Management Accounting Report: Techniques for Unicorn Grocery Analysis

VerifiedAdded on 2020/01/23

|16

|5556

|267

Report

AI Summary

This report delves into the principles of management accounting, using Unicorn Grocery as a case study. It begins by defining management accounting and outlining essential system requirements, followed by an explanation of various reporting methods. The core of the report involves preparing income statements using both absorption and marginal costing techniques, providing a comparative analysis of these methods. Furthermore, the report explores different planning tools used for budgetary control, evaluating their advantages and disadvantages in the context of the chosen scenario. It also analyzes how organizations adapt management accounting systems to address financial challenges, and provides insights on how Unicorn Grocery can achieve sustainable success. The report encompasses financial planning, fund flow analysis, decision-making accounting, management reporting, ratio analysis, and cost accounting, offering a comprehensive overview of management accounting's role in business operations and strategic planning.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 & M1 Explain management accounting and give the essential requirements of different

types of management accounting systems for the chosen scenario........................................1

P2 & D1 Explain different methods used for management accounting reporting.................3

TASK 2............................................................................................................................................5

P3, M2 & D2 Income Statements as per the techniques of absorption and marginal costing5

TASK 3............................................................................................................................................8

P4,M3 & D3 Advantages and disadvantages of different types of planning tools used for

budgetary control for the chosen scenario..............................................................................8

Analysis over the use of different planning tools and their application for preparing a budget. 9

TASK 4..........................................................................................................................................10

P5 & M4 Compare how organisations are adapting management accounting systems to

respond to financial problems and elaborate the way through which Unicorn Grocery can

achieve sustainable success..................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 & M1 Explain management accounting and give the essential requirements of different

types of management accounting systems for the chosen scenario........................................1

P2 & D1 Explain different methods used for management accounting reporting.................3

TASK 2............................................................................................................................................5

P3, M2 & D2 Income Statements as per the techniques of absorption and marginal costing5

TASK 3............................................................................................................................................8

P4,M3 & D3 Advantages and disadvantages of different types of planning tools used for

budgetary control for the chosen scenario..............................................................................8

Analysis over the use of different planning tools and their application for preparing a budget. 9

TASK 4..........................................................................................................................................10

P5 & M4 Compare how organisations are adapting management accounting systems to

respond to financial problems and elaborate the way through which Unicorn Grocery can

achieve sustainable success..................................................................................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a branch of accounting which considers and combines the

method of accounting and the principles of management. Through this they can analyse the

organisational and its environmental situation in a better way which actually covers the entire

process with various steps that deals with the overall profitability and efficiency of process

which are carried on in an entity(Baldvinsdottir Mitchell and Nørreklit 2010). This report is

based on the case study of Unicorn Grocery which deals in sale of various grocery products. It is

basically a co-operative grocery store which deals in sale and purchase activity of daily usable

products. Cited entity is having its headquarters at Chorlton-cum-Hardy, Manchester, England.

In this report the income statements has been prepared through using the methods of absorption

and marginal costing. Further this report also presents the fact that how implementation of

management accounting techniques can be helpful in sustaining the sustainable development.

TASK 1

P1 & M1 Explain management accounting and give the essential requirements of different types

of management accounting systems for the chosen scenario

Definition: Management accounting is also known as a cost accounting management accounting

is the process of analysis and identify information to collect data and measuring,interpreting

same related data to communicate information for to convey of an organisation. Accounting

management provide of financial and non financial decision to regarding information to relate

planning and performance management system. Management accounting provide financial

report an control to assist management in the implement and formulating(Bennett Schaltegger

and Zvezdov 2013) . Interpreting of an entity strategies. There are two different key element of

cost accounting managerial and financial.

Types of cost accounting: There are various type of cost accounting cost accounting,inventory

management system job sharing system price optimizing system.

Cost accounting system : Cost accounting system in this system is also called a costing

system or costing system is used to analysis profit of an organisation and to inventory

valuation and cost control of their products(Busco and Scapens 2011). Cost accounting is

the process of collecting various alternatives to recording summarizing

classifying ,allocating evaluating alternatives course of action and control of cost to

provide the detailed information the management needs to control operation planing for

1

Management accounting is a branch of accounting which considers and combines the

method of accounting and the principles of management. Through this they can analyse the

organisational and its environmental situation in a better way which actually covers the entire

process with various steps that deals with the overall profitability and efficiency of process

which are carried on in an entity(Baldvinsdottir Mitchell and Nørreklit 2010). This report is

based on the case study of Unicorn Grocery which deals in sale of various grocery products. It is

basically a co-operative grocery store which deals in sale and purchase activity of daily usable

products. Cited entity is having its headquarters at Chorlton-cum-Hardy, Manchester, England.

In this report the income statements has been prepared through using the methods of absorption

and marginal costing. Further this report also presents the fact that how implementation of

management accounting techniques can be helpful in sustaining the sustainable development.

TASK 1

P1 & M1 Explain management accounting and give the essential requirements of different types

of management accounting systems for the chosen scenario

Definition: Management accounting is also known as a cost accounting management accounting

is the process of analysis and identify information to collect data and measuring,interpreting

same related data to communicate information for to convey of an organisation. Accounting

management provide of financial and non financial decision to regarding information to relate

planning and performance management system. Management accounting provide financial

report an control to assist management in the implement and formulating(Bennett Schaltegger

and Zvezdov 2013) . Interpreting of an entity strategies. There are two different key element of

cost accounting managerial and financial.

Types of cost accounting: There are various type of cost accounting cost accounting,inventory

management system job sharing system price optimizing system.

Cost accounting system : Cost accounting system in this system is also called a costing

system or costing system is used to analysis profit of an organisation and to inventory

valuation and cost control of their products(Busco and Scapens 2011). Cost accounting is

the process of collecting various alternatives to recording summarizing

classifying ,allocating evaluating alternatives course of action and control of cost to

provide the detailed information the management needs to control operation planing for

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the future course of action. cost accounting help to preparation financial report in this

report to use not subject rules and use only general accepted accounting principles and

accounting information is commonly used in financial accounting information to facilities

making decision(Pipan and Czarniawska, 2010). There are two main accounting system

job order,process costing in a cost accounting system to a information allocation based on

the traditional system activity based cost system.

Inventory management system: Inventory to also represent to stock goods or material and

such as term to stock and inventory, an inventory management system combines to use

of software barcode scanners ,printers and mobile devices to the management of

inventory like goods consumables suppliers stock. The goal of inventory accurately

under stock and overstock situations(Setthasakko 2010). inventory tracing quantities

across locations insight able to make inventory decision.

There are various types benefits and function system to involves: to create purchases

order,create,to improve company workflow,inventory accuracy of an entity.

Job creation system :In this process information about the cost associate with a special

product or service job . In this system to direct material,direct labours,overheads costs are

including to improve a cost creation system.

Pricing optimizing: Pricing optimising system are analysis mathematical information

programs that calculate different price levels combine that various data and information

on costs and inventory level to prices to improve profits(Weißenberger and Angelkort,

2011) .in this system analysis the value of product to buy and seller and manage all

impacting profitability to measuring pricing strategies.

Difference method use in management accounting: There are different method are explained:

Financial planning: the main objective of entity is hight profit to achieve by make proper

sound panning to considered best object achieving business objectives. financial planning

to helps to utilisation resources in better way.

Fund flow analysis: Thought analysis of movement of fund one period to another the

fund is properly or not in a year when compared to past year. The working capital change

fund are also find out this any sis

Decision making accounting: The decision making accounting system is free flow

communication within the entity is effective functioning or business. And the

2

report to use not subject rules and use only general accepted accounting principles and

accounting information is commonly used in financial accounting information to facilities

making decision(Pipan and Czarniawska, 2010). There are two main accounting system

job order,process costing in a cost accounting system to a information allocation based on

the traditional system activity based cost system.

Inventory management system: Inventory to also represent to stock goods or material and

such as term to stock and inventory, an inventory management system combines to use

of software barcode scanners ,printers and mobile devices to the management of

inventory like goods consumables suppliers stock. The goal of inventory accurately

under stock and overstock situations(Setthasakko 2010). inventory tracing quantities

across locations insight able to make inventory decision.

There are various types benefits and function system to involves: to create purchases

order,create,to improve company workflow,inventory accuracy of an entity.

Job creation system :In this process information about the cost associate with a special

product or service job . In this system to direct material,direct labours,overheads costs are

including to improve a cost creation system.

Pricing optimizing: Pricing optimising system are analysis mathematical information

programs that calculate different price levels combine that various data and information

on costs and inventory level to prices to improve profits(Weißenberger and Angelkort,

2011) .in this system analysis the value of product to buy and seller and manage all

impacting profitability to measuring pricing strategies.

Difference method use in management accounting: There are different method are explained:

Financial planning: the main objective of entity is hight profit to achieve by make proper

sound panning to considered best object achieving business objectives. financial planning

to helps to utilisation resources in better way.

Fund flow analysis: Thought analysis of movement of fund one period to another the

fund is properly or not in a year when compared to past year. The working capital change

fund are also find out this any sis

Decision making accounting: The decision making accounting system is free flow

communication within the entity is effective functioning or business. And the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management can design the information system hence which all employee of an entity

can access the information using discharging their duties and to access the different types

of quality decision

Management reporting: The management of reporting is the prepare on the specific

accounting report to related basic concept of contents are including this report(Kaplan

and Atkinson 2015). Content of profit loss account and balance sheet and other basic

data and information to be submitted the same before top management. The prepare a

report disclose the are positive and negative strength ,weakness in different area of

financial and operating activity. In this activity to identify, hight useful to management

for excising control and decision making.

Ratio analysis: The ratio analysis is a used to management in the discharge or basic

functions of planning coordinating ,forecasting and effective control. the way for

business activity by undertaking appraisal of target the physical(Dillard and Roslender

2011).

Cost accounting: The cost accounting method thought represent current data in

product ,process department wise to comparison two cost enables management decisions

to the reasons responsible difference various cost (Cost-Volume Profit Analysis.).

Marginal-costing: In this method used marginal costing techniques in which fix the

product selling price,section of best sales mix strategies, to select use of product related

sources of raw materials. To make a buying decision which is based on cost of variable

and contribution.

P2 & D1 Explain different methods used for management accounting reporting

Management accounting reports prepared by every type of an enterprise to evaluate the

performance of their company. Management accounting reports can be made on quarterly,

monthly or on a daily basis.

Types of Management accounting reports which can be used by the Unicorn grocery

Budget report:Budgets are made by small business enterprises or help them to study and

evaluate the performance of their company. Every enterprise owner evaluate the budget

and try to minimize the cost or expenses of the enterprise,if the budget is very large then

it is evaluated by mangers according to the department wise(van der Meer-Kooistra and

Vosselman 2012). After the budget get prepared every enterprise owner try to cut down

3

can access the information using discharging their duties and to access the different types

of quality decision

Management reporting: The management of reporting is the prepare on the specific

accounting report to related basic concept of contents are including this report(Kaplan

and Atkinson 2015). Content of profit loss account and balance sheet and other basic

data and information to be submitted the same before top management. The prepare a

report disclose the are positive and negative strength ,weakness in different area of

financial and operating activity. In this activity to identify, hight useful to management

for excising control and decision making.

Ratio analysis: The ratio analysis is a used to management in the discharge or basic

functions of planning coordinating ,forecasting and effective control. the way for

business activity by undertaking appraisal of target the physical(Dillard and Roslender

2011).

Cost accounting: The cost accounting method thought represent current data in

product ,process department wise to comparison two cost enables management decisions

to the reasons responsible difference various cost (Cost-Volume Profit Analysis.).

Marginal-costing: In this method used marginal costing techniques in which fix the

product selling price,section of best sales mix strategies, to select use of product related

sources of raw materials. To make a buying decision which is based on cost of variable

and contribution.

P2 & D1 Explain different methods used for management accounting reporting

Management accounting reports prepared by every type of an enterprise to evaluate the

performance of their company. Management accounting reports can be made on quarterly,

monthly or on a daily basis.

Types of Management accounting reports which can be used by the Unicorn grocery

Budget report:Budgets are made by small business enterprises or help them to study and

evaluate the performance of their company. Every enterprise owner evaluate the budget

and try to minimize the cost or expenses of the enterprise,if the budget is very large then

it is evaluated by mangers according to the department wise(van der Meer-Kooistra and

Vosselman 2012). After the budget get prepared every enterprise owner try to cut down

3

or trim the cost of the budget. In some budgets the incentives given by the enterprises to

its employees also comes under the budget.

Accounts receivable: Accounts receivable is a critical tool available for the enterprises to

evaluate or to know how the enterprise is managing its cash flow activity from its

debtors(Quinn 2011). Under this the enterprise evaluate or study to know what is the

problem arising from the process of collecting money from the debtors and try to remove

if any hurdle get found and to make the policy more effective the enterprise tighten its

policy of collecting money from the customers.

Job cost reports:Job cost reports are prepared for evaluating the profitability of a job or to

measure what revenue is created in the organisation by that particular job. This is done by

the firms to calculate the more profitable jobs of the enterprise and than focusing on that

jobs rather than wasting time on the jobs with low profitable jobs. This help the

organisation in identifying the higher earning areas of the enterprise and also to analyse

the expenses before a project can be started this help the managers to reduce or eliminate

the waste of the project.

Inventory and manufacturing: Inventory and manufacturing accounting reports are used

by the enterprises to reduce the cost related with the storage of inventory like inventory

waste ,overhead cost and labour cost related with the inventory(Shah Malik and Malik

2011). This help the enterprises in making their process of holding inventory more

efficient. This report make the enterprise in holding their cost with minimum cost.

Management can use management accounting and reporting system in the enterprise in

following areas:

Relevant cost analysis: Management Accounting and reporting provide enterprise the

relevant in formation related to the cost related with each decision and helps the

management in making more efficient decision for the enterprise. Like if the Unicorn

grocery wants do the advertising of its products than there are various methods available

to them for advertising each related with its cost and benefits so this evaluation will help

the Unicorn grocery management in making a efficient decision for the advertising of

their products(Contrafatto and Burn 2013). This can also be used by the enterprise to

making other decisions like adding a new product line in the enterprise will proof

beneficial or not.

4

its employees also comes under the budget.

Accounts receivable: Accounts receivable is a critical tool available for the enterprises to

evaluate or to know how the enterprise is managing its cash flow activity from its

debtors(Quinn 2011). Under this the enterprise evaluate or study to know what is the

problem arising from the process of collecting money from the debtors and try to remove

if any hurdle get found and to make the policy more effective the enterprise tighten its

policy of collecting money from the customers.

Job cost reports:Job cost reports are prepared for evaluating the profitability of a job or to

measure what revenue is created in the organisation by that particular job. This is done by

the firms to calculate the more profitable jobs of the enterprise and than focusing on that

jobs rather than wasting time on the jobs with low profitable jobs. This help the

organisation in identifying the higher earning areas of the enterprise and also to analyse

the expenses before a project can be started this help the managers to reduce or eliminate

the waste of the project.

Inventory and manufacturing: Inventory and manufacturing accounting reports are used

by the enterprises to reduce the cost related with the storage of inventory like inventory

waste ,overhead cost and labour cost related with the inventory(Shah Malik and Malik

2011). This help the enterprises in making their process of holding inventory more

efficient. This report make the enterprise in holding their cost with minimum cost.

Management can use management accounting and reporting system in the enterprise in

following areas:

Relevant cost analysis: Management Accounting and reporting provide enterprise the

relevant in formation related to the cost related with each decision and helps the

management in making more efficient decision for the enterprise. Like if the Unicorn

grocery wants do the advertising of its products than there are various methods available

to them for advertising each related with its cost and benefits so this evaluation will help

the Unicorn grocery management in making a efficient decision for the advertising of

their products(Contrafatto and Burn 2013). This can also be used by the enterprise to

making other decisions like adding a new product line in the enterprise will proof

beneficial or not.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity based costing methods :Activity based costing helps the enterprise in making a

decision that what will be the customers of the products or to whom the company will

serve it services. It is basically a method used for analysing which customers will proof

more beneficial to the company(Lukka and Modell 2010). Once the customers get

known by the firm or when the company is able to identify its more beneficial customers

the company will than focus the advertising efforts on that customers.

Make or buy analysis :One of the more important use of management accounting that it

helps the enterprise in making a decision about make or buy the equipments needed in the

manufacturing process. If making a product will proof more expensive and costly to the

enterprise than in this situation it will be better for the enterprise to buy it from the

outside on the other hand if making equipments in the enterprise is very cheap for the

firm than the company should produce the same in the enterprise.

Utilizing the data: The information provided by the management accounting and

reporting system can be further used by the enterprise in making decision relating to the

growth and development of the enterprise(Setthasakko 2010). The management

accounting and reporting give the manager important information and the manager of the

company can use the same in guiding the future of the company.

TASK 2

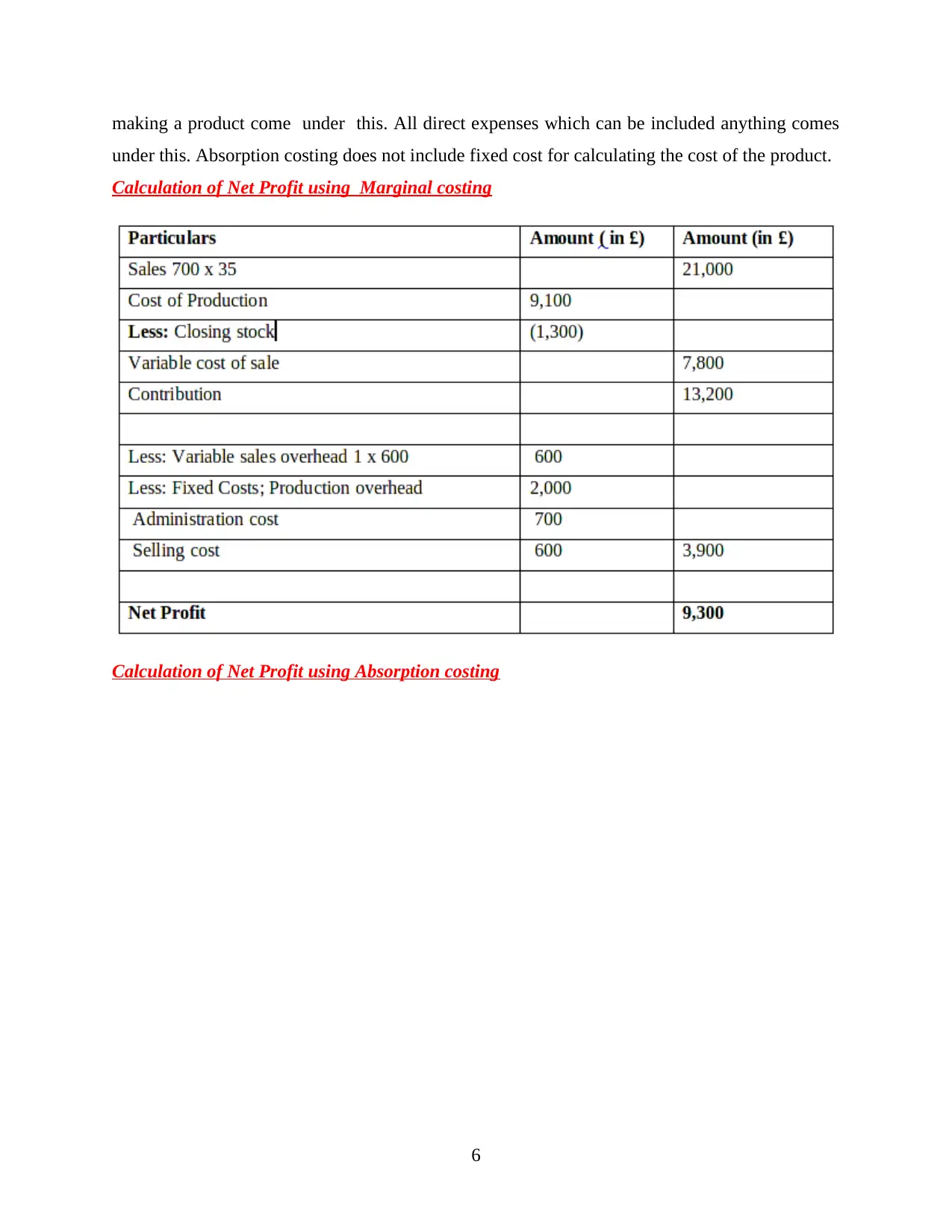

P3, M2 & D2 Income Statements as per the techniques of absorption and marginal costing

Marginal costing: Marginal costing is a costing method used in decision making of an

organisation. Marginal costing calculates or measure the changes arises in cost by making a new

additional product. Marginal cost is that cost which can be avoided by not making the additional

unit of product. Basically an increase and decrease in the total cost of production by making a

new product is known as marginal costing. If the price increases the company will not produce

the product on the other hand if the price decreases than it will proof beneficial for the company

to making that additional unit of product.

Absorption costing: Absorption costing is the cost which arise on a product or the price of a

product including all indirected expenses and direct cost. Absorption costing is the calculated

cost arises in manufacturing a product include all expenses from raw material to labour cost and

many more all comes under the absorption costing(Sánchez-Rodríguez and Spraakman 2012).

Absorption costing include all the direct expenses incur on making a product. All utility costs for

5

decision that what will be the customers of the products or to whom the company will

serve it services. It is basically a method used for analysing which customers will proof

more beneficial to the company(Lukka and Modell 2010). Once the customers get

known by the firm or when the company is able to identify its more beneficial customers

the company will than focus the advertising efforts on that customers.

Make or buy analysis :One of the more important use of management accounting that it

helps the enterprise in making a decision about make or buy the equipments needed in the

manufacturing process. If making a product will proof more expensive and costly to the

enterprise than in this situation it will be better for the enterprise to buy it from the

outside on the other hand if making equipments in the enterprise is very cheap for the

firm than the company should produce the same in the enterprise.

Utilizing the data: The information provided by the management accounting and

reporting system can be further used by the enterprise in making decision relating to the

growth and development of the enterprise(Setthasakko 2010). The management

accounting and reporting give the manager important information and the manager of the

company can use the same in guiding the future of the company.

TASK 2

P3, M2 & D2 Income Statements as per the techniques of absorption and marginal costing

Marginal costing: Marginal costing is a costing method used in decision making of an

organisation. Marginal costing calculates or measure the changes arises in cost by making a new

additional product. Marginal cost is that cost which can be avoided by not making the additional

unit of product. Basically an increase and decrease in the total cost of production by making a

new product is known as marginal costing. If the price increases the company will not produce

the product on the other hand if the price decreases than it will proof beneficial for the company

to making that additional unit of product.

Absorption costing: Absorption costing is the cost which arise on a product or the price of a

product including all indirected expenses and direct cost. Absorption costing is the calculated

cost arises in manufacturing a product include all expenses from raw material to labour cost and

many more all comes under the absorption costing(Sánchez-Rodríguez and Spraakman 2012).

Absorption costing include all the direct expenses incur on making a product. All utility costs for

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

making a product come under this. All direct expenses which can be included anything comes

under this. Absorption costing does not include fixed cost for calculating the cost of the product.

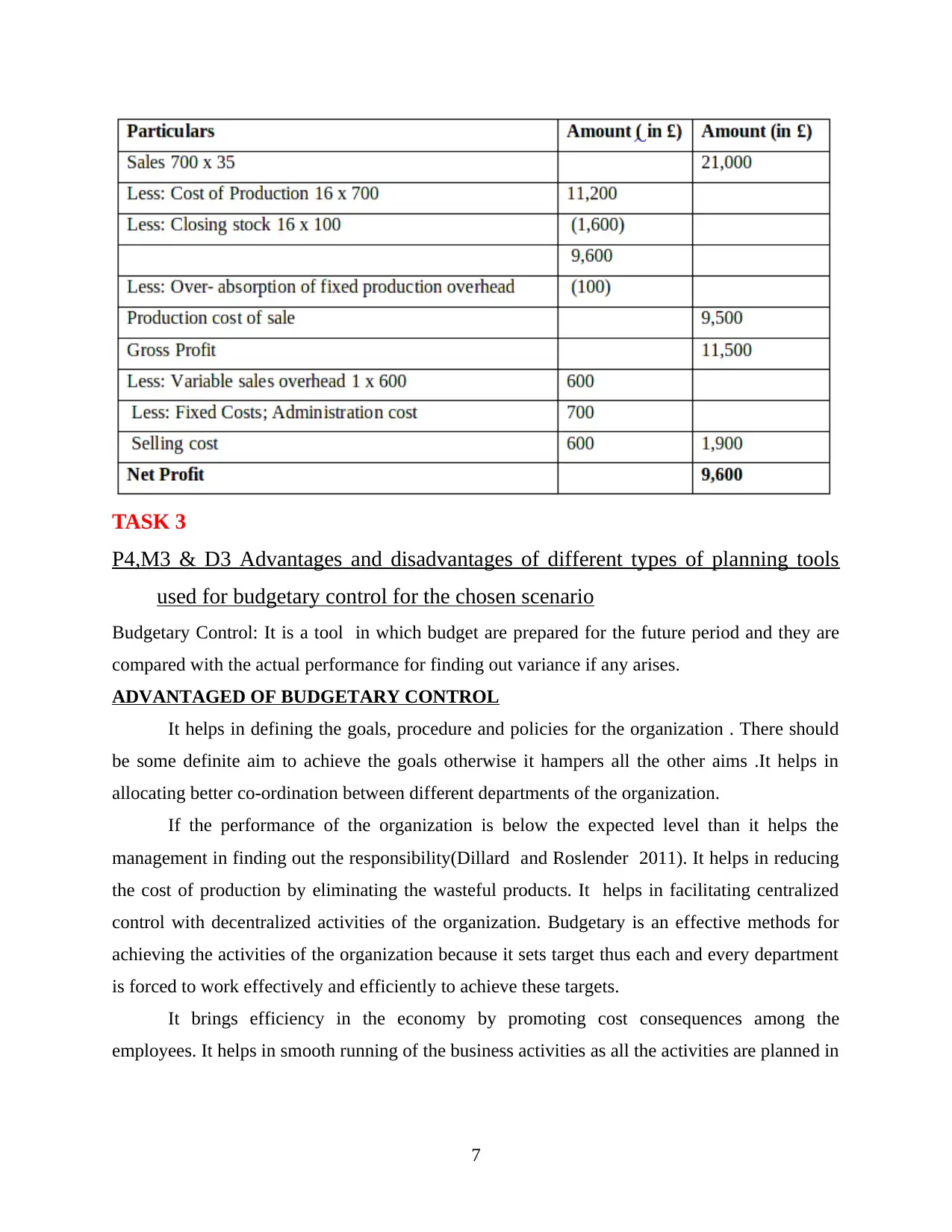

Calculation of Net Profit using Marginal costing

Calculation of Net Profit using Absorption costing

6

under this. Absorption costing does not include fixed cost for calculating the cost of the product.

Calculation of Net Profit using Marginal costing

Calculation of Net Profit using Absorption costing

6

TASK 3

P4,M3 & D3 Advantages and disadvantages of different types of planning tools

used for budgetary control for the chosen scenario

Budgetary Control: It is a tool in which budget are prepared for the future period and they are

compared with the actual performance for finding out variance if any arises.

ADVANTAGED OF BUDGETARY CONTROL

It helps in defining the goals, procedure and policies for the organization . There should

be some definite aim to achieve the goals otherwise it hampers all the other aims .It helps in

allocating better co-ordination between different departments of the organization.

If the performance of the organization is below the expected level than it helps the

management in finding out the responsibility(Dillard and Roslender 2011). It helps in reducing

the cost of production by eliminating the wasteful products. It helps in facilitating centralized

control with decentralized activities of the organization. Budgetary is an effective methods for

achieving the activities of the organization because it sets target thus each and every department

is forced to work effectively and efficiently to achieve these targets.

It brings efficiency in the economy by promoting cost consequences among the

employees. It helps in smooth running of the business activities as all the activities are planned in

7

P4,M3 & D3 Advantages and disadvantages of different types of planning tools

used for budgetary control for the chosen scenario

Budgetary Control: It is a tool in which budget are prepared for the future period and they are

compared with the actual performance for finding out variance if any arises.

ADVANTAGED OF BUDGETARY CONTROL

It helps in defining the goals, procedure and policies for the organization . There should

be some definite aim to achieve the goals otherwise it hampers all the other aims .It helps in

allocating better co-ordination between different departments of the organization.

If the performance of the organization is below the expected level than it helps the

management in finding out the responsibility(Dillard and Roslender 2011). It helps in reducing

the cost of production by eliminating the wasteful products. It helps in facilitating centralized

control with decentralized activities of the organization. Budgetary is an effective methods for

achieving the activities of the organization because it sets target thus each and every department

is forced to work effectively and efficiently to achieve these targets.

It brings efficiency in the economy by promoting cost consequences among the

employees. It helps in smooth running of the business activities as all the activities are planned in

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

advance(van der Meer-Kooistra and Vosselman2012). It helps management as to where the

problem is arising and how than problem can be solved without delay in an effective manner.

DISADVANTAGES OF BUDGETARY CONTROL

When there is inflation in the economy is is difficult to prepare the budgets for the

economy. Budget requires Heavey expenditure to prepare the budgets which small companies

cannot afford.

Budgets are prepared for the future period which is always uncertain in future the

economic conditions can change which will bring ups and down in the budget(Kaplan and

Atkinson 2015). Thus future uncertainties may minimize the use of budgetary control devices.

Budgetary control is a management tool and thus it cannot replace the management in decision

making process because it is a substitute for management.

The budgetary control will succeed if there is support of the top management and if there

is no support of the top management than the budgetary process will not succeed(Dillard and

Roslender 2011). The success of budget depends upon the team work and if there is no co-

ordination between the team members than the budgets will not be achieved for the economy.

Budgets can be developed keeping in view the current organizational structure. This

organization structure may be inappropriate for current conditions(What is Budgetary control?.

2017). The correlation and co-ordination of various budget is expensive so small organization

cannot use this budget as a cost control technique.

Analysis over the use of different planning tools and their application for preparing a budget

Future Forecasting- Budgetary control is a device which is helpful in future estimation of

the budgets and these budgets can be prepared in advance.

Cost Aggregation- To minimise the cost of different activities in Work Breakdown

structure and it also helps to reduce the risk and increase the productivity in the

organization. The work package cost are higher for higher level of WBS and ultimately

for the entire project(Sánchez-Rodríguez and Spraakman 2012).

Reserve Analysis- It is a technique to review the project manage plan to identify the risk

factor involved. Cost estimation plan includes contingency reserves to account for cost

uncertainty.

Expert Judgement – Project manager is responsible for monitoring and controlling the

project work and thus the judgement of of the manager to find out the performance level

8

problem is arising and how than problem can be solved without delay in an effective manner.

DISADVANTAGES OF BUDGETARY CONTROL

When there is inflation in the economy is is difficult to prepare the budgets for the

economy. Budget requires Heavey expenditure to prepare the budgets which small companies

cannot afford.

Budgets are prepared for the future period which is always uncertain in future the

economic conditions can change which will bring ups and down in the budget(Kaplan and

Atkinson 2015). Thus future uncertainties may minimize the use of budgetary control devices.

Budgetary control is a management tool and thus it cannot replace the management in decision

making process because it is a substitute for management.

The budgetary control will succeed if there is support of the top management and if there

is no support of the top management than the budgetary process will not succeed(Dillard and

Roslender 2011). The success of budget depends upon the team work and if there is no co-

ordination between the team members than the budgets will not be achieved for the economy.

Budgets can be developed keeping in view the current organizational structure. This

organization structure may be inappropriate for current conditions(What is Budgetary control?.

2017). The correlation and co-ordination of various budget is expensive so small organization

cannot use this budget as a cost control technique.

Analysis over the use of different planning tools and their application for preparing a budget

Future Forecasting- Budgetary control is a device which is helpful in future estimation of

the budgets and these budgets can be prepared in advance.

Cost Aggregation- To minimise the cost of different activities in Work Breakdown

structure and it also helps to reduce the risk and increase the productivity in the

organization. The work package cost are higher for higher level of WBS and ultimately

for the entire project(Sánchez-Rodríguez and Spraakman 2012).

Reserve Analysis- It is a technique to review the project manage plan to identify the risk

factor involved. Cost estimation plan includes contingency reserves to account for cost

uncertainty.

Expert Judgement – Project manager is responsible for monitoring and controlling the

project work and thus the judgement of of the manager to find out the performance level

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of the employees so that it can be evaluated and thus necessary actions could be taken

improve the performance level and this will be solved from the judgement and decision

of the expertise in budgeting and particularly in the area of interest(Bennett Schaltegger

and Zvezdov 2013).

Historical Relationship-It means including data from past references or from other

projects in which cost are known for some or similar type of the activities.

Funding Limit Reconciliation- The expenditure of fund should be reconciled with any

funding limits on the commitments of the fund for the projects which are undertaken .

Government Policies- Budgets are made for different policies of the government like tax.

Tax is a compulsory payment which is imposed by the government and balance of

payment .BOP is a systematic transition between the import and export policies of the

government(Renz 2016). It is categorised into two parts monetary polity and fiscal

policy. Monetary policy indicates the flow of money in the economy and fiscal policy

indicates the taxation policy which the government impose in the economy.

Planning tool for accounts to solve problems to leads to organizational success.

The success of any organization depend upon its functioning the procedure it follows in

the organization and the co-ordination between different activities and employees of the

organization(Macintosh and Quattrone 2010). The skill and competence level of the employees

who are working in the organization how effectively and efficiently they are using the resources

of the organization for the long term success of the organization.

Helping organization to use updated technology the use of different new software and

application. The process involves certain phases from planning, evaluating, monitoring and

control of the business activities in the organization. Problem solving enhances the area of

interest of the employees because employees feel satisfied that is someone in the organization to

solve their problems.

9

improve the performance level and this will be solved from the judgement and decision

of the expertise in budgeting and particularly in the area of interest(Bennett Schaltegger

and Zvezdov 2013).

Historical Relationship-It means including data from past references or from other

projects in which cost are known for some or similar type of the activities.

Funding Limit Reconciliation- The expenditure of fund should be reconciled with any

funding limits on the commitments of the fund for the projects which are undertaken .

Government Policies- Budgets are made for different policies of the government like tax.

Tax is a compulsory payment which is imposed by the government and balance of

payment .BOP is a systematic transition between the import and export policies of the

government(Renz 2016). It is categorised into two parts monetary polity and fiscal

policy. Monetary policy indicates the flow of money in the economy and fiscal policy

indicates the taxation policy which the government impose in the economy.

Planning tool for accounts to solve problems to leads to organizational success.

The success of any organization depend upon its functioning the procedure it follows in

the organization and the co-ordination between different activities and employees of the

organization(Macintosh and Quattrone 2010). The skill and competence level of the employees

who are working in the organization how effectively and efficiently they are using the resources

of the organization for the long term success of the organization.

Helping organization to use updated technology the use of different new software and

application. The process involves certain phases from planning, evaluating, monitoring and

control of the business activities in the organization. Problem solving enhances the area of

interest of the employees because employees feel satisfied that is someone in the organization to

solve their problems.

9

TASK 4

P5 & M4 Compare how organisations are adapting management accounting

systems to respond to financial problems and elaborate the way through

which Unicorn Grocery can achieve sustainable success

Management accounting System is now a days used by many organisations.

Like unicorn the Agmet also uses the same for calculating or analysing the performance of their

enterprise.

Unicorn Grocery use the accounting management and reporting to making important

decisions like buying and making of product. Other than this how the guidance can be done

about the company's growth or other than this following important decisions are taken by the

information grasped by the accounting management and reporting system(Herbert and Seal

2012). Relevant cost analysis can be done by accounting report system other than this efficient

decision can be made by the unicorn grocery by following the accounting report system. The

firm can analyse what are the main hurdles or drawbacks of its current collecting policy from

debtors and the firm can then try to remove these hurdles and can make their collecting policy

more effective and efficient.

Same like the unicorn the Agmet uses the accounting report system for taking the

efficient decision or same as the unicorn but the Agmet uses it for other purposes also like how

to manage all the activities of the enterprise(Kaplan and Atkinson 2015). How to make effective

and efficient use of human resources and other resources available in the enterprise. How

company can improve its collecting policy from debtors.

Unicorn uses the management ans accounting report system to keep check on the

activities of the enterprise at the same time how these activities can be done better by the

enterprise to get more profitable results with the minimum cost and how these activities can be

proof more profitable to the enterprise(marginal cost. 2017). The Agmet uses the same reporting

system for achieving better results like more profitability with the minimum cost associate with

each operation and how to get more powerful image in the market than its competitors. The

unicorn can make the better use of accounting management and report system to get optimum

results from all of its job activities.

10

P5 & M4 Compare how organisations are adapting management accounting

systems to respond to financial problems and elaborate the way through

which Unicorn Grocery can achieve sustainable success

Management accounting System is now a days used by many organisations.

Like unicorn the Agmet also uses the same for calculating or analysing the performance of their

enterprise.

Unicorn Grocery use the accounting management and reporting to making important

decisions like buying and making of product. Other than this how the guidance can be done

about the company's growth or other than this following important decisions are taken by the

information grasped by the accounting management and reporting system(Herbert and Seal

2012). Relevant cost analysis can be done by accounting report system other than this efficient

decision can be made by the unicorn grocery by following the accounting report system. The

firm can analyse what are the main hurdles or drawbacks of its current collecting policy from

debtors and the firm can then try to remove these hurdles and can make their collecting policy

more effective and efficient.

Same like the unicorn the Agmet uses the accounting report system for taking the

efficient decision or same as the unicorn but the Agmet uses it for other purposes also like how

to manage all the activities of the enterprise(Kaplan and Atkinson 2015). How to make effective

and efficient use of human resources and other resources available in the enterprise. How

company can improve its collecting policy from debtors.

Unicorn uses the management ans accounting report system to keep check on the

activities of the enterprise at the same time how these activities can be done better by the

enterprise to get more profitable results with the minimum cost and how these activities can be

proof more profitable to the enterprise(marginal cost. 2017). The Agmet uses the same reporting

system for achieving better results like more profitability with the minimum cost associate with

each operation and how to get more powerful image in the market than its competitors. The

unicorn can make the better use of accounting management and report system to get optimum

results from all of its job activities.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.