Management Accounting Report and Presentation - NSAB567B5 Assignment

VerifiedAdded on 2023/05/26

|17

|2506

|472

Report

AI Summary

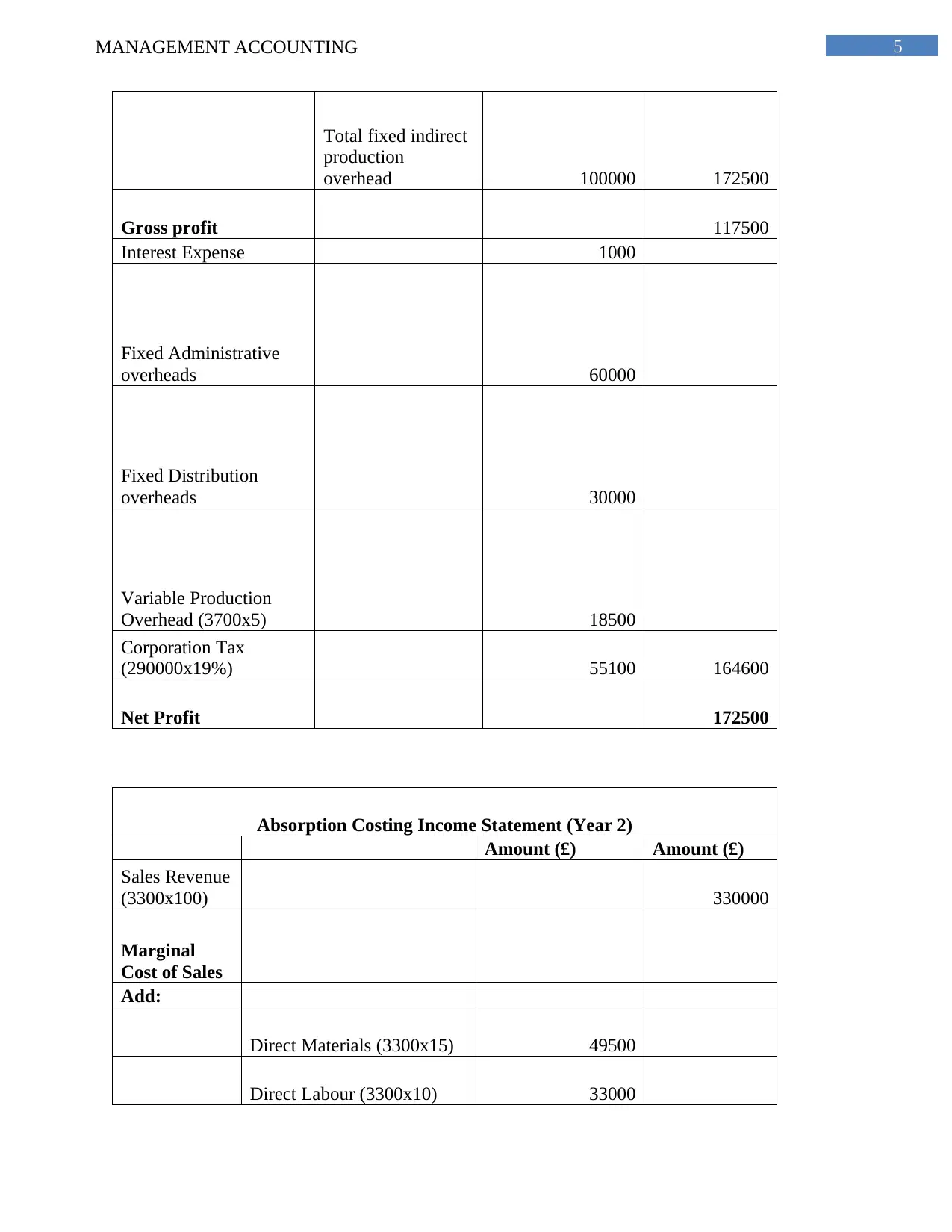

This assignment report delves into the core concepts of management accounting, beginning with the preparation of income statements using both marginal and absorption costing methods across three years. The report includes detailed calculations of sales revenue, marginal cost of sales, contribution, and net profit under marginal costing, followed by similar calculations under absorption costing, along with comments comparing the results and highlighting the reasons for profit differences. Furthermore, the report presents a presentation on management accounting, defining its roles, principles, and various reports like financial reports, pro forma cash flow, sales reports, item costs reports, budget reports, and performance reports. It also discusses the benefits of management accounting and its application within an organization. The assignment further explores the advantages and disadvantages of planning tools, such as budgetary control, and examines how organizations adapt management accounting systems to address financial problems, leading to sustainable success. The report concludes with a critical evaluation of integration and its application within an organization. It is a comprehensive study of the subject, covering various aspects of management accounting with detailed financial analysis and practical applications.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.