Management Accounting: Customer Performance Measurement System Design

VerifiedAdded on 2023/06/14

|6

|739

|444

Report

AI Summary

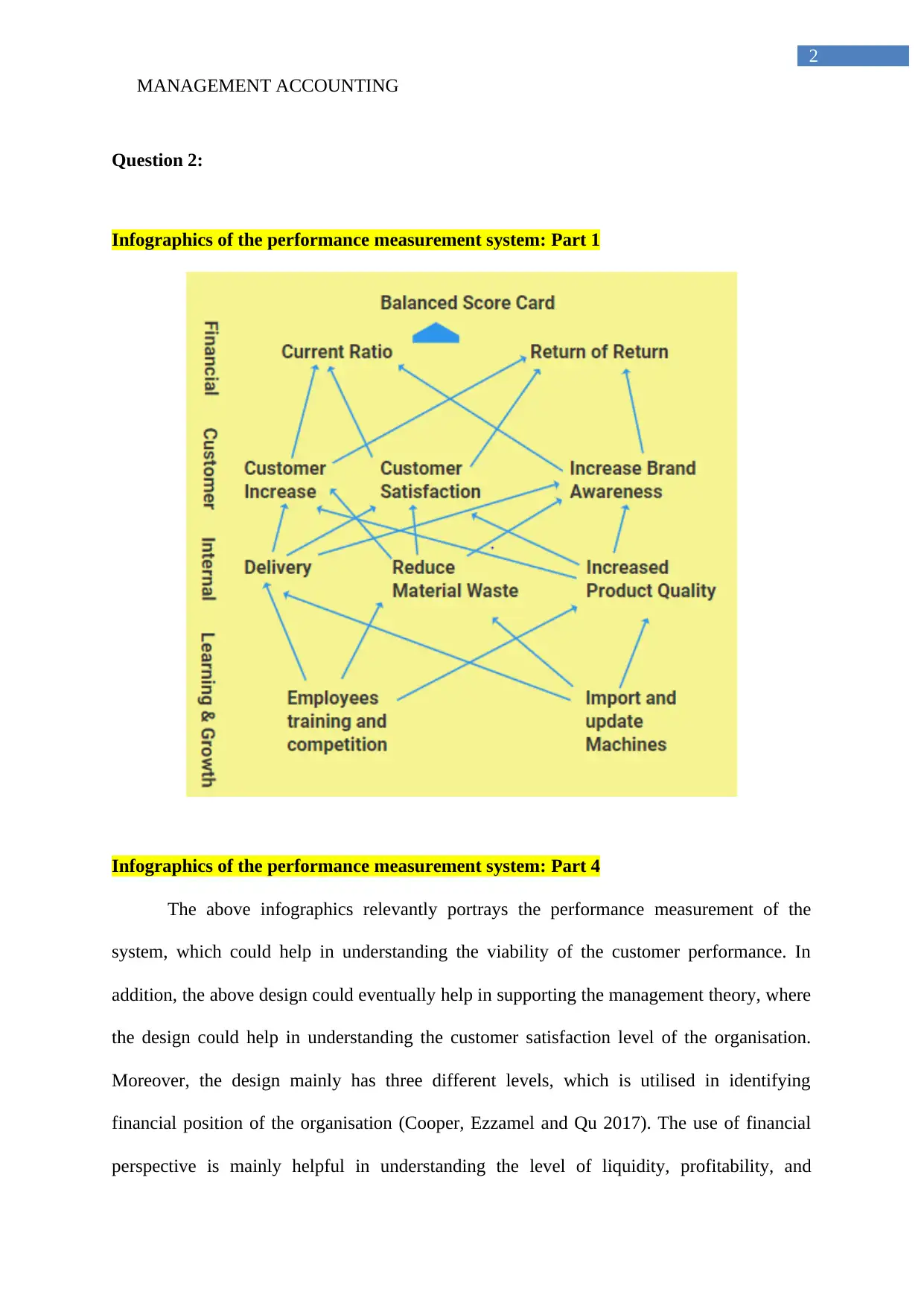

This report presents a comprehensive design for a performance measurement system, emphasizing customer performance within the framework of management accounting. The design incorporates four key perspectives: financial, customer, internal, and learning & growth. The financial perspective focuses on liquidity, profitability, and activity ratios. The customer perspective aims to enhance customer satisfaction and brand awareness. The internal perspective seeks to reduce waste and improve product quality. The learning & growth perspective emphasizes employee training and technological advancements. The report justifies the design's adoption by highlighting its potential to improve financial performance through enhanced customer satisfaction, operational efficiency, and strategic alignment. The design leverages management accounting theory to generate higher returns from operations and improve financial projections. Desklib offers this and many other solved assignments and past papers for students.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.