Polytechnic Institute Australia ACC203 Management Accounting Report

VerifiedAdded on 2023/06/04

|10

|2105

|107

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on the shift from compliance and control to competitive support in modern business environments. The first part of the report discusses the factors contributing to the development of management accounting, including cost leadership, differentiation, and strategic risk management, and evaluates the usefulness of the Balanced Scorecard as a key tool. The second part of the report delves into a case study of Qantas, an ASX-listed company. It identifies Qantas's critical success factors (CSFs) and key performance indicators (KPIs), constructs a strategic map aligning with Qantas's long-term objectives, and develops a Balanced Scorecard based on the analysis of the company's annual report. The report integrates theoretical concepts with practical application, providing a detailed examination of management accounting principles and their application in a real-world business context, with the goal of aiding strategic decision-making and performance evaluation. This report is designed to provide a comprehensive understanding of the role of management accounting in today's business environment, and the key tools and strategies that are used to drive performance and achieve strategic objectives.

ACC203 Management Accounting

Term 2

Major Assignment

Term 2

Major Assignment

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Introduction............................................................................................................................3

Factors contributed in development of management accounting practice.............................3

Evaluating the usefulness of balanced scorecard...................................................................5

Conclusion..............................................................................................................................6

Question 2..................................................................................................................................6

Part A.....................................................................................................................................6

Part B......................................................................................................................................6

Part C......................................................................................................................................6

References..................................................................................................................................7

Question 1..................................................................................................................................3

Introduction............................................................................................................................3

Factors contributed in development of management accounting practice.............................3

Evaluating the usefulness of balanced scorecard...................................................................5

Conclusion..............................................................................................................................6

Question 2..................................................................................................................................6

Part A.....................................................................................................................................6

Part B......................................................................................................................................6

Part C......................................................................................................................................6

References..................................................................................................................................7

QUESTION 1

Introduction

Modern management accounting practices are playing a significant role in business

decision process within highly volatile market trends. In the current market trends,

management accounting is not only focused on traditional accounting based on compliance

and control but also strategic and competitive factors which assist top managers in collection

of wide range of information such as market demand, market share of competitors, growth

trends, costing of new goods and services and product lifecycle (Mårtensson et al.2016). All

these elements have a great involvement in strategic business accounting as well as a

decision-making process.

Factors contributed to the development of management accounting practice

As a result of a change in business trends, companies in different industries are

applying organizational changes in which management is mainly focusing on innovative

approaches within management accounting practices. In traditional accounting practices,

companies have mainly focused for control and compliance practices through several tools

like cost control, budgeting, cost-benefit analysis and investment appraisal (Nuhu, Baird &

Appuhami, 2016). Apart from that application of a customer-centric approach in the strategic

planning process has influenced management for the adoption of new trends in business

accounting practices that provide significant support to a business entity in highly

competitive market trends. In this context, some important elements of management

accounting practices are discussed below that provide competitive support to top authorities

in a huge competition.

Cost leadership: It is one of the key factors of organizational success within in highly

completive market. According to this approach, companies make an effort in order to produce

its products at the lowest cost with reference to the price of its competitors. This approach

influences companies for application modern accounting practices in business operations

such as business process re-engineering for changing the structure production process,

determination of product lifecycle costing for assessment of cost of products in whole life and

consideration of Zero-base budgeting through which organization can manage its expenditure

as per business priorities (Hald & Thrane, 2016). All these tactics help the firm in offering its

products and services at lower prices as compared to other organization. It also provides

Introduction

Modern management accounting practices are playing a significant role in business

decision process within highly volatile market trends. In the current market trends,

management accounting is not only focused on traditional accounting based on compliance

and control but also strategic and competitive factors which assist top managers in collection

of wide range of information such as market demand, market share of competitors, growth

trends, costing of new goods and services and product lifecycle (Mårtensson et al.2016). All

these elements have a great involvement in strategic business accounting as well as a

decision-making process.

Factors contributed to the development of management accounting practice

As a result of a change in business trends, companies in different industries are

applying organizational changes in which management is mainly focusing on innovative

approaches within management accounting practices. In traditional accounting practices,

companies have mainly focused for control and compliance practices through several tools

like cost control, budgeting, cost-benefit analysis and investment appraisal (Nuhu, Baird &

Appuhami, 2016). Apart from that application of a customer-centric approach in the strategic

planning process has influenced management for the adoption of new trends in business

accounting practices that provide significant support to a business entity in highly

competitive market trends. In this context, some important elements of management

accounting practices are discussed below that provide competitive support to top authorities

in a huge competition.

Cost leadership: It is one of the key factors of organizational success within in highly

completive market. According to this approach, companies make an effort in order to produce

its products at the lowest cost with reference to the price of its competitors. This approach

influences companies for application modern accounting practices in business operations

such as business process re-engineering for changing the structure production process,

determination of product lifecycle costing for assessment of cost of products in whole life and

consideration of Zero-base budgeting through which organization can manage its expenditure

as per business priorities (Hald & Thrane, 2016). All these tactics help the firm in offering its

products and services at lower prices as compared to other organization. It also provides

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

significant assistance to management for ensuring competitive edge over other companies.

For example; Walmart has adopted the cost leadership model through company offers

thousands of products at the lowest prices based competitor’s prices of similar products that

have played an important role to outcompete its rival companies for many years.

Differentiation: In the current management accounting practices, top managers within an

organization considers differentiation strategy in its product or service range. According to

this approach, business entity makes efforts in the development of such kinds of products or

services which are unique and superior in quality and speciation with reference competitor’s

goods and services (Nuhu, Baird & Bala Appuhamilage, 2017). Therefore, differentiation

plays an important role in obtaining a competitive advantage over other companies. In this

context, modern management accounting has found very effective in rectification of modern

organizational management issues and increase effectiveness traditional management

accounting operations for financial decision non-financial. This is because different kinds of

information are acquired in contemporary accounting operations such as nature of activities,

size of the market, external business environment and market conditions, the profile of target

consumer, human resource related issues, structural business issues, etc. (Schaltegger &

Burritt, 2017). In this context of differentiation approach, total quality management can be

considered as an important and most effective system through the organization is able to

improve the quality and specification of goods/services. For example, Tesla, a US-based

company, has differentiated itself through its high luxury electric sports cars.

Strategic risk management: In the present era, business entities face a wide range of business

risks in the form of cost of investment, change in needs of customers, alteration in market

demand and other international as well as domestic factors. In this regards, management

accounting operations support manager in the assessment of risk or potential hazards factors

that could lead negative impact on overall business performance, and markets share of

organization (Epstein, Verbeeten & Widener, 2018). In this context, balance scorecard has

found very effective tools for assessment of risk because it covers all areas of business

management such as growth, internal business environment, customer trends, financial

perspective, etc. through which manager can handle different aspects of business trends.

Evaluating the usefulness of balanced scorecard

The balanced scorecard is a termed as most effective management system organizations of

modern management accounting practices that enables management to get clarify about

For example; Walmart has adopted the cost leadership model through company offers

thousands of products at the lowest prices based competitor’s prices of similar products that

have played an important role to outcompete its rival companies for many years.

Differentiation: In the current management accounting practices, top managers within an

organization considers differentiation strategy in its product or service range. According to

this approach, business entity makes efforts in the development of such kinds of products or

services which are unique and superior in quality and speciation with reference competitor’s

goods and services (Nuhu, Baird & Bala Appuhamilage, 2017). Therefore, differentiation

plays an important role in obtaining a competitive advantage over other companies. In this

context, modern management accounting has found very effective in rectification of modern

organizational management issues and increase effectiveness traditional management

accounting operations for financial decision non-financial. This is because different kinds of

information are acquired in contemporary accounting operations such as nature of activities,

size of the market, external business environment and market conditions, the profile of target

consumer, human resource related issues, structural business issues, etc. (Schaltegger &

Burritt, 2017). In this context of differentiation approach, total quality management can be

considered as an important and most effective system through the organization is able to

improve the quality and specification of goods/services. For example, Tesla, a US-based

company, has differentiated itself through its high luxury electric sports cars.

Strategic risk management: In the present era, business entities face a wide range of business

risks in the form of cost of investment, change in needs of customers, alteration in market

demand and other international as well as domestic factors. In this regards, management

accounting operations support manager in the assessment of risk or potential hazards factors

that could lead negative impact on overall business performance, and markets share of

organization (Epstein, Verbeeten & Widener, 2018). In this context, balance scorecard has

found very effective tools for assessment of risk because it covers all areas of business

management such as growth, internal business environment, customer trends, financial

perspective, etc. through which manager can handle different aspects of business trends.

Evaluating the usefulness of balanced scorecard

The balanced scorecard is a termed as most effective management system organizations of

modern management accounting practices that enables management to get clarify about

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

vision and strategy of business entity and convert it into the day to day business actions. This

system provides feedback to management about both the internal business operations as well

as external outcomes that play an important role in managing continuous improvement in

strategic performance. In addition to that, the balanced scorecard has found very effective for

transforming strategic planning from a management desk to real-time business practices

(Nuhu, Baird & Bala Appuhamilage, 2017). It covers four elements which are mentioned

below:

Learning & Growth Perspective: Advancement in skills of employees and the application

of new business practices.

Internal Business Practices: Assessment of current business operations.

Customer Perspective: Evaluation of present trends in customer, products and market

demand,

Financial Perspective: Investment appraisal, assessment of financial performance and

cost-benefit analysis.

Apart from that, some other uses of the balanced scorecard are mentioned below:

Better Strategic Planning: The Balanced Scorecard provides a powerful and most

effective framework for building and communicating business strategy so as top

managers are able to consider the cause-and-effect relationships among various

business operations.

Improved Strategy Communication & Execution: In the process of management

accounting practices, this approach facilities one-page picture of organizational goals

and strategy which can communicate strategy internal and external stakeholder

(Nuhu, Baird & Appuhami, 2016).

Better Alignment of Projects and Initiatives: It assists managers in order to map

company’s projects as well as initiatives towards a wide range of strategic objectives

so as a business entity could generate optimum results.

Better Management Information: The Balanced Scorecard has found very effective in

designing of key performance indicators with reference to primary strategic

objectives. Therefore, the performance of the organization and its employees can be

evaluated easily on the basis of predetermined standards (Hald & Thrane, 2016).

system provides feedback to management about both the internal business operations as well

as external outcomes that play an important role in managing continuous improvement in

strategic performance. In addition to that, the balanced scorecard has found very effective for

transforming strategic planning from a management desk to real-time business practices

(Nuhu, Baird & Bala Appuhamilage, 2017). It covers four elements which are mentioned

below:

Learning & Growth Perspective: Advancement in skills of employees and the application

of new business practices.

Internal Business Practices: Assessment of current business operations.

Customer Perspective: Evaluation of present trends in customer, products and market

demand,

Financial Perspective: Investment appraisal, assessment of financial performance and

cost-benefit analysis.

Apart from that, some other uses of the balanced scorecard are mentioned below:

Better Strategic Planning: The Balanced Scorecard provides a powerful and most

effective framework for building and communicating business strategy so as top

managers are able to consider the cause-and-effect relationships among various

business operations.

Improved Strategy Communication & Execution: In the process of management

accounting practices, this approach facilities one-page picture of organizational goals

and strategy which can communicate strategy internal and external stakeholder

(Nuhu, Baird & Appuhami, 2016).

Better Alignment of Projects and Initiatives: It assists managers in order to map

company’s projects as well as initiatives towards a wide range of strategic objectives

so as a business entity could generate optimum results.

Better Management Information: The Balanced Scorecard has found very effective in

designing of key performance indicators with reference to primary strategic

objectives. Therefore, the performance of the organization and its employees can be

evaluated easily on the basis of predetermined standards (Hald & Thrane, 2016).

Conclusion

On the basis of the above study, it has been concluded that contemporary management

accounting practices have found more effective for business operations in comparison to

traditional accounting operations. This investigation has found that companies are giving

more attention to competitive management accounting operations rather than traditional

practices related to control and compliance.

QUESTION 2

Part A

Critical success factors

Non-stop flights: Company aims to provide the nonstop flying towards the destination routes

covered in their network. Such facility provided by the airlines helps to reduce its travel time

to reach an exacting destination.

Continuous promotions & in-flight services: Qantas construct the best airlines in contrast

to other airlines as they provide promotional services in airlines sectors refers to aiming the

loyal consumers and concentrating on high revenue clientele. Additional flight facilities are

provided such as the selection of seats, effortlessly booking the tickets & categorisation of the

class of services (QANTAS ANNUAL REPORT 2017, 2017). Moreover, Qantas has also

been known for its exercise of cardiac defibrillators in their flights. Proper guidance is given

to the workers so that they can use the physician kit and cardiac defibrillators in a situation of

any crisis on board.

Low price strategy: Further airline companies aims to reduce their cost of operations to

uplift their profits without compromising with quality. For this aspects, Qantas implements

training and development programs to enhance the skills of their workforces (Annual reports

of Qantas Airways, 2016). Further, for operational efficiency, the company implements

updated technologies by considering environment sustainability.

Quality services: Company aims to provide regular and punctual services to enhance

customer satisfaction. Further, they improvise operational strategies by considering customer

feedbacks and complaints.

Key performance indicators

Optimum capital structure

On the basis of the above study, it has been concluded that contemporary management

accounting practices have found more effective for business operations in comparison to

traditional accounting operations. This investigation has found that companies are giving

more attention to competitive management accounting operations rather than traditional

practices related to control and compliance.

QUESTION 2

Part A

Critical success factors

Non-stop flights: Company aims to provide the nonstop flying towards the destination routes

covered in their network. Such facility provided by the airlines helps to reduce its travel time

to reach an exacting destination.

Continuous promotions & in-flight services: Qantas construct the best airlines in contrast

to other airlines as they provide promotional services in airlines sectors refers to aiming the

loyal consumers and concentrating on high revenue clientele. Additional flight facilities are

provided such as the selection of seats, effortlessly booking the tickets & categorisation of the

class of services (QANTAS ANNUAL REPORT 2017, 2017). Moreover, Qantas has also

been known for its exercise of cardiac defibrillators in their flights. Proper guidance is given

to the workers so that they can use the physician kit and cardiac defibrillators in a situation of

any crisis on board.

Low price strategy: Further airline companies aims to reduce their cost of operations to

uplift their profits without compromising with quality. For this aspects, Qantas implements

training and development programs to enhance the skills of their workforces (Annual reports

of Qantas Airways, 2016). Further, for operational efficiency, the company implements

updated technologies by considering environment sustainability.

Quality services: Company aims to provide regular and punctual services to enhance

customer satisfaction. Further, they improvise operational strategies by considering customer

feedbacks and complaints.

Key performance indicators

Optimum capital structure

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increase in EBIT

Increase in shareholder’s wealth through an increase in EPS

Increase in shareholder’s wealth through an increase in EPS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

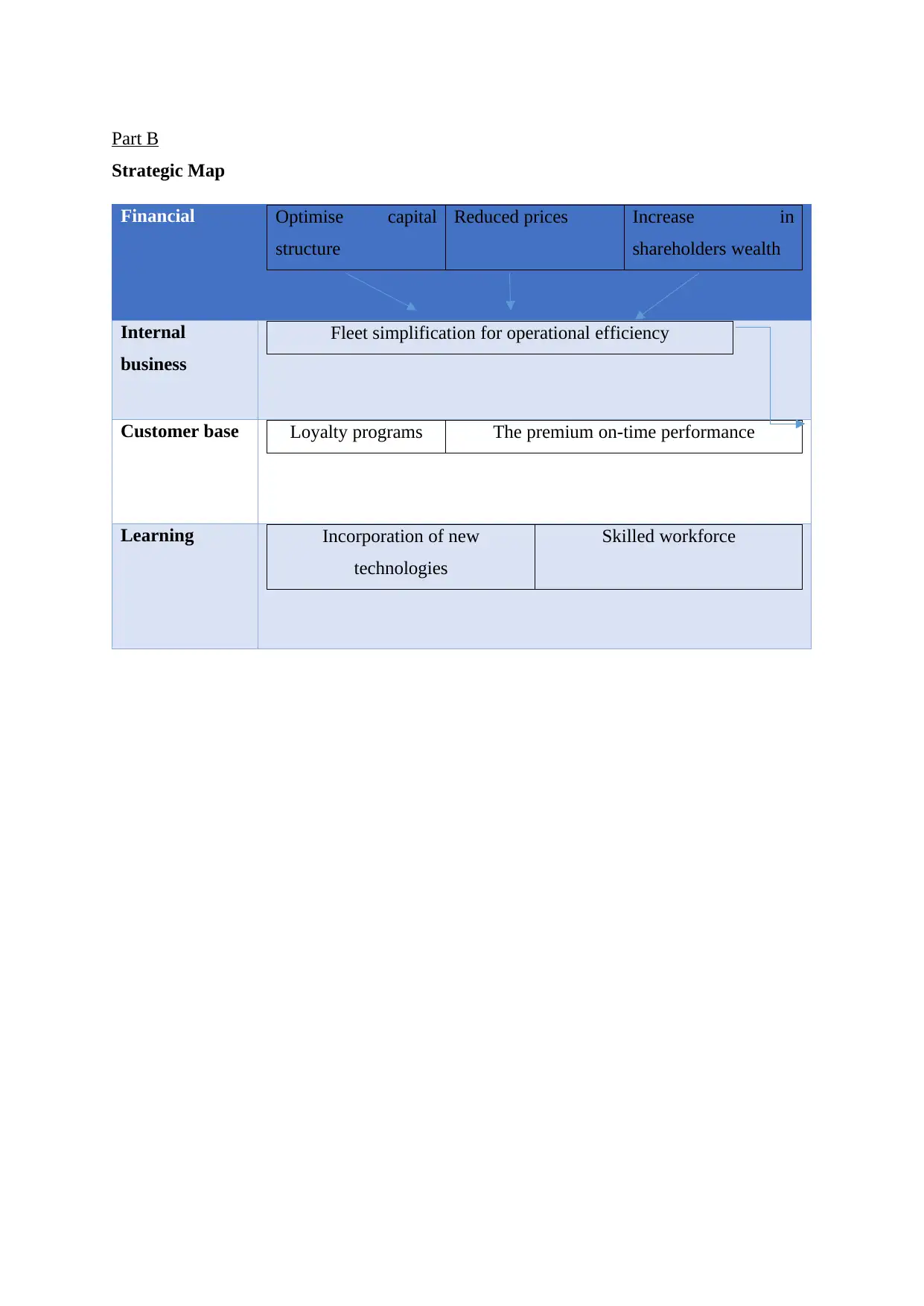

Part B

Strategic Map

Financial Optimise capital

structure

Reduced prices Increase in

shareholders wealth

Internal

business

Fleet simplification for operational efficiency

Customer base Loyalty programs The premium on-time performance

Learning Incorporation of new

technologies

Skilled workforce

Strategic Map

Financial Optimise capital

structure

Reduced prices Increase in

shareholders wealth

Internal

business

Fleet simplification for operational efficiency

Customer base Loyalty programs The premium on-time performance

Learning Incorporation of new

technologies

Skilled workforce

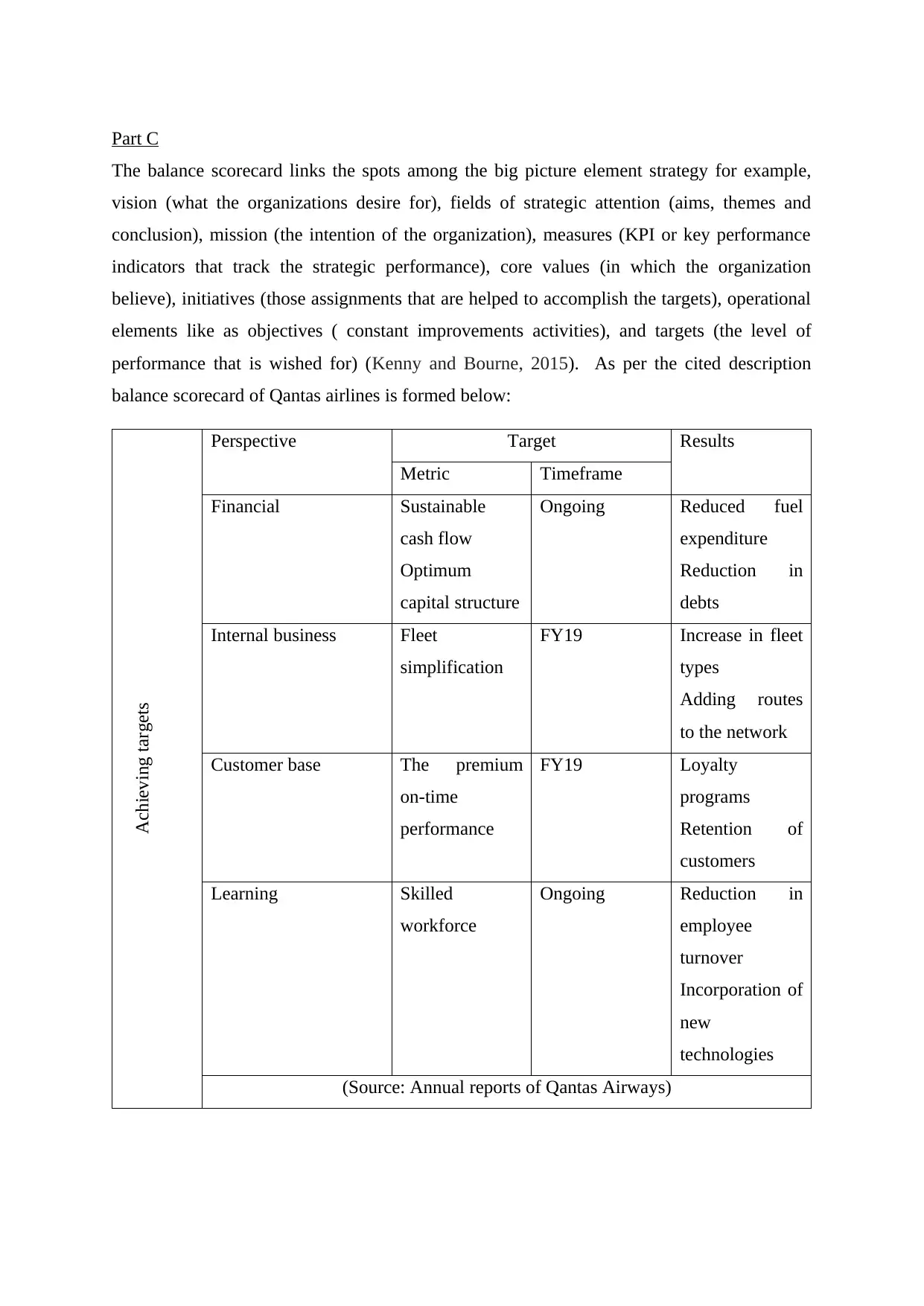

Part C

The balance scorecard links the spots among the big picture element strategy for example,

vision (what the organizations desire for), fields of strategic attention (aims, themes and

conclusion), mission (the intention of the organization), measures (KPI or key performance

indicators that track the strategic performance), core values (in which the organization

believe), initiatives (those assignments that are helped to accomplish the targets), operational

elements like as objectives ( constant improvements activities), and targets (the level of

performance that is wished for) (Kenny and Bourne, 2015). As per the cited description

balance scorecard of Qantas airlines is formed below:

Achieving targets

Perspective Target Results

Metric Timeframe

Financial Sustainable

cash flow

Optimum

capital structure

Ongoing Reduced fuel

expenditure

Reduction in

debts

Internal business Fleet

simplification

FY19 Increase in fleet

types

Adding routes

to the network

Customer base The premium

on-time

performance

FY19 Loyalty

programs

Retention of

customers

Learning Skilled

workforce

Ongoing Reduction in

employee

turnover

Incorporation of

new

technologies

(Source: Annual reports of Qantas Airways)

The balance scorecard links the spots among the big picture element strategy for example,

vision (what the organizations desire for), fields of strategic attention (aims, themes and

conclusion), mission (the intention of the organization), measures (KPI or key performance

indicators that track the strategic performance), core values (in which the organization

believe), initiatives (those assignments that are helped to accomplish the targets), operational

elements like as objectives ( constant improvements activities), and targets (the level of

performance that is wished for) (Kenny and Bourne, 2015). As per the cited description

balance scorecard of Qantas airlines is formed below:

Achieving targets

Perspective Target Results

Metric Timeframe

Financial Sustainable

cash flow

Optimum

capital structure

Ongoing Reduced fuel

expenditure

Reduction in

debts

Internal business Fleet

simplification

FY19 Increase in fleet

types

Adding routes

to the network

Customer base The premium

on-time

performance

FY19 Loyalty

programs

Retention of

customers

Learning Skilled

workforce

Ongoing Reduction in

employee

turnover

Incorporation of

new

technologies

(Source: Annual reports of Qantas Airways)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Annual reports of Qantas Airways, 2016. [Pdf]. Available through <

https://www.qantas.com.au/infodetail/about/corporateGovernance/2016AnnualReport.pdf >.

[Accessed on 24th September 2018].

Epstein, M. J., Verbeeten, F. H., and Widener, S. K. (Eds.). 2018. Performance Measurement

and Management Control: The Relevance of Performance Measurement and Management

Control Research. Emerald Publishing Limited.

Hald, K. S., and Thrane, S. 2016. Management Accounting and Supply Chain Strategy. In 1st

International Competitiveness Management Conference. Sage.

Kenny, G., and Bourne, M. 2015. Performance Measurement. Wiley Encyclopedia of

Management, 1-3.

Mårtensson, M., Höglund, L., Holmgren Caicedo, M., and Svärdsten, F. 2016. Management

accounting of control practices: a matter of and for strategy. In the 9TH INTERNATIONAL

EIASM PUBLIC SECTOR CONFERENCE, held in LISBON, PORTUGAL, SEPTEMBER 6-

8, 2016.

Nuhu, N. A., Baird, K., and Appuhami, R. 2016. The association between the use of

management accounting practices with organizational change and organizational

performance. In Advances in Management Accounting (pp. 67-98). Emerald Group

Publishing Limited.

Nuhu, N. A., Baird, K., and Bala Appuhamilage, A. 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting, 25(1), 106-126.

QANTAS ANNUAL REPORT 2017, 2017. [Pdf]. Available through <

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2017AnnualReport.pdf>. [Accessed on 24th September 2018].

Schaltegger, S., and Burritt, R. 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

Annual reports of Qantas Airways, 2016. [Pdf]. Available through <

https://www.qantas.com.au/infodetail/about/corporateGovernance/2016AnnualReport.pdf >.

[Accessed on 24th September 2018].

Epstein, M. J., Verbeeten, F. H., and Widener, S. K. (Eds.). 2018. Performance Measurement

and Management Control: The Relevance of Performance Measurement and Management

Control Research. Emerald Publishing Limited.

Hald, K. S., and Thrane, S. 2016. Management Accounting and Supply Chain Strategy. In 1st

International Competitiveness Management Conference. Sage.

Kenny, G., and Bourne, M. 2015. Performance Measurement. Wiley Encyclopedia of

Management, 1-3.

Mårtensson, M., Höglund, L., Holmgren Caicedo, M., and Svärdsten, F. 2016. Management

accounting of control practices: a matter of and for strategy. In the 9TH INTERNATIONAL

EIASM PUBLIC SECTOR CONFERENCE, held in LISBON, PORTUGAL, SEPTEMBER 6-

8, 2016.

Nuhu, N. A., Baird, K., and Appuhami, R. 2016. The association between the use of

management accounting practices with organizational change and organizational

performance. In Advances in Management Accounting (pp. 67-98). Emerald Group

Publishing Limited.

Nuhu, N. A., Baird, K., and Bala Appuhamilage, A. 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting, 25(1), 106-126.

QANTAS ANNUAL REPORT 2017, 2017. [Pdf]. Available through <

http://investor.qantas.com/FormBuilder/_Resource/_module/doLLG5ufYkCyEPjF1tpgyw/

file/annual-reports/2017AnnualReport.pdf>. [Accessed on 24th September 2018].

Schaltegger, S., and Burritt, R. 2017. Contemporary environmental accounting: issues,

concepts and practice. Routledge.

1 out of 10