University Report: Management Accounting and Performance Evaluation

VerifiedAdded on 2022/08/15

|7

|1026

|14

Report

AI Summary

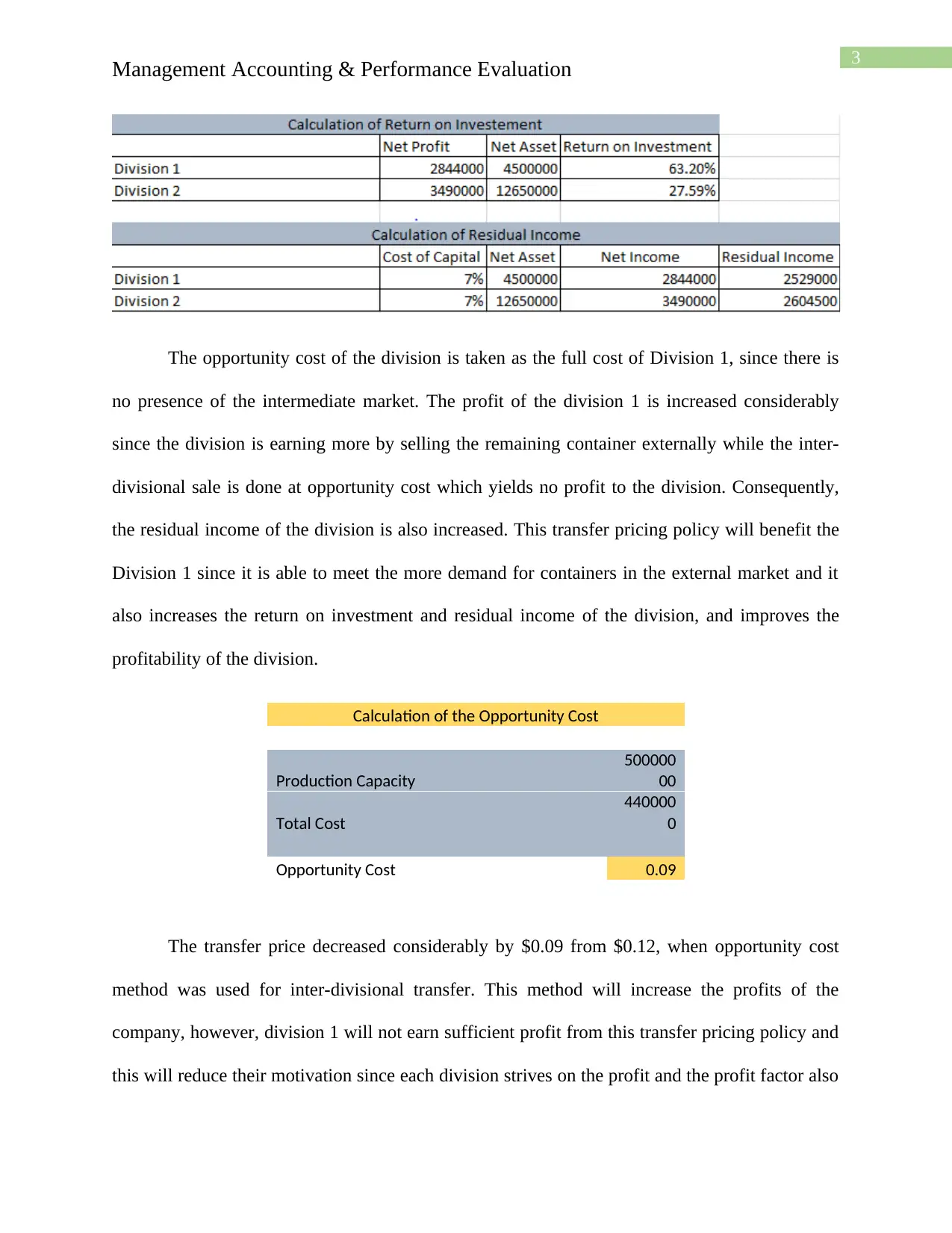

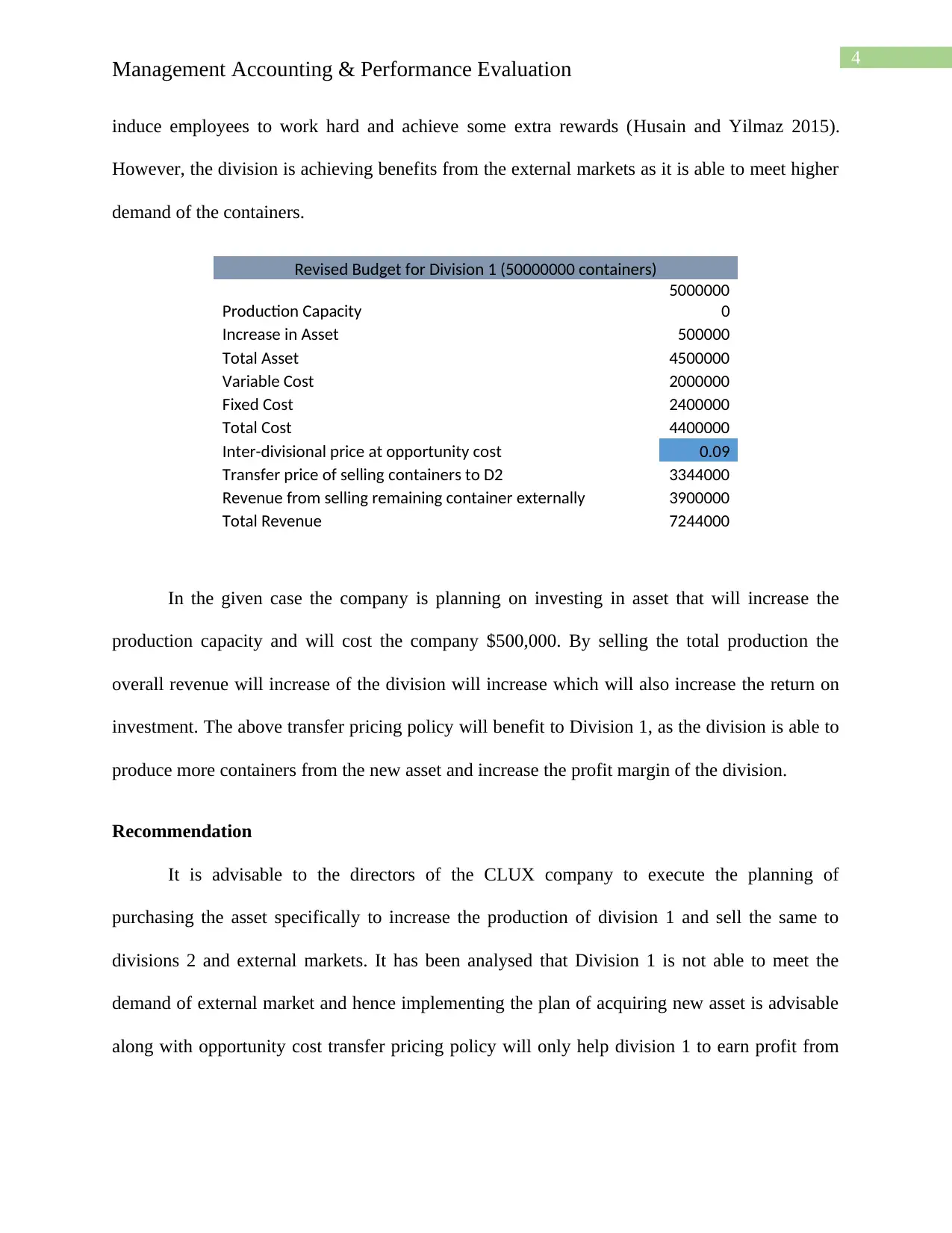

This report examines the transfer pricing policies of CLUX company, focusing on the impact of an asset investment on divisional performance. It analyzes how transfer pricing methods, specifically opportunity cost, affect profitability, return on investment (ROI), and residual income (RI). The report discusses the implications of inter-divisional transfers and external sales, evaluating how these strategies can benefit Division 1. It includes a revised budget for Division 1, detailing the financial impact of increased production capacity. The report concludes with recommendations for the directors of CLUX, suggesting the implementation of the asset purchase and opportunity cost transfer pricing to maximize profitability. The report highlights the importance of transfer pricing in optimizing company performance and provides insights into strategic decision-making for investment and divisional profit maximization.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.