Management Accounting Systems, Techniques & Financial Reporting

VerifiedAdded on 2024/06/07

|21

|4415

|400

Report

AI Summary

This report provides a detailed overview of management accounting principles and techniques used for planning and strategic purposes within a medium-sized manufacturing organization. It explains management accounting systems, their application in an organizational context, and the differences between management and financial accounting. The report covers cost accounting systems, inventory management systems, and job costing systems, illustrating each with examples. It also explains various management report methods, such as cost accounting, budget, financial, accounts receivable, and accounts payable reports, highlighting their importance. Furthermore, the document includes a detailed explanation of absorption and marginal costing techniques, with income statements produced using both methods, and delves into planning tools and techniques for making plans and solving financial problems. Finally, the report discusses the merits and demerits of budgetary control, applications of planning tools in budget preparation, and how management accounting helps organizations overcome financial problems and achieve sustainable success. Desklib provides access to this report and many other solved assignments.

Unit-5 Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction.....................................................................................................................................................................3

Task 1:.............................................................................................................................................................................4

A. Explain management accounting as well as explain the different types of accounting systems and their

requirements in the management with the suitable examples....................................................................................4

B. Explain the methods of the management reports as well as justify their importance in the organizational

context........................................................................................................................................................................6

C. Explain the significance of the management systems in the organizational context as well as explain, the

importance of the management accounting information presented in an understandable manner.............................7

D. Evaluate how management accounting systems and management accounting reporting.....................................8

Is integrated within organizational processes.............................................................................................................8

Task 2:.............................................................................................................................................................................9

A. 1) Explain absorption costing and marginal costing methods...............................................................................9

2) Prepare an Income Statement based on the calculations of costs as per the information given

above using both a) absorption costing method and b) marginal costing method...................................................10

Income statement as per marginal costing:..............................................................................................................10

B. Using Break-Even formula, calculate:.................................................................................................................12

C. Apply the range of management accounting techniques and produce appropriate financial reporting documents.

..................................................................................................................................................................................13

D. Produce financial reports that accurately apply and interpret the data for the business activities......................14

Task 3;...........................................................................................................................................................................15

A. Explain the merits and demerits of the planning tools of the budgetary control.................................................15

B. Explain the applications of the planning tools in preparation of budgets........................................................17

C. Explain with examples how much our organization is different in adapting the management accounting and

responding to the financial problems.......................................................................................................................17

D. Explain the management accounting techniques that are responsible in overcoming the financial problems that

helps in sustainable success......................................................................................................................................17

E. Ways or methods in which various planning tools can help or assist an organization to....................................18

Solve financial problems so that it can achieve sustainable success are as follows:...............................................18

Conclusion;...................................................................................................................................................................19

References:....................................................................................................................................................................20

2

Introduction.....................................................................................................................................................................3

Task 1:.............................................................................................................................................................................4

A. Explain management accounting as well as explain the different types of accounting systems and their

requirements in the management with the suitable examples....................................................................................4

B. Explain the methods of the management reports as well as justify their importance in the organizational

context........................................................................................................................................................................6

C. Explain the significance of the management systems in the organizational context as well as explain, the

importance of the management accounting information presented in an understandable manner.............................7

D. Evaluate how management accounting systems and management accounting reporting.....................................8

Is integrated within organizational processes.............................................................................................................8

Task 2:.............................................................................................................................................................................9

A. 1) Explain absorption costing and marginal costing methods...............................................................................9

2) Prepare an Income Statement based on the calculations of costs as per the information given

above using both a) absorption costing method and b) marginal costing method...................................................10

Income statement as per marginal costing:..............................................................................................................10

B. Using Break-Even formula, calculate:.................................................................................................................12

C. Apply the range of management accounting techniques and produce appropriate financial reporting documents.

..................................................................................................................................................................................13

D. Produce financial reports that accurately apply and interpret the data for the business activities......................14

Task 3;...........................................................................................................................................................................15

A. Explain the merits and demerits of the planning tools of the budgetary control.................................................15

B. Explain the applications of the planning tools in preparation of budgets........................................................17

C. Explain with examples how much our organization is different in adapting the management accounting and

responding to the financial problems.......................................................................................................................17

D. Explain the management accounting techniques that are responsible in overcoming the financial problems that

helps in sustainable success......................................................................................................................................17

E. Ways or methods in which various planning tools can help or assist an organization to....................................18

Solve financial problems so that it can achieve sustainable success are as follows:...............................................18

Conclusion;...................................................................................................................................................................19

References:....................................................................................................................................................................20

2

Introduction

The preparation of following report is concerned with obtaining a detailed knowledge about the

management accounting principles and techniques that can be used in an organisation for

planning and strategically purposes. The use of management accounting traditionally was limited

for the purpose of presenting information to the management but in modern business

environment they same has been used for producing value added reports for business managers

and assisting them in taking critical business decisions. The report will involve an explanation

regarding the management accounting systems and their application in an organizational context.

The organisation selected here will be a medium sized organisation which is operating in

manufacturing industry. The report will include the detailed explanation regarding the two

techniques of costing covering absorption costing and marginal costing. The income statements

will be produced based on these techniques. Further the report will also include a detailed

knowledge about the various planning tools and techniques that can be used in an enterprise for

making plans and solving the financial problems.

3

The preparation of following report is concerned with obtaining a detailed knowledge about the

management accounting principles and techniques that can be used in an organisation for

planning and strategically purposes. The use of management accounting traditionally was limited

for the purpose of presenting information to the management but in modern business

environment they same has been used for producing value added reports for business managers

and assisting them in taking critical business decisions. The report will involve an explanation

regarding the management accounting systems and their application in an organizational context.

The organisation selected here will be a medium sized organisation which is operating in

manufacturing industry. The report will include the detailed explanation regarding the two

techniques of costing covering absorption costing and marginal costing. The income statements

will be produced based on these techniques. Further the report will also include a detailed

knowledge about the various planning tools and techniques that can be used in an enterprise for

making plans and solving the financial problems.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1:

A. Explain management accounting as well as explain the different types of accounting

systems and their requirements in the management with the suitable examples.

The term management accounting refers to the set of accounting conducted in an enterprise for

producing appropriate reports that can be used by management in decision making purposes. The

process of management accounting involves identifying the critical sources of information and

recording and presenting the data in a report format in order to provide accurate and timely

information to the management. The information will thus be utilized for the purpose of making

economic decision in the company. The system of management accounting will be used in a

manufacturing organisation in order to keep record of manufacturing operations of the company

and analysing the efficiency and effectiveness with which they are conducted (Charles, et. al.,

2017).

Difference between management accounting and financial accounting:

Objective – The objective of management accounting is to assist business managers in taking

significant decision regarding the company. The reports will be utilized for evaluating and

analysing the performance of company and the decision will be taken accordingly. However

financial accounting is the form of accounting in which financial reports are presented to the

investors and other outsiders in order to assist them in taking their investment decisions.

Users – The users which are concerned with management accounting reports are associated with

internal people of the organisation consisting of employees, managers etc. whereas the financial

accounting reports are used by external people of organisation consisting of investors, creditors

etc.

Frequency of reporting – The management accounting reports can be prepared at the will of the

management and there is no boundation for preparing the same at a regular interval if time.

However the financial reports are subjected to regulations in which the periodical reports must be

prepared by the management in order to present the same before users (Carley and Christie,

2017).

4

A. Explain management accounting as well as explain the different types of accounting

systems and their requirements in the management with the suitable examples.

The term management accounting refers to the set of accounting conducted in an enterprise for

producing appropriate reports that can be used by management in decision making purposes. The

process of management accounting involves identifying the critical sources of information and

recording and presenting the data in a report format in order to provide accurate and timely

information to the management. The information will thus be utilized for the purpose of making

economic decision in the company. The system of management accounting will be used in a

manufacturing organisation in order to keep record of manufacturing operations of the company

and analysing the efficiency and effectiveness with which they are conducted (Charles, et. al.,

2017).

Difference between management accounting and financial accounting:

Objective – The objective of management accounting is to assist business managers in taking

significant decision regarding the company. The reports will be utilized for evaluating and

analysing the performance of company and the decision will be taken accordingly. However

financial accounting is the form of accounting in which financial reports are presented to the

investors and other outsiders in order to assist them in taking their investment decisions.

Users – The users which are concerned with management accounting reports are associated with

internal people of the organisation consisting of employees, managers etc. whereas the financial

accounting reports are used by external people of organisation consisting of investors, creditors

etc.

Frequency of reporting – The management accounting reports can be prepared at the will of the

management and there is no boundation for preparing the same at a regular interval if time.

However the financial reports are subjected to regulations in which the periodical reports must be

prepared by the management in order to present the same before users (Carley and Christie,

2017).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Different types of management accounting systems.

Cost Accounting system – The cost accounting system refers to the process of accounting in

which cost records and cost items are maintained in a manner that will assist the management in

making decision regarding the cost control and cost management. The process of cost accounting

is concerned with classification of each cost activity concerned with the manufacturing

operations of an enterprise and analyzing each activity for the purpose of controlling. There are

various systems associated with cost accounting and these are presented below:

Actual costing – The actual costing system is a costing process in which real costs are

identified and recorded for the purpose of calculating unit cost of product. The actual

overheads incurred for the product are considered in this process (Charles, et. al.,

2017).

Example – In a manufacturing unit the cost associated with direct material acquired

by the company will be recorded at the purchase price paid by the company.

Normal costing – The normal costing system takes into account the normal or

budgeted cost of production that has to be incurred in the manufacturing of products.

Example – The budgeted cost of direct material will be £2000 for 100 units of output

and therefore £2000 will be taken to value the unit cost of product.

Standard costing – The standard costing process involves the determination of

standard cost that has to be incurred in the manufacturing operations and the same are

utilized for the purpose of valuing the unit cost of product.

Example – In a manufacturing unit the standard cost for producing a unit is direct

material £10, direct labour £5 and other overheads £5, therefore the unit cost of

product as per standard costing method will be £20.

Inventory management system – The inventory management system of management

accounting is associated with recognizing the type of costs that has to be incurred in

manufacturing the inventory of the company and these will include raw materials utilized and

5

Cost Accounting system – The cost accounting system refers to the process of accounting in

which cost records and cost items are maintained in a manner that will assist the management in

making decision regarding the cost control and cost management. The process of cost accounting

is concerned with classification of each cost activity concerned with the manufacturing

operations of an enterprise and analyzing each activity for the purpose of controlling. There are

various systems associated with cost accounting and these are presented below:

Actual costing – The actual costing system is a costing process in which real costs are

identified and recorded for the purpose of calculating unit cost of product. The actual

overheads incurred for the product are considered in this process (Charles, et. al.,

2017).

Example – In a manufacturing unit the cost associated with direct material acquired

by the company will be recorded at the purchase price paid by the company.

Normal costing – The normal costing system takes into account the normal or

budgeted cost of production that has to be incurred in the manufacturing of products.

Example – The budgeted cost of direct material will be £2000 for 100 units of output

and therefore £2000 will be taken to value the unit cost of product.

Standard costing – The standard costing process involves the determination of

standard cost that has to be incurred in the manufacturing operations and the same are

utilized for the purpose of valuing the unit cost of product.

Example – In a manufacturing unit the standard cost for producing a unit is direct

material £10, direct labour £5 and other overheads £5, therefore the unit cost of

product as per standard costing method will be £20.

Inventory management system – The inventory management system of management

accounting is associated with recognizing the type of costs that has to be incurred in

manufacturing the inventory of the company and these will include raw materials utilized and

5

other costs. The inventory of the company can be in the form of work in progress or finished

goods of the company. There are various kinds of inventory systems utilized in the companies

some of which are explained below:

FIFO – The first in first out method of recording inventory is associated with the process

in which the oldest inventory is considered first to calculate the cost of goods sold. The

same helps in obtaining the actual cost incurred.

LIFO – The last in first put method considers the latest inventory purchased to value the

unit cost of product and therefore the updated cost of obtained.

JIT – Just in time is the inventory system in which the orders for purchases are placed as

soon as inventory becomes out of stock for the company (Carley and Christie, 2017).

Job costing system – The job costing system is the accounting system in which individual jobs

are identified which are received form customers and the cost records are maintained for each of

the job. The job costing system is not as same as the process costing system.

Example – In a manufacturing unit the job can be related with manufacturing the single product

and identifying the cost related with materials, labour and other overheads for producing the

product.

B. Explain the methods of the management reports as well as justify their importance in

the organizational context.

The different types of reports along with their importance are presented below:

Cost accounting report – The cost accounting reports contain the information about cost data of

the company and helps in classifying the cost according to nature and level of activity of

performed. The cost accounting reports is essential for presenting the right cost information

before the managers of company (Goetsch & Davis, 2014).

Budget report – The budget report will be concerned with presenting a statement about the cost

and revenues to be achieved by the company based on past and predicted data of the company.

The same helps in alloctai8ng the resources and controlling the activities in a manufacturing

organisation.

6

goods of the company. There are various kinds of inventory systems utilized in the companies

some of which are explained below:

FIFO – The first in first out method of recording inventory is associated with the process

in which the oldest inventory is considered first to calculate the cost of goods sold. The

same helps in obtaining the actual cost incurred.

LIFO – The last in first put method considers the latest inventory purchased to value the

unit cost of product and therefore the updated cost of obtained.

JIT – Just in time is the inventory system in which the orders for purchases are placed as

soon as inventory becomes out of stock for the company (Carley and Christie, 2017).

Job costing system – The job costing system is the accounting system in which individual jobs

are identified which are received form customers and the cost records are maintained for each of

the job. The job costing system is not as same as the process costing system.

Example – In a manufacturing unit the job can be related with manufacturing the single product

and identifying the cost related with materials, labour and other overheads for producing the

product.

B. Explain the methods of the management reports as well as justify their importance in

the organizational context.

The different types of reports along with their importance are presented below:

Cost accounting report – The cost accounting reports contain the information about cost data of

the company and helps in classifying the cost according to nature and level of activity of

performed. The cost accounting reports is essential for presenting the right cost information

before the managers of company (Goetsch & Davis, 2014).

Budget report – The budget report will be concerned with presenting a statement about the cost

and revenues to be achieved by the company based on past and predicted data of the company.

The same helps in alloctai8ng the resources and controlling the activities in a manufacturing

organisation.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial reports – The financial reports consists of income statements, balance sheet and cash

flow statement which can be helpful in analyzing the financial performance and position of the

company. The same will help the users in decision making process.

Accounts receivable report – The accounts receivable report is the statement showing the

balances of receivables for the company and helps in managing the debtors of the company by

setting an appropriate debtor policy. The report will help in speeding up the collection process

and avoid any ambiguities in collection.

Accounts payable reports – The accounts payable report will be associated with managing the

payables of the company and establishing an appropriate payment policy of the company. The

report will help in ensuring that the data is reliable and transparent (Goetsch & Davis, 2014).

C. Explain the significance of the management systems in the organizational context as well

as explain, the importance of the management accounting information presented in an

understandable manner.

There is a significant importance of management accounting information for a medium sized

enterprise working in a manufacturing sector as the information will be required to ensure the

quality of the product and it will be helpful in analysing the efficiency and effectiveness with

which the operations are performed in an enterprise. The benefits are presented below:

The decision can be taken for either making the product or purchasing the [product by

analysing the manufacturing cost and purchasing cost for the company.

The reports and the data presented will help in understanding the performance variances

and this will help the company in controlling the performance to an acceptable level.

The same will help in controlling the cost and evaluating the rate of return that the

production and selling of product is achieving for the company.

The future results can be forecasted by the company and based on that allocation of

resources will be made correctly.

7

flow statement which can be helpful in analyzing the financial performance and position of the

company. The same will help the users in decision making process.

Accounts receivable report – The accounts receivable report is the statement showing the

balances of receivables for the company and helps in managing the debtors of the company by

setting an appropriate debtor policy. The report will help in speeding up the collection process

and avoid any ambiguities in collection.

Accounts payable reports – The accounts payable report will be associated with managing the

payables of the company and establishing an appropriate payment policy of the company. The

report will help in ensuring that the data is reliable and transparent (Goetsch & Davis, 2014).

C. Explain the significance of the management systems in the organizational context as well

as explain, the importance of the management accounting information presented in an

understandable manner.

There is a significant importance of management accounting information for a medium sized

enterprise working in a manufacturing sector as the information will be required to ensure the

quality of the product and it will be helpful in analysing the efficiency and effectiveness with

which the operations are performed in an enterprise. The benefits are presented below:

The decision can be taken for either making the product or purchasing the [product by

analysing the manufacturing cost and purchasing cost for the company.

The reports and the data presented will help in understanding the performance variances

and this will help the company in controlling the performance to an acceptable level.

The same will help in controlling the cost and evaluating the rate of return that the

production and selling of product is achieving for the company.

The future results can be forecasted by the company and based on that allocation of

resources will be made correctly.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

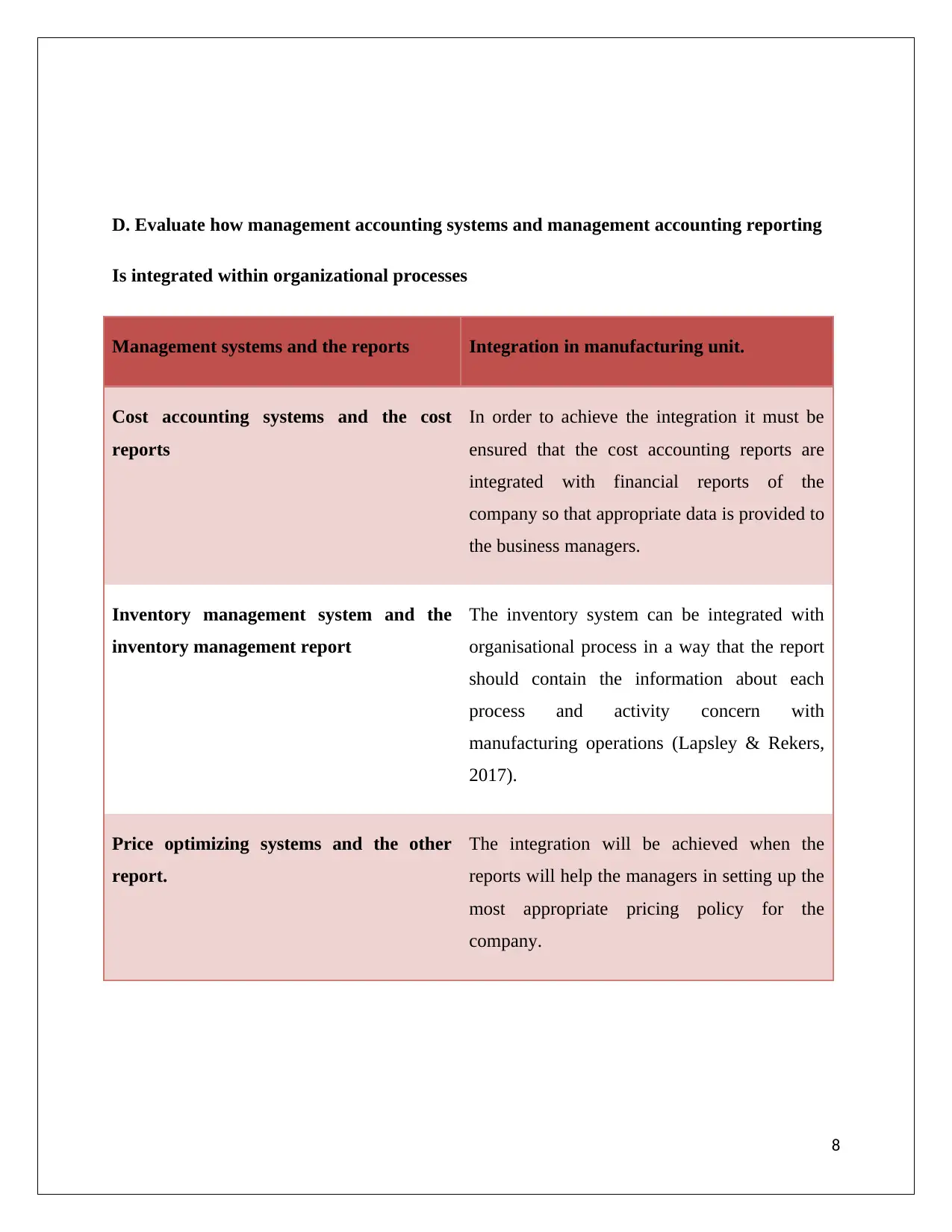

D. Evaluate how management accounting systems and management accounting reporting

Is integrated within organizational processes

Management systems and the reports Integration in manufacturing unit.

Cost accounting systems and the cost

reports

In order to achieve the integration it must be

ensured that the cost accounting reports are

integrated with financial reports of the

company so that appropriate data is provided to

the business managers.

Inventory management system and the

inventory management report

The inventory system can be integrated with

organisational process in a way that the report

should contain the information about each

process and activity concern with

manufacturing operations (Lapsley & Rekers,

2017).

Price optimizing systems and the other

report.

The integration will be achieved when the

reports will help the managers in setting up the

most appropriate pricing policy for the

company.

8

Is integrated within organizational processes

Management systems and the reports Integration in manufacturing unit.

Cost accounting systems and the cost

reports

In order to achieve the integration it must be

ensured that the cost accounting reports are

integrated with financial reports of the

company so that appropriate data is provided to

the business managers.

Inventory management system and the

inventory management report

The inventory system can be integrated with

organisational process in a way that the report

should contain the information about each

process and activity concern with

manufacturing operations (Lapsley & Rekers,

2017).

Price optimizing systems and the other

report.

The integration will be achieved when the

reports will help the managers in setting up the

most appropriate pricing policy for the

company.

8

Task 2:

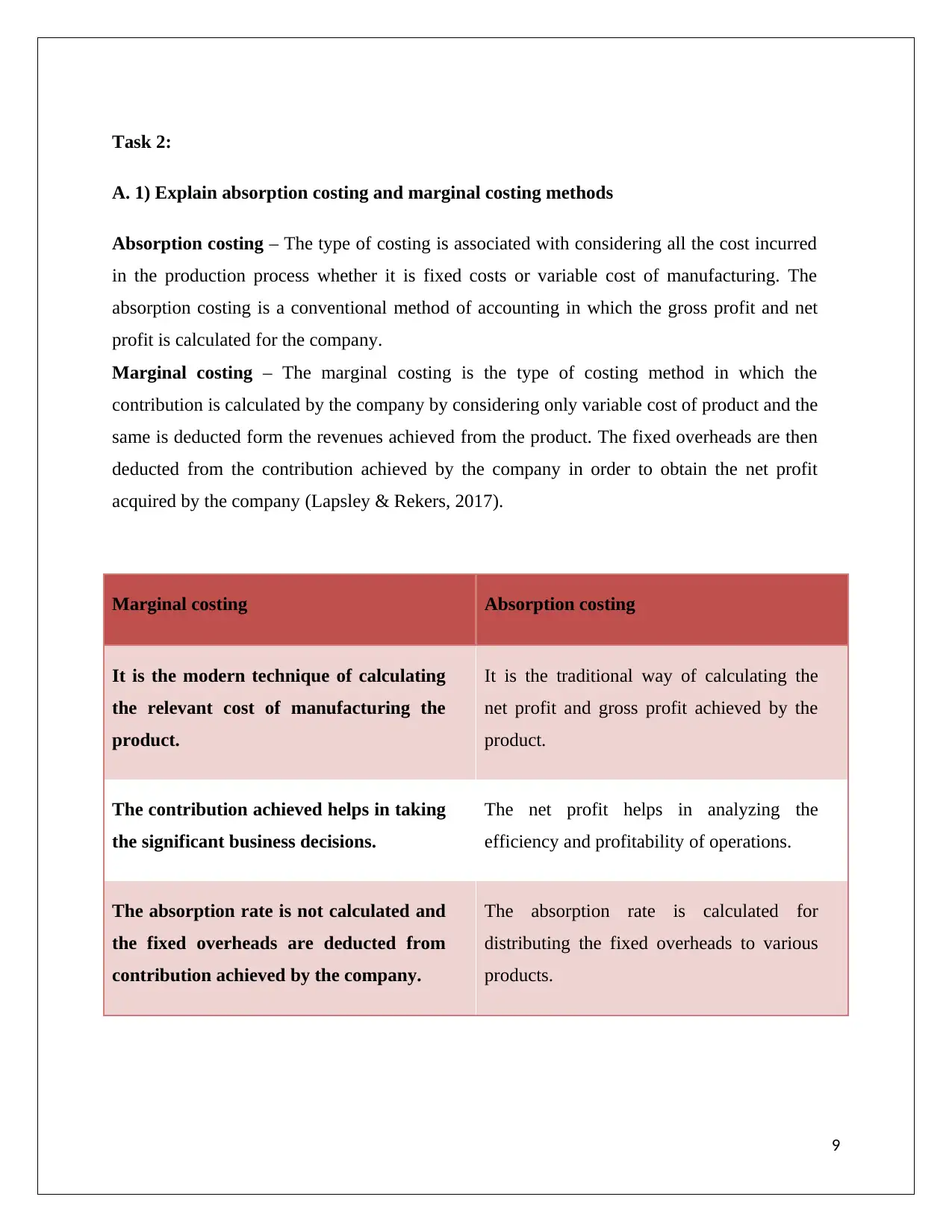

A. 1) Explain absorption costing and marginal costing methods

Absorption costing – The type of costing is associated with considering all the cost incurred

in the production process whether it is fixed costs or variable cost of manufacturing. The

absorption costing is a conventional method of accounting in which the gross profit and net

profit is calculated for the company.

Marginal costing – The marginal costing is the type of costing method in which the

contribution is calculated by the company by considering only variable cost of product and the

same is deducted form the revenues achieved from the product. The fixed overheads are then

deducted from the contribution achieved by the company in order to obtain the net profit

acquired by the company (Lapsley & Rekers, 2017).

Marginal costing Absorption costing

It is the modern technique of calculating

the relevant cost of manufacturing the

product.

It is the traditional way of calculating the

net profit and gross profit achieved by the

product.

The contribution achieved helps in taking

the significant business decisions.

The net profit helps in analyzing the

efficiency and profitability of operations.

The absorption rate is not calculated and

the fixed overheads are deducted from

contribution achieved by the company.

The absorption rate is calculated for

distributing the fixed overheads to various

products.

9

A. 1) Explain absorption costing and marginal costing methods

Absorption costing – The type of costing is associated with considering all the cost incurred

in the production process whether it is fixed costs or variable cost of manufacturing. The

absorption costing is a conventional method of accounting in which the gross profit and net

profit is calculated for the company.

Marginal costing – The marginal costing is the type of costing method in which the

contribution is calculated by the company by considering only variable cost of product and the

same is deducted form the revenues achieved from the product. The fixed overheads are then

deducted from the contribution achieved by the company in order to obtain the net profit

acquired by the company (Lapsley & Rekers, 2017).

Marginal costing Absorption costing

It is the modern technique of calculating

the relevant cost of manufacturing the

product.

It is the traditional way of calculating the

net profit and gross profit achieved by the

product.

The contribution achieved helps in taking

the significant business decisions.

The net profit helps in analyzing the

efficiency and profitability of operations.

The absorption rate is not calculated and

the fixed overheads are deducted from

contribution achieved by the company.

The absorption rate is calculated for

distributing the fixed overheads to various

products.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2) Prepare an Income Statement based on the calculations of costs as per the information

given above using both a) absorption costing method and b) marginal costing method.

Income statement as per marginal costing:

Income statement as per marginal costing

Particular Amount (₤)

Production units 800

Sales units 600

Sales @55 per unit 33000

Opening stock

Production cost: Variable

Direct material cost@ £7 per unit 5600

Direct labour @£ 6 per unit 4800

Other variable expenses @ £3 per unit 2400

Total Variable production cost 12800

Less: Closing stock 3200

Cost of goods sold 9600

Contribution 23400

Fixed Production Overhead 3200

Fixed Administration cost 1200

Fixed selling cost 1500

Net profit before tax 17500

11

given above using both a) absorption costing method and b) marginal costing method.

Income statement as per marginal costing:

Income statement as per marginal costing

Particular Amount (₤)

Production units 800

Sales units 600

Sales @55 per unit 33000

Opening stock

Production cost: Variable

Direct material cost@ £7 per unit 5600

Direct labour @£ 6 per unit 4800

Other variable expenses @ £3 per unit 2400

Total Variable production cost 12800

Less: Closing stock 3200

Cost of goods sold 9600

Contribution 23400

Fixed Production Overhead 3200

Fixed Administration cost 1200

Fixed selling cost 1500

Net profit before tax 17500

11

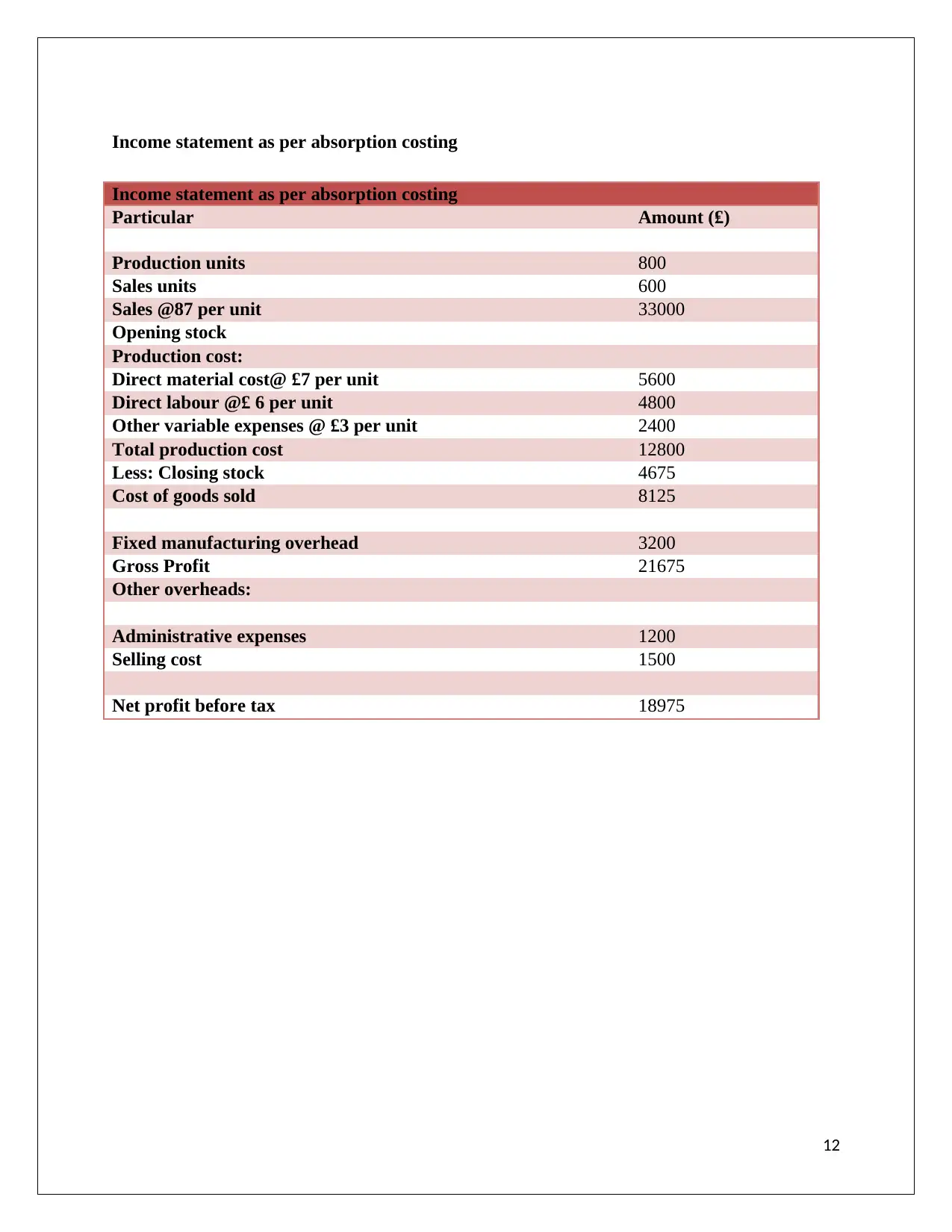

Income statement as per absorption costing

Income statement as per absorption costing

Particular Amount (₤)

Production units 800

Sales units 600

Sales @87 per unit 33000

Opening stock

Production cost:

Direct material cost@ £7 per unit 5600

Direct labour @£ 6 per unit 4800

Other variable expenses @ £3 per unit 2400

Total production cost 12800

Less: Closing stock 4675

Cost of goods sold 8125

Fixed manufacturing overhead 3200

Gross Profit 21675

Other overheads:

Administrative expenses 1200

Selling cost 1500

Net profit before tax 18975

12

Income statement as per absorption costing

Particular Amount (₤)

Production units 800

Sales units 600

Sales @87 per unit 33000

Opening stock

Production cost:

Direct material cost@ £7 per unit 5600

Direct labour @£ 6 per unit 4800

Other variable expenses @ £3 per unit 2400

Total production cost 12800

Less: Closing stock 4675

Cost of goods sold 8125

Fixed manufacturing overhead 3200

Gross Profit 21675

Other overheads:

Administrative expenses 1200

Selling cost 1500

Net profit before tax 18975

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.