Management Accounting Report: Toyota PLC Analysis and Evaluation

VerifiedAdded on 2020/07/22

|16

|5130

|85

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Toyota PLC. It begins with an introduction to management accounting, differentiating it from financial accounting and outlining various essential types such as financial accounting, auditing, cost accounting, taxation, budgetary accounting, and others. The report then delves into the specific reports and techniques utilized by Toyota PLC, including budget reports, accounts receivable aging, job cost reports, and inventory management. It evaluates the benefits of management accounting systems, emphasizing how they aid in financial tracking, expense reduction, and improved decision-making. Furthermore, the report critically assesses the integration of management accounting systems and reporting within the organizational processes of Toyota PLC. The report also explores profitability analysis using costing measurements, identifies planning tools and budgetary techniques, and discusses methods to overcome economic problems within the company, concluding with an evaluation of how these techniques contribute to sustainable organizational success. The report includes an examination of key accounting functions like forecasting, planning, organizing, coordinating, and controlling performance, and provides a comparative table of management and financial accounting.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining the management accounting and its essential types........................................1

P2 Determining various kinds of reports techniques used by Toyota plc in context with

management accounting.........................................................................................................3

M1 Evaluating benefits of management accounting systems and their application within

Toyota.....................................................................................................................................4

D1 Critically evaluating how management accounting systems and management accounting

reporting are integrated within process of organisation.........................................................5

TASK 2............................................................................................................................................5

P3 Analysing the profitability of Toyota plc with the help of two costing measurements....5

TASK 3............................................................................................................................................7

P4 Identification of planning tools and budgetary techniques as well as their pros and cons for

Toyota plc...............................................................................................................................7

P5 Identification of techniques to overcome with economical problem in Toyota plc.........9

M4 Analysing how these techniques will be leading to sustainable success of organisation.10

D3 Evaluating how planning tools will be accounting to solve the financial problems......10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining the management accounting and its essential types........................................1

P2 Determining various kinds of reports techniques used by Toyota plc in context with

management accounting.........................................................................................................3

M1 Evaluating benefits of management accounting systems and their application within

Toyota.....................................................................................................................................4

D1 Critically evaluating how management accounting systems and management accounting

reporting are integrated within process of organisation.........................................................5

TASK 2............................................................................................................................................5

P3 Analysing the profitability of Toyota plc with the help of two costing measurements....5

TASK 3............................................................................................................................................7

P4 Identification of planning tools and budgetary techniques as well as their pros and cons for

Toyota plc...............................................................................................................................7

P5 Identification of techniques to overcome with economical problem in Toyota plc.........9

M4 Analysing how these techniques will be leading to sustainable success of organisation.10

D3 Evaluating how planning tools will be accounting to solve the financial problems......10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

The importance of implicating management accounting techniques in an organisation is

helpful in terms of making satisfactory changes in the operations as well as enhancing the

efficiency of the entity. For this, transactions belong to all the operational activities in the firm

such as purchase, production, sales, marketing etc. which are to be recorded in the books and

then summarised as well as analysed by the accounting professionals. The outcomes from such

analysis will be very helpful for them in terms of making suitable changes in the operations,

planning and forecasting the budgets of such activities. In the present report, there will be

discussion based on accounting operations in Toyota Plc as well as the managerial professionals

will be suggested to make required changes in the operations of the firm.

TASK 1

P1 Explaining the management accounting and its essential types

To enhance the operational performance of Toyota Plc, there are various tools and

techniques that will be helpful for the managers in terms of making adequate increment in the

profitability and growth of the entity (Management accounting, what is management

accounting?., 2018). However, there are several techniques and methods that will be helpful in

bringing the accuracy in decision making and planning for the business prospective. There are

several types of accounting such as:

Financial Accounting: In accordance with the operations made by the firm during the

period which will be presented in the various accounts and statement for the period. There will

be financial disclosure of such data set in the income statement, balance sheet, cash flow

statement and changes in equity (Givoly and et.al., 2017). Therefore, the fruitfulness of such

accounting disclosure will be helpful for Toyota plc in context with having stable operations,

capital generation as well as planning for the business expansion.

Auditing: These are the essential tools for the management in terms of making suitable

plans for business development. Here, the accounting professionals or auditors of the firm make

analysis over the accounts and present the necessary details regarding profits, costs and expenses

made Toyota plc during such period (Hopper and Bui, 2016).

1

The importance of implicating management accounting techniques in an organisation is

helpful in terms of making satisfactory changes in the operations as well as enhancing the

efficiency of the entity. For this, transactions belong to all the operational activities in the firm

such as purchase, production, sales, marketing etc. which are to be recorded in the books and

then summarised as well as analysed by the accounting professionals. The outcomes from such

analysis will be very helpful for them in terms of making suitable changes in the operations,

planning and forecasting the budgets of such activities. In the present report, there will be

discussion based on accounting operations in Toyota Plc as well as the managerial professionals

will be suggested to make required changes in the operations of the firm.

TASK 1

P1 Explaining the management accounting and its essential types

To enhance the operational performance of Toyota Plc, there are various tools and

techniques that will be helpful for the managers in terms of making adequate increment in the

profitability and growth of the entity (Management accounting, what is management

accounting?., 2018). However, there are several techniques and methods that will be helpful in

bringing the accuracy in decision making and planning for the business prospective. There are

several types of accounting such as:

Financial Accounting: In accordance with the operations made by the firm during the

period which will be presented in the various accounts and statement for the period. There will

be financial disclosure of such data set in the income statement, balance sheet, cash flow

statement and changes in equity (Givoly and et.al., 2017). Therefore, the fruitfulness of such

accounting disclosure will be helpful for Toyota plc in context with having stable operations,

capital generation as well as planning for the business expansion.

Auditing: These are the essential tools for the management in terms of making suitable

plans for business development. Here, the accounting professionals or auditors of the firm make

analysis over the accounts and present the necessary details regarding profits, costs and expenses

made Toyota plc during such period (Hopper and Bui, 2016).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting: These are the techniques which will be performed as per assigning the

costs to each particular department and operation of Toyota plc. Therefore, it helps in analysing

the requirements of funds for performing the tasks as well as revenue gatheredby them (Laudon

and Laudon, 2016). In this regard, the managers will make efficient decision and propose

techniques to reduce the costs as well as increase funds for the specific piece of operations.

Taxation: This method is helpful for the government in revenue generation and making

the development of the economy. Therefore, in every period, the company has to make the

payments of taxes such as corporate taxes, custom duties and various taxations levied over

transactions of the products and services (McCartney, Pierce and Mackie, 2016). Toyota Plc

must disclose the amount of taxes being paid by them in the accounting year therefore, it will be

helpful for the government, taxation authorities and the banks to analyse the tax payments as

well as revenue gathered by the organisation.

Budgetary accounting: In these techniques, here the managerial professional and the

accountant of the firm analyse the operation in each department. They analyse the required

amount of funds for the completion of tasks and operations in such units. Furthermore, they

make planning and budgets for them which help the firm in having better financial operations as

well as better revenue generation (Turner, 2014). Thus, it can be said that making budgets will be

beneficial for Toyota Plc as the expenditures are required to be made in the decided limited,

which will help in proper utilisation of funds and resources.

Debtors ageing period: This is the period which helps in analysing the payment received

by consumers and stakeholders of the firm in required duration. Therefore, with the help of such

analysis, it can be said that the firm become able to analyse adequate payments made by the

professionals in terms of making the payments of the operations (Kerzner, 2013). However, in

this case, Toyota Plc will have proper record of its debtors and the amount of granted money to

them. It will be helpful for them in terms of having the instalment amounts over the vehicle

which is being purchased by the buyers.

Job costing: These technique helps in setting the limit over the operational activities in

the industries such as manufacturing, production, sales etc. thus, such limited are belongs to

analysing the costs and finance need for the completion of tasks. The costs' estimation belongs to

determine the profitability of such activities in the growth Toyota plc (Givoly and et.al., 2017). If

2

costs to each particular department and operation of Toyota plc. Therefore, it helps in analysing

the requirements of funds for performing the tasks as well as revenue gatheredby them (Laudon

and Laudon, 2016). In this regard, the managers will make efficient decision and propose

techniques to reduce the costs as well as increase funds for the specific piece of operations.

Taxation: This method is helpful for the government in revenue generation and making

the development of the economy. Therefore, in every period, the company has to make the

payments of taxes such as corporate taxes, custom duties and various taxations levied over

transactions of the products and services (McCartney, Pierce and Mackie, 2016). Toyota Plc

must disclose the amount of taxes being paid by them in the accounting year therefore, it will be

helpful for the government, taxation authorities and the banks to analyse the tax payments as

well as revenue gathered by the organisation.

Budgetary accounting: In these techniques, here the managerial professional and the

accountant of the firm analyse the operation in each department. They analyse the required

amount of funds for the completion of tasks and operations in such units. Furthermore, they

make planning and budgets for them which help the firm in having better financial operations as

well as better revenue generation (Turner, 2014). Thus, it can be said that making budgets will be

beneficial for Toyota Plc as the expenditures are required to be made in the decided limited,

which will help in proper utilisation of funds and resources.

Debtors ageing period: This is the period which helps in analysing the payment received

by consumers and stakeholders of the firm in required duration. Therefore, with the help of such

analysis, it can be said that the firm become able to analyse adequate payments made by the

professionals in terms of making the payments of the operations (Kerzner, 2013). However, in

this case, Toyota Plc will have proper record of its debtors and the amount of granted money to

them. It will be helpful for them in terms of having the instalment amounts over the vehicle

which is being purchased by the buyers.

Job costing: These technique helps in setting the limit over the operational activities in

the industries such as manufacturing, production, sales etc. thus, such limited are belongs to

analysing the costs and finance need for the completion of tasks. The costs' estimation belongs to

determine the profitability of such activities in the growth Toyota plc (Givoly and et.al., 2017). If

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the managerial professionals do not find such operations very healthy then they will make

changes in the costing techniques and then they reduce the level of funds for such operations.

Price optimisation: This method helps in generating the adequate amount of revenue

from the sales of the products. Here, the managers in Toyota plc will analyse consumer reaction

over each vehicle and the most preferable prices paid by them (Hopper and Bui, 2016). Thus,

this technique will help them in analysing adequate rates over the vehicle and then they will plan

costs decisions over such operational activities.

Inventory management: all the raw materials and stocks which are kept and used by

company in preparing of the final goods and products are known as the inventory. So this

becomes quite important to mange, control, store and use that material which will be helping

company in forming or manufacturing products (Bennett, Schaltegger and Zvezdov, 2011). The

method of managing and ordering raw materials is knowns as inventory management.

Major functions of management accounting-

The functions of management accounting included:

Forecasting and planning for whole year or financial period in form of collecting important

information and data analysing so that profits and sales could be forecasted.

Organising is also done of the available data which was collected which will then be helping the

management in separating human ad non human resource which is available.

Coordinating of the efficiency of organisation and also maximising all kind of profits which it

want to achieve.

Controlling Performance which is done with the help of standard costing, budgetary control,

accounting ratios and fund flow statements.

Basis Management accounting Financial accounting

Users All the managers and

employees who are working in

company

External users

Time focus Future Past or historic data is used

3

changes in the costing techniques and then they reduce the level of funds for such operations.

Price optimisation: This method helps in generating the adequate amount of revenue

from the sales of the products. Here, the managers in Toyota plc will analyse consumer reaction

over each vehicle and the most preferable prices paid by them (Hopper and Bui, 2016). Thus,

this technique will help them in analysing adequate rates over the vehicle and then they will plan

costs decisions over such operational activities.

Inventory management: all the raw materials and stocks which are kept and used by

company in preparing of the final goods and products are known as the inventory. So this

becomes quite important to mange, control, store and use that material which will be helping

company in forming or manufacturing products (Bennett, Schaltegger and Zvezdov, 2011). The

method of managing and ordering raw materials is knowns as inventory management.

Major functions of management accounting-

The functions of management accounting included:

Forecasting and planning for whole year or financial period in form of collecting important

information and data analysing so that profits and sales could be forecasted.

Organising is also done of the available data which was collected which will then be helping the

management in separating human ad non human resource which is available.

Coordinating of the efficiency of organisation and also maximising all kind of profits which it

want to achieve.

Controlling Performance which is done with the help of standard costing, budgetary control,

accounting ratios and fund flow statements.

Basis Management accounting Financial accounting

Users All the managers and

employees who are working in

company

External users

Time focus Future Past or historic data is used

3

Verifiability Satisfaction of need of

management

Emphases on judgement and

origin of documentation.

Subjects Segment reporting Company wide report

P2 Determining various kinds of reports techniques used by Toyota plc in context with

management accounting

Management accounting reports will be helping business and its owners in monitoring

performance of company so they are prepared throughout accounting period. Depending upon

type of project and time sensitivity of information the manager or owner could also ask for

reports on quarterly or monthly basis as well (Boyns and Edwards, 2013). This reporting will be

helping both big and small enterprises in monitoring there and their performance of company

various types of management accounting reports which Toyota plc will be preparing are as

follows:

Budget report- according to the previous years spending or expenditure and the profits the

budget of this current year would be prepared. This will be including budget or total expenditure

of all different departments of Toyota including manufacturing, production, marketing, sales,

research and development. This budget will also be including all source of revenue and

expenditure of different departments of Toyota which will be according to goals and objectives

need to be accomplish. If the revenue of last year are low and expenditure of last year are high

then this will be including for saving money and finding new suppliers of company as well

(Endenich, Brandau and Hoffjan, 2011). This will in tern help in increasing sales and decreasing

expenses so that budgets are not consuming more time and efforts in its preparation.

Accounts Receivable ageing- this report will b including how long a customer is holding money

of company and when is due date of his repayment or instalment. This accounts report will be

including separate columns for debtor who are having more late than 30 days or 90 days. As the

management is having or preparing this report they would be having clue of what and where is

the problems relating to collection procedures of company (Fowzia, 2011). This will in tern

helping them to solve issues which will be prevailing within Toyota for longer duration of time.

Like if there are many numbers of customers who are not been able to give their amount to

4

management

Emphases on judgement and

origin of documentation.

Subjects Segment reporting Company wide report

P2 Determining various kinds of reports techniques used by Toyota plc in context with

management accounting

Management accounting reports will be helping business and its owners in monitoring

performance of company so they are prepared throughout accounting period. Depending upon

type of project and time sensitivity of information the manager or owner could also ask for

reports on quarterly or monthly basis as well (Boyns and Edwards, 2013). This reporting will be

helping both big and small enterprises in monitoring there and their performance of company

various types of management accounting reports which Toyota plc will be preparing are as

follows:

Budget report- according to the previous years spending or expenditure and the profits the

budget of this current year would be prepared. This will be including budget or total expenditure

of all different departments of Toyota including manufacturing, production, marketing, sales,

research and development. This budget will also be including all source of revenue and

expenditure of different departments of Toyota which will be according to goals and objectives

need to be accomplish. If the revenue of last year are low and expenditure of last year are high

then this will be including for saving money and finding new suppliers of company as well

(Endenich, Brandau and Hoffjan, 2011). This will in tern help in increasing sales and decreasing

expenses so that budgets are not consuming more time and efforts in its preparation.

Accounts Receivable ageing- this report will b including how long a customer is holding money

of company and when is due date of his repayment or instalment. This accounts report will be

including separate columns for debtor who are having more late than 30 days or 90 days. As the

management is having or preparing this report they would be having clue of what and where is

the problems relating to collection procedures of company (Fowzia, 2011). This will in tern

helping them to solve issues which will be prevailing within Toyota for longer duration of time.

Like if there are many numbers of customers who are not been able to give their amount to

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Toyota then company need to tighten their credit policy. Company must also be analysing this

report on periodical basis so that they are keeping track of all the old and new debt.

Job cost reports- this report will be prepared in showing the expenditure of all specified. Then

after the cost or expenditure of all projects company will be evaluating job profitability. Thus, all

higher earning or area which will be having spending more on its projects could be taken out.

That project which is spending more on its business need to be brought under control so that

there are fewer expenses (France, 2010). Job cost report means making reports as according to

specified project or department which they are incurring and whichever is higher among all must

be kept under supervision. This is most efficient in cost controlling and less amount of spending

or expenditures will also occur.

Inventory and manufacturing- this will be most effective report which would be used by Toyota

as will be helping in managing all physical inventory and thus making management process more

efficient. Inventory and manufacturing report would be covering all parts which are related to

stocks like that of wastage, per unit overhead cost, labour cost per hour (Hammad, Jusoh and

Ghozali, 2013). Thus, in tern helping for controlling the wastage of inventory and manufacturing

so that corrective actions could be taken in future time period.

M1 Evaluating benefits of management accounting systems and their application within Toyota.

Management accounting system will be helpful for Toyota as they could track and report

financial information so that owner could review them. This also help in reducing expenses as if

they are reviewing the cost then cost of economic resources will be under control. The cash flow

within company will also be improved as Toyota would be preparing budgets for further

expenditure (Harris and Durden, 2012). Decision making procedures of business will also be

improved as management will be having information which is of whole business.

D1 Critically evaluating how management accounting systems and management accounting

reporting are integrated within process of organisation.

Management accounting system- this is the process of keeping and recording all information

which are necessary for business and thus will be helping in formulating business decisions. This

is integrated within organisation by the help of management and employee of Toyota.

5

report on periodical basis so that they are keeping track of all the old and new debt.

Job cost reports- this report will be prepared in showing the expenditure of all specified. Then

after the cost or expenditure of all projects company will be evaluating job profitability. Thus, all

higher earning or area which will be having spending more on its projects could be taken out.

That project which is spending more on its business need to be brought under control so that

there are fewer expenses (France, 2010). Job cost report means making reports as according to

specified project or department which they are incurring and whichever is higher among all must

be kept under supervision. This is most efficient in cost controlling and less amount of spending

or expenditures will also occur.

Inventory and manufacturing- this will be most effective report which would be used by Toyota

as will be helping in managing all physical inventory and thus making management process more

efficient. Inventory and manufacturing report would be covering all parts which are related to

stocks like that of wastage, per unit overhead cost, labour cost per hour (Hammad, Jusoh and

Ghozali, 2013). Thus, in tern helping for controlling the wastage of inventory and manufacturing

so that corrective actions could be taken in future time period.

M1 Evaluating benefits of management accounting systems and their application within Toyota.

Management accounting system will be helpful for Toyota as they could track and report

financial information so that owner could review them. This also help in reducing expenses as if

they are reviewing the cost then cost of economic resources will be under control. The cash flow

within company will also be improved as Toyota would be preparing budgets for further

expenditure (Harris and Durden, 2012). Decision making procedures of business will also be

improved as management will be having information which is of whole business.

D1 Critically evaluating how management accounting systems and management accounting

reporting are integrated within process of organisation.

Management accounting system- this is the process of keeping and recording all information

which are necessary for business and thus will be helping in formulating business decisions. This

is integrated within organisation by the help of management and employee of Toyota.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting reporting- while this is the procedures of reporting ot management

what are expenditure and expected revenue for the period. This will also be integrated within

organisation by help of management and employee of Toyota.

TASK 2

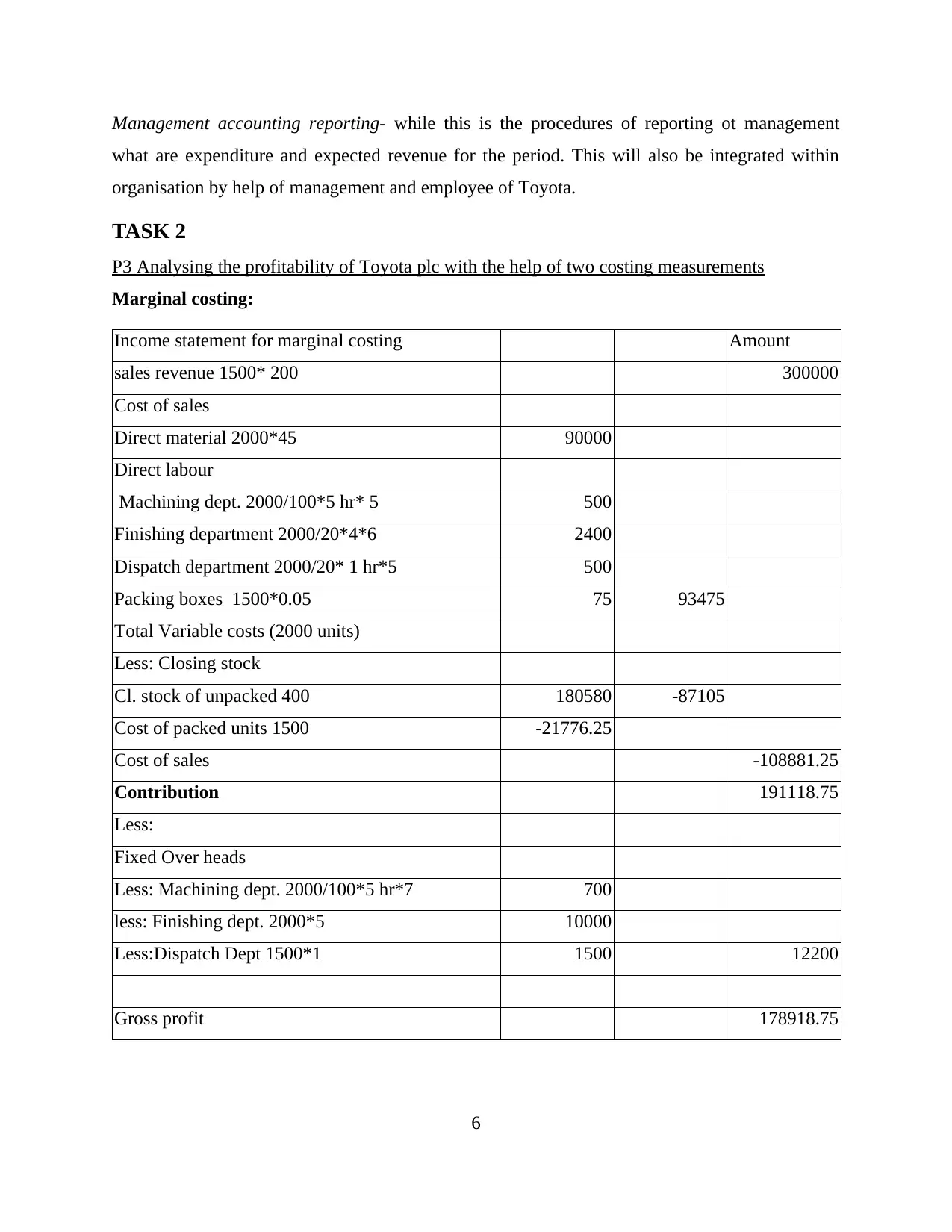

P3 Analysing the profitability of Toyota plc with the help of two costing measurements

Marginal costing:

Income statement for marginal costing Amount

sales revenue 1500* 200 300000

Cost of sales

Direct material 2000*45 90000

Direct labour

Machining dept. 2000/100*5 hr* 5 500

Finishing department 2000/20*4*6 2400

Dispatch department 2000/20* 1 hr*5 500

Packing boxes 1500*0.05 75 93475

Total Variable costs (2000 units)

Less: Closing stock

Cl. stock of unpacked 400 180580 -87105

Cost of packed units 1500 -21776.25

Cost of sales -108881.25

Contribution 191118.75

Less:

Fixed Over heads

Less: Machining dept. 2000/100*5 hr*7 700

less: Finishing dept. 2000*5 10000

Less:Dispatch Dept 1500*1 1500 12200

Gross profit 178918.75

6

what are expenditure and expected revenue for the period. This will also be integrated within

organisation by help of management and employee of Toyota.

TASK 2

P3 Analysing the profitability of Toyota plc with the help of two costing measurements

Marginal costing:

Income statement for marginal costing Amount

sales revenue 1500* 200 300000

Cost of sales

Direct material 2000*45 90000

Direct labour

Machining dept. 2000/100*5 hr* 5 500

Finishing department 2000/20*4*6 2400

Dispatch department 2000/20* 1 hr*5 500

Packing boxes 1500*0.05 75 93475

Total Variable costs (2000 units)

Less: Closing stock

Cl. stock of unpacked 400 180580 -87105

Cost of packed units 1500 -21776.25

Cost of sales -108881.25

Contribution 191118.75

Less:

Fixed Over heads

Less: Machining dept. 2000/100*5 hr*7 700

less: Finishing dept. 2000*5 10000

Less:Dispatch Dept 1500*1 1500 12200

Gross profit 178918.75

6

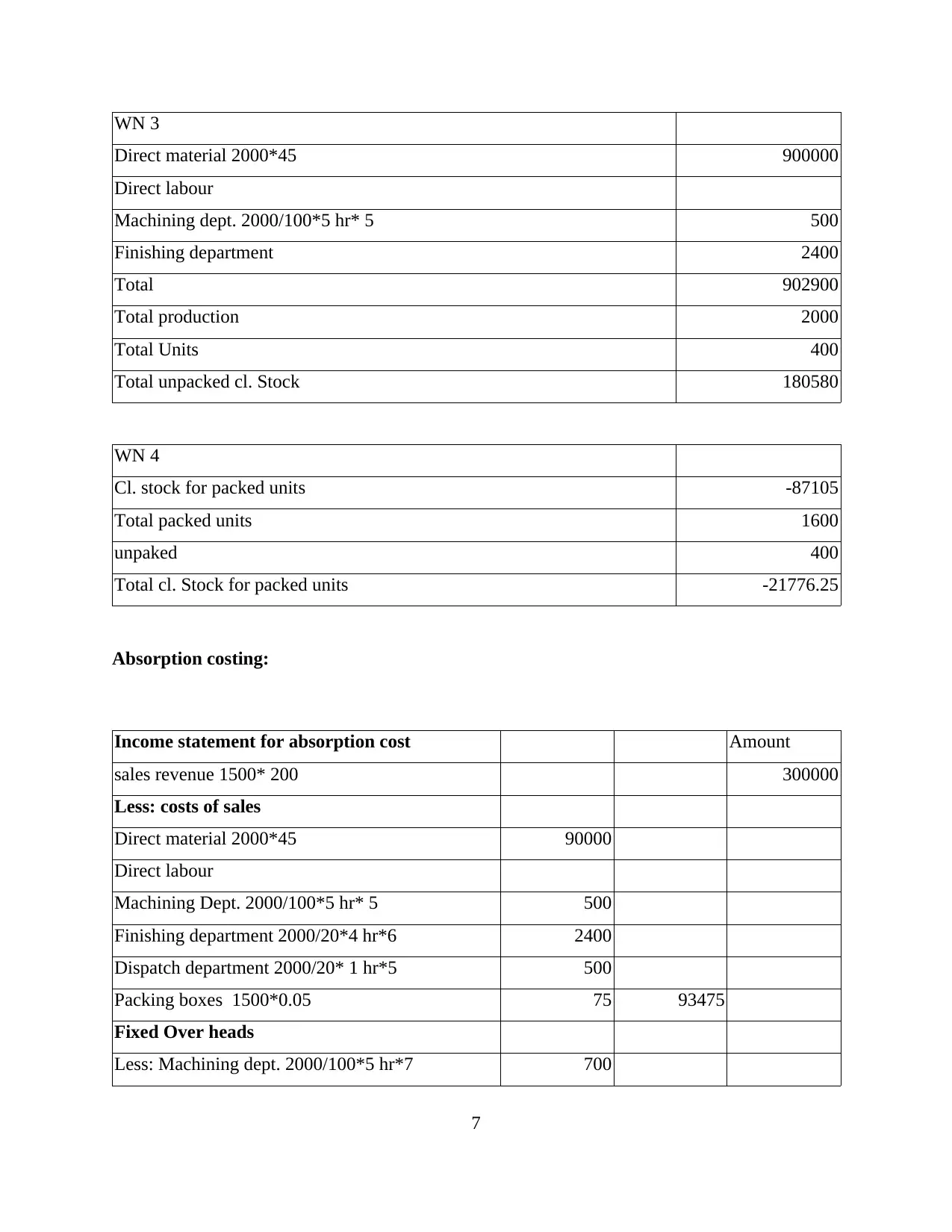

WN 3

Direct material 2000*45 900000

Direct labour

Machining dept. 2000/100*5 hr* 5 500

Finishing department 2400

Total 902900

Total production 2000

Total Units 400

Total unpacked cl. Stock 180580

WN 4

Cl. stock for packed units -87105

Total packed units 1600

unpaked 400

Total cl. Stock for packed units -21776.25

Absorption costing:

Income statement for absorption cost Amount

sales revenue 1500* 200 300000

Less: costs of sales

Direct material 2000*45 90000

Direct labour

Machining Dept. 2000/100*5 hr* 5 500

Finishing department 2000/20*4 hr*6 2400

Dispatch department 2000/20* 1 hr*5 500

Packing boxes 1500*0.05 75 93475

Fixed Over heads

Less: Machining dept. 2000/100*5 hr*7 700

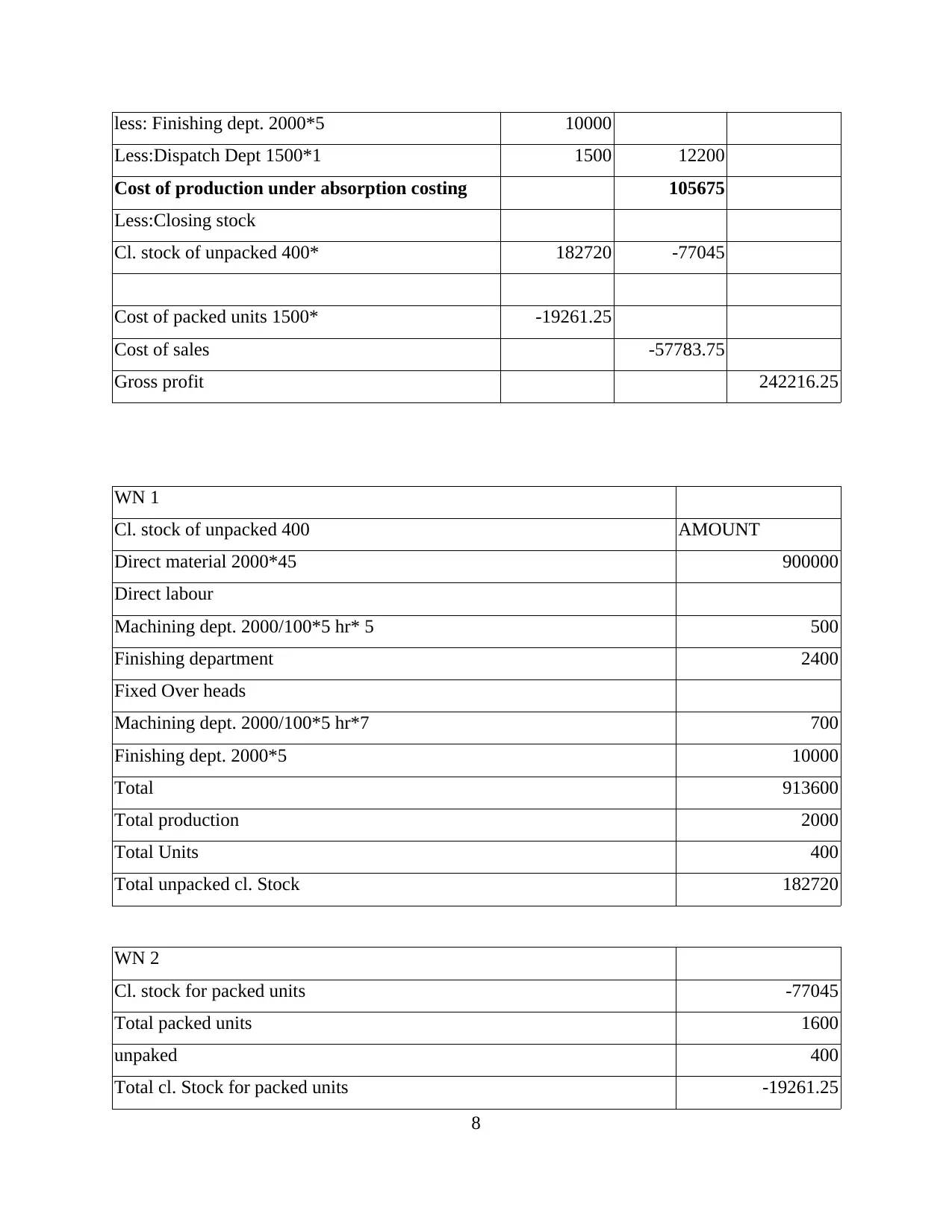

7

Direct material 2000*45 900000

Direct labour

Machining dept. 2000/100*5 hr* 5 500

Finishing department 2400

Total 902900

Total production 2000

Total Units 400

Total unpacked cl. Stock 180580

WN 4

Cl. stock for packed units -87105

Total packed units 1600

unpaked 400

Total cl. Stock for packed units -21776.25

Absorption costing:

Income statement for absorption cost Amount

sales revenue 1500* 200 300000

Less: costs of sales

Direct material 2000*45 90000

Direct labour

Machining Dept. 2000/100*5 hr* 5 500

Finishing department 2000/20*4 hr*6 2400

Dispatch department 2000/20* 1 hr*5 500

Packing boxes 1500*0.05 75 93475

Fixed Over heads

Less: Machining dept. 2000/100*5 hr*7 700

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

less: Finishing dept. 2000*5 10000

Less:Dispatch Dept 1500*1 1500 12200

Cost of production under absorption costing 105675

Less:Closing stock

Cl. stock of unpacked 400* 182720 -77045

Cost of packed units 1500* -19261.25

Cost of sales -57783.75

Gross profit 242216.25

WN 1

Cl. stock of unpacked 400 AMOUNT

Direct material 2000*45 900000

Direct labour

Machining dept. 2000/100*5 hr* 5 500

Finishing department 2400

Fixed Over heads

Machining dept. 2000/100*5 hr*7 700

Finishing dept. 2000*5 10000

Total 913600

Total production 2000

Total Units 400

Total unpacked cl. Stock 182720

WN 2

Cl. stock for packed units -77045

Total packed units 1600

unpaked 400

Total cl. Stock for packed units -19261.25

8

Less:Dispatch Dept 1500*1 1500 12200

Cost of production under absorption costing 105675

Less:Closing stock

Cl. stock of unpacked 400* 182720 -77045

Cost of packed units 1500* -19261.25

Cost of sales -57783.75

Gross profit 242216.25

WN 1

Cl. stock of unpacked 400 AMOUNT

Direct material 2000*45 900000

Direct labour

Machining dept. 2000/100*5 hr* 5 500

Finishing department 2400

Fixed Over heads

Machining dept. 2000/100*5 hr*7 700

Finishing dept. 2000*5 10000

Total 913600

Total production 2000

Total Units 400

Total unpacked cl. Stock 182720

WN 2

Cl. stock for packed units -77045

Total packed units 1600

unpaked 400

Total cl. Stock for packed units -19261.25

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Identification of planning tools and budgetary techniques as well as their pros and cons for

Toyota plc

Budgets are the financial aid or help which will be given by side of management ot all

other department of business so that they could manage the flow of fund and expenditure within

their departments (Hutaibat, 2012). If there are any mismatches with the allotted budget and with

actual expenditure then management need to apply some tools and techniques which are related

ot control of budgets.

Variance analysis- this will be the simplest form of controlling the mismatches of budgets if any.

Which is done by taking the budget and then comparing it with the expenses which are actually

caused to firm according ot department basis and then variance are been found. Variance will be

found in both labour and overhead cost of firm and thus helpful in reducing the cost of business.

Zero base budgeting method- this one is the most popular form of method which are been used

nowadays by management of business (Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011). Under

this method budget of every year are made on nil or taking zero as base. Which clearly means

that if any amount is been undue in last year's budget then that amount will not be included or

forming part of current year's budget. But this method is only applicable if income of last year is

equal to that of expense of that year so there will be no amount left for adjustment. But if the

income is more than expenses then amount which need to be allocated need to be raised so that

there is nothing left for next coming year.

Adjustment of fund- this will be wholly and solely depending upon the top management who will

be making decision to adjust fund from one project to other project which need help.

Management will be evaluating that one project is running short of funds for meeting its

expenses and other one is having excess of funds so they will bed adjusting funds from both the

departments or project (Mat, Smith and Djajadikerta, 2010). This will thus be helping

management in decreasing the wastage and misuse of money which is been given to all the

departments or projects of Toyota

Advantages Of Budget Control

9

P4 Identification of planning tools and budgetary techniques as well as their pros and cons for

Toyota plc

Budgets are the financial aid or help which will be given by side of management ot all

other department of business so that they could manage the flow of fund and expenditure within

their departments (Hutaibat, 2012). If there are any mismatches with the allotted budget and with

actual expenditure then management need to apply some tools and techniques which are related

ot control of budgets.

Variance analysis- this will be the simplest form of controlling the mismatches of budgets if any.

Which is done by taking the budget and then comparing it with the expenses which are actually

caused to firm according ot department basis and then variance are been found. Variance will be

found in both labour and overhead cost of firm and thus helpful in reducing the cost of business.

Zero base budgeting method- this one is the most popular form of method which are been used

nowadays by management of business (Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011). Under

this method budget of every year are made on nil or taking zero as base. Which clearly means

that if any amount is been undue in last year's budget then that amount will not be included or

forming part of current year's budget. But this method is only applicable if income of last year is

equal to that of expense of that year so there will be no amount left for adjustment. But if the

income is more than expenses then amount which need to be allocated need to be raised so that

there is nothing left for next coming year.

Adjustment of fund- this will be wholly and solely depending upon the top management who will

be making decision to adjust fund from one project to other project which need help.

Management will be evaluating that one project is running short of funds for meeting its

expenses and other one is having excess of funds so they will bed adjusting funds from both the

departments or project (Mat, Smith and Djajadikerta, 2010). This will thus be helping

management in decreasing the wastage and misuse of money which is been given to all the

departments or projects of Toyota

Advantages Of Budget Control

9

This will be helping Toyota in analysing which budgeting method or techniques must be

used by firm so that mismatch of budgets are been corrected. As budgets will be helping firm in

reaching to their goals and objectives of firm which they have set for all departments.

Coordinating activities across department- the budgets or methods which are used to control the

budget will be helping Toyota in coordinating all activities within department. Like if top

management are using adjustment of fund method then this will be helping one department with

the available fund of other department.

Recording of activities- budget controlling methods will also be helping in recording and

maintaining all activities which are performed by business (Messner, 2016). Like in Toyota

management could any time have a look on which activity is making profits and which is just

creating loss. So company could increase the amount of efforts which they are putting onto that

loss making department.

Improving communication- all employees of firm will be easily coordinating with each other in

order to have a look on the area which is making higher profits and which is not.

Helping in comparing- variance method will be helping in making comparison of actual budget

with that of budget which was set at the beginning of current year.

Disadvantages Of Budget Control

Lack of employee participation- as the budgets are mainly allotted by top management to

employees which will be creating demotivation among them (Pimentel and Major, 2010). The

budgets are simply made and allocated to employees in which they are having no participation

thus they will not be taking interest in understanding that budget.

Reduce in initiative- if the budget which is been prepared is very rigid then this will not be

attracting initiative or employee participation within business ideas or projects. The innovation

within lower level of managers whose innovation is very important will not be seen . Thus, this

will b making it very hard to get money for any kind of new idea or development within

organisation.

10

used by firm so that mismatch of budgets are been corrected. As budgets will be helping firm in

reaching to their goals and objectives of firm which they have set for all departments.

Coordinating activities across department- the budgets or methods which are used to control the

budget will be helping Toyota in coordinating all activities within department. Like if top

management are using adjustment of fund method then this will be helping one department with

the available fund of other department.

Recording of activities- budget controlling methods will also be helping in recording and

maintaining all activities which are performed by business (Messner, 2016). Like in Toyota

management could any time have a look on which activity is making profits and which is just

creating loss. So company could increase the amount of efforts which they are putting onto that

loss making department.

Improving communication- all employees of firm will be easily coordinating with each other in

order to have a look on the area which is making higher profits and which is not.

Helping in comparing- variance method will be helping in making comparison of actual budget

with that of budget which was set at the beginning of current year.

Disadvantages Of Budget Control

Lack of employee participation- as the budgets are mainly allotted by top management to

employees which will be creating demotivation among them (Pimentel and Major, 2010). The

budgets are simply made and allocated to employees in which they are having no participation

thus they will not be taking interest in understanding that budget.

Reduce in initiative- if the budget which is been prepared is very rigid then this will not be

attracting initiative or employee participation within business ideas or projects. The innovation

within lower level of managers whose innovation is very important will not be seen . Thus, this

will b making it very hard to get money for any kind of new idea or development within

organisation.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.