like system

of cost accounting, job costing, inventory management and price optimisation. These systems

provides help in the management of financial information and data of Imda Tech. Pipan and

Czarniawska (2010) says that these management accounting system also helps in determining

objectives and goals and performance management.

TASK 2

P3 Income statement using absorption costing and marginal costing methods

Imda Tech can calculate its net profit with the help of different techniques and methods

used in management accounting. Net profit of the mentioned entity according to the marginal

and absorption costing methods is described as follows:

documents and material bills. Inventory management system helps to avoid product

outages and overstock. It is a tool which helps in organising data of inventory. It is

helpful for Imda Tech in order management, service management, asset tracking,

inventory optimization and product identification. Job costing system: It is process used for the accumulation of information regarding cost

which is associated with service job or production. This kind of information may be

required for submitting information related to cost to a customer under the contract where

there is reimbursement of cost. The information also helps in determining accuracy

regarding estimating system of company. It provides necessary information regarding

direct material, direct labor and overhead (Quinn, 2011).

Price optimising systems: It is the kind of mathematical analysis which is being done by

Imda Tech in order to determine how customers are going to respond to several prices

regarding services and products through several channels. It also helps in determining the

prices which are determined by company in order to meet targets like maximisation of

operating profit.

There are various benefits of management accounting which is very helpful for Imda

Tech. It helps in the management of company's financial accounts and statements. It also helps in

the process of decision making, as it assist in short and long term planning. Company can create

accurate and exact financial information with the help of budgeting and forecasting.

According to Merchant (2012), there are four management accounting system like system

of cost accounting, job costing, inventory management and price optimisation. These systems

provides help in the management of financial information and data of Imda Tech. Pipan and

Czarniawska (2010) says that these management accounting system also helps in determining

objectives and goals and performance management.

TASK 2

P3 Income statement using absorption costing and marginal costing methods

Imda Tech can calculate its net profit with the help of different techniques and methods

used in management accounting. Net profit of the mentioned entity according to the marginal

and absorption costing methods is described as follows:

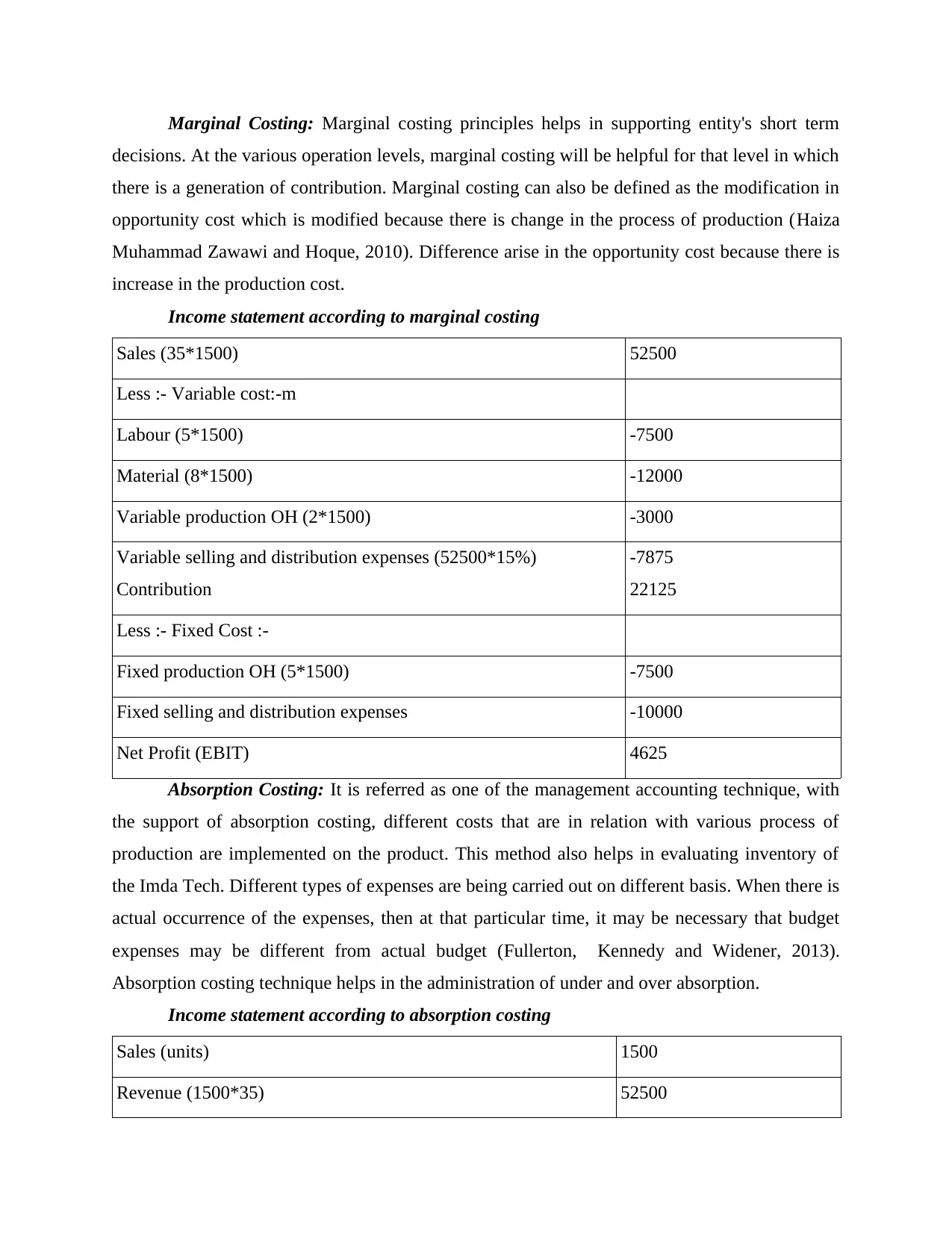

Marginal Costing: Marginal costing principles helps in supporting entity's short term

decisions. At the various operation levels, marginal costing will be helpful for that level in which

there is a generation of contribution. Marginal costing can also be defined as the modification in

opportunity cost which is modified because there is change in the process of production (Haiza

Muhammad Zawawi and Hoque, 2010). Difference arise in the opportunity cost because there is

increase in the production cost.

Income statement according to marginal costing

Sales (35*1500) 52500

Less :- Variable cost:-m

Labour (5*1500) -7500

Material (8*1500) -12000

Variable production OH (2*1500) -3000

Variable selling and distribution expenses (52500*15%)

Contribution

-7875

22125

Less :- Fixed Cost :-

Fixed production OH (5*1500) -7500

Fixed selling and distribution expenses -10000

Net Profit (EBIT) 4625

Absorption Costing: It is referred as one of the management accounting technique, with

the support of absorption costing, different costs that are in relation with various process of

production are implemented on the product. This method also helps in evaluating inventory of

the Imda Tech. Different types of expenses are being carried out on different basis. When there is

actual occurrence of the expenses, then at that particular time, it may be necessary that budget

expenses may be different from actual budget (Fullerton, Kennedy and Widener, 2013).

Absorption costing technique helps in the administration of under and over absorption.

Income statement according to absorption costing

Sales (units) 1500

Revenue (1500*35) 52500

decisions. At the various operation levels, marginal costing will be helpful for that level in which

there is a generation of contribution. Marginal costing can also be defined as the modification in

opportunity cost which is modified because there is change in the process of production (Haiza

Muhammad Zawawi and Hoque, 2010). Difference arise in the opportunity cost because there is

increase in the production cost.

Income statement according to marginal costing

Sales (35*1500) 52500

Less :- Variable cost:-m

Labour (5*1500) -7500

Material (8*1500) -12000

Variable production OH (2*1500) -3000

Variable selling and distribution expenses (52500*15%)

Contribution

-7875

22125

Less :- Fixed Cost :-

Fixed production OH (5*1500) -7500

Fixed selling and distribution expenses -10000

Net Profit (EBIT) 4625

Absorption Costing: It is referred as one of the management accounting technique, with

the support of absorption costing, different costs that are in relation with various process of

production are implemented on the product. This method also helps in evaluating inventory of

the Imda Tech. Different types of expenses are being carried out on different basis. When there is

actual occurrence of the expenses, then at that particular time, it may be necessary that budget

expenses may be different from actual budget (Fullerton, Kennedy and Widener, 2013).

Absorption costing technique helps in the administration of under and over absorption.

Income statement according to absorption costing

Sales (units) 1500

Revenue (1500*35) 52500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

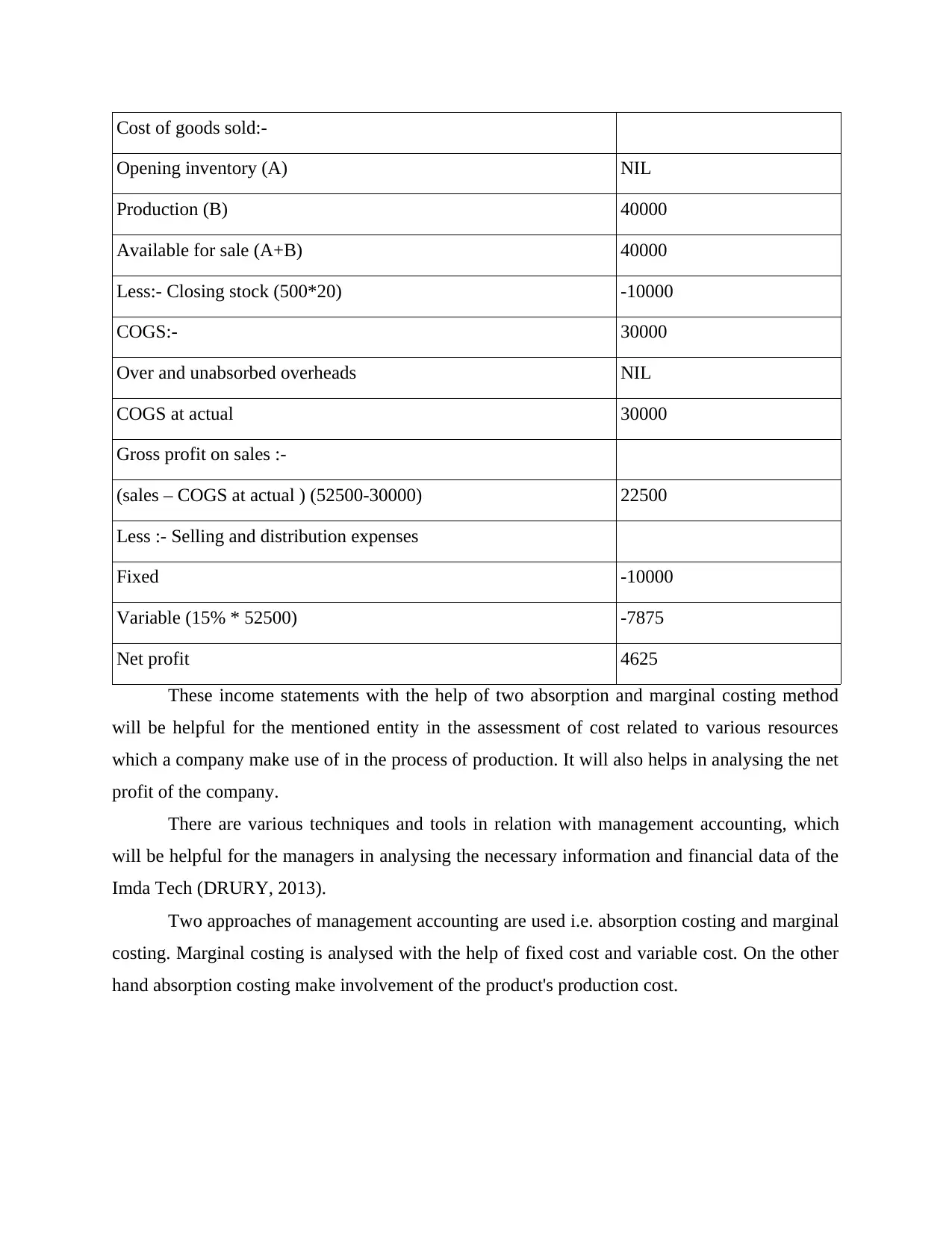

Cost of goods sold:-

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less:- Closing stock (500*20) -10000

COGS:- 30000

Over and unabsorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual ) (52500-30000) 22500

Less :- Selling and distribution expenses

Fixed -10000

Variable (15% * 52500) -7875

Net profit 4625

These income statements with the help of two absorption and marginal costing method

will be helpful for the mentioned entity in the assessment of cost related to various resources

which a company make use of in the process of production. It will also helps in analysing the net

profit of the company.

There are various techniques and tools in relation with management accounting, which

will be helpful for the managers in analysing the necessary information and financial data of the

Imda Tech (DRURY, 2013).

Two approaches of management accounting are used i.e. absorption costing and marginal

costing. Marginal costing is analysed with the help of fixed cost and variable cost. On the other

hand absorption costing make involvement of the product's production cost.

Opening inventory (A) NIL

Production (B) 40000

Available for sale (A+B) 40000

Less:- Closing stock (500*20) -10000

COGS:- 30000

Over and unabsorbed overheads NIL

COGS at actual 30000

Gross profit on sales :-

(sales – COGS at actual ) (52500-30000) 22500

Less :- Selling and distribution expenses

Fixed -10000

Variable (15% * 52500) -7875

Net profit 4625

These income statements with the help of two absorption and marginal costing method

will be helpful for the mentioned entity in the assessment of cost related to various resources

which a company make use of in the process of production. It will also helps in analysing the net

profit of the company.

There are various techniques and tools in relation with management accounting, which

will be helpful for the managers in analysing the necessary information and financial data of the

Imda Tech (DRURY, 2013).

Two approaches of management accounting are used i.e. absorption costing and marginal

costing. Marginal costing is analysed with the help of fixed cost and variable cost. On the other

hand absorption costing make involvement of the product's production cost.

TASK 3

P4 a) Types of budgets

An important role is being played by the budget in every firm for maintaining records and

financial statements. It also helps in the management and tracking of resources (Contrafatto and

Burns, 2013). Therefore planning of the budget is essential for Imda Tech. It assist in forecasting

future expenses and risks, which will be helpful for the managers to prepare policies and

strategies accordingly. Budget plan is being prepared by the company for the allocation of funds

in next financial year. There are different types of budgets which are being used by the firms are

as follows: Master budget: It can be defined as the aggregation of low level budgets which is being

prepared by the company's different areas of function. It includes financial statements

which are budgeted, financing plan and cash forecast (Busco and Scapens, 2011). It

helps in presenting overall firm's image. It is basically a set of interconnected budgets of

purchase, sales, production cost, income etc. Operating budget: It is the detailed statement of all estimated expenses and income on

the basis of forecasted sales revenue in a particular time period. It consist of different

sub-budgets, most important is the sales budget, which is prepared at the first position. Cash flow budget: These kinds of budgets are prepared in order to find out cash inflow

and outflow, in regards with various business activities. This budget is prepared for

examining shortfall in sales and expenses.

Static budget: In this there are several elements which are not changed with the change

in level of sales like overhead cost. Different departments allocate some money in the

budget which is used for various expenses (Burritt and Schaltegger, 2010).

Advantages and disadvantages of different types of budget

Advantages:

Budgets helps to verify information and also helps in forecasting information related to

balance sheet.

Projection of future and current expense can also be done with the help of budget.

Accountabilities and reserves can also be maintained.

Determination of cash balance with the for the management of operations are done with

the help of budgets.

P4 a) Types of budgets

An important role is being played by the budget in every firm for maintaining records and

financial statements. It also helps in the management and tracking of resources (Contrafatto and

Burns, 2013). Therefore planning of the budget is essential for Imda Tech. It assist in forecasting

future expenses and risks, which will be helpful for the managers to prepare policies and

strategies accordingly. Budget plan is being prepared by the company for the allocation of funds

in next financial year. There are different types of budgets which are being used by the firms are

as follows: Master budget: It can be defined as the aggregation of low level budgets which is being

prepared by the company's different areas of function. It includes financial statements

which are budgeted, financing plan and cash forecast (Busco and Scapens, 2011). It

helps in presenting overall firm's image. It is basically a set of interconnected budgets of

purchase, sales, production cost, income etc. Operating budget: It is the detailed statement of all estimated expenses and income on

the basis of forecasted sales revenue in a particular time period. It consist of different

sub-budgets, most important is the sales budget, which is prepared at the first position. Cash flow budget: These kinds of budgets are prepared in order to find out cash inflow

and outflow, in regards with various business activities. This budget is prepared for

examining shortfall in sales and expenses.

Static budget: In this there are several elements which are not changed with the change

in level of sales like overhead cost. Different departments allocate some money in the

budget which is used for various expenses (Burritt and Schaltegger, 2010).

Advantages and disadvantages of different types of budget

Advantages:

Budgets helps to verify information and also helps in forecasting information related to

balance sheet.

Projection of future and current expense can also be done with the help of budget.

Accountabilities and reserves can also be maintained.

Determination of cash balance with the for the management of operations are done with

the help of budgets.

Disadvantages:

Budgets sometimes lack in providing specific information, and it is not at all easy to

make modifications in master budget as it includes several categories.

There can be negative impact on the revenue of company as budgets are less flexible

which means changes are not easy to make (Bennett, Schaltegger and Zvezdov, 2013).

There may be pressure on workforce as there are large targets which are created by

budgets.

b) Process of budget preparation

There are various steps which are involved in the process of preparing budget. Information gathering and setting of goals: In order to prepare annual budget for Imda

Tech, necessary information is been collected by managers. After that targets and goals

are set up for sales. These goals have been set for the achievement of mission and vision. Designing of budget: After setting goals, budget plan is being prepared by the mangers

of the firm, and it is made sure that large amount is not spent by managers on this

process. In Imda Tech, managers identifies expenses and incomes and design budget

accordingly (Baldvinsdottir, Mitchell and Nørreklit, 2010). Implementation of plan into action: After the designing and preparation of the budget, it

is the duty of the managers to implement it in the entire firm. In which there is an

inclusion of all income and expenses. Human resources, labours and various financial

facilities are helpful to carry out plan of budget.

Reporting of interim process: It is the duty of the managers to make time to time analysis

of financial activities in order to maintain profit and loss statements and accounts

according to the plan of budget.

c) Pricing strategies

Pricing strategies are helpful to maintain price rates of specific goods or services. In Imda

Tech, pricing strategy helps to determine price points so as to gain profit on sales. There are

different pricing strategies which is used by firm in order to evaluate product's price. Premium Pricing: This strategy helps in establishing that the price of particular product

is higher than its competitors (Arroyo, 2012). This is used when there is antique or

unique product. It helps managers to achieve competitive market by giving good quality

of products.

Budgets sometimes lack in providing specific information, and it is not at all easy to

make modifications in master budget as it includes several categories.

There can be negative impact on the revenue of company as budgets are less flexible

which means changes are not easy to make (Bennett, Schaltegger and Zvezdov, 2013).

There may be pressure on workforce as there are large targets which are created by

budgets.

b) Process of budget preparation

There are various steps which are involved in the process of preparing budget. Information gathering and setting of goals: In order to prepare annual budget for Imda

Tech, necessary information is been collected by managers. After that targets and goals

are set up for sales. These goals have been set for the achievement of mission and vision. Designing of budget: After setting goals, budget plan is being prepared by the mangers

of the firm, and it is made sure that large amount is not spent by managers on this

process. In Imda Tech, managers identifies expenses and incomes and design budget

accordingly (Baldvinsdottir, Mitchell and Nørreklit, 2010). Implementation of plan into action: After the designing and preparation of the budget, it

is the duty of the managers to implement it in the entire firm. In which there is an

inclusion of all income and expenses. Human resources, labours and various financial

facilities are helpful to carry out plan of budget.

Reporting of interim process: It is the duty of the managers to make time to time analysis

of financial activities in order to maintain profit and loss statements and accounts

according to the plan of budget.

c) Pricing strategies

Pricing strategies are helpful to maintain price rates of specific goods or services. In Imda

Tech, pricing strategy helps to determine price points so as to gain profit on sales. There are

different pricing strategies which is used by firm in order to evaluate product's price. Premium Pricing: This strategy helps in establishing that the price of particular product

is higher than its competitors (Arroyo, 2012). This is used when there is antique or

unique product. It helps managers to achieve competitive market by giving good quality

of products.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Penetration Pricing: It is helpful for the mentioned firm in order to have market share by

keeping low price for services and products. With the help of it company will be able to

attract more clients and customers.

TASK 4

P5 Explain what a Balance Score Card approach is and its implementation

The Balance scorecard method works with controlling and maintaining the for function

related to the organisation effectiveness. The for factors are financial prospective, internal

business perspective, Customer perspective and innovative learning perspective. Te company is

having problems in maintaining the various prospective effectively in the business. The various

problem identified with the help of the balance scorecard approach are:

The private sector company is main goal is to achieve more profit for the organisation

development. The various problems related to the budgeting cash flows statements etc.

can be identified with the help of this approach.

The companies are not only focusses on the profitability index of the organisation also

focusses on the cost reduction problems of the business firm (Macintosh and Quattrone,

2010).

To maintain good relationship with customers and the effective analysis of the needs of

customers is the main financial problem of the organisation to decrease the incurred cost

in the customer ranking survey of consumer satisfaction index etc.

The problems related to the internal system like the cost incurred in the safety of the

employee, return on investment on the individual employee etc.

The response to these defined problems of balance score card system, are as follows:

The approach defines various resources of the investment that eliminates the risk

associated with the internal project.

The helps in developing Imda tech a safe and secure system of the mobile phone charging

system.

Balance score card is the management tools which help management top control the

business activities. The enterprise can have the track of the business activities and by this

company can monitor each and every activities which takes into the business premises. The

approach help the manger to identify the problem incurring in the organisation. It help the

keeping low price for services and products. With the help of it company will be able to

attract more clients and customers.

TASK 4

P5 Explain what a Balance Score Card approach is and its implementation

The Balance scorecard method works with controlling and maintaining the for function

related to the organisation effectiveness. The for factors are financial prospective, internal

business perspective, Customer perspective and innovative learning perspective. Te company is

having problems in maintaining the various prospective effectively in the business. The various

problem identified with the help of the balance scorecard approach are:

The private sector company is main goal is to achieve more profit for the organisation

development. The various problems related to the budgeting cash flows statements etc.

can be identified with the help of this approach.

The companies are not only focusses on the profitability index of the organisation also

focusses on the cost reduction problems of the business firm (Macintosh and Quattrone,

2010).

To maintain good relationship with customers and the effective analysis of the needs of

customers is the main financial problem of the organisation to decrease the incurred cost

in the customer ranking survey of consumer satisfaction index etc.

The problems related to the internal system like the cost incurred in the safety of the

employee, return on investment on the individual employee etc.

The response to these defined problems of balance score card system, are as follows:

The approach defines various resources of the investment that eliminates the risk

associated with the internal project.

The helps in developing Imda tech a safe and secure system of the mobile phone charging

system.

Balance score card is the management tools which help management top control the

business activities. The enterprise can have the track of the business activities and by this

company can monitor each and every activities which takes into the business premises. The

approach help the manger to identify the problem incurring in the organisation. It help the

company to make its strategies (Lukka, 2010). By using the balance score card method manager

can collect all the required information such as employees performance, different departments,

sales records, receivable etc. and according to this information manger took the decision.

Companies can create the share holders value by the effective governance. The balance

score card is a tool which is used by company y to create the great value at the business,

corporate and board level. The balance score card link the work all together. By which company

gets the information about the every activities taken into place. The balance score card approach

help to make the investment decisions. If there is more information available about the company

there can be more investors interested to invest. It also improve the financial performance of the

company because board has the adequate information to make the decision (Hopwood, Unerman

and Fries, 2010).

Balance score card provides the structure to the organisation so that it can achieve the

better goals, supervisor governance and result in the better share holder value. BSC approach

helps to mange the creation of value at the different level of the management. BSC help to

understand the business drives and make the strategy for enterprise future. It provide the clear

picture of the business entities.

CONCLUSION

From the above report it can be concluded that management accounting helps Imda Tech

in many ways. It is the combination of techniques and tools of finance which support in making

various strategies related to finance and financial decisions. This report will help in analysing the

net profit of the firm with the help of absorption and marginal costing methods. It is also

analysed that the different systems of management accounting help in the preparation of

effective financial statements. An important role is played by the pricing strategy of the company

in determining price of various services and products. Apart from this , benefit of balance score

card is also analysed which is helpful in management accounting.

can collect all the required information such as employees performance, different departments,

sales records, receivable etc. and according to this information manger took the decision.

Companies can create the share holders value by the effective governance. The balance

score card is a tool which is used by company y to create the great value at the business,

corporate and board level. The balance score card link the work all together. By which company

gets the information about the every activities taken into place. The balance score card approach

help to make the investment decisions. If there is more information available about the company

there can be more investors interested to invest. It also improve the financial performance of the

company because board has the adequate information to make the decision (Hopwood, Unerman

and Fries, 2010).

Balance score card provides the structure to the organisation so that it can achieve the

better goals, supervisor governance and result in the better share holder value. BSC approach

helps to mange the creation of value at the different level of the management. BSC help to

understand the business drives and make the strategy for enterprise future. It provide the clear

picture of the business entities.

CONCLUSION

From the above report it can be concluded that management accounting helps Imda Tech

in many ways. It is the combination of techniques and tools of finance which support in making

various strategies related to finance and financial decisions. This report will help in analysing the

net profit of the firm with the help of absorption and marginal costing methods. It is also

analysed that the different systems of management accounting help in the preparation of

effective financial statements. An important role is played by the pricing strategy of the company

in determining price of various services and products. Apart from this , benefit of balance score

card is also analysed which is helpful in management accounting.

REFERENCES

Books and Journals

Arroyo, P., 2012. Management accounting change and sustainability: an institutional approach.

Journal of Accounting & Organizational Change. 8(3). pp.286-309.

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Bennett, M.D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices in

management accounting for sustainability (pp. 1-56). London: ICAEW.

Burritt, R.L. and Schaltegger, S., 2010. Sustainability accounting and reporting: fad or trend?.

Accounting, Auditing & Accountability Journal. 23(7). pp.829-846.

Busco, C. and Scapens, R.W., 2011. Management accounting systems and organisational culture:

Interpreting their linkages and processes of change. Qualitative Research in Accounting

& Management. 8(4). pp.320-357.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting Research.

24(4). pp.349-365.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp.50-71.

Haiza Muhammad Zawawi, N. and Hoque, Z., 2010. Research in management accounting

innovations: An overview of its recent development. Qualitative Research in

Accounting & Management. 7(4). pp.505-568.

Hopwood, A.G., Unerman, J. and Fries, J., 2010. Accounting for sustainability: Practical

insights. Earthscan.

Lukka, K., 2010. The roles and effects of paradigms in accounting research. Management

Accounting Research. 21(2). pp.110-115.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Merchant, K.A., 2012. Making management accounting research more useful. Pacific

Accounting Review. 24(3). pp.334-356.

Books and Journals

Arroyo, P., 2012. Management accounting change and sustainability: an institutional approach.

Journal of Accounting & Organizational Change. 8(3). pp.286-309.

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

Bennett, M.D., Schaltegger, S. and Zvezdov, D., 2013. Exploring corporate practices in

management accounting for sustainability (pp. 1-56). London: ICAEW.

Burritt, R.L. and Schaltegger, S., 2010. Sustainability accounting and reporting: fad or trend?.

Accounting, Auditing & Accountability Journal. 23(7). pp.829-846.

Busco, C. and Scapens, R.W., 2011. Management accounting systems and organisational culture:

Interpreting their linkages and processes of change. Qualitative Research in Accounting

& Management. 8(4). pp.320-357.

Contrafatto, M. and Burns, J., 2013. Social and environmental accounting, organisational change

and management accounting: A processual view. Management Accounting Research.

24(4). pp.349-365.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp.50-71.

Haiza Muhammad Zawawi, N. and Hoque, Z., 2010. Research in management accounting

innovations: An overview of its recent development. Qualitative Research in

Accounting & Management. 7(4). pp.505-568.

Hopwood, A.G., Unerman, J. and Fries, J., 2010. Accounting for sustainability: Practical

insights. Earthscan.

Lukka, K., 2010. The roles and effects of paradigms in accounting research. Management

Accounting Research. 21(2). pp.110-115.

Macintosh, N.B. and Quattrone, P., 2010. Management accounting and control systems: An

organizational and sociological approach. John Wiley & Sons.

Merchant, K.A., 2012. Making management accounting research more useful. Pacific

Accounting Review. 24(3). pp.334-356.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pipan, T. and Czarniawska, B., 2010. How to construct an actor-network: Management

accounting from idea to practice. Critical Perspectives on Accounting. 21(3). pp.243-

251.

Quinn, M., 2011. Routines in management accounting research: further exploration. Journal of

Accounting & Organizational Change. 7(4). pp.337-357.

ter Bogt, H. and van Helden, J., 2012. The practical relevance of management accounting

research and the role of qualitative methods therein: the debate continues. Qualitative

Research in Accounting & Management. 9(3). pp.265-273.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive

management accounting research. Management Accounting Research. 21(2). pp.130-

141.

Ward, K., 2012. Strategic management accounting. Routledge.

Online

Define Management Accounting. What are its objectives. 2016. [Online]. Available Through:<

http://www.careerride.com/fa-management-accounting.aspx>. [Accessed on 19th May

2017].

What is Budgetary control?. 2017. [Online]. Available through

:<http://accountlearning.com/budgetary-control-objectives-advantages-disadvantages/>.

[Accessed on 19th May 2017].

accounting from idea to practice. Critical Perspectives on Accounting. 21(3). pp.243-

251.

Quinn, M., 2011. Routines in management accounting research: further exploration. Journal of

Accounting & Organizational Change. 7(4). pp.337-357.

ter Bogt, H. and van Helden, J., 2012. The practical relevance of management accounting

research and the role of qualitative methods therein: the debate continues. Qualitative

Research in Accounting & Management. 9(3). pp.265-273.

Vaivio, J. and Sirén, A., 2010. Insights into method triangulation and “paradigms” in interpretive

management accounting research. Management Accounting Research. 21(2). pp.130-

141.

Ward, K., 2012. Strategic management accounting. Routledge.

Online

Define Management Accounting. What are its objectives. 2016. [Online]. Available Through:<

http://www.careerride.com/fa-management-accounting.aspx>. [Accessed on 19th May

2017].

What is Budgetary control?. 2017. [Online]. Available through

:<http://accountlearning.com/budgetary-control-objectives-advantages-disadvantages/>.

[Accessed on 19th May 2017].

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.