Management Accounting for Planning and Control Case Studies Analysis

VerifiedAdded on 2023/06/18

|13

|2906

|480

Case Study

AI Summary

This document presents solutions to several management accounting case studies, covering topics such as ethical considerations in sales management, investment decisions using ROI, cost-volume-profit (CVP) analysis, and the importance of budgeting and strategic planning. The case studies address issues like laying off expensive salespeople, ethical dilemmas in investment decisions, calculating breakeven points and margin of safety, and creating sales budgets. The solutions provide detailed calculations, explanations, and recommendations, emphasizing the importance of ethical behavior and strategic financial management in achieving organizational goals. This resource is designed to assist students in understanding and applying management accounting principles to real-world scenarios.

Management Accounting for

Planning and Control

Planning and Control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

CASE STUDY 1..............................................................................................................................3

PART A...........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

PART B...........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................4

4...................................................................................................................................................4

CASE STUDY 2..............................................................................................................................4

1)..................................................................................................................................................4

2)..................................................................................................................................................4

3)..................................................................................................................................................5

CASE STUDY 3..............................................................................................................................6

1...................................................................................................................................................6

2. Calculating breakeven point....................................................................................................6

3. Calculating margin of safety in both units and sales dollar.....................................................7

4...................................................................................................................................................7

5...................................................................................................................................................8

6. Explaining the limitation of CVP analysis and reason for its usage........................................8

CASE STUDY 4..............................................................................................................................9

1. Importance of budgeting..........................................................................................................9

2. Importance of strategic plan for DW99...................................................................................9

3. Sales Budget..........................................................................................................................10

4. Budgeting, Planning and control, setting up of strategic goal in improvement in business

performance...............................................................................................................................11

REFERENCES................................................................................................................................1

CASE STUDY 1..............................................................................................................................3

PART A...........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

PART B...........................................................................................................................................3

1...................................................................................................................................................3

2...................................................................................................................................................3

3...................................................................................................................................................4

4...................................................................................................................................................4

CASE STUDY 2..............................................................................................................................4

1)..................................................................................................................................................4

2)..................................................................................................................................................4

3)..................................................................................................................................................5

CASE STUDY 3..............................................................................................................................6

1...................................................................................................................................................6

2. Calculating breakeven point....................................................................................................6

3. Calculating margin of safety in both units and sales dollar.....................................................7

4...................................................................................................................................................7

5...................................................................................................................................................8

6. Explaining the limitation of CVP analysis and reason for its usage........................................8

CASE STUDY 4..............................................................................................................................9

1. Importance of budgeting..........................................................................................................9

2. Importance of strategic plan for DW99...................................................................................9

3. Sales Budget..........................................................................................................................10

4. Budgeting, Planning and control, setting up of strategic goal in improvement in business

performance...............................................................................................................................11

REFERENCES................................................................................................................................1

CASE STUDY 1

PART A

1.

The right choice for the manager to make is to not lay off its most expensive salespeople.

The reason pertaining to the fact is that these are the people who bring sales to the company. Just

to earn the bonus of $10000 the manager cannot lay off these sales person from the company. the

manager was thinking to use these sales person in fourth quarter as it provides maximum orders

and hire new people at beginning of next year which is not a correct practice.

2.

The ethical dilemma aroused with the choice that whether the company need to lay off its

most expensive sales people or not. This is pertaining to the reason that laying off the expensive

sales person is not a good option and as a result of this business operations and goodwill will be

affected (Endenich & Trapp, 2020). With respect to accounting there is a way to redesign the

accounting reporting system to discourage this type of behaviour of manager. For this the

company can undertake the use of proper bonus system in order to ensure that there are proper

sales and on that a percentage of bonus will be provided. Hence, this bonus will assist the

company in improving the sales as well as employees will try to sell more and more for earning

large amount of profit.

PART B

1.

Yes, it is true that ethical working plays a great role at time of learning and working in

corporate world. the reason pertaining to the fact is that in case students are not taught ethics at

initial level only then this will not provide a good learning (Othman & Hamid, 2018). this is

particularly because of the fact that ethical working is necessary so that person chooses right

course of action to do work.

2.

This simply means that business need to sacrifice their self- interest for the collective

good in order to work in direction of society’s development (Weetman, 2019). This is necessary

PART A

1.

The right choice for the manager to make is to not lay off its most expensive salespeople.

The reason pertaining to the fact is that these are the people who bring sales to the company. Just

to earn the bonus of $10000 the manager cannot lay off these sales person from the company. the

manager was thinking to use these sales person in fourth quarter as it provides maximum orders

and hire new people at beginning of next year which is not a correct practice.

2.

The ethical dilemma aroused with the choice that whether the company need to lay off its

most expensive sales people or not. This is pertaining to the reason that laying off the expensive

sales person is not a good option and as a result of this business operations and goodwill will be

affected (Endenich & Trapp, 2020). With respect to accounting there is a way to redesign the

accounting reporting system to discourage this type of behaviour of manager. For this the

company can undertake the use of proper bonus system in order to ensure that there are proper

sales and on that a percentage of bonus will be provided. Hence, this bonus will assist the

company in improving the sales as well as employees will try to sell more and more for earning

large amount of profit.

PART B

1.

Yes, it is true that ethical working plays a great role at time of learning and working in

corporate world. the reason pertaining to the fact is that in case students are not taught ethics at

initial level only then this will not provide a good learning (Othman & Hamid, 2018). this is

particularly because of the fact that ethical working is necessary so that person chooses right

course of action to do work.

2.

This simply means that business need to sacrifice their self- interest for the collective

good in order to work in direction of society’s development (Weetman, 2019). This is necessary

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

because when the companies will sacrifice their self-interest for the development of Australia

and its people then it will improve country’s development.

3.

This is true that the monetary benefits and titles are the by- products for doing a good job.

The reason underlying this fact is that when the employees and resources will be provided with

some monetary benefits then it will motivate the employees to work in ethical and correct

manner and in direction of good of society (Bafghi, 2021). This is necessary because when the

people will be managed in proper and good manner then they will work in required manner then

overall performance of company will increase.

4.

This is also true that when the companies prefer to have unethical behaviour and practices

then at first they get more benefits like high rollers in casino. But eventually after some time they

are wiped off financially (Charifzadeh & Taschner, 2017). This simply means that when the

person is working in wrong manner then at first they will earn profit but after some time this will

result in loss for the company.

CASE STUDY 2

1)

ROI based on initial investment:

Operating income: 1870000

Total cost: 15600000

ROI: Operating income / average total investment * 100

= 1870000 / 15600000 * 100

= 11.99%

ROI based on Mel's estimate:

2340000 / 15600000 * 100

= 15%

2)

Jason is surely facing an ethical dilemma in context to make the investment decision for

investing in the project. The lower estimate revenue or return could certainly allow the

and its people then it will improve country’s development.

3.

This is true that the monetary benefits and titles are the by- products for doing a good job.

The reason underlying this fact is that when the employees and resources will be provided with

some monetary benefits then it will motivate the employees to work in ethical and correct

manner and in direction of good of society (Bafghi, 2021). This is necessary because when the

people will be managed in proper and good manner then they will work in required manner then

overall performance of company will increase.

4.

This is also true that when the companies prefer to have unethical behaviour and practices

then at first they get more benefits like high rollers in casino. But eventually after some time they

are wiped off financially (Charifzadeh & Taschner, 2017). This simply means that when the

person is working in wrong manner then at first they will earn profit but after some time this will

result in loss for the company.

CASE STUDY 2

1)

ROI based on initial investment:

Operating income: 1870000

Total cost: 15600000

ROI: Operating income / average total investment * 100

= 1870000 / 15600000 * 100

= 11.99%

ROI based on Mel's estimate:

2340000 / 15600000 * 100

= 15%

2)

Jason is surely facing an ethical dilemma in context to make the investment decision for

investing in the project. The lower estimate revenue or return could certainly allow the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stakeholder to face lower return than the expected value. In case the return are estimated to be

the maximum possible or in the best possible situation than the investment look more feasible

and profitable to invest. Every investment contains the best capacity as well the worst capacity.

In the present situation the best capacity of the project would allow the investor to generate the

return that is expected by the respective party (King and Van Den Bergh, 2018). Investment must

always be monitored with the use of the best possible situation as this will only motivate the

stakeholder to invest in the operation. This is ethically justifiable to evaluate the investment

decision-making with support of the best possible estimate in term of return on investment in the

project. This will only allow the stakeholder to work positively over the decided investment

proposal. This is not unethical to select the higher return as this cannot be predicted that how low

the return can go. Many times return are entertain more than the best possible situation of the

investment. Hence this is completely ethical to evaluate the proposal with use of the maximum

estimated return on investment in the project.

3)

Jason should surely take the investment decision. This will allow the stakeholder to

identify the best possible situation in context to the investment made. This would surely allow

the stakeholder to understand the need of the investment option and make a positivize decision

towards investment in the project. This is not ethical to take the bets possible situation when it

comes to evaluate about the investment decision-making. The required rate of return on

investment is also 15% and also the investment is capable enough to generate the estimated

return on investment made. On the basis of the best possible situation the investment look

feasible. Also this is only estimated figures or value which clearly demonstrate that the investor

might generate more than the expected value in against to the investment is made (Masters and

et.al., 2017). This is completely looked feasible to invest in the respective project. 15% is a good

return that investor can expect from any investment and this is also fulfilling the expectations of

the investor in against to invest in the project. Hence, choosing the investment option will be a

right decision for the investor. Also this is only a estimation that indicate that the return might go

beyond this value which will further improve the profitability and feasibility of the investment

decision that will be made by the stakeholder.

the maximum possible or in the best possible situation than the investment look more feasible

and profitable to invest. Every investment contains the best capacity as well the worst capacity.

In the present situation the best capacity of the project would allow the investor to generate the

return that is expected by the respective party (King and Van Den Bergh, 2018). Investment must

always be monitored with the use of the best possible situation as this will only motivate the

stakeholder to invest in the operation. This is ethically justifiable to evaluate the investment

decision-making with support of the best possible estimate in term of return on investment in the

project. This will only allow the stakeholder to work positively over the decided investment

proposal. This is not unethical to select the higher return as this cannot be predicted that how low

the return can go. Many times return are entertain more than the best possible situation of the

investment. Hence this is completely ethical to evaluate the proposal with use of the maximum

estimated return on investment in the project.

3)

Jason should surely take the investment decision. This will allow the stakeholder to

identify the best possible situation in context to the investment made. This would surely allow

the stakeholder to understand the need of the investment option and make a positivize decision

towards investment in the project. This is not ethical to take the bets possible situation when it

comes to evaluate about the investment decision-making. The required rate of return on

investment is also 15% and also the investment is capable enough to generate the estimated

return on investment made. On the basis of the best possible situation the investment look

feasible. Also this is only estimated figures or value which clearly demonstrate that the investor

might generate more than the expected value in against to the investment is made (Masters and

et.al., 2017). This is completely looked feasible to invest in the respective project. 15% is a good

return that investor can expect from any investment and this is also fulfilling the expectations of

the investor in against to invest in the project. Hence, choosing the investment option will be a

right decision for the investor. Also this is only a estimation that indicate that the return might go

beyond this value which will further improve the profitability and feasibility of the investment

decision that will be made by the stakeholder.

CASE STUDY 3

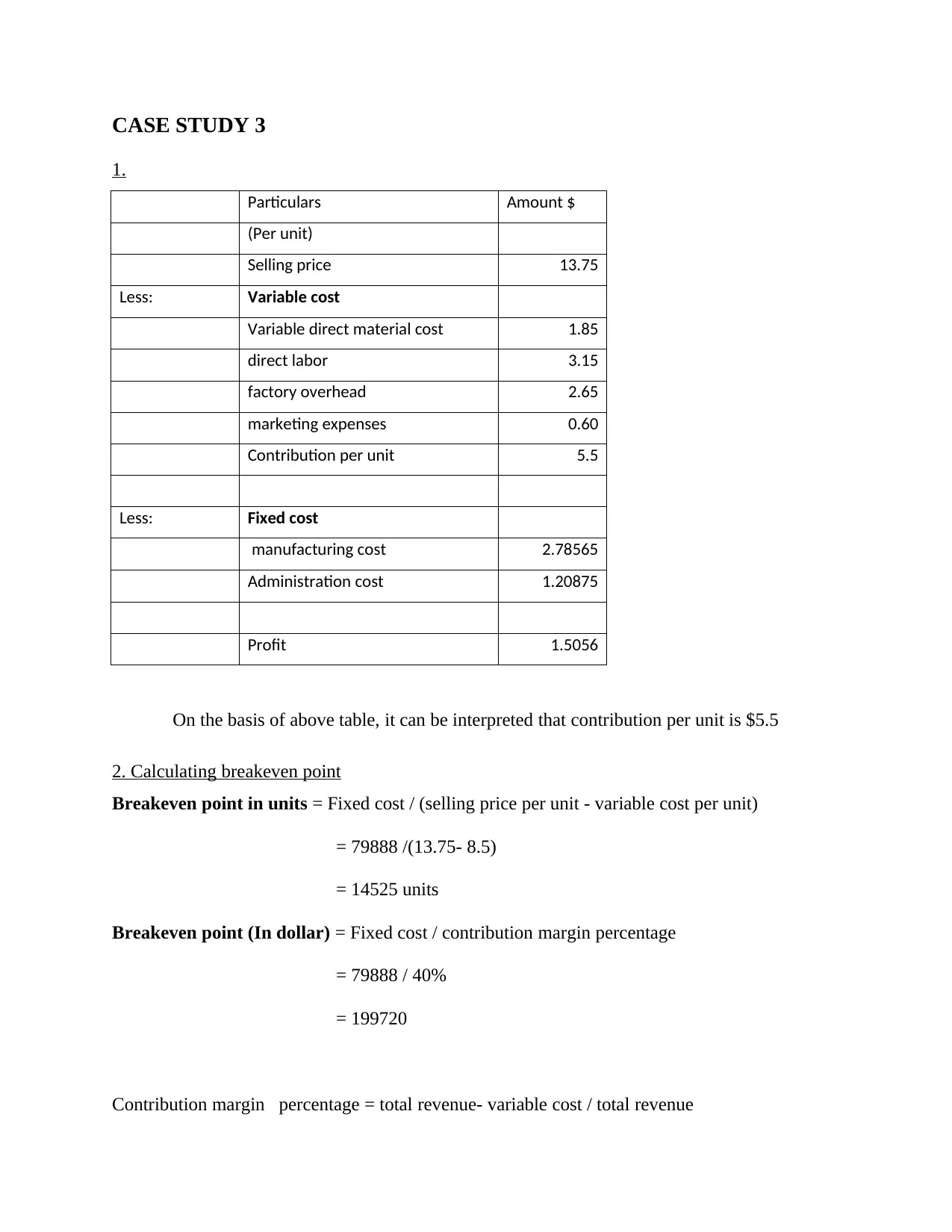

1.

Particulars Amount $

(Per unit)

Selling price 13.75

Less: Variable cost

Variable direct material cost 1.85

direct labor 3.15

factory overhead 2.65

marketing expenses 0.60

Contribution per unit 5.5

Less: Fixed cost

manufacturing cost 2.78565

Administration cost 1.20875

Profit 1.5056

On the basis of above table, it can be interpreted that contribution per unit is $5.5

2. Calculating breakeven point

Breakeven point in units = Fixed cost / (selling price per unit - variable cost per unit)

= 79888 /(13.75- 8.5)

= 14525 units

Breakeven point (In dollar) = Fixed cost / contribution margin percentage

= 79888 / 40%

= 199720

Contribution margin percentage = total revenue- variable cost / total revenue

1.

Particulars Amount $

(Per unit)

Selling price 13.75

Less: Variable cost

Variable direct material cost 1.85

direct labor 3.15

factory overhead 2.65

marketing expenses 0.60

Contribution per unit 5.5

Less: Fixed cost

manufacturing cost 2.78565

Administration cost 1.20875

Profit 1.5056

On the basis of above table, it can be interpreted that contribution per unit is $5.5

2. Calculating breakeven point

Breakeven point in units = Fixed cost / (selling price per unit - variable cost per unit)

= 79888 /(13.75- 8.5)

= 14525 units

Breakeven point (In dollar) = Fixed cost / contribution margin percentage

= 79888 / 40%

= 199720

Contribution margin percentage = total revenue- variable cost / total revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

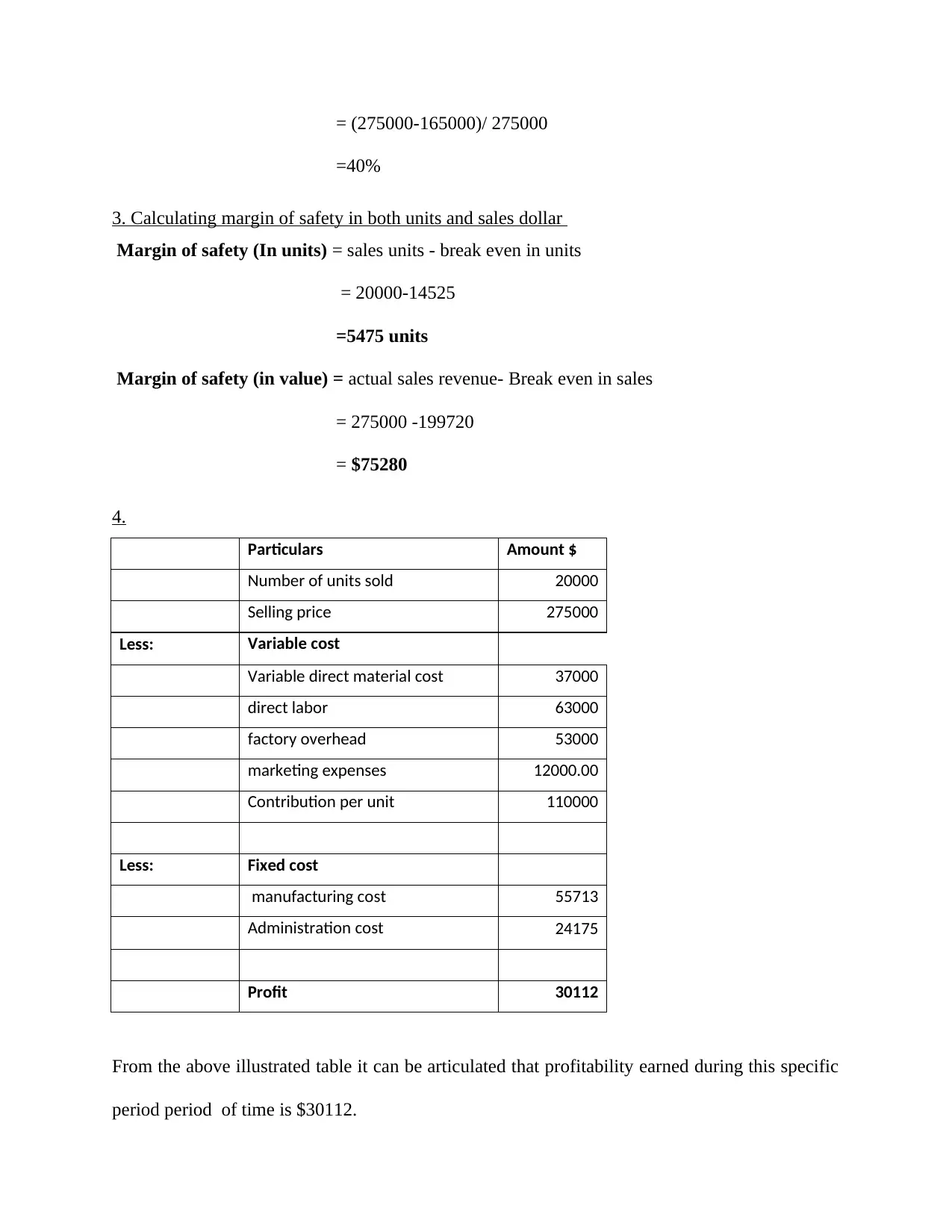

= (275000-165000)/ 275000

=40%

3. Calculating margin of safety in both units and sales dollar

Margin of safety (In units) = sales units - break even in units

= 20000-14525

=5475 units

Margin of safety (in value) = actual sales revenue- Break even in sales

= 275000 -199720

= $75280

4.

Particulars Amount $

Number of units sold 20000

Selling price 275000

Less: Variable cost

Variable direct material cost 37000

direct labor 63000

factory overhead 53000

marketing expenses 12000.00

Contribution per unit 110000

Less: Fixed cost

manufacturing cost 55713

Administration cost 24175

Profit 30112

From the above illustrated table it can be articulated that profitability earned during this specific

period period of time is $30112.

=40%

3. Calculating margin of safety in both units and sales dollar

Margin of safety (In units) = sales units - break even in units

= 20000-14525

=5475 units

Margin of safety (in value) = actual sales revenue- Break even in sales

= 275000 -199720

= $75280

4.

Particulars Amount $

Number of units sold 20000

Selling price 275000

Less: Variable cost

Variable direct material cost 37000

direct labor 63000

factory overhead 53000

marketing expenses 12000.00

Contribution per unit 110000

Less: Fixed cost

manufacturing cost 55713

Administration cost 24175

Profit 30112

From the above illustrated table it can be articulated that profitability earned during this specific

period period of time is $30112.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5.

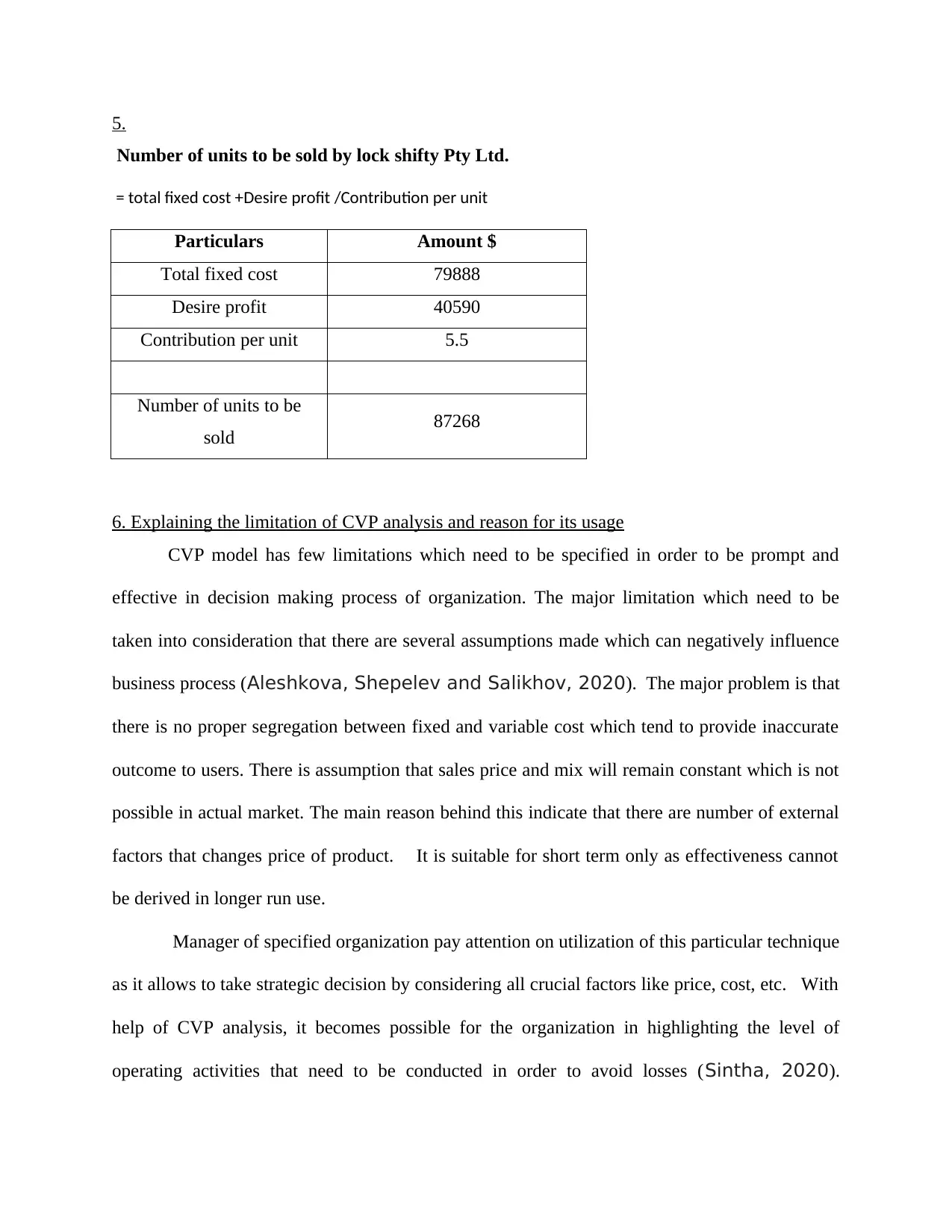

Number of units to be sold by lock shifty Pty Ltd.

= total fixed cost +Desire profit /Contribution per unit

Particulars Amount $

Total fixed cost 79888

Desire profit 40590

Contribution per unit 5.5

Number of units to be

sold 87268

6. Explaining the limitation of CVP analysis and reason for its usage

CVP model has few limitations which need to be specified in order to be prompt and

effective in decision making process of organization. The major limitation which need to be

taken into consideration that there are several assumptions made which can negatively influence

business process (Aleshkova, Shepelev and Salikhov, 2020). The major problem is that

there is no proper segregation between fixed and variable cost which tend to provide inaccurate

outcome to users. There is assumption that sales price and mix will remain constant which is not

possible in actual market. The main reason behind this indicate that there are number of external

factors that changes price of product. It is suitable for short term only as effectiveness cannot

be derived in longer run use.

Manager of specified organization pay attention on utilization of this particular technique

as it allows to take strategic decision by considering all crucial factors like price, cost, etc. With

help of CVP analysis, it becomes possible for the organization in highlighting the level of

operating activities that need to be conducted in order to avoid losses (Sintha, 2020).

Number of units to be sold by lock shifty Pty Ltd.

= total fixed cost +Desire profit /Contribution per unit

Particulars Amount $

Total fixed cost 79888

Desire profit 40590

Contribution per unit 5.5

Number of units to be

sold 87268

6. Explaining the limitation of CVP analysis and reason for its usage

CVP model has few limitations which need to be specified in order to be prompt and

effective in decision making process of organization. The major limitation which need to be

taken into consideration that there are several assumptions made which can negatively influence

business process (Aleshkova, Shepelev and Salikhov, 2020). The major problem is that

there is no proper segregation between fixed and variable cost which tend to provide inaccurate

outcome to users. There is assumption that sales price and mix will remain constant which is not

possible in actual market. The main reason behind this indicate that there are number of external

factors that changes price of product. It is suitable for short term only as effectiveness cannot

be derived in longer run use.

Manager of specified organization pay attention on utilization of this particular technique

as it allows to take strategic decision by considering all crucial factors like price, cost, etc. With

help of CVP analysis, it becomes possible for the organization in highlighting the level of

operating activities that need to be conducted in order to avoid losses (Sintha, 2020).

Planning & forecasting future activities can be done effectively by utilizing CVP technique in

business activities.

CASE STUDY 4

1. Importance of budgeting

Budgeting is highly essential for DW99 because with the help of budgeting, the standards

in terms of cost and expenses along with expected revenue would be determined. Likewise,

budgeting would assist the DW99 to peruse its activities in the direction of the set budget. Also

with the help of budgeting DW99 would ensure that adequate funds will always be available for

the company with respect to spending. Budgeting will also lead the DW99 to be in the situation

of out of debt so that operation of the company would be performed in the desired manner.

Budgeting would also ensure that a comparison of its actual expenses against the budgeted one

so that corrective action in terms of reduction of expenses and raising of efficiency towards the

generation of revenue would be taken (Batt, Rikhardsson and Karlsson, 2021).

2. Importance of strategic plan for DW99

Planning would lead to have a determination of various steps and ways that could assist

the organization to attain its objectives. Likewise, with the aspect of controlling the current

performance of the company would be measured against the standard so that deviation would be

determined and corrective action can be taken. In case of DW99 the strategic plan would assist

the company to track its progress along with the assisting the direction towards the goal.

Likewise, this plan would also assist the DW99 to make improvisation in its performance so that

the goal of making establishment in Australia would get accomplished. This plan would also

assist the organization to attain growth (Soni, 2020). With the help of strategic plan, the

controlling over the future in terms of controlling of expense would be possible.

business activities.

CASE STUDY 4

1. Importance of budgeting

Budgeting is highly essential for DW99 because with the help of budgeting, the standards

in terms of cost and expenses along with expected revenue would be determined. Likewise,

budgeting would assist the DW99 to peruse its activities in the direction of the set budget. Also

with the help of budgeting DW99 would ensure that adequate funds will always be available for

the company with respect to spending. Budgeting will also lead the DW99 to be in the situation

of out of debt so that operation of the company would be performed in the desired manner.

Budgeting would also ensure that a comparison of its actual expenses against the budgeted one

so that corrective action in terms of reduction of expenses and raising of efficiency towards the

generation of revenue would be taken (Batt, Rikhardsson and Karlsson, 2021).

2. Importance of strategic plan for DW99

Planning would lead to have a determination of various steps and ways that could assist

the organization to attain its objectives. Likewise, with the aspect of controlling the current

performance of the company would be measured against the standard so that deviation would be

determined and corrective action can be taken. In case of DW99 the strategic plan would assist

the company to track its progress along with the assisting the direction towards the goal.

Likewise, this plan would also assist the DW99 to make improvisation in its performance so that

the goal of making establishment in Australia would get accomplished. This plan would also

assist the organization to attain growth (Soni, 2020). With the help of strategic plan, the

controlling over the future in terms of controlling of expense would be possible.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

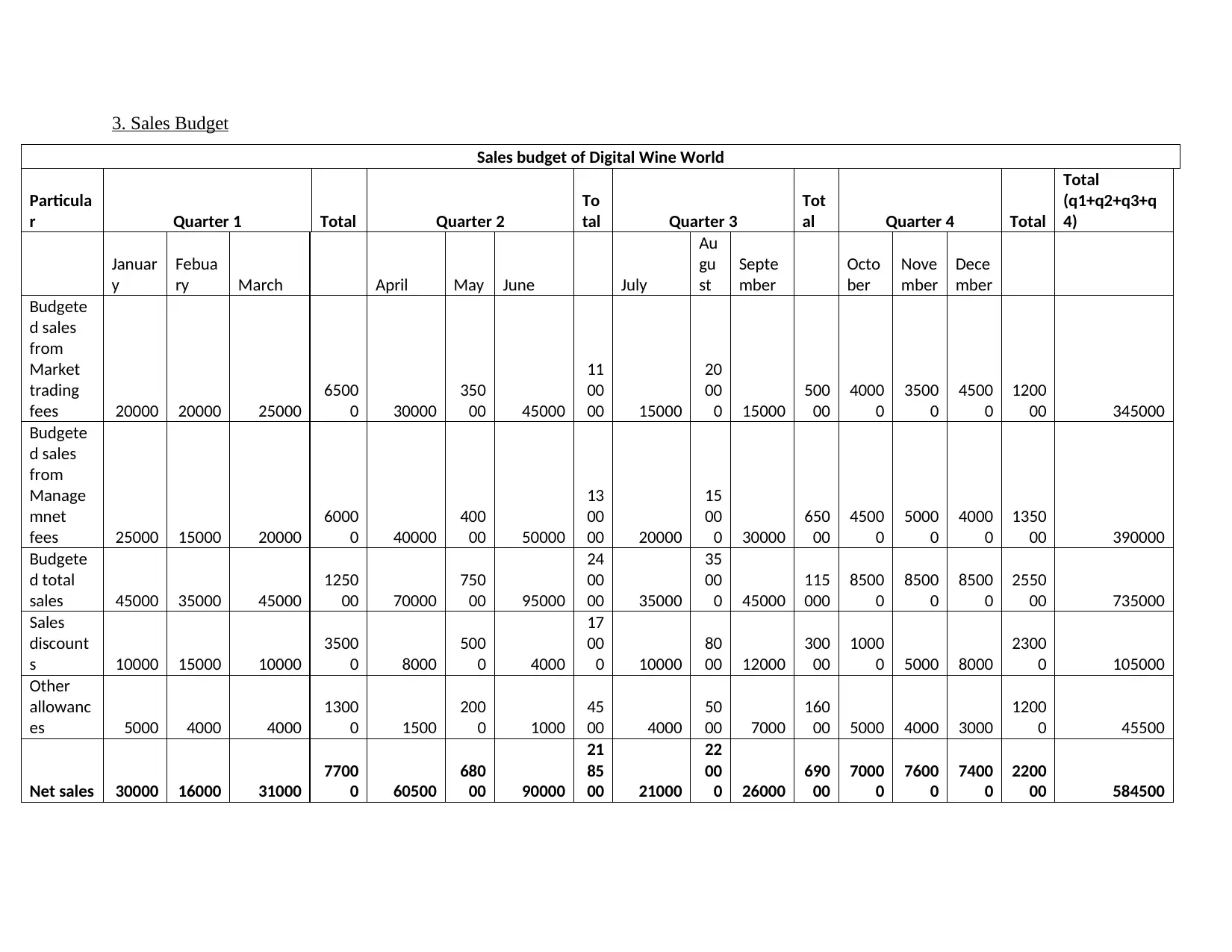

3. Sales Budget

Sales budget of Digital Wine World

Particula

r Quarter 1 Total Quarter 2

To

tal Quarter 3

Tot

al Quarter 4 Total

Total

(q1+q2+q3+q

4)

Januar

y

Febua

ry March April May June July

Au

gu

st

Septe

mber

Octo

ber

Nove

mber

Dece

mber

Budgete

d sales

from

Market

trading

fees 20000 20000 25000

6500

0 30000

350

00 45000

11

00

00 15000

20

00

0 15000

500

00

4000

0

3500

0

4500

0

1200

00 345000

Budgete

d sales

from

Manage

mnet

fees 25000 15000 20000

6000

0 40000

400

00 50000

13

00

00 20000

15

00

0 30000

650

00

4500

0

5000

0

4000

0

1350

00 390000

Budgete

d total

sales 45000 35000 45000

1250

00 70000

750

00 95000

24

00

00 35000

35

00

0 45000

115

000

8500

0

8500

0

8500

0

2550

00 735000

Sales

discount

s 10000 15000 10000

3500

0 8000

500

0 4000

17

00

0 10000

80

00 12000

300

00

1000

0 5000 8000

2300

0 105000

Other

allowanc

es 5000 4000 4000

1300

0 1500

200

0 1000

45

00 4000

50

00 7000

160

00 5000 4000 3000

1200

0 45500

Net sales 30000 16000 31000

7700

0 60500

680

00 90000

21

85

00 21000

22

00

0 26000

690

00

7000

0

7600

0

7400

0

2200

00 584500

Sales budget of Digital Wine World

Particula

r Quarter 1 Total Quarter 2

To

tal Quarter 3

Tot

al Quarter 4 Total

Total

(q1+q2+q3+q

4)

Januar

y

Febua

ry March April May June July

Au

gu

st

Septe

mber

Octo

ber

Nove

mber

Dece

mber

Budgete

d sales

from

Market

trading

fees 20000 20000 25000

6500

0 30000

350

00 45000

11

00

00 15000

20

00

0 15000

500

00

4000

0

3500

0

4500

0

1200

00 345000

Budgete

d sales

from

Manage

mnet

fees 25000 15000 20000

6000

0 40000

400

00 50000

13

00

00 20000

15

00

0 30000

650

00

4500

0

5000

0

4000

0

1350

00 390000

Budgete

d total

sales 45000 35000 45000

1250

00 70000

750

00 95000

24

00

00 35000

35

00

0 45000

115

000

8500

0

8500

0

8500

0

2550

00 735000

Sales

discount

s 10000 15000 10000

3500

0 8000

500

0 4000

17

00

0 10000

80

00 12000

300

00

1000

0 5000 8000

2300

0 105000

Other

allowanc

es 5000 4000 4000

1300

0 1500

200

0 1000

45

00 4000

50

00 7000

160

00 5000 4000 3000

1200

0 45500

Net sales 30000 16000 31000

7700

0 60500

680

00 90000

21

85

00 21000

22

00

0 26000

690

00

7000

0

7600

0

7400

0

2200

00 584500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Budgeting, Planning and control, setting up of strategic goal in improvement in business

performance

The concept of budgeting, planning and controlling would assist the DW99 to make

improvisation in its performance in terms of attainment of the goal along with taking of

improved and corrective steps that could lead to have improvisation in the existing performance.

Likewise, setting up of strategic goal would assist the company to take initiative in the direction

of goal which would automatically lead to performance improvisation. It can also be

Recommendation:

In order to make improvisation in sales it is recommended to DW99 to plan for reduction

of sales discounts.

It will also be recommended to the company that it must control over other allowances.

A focus over the raising of marketing revenue would also be recommended to DW99 so

that the sales will raise.

In order to raise sales, setting up of strategic goals to raise the marketing revenue would

be highly recommended.

performance

The concept of budgeting, planning and controlling would assist the DW99 to make

improvisation in its performance in terms of attainment of the goal along with taking of

improved and corrective steps that could lead to have improvisation in the existing performance.

Likewise, setting up of strategic goal would assist the company to take initiative in the direction

of goal which would automatically lead to performance improvisation. It can also be

Recommendation:

In order to make improvisation in sales it is recommended to DW99 to plan for reduction

of sales discounts.

It will also be recommended to the company that it must control over other allowances.

A focus over the raising of marketing revenue would also be recommended to DW99 so

that the sales will raise.

In order to raise sales, setting up of strategic goals to raise the marketing revenue would

be highly recommended.

REFERENCES

Books and journals

Aleshkova, D. V., Shepelev, A. V., & Salikhov, K. M., 2020. Innovative

Methods of Managing the Company’s Financial Results. In International

Scientific and Practical Conference (pp. 649-658). Springer, Cham.

Bafghi, A. A. T. (2021). Professional Ethics and Behavior in Accounting. International Journal

of Multicultural and Multireligious Understanding. 8(1). 545-555.

Batt, C., Rikhardsson, P. and Karlsson, T., 2021. Exploring the Impact of Organizational Context

on Budgeting. Corporate Ownership and Control. 18(4). pp.134-151.

Charifzadeh, M., & Taschner, A. (2017). Management accounting and control: tools and

concepts in a Central European context. John Wiley & Sons.

Endenich, C., & Trapp, R. (2020). Ethical implications of management accounting and control:

A systematic review of the contributions from the Journal of Business Ethics. Journal of

business ethics. 163(2). 309-328.

King, L. C., & Van Den Bergh, J. C. (2018). Implications of net energy-return-on-investment for

a low-carbon energy transition. Nature Energy. 3(4). 334-340.

Masters, R. & et.al., (2017). Return on investment of public health interventions: a systematic

review. J Epidemiol Community Health. 71(8). 827-834.

Othman, Z., & Hamid, F. Z. A. (2018). Dealing with un (expected) ethical dilemma: Experience

from the field. The Qualitative Report. 23(4). pp.733-741.

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and

Medium Enterprises. International Journal of Research-Granthaalayah.

8(6).

Soni, V.D., 2020. Importance and Strategic Planning of Team Management. International

Journal of Innovative Research in Technology. 7(2). pp.47-50.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

1

Books and journals

Aleshkova, D. V., Shepelev, A. V., & Salikhov, K. M., 2020. Innovative

Methods of Managing the Company’s Financial Results. In International

Scientific and Practical Conference (pp. 649-658). Springer, Cham.

Bafghi, A. A. T. (2021). Professional Ethics and Behavior in Accounting. International Journal

of Multicultural and Multireligious Understanding. 8(1). 545-555.

Batt, C., Rikhardsson, P. and Karlsson, T., 2021. Exploring the Impact of Organizational Context

on Budgeting. Corporate Ownership and Control. 18(4). pp.134-151.

Charifzadeh, M., & Taschner, A. (2017). Management accounting and control: tools and

concepts in a Central European context. John Wiley & Sons.

Endenich, C., & Trapp, R. (2020). Ethical implications of management accounting and control:

A systematic review of the contributions from the Journal of Business Ethics. Journal of

business ethics. 163(2). 309-328.

King, L. C., & Van Den Bergh, J. C. (2018). Implications of net energy-return-on-investment for

a low-carbon energy transition. Nature Energy. 3(4). 334-340.

Masters, R. & et.al., (2017). Return on investment of public health interventions: a systematic

review. J Epidemiol Community Health. 71(8). 827-834.

Othman, Z., & Hamid, F. Z. A. (2018). Dealing with un (expected) ethical dilemma: Experience

from the field. The Qualitative Report. 23(4). pp.733-741.

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and

Medium Enterprises. International Journal of Research-Granthaalayah.

8(6).

Soni, V.D., 2020. Importance and Strategic Planning of Team Management. International

Journal of Innovative Research in Technology. 7(2). pp.47-50.

Weetman, P., 2019. Financial and management accounting. Pearson UK.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.