Detailed Management Accounting Report: Smart Looks Limited Performance

VerifiedAdded on 2020/02/17

|27

|4551

|367

Report

AI Summary

This report provides a detailed analysis of the financial and accounting data for Smart Looks Limited, a textile company. It covers cost classification, including fixed, variable, and semi-variable expenses, and explores various cost segregation methods. The report calculates total and unit costs of production, and examines inventory valuation methods such as FIFO, LIFO, and weighted average, alongside the cost of goods sold. Key performance indicators (KPIs) are identified to measure business performance, along with strategies to reduce costs and improve quality. The report further delves into budgeting, its importance, and different budgeting methods. It includes the preparation of various budgets and a cash budget for decision-making. Finally, the report analyzes budgeted versus actual profit, material and sub-variances, and concludes with a budgetary report for the board of directors.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

1.1 Segregation of expenditures.............................................................................................3

QUESTION 2...................................................................................................................................4

Calculating total as well as unit cost of production................................................................4

QUESTION 3...................................................................................................................................5

Inventory or stock method for costing....................................................................................5

1. FIFO...................................................................................................................................6

2. LIFO...................................................................................................................................6

3. Weighted Average Method.................................................................................................7

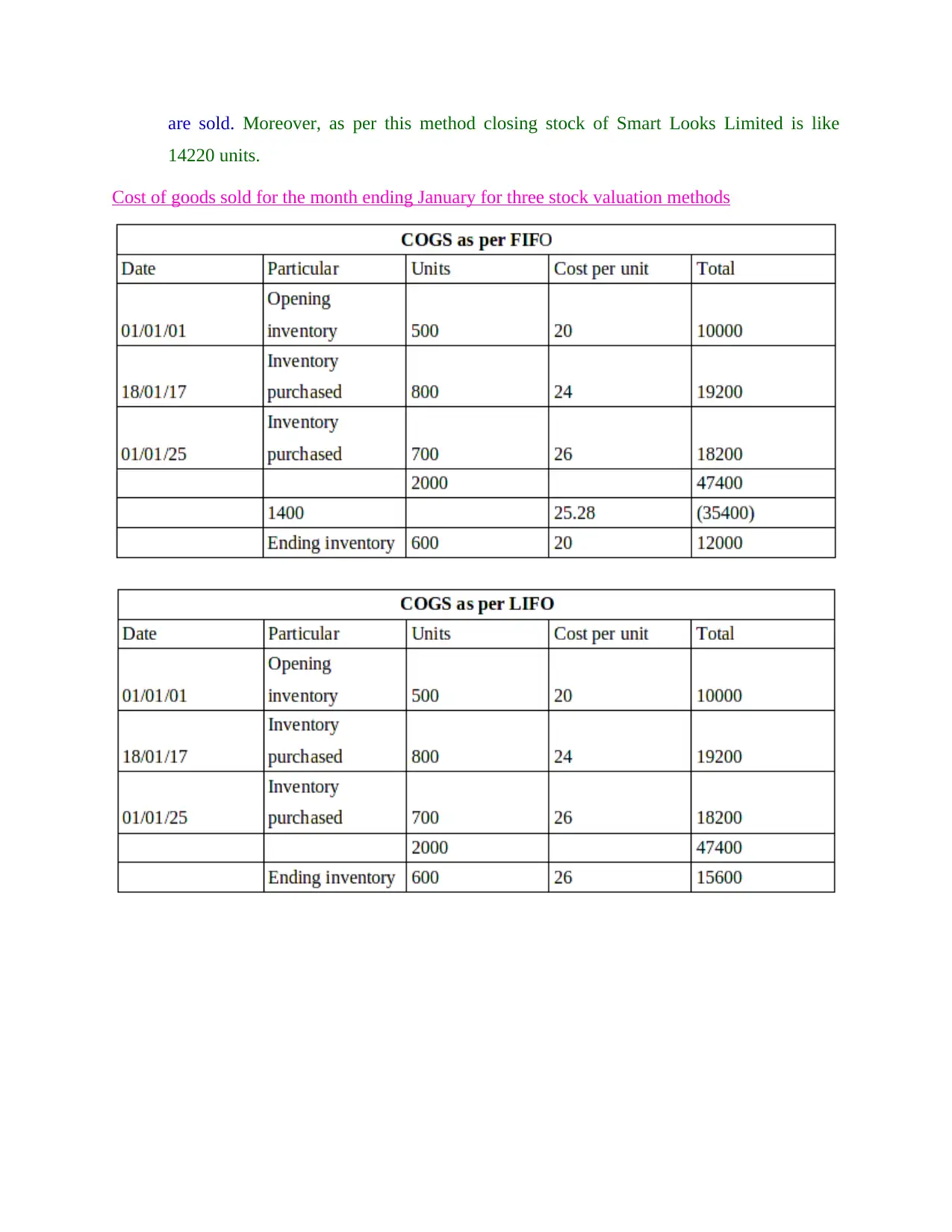

Cost of goods sold for the month ending January for three stock valuation methods............8

QUESTION 4...................................................................................................................................9

Analysis of financial data such as cost...................................................................................9

QUESTION 5.................................................................................................................................11

A) Key performance indicators to measure and analyse business performance..................11

B) Ways to reduce cost and improve quality........................................................................14

QUESTION 6.................................................................................................................................14

A) and B) Budget along with its importance for firm..........................................................14

C) Methods or ways to prepare budget.................................................................................15

QUESTION 7.................................................................................................................................16

Preparation of different budgets for three months................................................................16

QUESTION 8.................................................................................................................................19

Preparation of cash budget in order to take decision............................................................19

QUESTION 9.................................................................................................................................19

A) Budgeted profit ...............................................................................................................19

B) Actual profit.....................................................................................................................20

C) Material and sub variances..............................................................................................21

D) Reconciliation Operating statement:-..............................................................................22

QUESTION 10...............................................................................................................................23

Report on budgetary for board of directors..........................................................................23

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

1.1 Segregation of expenditures.............................................................................................3

QUESTION 2...................................................................................................................................4

Calculating total as well as unit cost of production................................................................4

QUESTION 3...................................................................................................................................5

Inventory or stock method for costing....................................................................................5

1. FIFO...................................................................................................................................6

2. LIFO...................................................................................................................................6

3. Weighted Average Method.................................................................................................7

Cost of goods sold for the month ending January for three stock valuation methods............8

QUESTION 4...................................................................................................................................9

Analysis of financial data such as cost...................................................................................9

QUESTION 5.................................................................................................................................11

A) Key performance indicators to measure and analyse business performance..................11

B) Ways to reduce cost and improve quality........................................................................14

QUESTION 6.................................................................................................................................14

A) and B) Budget along with its importance for firm..........................................................14

C) Methods or ways to prepare budget.................................................................................15

QUESTION 7.................................................................................................................................16

Preparation of different budgets for three months................................................................16

QUESTION 8.................................................................................................................................19

Preparation of cash budget in order to take decision............................................................19

QUESTION 9.................................................................................................................................19

A) Budgeted profit ...............................................................................................................19

B) Actual profit.....................................................................................................................20

C) Material and sub variances..............................................................................................21

D) Reconciliation Operating statement:-..............................................................................22

QUESTION 10...............................................................................................................................23

Report on budgetary for board of directors..........................................................................23

CONCLUSION..............................................................................................................................24

REFERENCES..............................................................................................................................25

REFERENCES..............................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

For every company it is compulsory to manage different financial and accounting data

and information to enhance its financial health. In the current case there is Smart Looks Limited

company is selected which is operating in the textile industry and produces cloths for different

retail firms. It shows about the classification of different kinds of expenditures which are

incurred for producing cloths. Apart from this, it describes about various methods for reduce

cost, enhance quality of products and assess business performance in the industry. Moreover, it

helps to analyse about importance of budget and various types of budget statements for the Smart

Looks company. At the last, report looks upon calculation of actual as well as budgeted and

standard profit.

QUESTION 1

1.1 Segregation of expenditures

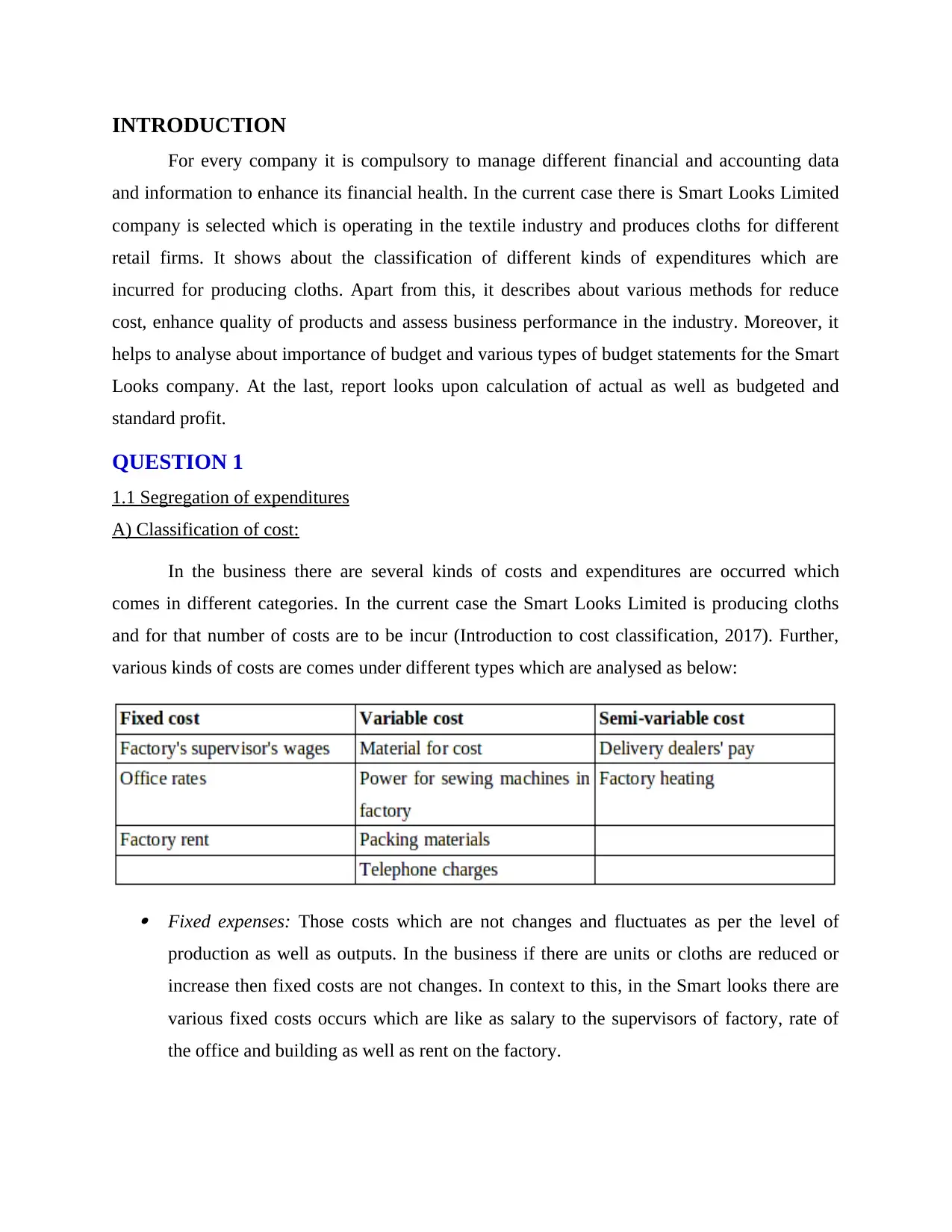

A) Classification of cost:

In the business there are several kinds of costs and expenditures are occurred which

comes in different categories. In the current case the Smart Looks Limited is producing cloths

and for that number of costs are to be incur (Introduction to cost classification, 2017). Further,

various kinds of costs are comes under different types which are analysed as below:

Fixed expenses: Those costs which are not changes and fluctuates as per the level of

production as well as outputs. In the business if there are units or cloths are reduced or

increase then fixed costs are not changes. In context to this, in the Smart looks there are

various fixed costs occurs which are like as salary to the supervisors of factory, rate of

the office and building as well as rent on the factory.

For every company it is compulsory to manage different financial and accounting data

and information to enhance its financial health. In the current case there is Smart Looks Limited

company is selected which is operating in the textile industry and produces cloths for different

retail firms. It shows about the classification of different kinds of expenditures which are

incurred for producing cloths. Apart from this, it describes about various methods for reduce

cost, enhance quality of products and assess business performance in the industry. Moreover, it

helps to analyse about importance of budget and various types of budget statements for the Smart

Looks company. At the last, report looks upon calculation of actual as well as budgeted and

standard profit.

QUESTION 1

1.1 Segregation of expenditures

A) Classification of cost:

In the business there are several kinds of costs and expenditures are occurred which

comes in different categories. In the current case the Smart Looks Limited is producing cloths

and for that number of costs are to be incur (Introduction to cost classification, 2017). Further,

various kinds of costs are comes under different types which are analysed as below:

Fixed expenses: Those costs which are not changes and fluctuates as per the level of

production as well as outputs. In the business if there are units or cloths are reduced or

increase then fixed costs are not changes. In context to this, in the Smart looks there are

various fixed costs occurs which are like as salary to the supervisors of factory, rate of

the office and building as well as rent on the factory.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Variable expenses: Apart from this, the costs which are varied and changes on the basis

of level of production and units. Further, if firm makes and produces 1000 units of cloths

previously and as of now it produces 1200 or 800 units then variable cost will be increase

or decrease respectively (Bowling, 2014). In the current case such kind of expenses are

like as material purchase amount, power used in sewing machine, packing expenses and

charges on telephone.

Semi-variable expenses: The expenditures which are not fixed and not variable are

known as semi-variable costs. These are sometimes fixed and sometimes variable that

means in some cases changes as per the production level and in some case not varied. In

the smart looks company such type of costs are like as payment of the dealers and heating

charges of the factory and production process.

B) Other methods for classifying cost:

Apart from above mentioned various types of costs there are some other criterias also

used by the management. Furthermore, another methods to segregate costs are like as production,

prime, stepped fixed, stepped variable, direct and indirect, quality costs etc. The expenses which

are incurred in the production process as per the every phase and stage are known as stepped

expenses (Cheng and Roïz, 2015). Moreover, those cost which are directly as well as indirect

manner used are identified as direct and indirect which are such as direct material, labour, wages,

depreciation, insurance, tax etc.

Apart from this, there are several kinds if methods on the basis of which costs and

expenses are segregated and classified within the workplace of Smart Looks Limited. Other than

above discussed ways another are like as controllable and uncontrollable, normal and abnormal,

historical, production, service, predetermined, based on the functions like as IT, HR, finance,

marketing, operation, research and development, marketing etc. By considering such ways the

management easily able to classify and then analyse the expenses in appropriate manner.

QUESTION 2

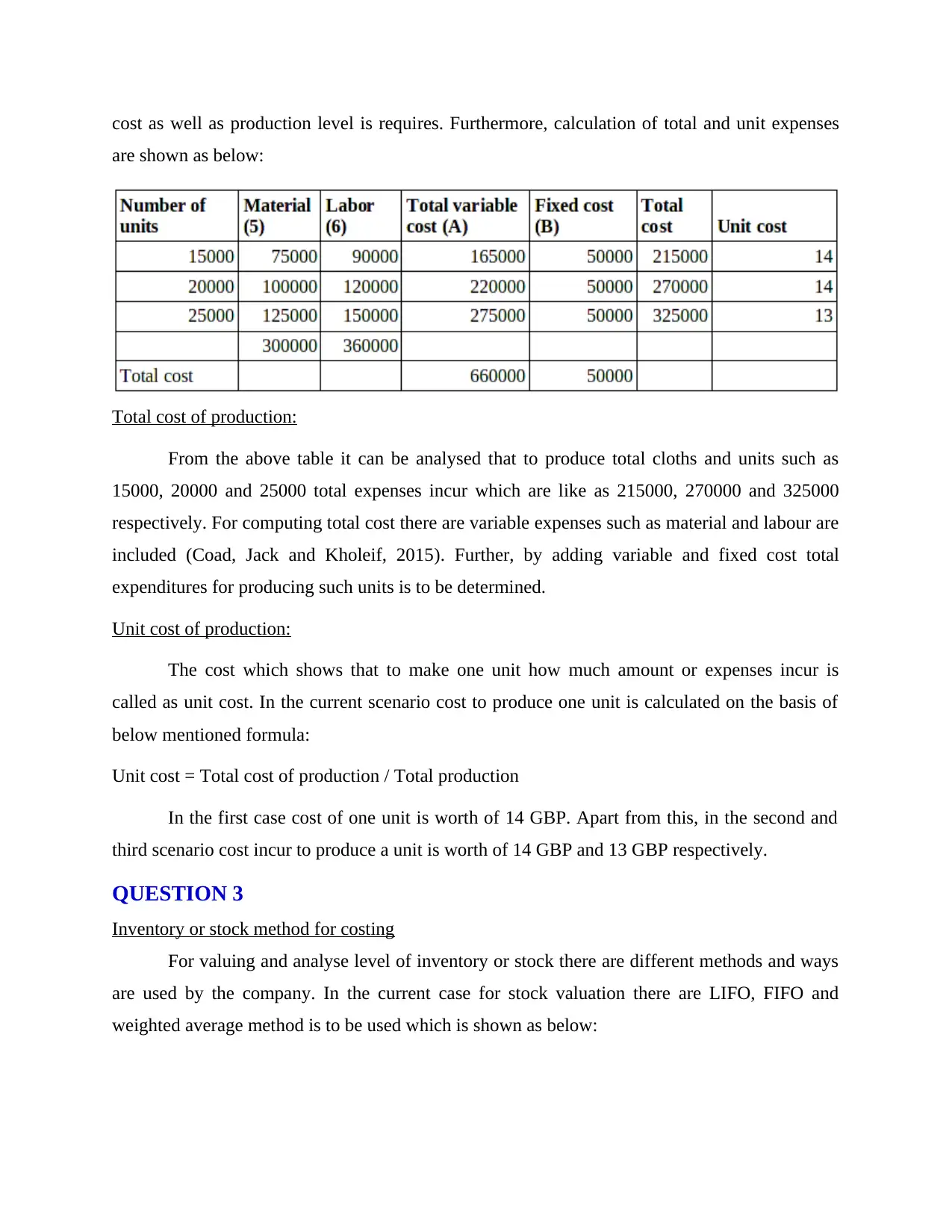

Calculating total as well as unit cost of production

The management of Smart Looks Limited needs to take and compute cost of the total

production and units. For that different types of costs are necessary because on the basis of all

variable and fixed cost total expenses are to be calculated. For assessing cost of one unit total

of level of production and units. Further, if firm makes and produces 1000 units of cloths

previously and as of now it produces 1200 or 800 units then variable cost will be increase

or decrease respectively (Bowling, 2014). In the current case such kind of expenses are

like as material purchase amount, power used in sewing machine, packing expenses and

charges on telephone.

Semi-variable expenses: The expenditures which are not fixed and not variable are

known as semi-variable costs. These are sometimes fixed and sometimes variable that

means in some cases changes as per the production level and in some case not varied. In

the smart looks company such type of costs are like as payment of the dealers and heating

charges of the factory and production process.

B) Other methods for classifying cost:

Apart from above mentioned various types of costs there are some other criterias also

used by the management. Furthermore, another methods to segregate costs are like as production,

prime, stepped fixed, stepped variable, direct and indirect, quality costs etc. The expenses which

are incurred in the production process as per the every phase and stage are known as stepped

expenses (Cheng and Roïz, 2015). Moreover, those cost which are directly as well as indirect

manner used are identified as direct and indirect which are such as direct material, labour, wages,

depreciation, insurance, tax etc.

Apart from this, there are several kinds if methods on the basis of which costs and

expenses are segregated and classified within the workplace of Smart Looks Limited. Other than

above discussed ways another are like as controllable and uncontrollable, normal and abnormal,

historical, production, service, predetermined, based on the functions like as IT, HR, finance,

marketing, operation, research and development, marketing etc. By considering such ways the

management easily able to classify and then analyse the expenses in appropriate manner.

QUESTION 2

Calculating total as well as unit cost of production

The management of Smart Looks Limited needs to take and compute cost of the total

production and units. For that different types of costs are necessary because on the basis of all

variable and fixed cost total expenses are to be calculated. For assessing cost of one unit total

cost as well as production level is requires. Furthermore, calculation of total and unit expenses

are shown as below:

Total cost of production:

From the above table it can be analysed that to produce total cloths and units such as

15000, 20000 and 25000 total expenses incur which are like as 215000, 270000 and 325000

respectively. For computing total cost there are variable expenses such as material and labour are

included (Coad, Jack and Kholeif, 2015). Further, by adding variable and fixed cost total

expenditures for producing such units is to be determined.

Unit cost of production:

The cost which shows that to make one unit how much amount or expenses incur is

called as unit cost. In the current scenario cost to produce one unit is calculated on the basis of

below mentioned formula:

Unit cost = Total cost of production / Total production

In the first case cost of one unit is worth of 14 GBP. Apart from this, in the second and

third scenario cost incur to produce a unit is worth of 14 GBP and 13 GBP respectively.

QUESTION 3

Inventory or stock method for costing

For valuing and analyse level of inventory or stock there are different methods and ways

are used by the company. In the current case for stock valuation there are LIFO, FIFO and

weighted average method is to be used which is shown as below:

are shown as below:

Total cost of production:

From the above table it can be analysed that to produce total cloths and units such as

15000, 20000 and 25000 total expenses incur which are like as 215000, 270000 and 325000

respectively. For computing total cost there are variable expenses such as material and labour are

included (Coad, Jack and Kholeif, 2015). Further, by adding variable and fixed cost total

expenditures for producing such units is to be determined.

Unit cost of production:

The cost which shows that to make one unit how much amount or expenses incur is

called as unit cost. In the current scenario cost to produce one unit is calculated on the basis of

below mentioned formula:

Unit cost = Total cost of production / Total production

In the first case cost of one unit is worth of 14 GBP. Apart from this, in the second and

third scenario cost incur to produce a unit is worth of 14 GBP and 13 GBP respectively.

QUESTION 3

Inventory or stock method for costing

For valuing and analyse level of inventory or stock there are different methods and ways

are used by the company. In the current case for stock valuation there are LIFO, FIFO and

weighted average method is to be used which is shown as below:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

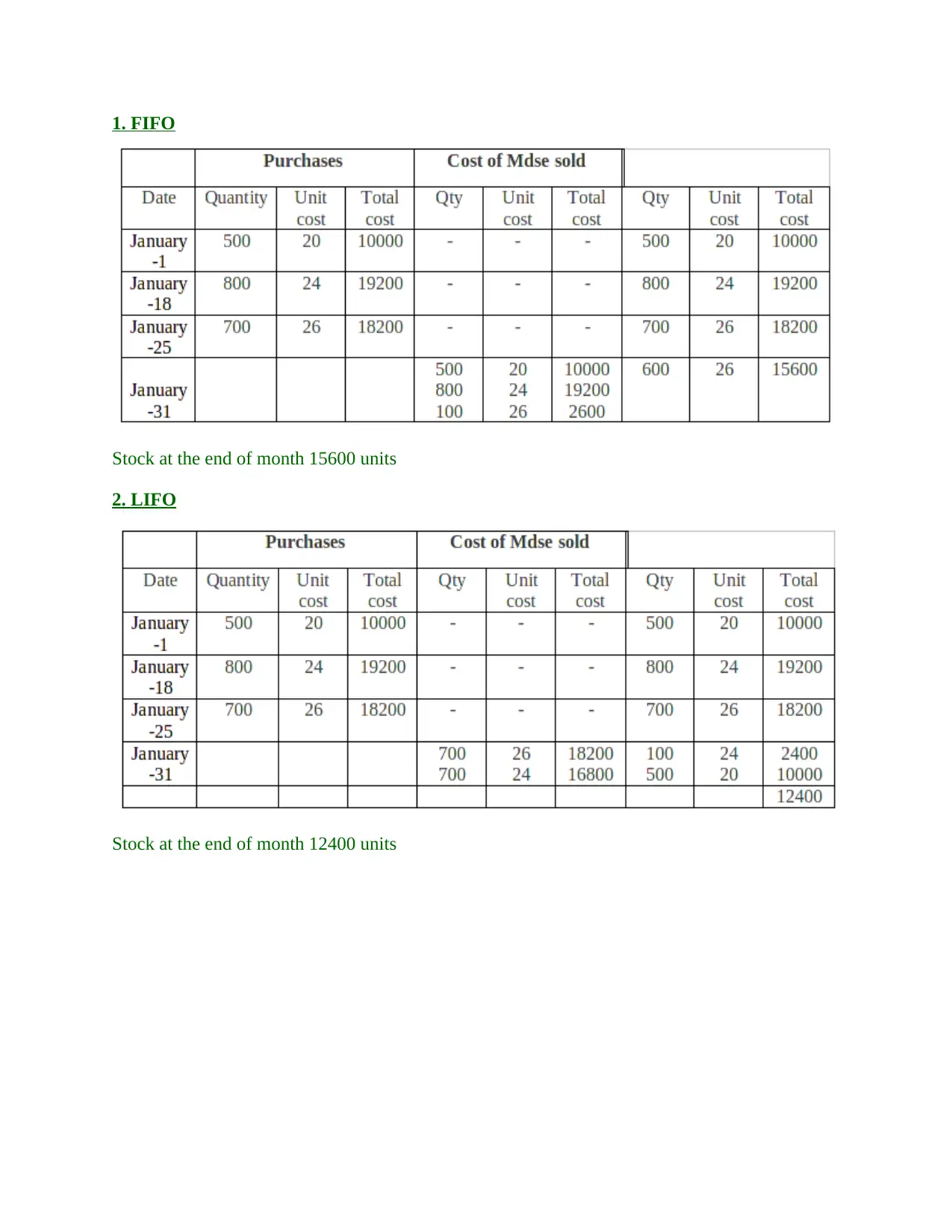

1. FIFO

Stock at the end of month 15600 units

2. LIFO

Stock at the end of month 12400 units

Stock at the end of month 15600 units

2. LIFO

Stock at the end of month 12400 units

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

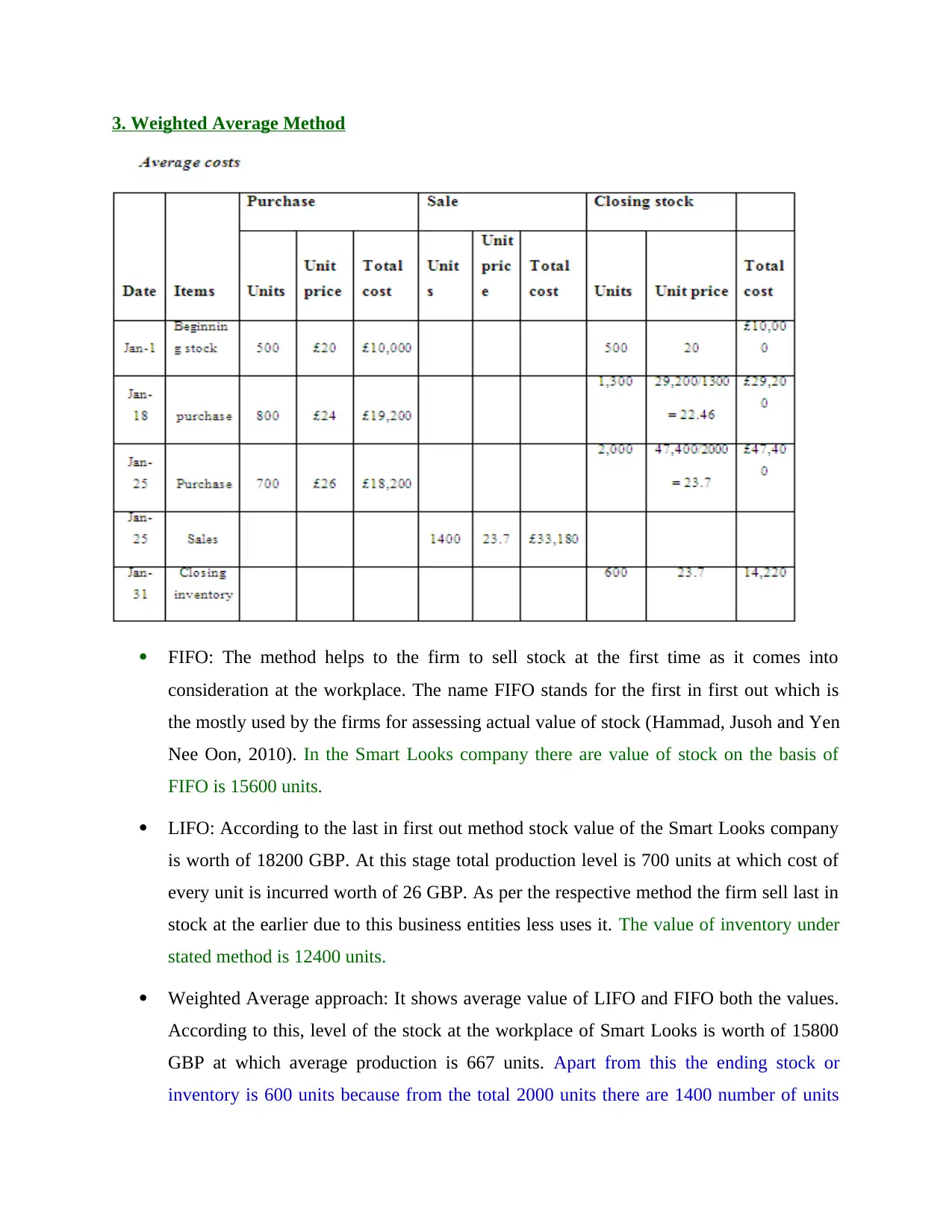

3. Weighted Average Method

FIFO: The method helps to the firm to sell stock at the first time as it comes into

consideration at the workplace. The name FIFO stands for the first in first out which is

the mostly used by the firms for assessing actual value of stock (Hammad, Jusoh and Yen

Nee Oon, 2010). In the Smart Looks company there are value of stock on the basis of

FIFO is 15600 units.

LIFO: According to the last in first out method stock value of the Smart Looks company

is worth of 18200 GBP. At this stage total production level is 700 units at which cost of

every unit is incurred worth of 26 GBP. As per the respective method the firm sell last in

stock at the earlier due to this business entities less uses it. The value of inventory under

stated method is 12400 units.

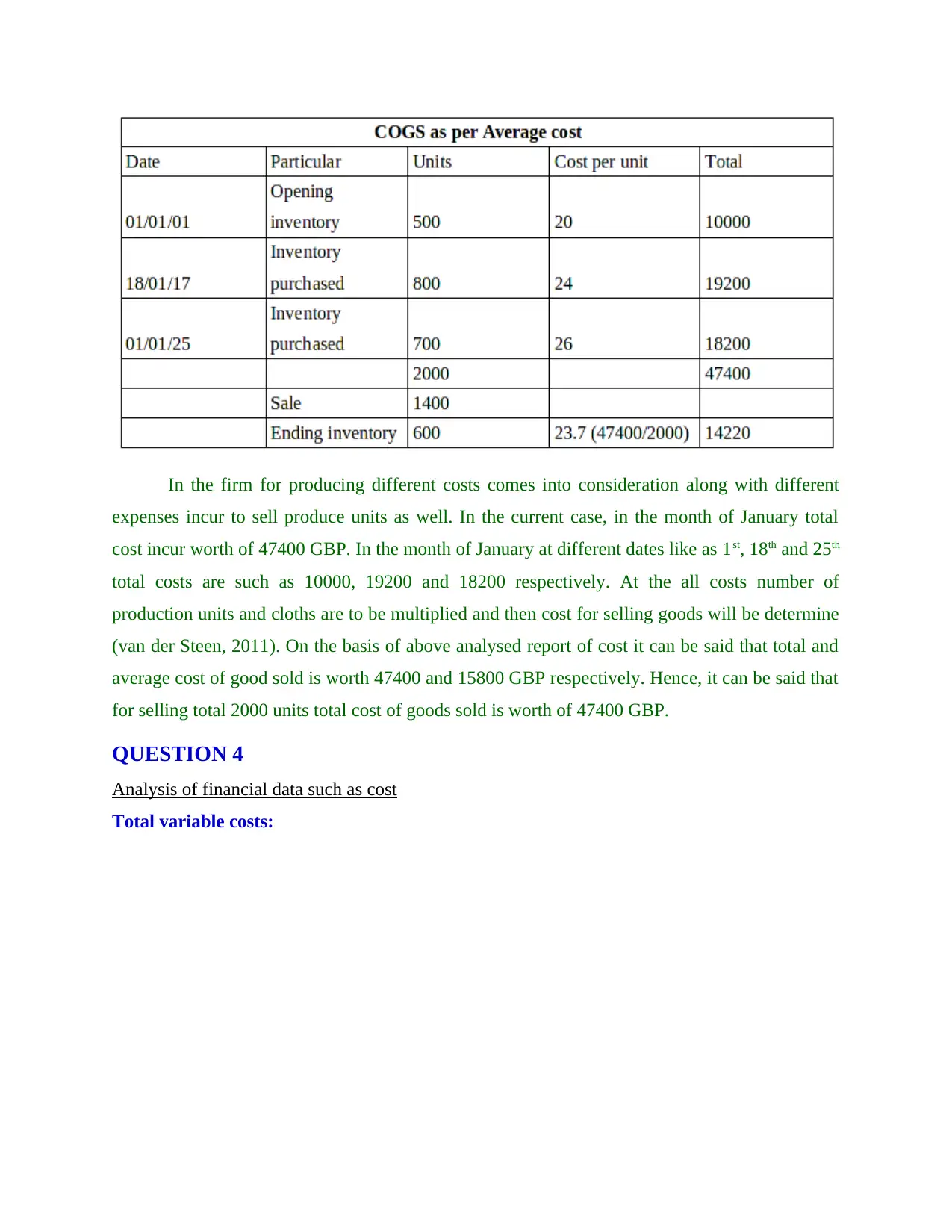

Weighted Average approach: It shows average value of LIFO and FIFO both the values.

According to this, level of the stock at the workplace of Smart Looks is worth of 15800

GBP at which average production is 667 units. Apart from this the ending stock or

inventory is 600 units because from the total 2000 units there are 1400 number of units

FIFO: The method helps to the firm to sell stock at the first time as it comes into

consideration at the workplace. The name FIFO stands for the first in first out which is

the mostly used by the firms for assessing actual value of stock (Hammad, Jusoh and Yen

Nee Oon, 2010). In the Smart Looks company there are value of stock on the basis of

FIFO is 15600 units.

LIFO: According to the last in first out method stock value of the Smart Looks company

is worth of 18200 GBP. At this stage total production level is 700 units at which cost of

every unit is incurred worth of 26 GBP. As per the respective method the firm sell last in

stock at the earlier due to this business entities less uses it. The value of inventory under

stated method is 12400 units.

Weighted Average approach: It shows average value of LIFO and FIFO both the values.

According to this, level of the stock at the workplace of Smart Looks is worth of 15800

GBP at which average production is 667 units. Apart from this the ending stock or

inventory is 600 units because from the total 2000 units there are 1400 number of units

are sold. Moreover, as per this method closing stock of Smart Looks Limited is like

14220 units.

Cost of goods sold for the month ending January for three stock valuation methods

14220 units.

Cost of goods sold for the month ending January for three stock valuation methods

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In the firm for producing different costs comes into consideration along with different

expenses incur to sell produce units as well. In the current case, in the month of January total

cost incur worth of 47400 GBP. In the month of January at different dates like as 1st, 18th and 25th

total costs are such as 10000, 19200 and 18200 respectively. At the all costs number of

production units and cloths are to be multiplied and then cost for selling goods will be determine

(van der Steen, 2011). On the basis of above analysed report of cost it can be said that total and

average cost of good sold is worth 47400 and 15800 GBP respectively. Hence, it can be said that

for selling total 2000 units total cost of goods sold is worth of 47400 GBP.

QUESTION 4

Analysis of financial data such as cost

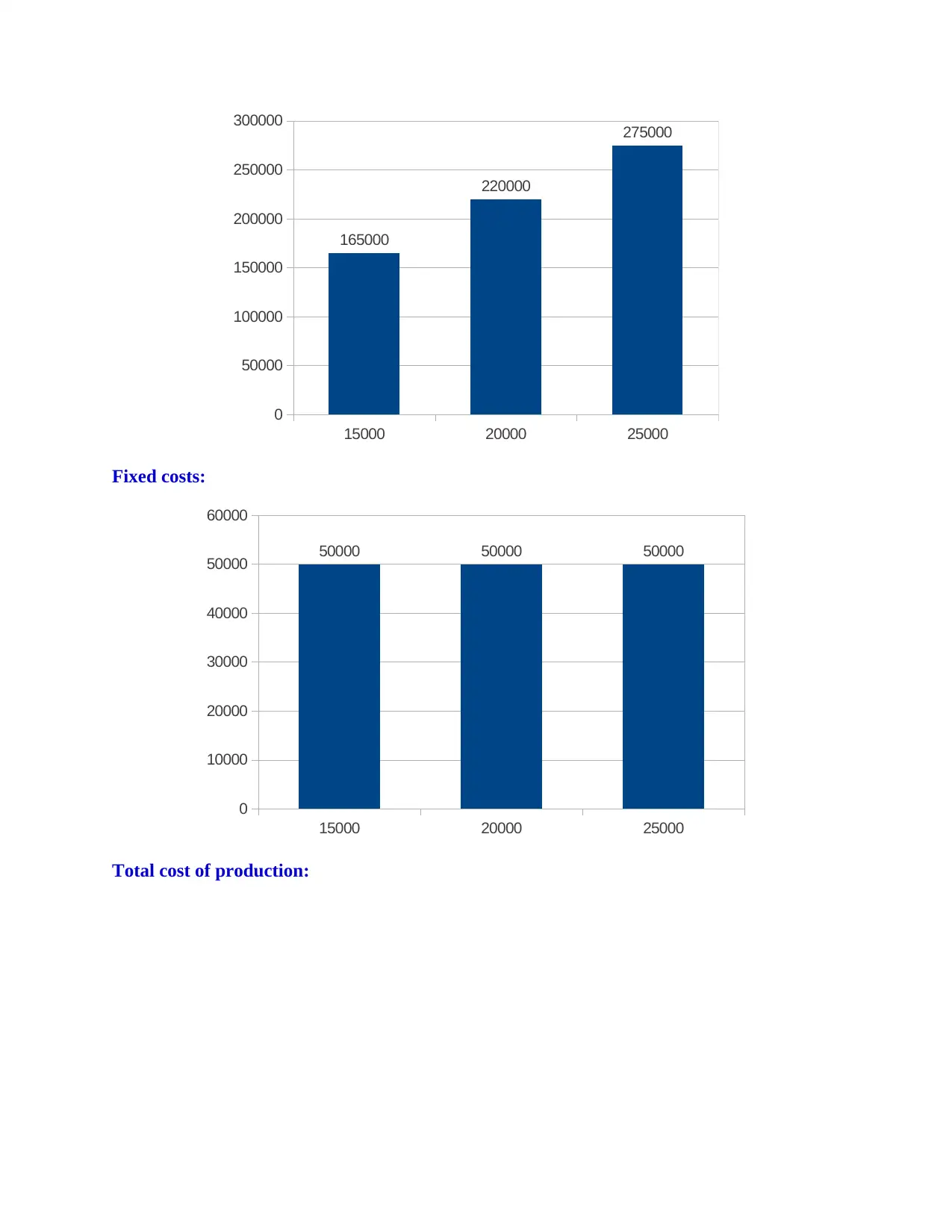

Total variable costs:

expenses incur to sell produce units as well. In the current case, in the month of January total

cost incur worth of 47400 GBP. In the month of January at different dates like as 1st, 18th and 25th

total costs are such as 10000, 19200 and 18200 respectively. At the all costs number of

production units and cloths are to be multiplied and then cost for selling goods will be determine

(van der Steen, 2011). On the basis of above analysed report of cost it can be said that total and

average cost of good sold is worth 47400 and 15800 GBP respectively. Hence, it can be said that

for selling total 2000 units total cost of goods sold is worth of 47400 GBP.

QUESTION 4

Analysis of financial data such as cost

Total variable costs:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

15000 20000 25000

0

50000

100000

150000

200000

250000

300000

165000

220000

275000

Fixed costs:

15000 20000 25000

0

10000

20000

30000

40000

50000

60000

50000 50000 50000

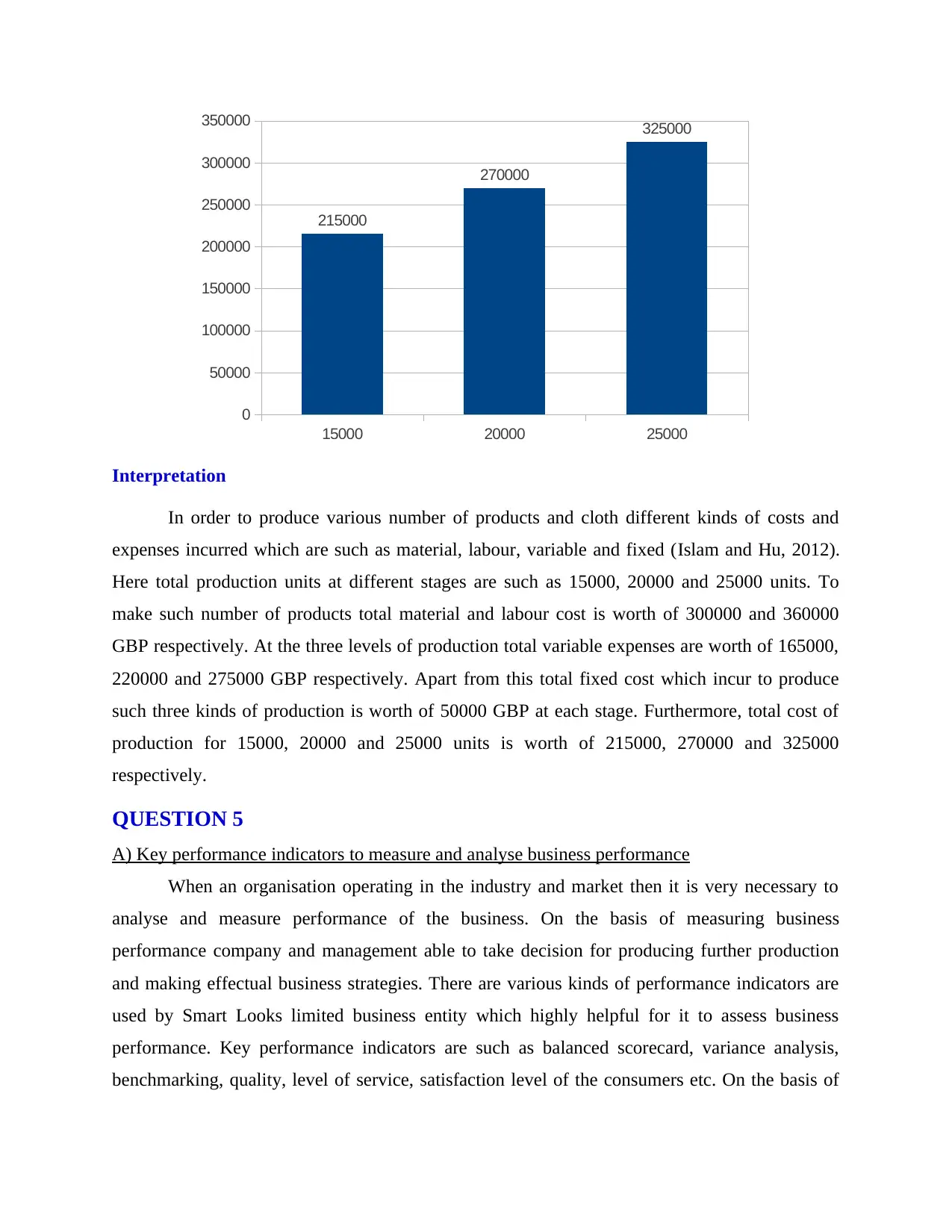

Total cost of production:

0

50000

100000

150000

200000

250000

300000

165000

220000

275000

Fixed costs:

15000 20000 25000

0

10000

20000

30000

40000

50000

60000

50000 50000 50000

Total cost of production:

15000 20000 25000

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

Interpretation

In order to produce various number of products and cloth different kinds of costs and

expenses incurred which are such as material, labour, variable and fixed (Islam and Hu, 2012).

Here total production units at different stages are such as 15000, 20000 and 25000 units. To

make such number of products total material and labour cost is worth of 300000 and 360000

GBP respectively. At the three levels of production total variable expenses are worth of 165000,

220000 and 275000 GBP respectively. Apart from this total fixed cost which incur to produce

such three kinds of production is worth of 50000 GBP at each stage. Furthermore, total cost of

production for 15000, 20000 and 25000 units is worth of 215000, 270000 and 325000

respectively.

QUESTION 5

A) Key performance indicators to measure and analyse business performance

When an organisation operating in the industry and market then it is very necessary to

analyse and measure performance of the business. On the basis of measuring business

performance company and management able to take decision for producing further production

and making effectual business strategies. There are various kinds of performance indicators are

used by Smart Looks limited business entity which highly helpful for it to assess business

performance. Key performance indicators are such as balanced scorecard, variance analysis,

benchmarking, quality, level of service, satisfaction level of the consumers etc. On the basis of

0

50000

100000

150000

200000

250000

300000

350000

215000

270000

325000

Interpretation

In order to produce various number of products and cloth different kinds of costs and

expenses incurred which are such as material, labour, variable and fixed (Islam and Hu, 2012).

Here total production units at different stages are such as 15000, 20000 and 25000 units. To

make such number of products total material and labour cost is worth of 300000 and 360000

GBP respectively. At the three levels of production total variable expenses are worth of 165000,

220000 and 275000 GBP respectively. Apart from this total fixed cost which incur to produce

such three kinds of production is worth of 50000 GBP at each stage. Furthermore, total cost of

production for 15000, 20000 and 25000 units is worth of 215000, 270000 and 325000

respectively.

QUESTION 5

A) Key performance indicators to measure and analyse business performance

When an organisation operating in the industry and market then it is very necessary to

analyse and measure performance of the business. On the basis of measuring business

performance company and management able to take decision for producing further production

and making effectual business strategies. There are various kinds of performance indicators are

used by Smart Looks limited business entity which highly helpful for it to assess business

performance. Key performance indicators are such as balanced scorecard, variance analysis,

benchmarking, quality, level of service, satisfaction level of the consumers etc. On the basis of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.