Management Accounting and Its Applications

VerifiedAdded on 2020/02/03

|15

|4546

|460

Essay

AI Summary

This assignment delves into the field of management accounting, examining its core concepts and practical applications. It discusses how management accountants utilize accounting information to aid decision-making processes within organizations. The assignment also explores the impact of management accounting on business performance, highlighting its contribution to strategic planning, cost control, and profitability analysis.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

a) Preparing report on the function of management accounting..................................................4

I. Definition of management accounting and distinguish management accounting from

financial accounting ....................................................................................................................4

ii. Importance of management accounting information as the decision making tool for

department managers...................................................................................................................5

b) Different types of management accounting system and its use for departments to improve

their reports..................................................................................................................................6

TASK 2............................................................................................................................................6

Preparing the income statements for the month of September using the absorption and

marginal costing methods............................................................................................................6

TASK 3............................................................................................................................................9

Providing the written report on planning tools............................................................................9

a) Different types of budgets and their advantages and disadvantage.........................................9

b) The process of preparing the budgets....................................................................................10

c) Pricing strategies....................................................................................................................10

TASK 4..........................................................................................................................................11

(a) Balance score card approach and describing the its implement of a balanced scorecard . . .11

i. Using Balance Score Card (BSC) to identify and respond financial problem........................11

ii) Use of Balance Score Card to improve the financial governance and development of

effective strategies.....................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

a) Preparing report on the function of management accounting..................................................4

I. Definition of management accounting and distinguish management accounting from

financial accounting ....................................................................................................................4

ii. Importance of management accounting information as the decision making tool for

department managers...................................................................................................................5

b) Different types of management accounting system and its use for departments to improve

their reports..................................................................................................................................6

TASK 2............................................................................................................................................6

Preparing the income statements for the month of September using the absorption and

marginal costing methods............................................................................................................6

TASK 3............................................................................................................................................9

Providing the written report on planning tools............................................................................9

a) Different types of budgets and their advantages and disadvantage.........................................9

b) The process of preparing the budgets....................................................................................10

c) Pricing strategies....................................................................................................................10

TASK 4..........................................................................................................................................11

(a) Balance score card approach and describing the its implement of a balanced scorecard . . .11

i. Using Balance Score Card (BSC) to identify and respond financial problem........................11

ii) Use of Balance Score Card to improve the financial governance and development of

effective strategies.....................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

The management accounting refers to the procedure of handling the cash related activities

and reporting regarding different department of the business so as to manage varied activities

effectively for controlling the expenses. The present report is based on Imda Tech Ltd which

deals in special charger for mobile telephone and other carry on gadgets for retail outlets in UK.

The report covers aspects related to functions of management account along with its importance

and varied management accounting systems. Furthermore, income statement have been prepared

in accordance with the absorption and marginal costing. In addition to this, different types of

budget and process of preparing the budgets have been explained. Moreover, financial problems

which are being faced by the business are identified and accordingly effective strategies are

developed to resolve the situation effectively.

TASK 1

a) Preparing report on the function of management accounting

The functions of management accounting are explained as follows with the explanation

of different kind of aspects associated with the same. It helps to conduct the operational activities

effectively and manage the performance of the business in the right manner. It has been

understood with the help of definition of the management accounting and its different from the

financial accounting (Fullerton, Kennedy and Widener, 2014). Management accounting helps to

track the expenses of the firm and increase the profitability through the proper record keeping.

I. Definition of management accounting and distinguish management accounting from financial

accounting

The process of management accounting consists of aspects such as estimating, collecting

and preparing the management accounting information for taking the suitable decision for well

being of the business. It is helpful for taking the decision on daily business and controlling the

business activities effectively so as to meet the objectives of the business in the right manner

(Chenhall and Moers, 2015). Financial accounting basically deals financial statements which are

rotated to the lenders and stockholders. On the other hand, management accounting deals with

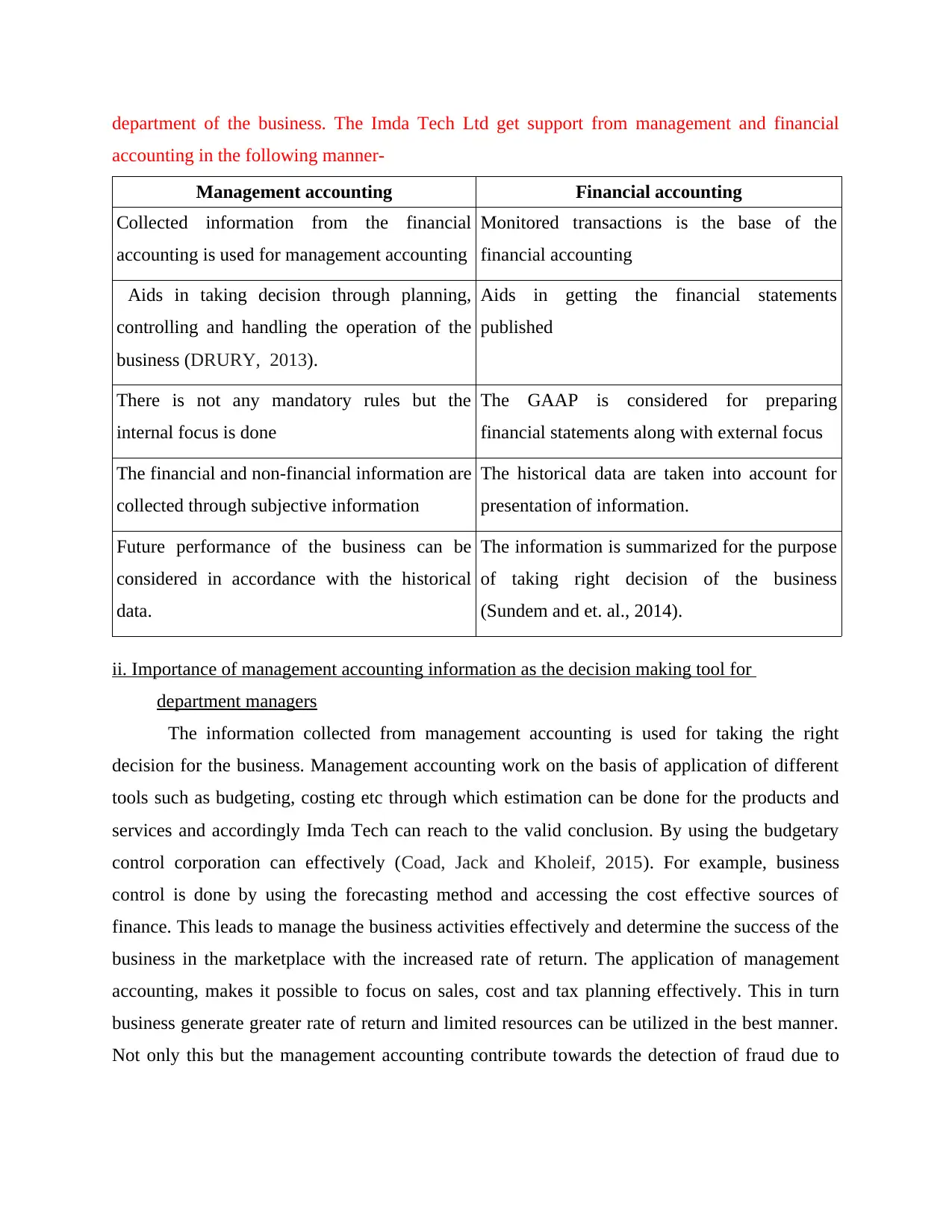

internal information management system so as to meet the requirement of all respective

The management accounting refers to the procedure of handling the cash related activities

and reporting regarding different department of the business so as to manage varied activities

effectively for controlling the expenses. The present report is based on Imda Tech Ltd which

deals in special charger for mobile telephone and other carry on gadgets for retail outlets in UK.

The report covers aspects related to functions of management account along with its importance

and varied management accounting systems. Furthermore, income statement have been prepared

in accordance with the absorption and marginal costing. In addition to this, different types of

budget and process of preparing the budgets have been explained. Moreover, financial problems

which are being faced by the business are identified and accordingly effective strategies are

developed to resolve the situation effectively.

TASK 1

a) Preparing report on the function of management accounting

The functions of management accounting are explained as follows with the explanation

of different kind of aspects associated with the same. It helps to conduct the operational activities

effectively and manage the performance of the business in the right manner. It has been

understood with the help of definition of the management accounting and its different from the

financial accounting (Fullerton, Kennedy and Widener, 2014). Management accounting helps to

track the expenses of the firm and increase the profitability through the proper record keeping.

I. Definition of management accounting and distinguish management accounting from financial

accounting

The process of management accounting consists of aspects such as estimating, collecting

and preparing the management accounting information for taking the suitable decision for well

being of the business. It is helpful for taking the decision on daily business and controlling the

business activities effectively so as to meet the objectives of the business in the right manner

(Chenhall and Moers, 2015). Financial accounting basically deals financial statements which are

rotated to the lenders and stockholders. On the other hand, management accounting deals with

internal information management system so as to meet the requirement of all respective

department of the business. The Imda Tech Ltd get support from management and financial

accounting in the following manner-

Management accounting Financial accounting

Collected information from the financial

accounting is used for management accounting

Monitored transactions is the base of the

financial accounting

Aids in taking decision through planning,

controlling and handling the operation of the

business (DRURY, 2013).

Aids in getting the financial statements

published

There is not any mandatory rules but the

internal focus is done

The GAAP is considered for preparing

financial statements along with external focus

The financial and non-financial information are

collected through subjective information

The historical data are taken into account for

presentation of information.

Future performance of the business can be

considered in accordance with the historical

data.

The information is summarized for the purpose

of taking right decision of the business

(Sundem and et. al., 2014).

ii. Importance of management accounting information as the decision making tool for

department managers

The information collected from management accounting is used for taking the right

decision for the business. Management accounting work on the basis of application of different

tools such as budgeting, costing etc through which estimation can be done for the products and

services and accordingly Imda Tech can reach to the valid conclusion. By using the budgetary

control corporation can effectively (Coad, Jack and Kholeif, 2015). For example, business

control is done by using the forecasting method and accessing the cost effective sources of

finance. This leads to manage the business activities effectively and determine the success of the

business in the marketplace with the increased rate of return. The application of management

accounting, makes it possible to focus on sales, cost and tax planning effectively. This in turn

business generate greater rate of return and limited resources can be utilized in the best manner.

Not only this but the management accounting contribute towards the detection of fraud due to

accounting in the following manner-

Management accounting Financial accounting

Collected information from the financial

accounting is used for management accounting

Monitored transactions is the base of the

financial accounting

Aids in taking decision through planning,

controlling and handling the operation of the

business (DRURY, 2013).

Aids in getting the financial statements

published

There is not any mandatory rules but the

internal focus is done

The GAAP is considered for preparing

financial statements along with external focus

The financial and non-financial information are

collected through subjective information

The historical data are taken into account for

presentation of information.

Future performance of the business can be

considered in accordance with the historical

data.

The information is summarized for the purpose

of taking right decision of the business

(Sundem and et. al., 2014).

ii. Importance of management accounting information as the decision making tool for

department managers

The information collected from management accounting is used for taking the right

decision for the business. Management accounting work on the basis of application of different

tools such as budgeting, costing etc through which estimation can be done for the products and

services and accordingly Imda Tech can reach to the valid conclusion. By using the budgetary

control corporation can effectively (Coad, Jack and Kholeif, 2015). For example, business

control is done by using the forecasting method and accessing the cost effective sources of

finance. This leads to manage the business activities effectively and determine the success of the

business in the marketplace with the increased rate of return. The application of management

accounting, makes it possible to focus on sales, cost and tax planning effectively. This in turn

business generate greater rate of return and limited resources can be utilized in the best manner.

Not only this but the management accounting contribute towards the detection of fraud due to

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

preparing the timely report. For example, fiance or departmental managers of the Imda Tech Ltd

can regulatory review the financial performance of the business and increase the possibility to

detect the fraud with regard to use of financial resources in the wrong activities of business.

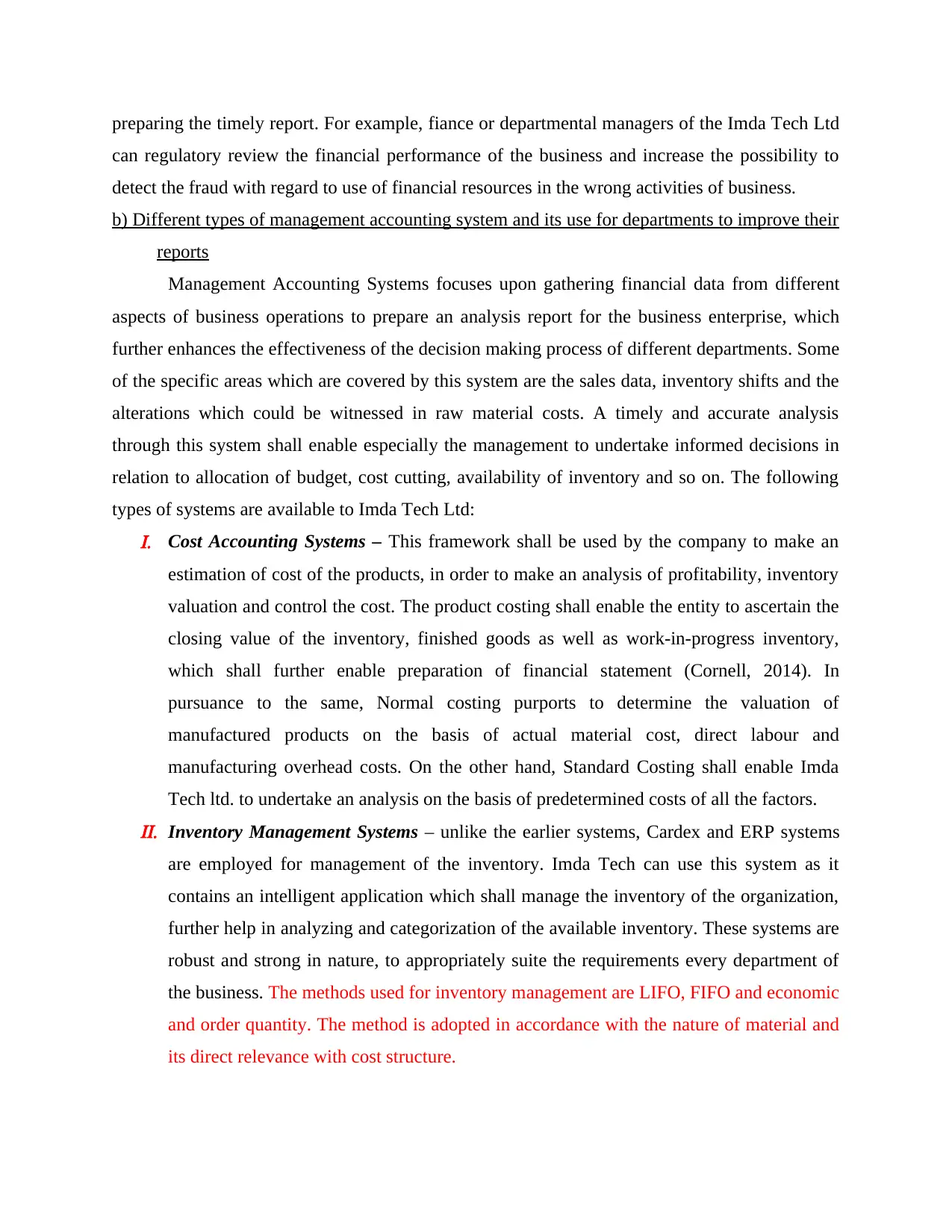

b) Different types of management accounting system and its use for departments to improve their

reports

Management Accounting Systems focuses upon gathering financial data from different

aspects of business operations to prepare an analysis report for the business enterprise, which

further enhances the effectiveness of the decision making process of different departments. Some

of the specific areas which are covered by this system are the sales data, inventory shifts and the

alterations which could be witnessed in raw material costs. A timely and accurate analysis

through this system shall enable especially the management to undertake informed decisions in

relation to allocation of budget, cost cutting, availability of inventory and so on. The following

types of systems are available to Imda Tech Ltd:I. Cost Accounting Systems – This framework shall be used by the company to make an

estimation of cost of the products, in order to make an analysis of profitability, inventory

valuation and control the cost. The product costing shall enable the entity to ascertain the

closing value of the inventory, finished goods as well as work-in-progress inventory,

which shall further enable preparation of financial statement (Cornell, 2014). In

pursuance to the same, Normal costing purports to determine the valuation of

manufactured products on the basis of actual material cost, direct labour and

manufacturing overhead costs. On the other hand, Standard Costing shall enable Imda

Tech ltd. to undertake an analysis on the basis of predetermined costs of all the factors.II. Inventory Management Systems – unlike the earlier systems, Cardex and ERP systems

are employed for management of the inventory. Imda Tech can use this system as it

contains an intelligent application which shall manage the inventory of the organization,

further help in analyzing and categorization of the available inventory. These systems are

robust and strong in nature, to appropriately suite the requirements every department of

the business. The methods used for inventory management are LIFO, FIFO and economic

and order quantity. The method is adopted in accordance with the nature of material and

its direct relevance with cost structure.

can regulatory review the financial performance of the business and increase the possibility to

detect the fraud with regard to use of financial resources in the wrong activities of business.

b) Different types of management accounting system and its use for departments to improve their

reports

Management Accounting Systems focuses upon gathering financial data from different

aspects of business operations to prepare an analysis report for the business enterprise, which

further enhances the effectiveness of the decision making process of different departments. Some

of the specific areas which are covered by this system are the sales data, inventory shifts and the

alterations which could be witnessed in raw material costs. A timely and accurate analysis

through this system shall enable especially the management to undertake informed decisions in

relation to allocation of budget, cost cutting, availability of inventory and so on. The following

types of systems are available to Imda Tech Ltd:I. Cost Accounting Systems – This framework shall be used by the company to make an

estimation of cost of the products, in order to make an analysis of profitability, inventory

valuation and control the cost. The product costing shall enable the entity to ascertain the

closing value of the inventory, finished goods as well as work-in-progress inventory,

which shall further enable preparation of financial statement (Cornell, 2014). In

pursuance to the same, Normal costing purports to determine the valuation of

manufactured products on the basis of actual material cost, direct labour and

manufacturing overhead costs. On the other hand, Standard Costing shall enable Imda

Tech ltd. to undertake an analysis on the basis of predetermined costs of all the factors.II. Inventory Management Systems – unlike the earlier systems, Cardex and ERP systems

are employed for management of the inventory. Imda Tech can use this system as it

contains an intelligent application which shall manage the inventory of the organization,

further help in analyzing and categorization of the available inventory. These systems are

robust and strong in nature, to appropriately suite the requirements every department of

the business. The methods used for inventory management are LIFO, FIFO and economic

and order quantity. The method is adopted in accordance with the nature of material and

its direct relevance with cost structure.

III. Job Costing System – This is one the techniques which involves the process of gathering

information in relation to costs connected to specific production or service jobs. These

systems are particularly helpful in providing the consumers with appropriate information

for costs incurred under different heads, with the intention to get them reimbursed

(Sundem and et. al., 2014). This is not a suitable option for Imda Ltd., as it is more

appropriate for the manufacturing entities where the production of products require

different material and conversion elements. It is particularly useful when the

organizations are required to produce inventoriable costs in relation to the manufactured

goods.

IV. Price Optimising Systems – These are the programs which ascertain the variation in

demand in pursuance to varying price levels. The information so gathered along with the

data in relation to costs as well as inventory levels can be used by entities to make

recommendation of prices, in order to improve profits. Imda Ltd. can use this system in

the form of powerful profit lever. The company shall utilize this system for tailor pricing

in connection to customer segments, which shall further enable to ascertain the manner in

which targeted customers shall respond to variations in pricing of the product.

TASK 2

Preparing the income statements for the month of September using the absorption and marginal

costing methods

The income statement in case of absorption or marginal cost different from each other

due to role of fixed and direct cost. In this manner, the allocation of cost is different in each case

which tends to affect the operational activities of corporation to a great extent (McPherson and

Karney, 2014). According to the information provided in context of Imda Tech Ltd, income

statement has been prepared as follows-

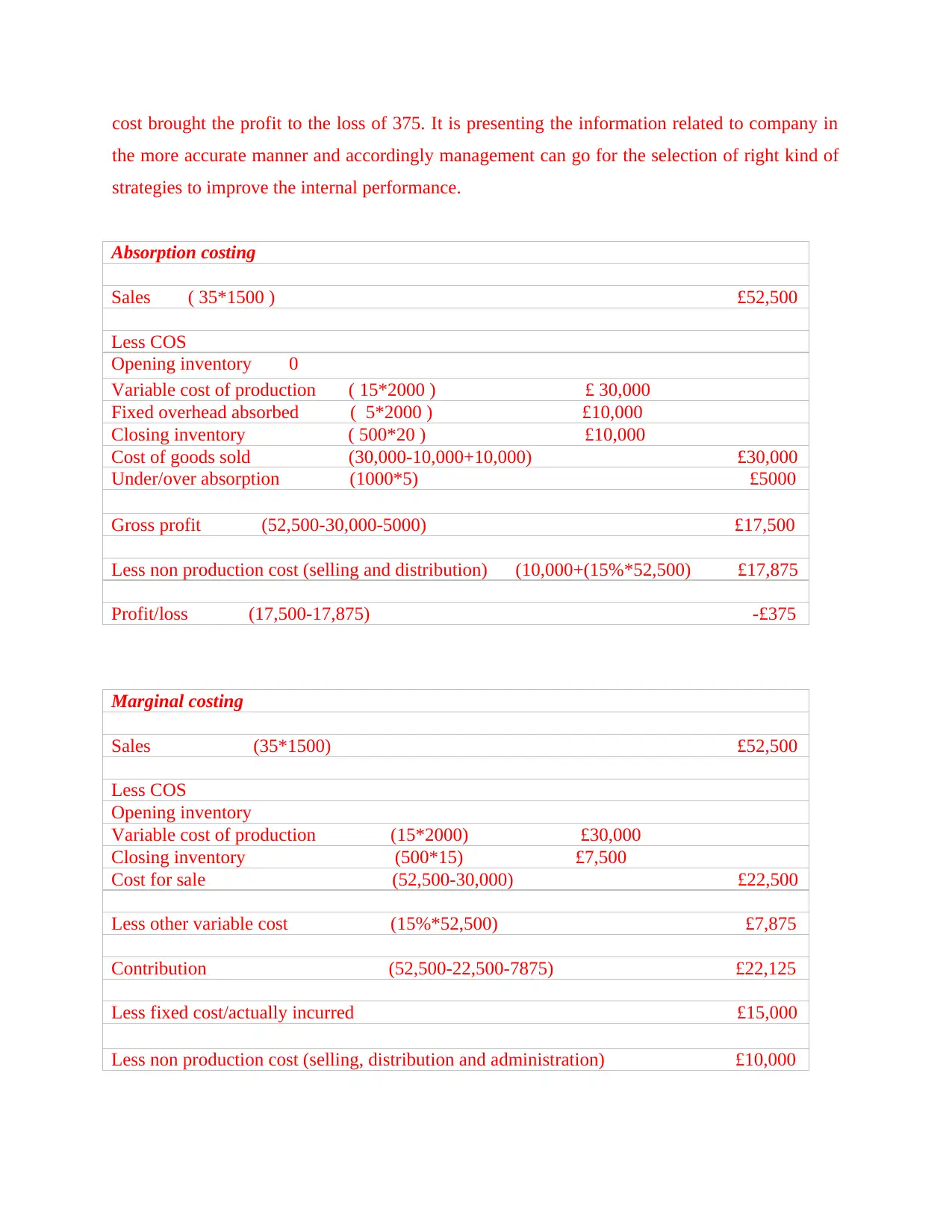

According to the below mentioned table, it has been found that Imda Tech Ltd incurred

the loss worth 375. It is because of higher fixed cost and the variable one. This leads to reduce

the profitability of the corporation and affect the overall earning in a significant manner. The

sales revenue incurred to the business was 52500 GBP whereas the to cost of goods sold was

30000 GBP along with under/over absorption worth 5000. In this manner, 17500 GBP was

found as the profitability of the business but the direct impact of aspects such as greater fixed

information in relation to costs connected to specific production or service jobs. These

systems are particularly helpful in providing the consumers with appropriate information

for costs incurred under different heads, with the intention to get them reimbursed

(Sundem and et. al., 2014). This is not a suitable option for Imda Ltd., as it is more

appropriate for the manufacturing entities where the production of products require

different material and conversion elements. It is particularly useful when the

organizations are required to produce inventoriable costs in relation to the manufactured

goods.

IV. Price Optimising Systems – These are the programs which ascertain the variation in

demand in pursuance to varying price levels. The information so gathered along with the

data in relation to costs as well as inventory levels can be used by entities to make

recommendation of prices, in order to improve profits. Imda Ltd. can use this system in

the form of powerful profit lever. The company shall utilize this system for tailor pricing

in connection to customer segments, which shall further enable to ascertain the manner in

which targeted customers shall respond to variations in pricing of the product.

TASK 2

Preparing the income statements for the month of September using the absorption and marginal

costing methods

The income statement in case of absorption or marginal cost different from each other

due to role of fixed and direct cost. In this manner, the allocation of cost is different in each case

which tends to affect the operational activities of corporation to a great extent (McPherson and

Karney, 2014). According to the information provided in context of Imda Tech Ltd, income

statement has been prepared as follows-

According to the below mentioned table, it has been found that Imda Tech Ltd incurred

the loss worth 375. It is because of higher fixed cost and the variable one. This leads to reduce

the profitability of the corporation and affect the overall earning in a significant manner. The

sales revenue incurred to the business was 52500 GBP whereas the to cost of goods sold was

30000 GBP along with under/over absorption worth 5000. In this manner, 17500 GBP was

found as the profitability of the business but the direct impact of aspects such as greater fixed

cost brought the profit to the loss of 375. It is presenting the information related to company in

the more accurate manner and accordingly management can go for the selection of right kind of

strategies to improve the internal performance.

Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

the more accurate manner and accordingly management can go for the selection of right kind of

strategies to improve the internal performance.

Absorption costing

Sales ( 35*1500 ) £52,500

Less COS

Opening inventory 0

Variable cost of production ( 15*2000 ) £ 30,000

Fixed overhead absorbed ( 5*2000 ) £10,000

Closing inventory ( 500*20 ) £10,000

Cost of goods sold (30,000-10,000+10,000) £30,000

Under/over absorption (1000*5) £5000

Gross profit (52,500-30,000-5000) £17,500

Less non production cost (selling and distribution) (10,000+(15%*52,500) £17,875

Profit/loss (17,500-17,875) -£375

Marginal costing

Sales (35*1500) £52,500

Less COS

Opening inventory

Variable cost of production (15*2000) £30,000

Closing inventory (500*15) £7,500

Cost for sale (52,500-30,000) £22,500

Less other variable cost (15%*52,500) £7,875

Contribution (52,500-22,500-7875) £22,125

Less fixed cost/actually incurred £15,000

Less non production cost (selling, distribution and administration) £10,000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit/loss (22,125-15,000-10,000) -£2,875

The table mentioned as follow reflects the information related to income statement

preparing in accordance with the marginal costing. The income statement is showing the loss of

-£2,875 under which fixed cost is not included. On the other hand, profit/loss in case of

absorption costing is -£375. It shows that absorption costing is must better in term of rate of

return but marginal one provide more accurate results.

Reconciliation

Reconciliation

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

The table mentioned as follow reflects the information related to income statement

preparing in accordance with the marginal costing. The income statement is showing the loss of

-£2,875 under which fixed cost is not included. On the other hand, profit/loss in case of

absorption costing is -£375. It shows that absorption costing is must better in term of rate of

return but marginal one provide more accurate results.

Reconciliation

Reconciliation

Absorption profit - £375

Less fixed overhead on inventory (500-0*5) £2,500

(closing inventory(production –sales2000-1500=500) -opening inventory*fixed overhead)

Marginal profit - £2,875

TASK 3

Providing the written report on planning tools

There are different planning tools such as budgets and other related techniques applied

for the selection of investment project and using the same in order to determine the long run

success of the business in the marketplace. The task covers the major aspects related to varied

kind of budgets and process applied for the same (Safaei and Keith, 2014). Along with that,

pricing strategies used by the corporation to recover the cost of production and increasing the

profitability have been covered-

a) Different types of budgets and their advantages and disadvantage

The budget is considered as the most important planning tool to allocate the financial or

other resources of varied activities of the business. This covers operational, master and sales as

well as cash budget. These are explained as follows- Operational budget-The budget prepared for daily business activities is known as the

operation one under which two distinct heads such as revenue and cost are prepared for

better presentation of profitability and cost incurred by the business in particular time

span. The major advantage of the operational budget is effective record keeping related to

the current expenses and income (Piacentino and et. al., 2015). On the other hand,

disadvantage of the operational budget is the rigid decision making and less accuracy in

the data. Master budget-This budget consists of major activities of the business which is produced

by considering all other budgets. This aids to provide the information related to estimated

earning for the business. The major disadvantage associated with the master budget is

reliability on other budgets such as sales and cash which might not be correct in

accordance with the external factors affecting the performance of the Imda Tech Ltd

(Miller and Kelber, 2015). Cash budget-The cash budget is very effective in allocating the financial resources on on

different operational activities of the business. This is helpful for Imda Tech Ltd to

control the expenses and focus on increasing the flow of production. The major

disadvantage of the cash budget is suffer change in the political or technological factor

which increase the cost (Armstrong, 2015).

Providing the written report on planning tools

There are different planning tools such as budgets and other related techniques applied

for the selection of investment project and using the same in order to determine the long run

success of the business in the marketplace. The task covers the major aspects related to varied

kind of budgets and process applied for the same (Safaei and Keith, 2014). Along with that,

pricing strategies used by the corporation to recover the cost of production and increasing the

profitability have been covered-

a) Different types of budgets and their advantages and disadvantage

The budget is considered as the most important planning tool to allocate the financial or

other resources of varied activities of the business. This covers operational, master and sales as

well as cash budget. These are explained as follows- Operational budget-The budget prepared for daily business activities is known as the

operation one under which two distinct heads such as revenue and cost are prepared for

better presentation of profitability and cost incurred by the business in particular time

span. The major advantage of the operational budget is effective record keeping related to

the current expenses and income (Piacentino and et. al., 2015). On the other hand,

disadvantage of the operational budget is the rigid decision making and less accuracy in

the data. Master budget-This budget consists of major activities of the business which is produced

by considering all other budgets. This aids to provide the information related to estimated

earning for the business. The major disadvantage associated with the master budget is

reliability on other budgets such as sales and cash which might not be correct in

accordance with the external factors affecting the performance of the Imda Tech Ltd

(Miller and Kelber, 2015). Cash budget-The cash budget is very effective in allocating the financial resources on on

different operational activities of the business. This is helpful for Imda Tech Ltd to

control the expenses and focus on increasing the flow of production. The major

disadvantage of the cash budget is suffer change in the political or technological factor

which increase the cost (Armstrong, 2015).

Sales budget-Under this budget management of Imda Tech Ltd can come to know

regarding the requirement of sales of particular number of units in order to earn the

desired rate of profit.

b) The process of preparing the budgets

Budget preparation is completing in the step by step manner under which varied activities

are considered. The first and forecast step is of obtaining the estimation. This is done for each

department of the organization such as production, sales and marketing as well as HR so as to get

the requirement of resources effectively. The second step is of coordinating the estimation in

which each department is asked to provide the estimation and accordingly aggregate demand of

the resources is known (Cornell, 2014). It is made possible through which clear communication

in each department so as to determine the success of the business effectively. Furthermore, third

step is regarding the communicating the budget with the all departments associated to Imda Tech

Ltd. At this stage, company integrate the view point of all managers and incorporate them into

the preparing of the final budget. For example, a particular department might have requirement

related to installation of new machine through which budget increases (Jelsma and et. al., 2014).

In addition to this, the last stage is of implementing the budget plan through proper

communication in the respective department. In addition to this, reporting interim progress is the

last stage whereby reporting is done in the light of the set budgeted objectives. This leads to

derive the valid outcome for the business and accordingly integrate the business activities

effectively.

c) Pricing strategies

Selection of right pricing strategy is the reason behind the success of many small

businesses operating in the marketplace. There are different pricing strategies such as

competitive, skimming and penetration as well as premium pricing strategies as per the nature

of market and product and services both. The penetration pricing strategy is adopted by the Imda

Tech Ltd to enter into new market through putting very low price of the product at the initial

stage. Though, firm increase the price by bringing the innovation in the services slowly. This

strategy is helpful in increasing more customers and raising the overall return for the firm.

Furthermore, skimming pricing strategy is applied for the unique product which is very less in

the marketplace (Ali and et. al., 2015). Though, company forms the strategy to reduce the price

regarding the requirement of sales of particular number of units in order to earn the

desired rate of profit.

b) The process of preparing the budgets

Budget preparation is completing in the step by step manner under which varied activities

are considered. The first and forecast step is of obtaining the estimation. This is done for each

department of the organization such as production, sales and marketing as well as HR so as to get

the requirement of resources effectively. The second step is of coordinating the estimation in

which each department is asked to provide the estimation and accordingly aggregate demand of

the resources is known (Cornell, 2014). It is made possible through which clear communication

in each department so as to determine the success of the business effectively. Furthermore, third

step is regarding the communicating the budget with the all departments associated to Imda Tech

Ltd. At this stage, company integrate the view point of all managers and incorporate them into

the preparing of the final budget. For example, a particular department might have requirement

related to installation of new machine through which budget increases (Jelsma and et. al., 2014).

In addition to this, the last stage is of implementing the budget plan through proper

communication in the respective department. In addition to this, reporting interim progress is the

last stage whereby reporting is done in the light of the set budgeted objectives. This leads to

derive the valid outcome for the business and accordingly integrate the business activities

effectively.

c) Pricing strategies

Selection of right pricing strategy is the reason behind the success of many small

businesses operating in the marketplace. There are different pricing strategies such as

competitive, skimming and penetration as well as premium pricing strategies as per the nature

of market and product and services both. The penetration pricing strategy is adopted by the Imda

Tech Ltd to enter into new market through putting very low price of the product at the initial

stage. Though, firm increase the price by bringing the innovation in the services slowly. This

strategy is helpful in increasing more customers and raising the overall return for the firm.

Furthermore, skimming pricing strategy is applied for the unique product which is very less in

the marketplace (Ali and et. al., 2015). Though, company forms the strategy to reduce the price

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

as the competitions related to product start increasing. Apart form this, competitive pricing are

used to stay competitive in the marketplace. For this purpose, company put efforts to recover the

cost of production and attract more customers by offering them product on the competitive

pricing. Apart from this, scenario reflects that Imda Tech Ltd is dealing in the special chargers

where it is not possible to set the low prices. Owing to this, it is necessary for the business to

charge very higher price of the products and services. Therefore, company follows different kind

of pricing strategies as per the nature of products and services.

Price are set by considering the cost and mark up of associated with the product or

services. The below mentioned table is showing that variable and fixed cost are considered to

find the total one. It helps to take out the margin of profit. In this manner, margin of profit is

added under the cost and then accordingly selling price is derived. For this purpose, Imda Tech

focuses on recovering the its overall cost by putting the suitable margin over the cost.

Variable cost

Fixed Cost

Total cost

Margin of profit

Selling price

TASK 4

(a) Balance score card approach and describing the its implement of a balanced scorecard

The balance score card is the effective aspect for the measurement of the business

performance under which corporation can put efforts to manage the business performance in the

direction so as to integrate all business activities for producing valid outcome. It has been

explained as follows- There are several components of balance score card such as financial

perceptive, internal process and customers as well as earning and growth perspective. These are

applied by setting the specific standards for the business and accordingly focus on deriving the

valid outcome. Each of these mentioned component specific the objectives and targets whereby

business can track the performance effectively.

used to stay competitive in the marketplace. For this purpose, company put efforts to recover the

cost of production and attract more customers by offering them product on the competitive

pricing. Apart from this, scenario reflects that Imda Tech Ltd is dealing in the special chargers

where it is not possible to set the low prices. Owing to this, it is necessary for the business to

charge very higher price of the products and services. Therefore, company follows different kind

of pricing strategies as per the nature of products and services.

Price are set by considering the cost and mark up of associated with the product or

services. The below mentioned table is showing that variable and fixed cost are considered to

find the total one. It helps to take out the margin of profit. In this manner, margin of profit is

added under the cost and then accordingly selling price is derived. For this purpose, Imda Tech

focuses on recovering the its overall cost by putting the suitable margin over the cost.

Variable cost

Fixed Cost

Total cost

Margin of profit

Selling price

TASK 4

(a) Balance score card approach and describing the its implement of a balanced scorecard

The balance score card is the effective aspect for the measurement of the business

performance under which corporation can put efforts to manage the business performance in the

direction so as to integrate all business activities for producing valid outcome. It has been

explained as follows- There are several components of balance score card such as financial

perceptive, internal process and customers as well as earning and growth perspective. These are

applied by setting the specific standards for the business and accordingly focus on deriving the

valid outcome. Each of these mentioned component specific the objectives and targets whereby

business can track the performance effectively.

(Source:The Balanced Scorecard approach. 2017)

i. Using Balance Score Card (BSC) to identify and respond financial problem

The balance score card approach is used to set the standard performance of the

organization so that the actual one can be used for the purpose of comparison. It covers several

aspects related to performance of the business such as financial, human resources and customers

perspective, internal business process etc. Along with that, innovation related perspective is also

covered under the balance score card (Burk and et. al., 2013). It proves to be effective to analyze

the business performance in the right manner and derive the valid outcome so as to create

competitive edge of the business in the marketplace. According to the given scenario, Imda Tech

is suffering from loss of 1.5 million GBP, hence, business will apply the balance score card

approach so as to assess the internal performance and accordingly form the effective strategies

for settlement of the business activities. At this juncture, SMART objective strategy will be

followed by the management of Imda Tech Ltd in the following manner-

To raise the sales turnover of by 25% till the end of financial year 2017

To increase the customer retention by 20% till the mid of financial year 2017

Illustration 1: Components of balance score card approach

i. Using Balance Score Card (BSC) to identify and respond financial problem

The balance score card approach is used to set the standard performance of the

organization so that the actual one can be used for the purpose of comparison. It covers several

aspects related to performance of the business such as financial, human resources and customers

perspective, internal business process etc. Along with that, innovation related perspective is also

covered under the balance score card (Burk and et. al., 2013). It proves to be effective to analyze

the business performance in the right manner and derive the valid outcome so as to create

competitive edge of the business in the marketplace. According to the given scenario, Imda Tech

is suffering from loss of 1.5 million GBP, hence, business will apply the balance score card

approach so as to assess the internal performance and accordingly form the effective strategies

for settlement of the business activities. At this juncture, SMART objective strategy will be

followed by the management of Imda Tech Ltd in the following manner-

To raise the sales turnover of by 25% till the end of financial year 2017

To increase the customer retention by 20% till the mid of financial year 2017

Illustration 1: Components of balance score card approach

To enhance the profitability of Imda Tech Ltd by 35% till the mid of financial year 2018.

These SMART objectives will be fulfilled by the business in order to accomplish the all

related activities of corporation in the right direction. However, respective department of Imda

Tech Ltd will look over the issues in order to grab the attention of more customers and enhance

the ratio of profitability in the mentioned time span.

ii) Use of Balance Score Card to improve the financial governance and development of effective

strategies

The balance score card is applied as the effective aspect for address the issues which are

being faced in the finance department of the organization. Here, corporation shed light on each

perspective of the balance score card such as customer perspective wherein focus will be laid on

specific requirement of the customers and accordingly services will be provided to them

(Toluwalope, 2017). For example, marketing manager of Imda Tech Ltd will ask for more

budget in order to offer the discount among customers and promoting the products by using

different mode of communication. This leads to cater the requirement of all related parties. On

the other hand, internal business practices are also covered under the balance score card

approach by setting standard for employees. However, their performance is reviewed in

accordance with the targets and accordingly learning program are introduced for higher

productivity of the business. It facilitates to establish proper control and support for the business

whereby company can effectively go into the upward direction. In this manner, application of

balance score aids to reduce the actual and expected outcome of the business (Fullerton,

Kennedy and Widener, 2014). Therefore, each department of the Imda Tech Ltd remain under

the control of management and organization objectives can be achieved effectively.

CONCLUSION

The aforementioned report concludes management accounting plays important role in

reducing the deviation in the actual and expected performance of the business due to use of

appropriate tools such as budgeting, balance score card etc. This aspect is helpful to have tight

control overall all resources employed to produce the valid outcome. It can also be concluded

different kind of budget system are used along with setting the right kind of pricing strategies so

as to ensure the attraction of large number of buyers and create competitive edge of the business.

These SMART objectives will be fulfilled by the business in order to accomplish the all

related activities of corporation in the right direction. However, respective department of Imda

Tech Ltd will look over the issues in order to grab the attention of more customers and enhance

the ratio of profitability in the mentioned time span.

ii) Use of Balance Score Card to improve the financial governance and development of effective

strategies

The balance score card is applied as the effective aspect for address the issues which are

being faced in the finance department of the organization. Here, corporation shed light on each

perspective of the balance score card such as customer perspective wherein focus will be laid on

specific requirement of the customers and accordingly services will be provided to them

(Toluwalope, 2017). For example, marketing manager of Imda Tech Ltd will ask for more

budget in order to offer the discount among customers and promoting the products by using

different mode of communication. This leads to cater the requirement of all related parties. On

the other hand, internal business practices are also covered under the balance score card

approach by setting standard for employees. However, their performance is reviewed in

accordance with the targets and accordingly learning program are introduced for higher

productivity of the business. It facilitates to establish proper control and support for the business

whereby company can effectively go into the upward direction. In this manner, application of

balance score aids to reduce the actual and expected outcome of the business (Fullerton,

Kennedy and Widener, 2014). Therefore, each department of the Imda Tech Ltd remain under

the control of management and organization objectives can be achieved effectively.

CONCLUSION

The aforementioned report concludes management accounting plays important role in

reducing the deviation in the actual and expected performance of the business due to use of

appropriate tools such as budgeting, balance score card etc. This aspect is helpful to have tight

control overall all resources employed to produce the valid outcome. It can also be concluded

different kind of budget system are used along with setting the right kind of pricing strategies so

as to ensure the attraction of large number of buyers and create competitive edge of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Journals and books

Ali, M.S. and et. al., 2015. Reporting of covariate selection and balance assessment in

propensity score analysis is suboptimal: a systematic review. Journal of clinical

epidemiology. 68(2). pp.122-131.

Armstrong, V.S., 2015. Using real option analysis to improve capital budgeting decisions when

project cash flows are subject to capacity constraints. Academy of Accounting and

Financial Studies Journal. 19(2). p.19.

Burk, J.M. and et. al., 2013. Balance error scoring system performance changes after a

competitive athletic season. Clinical Journal of Sport Medicine. 23(4). pp.312-317.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47. pp.1-13.

Coad, A., Jack, L. and Kholeif, A.O.R., 2015. Structuration theory: reflections on its further

potential for management accounting research. Qualitative Research in Accounting &

Management. 12(2). pp.153-171.

Cornell, B., 2014. Capital Budgeting: A'General Equilibrium'Analysis. Browser Download This

Paper.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7). pp.414-428.

Jelsma, D. and et. al., 2014. The impact of Wii Fit intervention on dynamic balance control in

children with probable Developmental Coordination Disorder and balance

problems. Human movement science. 33, pp.404-418.

McPherson, M. and Karney, B., 2014. Long-term scenario alternatives and their implications:

LEAP model application of Panama׳ s electricity sector. Energy Policy. 68, pp.146-157.

Miller, L. and Kelber, J.W., 2015. Using Options Pricing Theory To Value Safety &

Ergonomics Projects: A Case Study. Review of Business and Finance Studies. 6(2). pp.75-

84.

Journals and books

Ali, M.S. and et. al., 2015. Reporting of covariate selection and balance assessment in

propensity score analysis is suboptimal: a systematic review. Journal of clinical

epidemiology. 68(2). pp.122-131.

Armstrong, V.S., 2015. Using real option analysis to improve capital budgeting decisions when

project cash flows are subject to capacity constraints. Academy of Accounting and

Financial Studies Journal. 19(2). p.19.

Burk, J.M. and et. al., 2013. Balance error scoring system performance changes after a

competitive athletic season. Clinical Journal of Sport Medicine. 23(4). pp.312-317.

Chenhall, R.H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47. pp.1-13.

Coad, A., Jack, L. and Kholeif, A.O.R., 2015. Structuration theory: reflections on its further

potential for management accounting research. Qualitative Research in Accounting &

Management. 12(2). pp.153-171.

Cornell, B., 2014. Capital Budgeting: A'General Equilibrium'Analysis. Browser Download This

Paper.

DRURY, C.M., 2013. Management and cost accounting. Springer.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7). pp.414-428.

Jelsma, D. and et. al., 2014. The impact of Wii Fit intervention on dynamic balance control in

children with probable Developmental Coordination Disorder and balance

problems. Human movement science. 33, pp.404-418.

McPherson, M. and Karney, B., 2014. Long-term scenario alternatives and their implications:

LEAP model application of Panama׳ s electricity sector. Energy Policy. 68, pp.146-157.

Miller, L. and Kelber, J.W., 2015. Using Options Pricing Theory To Value Safety &

Ergonomics Projects: A Case Study. Review of Business and Finance Studies. 6(2). pp.75-

84.

Piacentino, A. and et. al., 2015. Optimization of trigeneration systems by mathematical

programming: influence of plant scheme and boundary conditions. Energy Conversion and

Management. 104. pp.100-114.

Safaei, H. and Keith, D.W., 2014. Compressed air energy storage with waste heat export: An

Alberta case study. Energy Conversion and Management. 78. pp.114-124.

Sundem, G. and et. al., 2014. The Search for a Better Accounting System: The Overlooked

Concern. Accounting Education for the 21st Century: The Global Challenges. p.465.

Online

Toluwalope, 2017. Importance of Management Accounting. [Online]. Available through:

<http://www.gemanalyst.com/importance-of-management-accounting/>. [Accessed on

25th April 2017].

The Balanced Scorecard approach. 2017. [Online]. Available through:

<https://blog.arkieva.com/the-balanced-scorecard-approach-to-roi-for-your-supply-chain-

planning-project/>. [Accessed on 12th May 2017].

programming: influence of plant scheme and boundary conditions. Energy Conversion and

Management. 104. pp.100-114.

Safaei, H. and Keith, D.W., 2014. Compressed air energy storage with waste heat export: An

Alberta case study. Energy Conversion and Management. 78. pp.114-124.

Sundem, G. and et. al., 2014. The Search for a Better Accounting System: The Overlooked

Concern. Accounting Education for the 21st Century: The Global Challenges. p.465.

Online

Toluwalope, 2017. Importance of Management Accounting. [Online]. Available through:

<http://www.gemanalyst.com/importance-of-management-accounting/>. [Accessed on

25th April 2017].

The Balanced Scorecard approach. 2017. [Online]. Available through:

<https://blog.arkieva.com/the-balanced-scorecard-approach-to-roi-for-your-supply-chain-

planning-project/>. [Accessed on 12th May 2017].

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.