Management Accounting Report: Financial Problem Response Analysis

VerifiedAdded on 2020/10/05

|19

|5443

|241

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on The Berkeley Partnership. It begins with an introduction to management accounting systems, detailing their importance in recording data, evaluating weaknesses, and making informed decisions. The report explores various management accounting techniques, including cost accounting systems, inventory management, and job-costing systems. It further examines methods used for management accounting reporting, such as cost accounting reports, budget reports, inventory control reports, and performance reporting. The core of the report delves into the calculation of costs using marginal and absorption costing techniques, providing detailed income statements for each method. Additionally, the report discusses the advantages and disadvantages of different planning tools used for budgetary control, such as cash budgets, operating budgets, and zero-based budgets. Finally, it analyzes how organizations adapt management accounting systems to respond to financial problems, offering practical insights and recommendations. The report concludes with a summary of key findings and references for further study.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

LO1 .................................................................................................................................................3

P1 Management accounting systems......................................................................................3

P2 Methods used for management accounting reporting.......................................................5

M1-.........................................................................................................................................6

D1...........................................................................................................................................6

LO 2.................................................................................................................................................7

P3, M2 and D2. Calculation of costs for preparation of income statement by using the

marginal and absorption costing technique............................................................................7

LO 3.................................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tool used for budgetary

control.....................................................................................................................................9

M3 Application of planning tools ........................................................................................11

LO 4...............................................................................................................................................12

P5, D3 and M4 Organisation are adapting management accounting systems to respond to

financial problems................................................................................................................12

.......................................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

LO1 .................................................................................................................................................3

P1 Management accounting systems......................................................................................3

P2 Methods used for management accounting reporting.......................................................5

M1-.........................................................................................................................................6

D1...........................................................................................................................................6

LO 2.................................................................................................................................................7

P3, M2 and D2. Calculation of costs for preparation of income statement by using the

marginal and absorption costing technique............................................................................7

LO 3.................................................................................................................................................9

P4 Advantages and disadvantages of different types of planning tool used for budgetary

control.....................................................................................................................................9

M3 Application of planning tools ........................................................................................11

LO 4...............................................................................................................................................12

P5, D3 and M4 Organisation are adapting management accounting systems to respond to

financial problems................................................................................................................12

.......................................................................................................................................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is a process of managing the accounts and finance of the

company to maintain the company financial position stable. Accounting is done by the

accounting department team on the internal bases as it is not regulated by law and rules.

Management accounting is very beneficial to the company as they manage the decision making

power of the employees working in the company. By managing the accounts of the company

they can early identify the problems arises in the company and can prepare a proper feedback to

overcome from that problems.

For this project The Berkeley Partnership has been selected which involved in offers

consultancy services to variety of businesses. Report will include a brief understanding of

management accounting systems. It also includes the techniques for management accounting.

Further it describes the various planning tool such as cash budget, operating budget and Zero

based budget to helps in managing accounts. Lastly it includes the various ways that organisation

uses to respond to financial problems in managing accounts.

LO1

P1 Management accounting systems

With the growing organisations and techniques there is a need to maintain the records of

the company and plan the manufacturing process and sales in by the company. Management

accounting system is the system which contains recording of the daily data in the organization

and evaluating the weak points in the company (What is management accounting, 2019). There

is preparation of the statistical data and reports that are used by the company to make the daily

decisions. The management accounting also help in studying the previous data and making

budget accordingly for the next business cycle (Maas, Schaltegger and Crutzen, 2016). The

budgets are made at various level to compare the cost incurred and the cost expected to be

incurred. Management accounting also helps in the process of financial accounting too as the

data and reports made in the management accounting is used to make decisions on the financial

projects and investment for the product. It includes reports on income and expenses, return on

investment and sales analysis reports, improving the performance and reduce the flaws in the

functioning of the Berkeley Partnership. The income and expenses reports are used to balance

the expenses and income through any product. Return on investment reports are necessary to

Management accounting is a process of managing the accounts and finance of the

company to maintain the company financial position stable. Accounting is done by the

accounting department team on the internal bases as it is not regulated by law and rules.

Management accounting is very beneficial to the company as they manage the decision making

power of the employees working in the company. By managing the accounts of the company

they can early identify the problems arises in the company and can prepare a proper feedback to

overcome from that problems.

For this project The Berkeley Partnership has been selected which involved in offers

consultancy services to variety of businesses. Report will include a brief understanding of

management accounting systems. It also includes the techniques for management accounting.

Further it describes the various planning tool such as cash budget, operating budget and Zero

based budget to helps in managing accounts. Lastly it includes the various ways that organisation

uses to respond to financial problems in managing accounts.

LO1

P1 Management accounting systems

With the growing organisations and techniques there is a need to maintain the records of

the company and plan the manufacturing process and sales in by the company. Management

accounting system is the system which contains recording of the daily data in the organization

and evaluating the weak points in the company (What is management accounting, 2019). There

is preparation of the statistical data and reports that are used by the company to make the daily

decisions. The management accounting also help in studying the previous data and making

budget accordingly for the next business cycle (Maas, Schaltegger and Crutzen, 2016). The

budgets are made at various level to compare the cost incurred and the cost expected to be

incurred. Management accounting also helps in the process of financial accounting too as the

data and reports made in the management accounting is used to make decisions on the financial

projects and investment for the product. It includes reports on income and expenses, return on

investment and sales analysis reports, improving the performance and reduce the flaws in the

functioning of the Berkeley Partnership. The income and expenses reports are used to balance

the expenses and income through any product. Return on investment reports are necessary to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

know the income incurred by the investment made by the company. Sales analysis reports shows

the sales over a period, by the company and take decisions on the future production of the

product (Cooper, Ezzamel and Qu, 2017).

There are different types of management accounting system these are as follows-

Cost accounting systems- Cost accounting is the process which is used to estimate the

price of a product in the organisation for the purpose of inventory valuation, controlling

the cost and the profitability of the product so produced. The cost of product is the

expenses incurred on the manufacturing of the product till the product is sold by the

company The Berkeley Partnership. There are two main components of cost accounting

system that are- Job order costing and process costing (Chenhall and Moers, 2015).

Inventory management systems- Inventory is the stock of finished goods in the

organization. This is a system through which the amount of stock is calculated by the

managers for the purpose of further manufacturing, and making budgets accordingly.

Inventory management helps in evaluating the level of goods produced and sold by the

company so that there is no misuse of valuable resources in The Berkeley Partnership.

The inventory is divided in three main categories the are- Raw material stock, work in

progress goods and the finished goods produced by the company. Inventory management

ensures that there is no excess amount of goods lying in the storage and on the other hand

there is no shortage of goods when needed for sale (Granlund and Lukka, 2017).

Job- Costing system- It is a system which involves calculation of cost of the product on

the basis of cost incurred in the production of the product. The cost is then used to

evaluate the price of product to the final customers. It also helps in evaluating the cost

incurred on labour, raw material, and manufacturing expenses by the company The

Berkeley Partnership

Price- optimising system- this is a mathematical process which involves the calculation

of price on the basis of change in demand on the different price levels of a produc .

(Kokubu and Kitada, 2015).The cost and inventory level is used to determine the price

level of the product which is more profitable to the company.

Thus, there are many ways of managing the accounting process in The Berkeley

Partnership. These systems help in the growth and development of the company by evaluating

and focusing on the problem areas of the company (Nielsen, Mitchell and Nørreklit, 2015).

the sales over a period, by the company and take decisions on the future production of the

product (Cooper, Ezzamel and Qu, 2017).

There are different types of management accounting system these are as follows-

Cost accounting systems- Cost accounting is the process which is used to estimate the

price of a product in the organisation for the purpose of inventory valuation, controlling

the cost and the profitability of the product so produced. The cost of product is the

expenses incurred on the manufacturing of the product till the product is sold by the

company The Berkeley Partnership. There are two main components of cost accounting

system that are- Job order costing and process costing (Chenhall and Moers, 2015).

Inventory management systems- Inventory is the stock of finished goods in the

organization. This is a system through which the amount of stock is calculated by the

managers for the purpose of further manufacturing, and making budgets accordingly.

Inventory management helps in evaluating the level of goods produced and sold by the

company so that there is no misuse of valuable resources in The Berkeley Partnership.

The inventory is divided in three main categories the are- Raw material stock, work in

progress goods and the finished goods produced by the company. Inventory management

ensures that there is no excess amount of goods lying in the storage and on the other hand

there is no shortage of goods when needed for sale (Granlund and Lukka, 2017).

Job- Costing system- It is a system which involves calculation of cost of the product on

the basis of cost incurred in the production of the product. The cost is then used to

evaluate the price of product to the final customers. It also helps in evaluating the cost

incurred on labour, raw material, and manufacturing expenses by the company The

Berkeley Partnership

Price- optimising system- this is a mathematical process which involves the calculation

of price on the basis of change in demand on the different price levels of a produc .

(Kokubu and Kitada, 2015).The cost and inventory level is used to determine the price

level of the product which is more profitable to the company.

Thus, there are many ways of managing the accounting process in The Berkeley

Partnership. These systems help in the growth and development of the company by evaluating

and focusing on the problem areas of the company (Nielsen, Mitchell and Nørreklit, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Methods used for management accounting reporting

Management accounting reporting is the systematic analysis of the recorded data by the

operation management and making the final reports and submitting the reports to the decision

makers of The Berkeley Partnership. This includes cost accounting records, the budget reports,

inventory control reports, accounts receivable reports and the performance report.

The cost accounting reports presents the cost and expenses incurred on the product so

manufactured for the purpose of its price determination and profit calculation by the managers in

The Berkeley Partnership. If the cost incurred on the production of the product increase than the

price of the product will also increase accordingly (Wagenhofer, 2016). Also, there are market

factors such as increase in demand there will be rise in price of a product thereby increasing the

profit of the company.

The budget reports are used to compare the current year data with the previous year data

of the financial year. The budget reports can also be made on the comparison of the expected

cost and the actual cost incurred in manufacturing of the product (Hiebl, 2018). The budget

report helps the managers on taking the decisions on the weak points of the manufacturing cost.

It helps in trimming the cost and expanding the profit of The Berkeley Partnership.

The inventory control analysis the flow of goods in and out from the company. The

inventory control ensues the recording of the incoming of the raw material, the work in process

goods lying with the company and also the finished goods in the company and the inventory out

for the purpose of sale by the company The Berkeley Partnership. Inventory control report is

used by the decision makers to take the decision on the production of the units in the future and

determining the cost of the product lying in the company.

Accounts receivable records are the reports includes the recording of data of the credit

sales. The sale of product on credit is shown in accounts receivable and included in the

management accounting reports knowing the amount owned by the company from the debtors of

the company. It acts as a crucial report for the calculation of future liquidity of the company. The

report also includes the recoverable and non-recoverable amount by the company through the

debtors (Senftlechner and Hiebl, 2015). Thereby managers can use the reports in checking and

illuminating the problems in the collection process by the company and the various methods used

in the collection process.

Management accounting reporting is the systematic analysis of the recorded data by the

operation management and making the final reports and submitting the reports to the decision

makers of The Berkeley Partnership. This includes cost accounting records, the budget reports,

inventory control reports, accounts receivable reports and the performance report.

The cost accounting reports presents the cost and expenses incurred on the product so

manufactured for the purpose of its price determination and profit calculation by the managers in

The Berkeley Partnership. If the cost incurred on the production of the product increase than the

price of the product will also increase accordingly (Wagenhofer, 2016). Also, there are market

factors such as increase in demand there will be rise in price of a product thereby increasing the

profit of the company.

The budget reports are used to compare the current year data with the previous year data

of the financial year. The budget reports can also be made on the comparison of the expected

cost and the actual cost incurred in manufacturing of the product (Hiebl, 2018). The budget

report helps the managers on taking the decisions on the weak points of the manufacturing cost.

It helps in trimming the cost and expanding the profit of The Berkeley Partnership.

The inventory control analysis the flow of goods in and out from the company. The

inventory control ensues the recording of the incoming of the raw material, the work in process

goods lying with the company and also the finished goods in the company and the inventory out

for the purpose of sale by the company The Berkeley Partnership. Inventory control report is

used by the decision makers to take the decision on the production of the units in the future and

determining the cost of the product lying in the company.

Accounts receivable records are the reports includes the recording of data of the credit

sales. The sale of product on credit is shown in accounts receivable and included in the

management accounting reports knowing the amount owned by the company from the debtors of

the company. It acts as a crucial report for the calculation of future liquidity of the company. The

report also includes the recoverable and non-recoverable amount by the company through the

debtors (Senftlechner and Hiebl, 2015). Thereby managers can use the reports in checking and

illuminating the problems in the collection process by the company and the various methods used

in the collection process.

Performance reporting is the overall representation of the report which includes the

evaluation of the work done and the successfulness of the policies opted by the managers in the

previous session and the decisions taken on any manufacturing process and the product

development. As the name suggests it is used to compare the original data with the present data

to calculate that how efficient the decision is taken by the managers (Coad, Jack and Kholeif,

2015). If the plans and policies doesn't work according to the planning than there is a need to

modify the plans of the company.

M1-

The management accounting have benefits for the organisation by being a quality check

on the functioning of the company. This includes the presentation of reports such as cost report,

inventory report, finance report etc. which reduces the risk factor for the company. Also, there

are reports on daily, weekly and monthly basis which ensures the regular check on the issues

relating to operation (Maskell, Baggaley and Grasso, 2016). The report includes the cost of

labour, the managers can best allocate the labour and reduce the cost in effective manner. TSR

Pvt. Ltd. Can use the data in reports in comparing the cost from previous operation there by

increasing the productivity and also The Berkeley Partnership. Can be a benchmark for all the

other companies in the country.

D1

Through management accounting system and reporting there can be regular quality

management of the product by checking the product on weekly and monthly basis which

evaluates and ensures the production of quality product at a minimal cost, the cost management

report shows the cost incurred on the product which includes raw material cost, cost of labour

and other manufacturing expenses and there comparison with the price of product so that there

can be profitability in the production of the product (Morden, 2016). Through continuous

evaluation of reports in the company The Berkeley Partnership. there is continuous elimination

of the errors and increasing the level of productivity thereby helping in continuous improvement

in The Berkeley Partnership.

evaluation of the work done and the successfulness of the policies opted by the managers in the

previous session and the decisions taken on any manufacturing process and the product

development. As the name suggests it is used to compare the original data with the present data

to calculate that how efficient the decision is taken by the managers (Coad, Jack and Kholeif,

2015). If the plans and policies doesn't work according to the planning than there is a need to

modify the plans of the company.

M1-

The management accounting have benefits for the organisation by being a quality check

on the functioning of the company. This includes the presentation of reports such as cost report,

inventory report, finance report etc. which reduces the risk factor for the company. Also, there

are reports on daily, weekly and monthly basis which ensures the regular check on the issues

relating to operation (Maskell, Baggaley and Grasso, 2016). The report includes the cost of

labour, the managers can best allocate the labour and reduce the cost in effective manner. TSR

Pvt. Ltd. Can use the data in reports in comparing the cost from previous operation there by

increasing the productivity and also The Berkeley Partnership. Can be a benchmark for all the

other companies in the country.

D1

Through management accounting system and reporting there can be regular quality

management of the product by checking the product on weekly and monthly basis which

evaluates and ensures the production of quality product at a minimal cost, the cost management

report shows the cost incurred on the product which includes raw material cost, cost of labour

and other manufacturing expenses and there comparison with the price of product so that there

can be profitability in the production of the product (Morden, 2016). Through continuous

evaluation of reports in the company The Berkeley Partnership. there is continuous elimination

of the errors and increasing the level of productivity thereby helping in continuous improvement

in The Berkeley Partnership.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

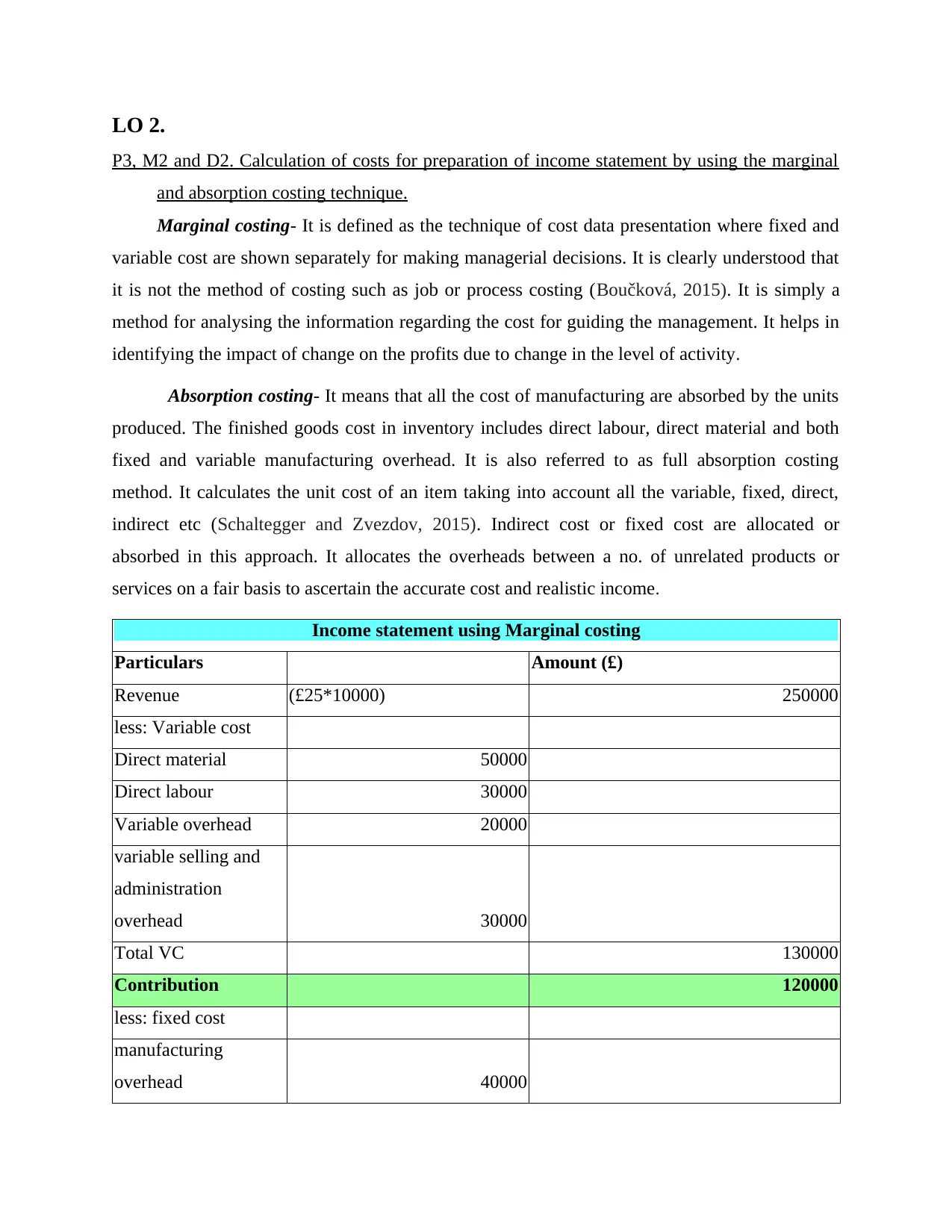

LO 2.

P3, M2 and D2. Calculation of costs for preparation of income statement by using the marginal

and absorption costing technique.

Marginal costing- It is defined as the technique of cost data presentation where fixed and

variable cost are shown separately for making managerial decisions. It is clearly understood that

it is not the method of costing such as job or process costing (Boučková, 2015). It is simply a

method for analysing the information regarding the cost for guiding the management. It helps in

identifying the impact of change on the profits due to change in the level of activity.

Absorption costing- It means that all the cost of manufacturing are absorbed by the units

produced. The finished goods cost in inventory includes direct labour, direct material and both

fixed and variable manufacturing overhead. It is also referred to as full absorption costing

method. It calculates the unit cost of an item taking into account all the variable, fixed, direct,

indirect etc (Schaltegger and Zvezdov, 2015). Indirect cost or fixed cost are allocated or

absorbed in this approach. It allocates the overheads between a no. of unrelated products or

services on a fair basis to ascertain the accurate cost and realistic income.

Income statement using Marginal costing

Particulars Amount (£)

Revenue (£25*10000) 250000

less: Variable cost

Direct material 50000

Direct labour 30000

Variable overhead 20000

variable selling and

administration

overhead 30000

Total VC 130000

Contribution 120000

less: fixed cost

manufacturing

overhead 40000

P3, M2 and D2. Calculation of costs for preparation of income statement by using the marginal

and absorption costing technique.

Marginal costing- It is defined as the technique of cost data presentation where fixed and

variable cost are shown separately for making managerial decisions. It is clearly understood that

it is not the method of costing such as job or process costing (Boučková, 2015). It is simply a

method for analysing the information regarding the cost for guiding the management. It helps in

identifying the impact of change on the profits due to change in the level of activity.

Absorption costing- It means that all the cost of manufacturing are absorbed by the units

produced. The finished goods cost in inventory includes direct labour, direct material and both

fixed and variable manufacturing overhead. It is also referred to as full absorption costing

method. It calculates the unit cost of an item taking into account all the variable, fixed, direct,

indirect etc (Schaltegger and Zvezdov, 2015). Indirect cost or fixed cost are allocated or

absorbed in this approach. It allocates the overheads between a no. of unrelated products or

services on a fair basis to ascertain the accurate cost and realistic income.

Income statement using Marginal costing

Particulars Amount (£)

Revenue (£25*10000) 250000

less: Variable cost

Direct material 50000

Direct labour 30000

Variable overhead 20000

variable selling and

administration

overhead 30000

Total VC 130000

Contribution 120000

less: fixed cost

manufacturing

overhead 40000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

selling and

administration

expenditure 30000 70000

Profit 50000

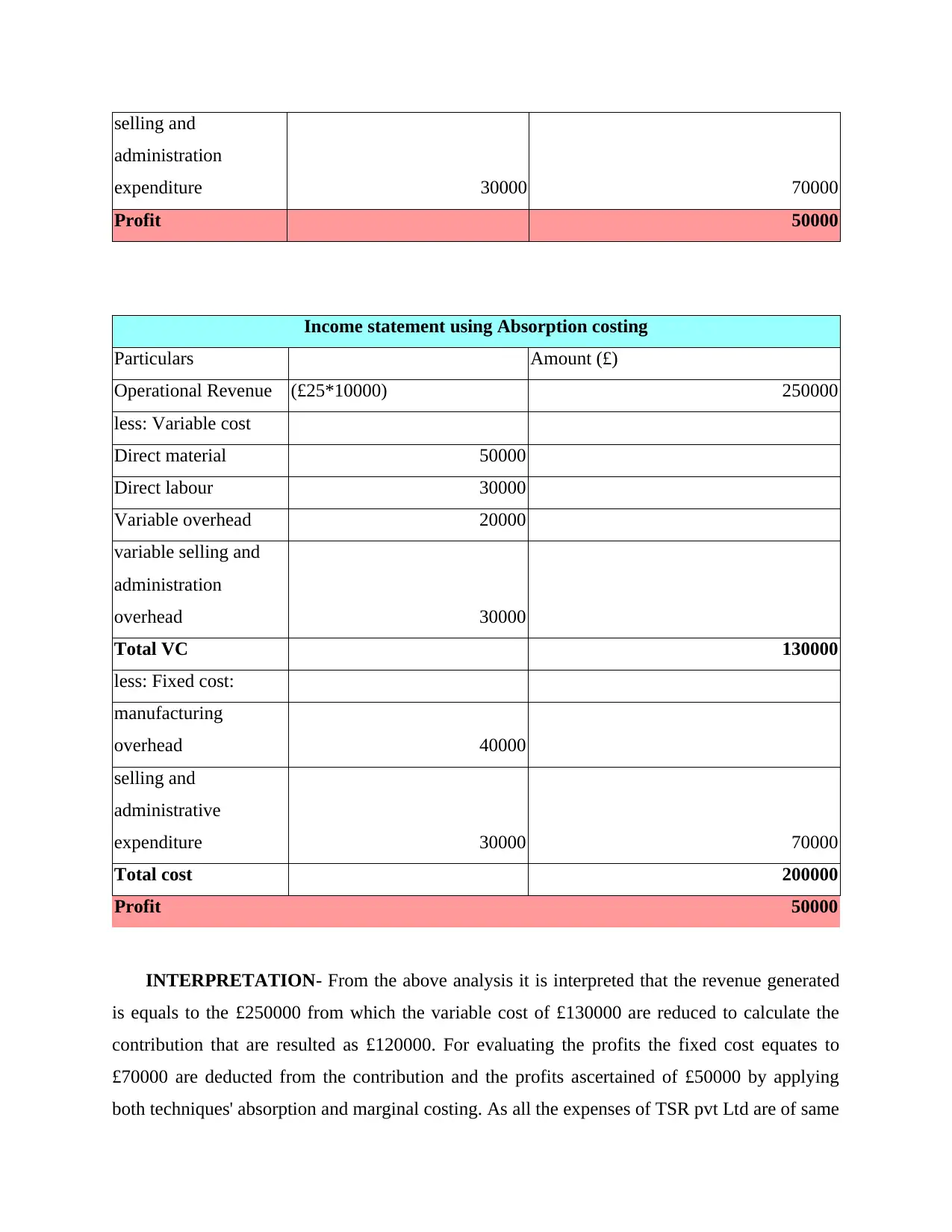

Income statement using Absorption costing

Particulars Amount (£)

Operational Revenue (£25*10000) 250000

less: Variable cost

Direct material 50000

Direct labour 30000

Variable overhead 20000

variable selling and

administration

overhead 30000

Total VC 130000

less: Fixed cost:

manufacturing

overhead 40000

selling and

administrative

expenditure 30000 70000

Total cost 200000

Profit 50000

INTERPRETATION- From the above analysis it is interpreted that the revenue generated

is equals to the £250000 from which the variable cost of £130000 are reduced to calculate the

contribution that are resulted as £120000. For evaluating the profits the fixed cost equates to

£70000 are deducted from the contribution and the profits ascertained of £50000 by applying

both techniques' absorption and marginal costing. As all the expenses of TSR pvt Ltd are of same

administration

expenditure 30000 70000

Profit 50000

Income statement using Absorption costing

Particulars Amount (£)

Operational Revenue (£25*10000) 250000

less: Variable cost

Direct material 50000

Direct labour 30000

Variable overhead 20000

variable selling and

administration

overhead 30000

Total VC 130000

less: Fixed cost:

manufacturing

overhead 40000

selling and

administrative

expenditure 30000 70000

Total cost 200000

Profit 50000

INTERPRETATION- From the above analysis it is interpreted that the revenue generated

is equals to the £250000 from which the variable cost of £130000 are reduced to calculate the

contribution that are resulted as £120000. For evaluating the profits the fixed cost equates to

£70000 are deducted from the contribution and the profits ascertained of £50000 by applying

both techniques' absorption and marginal costing. As all the expenses of TSR pvt Ltd are of same

amount so both the tools depicted the same amount of profit. From the analysis is determined

that absorption costing is a better tool for evaluating the income of the enterprise as it takes into

account both variable and fixed overheads in the inventory valuation and generates the realistic

profits. On the other hand, Marginal costing is not considered as an effective tool for computing

the profit as it ignores the fixed cost overheads in the valuation of inventory which leads to

incorrect and vague figures of profitability. Absorption technique helps in determining the over

and the underestimated overheads so that effective cost control can be exercised by the TSR pvt

Ltd. However, marginal costing does not provide information about the over and underestimation

of the overheads and no adjustments are made in it which results in unrealistic valuation.

LO 3

P4 Advantages and disadvantages of different types of planning tool used for budgetary control.

Budgetary control help the management to control the operation in the business in the

most efficient manner. They raise further funds for different purpose and utilize their resource

and company objective effectively. There are various advantages and disadvantages for

budgetary control in planning tool of ABC company. Advantages and disadvantages associated

with planning tools, in the context of budgetary control, are enumerated below:

~ Cash budget: Cash This budget is prepared by the BERKELEY PARTNERSHIP company to

estimatedestimate the cash inflow and outflow during the monthly, quarterly or yearly basis. The

main purpose to prepare the cash flow is to identify the overall cash that available in the

company and they can set their future project through the management of cash budget. To

analyse the proper cash budget helps the company to task risk in project and invest the amount

which results to the gain and profits to the company (The Advantages and Disadvantages of

Using Cash Budget, 2019)

The advantages of cash budget are -

THE BERKELEY PARTNERSHIP company can improve their financial position on the

market by strongly communicating and investing in the project deals.

that absorption costing is a better tool for evaluating the income of the enterprise as it takes into

account both variable and fixed overheads in the inventory valuation and generates the realistic

profits. On the other hand, Marginal costing is not considered as an effective tool for computing

the profit as it ignores the fixed cost overheads in the valuation of inventory which leads to

incorrect and vague figures of profitability. Absorption technique helps in determining the over

and the underestimated overheads so that effective cost control can be exercised by the TSR pvt

Ltd. However, marginal costing does not provide information about the over and underestimation

of the overheads and no adjustments are made in it which results in unrealistic valuation.

LO 3

P4 Advantages and disadvantages of different types of planning tool used for budgetary control.

Budgetary control help the management to control the operation in the business in the

most efficient manner. They raise further funds for different purpose and utilize their resource

and company objective effectively. There are various advantages and disadvantages for

budgetary control in planning tool of ABC company. Advantages and disadvantages associated

with planning tools, in the context of budgetary control, are enumerated below:

~ Cash budget: Cash This budget is prepared by the BERKELEY PARTNERSHIP company to

estimatedestimate the cash inflow and outflow during the monthly, quarterly or yearly basis. The

main purpose to prepare the cash flow is to identify the overall cash that available in the

company and they can set their future project through the management of cash budget. To

analyse the proper cash budget helps the company to task risk in project and invest the amount

which results to the gain and profits to the company (The Advantages and Disadvantages of

Using Cash Budget, 2019)

The advantages of cash budget are -

THE BERKELEY PARTNERSHIP company can improve their financial position on the

market by strongly communicating and investing in the project deals.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With the cash budget THE BERKELEY PARTNERSHIP company can identity and

predict the upcoming challenges that company needs to face in the near future (Locke,

Lucas and Grayson, 2016). THE BERKELEY PARTNERSHIP company can invest in small business organisation

or cam also deal in financial services to provide loan to the companies to maintain

reputation in the market.

Disadvantages of cash budget are -

It stops company to invest in market as people are not trust worthy and they can use their

cash for some other illegal purpose also which affects the company dignity.

There are more chances of theft of cash as company makes strategy to save the money

which result Iin getting more links to the people to commit fraud in the

company(Mouritsen and Kreiner, 2016).

As cash inflow and cash outflow in previous year is allotted in the next year which

means company take the profit ratio from the previous year but one disadvantages is that no year

is same in cash budget ratio as if one year suffer loss than it reflect the next upcoming year.

~ Operating budget: Suchoperating budgets depends upon the overall financial budget

plan in terms of revenue, profits and expenses of the BERKELEY PARTNERSHIP company.

As THE BERKELEY PARTNERSHIP company is a medium sized base having 50 employees

working under the following department as to operate of finalise the actual plan made an

operating budgets plan. If company want to engage in establishing new products than it includes

project expense, profit or losses raising and resources utilizing are evaluated in the operating

budget (Pros & Cons of an Operational Budget, 2019).

Advantages: of operating budget are -

If company grows business for longer term than this budget is helpful to take risk and fulfil the

targets.

Operating budget It helps the company in federal tax compliance to save the tax from different

ways and invest in other projects which is also beneficial to company use.

predict the upcoming challenges that company needs to face in the near future (Locke,

Lucas and Grayson, 2016). THE BERKELEY PARTNERSHIP company can invest in small business organisation

or cam also deal in financial services to provide loan to the companies to maintain

reputation in the market.

Disadvantages of cash budget are -

It stops company to invest in market as people are not trust worthy and they can use their

cash for some other illegal purpose also which affects the company dignity.

There are more chances of theft of cash as company makes strategy to save the money

which result Iin getting more links to the people to commit fraud in the

company(Mouritsen and Kreiner, 2016).

As cash inflow and cash outflow in previous year is allotted in the next year which

means company take the profit ratio from the previous year but one disadvantages is that no year

is same in cash budget ratio as if one year suffer loss than it reflect the next upcoming year.

~ Operating budget: Suchoperating budgets depends upon the overall financial budget

plan in terms of revenue, profits and expenses of the BERKELEY PARTNERSHIP company.

As THE BERKELEY PARTNERSHIP company is a medium sized base having 50 employees

working under the following department as to operate of finalise the actual plan made an

operating budgets plan. If company want to engage in establishing new products than it includes

project expense, profit or losses raising and resources utilizing are evaluated in the operating

budget (Pros & Cons of an Operational Budget, 2019).

Advantages: of operating budget are -

If company grows business for longer term than this budget is helpful to take risk and fulfil the

targets.

Operating budget It helps the company in federal tax compliance to save the tax from different

ways and invest in other projects which is also beneficial to company use.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This budget helps the company to keep their data accurate and in systematic manner so

that if new person are appointed they can easily take over the data (Dekker, 2016).

Disadvantages of operating budget -

To prepare a proper operating budget sometimes neglect the minimum requirement which

affects the whole budget planning.

To operate in different operational budgets it neglect the bank investment scheme which

help employees to retain more in the company. Operational budgets are not prepared for the upcoming challenges that company can face

any time without any planning (Otley, 2016).

Zero based budgeting: The word itself describes the budget like zero base. This means that

company had to start their budget planning from the zero base. As other budgets are prepared on

the bases of previous profits but this budget is prepared under the proper guidance and reviews

from the employees working in the company (Quattrone, 2016). They ask the employees about

the expense they bear in office and how they cut the expense incurred and that's how the zero

bases budgets prepared.

Advantages of zero base budgeting are -

Zero Based budgeting are justified and clear to show all the budgets plan easily. They discuss

with the internal team members and then make budget which motivate employees to engage into

business decision. THE BERKELEY PARTNERSHIP company can look the actual base number and

make the plan they are not refereed to the previous plan budget to make the budget plan

(Maas, Schaltegger and Crutzen, 2016).

Disadvantage -

This budgets is not effectual for the companies engages with high number of employees.

This is the time consuming method as it take the decision of all the employees and the

budget plan is prepared which sometimes considered to be inaccurate.

that if new person are appointed they can easily take over the data (Dekker, 2016).

Disadvantages of operating budget -

To prepare a proper operating budget sometimes neglect the minimum requirement which

affects the whole budget planning.

To operate in different operational budgets it neglect the bank investment scheme which

help employees to retain more in the company. Operational budgets are not prepared for the upcoming challenges that company can face

any time without any planning (Otley, 2016).

Zero based budgeting: The word itself describes the budget like zero base. This means that

company had to start their budget planning from the zero base. As other budgets are prepared on

the bases of previous profits but this budget is prepared under the proper guidance and reviews

from the employees working in the company (Quattrone, 2016). They ask the employees about

the expense they bear in office and how they cut the expense incurred and that's how the zero

bases budgets prepared.

Advantages of zero base budgeting are -

Zero Based budgeting are justified and clear to show all the budgets plan easily. They discuss

with the internal team members and then make budget which motivate employees to engage into

business decision. THE BERKELEY PARTNERSHIP company can look the actual base number and

make the plan they are not refereed to the previous plan budget to make the budget plan

(Maas, Schaltegger and Crutzen, 2016).

Disadvantage -

This budgets is not effectual for the companies engages with high number of employees.

This is the time consuming method as it take the decision of all the employees and the

budget plan is prepared which sometimes considered to be inaccurate.

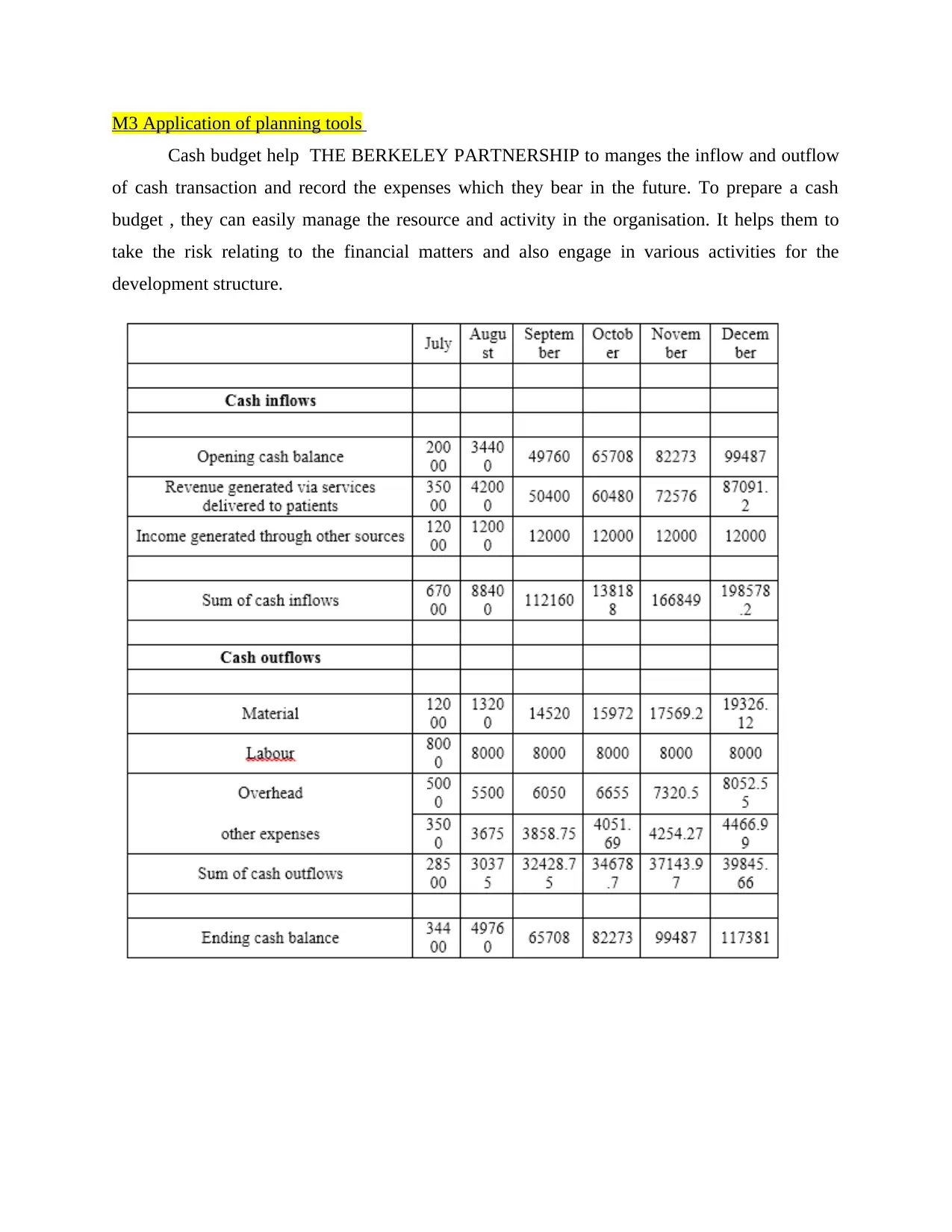

M3 Application of planning tools

Cash budget help THE BERKELEY PARTNERSHIP to manges the inflow and outflow

of cash transaction and record the expenses which they bear in the future. To prepare a cash

budget , they can easily manage the resource and activity in the organisation. It helps them to

take the risk relating to the financial matters and also engage in various activities for the

development structure.

Cash budget help THE BERKELEY PARTNERSHIP to manges the inflow and outflow

of cash transaction and record the expenses which they bear in the future. To prepare a cash

budget , they can easily manage the resource and activity in the organisation. It helps them to

take the risk relating to the financial matters and also engage in various activities for the

development structure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.