Introduction to Management Accounting - Plaistead Plc and Crawford Plc

VerifiedAdded on 2023/06/18

|19

|4234

|466

AI Summary

This article covers the topics of estimating contribution per unit, break-even sales revenue, profit estimation, and pricing strategy for Plaistead Plc. It also covers cost allocation and overhead cost allocation for Crawford Plc. The content is relevant for courses in management accounting and is applicable to students in various colleges and universities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Introduction to

management accounting

management accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents................................................................................................................................................2

Part 1.....................................................................................................................................................3

Question 2: Plaistead Plc..................................................................................................................3

Part 2.....................................................................................................................................................8

Question 3: Crawford Plc.................................................................................................................8

Part 3.....................................................................................................................................................3

Question 4:........................................................................................................................................3

REFERENCES.....................................................................................................................................9

Contents................................................................................................................................................2

Part 1.....................................................................................................................................................3

Question 2: Plaistead Plc..................................................................................................................3

Part 2.....................................................................................................................................................8

Question 3: Crawford Plc.................................................................................................................8

Part 3.....................................................................................................................................................3

Question 4:........................................................................................................................................3

REFERENCES.....................................................................................................................................9

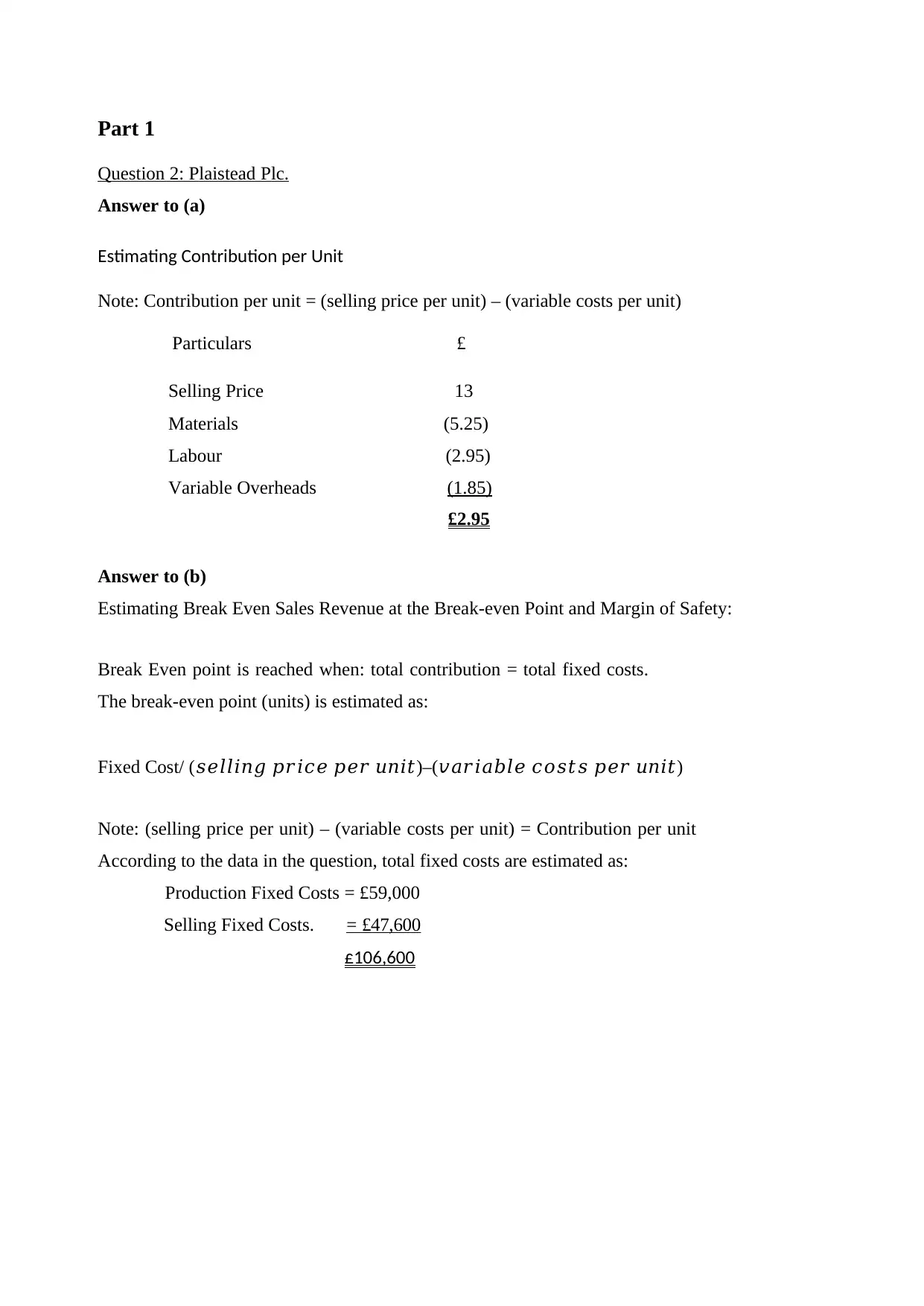

Part 1

Question 2: Plaistead Plc.

Answer to (a)

Estimating Contribution per Unit

Note: Contribution per unit = (selling price per unit) – (variable costs per unit)

Particulars £

Selling Price 13

Materials (5.25)

Labour (2.95)

Variable Overheads (1.85)

£2.95

Answer to (b)

Estimating Break Even Sales Revenue at the Break-even Point and Margin of Safety:

Break Even point is reached when: total contribution = total fixed costs.

The break-even point (units) is estimated as:

Fixed Cost/ (𝑠𝑒𝑙𝑙𝑖𝑛𝑔 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)–(𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝑐𝑜𝑠𝑡𝑠 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)

Note: (selling price per unit) – (variable costs per unit) = Contribution per unit

According to the data in the question, total fixed costs are estimated as:

Production Fixed Costs = £59,000

Selling Fixed Costs. = £47,600

£106,600

Question 2: Plaistead Plc.

Answer to (a)

Estimating Contribution per Unit

Note: Contribution per unit = (selling price per unit) – (variable costs per unit)

Particulars £

Selling Price 13

Materials (5.25)

Labour (2.95)

Variable Overheads (1.85)

£2.95

Answer to (b)

Estimating Break Even Sales Revenue at the Break-even Point and Margin of Safety:

Break Even point is reached when: total contribution = total fixed costs.

The break-even point (units) is estimated as:

Fixed Cost/ (𝑠𝑒𝑙𝑙𝑖𝑛𝑔 𝑝𝑟𝑖𝑐𝑒 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)–(𝑣𝑎𝑟𝑖𝑎𝑏𝑙𝑒 𝑐𝑜𝑠𝑡𝑠 𝑝𝑒𝑟 𝑢𝑛𝑖𝑡)

Note: (selling price per unit) – (variable costs per unit) = Contribution per unit

According to the data in the question, total fixed costs are estimated as:

Production Fixed Costs = £59,000

Selling Fixed Costs. = £47,600

£106,600

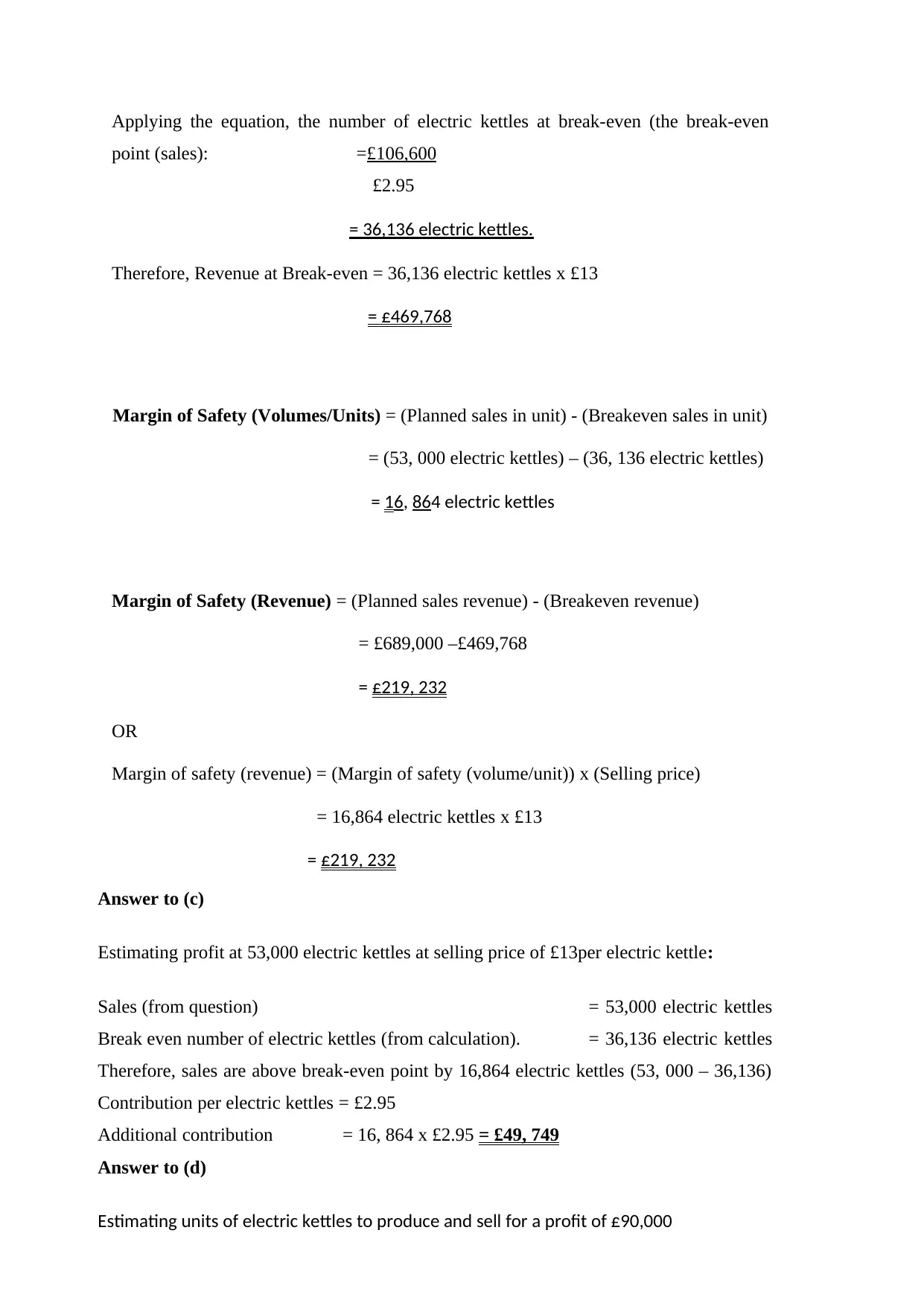

Applying the equation, the number of electric kettles at break-even (the break-even

point (sales): =£106,600

£2.95

= 36,136 electric kettles.

Therefore, Revenue at Break-even = 36,136 electric kettles x £13

= £469,768

Margin of Safety (Volumes/Units) = (Planned sales in unit) - (Breakeven sales in unit)

= (53, 000 electric kettles) – (36, 136 electric kettles)

= 16, 864 electric kettles

Margin of Safety (Revenue) = (Planned sales revenue) - (Breakeven revenue)

= £689,000 –£469,768

= £219, 232

OR

Margin of safety (revenue) = (Margin of safety (volume/unit)) x (Selling price)

= 16,864 electric kettles x £13

= £219, 232

Answer to (c)

Estimating profit at 53,000 electric kettles at selling price of £13per electric kettle:

Sales (from question) = 53,000 electric kettles

Break even number of electric kettles (from calculation). = 36,136 electric kettles

Therefore, sales are above break-even point by 16,864 electric kettles (53, 000 – 36,136)

Contribution per electric kettles = £2.95

Additional contribution = 16, 864 x £2.95 = £49, 749

Answer to (d)

Estimating units of electric kettles to produce and sell for a profit of £90,000

point (sales): =£106,600

£2.95

= 36,136 electric kettles.

Therefore, Revenue at Break-even = 36,136 electric kettles x £13

= £469,768

Margin of Safety (Volumes/Units) = (Planned sales in unit) - (Breakeven sales in unit)

= (53, 000 electric kettles) – (36, 136 electric kettles)

= 16, 864 electric kettles

Margin of Safety (Revenue) = (Planned sales revenue) - (Breakeven revenue)

= £689,000 –£469,768

= £219, 232

OR

Margin of safety (revenue) = (Margin of safety (volume/unit)) x (Selling price)

= 16,864 electric kettles x £13

= £219, 232

Answer to (c)

Estimating profit at 53,000 electric kettles at selling price of £13per electric kettle:

Sales (from question) = 53,000 electric kettles

Break even number of electric kettles (from calculation). = 36,136 electric kettles

Therefore, sales are above break-even point by 16,864 electric kettles (53, 000 – 36,136)

Contribution per electric kettles = £2.95

Additional contribution = 16, 864 x £2.95 = £49, 749

Answer to (d)

Estimating units of electric kettles to produce and sell for a profit of £90,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

According to the calculations provided, producing and offering to sell 36,136 electric

kettles will result in neither a loss nor profit. This is the moment at which the venture

pays off, and it is referred to as the break-even stage (Borthick and Pennington, 2017). .

If 36,136 electric kettles are created and sold, this would have been agreed to create

no gain, no losses (zero profits).

Every additional electric kettle purchased and sold would generate £2.95 (see

answer (a) above).

The variety of unique electric kettles to produce (in addition to 36,136 electric

kettles) to make £90,000 income is:

£90,000

£2.95

= 30,508 electric kettles.

As a result, the greatest number of electric kettles which could have been produced and sold in

order to generate a £90,000 profit would've been:

= (36,136 electric kettles) + (30,508 electric kettles = 66,644 electric kettles

Answer to (e)

Recalculating the sales price at which 53,000 electric kettles may be supplied for a £90,000 gain

Total contribution = (fixed costs) + (profit)

Therefore: Profit = (Total Contribution) – (Fixed Costs)

Thereafter: Derive ‘contribution per unit’ of 53, 000 electric kettles.

Note that: Contribution per unit = (selling price per unit) – (variable costs per unit)

Therefore: Selling Price per unit = (Contribution per unit) + (variable costs per unit) Total

Contribution is estimated as: £106,600 (Fixed costs) + £90,000 (Profit desired) = £196, 600

kettles will result in neither a loss nor profit. This is the moment at which the venture

pays off, and it is referred to as the break-even stage (Borthick and Pennington, 2017). .

If 36,136 electric kettles are created and sold, this would have been agreed to create

no gain, no losses (zero profits).

Every additional electric kettle purchased and sold would generate £2.95 (see

answer (a) above).

The variety of unique electric kettles to produce (in addition to 36,136 electric

kettles) to make £90,000 income is:

£90,000

£2.95

= 30,508 electric kettles.

As a result, the greatest number of electric kettles which could have been produced and sold in

order to generate a £90,000 profit would've been:

= (36,136 electric kettles) + (30,508 electric kettles = 66,644 electric kettles

Answer to (e)

Recalculating the sales price at which 53,000 electric kettles may be supplied for a £90,000 gain

Total contribution = (fixed costs) + (profit)

Therefore: Profit = (Total Contribution) – (Fixed Costs)

Thereafter: Derive ‘contribution per unit’ of 53, 000 electric kettles.

Note that: Contribution per unit = (selling price per unit) – (variable costs per unit)

Therefore: Selling Price per unit = (Contribution per unit) + (variable costs per unit) Total

Contribution is estimated as: £106,600 (Fixed costs) + £90,000 (Profit desired) = £196, 600

If 53,000 electric kettles are sold, contribution needed per electric kettles is estimated as:

£196, 600

53, 000 (electric kettles)

= £3.71

Therefore, the estimated selling price = (Contribution per unit) + (variable costs per unit):

Contribution per unit £3.71

Materials £5.25

Labour £2.95

Variable Overheads £1.85

New Selling Price £13.76

Answer to (f)

Adoption of new pricing strategy:

Proposed Strategy’s Selling Price = £13 x 1.09 (estimating 9% increase in

selling price)

= £14.17

Proposed Strategy’s Contribution (per kettle) = £2.95 + £1.17 (This is the proposed

Strategy’s selling price less old selling price)

= £4.12

Proposed Strategy’s Sales (in Units/Volume) = 53, 000 x 1.17 (estimating 17% increase in

Sales volume)

=62, 010 electric kettles

£196, 600

53, 000 (electric kettles)

= £3.71

Therefore, the estimated selling price = (Contribution per unit) + (variable costs per unit):

Contribution per unit £3.71

Materials £5.25

Labour £2.95

Variable Overheads £1.85

New Selling Price £13.76

Answer to (f)

Adoption of new pricing strategy:

Proposed Strategy’s Selling Price = £13 x 1.09 (estimating 9% increase in

selling price)

= £14.17

Proposed Strategy’s Contribution (per kettle) = £2.95 + £1.17 (This is the proposed

Strategy’s selling price less old selling price)

= £4.12

Proposed Strategy’s Sales (in Units/Volume) = 53, 000 x 1.17 (estimating 17% increase in

Sales volume)

=62, 010 electric kettles

Proposed Strategy’s Total Contribution = £4.12 x 62, 010 electric kettles

= £255,481

Proposed Strategy’s Fixed Costs = £106,600 + £45,000

= £151, 600

Proposed Strategy’s Profit = New Total Contribution – New Fixed Costs

= £255, 481 - £151,600

= £103, 881

The proposed approach provides a profit of £103, 881, which is higher than the £49,749

beginning cash profit. As a consequence (as mentioned in answer (c) above), the proposed plan

is a critical step that Plaistead Plc must accept.

Answer to (g)

The break-even calculation is dependent on several factors, such as the following:

Production, shipping, and carrying cost are all subdivided into permanent and variable parts.

There will be a propensity if assessment information is recorded on a graph because the

structure of spending is ongoing (Bühler, Wallenburg and Wieland, 2016).

At every present generation, the overall amount of capital expenditures will remain constant,

whereas operating cost will fluctuate in relation to output.

The maker's sales costs would remain constant regardless of the number of sales, suggesting

that they would not alter in reaction to differences in end products.

The installation costs, workers, accommodation, marketing, and other purchased technology

will all remain same.

The public's perceptions, as well as the scientific capabilities and effectiveness of computer

networks, would stay constant.

Profits and expenses were also calculated utilizing a completely electronic assessment, such

as stock fair pricing or quantity demanded (Chung and Chen, 2016).

Only the productive capacity or advertising is considered a significant part of the cost.

= £255,481

Proposed Strategy’s Fixed Costs = £106,600 + £45,000

= £151, 600

Proposed Strategy’s Profit = New Total Contribution – New Fixed Costs

= £255, 481 - £151,600

= £103, 881

The proposed approach provides a profit of £103, 881, which is higher than the £49,749

beginning cash profit. As a consequence (as mentioned in answer (c) above), the proposed plan

is a critical step that Plaistead Plc must accept.

Answer to (g)

The break-even calculation is dependent on several factors, such as the following:

Production, shipping, and carrying cost are all subdivided into permanent and variable parts.

There will be a propensity if assessment information is recorded on a graph because the

structure of spending is ongoing (Bühler, Wallenburg and Wieland, 2016).

At every present generation, the overall amount of capital expenditures will remain constant,

whereas operating cost will fluctuate in relation to output.

The maker's sales costs would remain constant regardless of the number of sales, suggesting

that they would not alter in reaction to differences in end products.

The installation costs, workers, accommodation, marketing, and other purchased technology

will all remain same.

The public's perceptions, as well as the scientific capabilities and effectiveness of computer

networks, would stay constant.

Profits and expenses were also calculated utilizing a completely electronic assessment, such

as stock fair pricing or quantity demanded (Chung and Chen, 2016).

Only the productive capacity or advertising is considered a significant part of the cost.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Part 2

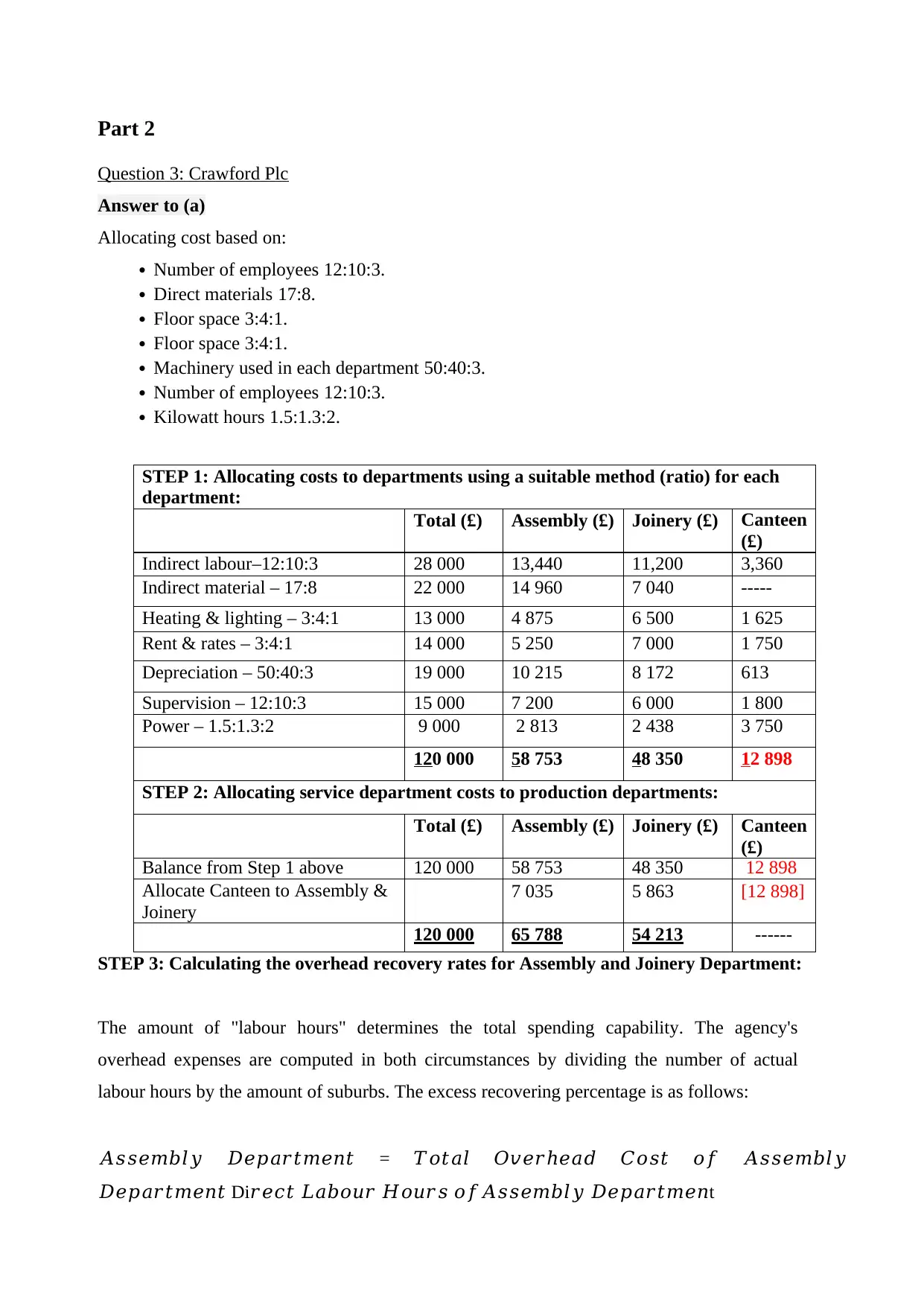

Question 3: Crawford Plc

Answer to (a)

Allocating cost based on:

Number of employees 12:10:3.

Direct materials 17:8.

Floor space 3:4:1.

Floor space 3:4:1.

Machinery used in each department 50:40:3.

Number of employees 12:10:3.

Kilowatt hours 1.5:1.3:2.

STEP 1: Allocating costs to departments using a suitable method (ratio) for each

department:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Indirect labour–12:10:3 28 000 13,440 11,200 3,360

Indirect material – 17:8 22 000 14 960 7 040 -----

Heating & lighting – 3:4:1 13 000 4 875 6 500 1 625

Rent & rates – 3:4:1 14 000 5 250 7 000 1 750

Depreciation – 50:40:3 19 000 10 215 8 172 613

Supervision – 12:10:3 15 000 7 200 6 000 1 800

Power – 1.5:1.3:2 9 000 2 813 2 438 3 750

120 000 58 753 48 350 12 898

STEP 2: Allocating service department costs to production departments:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Balance from Step 1 above 120 000 58 753 48 350 12 898

Allocate Canteen to Assembly &

Joinery

7 035 5 863 [12 898]

120 000 65 788 54 213 ------

STEP 3: Calculating the overhead recovery rates for Assembly and Joinery Department:

The amount of "labour hours" determines the total spending capability. The agency's

overhead expenses are computed in both circumstances by dividing the number of actual

labour hours by the amount of suburbs. The excess recovering percentage is as follows:

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦

𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 Di𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

Question 3: Crawford Plc

Answer to (a)

Allocating cost based on:

Number of employees 12:10:3.

Direct materials 17:8.

Floor space 3:4:1.

Floor space 3:4:1.

Machinery used in each department 50:40:3.

Number of employees 12:10:3.

Kilowatt hours 1.5:1.3:2.

STEP 1: Allocating costs to departments using a suitable method (ratio) for each

department:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Indirect labour–12:10:3 28 000 13,440 11,200 3,360

Indirect material – 17:8 22 000 14 960 7 040 -----

Heating & lighting – 3:4:1 13 000 4 875 6 500 1 625

Rent & rates – 3:4:1 14 000 5 250 7 000 1 750

Depreciation – 50:40:3 19 000 10 215 8 172 613

Supervision – 12:10:3 15 000 7 200 6 000 1 800

Power – 1.5:1.3:2 9 000 2 813 2 438 3 750

120 000 58 753 48 350 12 898

STEP 2: Allocating service department costs to production departments:

Total (£) Assembly (£) Joinery (£) Canteen

(£)

Balance from Step 1 above 120 000 58 753 48 350 12 898

Allocate Canteen to Assembly &

Joinery

7 035 5 863 [12 898]

120 000 65 788 54 213 ------

STEP 3: Calculating the overhead recovery rates for Assembly and Joinery Department:

The amount of "labour hours" determines the total spending capability. The agency's

overhead expenses are computed in both circumstances by dividing the number of actual

labour hours by the amount of suburbs. The excess recovering percentage is as follows:

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦

𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 Di𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

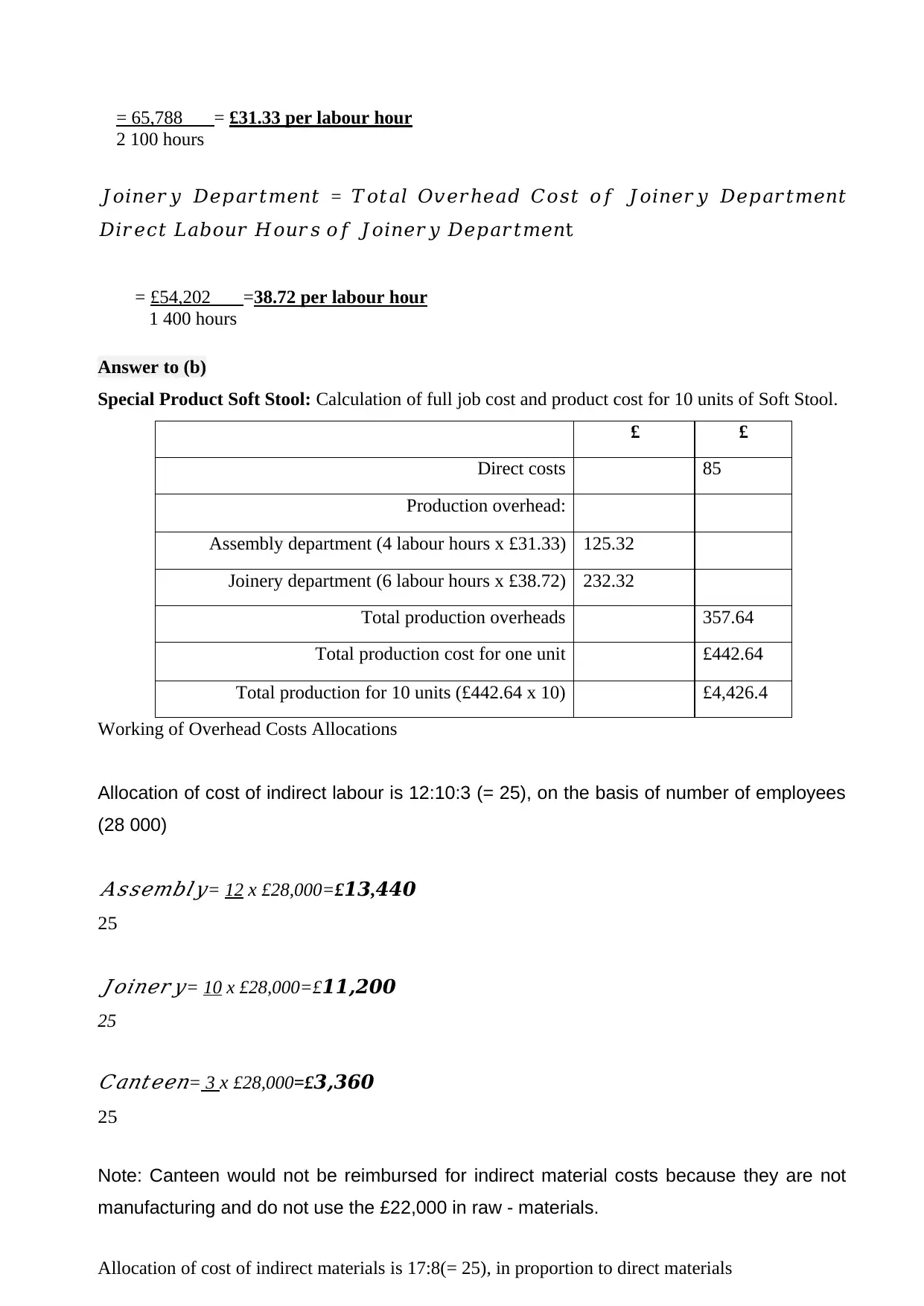

= 65,788 = £31.33 per labour hour

2 100 hours

𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡

𝐷𝑖𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

= £54,202 =38.72 per labour hour

1 400 hours

Answer to (b)

Special Product Soft Stool: Calculation of full job cost and product cost for 10 units of Soft Stool.

£ £

Direct costs 85

Production overhead:

Assembly department (4 labour hours x £31.33) 125.32

Joinery department (6 labour hours x £38.72) 232.32

Total production overheads 357.64

Total production cost for one unit £442.64

Total production for 10 units (£442.64 x 10) £4,426.4

Working of Overhead Costs Allocations

Allocation of cost of indirect labour is 12:10:3 (= 25), on the basis of number of employees

(28 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 12 x £28,000=£13,440

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 10 x £28,000=£11,200

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 3 x £28,000=£3,360

25

Note: Canteen would not be reimbursed for indirect material costs because they are not

manufacturing and do not use the £22,000 in raw - materials.

Allocation of cost of indirect materials is 17:8(= 25), in proportion to direct materials

2 100 hours

𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡 = 𝑇𝑜𝑡𝑎𝑙 𝑂𝑣𝑒𝑟ℎ𝑒𝑎𝑑 𝐶𝑜𝑠𝑡 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛𝑡

𝐷𝑖𝑟𝑒𝑐𝑡 𝐿𝑎𝑏𝑜𝑢𝑟 𝐻𝑜𝑢𝑟𝑠 𝑜𝑓 𝐽𝑜𝑖𝑛𝑒𝑟𝑦 𝐷𝑒𝑝𝑎𝑟𝑡𝑚𝑒𝑛t

= £54,202 =38.72 per labour hour

1 400 hours

Answer to (b)

Special Product Soft Stool: Calculation of full job cost and product cost for 10 units of Soft Stool.

£ £

Direct costs 85

Production overhead:

Assembly department (4 labour hours x £31.33) 125.32

Joinery department (6 labour hours x £38.72) 232.32

Total production overheads 357.64

Total production cost for one unit £442.64

Total production for 10 units (£442.64 x 10) £4,426.4

Working of Overhead Costs Allocations

Allocation of cost of indirect labour is 12:10:3 (= 25), on the basis of number of employees

(28 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 12 x £28,000=£13,440

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 10 x £28,000=£11,200

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 3 x £28,000=£3,360

25

Note: Canteen would not be reimbursed for indirect material costs because they are not

manufacturing and do not use the £22,000 in raw - materials.

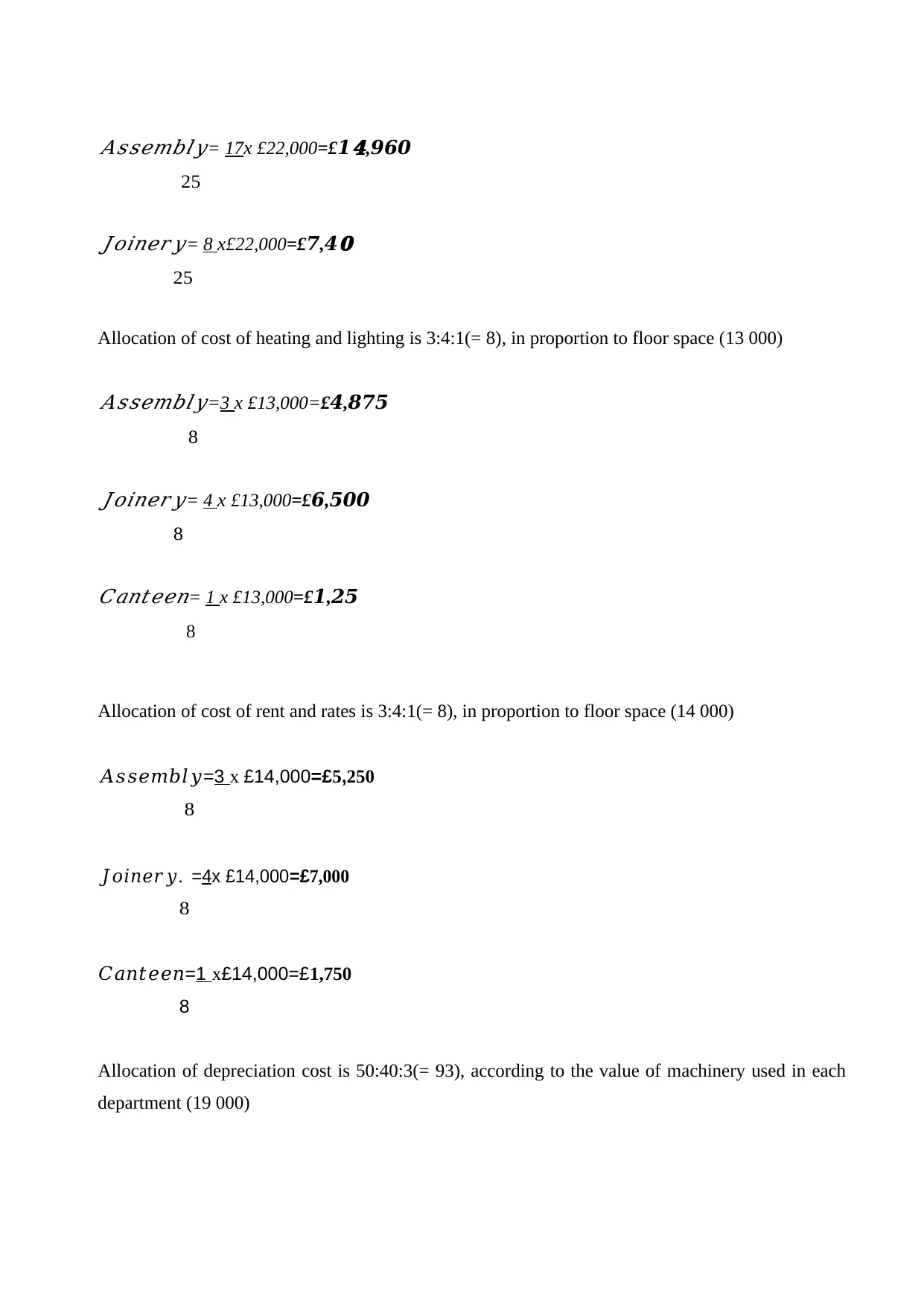

Allocation of cost of indirect materials is 17:8(= 25), in proportion to direct materials

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦= 17x £22,000=£1

𝟒,960

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 8 x£22,000=£7,4

𝟎

25

Allocation of cost of heating and lighting is 3:4:1(= 8), in proportion to floor space (13 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £13,000=£4,875

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 4 x £13,000=£6,500

8𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 1 x £13,000=£1,25

8

Allocation of cost of rent and rates is 3:4:1(= 8), in proportion to floor space (14 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £14,000=£5,250

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦. =4x £14,000=£7,000

8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=1 x£14,000=£1,750

8

Allocation of depreciation cost is 50:40:3(= 93), according to the value of machinery used in each

department (19 000)

𝟒,960

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 8 x£22,000=£7,4

𝟎

25

Allocation of cost of heating and lighting is 3:4:1(= 8), in proportion to floor space (13 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £13,000=£4,875

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦= 4 x £13,000=£6,500

8𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 1 x £13,000=£1,25

8

Allocation of cost of rent and rates is 3:4:1(= 8), in proportion to floor space (14 000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=3 x £14,000=£5,250

8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦. =4x £14,000=£7,000

8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=1 x£14,000=£1,750

8

Allocation of depreciation cost is 50:40:3(= 93), according to the value of machinery used in each

department (19 000)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

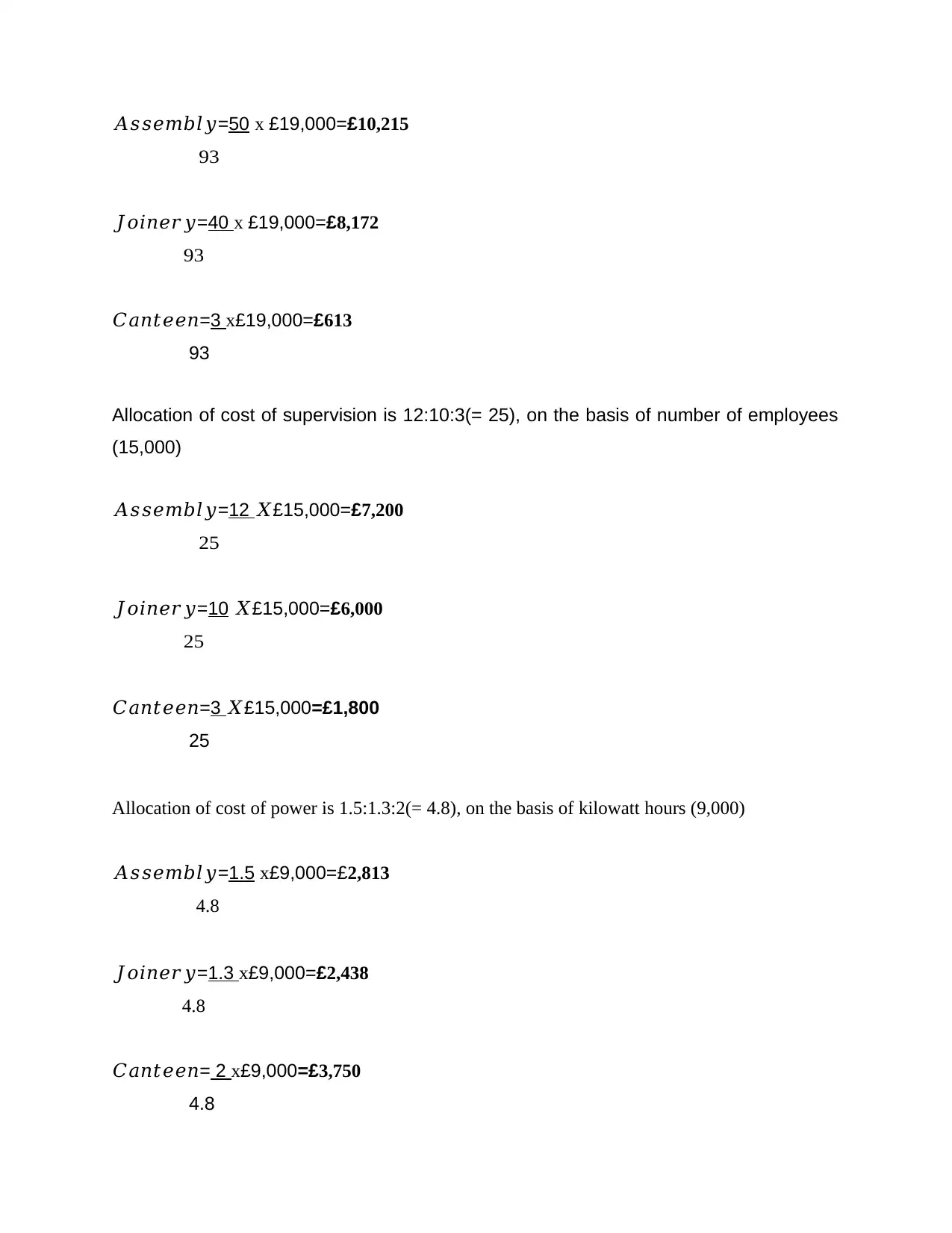

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=50 x £19,000=£10,215

93

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=40 x £19,000=£8,172

93

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 x£19,000=£613

93

Allocation of cost of supervision is 12:10:3(= 25), on the basis of number of employees

(15,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 𝑋£15,000=£7,200

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋£15,000=£6,000

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 𝑋£15,000=£1,800

25

Allocation of cost of power is 1.5:1.3:2(= 4.8), on the basis of kilowatt hours (9,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=1.5 x£9,000=£2,813

4.8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=1.3 x£9,000=£2,438

4.8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 2 x£9,000=£3,750

4.8

93

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=40 x £19,000=£8,172

93

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 x£19,000=£613

93

Allocation of cost of supervision is 12:10:3(= 25), on the basis of number of employees

(15,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 𝑋£15,000=£7,200

25

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋£15,000=£6,000

25

𝐶𝑎𝑛𝑡𝑒𝑒𝑛=3 𝑋£15,000=£1,800

25

Allocation of cost of power is 1.5:1.3:2(= 4.8), on the basis of kilowatt hours (9,000)

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=1.5 x£9,000=£2,813

4.8

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=1.3 x£9,000=£2,438

4.8

𝐶𝑎𝑛𝑡𝑒𝑒𝑛= 2 x£9,000=£3,750

4.8

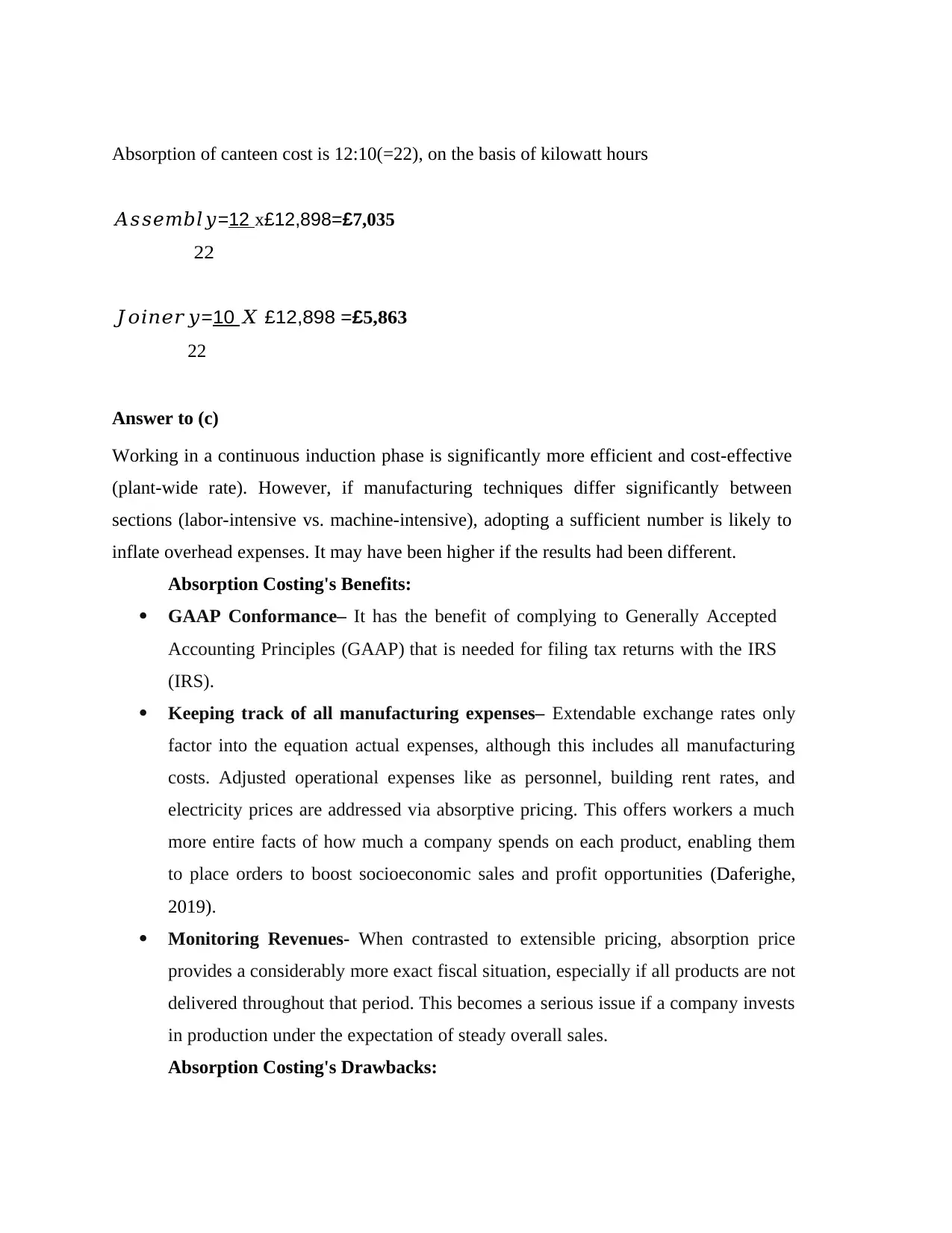

Absorption of canteen cost is 12:10(=22), on the basis of kilowatt hours

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 x£12,898=£7,035

22

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋 £12,898 =£5,863

22

Answer to (c)

Working in a continuous induction phase is significantly more efficient and cost-effective

(plant-wide rate). However, if manufacturing techniques differ significantly between

sections (labor-intensive vs. machine-intensive), adopting a sufficient number is likely to

inflate overhead expenses. It may have been higher if the results had been different.

Absorption Costing's Benefits:

GAAP Conformance– It has the benefit of complying to Generally Accepted

Accounting Principles (GAAP) that is needed for filing tax returns with the IRS

(IRS).

Keeping track of all manufacturing expenses– Extendable exchange rates only

factor into the equation actual expenses, although this includes all manufacturing

costs. Adjusted operational expenses like as personnel, building rent rates, and

electricity prices are addressed via absorptive pricing. This offers workers a much

more entire facts of how much a company spends on each product, enabling them

to place orders to boost socioeconomic sales and profit opportunities (Daferighe,

2019).

Monitoring Revenues- When contrasted to extensible pricing, absorption price

provides a considerably more exact fiscal situation, especially if all products are not

delivered throughout that period. This becomes a serious issue if a company invests

in production under the expectation of steady overall sales.

Absorption Costing's Drawbacks:

𝐴𝑠𝑠𝑒𝑚𝑏𝑙𝑦=12 x£12,898=£7,035

22

𝐽𝑜𝑖𝑛𝑒𝑟𝑦=10 𝑋 £12,898 =£5,863

22

Answer to (c)

Working in a continuous induction phase is significantly more efficient and cost-effective

(plant-wide rate). However, if manufacturing techniques differ significantly between

sections (labor-intensive vs. machine-intensive), adopting a sufficient number is likely to

inflate overhead expenses. It may have been higher if the results had been different.

Absorption Costing's Benefits:

GAAP Conformance– It has the benefit of complying to Generally Accepted

Accounting Principles (GAAP) that is needed for filing tax returns with the IRS

(IRS).

Keeping track of all manufacturing expenses– Extendable exchange rates only

factor into the equation actual expenses, although this includes all manufacturing

costs. Adjusted operational expenses like as personnel, building rent rates, and

electricity prices are addressed via absorptive pricing. This offers workers a much

more entire facts of how much a company spends on each product, enabling them

to place orders to boost socioeconomic sales and profit opportunities (Daferighe,

2019).

Monitoring Revenues- When contrasted to extensible pricing, absorption price

provides a considerably more exact fiscal situation, especially if all products are not

delivered throughout that period. This becomes a serious issue if a company invests

in production under the expectation of steady overall sales.

Absorption Costing's Drawbacks:

Lopsided Gain and Loss- Absorb costs can creates the appearance that a business

earns more money than it really does over the course of a financial year. This is

because all monetary obligations aren't deducted from the company's revenue until

all manufactured goods have been delivered. As a consequence, it's possible that top

leadership will be duped (Ejiogu and Ejiogu, 2018).

No operational effectiveness influence- Absorption sale costs do not give as

extensive a viability assessment as extensible cost, hence they have little impact on

plan efficacy. Despite the fact that constant costs make up a substantial share of

capital investment, finding out spending variations at different sales growth is

difficult, making it difficult for management to assure final judgments and activities.

Isn’t suitable for contrasting of items– Variable values, rather than absorbing

pricing, may well have been significantly more useful and successful in cases where

even a leader wants to integrate a maker's numerous income streams. This is owing

to the reality that tracking the produces higher of each product makes evaluating the

cost distinction between different items more simpler (Ghanem and Sulaiman,

2016).

Part 3

Question 4:

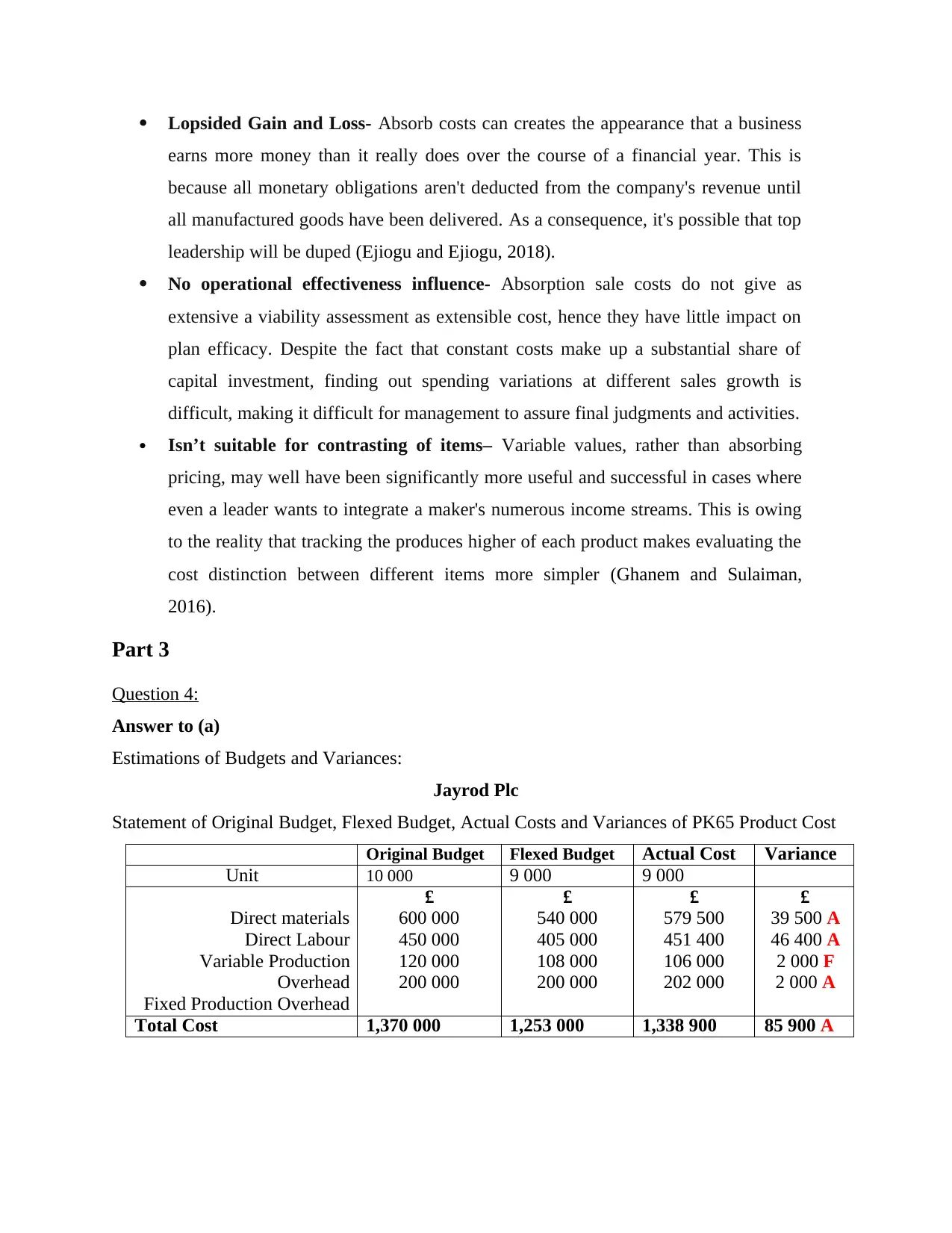

Answer to (a)

Estimations of Budgets and Variances:

Jayrod Plc

Statement of Original Budget, Flexed Budget, Actual Costs and Variances of PK65 Product Cost

Original Budget Flexed Budget Actual Cost Variance

Unit 10 000 9 000 9 000

£ £ £ £

Direct materials 600 000 540 000 579 500 39 500 A

Direct Labour 450 000 405 000 451 400 46 400 A

Variable Production 120 000 108 000 106 000 2 000 F

Overhead 200 000 200 000 202 000 2 000 A

Fixed Production Overhead

Total Cost 1,370 000 1,253 000 1,338 900 85 900 A

earns more money than it really does over the course of a financial year. This is

because all monetary obligations aren't deducted from the company's revenue until

all manufactured goods have been delivered. As a consequence, it's possible that top

leadership will be duped (Ejiogu and Ejiogu, 2018).

No operational effectiveness influence- Absorption sale costs do not give as

extensive a viability assessment as extensible cost, hence they have little impact on

plan efficacy. Despite the fact that constant costs make up a substantial share of

capital investment, finding out spending variations at different sales growth is

difficult, making it difficult for management to assure final judgments and activities.

Isn’t suitable for contrasting of items– Variable values, rather than absorbing

pricing, may well have been significantly more useful and successful in cases where

even a leader wants to integrate a maker's numerous income streams. This is owing

to the reality that tracking the produces higher of each product makes evaluating the

cost distinction between different items more simpler (Ghanem and Sulaiman,

2016).

Part 3

Question 4:

Answer to (a)

Estimations of Budgets and Variances:

Jayrod Plc

Statement of Original Budget, Flexed Budget, Actual Costs and Variances of PK65 Product Cost

Original Budget Flexed Budget Actual Cost Variance

Unit 10 000 9 000 9 000

£ £ £ £

Direct materials 600 000 540 000 579 500 39 500 A

Direct Labour 450 000 405 000 451 400 46 400 A

Variable Production 120 000 108 000 106 000 2 000 F

Overhead 200 000 200 000 202 000 2 000 A

Fixed Production Overhead

Total Cost 1,370 000 1,253 000 1,338 900 85 900 A

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

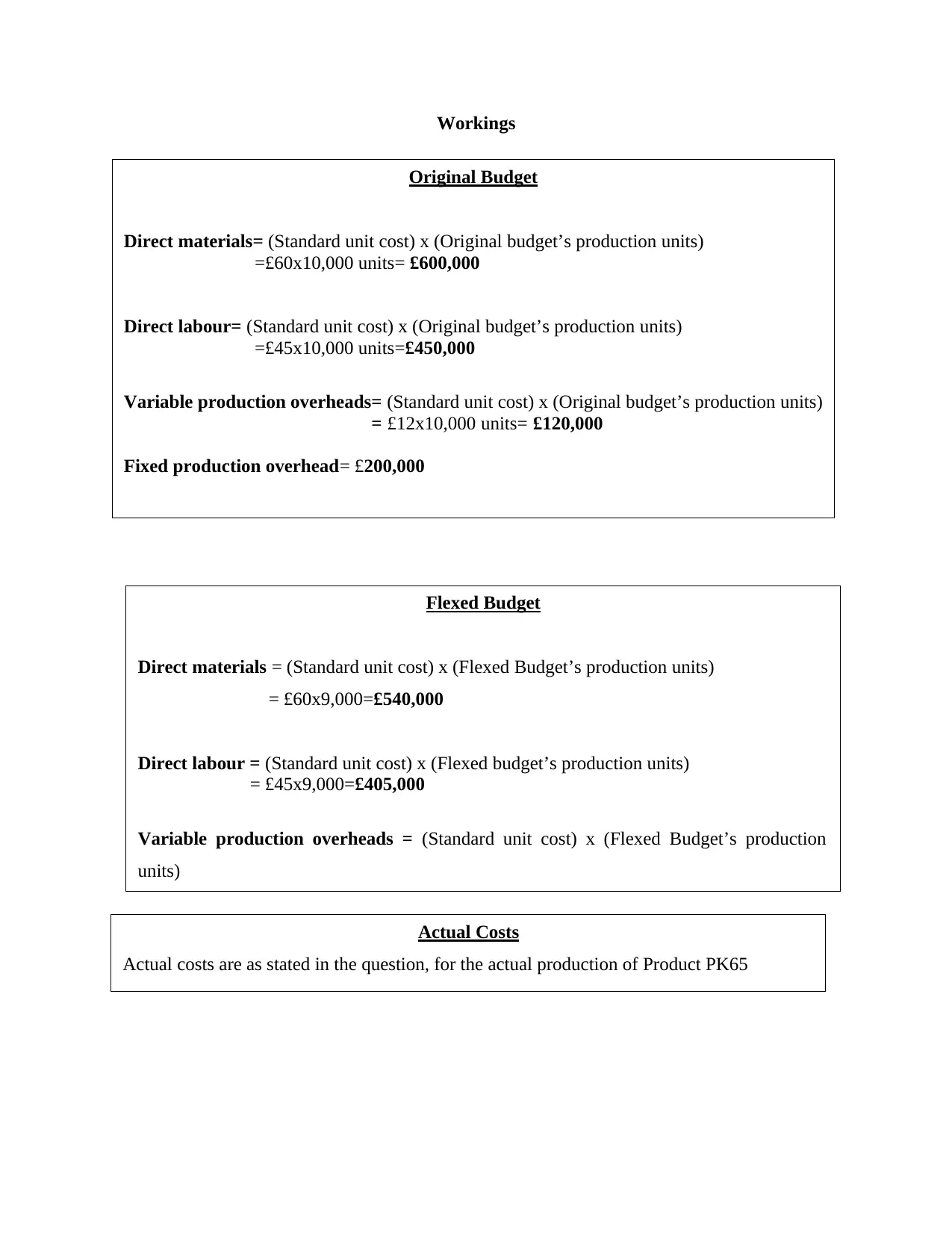

Original Budget

Direct materials= (Standard unit cost) x (Original budget’s production units)

=£60x10,000 units= £600,000

Direct labour= (Standard unit cost) x (Original budget’s production units)

=£45x10,000 units=£450,000

Variable production overheads= (Standard unit cost) x (Original budget’s production units)

= £12x10,000 units= £120,000

Fixed production overhead= £200,000

Actual Costs

Actual costs are as stated in the question, for the actual production of Product PK65

Workings

Flexed Budget

Direct materials = (Standard unit cost) x (Flexed Budget’s production units)

= £60x9,000=£540,000

Direct labour = (Standard unit cost) x (Flexed budget’s production units)

= £45x9,000=£405,000

Variable production overheads = (Standard unit cost) x (Flexed Budget’s production

units)

Direct materials= (Standard unit cost) x (Original budget’s production units)

=£60x10,000 units= £600,000

Direct labour= (Standard unit cost) x (Original budget’s production units)

=£45x10,000 units=£450,000

Variable production overheads= (Standard unit cost) x (Original budget’s production units)

= £12x10,000 units= £120,000

Fixed production overhead= £200,000

Actual Costs

Actual costs are as stated in the question, for the actual production of Product PK65

Workings

Flexed Budget

Direct materials = (Standard unit cost) x (Flexed Budget’s production units)

= £60x9,000=£540,000

Direct labour = (Standard unit cost) x (Flexed budget’s production units)

= £45x9,000=£405,000

Variable production overheads = (Standard unit cost) x (Flexed Budget’s production

units)

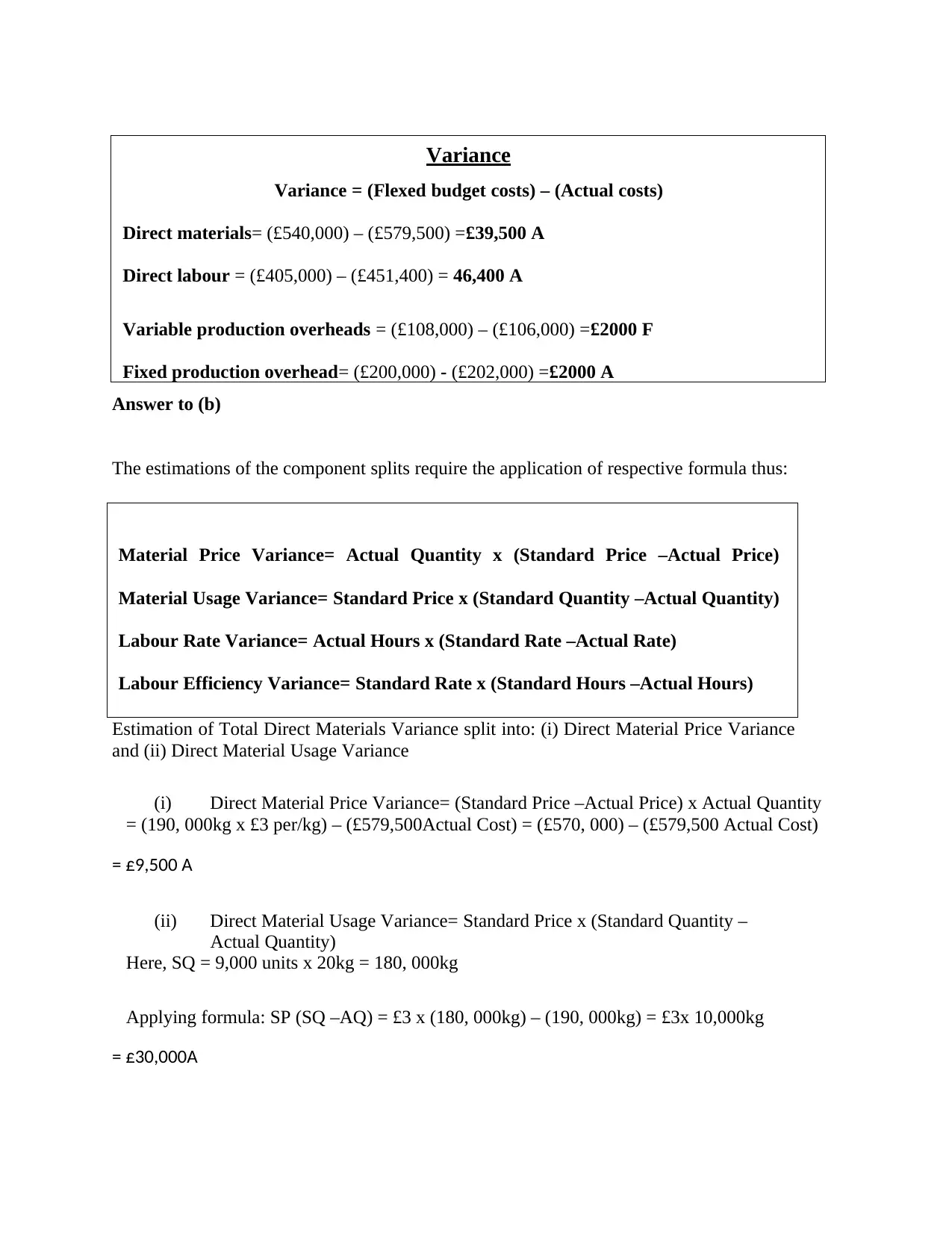

Variance

Variance = (Flexed budget costs) – (Actual costs)

Direct materials= (£540,000) – (£579,500) =£39,500 A

Direct labour = (£405,000) – (£451,400) = 46,400 A

Variable production overheads = (£108,000) – (£106,000) =£2000 F

Fixed production overhead= (£200,000) - (£202,000) =£2000 A

Material Price Variance= Actual Quantity x (Standard Price –Actual Price)

Material Usage Variance= Standard Price x (Standard Quantity –Actual Quantity)

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate)

Labour Efficiency Variance= Standard Rate x (Standard Hours –Actual Hours)

Answer to (b)

The estimations of the component splits require the application of respective formula thus:

Estimation of Total Direct Materials Variance split into: (i) Direct Material Price Variance

and (ii) Direct Material Usage Variance

(i) Direct Material Price Variance= (Standard Price –Actual Price) x Actual Quantity

= (190, 000kg x £3 per/kg) – (£579,500Actual Cost) = (£570, 000) – (£579,500 Actual Cost)

= £9,500 A

(ii) Direct Material Usage Variance= Standard Price x (Standard Quantity –

Actual Quantity)

Here, SQ = 9,000 units x 20kg = 180, 000kg

Applying formula: SP (SQ –AQ) = £3 x (180, 000kg) – (190, 000kg) = £3x 10,000kg

= £30,000A

Variance = (Flexed budget costs) – (Actual costs)

Direct materials= (£540,000) – (£579,500) =£39,500 A

Direct labour = (£405,000) – (£451,400) = 46,400 A

Variable production overheads = (£108,000) – (£106,000) =£2000 F

Fixed production overhead= (£200,000) - (£202,000) =£2000 A

Material Price Variance= Actual Quantity x (Standard Price –Actual Price)

Material Usage Variance= Standard Price x (Standard Quantity –Actual Quantity)

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate)

Labour Efficiency Variance= Standard Rate x (Standard Hours –Actual Hours)

Answer to (b)

The estimations of the component splits require the application of respective formula thus:

Estimation of Total Direct Materials Variance split into: (i) Direct Material Price Variance

and (ii) Direct Material Usage Variance

(i) Direct Material Price Variance= (Standard Price –Actual Price) x Actual Quantity

= (190, 000kg x £3 per/kg) – (£579,500Actual Cost) = (£570, 000) – (£579,500 Actual Cost)

= £9,500 A

(ii) Direct Material Usage Variance= Standard Price x (Standard Quantity –

Actual Quantity)

Here, SQ = 9,000 units x 20kg = 180, 000kg

Applying formula: SP (SQ –AQ) = £3 x (180, 000kg) – (190, 000kg) = £3x 10,000kg

= £30,000A

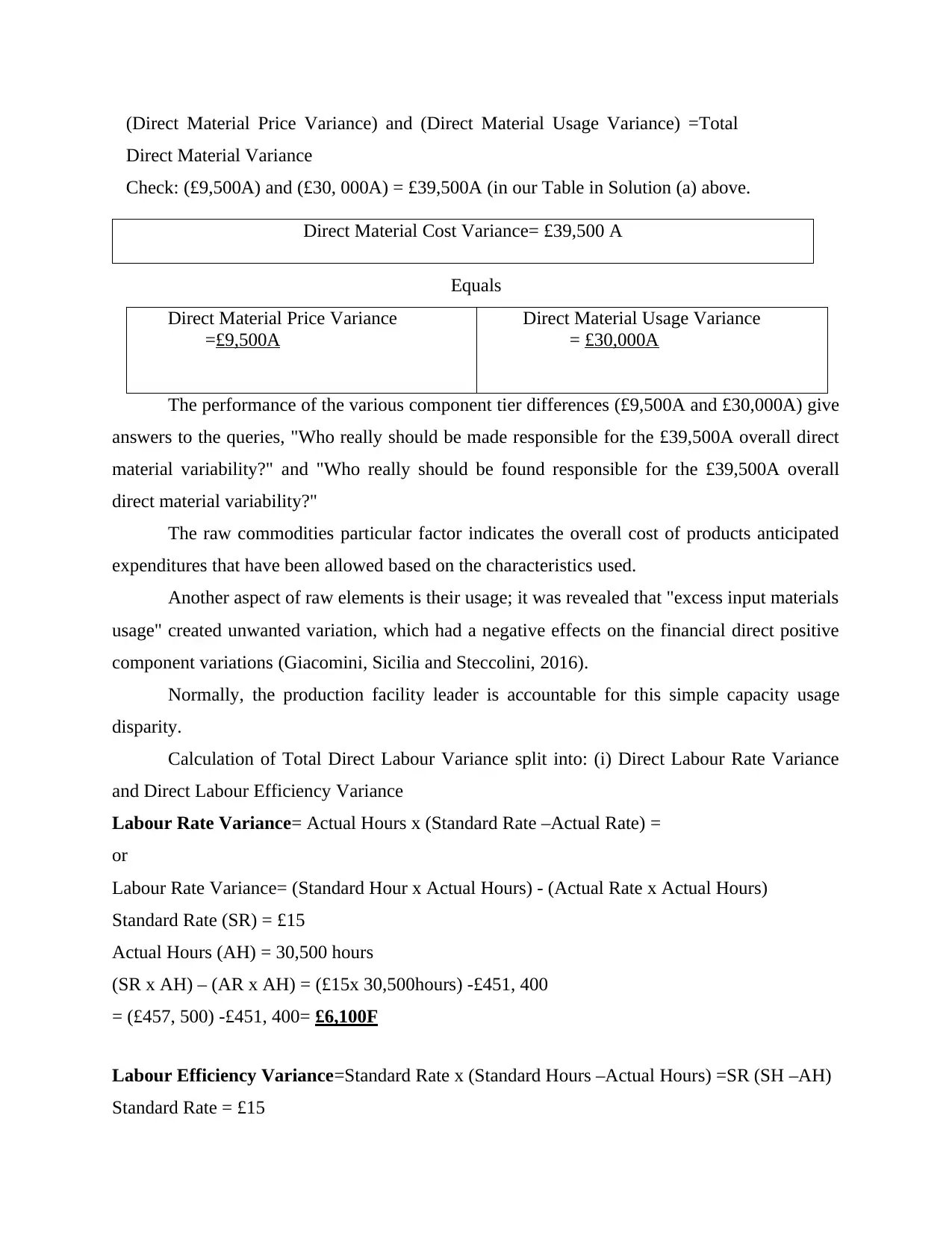

Direct Material Cost Variance= £39,500 A

(Direct Material Price Variance) and (Direct Material Usage Variance) =Total

Direct Material Variance

Check: (£9,500A) and (£30, 000A) = £39,500A (in our Table in Solution (a) above.

Equals

Direct Material Price Variance

=£9,500A

Direct Material Usage Variance

= £30,000A

The performance of the various component tier differences (£9,500A and £30,000A) give

answers to the queries, "Who really should be made responsible for the £39,500A overall direct

material variability?" and "Who really should be found responsible for the £39,500A overall

direct material variability?"

The raw commodities particular factor indicates the overall cost of products anticipated

expenditures that have been allowed based on the characteristics used.

Another aspect of raw elements is their usage; it was revealed that "excess input materials

usage" created unwanted variation, which had a negative effects on the financial direct positive

component variations (Giacomini, Sicilia and Steccolini, 2016).

Normally, the production facility leader is accountable for this simple capacity usage

disparity.

Calculation of Total Direct Labour Variance split into: (i) Direct Labour Rate Variance

and Direct Labour Efficiency Variance

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate) =

or

Labour Rate Variance= (Standard Hour x Actual Hours) - (Actual Rate x Actual Hours)

Standard Rate (SR) = £15

Actual Hours (AH) = 30,500 hours

(SR x AH) – (AR x AH) = (£15x 30,500hours) -£451, 400

= (£457, 500) -£451, 400= £6,100F

Labour Efficiency Variance=Standard Rate x (Standard Hours –Actual Hours) =SR (SH –AH)

Standard Rate = £15

(Direct Material Price Variance) and (Direct Material Usage Variance) =Total

Direct Material Variance

Check: (£9,500A) and (£30, 000A) = £39,500A (in our Table in Solution (a) above.

Equals

Direct Material Price Variance

=£9,500A

Direct Material Usage Variance

= £30,000A

The performance of the various component tier differences (£9,500A and £30,000A) give

answers to the queries, "Who really should be made responsible for the £39,500A overall direct

material variability?" and "Who really should be found responsible for the £39,500A overall

direct material variability?"

The raw commodities particular factor indicates the overall cost of products anticipated

expenditures that have been allowed based on the characteristics used.

Another aspect of raw elements is their usage; it was revealed that "excess input materials

usage" created unwanted variation, which had a negative effects on the financial direct positive

component variations (Giacomini, Sicilia and Steccolini, 2016).

Normally, the production facility leader is accountable for this simple capacity usage

disparity.

Calculation of Total Direct Labour Variance split into: (i) Direct Labour Rate Variance

and Direct Labour Efficiency Variance

Labour Rate Variance= Actual Hours x (Standard Rate –Actual Rate) =

or

Labour Rate Variance= (Standard Hour x Actual Hours) - (Actual Rate x Actual Hours)

Standard Rate (SR) = £15

Actual Hours (AH) = 30,500 hours

(SR x AH) – (AR x AH) = (£15x 30,500hours) -£451, 400

= (£457, 500) -£451, 400= £6,100F

Labour Efficiency Variance=Standard Rate x (Standard Hours –Actual Hours) =SR (SH –AH)

Standard Rate = £15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

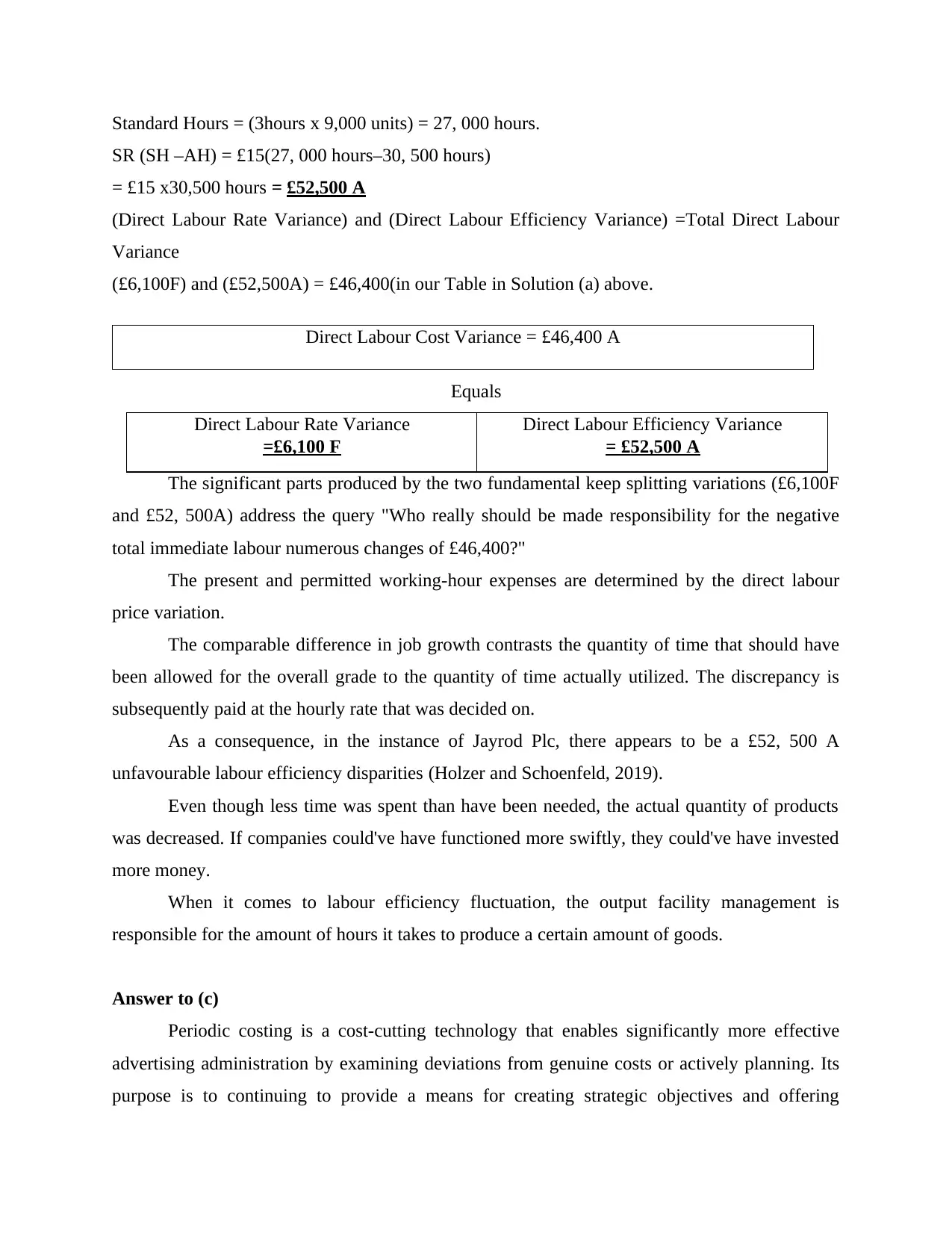

Direct Labour Cost Variance = £46,400 A

Standard Hours = (3hours x 9,000 units) = 27, 000 hours.

SR (SH –AH) = £15(27, 000 hours–30, 500 hours)

= £15 x30,500 hours = £52,500 A

(Direct Labour Rate Variance) and (Direct Labour Efficiency Variance) =Total Direct Labour

Variance

(£6,100F) and (£52,500A) = £46,400(in our Table in Solution (a) above.

Equals

Direct Labour Rate Variance

=£6,100 F

Direct Labour Efficiency Variance

= £52,500 A

The significant parts produced by the two fundamental keep splitting variations (£6,100F

and £52, 500A) address the query "Who really should be made responsibility for the negative

total immediate labour numerous changes of £46,400?"

The present and permitted working-hour expenses are determined by the direct labour

price variation.

The comparable difference in job growth contrasts the quantity of time that should have

been allowed for the overall grade to the quantity of time actually utilized. The discrepancy is

subsequently paid at the hourly rate that was decided on.

As a consequence, in the instance of Jayrod Plc, there appears to be a £52, 500 A

unfavourable labour efficiency disparities (Holzer and Schoenfeld, 2019).

Even though less time was spent than have been needed, the actual quantity of products

was decreased. If companies could've have functioned more swiftly, they could've have invested

more money.

When it comes to labour efficiency fluctuation, the output facility management is

responsible for the amount of hours it takes to produce a certain amount of goods.

Answer to (c)

Periodic costing is a cost-cutting technology that enables significantly more effective

advertising administration by examining deviations from genuine costs or actively planning. Its

purpose is to continuing to provide a means for creating strategic objectives and offering

Standard Hours = (3hours x 9,000 units) = 27, 000 hours.

SR (SH –AH) = £15(27, 000 hours–30, 500 hours)

= £15 x30,500 hours = £52,500 A

(Direct Labour Rate Variance) and (Direct Labour Efficiency Variance) =Total Direct Labour

Variance

(£6,100F) and (£52,500A) = £46,400(in our Table in Solution (a) above.

Equals

Direct Labour Rate Variance

=£6,100 F

Direct Labour Efficiency Variance

= £52,500 A

The significant parts produced by the two fundamental keep splitting variations (£6,100F

and £52, 500A) address the query "Who really should be made responsibility for the negative

total immediate labour numerous changes of £46,400?"

The present and permitted working-hour expenses are determined by the direct labour

price variation.

The comparable difference in job growth contrasts the quantity of time that should have

been allowed for the overall grade to the quantity of time actually utilized. The discrepancy is

subsequently paid at the hourly rate that was decided on.

As a consequence, in the instance of Jayrod Plc, there appears to be a £52, 500 A

unfavourable labour efficiency disparities (Holzer and Schoenfeld, 2019).

Even though less time was spent than have been needed, the actual quantity of products

was decreased. If companies could've have functioned more swiftly, they could've have invested

more money.

When it comes to labour efficiency fluctuation, the output facility management is

responsible for the amount of hours it takes to produce a certain amount of goods.

Answer to (c)

Periodic costing is a cost-cutting technology that enables significantly more effective

advertising administration by examining deviations from genuine costs or actively planning. Its

purpose is to continuing to provide a means for creating strategic objectives and offering

evaluation, and also essential decision-making factors and a technique for addressing the

quantity of assets available for sale.

The normal price provides for the following:

Regulate: This might be computed, and any inconsistencies in the findings and spending

may be investigated.

Productivity measurement: Any differences between the baseline and true cost can be

utilized to evaluate the efficacy of expenditure section senior executives.

Variants: Conventional expenditures are utilised to create socioeconomic component

records, but they're also required for monitoring and assessing variations that provide

management with 'input' on how far the company can go (Jermias, Gani and Juliana,

2018).

To value stock: To evaluate goods, costing accountancy that utilizes a stock price

technique, is an alternative to LIFO and FIFO.

Accountancy generalisation: It appears that the norm is the only cost (Kuurila, 2016).

The value and significance of variability analysis: The importance of variability analysis

and why it is necessary: Since management desires fewer variations from expected spending,

variation evaluation promotes good strategies. This leads to more accurate and forward-thinking

legislative changes (Mazarak and Fomina, 2016).

If labour efficiency variation is judged damaging, or gross resource cost variation in

acquisitions is considered bad, management could increase monitoring of these sections in an

effort to boost efficiency.

Variance analysis's drawbacks- Monetary results are being utilized to analyse variation

once a huge fraction has been accomplished. There may be an information gathering error that

would have an impact on the required remedial action. Moreover, because not all abnormalities

were appropriate for data gathering, effective variance assessment would have been hampered

(Roberts and Gnan, 2017).

quantity of assets available for sale.

The normal price provides for the following:

Regulate: This might be computed, and any inconsistencies in the findings and spending

may be investigated.

Productivity measurement: Any differences between the baseline and true cost can be

utilized to evaluate the efficacy of expenditure section senior executives.

Variants: Conventional expenditures are utilised to create socioeconomic component

records, but they're also required for monitoring and assessing variations that provide

management with 'input' on how far the company can go (Jermias, Gani and Juliana,

2018).

To value stock: To evaluate goods, costing accountancy that utilizes a stock price

technique, is an alternative to LIFO and FIFO.

Accountancy generalisation: It appears that the norm is the only cost (Kuurila, 2016).

The value and significance of variability analysis: The importance of variability analysis

and why it is necessary: Since management desires fewer variations from expected spending,

variation evaluation promotes good strategies. This leads to more accurate and forward-thinking

legislative changes (Mazarak and Fomina, 2016).

If labour efficiency variation is judged damaging, or gross resource cost variation in

acquisitions is considered bad, management could increase monitoring of these sections in an

effort to boost efficiency.

Variance analysis's drawbacks- Monetary results are being utilized to analyse variation

once a huge fraction has been accomplished. There may be an information gathering error that

would have an impact on the required remedial action. Moreover, because not all abnormalities

were appropriate for data gathering, effective variance assessment would have been hampered

(Roberts and Gnan, 2017).

REFERENCES

Books and journals

Borthick, A. F. and Pennington, R. R., 2017. When data become ubiquitous, what becomes of

accounting and assurance?. Journal of Information Systems. 31(3). pp.1-4.

Bühler, A., Wallenburg, C. M. and Wieland, A., 2016. Accounting for external turbulence of

logistics organizations via performance measurement systems. Supply Chain

Management: An International Journal.

Chung, S. H. and Chen, K. C., 2016, July. The Relationships among Personality, Management

Accounting Information Systems, and Customer Relationship Quality. In 2016 5th IIAI

International Congress on Advanced Applied Informatics (IIAI-AAI) (pp. 759-763).

IEEE.

Daferighe, E. E., 2019. The Evolving Dimensions Of The Accounting Profession And The 21st

Century Expectations. Archives of Business Research. 7(5). pp.226-232.

Ejiogu, A. R. and Ejiogu, C., 2018. Translation in the “contact zone” between accounting and

human resource management. Accounting, Auditing & Accountability Journal.

Ghanem, N. and Sulaiman, S., 2016. Management accounting system, information quality and

organizational performance: evidence from Libya. Asia-Pacific Management

Accounting Journal (APMAJ). 11(2). pp.1-23.

Giacomini, D., Sicilia, M. and Steccolini, I., 2016. Contextualizing politicians’ uses of

accounting information: reassurance and ammunition. Public Money & Management.

36(7). pp.483-490.

Holzer, H. P. and Schoenfeld, H. M. eds., 2019. Managerial accounting and analysis in

multinational enterprises. Walter de Gruyter GmbH & Co KG.

Jermias, J., Gani, L. and Juliana, C., 2018. Performance Implications of Misalignment Among

Business Strategy, Leadership Style, Organizational Culture and Management

Accounting Systems. Leadership Style, Organizational Culture and Management

Accounting Systems (January 9, 2018).

Kuurila, J., 2016. The role of big data in Finnish companies and the implications of big data on

management accounting.

Mazarak, A. and Fomina, O., 2016. Tools for management accounting. Economic Annals-XXI.

159(5-6). pp.48-51.

Roberts, H. and Gnan, L., 2017. Welcoming family business into the accounting family: an

introduction to the special issue. Qualitative Research in Accounting & Management.

Books and journals

Borthick, A. F. and Pennington, R. R., 2017. When data become ubiquitous, what becomes of

accounting and assurance?. Journal of Information Systems. 31(3). pp.1-4.

Bühler, A., Wallenburg, C. M. and Wieland, A., 2016. Accounting for external turbulence of

logistics organizations via performance measurement systems. Supply Chain

Management: An International Journal.

Chung, S. H. and Chen, K. C., 2016, July. The Relationships among Personality, Management

Accounting Information Systems, and Customer Relationship Quality. In 2016 5th IIAI

International Congress on Advanced Applied Informatics (IIAI-AAI) (pp. 759-763).

IEEE.

Daferighe, E. E., 2019. The Evolving Dimensions Of The Accounting Profession And The 21st

Century Expectations. Archives of Business Research. 7(5). pp.226-232.

Ejiogu, A. R. and Ejiogu, C., 2018. Translation in the “contact zone” between accounting and

human resource management. Accounting, Auditing & Accountability Journal.

Ghanem, N. and Sulaiman, S., 2016. Management accounting system, information quality and

organizational performance: evidence from Libya. Asia-Pacific Management

Accounting Journal (APMAJ). 11(2). pp.1-23.

Giacomini, D., Sicilia, M. and Steccolini, I., 2016. Contextualizing politicians’ uses of

accounting information: reassurance and ammunition. Public Money & Management.

36(7). pp.483-490.

Holzer, H. P. and Schoenfeld, H. M. eds., 2019. Managerial accounting and analysis in

multinational enterprises. Walter de Gruyter GmbH & Co KG.

Jermias, J., Gani, L. and Juliana, C., 2018. Performance Implications of Misalignment Among

Business Strategy, Leadership Style, Organizational Culture and Management

Accounting Systems. Leadership Style, Organizational Culture and Management

Accounting Systems (January 9, 2018).

Kuurila, J., 2016. The role of big data in Finnish companies and the implications of big data on

management accounting.

Mazarak, A. and Fomina, O., 2016. Tools for management accounting. Economic Annals-XXI.

159(5-6). pp.48-51.

Roberts, H. and Gnan, L., 2017. Welcoming family business into the accounting family: an

introduction to the special issue. Qualitative Research in Accounting & Management.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.