Factors contributing to the development of Management accounting practices

VerifiedAdded on 2022/11/25

|11

|2069

|397

AI Summary

This report discusses the factors behind the introduction of management accounting practices, including competition, compliance, and control. It also assesses the usefulness of the balanced scorecard and explores the key performance indicators and critical success factors of Qantas Airlines.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

May 31

2019

Management Accounting

May 31

2019

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 1

Table of Contents

Introduction................................................................................................................................2

Part A.........................................................................................................................................2

Factors contributing to the development of Management accounting practices....................2

Competition........................................................................................................................2

Compliance........................................................................................................................3

Control................................................................................................................................3

Usefulness of Balanced Scorecard.........................................................................................4

Part B..........................................................................................................................................5

Critical success factors...........................................................................................................5

Key performance indicators...................................................................................................6

Strategy Map..........................................................................................................................7

Balance scorecard of Qantas..................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

Table of Contents

Introduction................................................................................................................................2

Part A.........................................................................................................................................2

Factors contributing to the development of Management accounting practices....................2

Competition........................................................................................................................2

Compliance........................................................................................................................3

Control................................................................................................................................3

Usefulness of Balanced Scorecard.........................................................................................4

Part B..........................................................................................................................................5

Critical success factors...........................................................................................................5

Key performance indicators...................................................................................................6

Strategy Map..........................................................................................................................7

Balance scorecard of Qantas..................................................................................................8

Conclusion..................................................................................................................................9

References................................................................................................................................10

MANAGEMENT ACCOUNTING 2

Introduction

Management accounting is said to be the procedure of preparing accounts as well as reports

that offer suitable and detailed financial data to the executives of the company to make long-

term and short-term decisions. It helps in identifying, evaluating, analysing, understanding,

and communicates required information for attaining the goals of the organization (Uyar,

2010). The intent of this report is to highlight the concept of management accounting and the

factors behind the introduction of management accounting. The report is also being framed to

assess the usefulness of the balanced scorecard. In addition to this, the report is also

discussing regarding the key performance indicators and critical success factors of Qantas

Airlines, with the help of which the strategic map and balanced scorecard will be prepared.

Part A

Factors behind the introduction of Management accounting practices

Competition

One of the common things that are present in the 21st century is competition. Every business

and industry is presently dealing with competition due to presence of competitors. The level

of competition may vary between the rivals depending on the industry in which they operate.

The increasing number of competition impacts the operations as well as productivity of the

business (Bloom, Propper, Seiler and Van Reenen, 2015). In order to effectively deal with the

competition at domestic level and international level businesses work to develop different

practices that could provide proper and precise information of the market. Competition is one

of the major contributing factors that results in the development of management accounting

practices. The main reason for the development of these practices is because it identifies,

evaluates, analyse, understands and communities the information to the executives to take

Introduction

Management accounting is said to be the procedure of preparing accounts as well as reports

that offer suitable and detailed financial data to the executives of the company to make long-

term and short-term decisions. It helps in identifying, evaluating, analysing, understanding,

and communicates required information for attaining the goals of the organization (Uyar,

2010). The intent of this report is to highlight the concept of management accounting and the

factors behind the introduction of management accounting. The report is also being framed to

assess the usefulness of the balanced scorecard. In addition to this, the report is also

discussing regarding the key performance indicators and critical success factors of Qantas

Airlines, with the help of which the strategic map and balanced scorecard will be prepared.

Part A

Factors behind the introduction of Management accounting practices

Competition

One of the common things that are present in the 21st century is competition. Every business

and industry is presently dealing with competition due to presence of competitors. The level

of competition may vary between the rivals depending on the industry in which they operate.

The increasing number of competition impacts the operations as well as productivity of the

business (Bloom, Propper, Seiler and Van Reenen, 2015). In order to effectively deal with the

competition at domestic level and international level businesses work to develop different

practices that could provide proper and precise information of the market. Competition is one

of the major contributing factors that results in the development of management accounting

practices. The main reason for the development of these practices is because it identifies,

evaluates, analyse, understands and communities the information to the executives to take

MANAGEMENT ACCOUNTING 3

proper decisions for the benefit of the organization. This helps business in preparing the

reports and accounts that offer timely and accurate financial as well as non-financial

information. The precise and accurate information are essential for the business to take

decision which is provided by the practices of management accounting. For example, the

introduction of Activity Based Costing is one if the management accounting practise that

recognizes and allocates the cost to the overhead activities and then allots those costs to

different items or goods of the company. This results in providing precise and exact

information in comparison to traditional costing methods.

Compliance

Practices of the Management accounting are also developed to meet the key requirement of

the internal management in order to enhance the decision, attain goals, application of the

resource, use of capacity, internal business processes, and customer value to attain the

corporate objectives in a best manner.

Control

Control is another factor that helps in developing the management accounting practices. As

these practices support business on recording, analysing, summarizing and assigning the cost

related to the procedure, after developing the diverse courses of action in order to control the

costs. The goal is to advice the management of the company related to how to optimize the

practices of the business and procedures depending on the cost competence and capability.

One of the management accounting practice is cost accounting, which offers the detailed

information of the cost that is required by the management in order to control the present

operations and future plans (Drury, 2013).

proper decisions for the benefit of the organization. This helps business in preparing the

reports and accounts that offer timely and accurate financial as well as non-financial

information. The precise and accurate information are essential for the business to take

decision which is provided by the practices of management accounting. For example, the

introduction of Activity Based Costing is one if the management accounting practise that

recognizes and allocates the cost to the overhead activities and then allots those costs to

different items or goods of the company. This results in providing precise and exact

information in comparison to traditional costing methods.

Compliance

Practices of the Management accounting are also developed to meet the key requirement of

the internal management in order to enhance the decision, attain goals, application of the

resource, use of capacity, internal business processes, and customer value to attain the

corporate objectives in a best manner.

Control

Control is another factor that helps in developing the management accounting practices. As

these practices support business on recording, analysing, summarizing and assigning the cost

related to the procedure, after developing the diverse courses of action in order to control the

costs. The goal is to advice the management of the company related to how to optimize the

practices of the business and procedures depending on the cost competence and capability.

One of the management accounting practice is cost accounting, which offers the detailed

information of the cost that is required by the management in order to control the present

operations and future plans (Drury, 2013).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 4

Usefulness of Balanced Scorecard

A balanced scorecard is said to be the performance metric that is used by the management to

recognize and improve different internal processes of the business and their succeeding

external consequences. The balanced scorecard is utilized to assess and provide the opinion to

the business (Kaplan, Norton and Rugelsjoen, 2010). The balanced scorecard is very useful

for the businesses; some of the uses are presented below:

Strategic Planning – The balanced scorecard offer an influential outline for making and

communicating the strategies of the business. The business model is pictured in the Strategy

Map that assists organization executives about the case and cause and effect relationship

among varied strategic goals.

Improved Strategy Execution as well as Communication - With the help of one page

image strategy, business can simply communicate the strategy externally and internally. This

one page plan also provides the understanding of the strategy of the company and support in

engaging employees and other stakeholders to deliver the strategy (Niven, 2011).

Better project alignment - The balanced scorecard support businesses in mapping their

projects to varied strategic goals, which in result confirms that the projects are strictly

focused on offering strategic objectives.

Better Management Information - This approach of management accounting support

businesses in developing key performance indicators of the company for their strategic goals.

This confirms that businesses are evaluating the actual aspects. According to the research,

organizations with the framework of balance scorecard are inclined to report higher

information of the quality management and improved decision.

Performance reporting - The BCS can be used to monitor the design of the reports of the

performance and dashboards. This confirms that the management reporting concentrate in the

Usefulness of Balanced Scorecard

A balanced scorecard is said to be the performance metric that is used by the management to

recognize and improve different internal processes of the business and their succeeding

external consequences. The balanced scorecard is utilized to assess and provide the opinion to

the business (Kaplan, Norton and Rugelsjoen, 2010). The balanced scorecard is very useful

for the businesses; some of the uses are presented below:

Strategic Planning – The balanced scorecard offer an influential outline for making and

communicating the strategies of the business. The business model is pictured in the Strategy

Map that assists organization executives about the case and cause and effect relationship

among varied strategic goals.

Improved Strategy Execution as well as Communication - With the help of one page

image strategy, business can simply communicate the strategy externally and internally. This

one page plan also provides the understanding of the strategy of the company and support in

engaging employees and other stakeholders to deliver the strategy (Niven, 2011).

Better project alignment - The balanced scorecard support businesses in mapping their

projects to varied strategic goals, which in result confirms that the projects are strictly

focused on offering strategic objectives.

Better Management Information - This approach of management accounting support

businesses in developing key performance indicators of the company for their strategic goals.

This confirms that businesses are evaluating the actual aspects. According to the research,

organizations with the framework of balance scorecard are inclined to report higher

information of the quality management and improved decision.

Performance reporting - The BCS can be used to monitor the design of the reports of the

performance and dashboards. This confirms that the management reporting concentrate in the

MANAGEMENT ACCOUNTING 5

most noteworthy strategic matters and support companies in monitoring the execution of their

policies (Bernard Marr & Co., 2019).

Better process alignment - A properly executed balanced scorecard support in aligning the

organizational procedure like risk management and budgeting with the strategic goals. This in

turn supports in presenting organization as the truly strategic concentrated business.

Part B

Critical success factors

Qantas is known as one of the large ASX listed company that is operating the business in the

domestic as well as in the international market. According to the annual report of the

company below given are the key critical success factors: -

Competent workforce: - Qantas Company is successful in the market because of its

personnel as it has been seen that diverse personnel who can manage the business in

competent environment. In the aviation industry, it is essential for the companies to recruit

and hire such a diverse workforce that are highly qualified and can manage the operations

effectively (Qantas, 2018). The employees of Qantas are equipped with effective

communication skills, ability to handle responsibility and deliver the delight experience to

customers.

Route system: - The route system of the Qantas airline is reason behind the success of the

company. The company is connected with more than 186 destinations in more than 40

countries that include Australia and many other destinations (Qantas, 2018).

Cost structure: - The cost structure of the company relatively valuable as it is the way

through which they can manage the competitive pricing or innovation creativity. Qantas is

preferable for the customers because they manage the cost and focuses on price.

most noteworthy strategic matters and support companies in monitoring the execution of their

policies (Bernard Marr & Co., 2019).

Better process alignment - A properly executed balanced scorecard support in aligning the

organizational procedure like risk management and budgeting with the strategic goals. This in

turn supports in presenting organization as the truly strategic concentrated business.

Part B

Critical success factors

Qantas is known as one of the large ASX listed company that is operating the business in the

domestic as well as in the international market. According to the annual report of the

company below given are the key critical success factors: -

Competent workforce: - Qantas Company is successful in the market because of its

personnel as it has been seen that diverse personnel who can manage the business in

competent environment. In the aviation industry, it is essential for the companies to recruit

and hire such a diverse workforce that are highly qualified and can manage the operations

effectively (Qantas, 2018). The employees of Qantas are equipped with effective

communication skills, ability to handle responsibility and deliver the delight experience to

customers.

Route system: - The route system of the Qantas airline is reason behind the success of the

company. The company is connected with more than 186 destinations in more than 40

countries that include Australia and many other destinations (Qantas, 2018).

Cost structure: - The cost structure of the company relatively valuable as it is the way

through which they can manage the competitive pricing or innovation creativity. Qantas is

preferable for the customers because they manage the cost and focuses on price.

MANAGEMENT ACCOUNTING 6

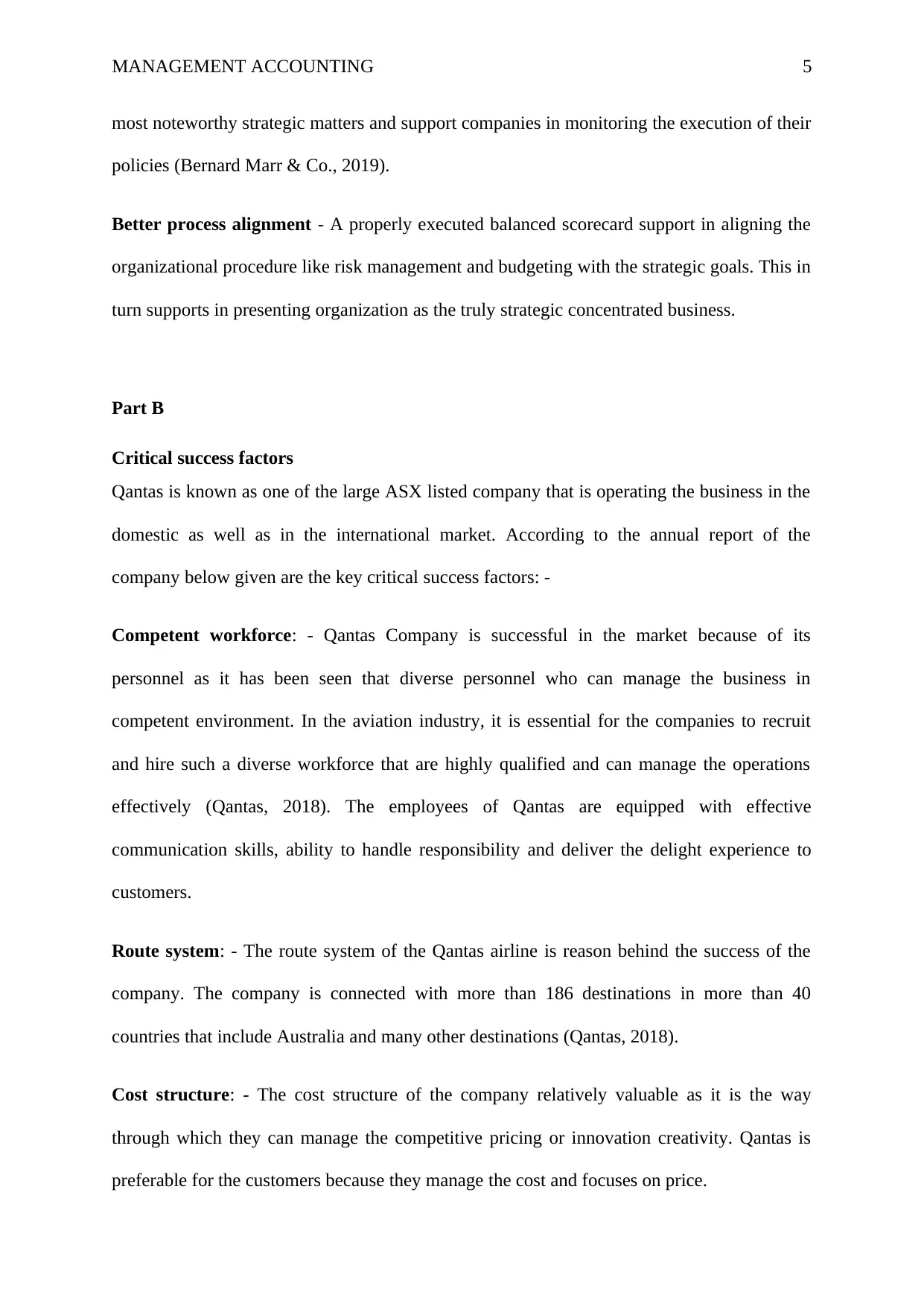

Key performance indicators

Qantas performance indicators are -

The profit before tax of Qantas has increased in 2018 from $1,604M that was low in the year

2017 with $ 1,401M. In addition to this, the statutory profit as well as the return on the capital

investment as also showed the increased in 2018 from the past few years (Qantas, 2018).

(Source: Qantas, 2018)

Qantas revenue in the international market is presented below indicates the performance of

the company. There is increase in the revenue with $6,892M then the year 2017, that was

$6,413M, this reflects that the performance has been enhanced due to critical success factors

(Qantas, 2018).

(Source: Qantas, 2018)

Key performance indicators

Qantas performance indicators are -

The profit before tax of Qantas has increased in 2018 from $1,604M that was low in the year

2017 with $ 1,401M. In addition to this, the statutory profit as well as the return on the capital

investment as also showed the increased in 2018 from the past few years (Qantas, 2018).

(Source: Qantas, 2018)

Qantas revenue in the international market is presented below indicates the performance of

the company. There is increase in the revenue with $6,892M then the year 2017, that was

$6,413M, this reflects that the performance has been enhanced due to critical success factors

(Qantas, 2018).

(Source: Qantas, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING 7

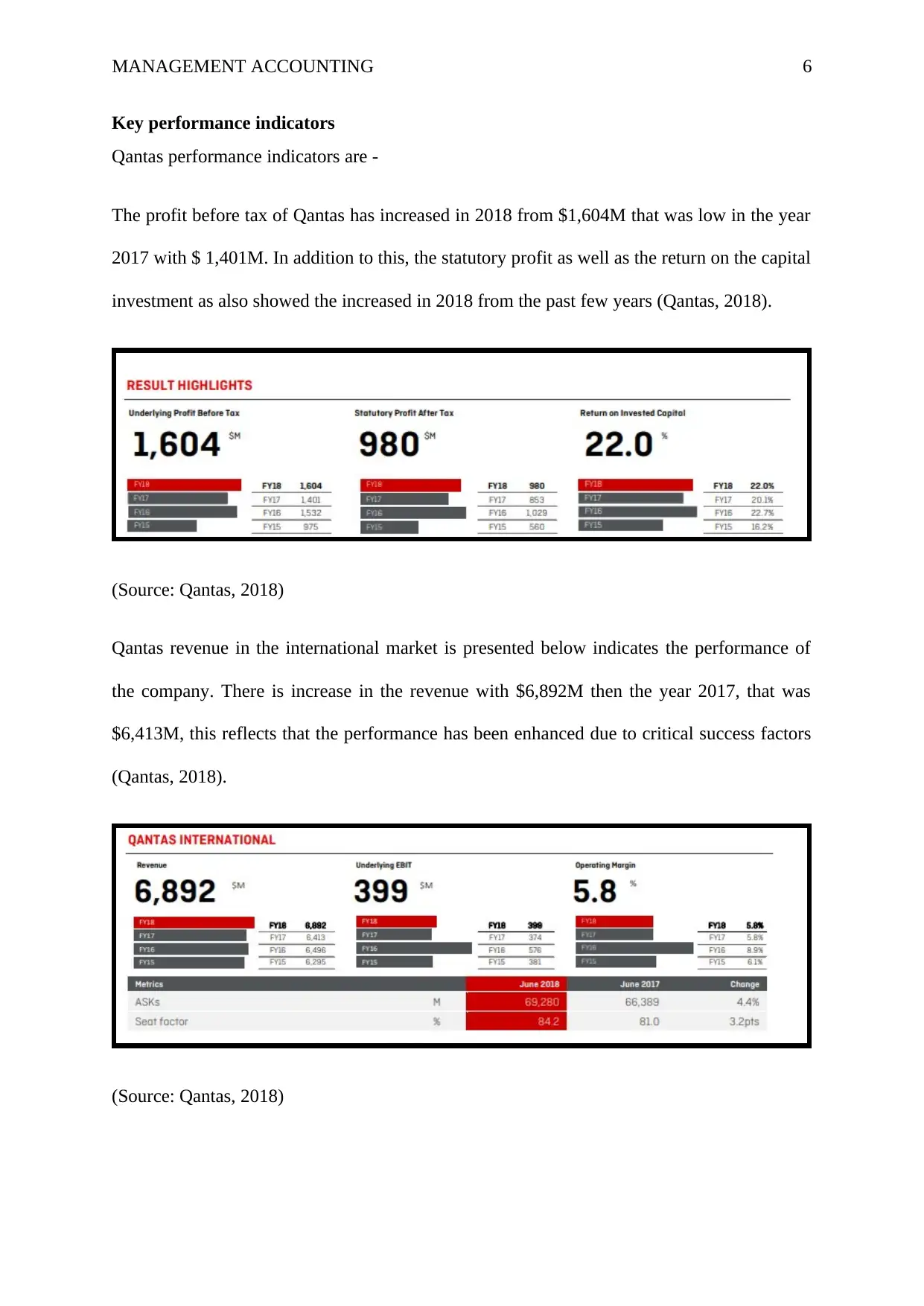

Further, this has been found that the long-term objectives of the company are to increase the

shareholders’ value and the performance of the company shows that they are able to offer

high return on investment.

Strategy Map

Considering the above analysis, below given is the strategy map for the Qantas company: -

Balance scorecard of Qantas

Balance scorecard is the strategy related to the performance management tool that is a semi-

structured report that helps the managers of the company to keep the track of the execution of

the activities. The below given is the balance scorecard of Qantas based on long term

objectives.

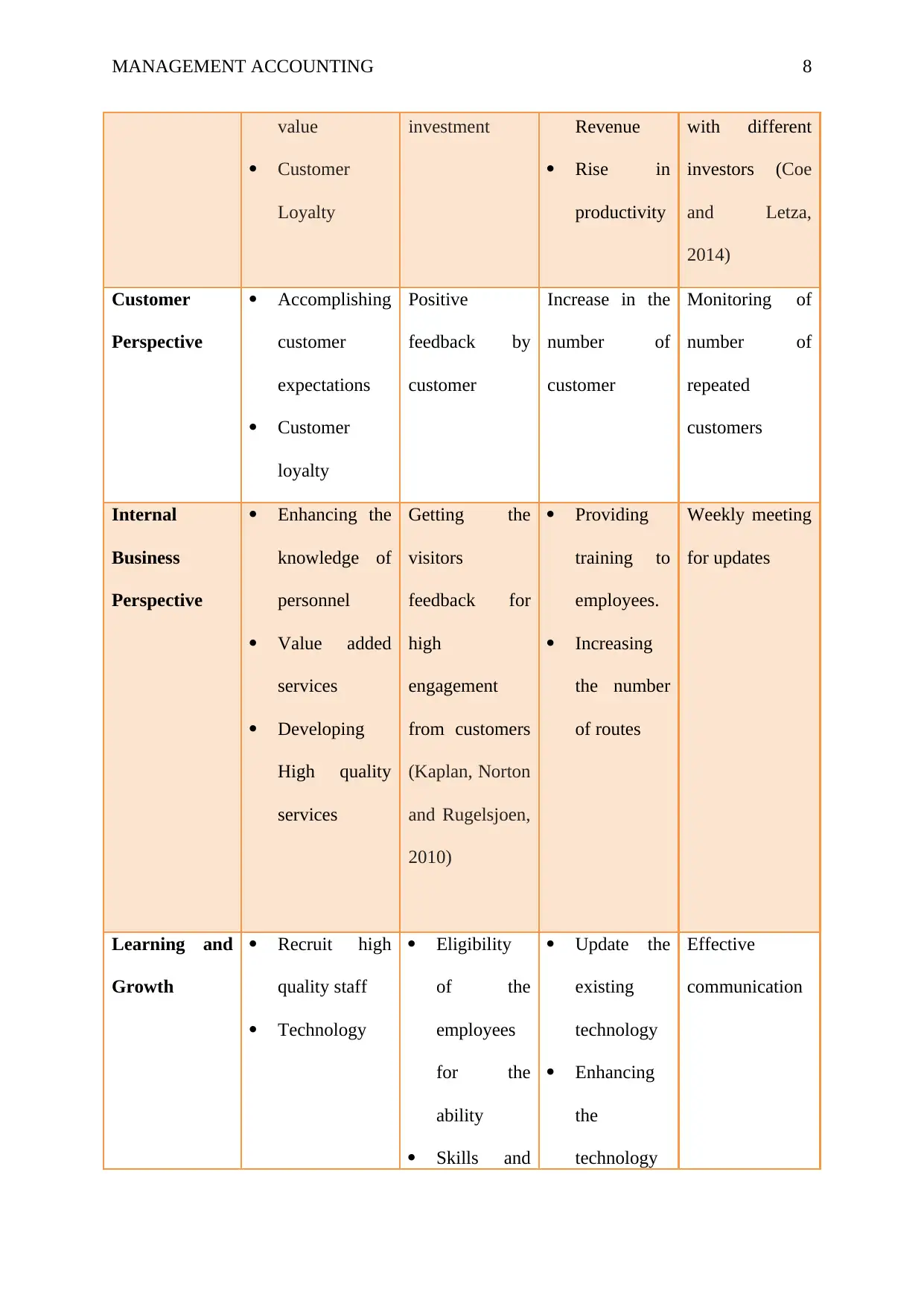

Perspectives Objectives Measures Target Initiatives

Financial

Perspective

Increasing the

shareholder’s

Increase in Increase in Contacting and

collaborating

Learning and Growth Perspective

Internal Business Perspective

Customer Perspective

Financial Perspective

Increasing the

Shareholder's

Value

Accomplishing

customer

expectations

Enhancing the

knowledge of

personnel

Recruit high

quality staff

Value added

services

Customer

Loyalty

Developing

High quality

services

Technology

Further, this has been found that the long-term objectives of the company are to increase the

shareholders’ value and the performance of the company shows that they are able to offer

high return on investment.

Strategy Map

Considering the above analysis, below given is the strategy map for the Qantas company: -

Balance scorecard of Qantas

Balance scorecard is the strategy related to the performance management tool that is a semi-

structured report that helps the managers of the company to keep the track of the execution of

the activities. The below given is the balance scorecard of Qantas based on long term

objectives.

Perspectives Objectives Measures Target Initiatives

Financial

Perspective

Increasing the

shareholder’s

Increase in Increase in Contacting and

collaborating

Learning and Growth Perspective

Internal Business Perspective

Customer Perspective

Financial Perspective

Increasing the

Shareholder's

Value

Accomplishing

customer

expectations

Enhancing the

knowledge of

personnel

Recruit high

quality staff

Value added

services

Customer

Loyalty

Developing

High quality

services

Technology

MANAGEMENT ACCOUNTING 8

value

Customer

Loyalty

investment Revenue

Rise in

productivity

with different

investors (Coe

and Letza,

2014)

Customer

Perspective

Accomplishing

customer

expectations

Customer

loyalty

Positive

feedback by

customer

Increase in the

number of

customer

Monitoring of

number of

repeated

customers

Internal

Business

Perspective

Enhancing the

knowledge of

personnel

Value added

services

Developing

High quality

services

Getting the

visitors

feedback for

high

engagement

from customers

(Kaplan, Norton

and Rugelsjoen,

2010)

Providing

training to

employees.

Increasing

the number

of routes

Weekly meeting

for updates

Learning and

Growth

Recruit high

quality staff

Technology

Eligibility

of the

employees

for the

ability

Skills and

Update the

existing

technology

Enhancing

the

technology

Effective

communication

value

Customer

Loyalty

investment Revenue

Rise in

productivity

with different

investors (Coe

and Letza,

2014)

Customer

Perspective

Accomplishing

customer

expectations

Customer

loyalty

Positive

feedback by

customer

Increase in the

number of

customer

Monitoring of

number of

repeated

customers

Internal

Business

Perspective

Enhancing the

knowledge of

personnel

Value added

services

Developing

High quality

services

Getting the

visitors

feedback for

high

engagement

from customers

(Kaplan, Norton

and Rugelsjoen,

2010)

Providing

training to

employees.

Increasing

the number

of routes

Weekly meeting

for updates

Learning and

Growth

Recruit high

quality staff

Technology

Eligibility

of the

employees

for the

ability

Skills and

Update the

existing

technology

Enhancing

the

technology

Effective

communication

MANAGEMENT ACCOUNTING 9

capabilities capabilities

Conclusion

The above report is discussing regarding the factors that contribute to the development of the

management accounting and the use of the balance scorecard. From the analysis it has been

identified that competition perform as the key factor for the introduction of management

accounting practices because it provide precise , and correct information to the management

of the company which is further used by them to take short-term and long-term decisions.

Besides this, the balanced scorecard is very useful tool as it provides a one page picture of the

complete strategy of the company. Moreover, it not just considers the financial aspects of the

company but it also incorporate non-financial aspects. Furthermore, the report has

highlighted that revenue is the key performance indicator of Qantas Airlines. In adition to this

the critical success factors of Qantas Airlines are competent workforce, root system, and cost

structure.

References

Bernard Marr & Co. (2019) 7 Benefits Of A Balanced Scorecard [Online]. Available from:

https://www.bernardmarr.com/default.asp?contentID=972 [Accessed on 31st May 2019]

Bloom, N., Propper, C., Seiler, S. and Van Reenen, J. (2015) The impact of competition on

management quality: evidence from public hospitals. The Review of Economic Studies, 82(2),

pp.457-489.

Coe, N. and Letza, S. (2014) Two decades of the balanced scorecard: A review of

developments. The Poznan University of Economics Review, 14(1), p.63.

capabilities capabilities

Conclusion

The above report is discussing regarding the factors that contribute to the development of the

management accounting and the use of the balance scorecard. From the analysis it has been

identified that competition perform as the key factor for the introduction of management

accounting practices because it provide precise , and correct information to the management

of the company which is further used by them to take short-term and long-term decisions.

Besides this, the balanced scorecard is very useful tool as it provides a one page picture of the

complete strategy of the company. Moreover, it not just considers the financial aspects of the

company but it also incorporate non-financial aspects. Furthermore, the report has

highlighted that revenue is the key performance indicator of Qantas Airlines. In adition to this

the critical success factors of Qantas Airlines are competent workforce, root system, and cost

structure.

References

Bernard Marr & Co. (2019) 7 Benefits Of A Balanced Scorecard [Online]. Available from:

https://www.bernardmarr.com/default.asp?contentID=972 [Accessed on 31st May 2019]

Bloom, N., Propper, C., Seiler, S. and Van Reenen, J. (2015) The impact of competition on

management quality: evidence from public hospitals. The Review of Economic Studies, 82(2),

pp.457-489.

Coe, N. and Letza, S. (2014) Two decades of the balanced scorecard: A review of

developments. The Poznan University of Economics Review, 14(1), p.63.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

MANAGEMENT ACCOUNTING 10

Drury, C.M. (2013) Management and cost accounting. Germany: Springer.

Kaplan, R.S., Norton, D.P. and Rugelsjoen, B. (2010) Managing alliances with the balanced

scorecard. Harvard business review, 88(1), pp.114-120.

Kaplan, R.S., Norton, D.P., and Rugelsjoen, B. (2010) Managing alliances with the balanced

scorecard. Harvard business review, 88(1), pp.114-120.

Niven, P.R. (2011) Balanced scorecard: Step-by-step for government and nonprofit agencies

1st ed. U.K: John Wiley & Sons.

Qantas (2018) Qantas annual report 2018 [Online]. Available from:

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2018-Annual-Report-ASX.pdf [Accessed on 31st May 2019]

Uyar, A. (2010) Cost and management accounting practices: a survey of manufacturing

companies. Eurasian Journal of Business and Economics, 3(6), pp.113-125.

Drury, C.M. (2013) Management and cost accounting. Germany: Springer.

Kaplan, R.S., Norton, D.P. and Rugelsjoen, B. (2010) Managing alliances with the balanced

scorecard. Harvard business review, 88(1), pp.114-120.

Kaplan, R.S., Norton, D.P., and Rugelsjoen, B. (2010) Managing alliances with the balanced

scorecard. Harvard business review, 88(1), pp.114-120.

Niven, P.R. (2011) Balanced scorecard: Step-by-step for government and nonprofit agencies

1st ed. U.K: John Wiley & Sons.

Qantas (2018) Qantas annual report 2018 [Online]. Available from:

https://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2018-Annual-Report-ASX.pdf [Accessed on 31st May 2019]

Uyar, A. (2010) Cost and management accounting practices: a survey of manufacturing

companies. Eurasian Journal of Business and Economics, 3(6), pp.113-125.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.