Management Accounting Principle

VerifiedAdded on 2023/05/29

|9

|1518

|415

AI Summary

This article discusses the principles, benefits, types and methods of management accounting. It also covers the integration of management account and the difference between absorption costing and marginal costing. An example of variable cost and its income statement is also provided.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING PRINCIPLE

Management accounting principle

Name of the student

Name of the university

Student ID

Author note

Management accounting principle

Name of the student

Name of the university

Student ID

Author note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1MANAGEMENT ACCOUNTING PRINCIPLE

Table of Contents

Principles of management accounting.......................................................................................2

Benefits of management accounting..........................................................................................2

Types of management accounting systems................................................................................2

Various methods used for the purpose of management accounting reports...............................3

Types of costs.............................................................................................................................3

Absorption costing Vs marginal costing....................................................................................3

Example of variable cost............................................................................................................4

Integration of management account...........................................................................................5

Conclusion..................................................................................................................................5

Reference....................................................................................................................................7

Table of Contents

Principles of management accounting.......................................................................................2

Benefits of management accounting..........................................................................................2

Types of management accounting systems................................................................................2

Various methods used for the purpose of management accounting reports...............................3

Types of costs.............................................................................................................................3

Absorption costing Vs marginal costing....................................................................................3

Example of variable cost............................................................................................................4

Integration of management account...........................................................................................5

Conclusion..................................................................................................................................5

Reference....................................................................................................................................7

2MANAGEMENT ACCOUNTING PRINCIPLE

Principles of management accounting

Resource utilization – management accounting ensures appropriate utilization of the

resources available with the company. This is important as some of the resources are

available in excess whereas some are available scarcely. Hence, the available

resources shall be used effectively.

Uncontrollable and controllable cost – based on the controllability costs are

segregated into uncontrollable and controllable costs. As the uncontrollable costs

cannot be controlled the management must take the required steps for controlling the

controllable costs.

Designing and compiling – accounting records, information, statements, reports and

future, past or present results shall be designed and compiled for meeting the

requirements of particular business. The management accounting system is designed

in such way that it presents relevant data and assists in compiling (Langfield-Smith et

al. 2017).

Benefits of management accounting

It assists in maximizing the return rate on the capital employed

Business activities of the company are managed in a better way through application

of planning as well as budgeting both

It helps in measuring actual performance as compared to the budgets

It helps in increasing the efficiency of business

It helps in improving the relation among employees and management (Van der Stede

2016)

Types of management accounting systems

Product costing or costing system – it is a framework that is used by the organization

for estimating the product cost in order to control the costs, valuing the inventories,

analysis and profitability

Inventory management system – it combines use of the software, mobile devices

barcode printers and barcode scanners for streamlining the inventory management.

Job costing system – it involves the procedure for accumulating the information

regarding costs related to particular service job or production.

Principles of management accounting

Resource utilization – management accounting ensures appropriate utilization of the

resources available with the company. This is important as some of the resources are

available in excess whereas some are available scarcely. Hence, the available

resources shall be used effectively.

Uncontrollable and controllable cost – based on the controllability costs are

segregated into uncontrollable and controllable costs. As the uncontrollable costs

cannot be controlled the management must take the required steps for controlling the

controllable costs.

Designing and compiling – accounting records, information, statements, reports and

future, past or present results shall be designed and compiled for meeting the

requirements of particular business. The management accounting system is designed

in such way that it presents relevant data and assists in compiling (Langfield-Smith et

al. 2017).

Benefits of management accounting

It assists in maximizing the return rate on the capital employed

Business activities of the company are managed in a better way through application

of planning as well as budgeting both

It helps in measuring actual performance as compared to the budgets

It helps in increasing the efficiency of business

It helps in improving the relation among employees and management (Van der Stede

2016)

Types of management accounting systems

Product costing or costing system – it is a framework that is used by the organization

for estimating the product cost in order to control the costs, valuing the inventories,

analysis and profitability

Inventory management system – it combines use of the software, mobile devices

barcode printers and barcode scanners for streamlining the inventory management.

Job costing system – it involves the procedure for accumulating the information

regarding costs related to particular service job or production.

3MANAGEMENT ACCOUNTING PRINCIPLE

Price organizational system – it is mathematical programme used for calculating how

the demand varies at various levels of prices. Further, it combines the data

information on the inventory and costs level for recommending the price that may

improve the profits (Nielsen, Mitchell and Nørreklit 2015).

Various methods used for the purpose of management accounting reports

Job cost reports – it reveals the expenses for particular project that is financed by the

small businesses. They are generally matched with the revenue estimates for

evaluating the profitability (Taylor and Scapens 2016).

Budget reports – it helps the small business owners to analyse the performance and

controlling costs. Estimated budget for the particular period is generally based on

actual expenses from the part years.

Types of costs

Product cost – it is the costs used for creating the product. These costs involve the

direct material, direct labour, factory overhead and supplies of consumable

production. It may also be considered as costs of labour required for delivering

service to the customers (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil 2015)

Prime cost – it is the direct manufacturing costs of an item for the purpose of sale.

Businesses use the prime costs as the method of measuring total cost of production

inputs required for creating the given output. Through analysis of prime cost the

company can set the prices that may yield the desired profits.

Absorption costing Vs marginal costing

Computation of profits – marginal costs uses the profit volume ratio for computing

profit whereas absorption costing considers the fixed costs in product for computing

profit.

Opening and closing stock – as marginal costing focuses on next unit changes in the

opening stock and closing stock does not have any impact on per unit cost. On the

other hand, as absorption costing focuses on each unit changes in the opening stock

and closing stock have its impact on per unit cost (Kihn and Ihantola 2015)

Price organizational system – it is mathematical programme used for calculating how

the demand varies at various levels of prices. Further, it combines the data

information on the inventory and costs level for recommending the price that may

improve the profits (Nielsen, Mitchell and Nørreklit 2015).

Various methods used for the purpose of management accounting reports

Job cost reports – it reveals the expenses for particular project that is financed by the

small businesses. They are generally matched with the revenue estimates for

evaluating the profitability (Taylor and Scapens 2016).

Budget reports – it helps the small business owners to analyse the performance and

controlling costs. Estimated budget for the particular period is generally based on

actual expenses from the part years.

Types of costs

Product cost – it is the costs used for creating the product. These costs involve the

direct material, direct labour, factory overhead and supplies of consumable

production. It may also be considered as costs of labour required for delivering

service to the customers (Lopez-Valeiras, Gomez-Conde and Naranjo-Gil 2015)

Prime cost – it is the direct manufacturing costs of an item for the purpose of sale.

Businesses use the prime costs as the method of measuring total cost of production

inputs required for creating the given output. Through analysis of prime cost the

company can set the prices that may yield the desired profits.

Absorption costing Vs marginal costing

Computation of profits – marginal costs uses the profit volume ratio for computing

profit whereas absorption costing considers the fixed costs in product for computing

profit.

Opening and closing stock – as marginal costing focuses on next unit changes in the

opening stock and closing stock does not have any impact on per unit cost. On the

other hand, as absorption costing focuses on each unit changes in the opening stock

and closing stock have its impact on per unit cost (Kihn and Ihantola 2015)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4MANAGEMENT ACCOUNTING PRINCIPLE

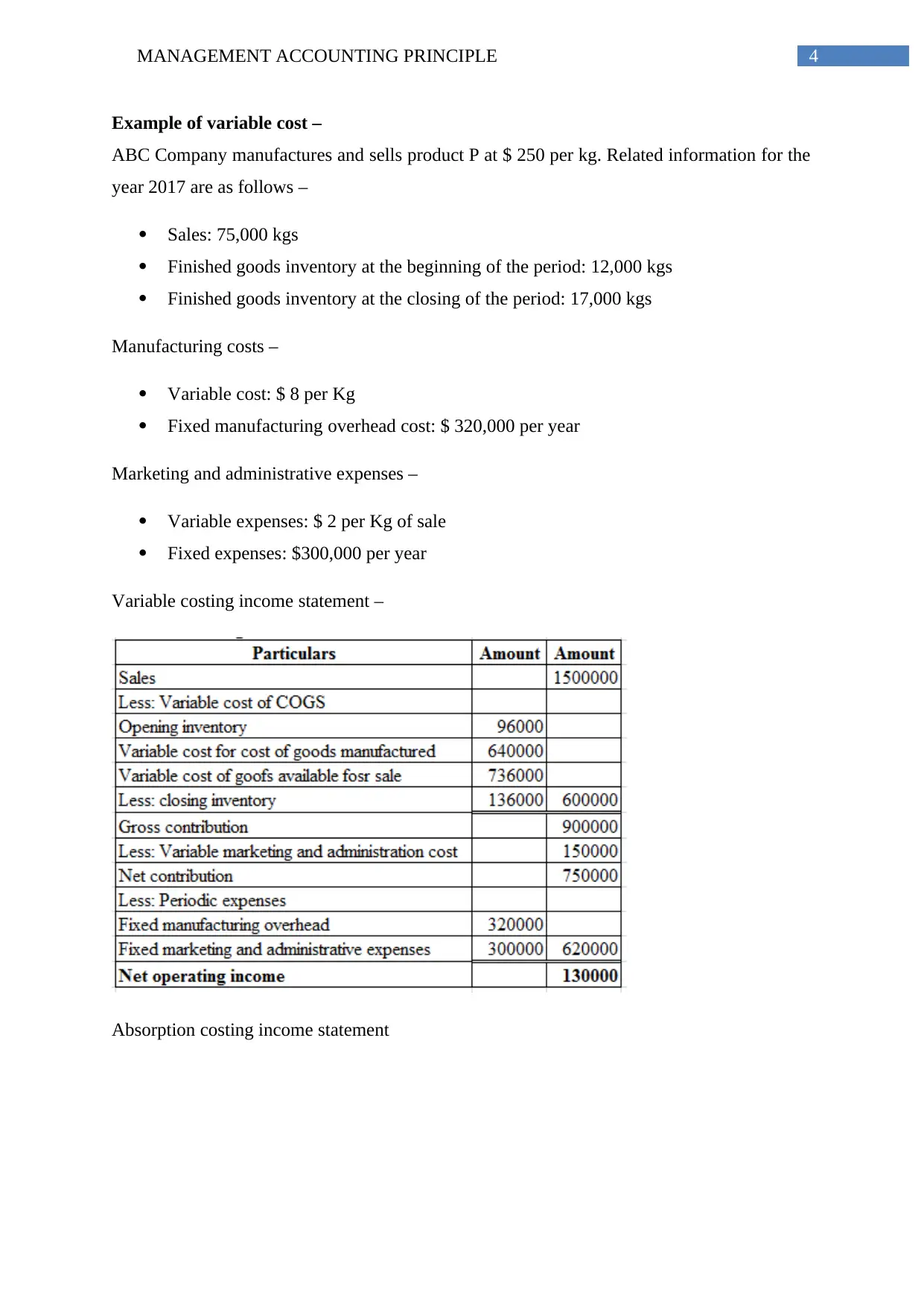

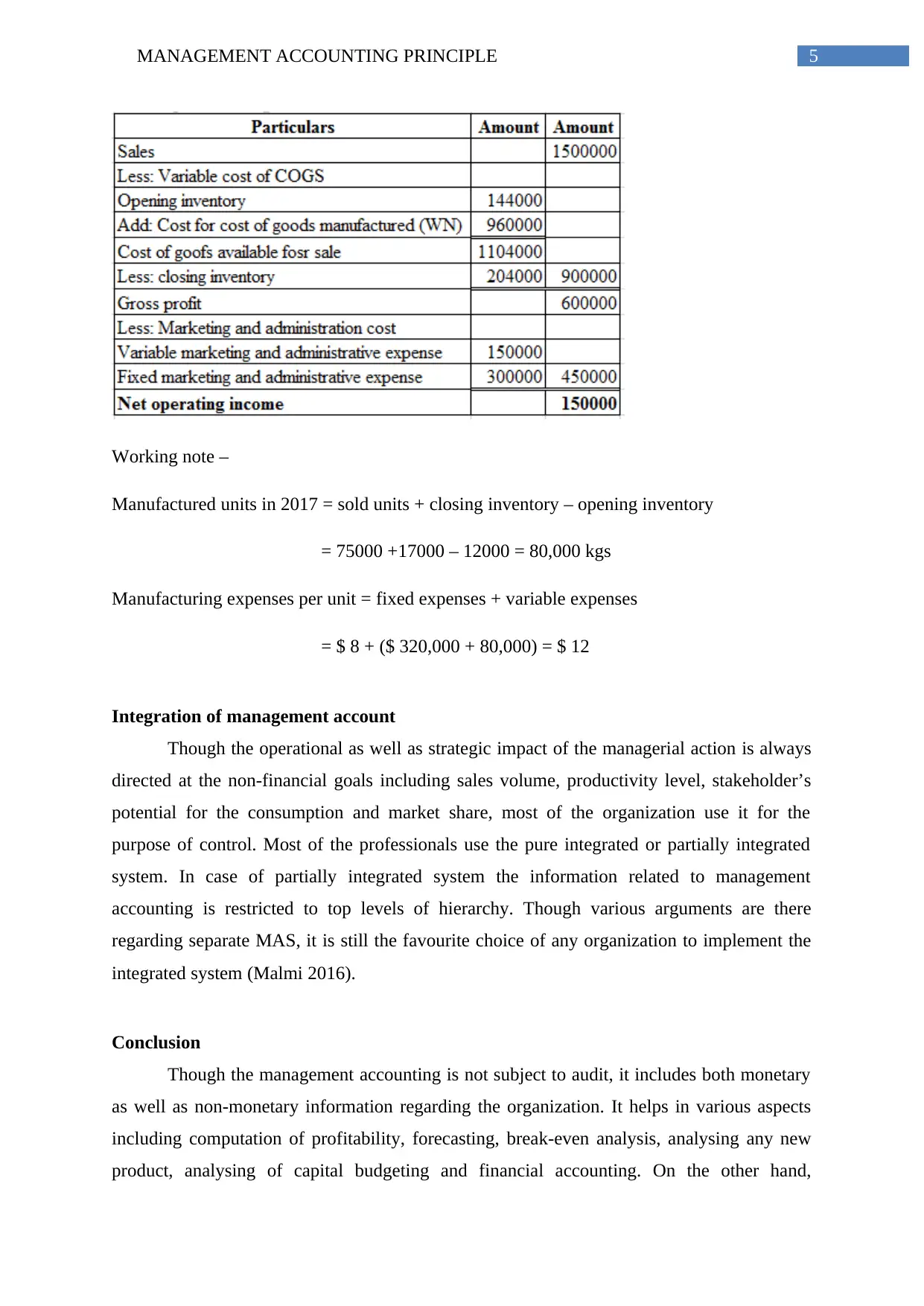

Example of variable cost –

ABC Company manufactures and sells product P at $ 250 per kg. Related information for the

year 2017 are as follows –

Sales: 75,000 kgs

Finished goods inventory at the beginning of the period: 12,000 kgs

Finished goods inventory at the closing of the period: 17,000 kgs

Manufacturing costs –

Variable cost: $ 8 per Kg

Fixed manufacturing overhead cost: $ 320,000 per year

Marketing and administrative expenses –

Variable expenses: $ 2 per Kg of sale

Fixed expenses: $300,000 per year

Variable costing income statement –

Absorption costing income statement

Example of variable cost –

ABC Company manufactures and sells product P at $ 250 per kg. Related information for the

year 2017 are as follows –

Sales: 75,000 kgs

Finished goods inventory at the beginning of the period: 12,000 kgs

Finished goods inventory at the closing of the period: 17,000 kgs

Manufacturing costs –

Variable cost: $ 8 per Kg

Fixed manufacturing overhead cost: $ 320,000 per year

Marketing and administrative expenses –

Variable expenses: $ 2 per Kg of sale

Fixed expenses: $300,000 per year

Variable costing income statement –

Absorption costing income statement

5MANAGEMENT ACCOUNTING PRINCIPLE

Working note –

Manufactured units in 2017 = sold units + closing inventory – opening inventory

= 75000 +17000 – 12000 = 80,000 kgs

Manufacturing expenses per unit = fixed expenses + variable expenses

= $ 8 + ($ 320,000 + 80,000) = $ 12

Integration of management account

Though the operational as well as strategic impact of the managerial action is always

directed at the non-financial goals including sales volume, productivity level, stakeholder’s

potential for the consumption and market share, most of the organization use it for the

purpose of control. Most of the professionals use the pure integrated or partially integrated

system. In case of partially integrated system the information related to management

accounting is restricted to top levels of hierarchy. Though various arguments are there

regarding separate MAS, it is still the favourite choice of any organization to implement the

integrated system (Malmi 2016).

Conclusion

Though the management accounting is not subject to audit, it includes both monetary

as well as non-monetary information regarding the organization. It helps in various aspects

including computation of profitability, forecasting, break-even analysis, analysing any new

product, analysing of capital budgeting and financial accounting. On the other hand,

Working note –

Manufactured units in 2017 = sold units + closing inventory – opening inventory

= 75000 +17000 – 12000 = 80,000 kgs

Manufacturing expenses per unit = fixed expenses + variable expenses

= $ 8 + ($ 320,000 + 80,000) = $ 12

Integration of management account

Though the operational as well as strategic impact of the managerial action is always

directed at the non-financial goals including sales volume, productivity level, stakeholder’s

potential for the consumption and market share, most of the organization use it for the

purpose of control. Most of the professionals use the pure integrated or partially integrated

system. In case of partially integrated system the information related to management

accounting is restricted to top levels of hierarchy. Though various arguments are there

regarding separate MAS, it is still the favourite choice of any organization to implement the

integrated system (Malmi 2016).

Conclusion

Though the management accounting is not subject to audit, it includes both monetary

as well as non-monetary information regarding the organization. It helps in various aspects

including computation of profitability, forecasting, break-even analysis, analysing any new

product, analysing of capital budgeting and financial accounting. On the other hand,

6MANAGEMENT ACCOUNTING PRINCIPLE

management accounting system includes internal system used by the organization for

measuring and evaluating the management process of the organization.

management accounting system includes internal system used by the organization for

measuring and evaluating the management process of the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING PRINCIPLE

Reference

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kihn, L.A. and Ihantola, E.M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management, 12(3), pp.230-255.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H., 2017. Management

accounting: Information for creating and managing value. McGraw-Hill Education

Australia.

Lopez-Valeiras, E., Gomez-Conde, J. and Naranjo-Gil, D., 2015. Sustainable innovation,

management accounting and control systems, and international

performance. Sustainability, 7(3), pp.3479-3492.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research, 31, pp.31-44.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1, pp.

64-82). Elsevier.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Taylor, L.C. and Scapens, R.W., 2016. The role of identity and image in shaping

management accounting change. Accounting, Auditing & Accountability Journal, 29(6),

pp.1075-1099.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research, 31, pp.100-102.

Reference

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management, 32(7-8), pp.414-428.

Kaplan, R.S. and Atkinson, A.A., 2015. Advanced management accounting. PHI Learning.

Kihn, L.A. and Ihantola, E.M., 2015. Approaches to validation and evaluation in qualitative

studies of management accounting. Qualitative Research in Accounting &

Management, 12(3), pp.230-255.

Langfield-Smith, K., Smith, D., Andon, P., Hilton, R. and Thorne, H., 2017. Management

accounting: Information for creating and managing value. McGraw-Hill Education

Australia.

Lopez-Valeiras, E., Gomez-Conde, J. and Naranjo-Gil, D., 2015. Sustainable innovation,

management accounting and control systems, and international

performance. Sustainability, 7(3), pp.3479-3492.

Malmi, T., 2016. Managerialist studies in management accounting: 1990–2014. Management

Accounting Research, 31, pp.31-44.

Messner, M., 2016. Does industry matter? How industry context shapes management

accounting practice. Management Accounting Research, 31, pp.103-111.

Nielsen, L.B., Mitchell, F. and Nørreklit, H., 2015, March. Management accounting and

decision making: Two case studies of outsourcing. In Accounting Forum (Vol. 39, No. 1, pp.

64-82). Elsevier.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it

wiser?. Management Accounting Research, 31, pp.118-122.

Taylor, L.C. and Scapens, R.W., 2016. The role of identity and image in shaping

management accounting change. Accounting, Auditing & Accountability Journal, 29(6),

pp.1075-1099.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research, 31, pp.100-102.

8MANAGEMENT ACCOUNTING PRINCIPLE

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management

accounting adaptability. International Journal of Accounting and Information

Management, 24(1), pp.20-37.

Yigitbasioglu, O., 2016. Firms’ information system characteristics and management

accounting adaptability. International Journal of Accounting and Information

Management, 24(1), pp.20-37.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.