Management Accounting - Pavestone Assignment Sample

VerifiedAdded on 2021/02/20

|16

|4511

|20

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management

Accounting

Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

ACTIVITY 1...................................................................................................................................3

Management Accounting Systems:.............................................................................................3

Management Accounting reports:................................................................................................4

Benefits of management accounting system:..............................................................................5

Evaluation of manner of integration of systems and reporting within process of business

entity:...........................................................................................................................................6

Costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs:....................................................................................................6

Interpret Financial reports prepared and data for a range of business activities:......................11

ACTIVITY 2.................................................................................................................................11

Explanation of different planning tool used for budgetary control...........................................11

Comparison of manner by which organisations are using management accounting systems to

respond financial problems:.......................................................................................................14

Analysis of the way in which management accounting lead to respond financial problems....15

Use of planning tools to respond financial problems:...............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

ACTIVITY 1...................................................................................................................................3

Management Accounting Systems:.............................................................................................3

Management Accounting reports:................................................................................................4

Benefits of management accounting system:..............................................................................5

Evaluation of manner of integration of systems and reporting within process of business

entity:...........................................................................................................................................6

Costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs:....................................................................................................6

Interpret Financial reports prepared and data for a range of business activities:......................11

ACTIVITY 2.................................................................................................................................11

Explanation of different planning tool used for budgetary control...........................................11

Comparison of manner by which organisations are using management accounting systems to

respond financial problems:.......................................................................................................14

Analysis of the way in which management accounting lead to respond financial problems....15

Use of planning tools to respond financial problems:...............................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting defines as a process to analyse business costs and operations, for

preparing the internal financial report and records. This would help managers of a company in

taking proper decisions related with achievement of business objectives. Along with this,

management accounting also aid in making sense of costing data by translating the same into

useful information for managing the business (Plumb and et.al., 2017). The present report is

going to describe the concept of management accounting and its role in managing a company.

Here, different reporting methods are also analysed to get internal business information and its

uses in managing the cost of production. For this purpose, Pavestone Company of UK has been

taken that deals in small level and manufacture as well as trade the concrete products to other

construction companies. It uses the concept of management accounting techniques like planning

and contingency tools, in order to respond future financial issues.

ACTIVITY 1

Management Accounting Systems:

Management accounting considers as an important concept in a business that helps in

analysing present situation and forecast the future condition also, on the basis of internal

analysis. It facilitates the information to managers of a company in making appropriate decisions

for increasing effectiveness of business (Hilton and Platt, 2013). For this purpose, it helps in

making record of overall fiscal transaction and other activities that includes financial and non-

financial data. Pavestone Ltd. deals in construction business and offers products like building

materials, paving, paver stones and more, to other builders on reasonable rates. This company

use management accounting system to determine number of labours used for manufacturing and

delivering its products to right customers (Hopper and Bui, 2016). It also forecasts the inventory

needs to reduce expenses and complete demand of marketplace on time. Along with this, to

increase the performance of business, this company uses a number of management accounting

tools such as inventory management, cost accounting, job costing and more, as explained

beneath:-

Job costing system - It is used to allocate costs in production due to diversify product

range which are entirely different from each other (Stein and et.al., 2015). It mainly

focuses on assigning costs as per classified jobs and batches to improve efficiencies of

Management accounting defines as a process to analyse business costs and operations, for

preparing the internal financial report and records. This would help managers of a company in

taking proper decisions related with achievement of business objectives. Along with this,

management accounting also aid in making sense of costing data by translating the same into

useful information for managing the business (Plumb and et.al., 2017). The present report is

going to describe the concept of management accounting and its role in managing a company.

Here, different reporting methods are also analysed to get internal business information and its

uses in managing the cost of production. For this purpose, Pavestone Company of UK has been

taken that deals in small level and manufacture as well as trade the concrete products to other

construction companies. It uses the concept of management accounting techniques like planning

and contingency tools, in order to respond future financial issues.

ACTIVITY 1

Management Accounting Systems:

Management accounting considers as an important concept in a business that helps in

analysing present situation and forecast the future condition also, on the basis of internal

analysis. It facilitates the information to managers of a company in making appropriate decisions

for increasing effectiveness of business (Hilton and Platt, 2013). For this purpose, it helps in

making record of overall fiscal transaction and other activities that includes financial and non-

financial data. Pavestone Ltd. deals in construction business and offers products like building

materials, paving, paver stones and more, to other builders on reasonable rates. This company

use management accounting system to determine number of labours used for manufacturing and

delivering its products to right customers (Hopper and Bui, 2016). It also forecasts the inventory

needs to reduce expenses and complete demand of marketplace on time. Along with this, to

increase the performance of business, this company uses a number of management accounting

tools such as inventory management, cost accounting, job costing and more, as explained

beneath:-

Job costing system - It is used to allocate costs in production due to diversify product

range which are entirely different from each other (Stein and et.al., 2015). It mainly

focuses on assigning costs as per classified jobs and batches to improve efficiencies of

production. For better assessment as well as accountability, Pavestone Ltd. can apply

process costing method instead of batch costing for increasing efficiencies of its

production cost.

Price management – It is generally used for analysing how demand of customers

fluctuate with change in price of products. As Pavestone deals with construction

materials therefore, any fluctuations in price will directly impact on its supply and

demand. It also helps in analysing factors that impact on price strategy of company, so

that concrete materials can be offered at better price on competitive rate.

Cost accounting – This system is mainly designed to keep track the inventories flow

during each stage of production (Turban, Volonino and Wood, 2015). Hereby, respective

company can assess the viability of different project by applying cost accounting system

because it provides a fixed cost structure, through which annual financial budget can be

planned. Along with this, Pavestone can also use this system to record production

activities as well, for keeping stock available in inventories to fulfil demand of customers

on time.

Inventory management – This system can help Pavestone in specifying the shape and

manner of placement of stocks as per consumer demand. For minimising the inventory

cost, it is required by management of this company to precede the regular as well as

planned course of stocks at each location of a supply (Nielsen, Mitchell and Nørreklit,

2015). As this company manufacture concrete materials, therefore, to handle the storage

of these products, it can adopt the concept of FIFO i.e. first in first out. It helps in

minimising cost of stock handling and storage by giving priority to sale products which

are manufacturing first so that quality of them can be managed.

Management Accounting reports:

Managerial accounting reports generally used by small entrepreneurs to monitor the

performance of company during an accounting period, so that necessary actions can be taken

timely to improve the same (Leitner, 2013). As per dependence on type of project and its time

limitation, Pavestone Ltd. can prepare reports in terms of monthly, quarterly, weekly or even

daily basis. Hereby, reporting method will help in circulating the precious information

throughout entire management chain by proper communication, so that top managers can take

process costing method instead of batch costing for increasing efficiencies of its

production cost.

Price management – It is generally used for analysing how demand of customers

fluctuate with change in price of products. As Pavestone deals with construction

materials therefore, any fluctuations in price will directly impact on its supply and

demand. It also helps in analysing factors that impact on price strategy of company, so

that concrete materials can be offered at better price on competitive rate.

Cost accounting – This system is mainly designed to keep track the inventories flow

during each stage of production (Turban, Volonino and Wood, 2015). Hereby, respective

company can assess the viability of different project by applying cost accounting system

because it provides a fixed cost structure, through which annual financial budget can be

planned. Along with this, Pavestone can also use this system to record production

activities as well, for keeping stock available in inventories to fulfil demand of customers

on time.

Inventory management – This system can help Pavestone in specifying the shape and

manner of placement of stocks as per consumer demand. For minimising the inventory

cost, it is required by management of this company to precede the regular as well as

planned course of stocks at each location of a supply (Nielsen, Mitchell and Nørreklit,

2015). As this company manufacture concrete materials, therefore, to handle the storage

of these products, it can adopt the concept of FIFO i.e. first in first out. It helps in

minimising cost of stock handling and storage by giving priority to sale products which

are manufacturing first so that quality of them can be managed.

Management Accounting reports:

Managerial accounting reports generally used by small entrepreneurs to monitor the

performance of company during an accounting period, so that necessary actions can be taken

timely to improve the same (Leitner, 2013). As per dependence on type of project and its time

limitation, Pavestone Ltd. can prepare reports in terms of monthly, quarterly, weekly or even

daily basis. Hereby, reporting method will help in circulating the precious information

throughout entire management chain by proper communication, so that top managers can take

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

better actions for improving the performance. But before applying any concept, it is better for

Pavestone Ltd. to understand the concept of each phase of reporting in following way -

Budget Report – This method of reporting helps respective company in evaluating the

performance of company and determining if business is able to meet its costs of production

(Lavia López and Hiebl, 2014). By analysing the performance of each department and cost

required for completing any project, managers of Pavestone Ltd. find feasible ways in order to

trim costs and prepare budget for further process.

Cost accounting reports: This report provides information related to cost required for

production and completion of any product. It helps in developing a basis for preparing budget by

using different kind of cost analysis method. In context with Pavestone, as it deals in

construction sector so cost refers to be a key factor for determining its profitability.

Inventory management report: This report is used by those companies that have

physical inventories in order to make manufacturing process more efficient. It mainly concerns

on terms like inventory wastage, per unit overhead costs and hourly labour costs etc. to

determine exhibits value of stock that a company has in its stores and warehouse. Therefore,

tracking of real time inventory movement and above stages, management of Pavestone Ltd. can

determine area where improvement is necessary to get best performance from each department,

so that profitability ratio can be increased by minimising expensive cost of production.

Benefits of management accounting system:

Adopting the concept of management accounting systems give various advantages to

Pavestone Ltd. in taking proper decisions related to price, management of inventories and more,

as shown below -

Price Optimisation System

This system aid Pavestone in developing the optimum price

strategy for its product with purpose to get high profitability

margin, as per customer requirements.

Inventory Management

System

Through techniques of this system, respective company can

manage its inventory well and make it available as per

customer demand.

Job Costing System

The management of respective manufacturing company in

estimating the cost of each specific task to analyse the overall

Pavestone Ltd. to understand the concept of each phase of reporting in following way -

Budget Report – This method of reporting helps respective company in evaluating the

performance of company and determining if business is able to meet its costs of production

(Lavia López and Hiebl, 2014). By analysing the performance of each department and cost

required for completing any project, managers of Pavestone Ltd. find feasible ways in order to

trim costs and prepare budget for further process.

Cost accounting reports: This report provides information related to cost required for

production and completion of any product. It helps in developing a basis for preparing budget by

using different kind of cost analysis method. In context with Pavestone, as it deals in

construction sector so cost refers to be a key factor for determining its profitability.

Inventory management report: This report is used by those companies that have

physical inventories in order to make manufacturing process more efficient. It mainly concerns

on terms like inventory wastage, per unit overhead costs and hourly labour costs etc. to

determine exhibits value of stock that a company has in its stores and warehouse. Therefore,

tracking of real time inventory movement and above stages, management of Pavestone Ltd. can

determine area where improvement is necessary to get best performance from each department,

so that profitability ratio can be increased by minimising expensive cost of production.

Benefits of management accounting system:

Adopting the concept of management accounting systems give various advantages to

Pavestone Ltd. in taking proper decisions related to price, management of inventories and more,

as shown below -

Price Optimisation System

This system aid Pavestone in developing the optimum price

strategy for its product with purpose to get high profitability

margin, as per customer requirements.

Inventory Management

System

Through techniques of this system, respective company can

manage its inventory well and make it available as per

customer demand.

Job Costing System

The management of respective manufacturing company in

estimating the cost of each specific task to analyse the overall

cost required for producing the product.

Cost Accounting System

This system can help Pavestone in minimising its expenses

or unproductive cost activities.

Evaluation of manner of integration of systems and reporting within process of business entity:

For increasing efficiencies of production and minimising the wastages, it is essential for

Pavestone Ltd. to integrate the management accounting and reporting system within business.

This would help in developing better strategies for managing costs and improving performance

of each department, so that ratio of profitability can be increased (Senftlechner and Hiebl, 2015).

Along with this, managerial accounting reports also aid this company in determining area where

improvement is essential for managing budget and controlling the wastages.

Costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs:

Marginal costing method: This concept is used to determine changes in total costs,

when quantity of products is increased by one unit. In other words, marginal costing method is

used to analyse the impact of variable cost on total volume of production (Wickramasinghe and

Alawattage, 2012). Therefore, managers of Pavestone can use this costing method for examining

the optimum production quantity where, company requires to put least costs for producing

addition units of inventory. Along with this, it also helps in meeting demand of customers when

they seek to get certain products on lowest price as much as possible.

Absorption costing method: This method of costing indicates that for producing any

additional quantity of products, all manufacturing costs will be calculated, in terms of direct

material, labour, fixed and variable overhead expenses etc. Pavestone Ltd. can use absorption

costing method calculating income tax reporting and external financial reporting, so that better

actions can be taken.

ANNEX (A)

Income statement in terms of marginal costing method:

Particulars Quarter 1

Product A

Product

B

Cost Accounting System

This system can help Pavestone in minimising its expenses

or unproductive cost activities.

Evaluation of manner of integration of systems and reporting within process of business entity:

For increasing efficiencies of production and minimising the wastages, it is essential for

Pavestone Ltd. to integrate the management accounting and reporting system within business.

This would help in developing better strategies for managing costs and improving performance

of each department, so that ratio of profitability can be increased (Senftlechner and Hiebl, 2015).

Along with this, managerial accounting reports also aid this company in determining area where

improvement is essential for managing budget and controlling the wastages.

Costs using appropriate techniques of cost analysis to prepare an income statement using

marginal and absorption costs:

Marginal costing method: This concept is used to determine changes in total costs,

when quantity of products is increased by one unit. In other words, marginal costing method is

used to analyse the impact of variable cost on total volume of production (Wickramasinghe and

Alawattage, 2012). Therefore, managers of Pavestone can use this costing method for examining

the optimum production quantity where, company requires to put least costs for producing

addition units of inventory. Along with this, it also helps in meeting demand of customers when

they seek to get certain products on lowest price as much as possible.

Absorption costing method: This method of costing indicates that for producing any

additional quantity of products, all manufacturing costs will be calculated, in terms of direct

material, labour, fixed and variable overhead expenses etc. Pavestone Ltd. can use absorption

costing method calculating income tax reporting and external financial reporting, so that better

actions can be taken.

ANNEX (A)

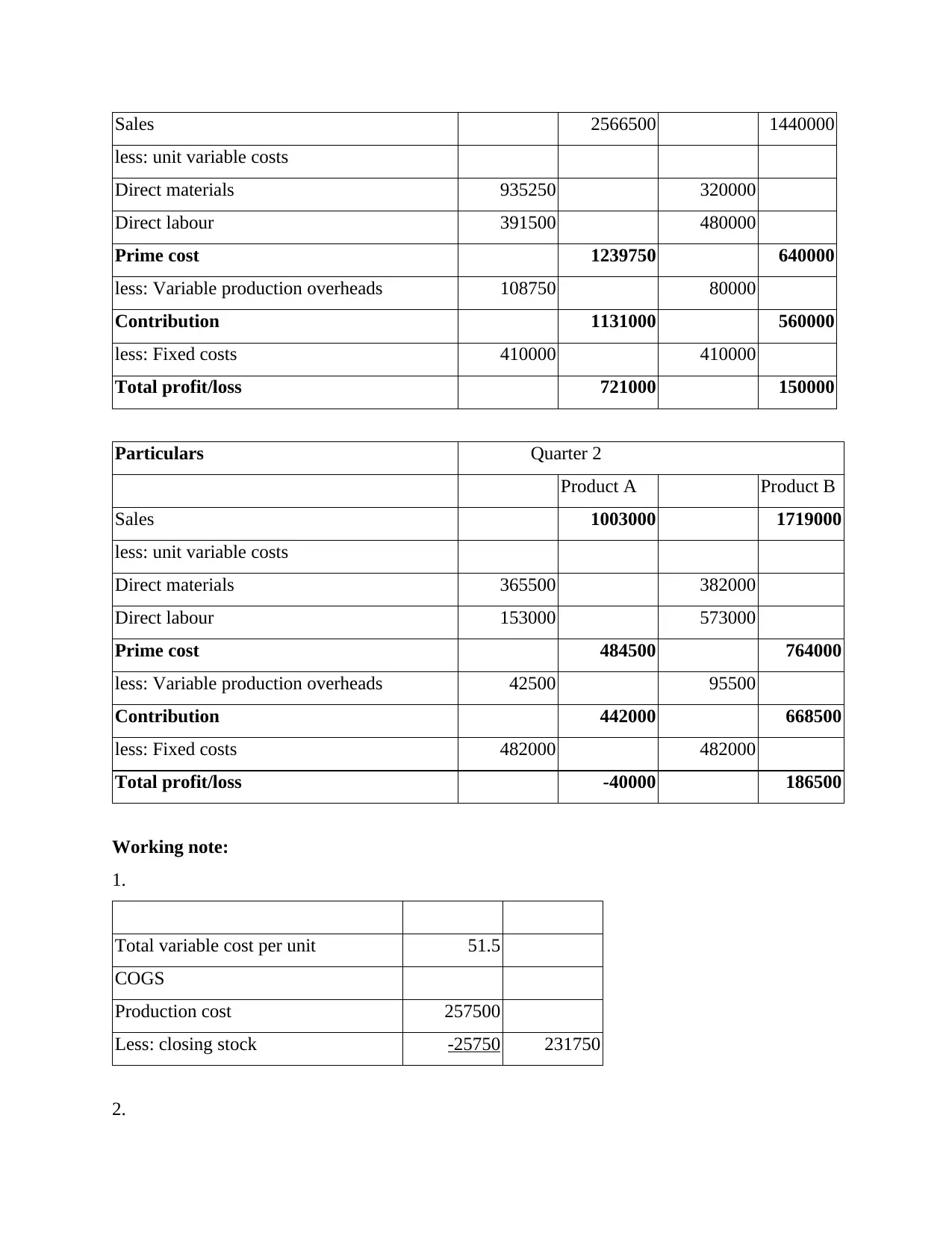

Income statement in terms of marginal costing method:

Particulars Quarter 1

Product A

Product

B

Sales 2566500 1440000

less: unit variable costs

Direct materials 935250 320000

Direct labour 391500 480000

Prime cost 1239750 640000

less: Variable production overheads 108750 80000

Contribution 1131000 560000

less: Fixed costs 410000 410000

Total profit/loss 721000 150000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: unit variable costs

Direct materials 365500 382000

Direct labour 153000 573000

Prime cost 484500 764000

less: Variable production overheads 42500 95500

Contribution 442000 668500

less: Fixed costs 482000 482000

Total profit/loss -40000 186500

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

less: unit variable costs

Direct materials 935250 320000

Direct labour 391500 480000

Prime cost 1239750 640000

less: Variable production overheads 108750 80000

Contribution 1131000 560000

less: Fixed costs 410000 410000

Total profit/loss 721000 150000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: unit variable costs

Direct materials 365500 382000

Direct labour 153000 573000

Prime cost 484500 764000

less: Variable production overheads 42500 95500

Contribution 442000 668500

less: Fixed costs 482000 482000

Total profit/loss -40000 186500

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

Absorption 6800

Income statement by absorption costing method

Particulars Quarter 1

Product A Product B

Sales 2566500 1440000

less: Cost of sales

Opening inventory - -

Direct materials 935250 320000

Direct labour 391500 480000

Variable overheads 108750 80000

Fixed costs 410000 410000

less: Closing inventory -650 1844850 -4000 1286000

Gross profit/loss 721650 154000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: Cost of sales

Opening inventory 650 4000

Direct materials 365500 382000

Direct labour 153000 573000

Variable overheads 42500 95500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

Absorption 6800

Income statement by absorption costing method

Particulars Quarter 1

Product A Product B

Sales 2566500 1440000

less: Cost of sales

Opening inventory - -

Direct materials 935250 320000

Direct labour 391500 480000

Variable overheads 108750 80000

Fixed costs 410000 410000

less: Closing inventory -650 1844850 -4000 1286000

Gross profit/loss 721650 154000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: Cost of sales

Opening inventory 650 4000

Direct materials 365500 382000

Direct labour 153000 573000

Variable overheads 42500 95500

Fixed costs 482000 482000

less: Closing inventory -3500 1040150 -2900 1533600

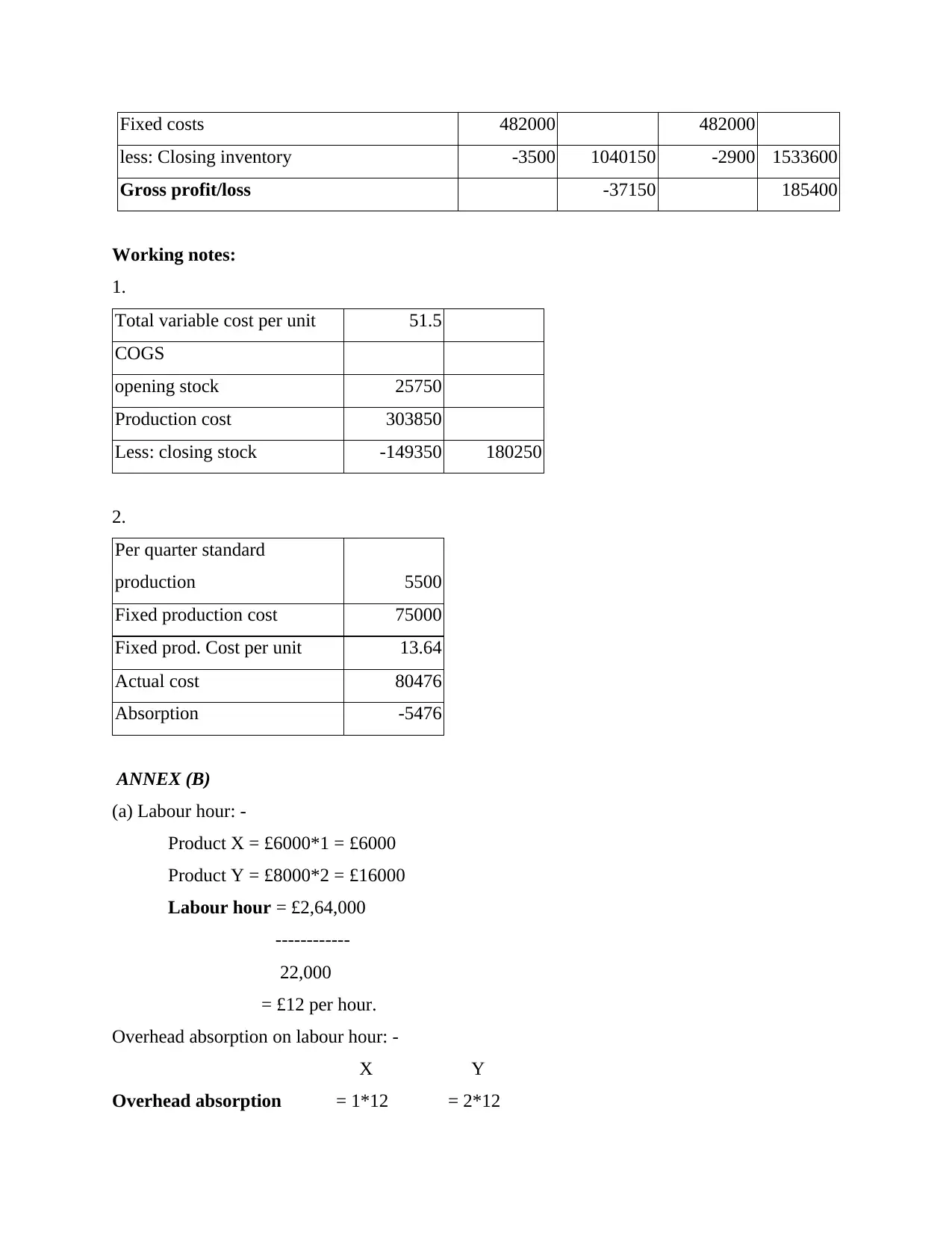

Gross profit/loss -37150 185400

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

Absorption -5476

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

less: Closing inventory -3500 1040150 -2900 1533600

Gross profit/loss -37150 185400

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

Absorption -5476

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

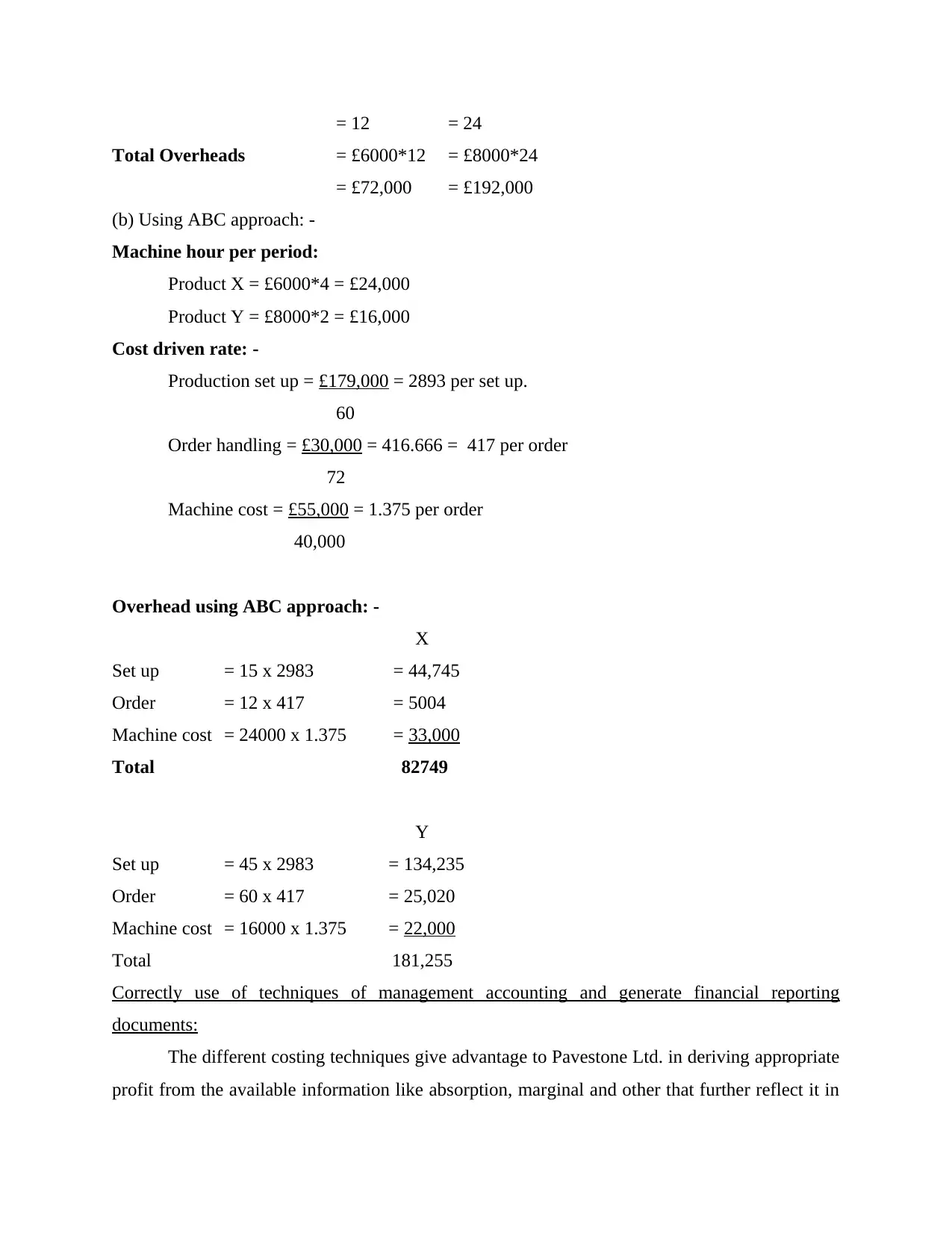

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15 x 2983 = 44,745

Order = 12 x 417 = 5004

Machine cost = 24000 x 1.375 = 33,000

Total 82749

Y

Set up = 45 x 2983 = 134,235

Order = 60 x 417 = 25,020

Machine cost = 16000 x 1.375 = 22,000

Total 181,255

Correctly use of techniques of management accounting and generate financial reporting

documents:

The different costing techniques give advantage to Pavestone Ltd. in deriving appropriate

profit from the available information like absorption, marginal and other that further reflect it in

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15 x 2983 = 44,745

Order = 12 x 417 = 5004

Machine cost = 24000 x 1.375 = 33,000

Total 82749

Y

Set up = 45 x 2983 = 134,235

Order = 60 x 417 = 25,020

Machine cost = 16000 x 1.375 = 22,000

Total 181,255

Correctly use of techniques of management accounting and generate financial reporting

documents:

The different costing techniques give advantage to Pavestone Ltd. in deriving appropriate

profit from the available information like absorption, marginal and other that further reflect it in

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

financial statements (Soin and Collier, 2013). Hereby, marginal costing can be used to obtain net

operating income require for producing external quantity. Along with this, by using concept of

break-even techniques, managers of this company can analyse the point where gross profit

income can raise high, so that price of products can be decided appropriately.

Interpret Financial reports prepared and data for a range of business activities:

From the above income statements, which has prepared via absorption and marginal costing

method, it has been interpreted that difference is occurred in both results due to application of

different approaches. As per marginal costing, net income required for increase one single

commodity is 721k for product A and 150k for B respectively, while for second quantity it is 40k

and 186.5k for product A and B respectively. While through absorption costing, the net income

is analysed for Q1 is 721.65k and 154k for product A and B respectively, on the other hand for

Q2 it is estimated as -37.15k and 185.4k. So, it is recommended to Pavestone to use absorption

costing method to produce additional quantities of inventory.

ACTIVITY 2

Explanation of different planning tool used for budgetary control

Budget and budgetary control can be defined as document which is prepared to

estimate the income that may acquire during an accounting period and expenses required for

producing and managing the inventory stocks. Having a specified budget can help managers of

Pavestone Ltd. in analysing entire funds required for operating different functions in desired

way. Along with this, by preparing the budget plan, managers of respective company can also

keep record of planned activities as well as control expenses required for manufacturing and

delivering its concrete materials to other construction companies (Ward, 2012). To formulate the

specific budget plan, this company also needs to analyse cost required for entire production

activities first so that strategies can be made to allocate finance in appropriate way to each

department. Furthermore, to keep finance and appropriate budget to meet future demand, it is

also essential for management of Pavestone to use proper planning tools as described below –

Zero based budget: This kind of budget plan starts with initial or zero base that guide

managers of respective company to keep record of each expense in books. In this regard, to begin

with each accounting year, a company needs to generate a new zero based budget plan, where

outstanding figures are generally ignored to analyse need of cost required for further activities.

operating income require for producing external quantity. Along with this, by using concept of

break-even techniques, managers of this company can analyse the point where gross profit

income can raise high, so that price of products can be decided appropriately.

Interpret Financial reports prepared and data for a range of business activities:

From the above income statements, which has prepared via absorption and marginal costing

method, it has been interpreted that difference is occurred in both results due to application of

different approaches. As per marginal costing, net income required for increase one single

commodity is 721k for product A and 150k for B respectively, while for second quantity it is 40k

and 186.5k for product A and B respectively. While through absorption costing, the net income

is analysed for Q1 is 721.65k and 154k for product A and B respectively, on the other hand for

Q2 it is estimated as -37.15k and 185.4k. So, it is recommended to Pavestone to use absorption

costing method to produce additional quantities of inventory.

ACTIVITY 2

Explanation of different planning tool used for budgetary control

Budget and budgetary control can be defined as document which is prepared to

estimate the income that may acquire during an accounting period and expenses required for

producing and managing the inventory stocks. Having a specified budget can help managers of

Pavestone Ltd. in analysing entire funds required for operating different functions in desired

way. Along with this, by preparing the budget plan, managers of respective company can also

keep record of planned activities as well as control expenses required for manufacturing and

delivering its concrete materials to other construction companies (Ward, 2012). To formulate the

specific budget plan, this company also needs to analyse cost required for entire production

activities first so that strategies can be made to allocate finance in appropriate way to each

department. Furthermore, to keep finance and appropriate budget to meet future demand, it is

also essential for management of Pavestone to use proper planning tools as described below –

Zero based budget: This kind of budget plan starts with initial or zero base that guide

managers of respective company to keep record of each expense in books. In this regard, to begin

with each accounting year, a company needs to generate a new zero based budget plan, where

outstanding figures are generally ignored to analyse need of cost required for further activities.

The main advantage and drawbacks of this type of budgeting plans can be analysed in following

way -

Advantages Disadvantages

Zero budget plan helps in allocating funds in

different departments efficiently for getting

high performance because having information

of entire expenses aid managers of Pavestone

Ltd. in taking right decisions for increasing

effectiveness of production cost.

As this method avoid outstanding figures

therefore, performance of previous accounting

year cannot be determined for evaluating the

efficiency of current year.

Master budget: To keep record of entire budget plans that gives detail of overall

financial projection, a company mainly use master budget plan, which is considered as

aggregation of all. The main benefits with limitation of this budget for Pavestone Ltd. can be

described as -

Advantages Disadvantages

Summarising information of each budget will

aid respective company in making proper

decisions for further forecasting of budget.

This method also give details of information

related to achievement of goals in terms of

cash flow, expenses and revenue.

Brief data may create issues in analysing

overall transaction that create issues between

stakeholders for making appropriate decisions

for future budget plans.

Capital budget: This kind of budget plan is prepared to make records of each capital

expense required to determine profitability of various projects, that are developed to increase

efficiency of business (Maas, Schaltegger and Crutzen, 2016). Therefore, using capital budget

plan, management of Pavestone Ltd. can make records of current financial position of business

so that, better investment can be made for attainment of future goals. Advantages and

disadvantages of this budget can be examined in following way -

Advantages Disadvantages

This method helps in making appropriate

decisions for making investment in those

Any wrong decision related to make

investment in a project which proves not

way -

Advantages Disadvantages

Zero budget plan helps in allocating funds in

different departments efficiently for getting

high performance because having information

of entire expenses aid managers of Pavestone

Ltd. in taking right decisions for increasing

effectiveness of production cost.

As this method avoid outstanding figures

therefore, performance of previous accounting

year cannot be determined for evaluating the

efficiency of current year.

Master budget: To keep record of entire budget plans that gives detail of overall

financial projection, a company mainly use master budget plan, which is considered as

aggregation of all. The main benefits with limitation of this budget for Pavestone Ltd. can be

described as -

Advantages Disadvantages

Summarising information of each budget will

aid respective company in making proper

decisions for further forecasting of budget.

This method also give details of information

related to achievement of goals in terms of

cash flow, expenses and revenue.

Brief data may create issues in analysing

overall transaction that create issues between

stakeholders for making appropriate decisions

for future budget plans.

Capital budget: This kind of budget plan is prepared to make records of each capital

expense required to determine profitability of various projects, that are developed to increase

efficiency of business (Maas, Schaltegger and Crutzen, 2016). Therefore, using capital budget

plan, management of Pavestone Ltd. can make records of current financial position of business

so that, better investment can be made for attainment of future goals. Advantages and

disadvantages of this budget can be examined in following way -

Advantages Disadvantages

This method helps in making appropriate

decisions for making investment in those

Any wrong decision related to make

investment in a project which proves not

projects that raise profitability of business, by

determining various risks associated with

same. formulate decision regarding making

investment in most profitable project.

beneficial, may result to acquire heavy losses

in such case of budget plan.

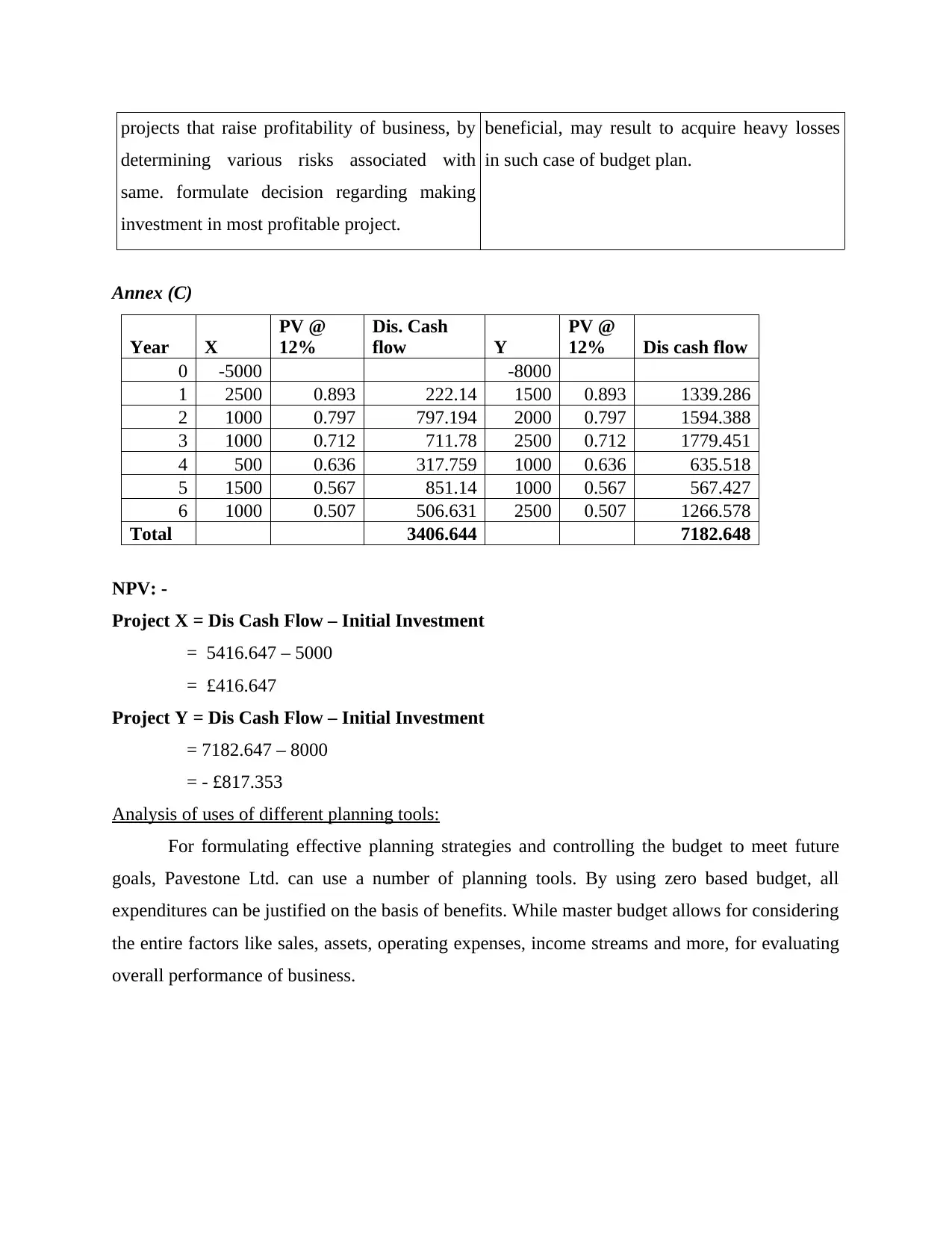

Annex (C)

Year X

PV @

12%

Dis. Cash

flow Y

PV @

12% Dis cash flow

0 -5000 -8000

1 2500 0.893 222.14 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.78 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.14 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 3406.644 7182.648

NPV: -

Project X = Dis Cash Flow – Initial Investment

= 5416.647 – 5000

= £416.647

Project Y = Dis Cash Flow – Initial Investment

= 7182.647 – 8000

= - £817.353

Analysis of uses of different planning tools:

For formulating effective planning strategies and controlling the budget to meet future

goals, Pavestone Ltd. can use a number of planning tools. By using zero based budget, all

expenditures can be justified on the basis of benefits. While master budget allows for considering

the entire factors like sales, assets, operating expenses, income streams and more, for evaluating

overall performance of business.

determining various risks associated with

same. formulate decision regarding making

investment in most profitable project.

beneficial, may result to acquire heavy losses

in such case of budget plan.

Annex (C)

Year X

PV @

12%

Dis. Cash

flow Y

PV @

12% Dis cash flow

0 -5000 -8000

1 2500 0.893 222.14 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.78 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.14 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 3406.644 7182.648

NPV: -

Project X = Dis Cash Flow – Initial Investment

= 5416.647 – 5000

= £416.647

Project Y = Dis Cash Flow – Initial Investment

= 7182.647 – 8000

= - £817.353

Analysis of uses of different planning tools:

For formulating effective planning strategies and controlling the budget to meet future

goals, Pavestone Ltd. can use a number of planning tools. By using zero based budget, all

expenditures can be justified on the basis of benefits. While master budget allows for considering

the entire factors like sales, assets, operating expenses, income streams and more, for evaluating

overall performance of business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Comparison of manner by which organisations are using management accounting systems to

respond financial problems:

Financial or budgetary problems in a company can raise by various issues like shortage of

resources, ineffective features of products or services, inappropriate way of processing and more.

All these problems can affect directly the profitability and productivity of business (Maas,

Schaltegger and Crutzen, 2016). Therefore, to respond over such issues, a company can use a

number of techniques like KPI, financial governance, benchmarking and more. In context with

Pavestone Ltd., the major financial issues has been occurred generally due to ineffective

management system, where lack of awareness of accounting principles, inability of recording

information in ledgers and books leads to increase financial crisis that affect entire performance

of business.

Therefore, in order to respond towards such financial issues, managers of Pavestone Ltd.

can use following techniques of management accounting -

KPI (Key performance indicators): The technique is used to determine how well a

company is doing to meet its desired goals, by evaluating the past record where it has gained

high profitability. Therefore, this would help Pavestone in identifying the area where

improvement is necessary so that chance of financial crises can be reduced.

Benchmarking: This technique is generally used for identifying internal opportunities

that a company has, for better improvement. It emphasises on measuring features of product or

services of a company by comparing with other competitors’, so that further improvement can be

made to increase efficiencies of same. This would help Pavestone in setting a benchmark of its

business against its major competitors and respond in better manner towards any financial issues.

In Pavestone Ltd. its managers mainly use KPI technique to resolve its financial issues by

identifying different factors that lead to raise such problems. This would help in identifying the

potential improvement that company can make for increasing the chance of getting high return of

investment on a particular project.

Comparison: To analyse the effectiveness of applications or techniques used by

company in order to respond different budgetary challenges, a comparison is done between

Pavestone Ltd. and one of its major rivalry as below :-

Pavestone Ltd. Aggregate Industry Concrete

Managers of Pavestone Ltd. mostly use capital Master budget plan is used by Aggregate

respond financial problems:

Financial or budgetary problems in a company can raise by various issues like shortage of

resources, ineffective features of products or services, inappropriate way of processing and more.

All these problems can affect directly the profitability and productivity of business (Maas,

Schaltegger and Crutzen, 2016). Therefore, to respond over such issues, a company can use a

number of techniques like KPI, financial governance, benchmarking and more. In context with

Pavestone Ltd., the major financial issues has been occurred generally due to ineffective

management system, where lack of awareness of accounting principles, inability of recording

information in ledgers and books leads to increase financial crisis that affect entire performance

of business.

Therefore, in order to respond towards such financial issues, managers of Pavestone Ltd.

can use following techniques of management accounting -

KPI (Key performance indicators): The technique is used to determine how well a

company is doing to meet its desired goals, by evaluating the past record where it has gained

high profitability. Therefore, this would help Pavestone in identifying the area where

improvement is necessary so that chance of financial crises can be reduced.

Benchmarking: This technique is generally used for identifying internal opportunities

that a company has, for better improvement. It emphasises on measuring features of product or

services of a company by comparing with other competitors’, so that further improvement can be

made to increase efficiencies of same. This would help Pavestone in setting a benchmark of its

business against its major competitors and respond in better manner towards any financial issues.

In Pavestone Ltd. its managers mainly use KPI technique to resolve its financial issues by

identifying different factors that lead to raise such problems. This would help in identifying the

potential improvement that company can make for increasing the chance of getting high return of

investment on a particular project.

Comparison: To analyse the effectiveness of applications or techniques used by

company in order to respond different budgetary challenges, a comparison is done between

Pavestone Ltd. and one of its major rivalry as below :-

Pavestone Ltd. Aggregate Industry Concrete

Managers of Pavestone Ltd. mostly use capital Master budget plan is used by Aggregate

budget plan before making any investment in

projects so that ratio of generating high return

on investment can be increased.

Industry Concrete deal with budgetary issues

and make proper plans for further investment

by analysing overall risks associated with

same.

This company use KPI technique like balance

scorecard to evaluate the success of any project

before making investment on it.

While Aggregate company uses the concept of

benchmarking for improving in cost structure

and internal process so that chance of getting

high return on investment can be increased.

Analysis of the way in which management accounting lead to respond financial problems

By applying different concepts of management accounting systems such as KPI and

benchmarking, managers of Pavestone Ltd. can recognise how to respond towards budgetary

issues. This would help in taking proper action against different problems by developing

effective strategic plans (Plumb and et.al., 2017). Hereby, benchmarking process will help

respective company in measuring current performance of products or services in a particular

marketplace, by making a comparison with other companies of same sector. While, KPI

application may help in determining the success of particular project by performance

measurement system. Thus, both processes help Pavestone in making proper decisions for

budgetary control and responding towards different situations, for increasing efficiencies of

business.

Use of planning tools to respond financial problems:

By using different planning tools such as master budget, capital budget, zero budget and

more, management of Pavestone Ltd. can make better plans for future expansion of business.

This would also help in analysing on which project, company needs to make investment so that

higher profitability ratio can be gained (Laudon and Laudon, 2015). Along with this, decisions

can also be taken for responding towards future demand of business, by keeping finance enough

to meet the same.

CONCLUSION

It has been summarised from this entire report that to manage entire profitability of

business and cost of production, it is essential for a company to apply different techniques of

projects so that ratio of generating high return

on investment can be increased.

Industry Concrete deal with budgetary issues

and make proper plans for further investment

by analysing overall risks associated with

same.

This company use KPI technique like balance

scorecard to evaluate the success of any project

before making investment on it.

While Aggregate company uses the concept of

benchmarking for improving in cost structure

and internal process so that chance of getting

high return on investment can be increased.

Analysis of the way in which management accounting lead to respond financial problems

By applying different concepts of management accounting systems such as KPI and

benchmarking, managers of Pavestone Ltd. can recognise how to respond towards budgetary

issues. This would help in taking proper action against different problems by developing

effective strategic plans (Plumb and et.al., 2017). Hereby, benchmarking process will help

respective company in measuring current performance of products or services in a particular

marketplace, by making a comparison with other companies of same sector. While, KPI

application may help in determining the success of particular project by performance

measurement system. Thus, both processes help Pavestone in making proper decisions for

budgetary control and responding towards different situations, for increasing efficiencies of

business.

Use of planning tools to respond financial problems:

By using different planning tools such as master budget, capital budget, zero budget and

more, management of Pavestone Ltd. can make better plans for future expansion of business.

This would also help in analysing on which project, company needs to make investment so that

higher profitability ratio can be gained (Laudon and Laudon, 2015). Along with this, decisions

can also be taken for responding towards future demand of business, by keeping finance enough

to meet the same.

CONCLUSION

It has been summarised from this entire report that to manage entire profitability of

business and cost of production, it is essential for a company to apply different techniques of

management accounting. This would help in making appropriate decisions for increasing

efficiencies of production by minimising the costs and expenses required for manufacturing the

products. Along with this, for making appropriate plans for strengthening the business

capabilities, organisations can apply different concept of managerial reporting and budget plans.

Furthermore, for responding towards various situations related to budgetary plans, a company

can also different applications like Benchmarking process, Key performance indicators and

financial governance.

efficiencies of production by minimising the costs and expenses required for manufacturing the

products. Along with this, for making appropriate plans for strengthening the business

capabilities, organisations can apply different concept of managerial reporting and budget plans.

Furthermore, for responding towards various situations related to budgetary plans, a company

can also different applications like Benchmarking process, Key performance indicators and

financial governance.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.