Management Accounting Report: Incremental Analysis for Coyle Company

VerifiedAdded on 2023/01/09

|6

|891

|32

Report

AI Summary

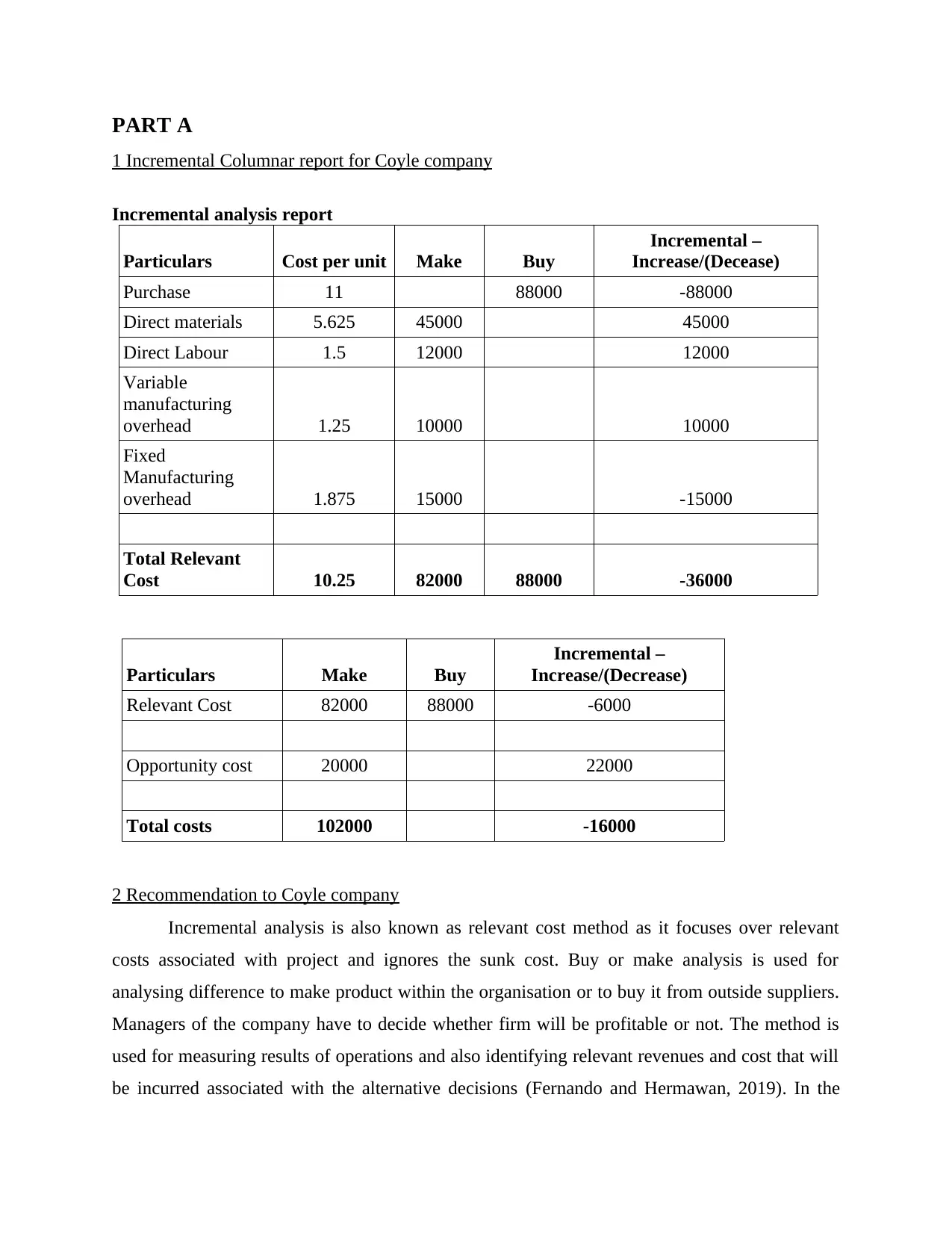

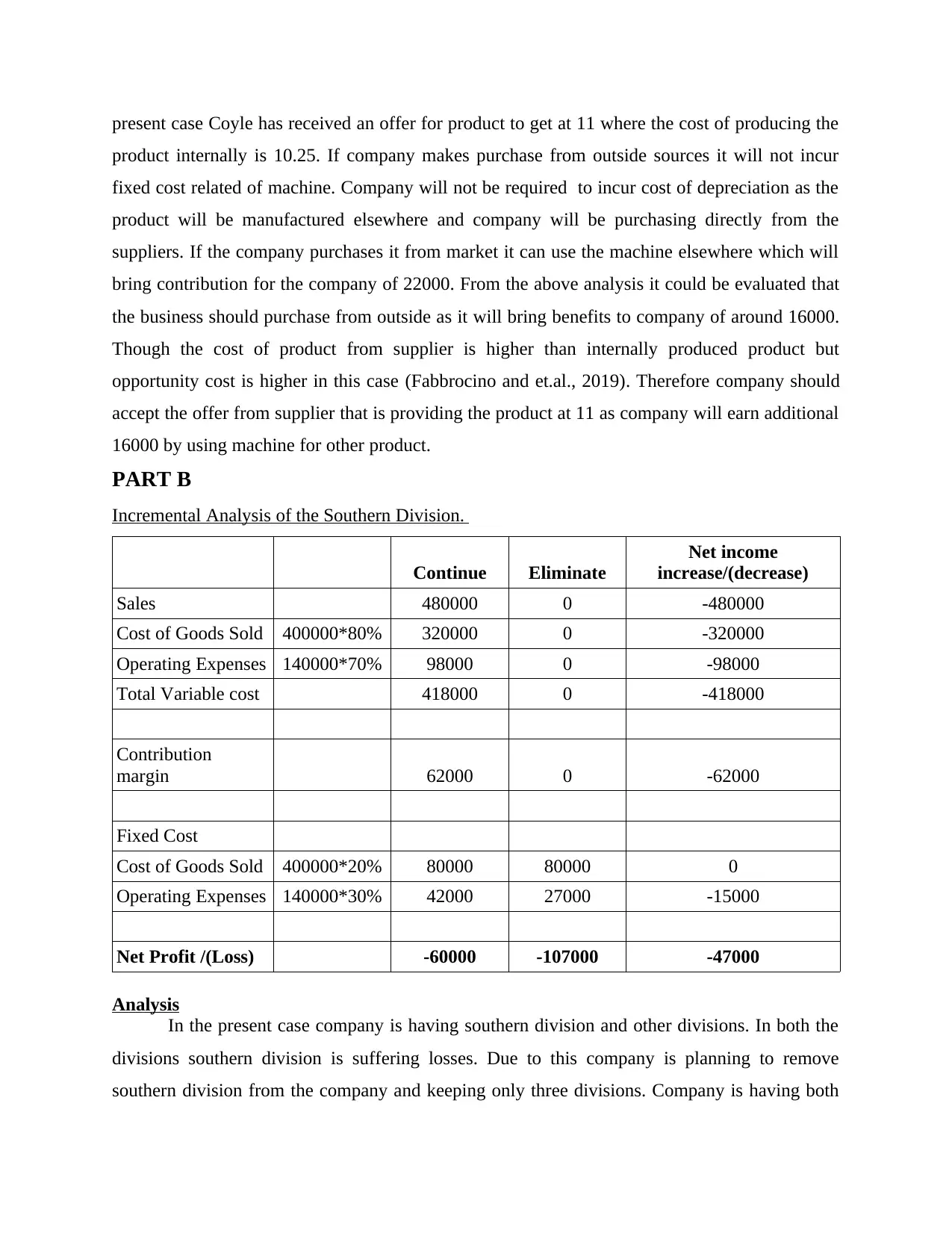

This report presents an incremental analysis for Coyle Company, evaluating a make-or-buy decision and the performance of the Southern Division. Part A of the report provides an incremental columnar analysis comparing the costs of producing a product internally versus purchasing it from an external supplier. The analysis includes calculations of relevant costs, opportunity costs, and total costs, leading to a recommendation to purchase from the supplier. Part B focuses on the Southern Division, examining the potential impact of its elimination on the company's profitability. The analysis considers sales, cost of goods sold (both variable and fixed), and operating expenses to determine the net effect of the division's removal. The report concludes that eliminating the Southern Division would decrease profit, highlighting the importance of considering internal and external factors, including fixed costs and production capacity, when making such decisions. The report references academic sources to support the analysis and recommendations.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.