Management Accounting Principles and Planning Tools for Budgetary Control

VerifiedAdded on 2023/06/14

|14

|3557

|386

AI Summary

This report discusses the role of management accounting in making business decisions, including the principles of management accounting, different types of management accounting systems, methods of management accounting reporting, benefits of management accounting systems, and their application within the organization. It also compares three planning tools for budgetary control with their advantages and disadvantages. The report includes a portfolio of calculations for financial statements and ways to implement management accounting within an enterprise.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT

ACCOUNTING PRINCIPLES

ACCOUNTING PRINCIPLES

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task-1..............................................................................................................................................3

Introduction to management accounting and its principals.........................................................3

The essential requirement of different types management accounting systems..........................3

Different methods of management accounting reporting............................................................4

Evaluation of the benefits of management accounting systems and its application within the

organization.................................................................................................................................5

Management accounting systems and management accounting reporting integrated within

organizational processes..............................................................................................................5

Part B...........................................................................................................................................5

Task-2..............................................................................................................................................7

Comparison of three planning tools for budgetary control with their advantages and

disadvantages...............................................................................................................................7

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Task-1..............................................................................................................................................3

Introduction to management accounting and its principals.........................................................3

The essential requirement of different types management accounting systems..........................3

Different methods of management accounting reporting............................................................4

Evaluation of the benefits of management accounting systems and its application within the

organization.................................................................................................................................5

Management accounting systems and management accounting reporting integrated within

organizational processes..............................................................................................................5

Part B...........................................................................................................................................5

Task-2..............................................................................................................................................7

Comparison of three planning tools for budgetary control with their advantages and

disadvantages...............................................................................................................................7

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION

A process of accounting by which organizations prepare financial statements that helps

the external users as well as internal users of accounting to make financial decisions is known as

management accounting. This report will be based on the case study of JM. It is a company

headquartered in London, United Kingdom and deals in products related to clothing and apparel

This report is prepared in order to analyse the use of planning tools and the role of management

accounting in making business decisions. This project will include a portfolio of calculations for

financial statements and further find ways to implement management accounting within an

enterprise.

MAIN BODY

Task-1

Part A

Introduction to management accounting and its principals

The process of determining, measuring, analysing and presenting financial information to

the internal management of an organization is known as management accounting. This financial

information assists the internal management to make business decisions for the purpose of

achieving organizational objectives (Ameen, Ahmed, and Abd Hafez, 2018.). The concept of

management accounting follows a set of principles which are presentation of unbiased data,

accurate presentation of financial statements, consistency, stability and punctuality. The

principle of unbiased data states that the information presented in the statement should be

relevant and accurate for the users. It should not focus on achieving personal objectives, rather it

must help the company in making business decisions. The methods and principals of accounting

followed for the preparation of the statements should be consistent throughout. The principle of

punctuality states that the financial information should be presented to its users on time so that

the management can make necessary decisions on time without being delayed.

The essential requirement of different types management accounting systems

The need of the different types of management accounting systems have been explained below:

Cost accounting

A process of accounting by which organizations prepare financial statements that helps

the external users as well as internal users of accounting to make financial decisions is known as

management accounting. This report will be based on the case study of JM. It is a company

headquartered in London, United Kingdom and deals in products related to clothing and apparel

This report is prepared in order to analyse the use of planning tools and the role of management

accounting in making business decisions. This project will include a portfolio of calculations for

financial statements and further find ways to implement management accounting within an

enterprise.

MAIN BODY

Task-1

Part A

Introduction to management accounting and its principals

The process of determining, measuring, analysing and presenting financial information to

the internal management of an organization is known as management accounting. This financial

information assists the internal management to make business decisions for the purpose of

achieving organizational objectives (Ameen, Ahmed, and Abd Hafez, 2018.). The concept of

management accounting follows a set of principles which are presentation of unbiased data,

accurate presentation of financial statements, consistency, stability and punctuality. The

principle of unbiased data states that the information presented in the statement should be

relevant and accurate for the users. It should not focus on achieving personal objectives, rather it

must help the company in making business decisions. The methods and principals of accounting

followed for the preparation of the statements should be consistent throughout. The principle of

punctuality states that the financial information should be presented to its users on time so that

the management can make necessary decisions on time without being delayed.

The essential requirement of different types management accounting systems

The need of the different types of management accounting systems have been explained below:

Cost accounting

Cost accounting is a part of management accounting used by the company Capital

Joinery. It helps the company in determining and segregating different costs associated with the

process of manufacturing and production (Maheshwari, Maheshwari, and Maheshwari, 2021).

With the help of the cost accounting, the company can find out costs associated with different

units and take necessary steps in order to control the cost and increase the profitability of the

company.

Inventory management system

The inventory management system is a way through which companies keep a track of

their inventory. There are various methods of inventory management followed by Capital Joinery

such as FIFO, LIFO, AVCO (Azudin, and Mansor, 2018.). These methods help the company in

identifying the need of inventory within the organization and ordering whenever required.

Job costing system

Job costing system of management accounting is used to identify the cost associated with

a specific project or job. The method of accounting is implemented within the capital joinery in

order to identify the accurate costs related to individual projects and take necessary actions

accordingly.

Different methods of management accounting reporting

Budgeting report

A budgeting report is projected report which helps the company in comparing the actual

expenditure with the forecasted budget. The method of management reporting is used by Capital

joinery for controlling cost and expenditure incurred by comparing their actual expenditure with

budgeted one (Pedroso, and Gomes, 2020).

Accounts receivables aging

The company Capital Joinery makes use of accounts receivables aging reporting for the

purpose of achieving the best financial results by managing the cash flow of the organization.

This report helps an enterprise in keeping a track of the debtors and creditors of the company.

Profit and Loss

The preparation of P&L statement by the Capital Joinery also comes under the scope of

management accounting reporting. P&L statement helps in identifying the expenditure incurred

and the profit earned within a specified period (Cescon, Costantini, and Grassetti,2019).

Joinery. It helps the company in determining and segregating different costs associated with the

process of manufacturing and production (Maheshwari, Maheshwari, and Maheshwari, 2021).

With the help of the cost accounting, the company can find out costs associated with different

units and take necessary steps in order to control the cost and increase the profitability of the

company.

Inventory management system

The inventory management system is a way through which companies keep a track of

their inventory. There are various methods of inventory management followed by Capital Joinery

such as FIFO, LIFO, AVCO (Azudin, and Mansor, 2018.). These methods help the company in

identifying the need of inventory within the organization and ordering whenever required.

Job costing system

Job costing system of management accounting is used to identify the cost associated with

a specific project or job. The method of accounting is implemented within the capital joinery in

order to identify the accurate costs related to individual projects and take necessary actions

accordingly.

Different methods of management accounting reporting

Budgeting report

A budgeting report is projected report which helps the company in comparing the actual

expenditure with the forecasted budget. The method of management reporting is used by Capital

joinery for controlling cost and expenditure incurred by comparing their actual expenditure with

budgeted one (Pedroso, and Gomes, 2020).

Accounts receivables aging

The company Capital Joinery makes use of accounts receivables aging reporting for the

purpose of achieving the best financial results by managing the cash flow of the organization.

This report helps an enterprise in keeping a track of the debtors and creditors of the company.

Profit and Loss

The preparation of P&L statement by the Capital Joinery also comes under the scope of

management accounting reporting. P&L statement helps in identifying the expenditure incurred

and the profit earned within a specified period (Cescon, Costantini, and Grassetti,2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Evaluation of the benefits of management accounting systems and its application within the

organization

Benefits of cost accounting includes ascertaining direct as well as indirect cost, improving cost

efficiency by controlling extra costs incurred. It helps the company in formulating targets for

different heads by considering all costs associated with the business.

The benefits of job costing consists of evaluating the profitability of each job individually and

providing a base for calculating the cost of jobs of similar nature (Zahid, and Vagif, 2020).

Management accounting systems and management accounting reporting integrated within

organizational processes.

The systems of management accounting and management accounting reporting makes

use of different sorts of data for increasing the effectiveness of the organizational performance. It

includes qualitative as well as quantitative information to help the management in making

informed business decisions. With the help of management accounting systems and its reporting,

the company Capital Joinery works on continuously improving the quality of goods and services

provided by increasing the productivity and reducing the waste (Yakupova, 2019). These

methods and reporting further helps the company with quality management and cost

management within the organization.

Part B

Cost per unit absorption costing

Opening stock 450000

Manufacturing cost 2760000

Closing stock 1000000 2210000

Fixed expense of manufacturing 3040000

Administrative expense 10500

Selling and distribution expense 10000

Fixed expense 100000

Salaries 200000

Depreciation 21000

Total cost 5591500

organization

Benefits of cost accounting includes ascertaining direct as well as indirect cost, improving cost

efficiency by controlling extra costs incurred. It helps the company in formulating targets for

different heads by considering all costs associated with the business.

The benefits of job costing consists of evaluating the profitability of each job individually and

providing a base for calculating the cost of jobs of similar nature (Zahid, and Vagif, 2020).

Management accounting systems and management accounting reporting integrated within

organizational processes.

The systems of management accounting and management accounting reporting makes

use of different sorts of data for increasing the effectiveness of the organizational performance. It

includes qualitative as well as quantitative information to help the management in making

informed business decisions. With the help of management accounting systems and its reporting,

the company Capital Joinery works on continuously improving the quality of goods and services

provided by increasing the productivity and reducing the waste (Yakupova, 2019). These

methods and reporting further helps the company with quality management and cost

management within the organization.

Part B

Cost per unit absorption costing

Opening stock 450000

Manufacturing cost 2760000

Closing stock 1000000 2210000

Fixed expense of manufacturing 3040000

Administrative expense 10500

Selling and distribution expense 10000

Fixed expense 100000

Salaries 200000

Depreciation 21000

Total cost 5591500

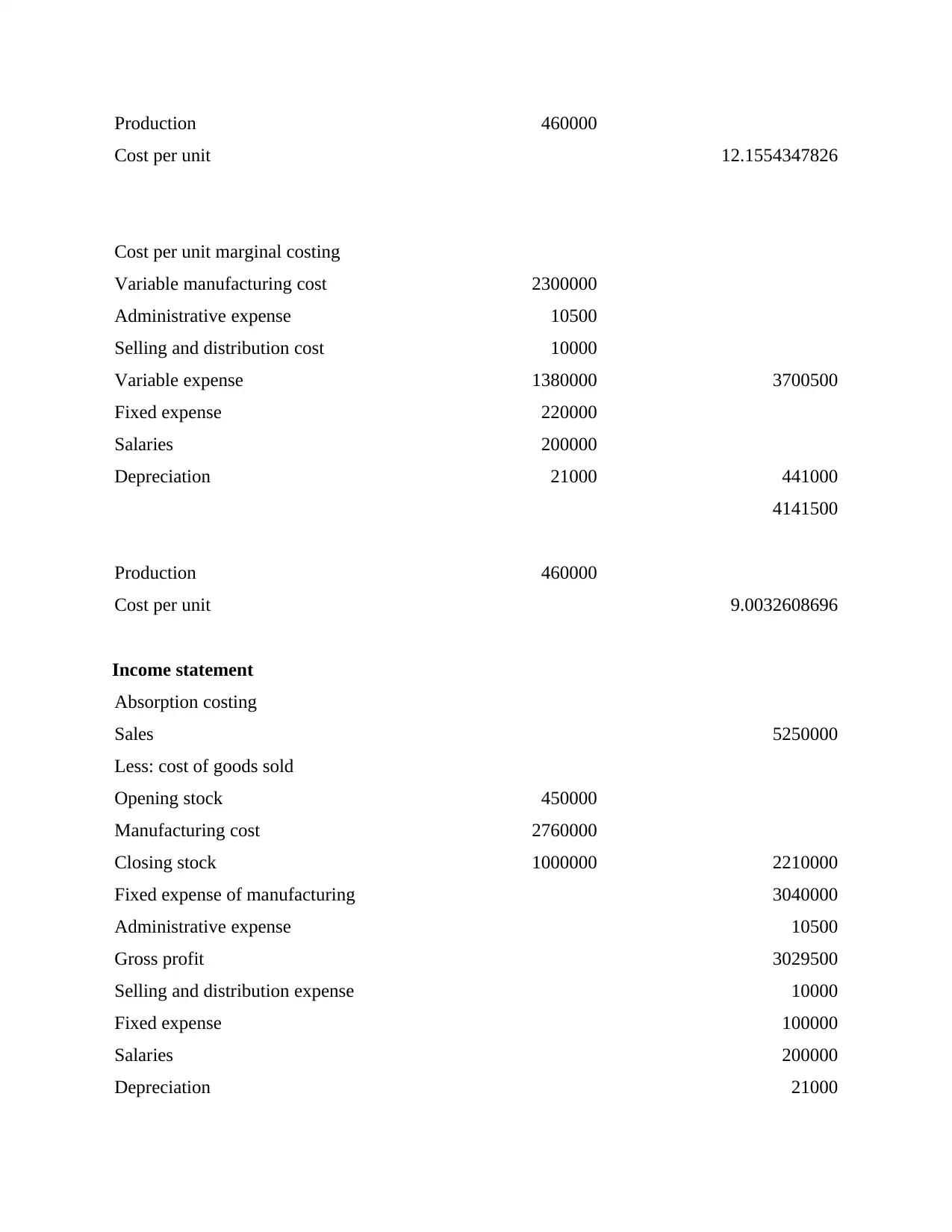

Production 460000

Cost per unit 12.1554347826

Cost per unit marginal costing

Variable manufacturing cost 2300000

Administrative expense 10500

Selling and distribution cost 10000

Variable expense 1380000 3700500

Fixed expense 220000

Salaries 200000

Depreciation 21000 441000

4141500

Production 460000

Cost per unit 9.0032608696

Income statement

Absorption costing

Sales 5250000

Less: cost of goods sold

Opening stock 450000

Manufacturing cost 2760000

Closing stock 1000000 2210000

Fixed expense of manufacturing 3040000

Administrative expense 10500

Gross profit 3029500

Selling and distribution expense 10000

Fixed expense 100000

Salaries 200000

Depreciation 21000

Cost per unit 12.1554347826

Cost per unit marginal costing

Variable manufacturing cost 2300000

Administrative expense 10500

Selling and distribution cost 10000

Variable expense 1380000 3700500

Fixed expense 220000

Salaries 200000

Depreciation 21000 441000

4141500

Production 460000

Cost per unit 9.0032608696

Income statement

Absorption costing

Sales 5250000

Less: cost of goods sold

Opening stock 450000

Manufacturing cost 2760000

Closing stock 1000000 2210000

Fixed expense of manufacturing 3040000

Administrative expense 10500

Gross profit 3029500

Selling and distribution expense 10000

Fixed expense 100000

Salaries 200000

Depreciation 21000

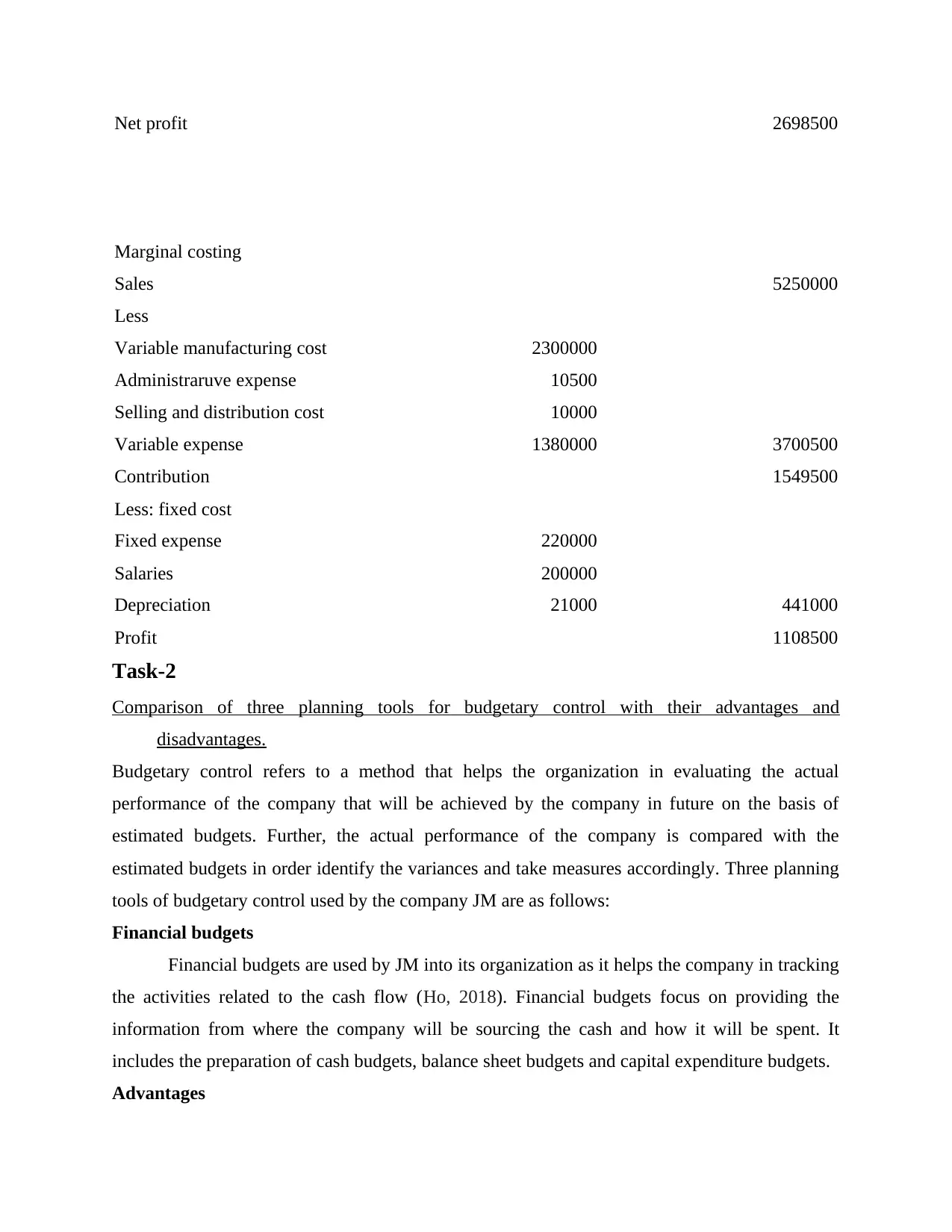

Net profit 2698500

Marginal costing

Sales 5250000

Less

Variable manufacturing cost 2300000

Administraruve expense 10500

Selling and distribution cost 10000

Variable expense 1380000 3700500

Contribution 1549500

Less: fixed cost

Fixed expense 220000

Salaries 200000

Depreciation 21000 441000

Profit 1108500

Task-2

Comparison of three planning tools for budgetary control with their advantages and

disadvantages.

Budgetary control refers to a method that helps the organization in evaluating the actual

performance of the company that will be achieved by the company in future on the basis of

estimated budgets. Further, the actual performance of the company is compared with the

estimated budgets in order identify the variances and take measures accordingly. Three planning

tools of budgetary control used by the company JM are as follows:

Financial budgets

Financial budgets are used by JM into its organization as it helps the company in tracking

the activities related to the cash flow (Ho, 2018). Financial budgets focus on providing the

information from where the company will be sourcing the cash and how it will be spent. It

includes the preparation of cash budgets, balance sheet budgets and capital expenditure budgets.

Advantages

Marginal costing

Sales 5250000

Less

Variable manufacturing cost 2300000

Administraruve expense 10500

Selling and distribution cost 10000

Variable expense 1380000 3700500

Contribution 1549500

Less: fixed cost

Fixed expense 220000

Salaries 200000

Depreciation 21000 441000

Profit 1108500

Task-2

Comparison of three planning tools for budgetary control with their advantages and

disadvantages.

Budgetary control refers to a method that helps the organization in evaluating the actual

performance of the company that will be achieved by the company in future on the basis of

estimated budgets. Further, the actual performance of the company is compared with the

estimated budgets in order identify the variances and take measures accordingly. Three planning

tools of budgetary control used by the company JM are as follows:

Financial budgets

Financial budgets are used by JM into its organization as it helps the company in tracking

the activities related to the cash flow (Ho, 2018). Financial budgets focus on providing the

information from where the company will be sourcing the cash and how it will be spent. It

includes the preparation of cash budgets, balance sheet budgets and capital expenditure budgets.

Advantages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The use of cash budget which falls under the category of financial budgets, helps the

company in identifying potential deficits within the enterprise. It helps the company to keep a

check of all the activities related to cash flow and ensures if the company has enough funds to

meet the obligations of the company.

Disadvantages

The major disadvantages of using financial budgets comprises of disability to build

creditworthiness and jeopardy of the documents prepared. The preparation financial budgets

might limit the amount of debt taken by the company (Nikulina, Butyugina, and Gorbunova,

2019). It is a good sign as company will be able to save more but it will affect the

creditworthiness of the company and will face difficulty in taking loans from the market in the

times of need.

Operating budgets

Operating budgets is a planning tool used by enterprises in order to plan the operations

for a specific period. It is used by the JM company as it provides the company with a detailed

forecasting statement relating to the revenue and expenditure of the company. Types of operating

budget include sales or revenue budget, expense budget and project budget.

Advantages

If the company efficiently follows the process of operating budget, it can help the

company in increasing the accountability of the company. With the help of operating budget, the

company can manage its expenses and even spend beyond its means. This develops a financial

obedience under the organization. Another advantage of operating budgets is that it helps the

company in building financial reserves by keeping a track of revenue and expenditure of the

enterprise. It helps in increasing the investment and reducing the debt taken.

Disadvantages

Operating budgets can be found very time consuming as preparation of operating budgets

involves various documents, information related to the process of accounting within the

organization. It includes continuously taking steps of similar nature in order to improve its

quality before it gets approved which it time consuming and a costly process to follow. Another

disadvantage of operating budget can be inaccuracy of information. Since, the operating budget

is merely a forecasted statement based on previous accounting information, it is possible that the

company in identifying potential deficits within the enterprise. It helps the company to keep a

check of all the activities related to cash flow and ensures if the company has enough funds to

meet the obligations of the company.

Disadvantages

The major disadvantages of using financial budgets comprises of disability to build

creditworthiness and jeopardy of the documents prepared. The preparation financial budgets

might limit the amount of debt taken by the company (Nikulina, Butyugina, and Gorbunova,

2019). It is a good sign as company will be able to save more but it will affect the

creditworthiness of the company and will face difficulty in taking loans from the market in the

times of need.

Operating budgets

Operating budgets is a planning tool used by enterprises in order to plan the operations

for a specific period. It is used by the JM company as it provides the company with a detailed

forecasting statement relating to the revenue and expenditure of the company. Types of operating

budget include sales or revenue budget, expense budget and project budget.

Advantages

If the company efficiently follows the process of operating budget, it can help the

company in increasing the accountability of the company. With the help of operating budget, the

company can manage its expenses and even spend beyond its means. This develops a financial

obedience under the organization. Another advantage of operating budgets is that it helps the

company in building financial reserves by keeping a track of revenue and expenditure of the

enterprise. It helps in increasing the investment and reducing the debt taken.

Disadvantages

Operating budgets can be found very time consuming as preparation of operating budgets

involves various documents, information related to the process of accounting within the

organization. It includes continuously taking steps of similar nature in order to improve its

quality before it gets approved which it time consuming and a costly process to follow. Another

disadvantage of operating budget can be inaccuracy of information. Since, the operating budget

is merely a forecasted statement based on previous accounting information, it is possible that the

projections do not match with the actual performance and lead to presentation of wrong

information.

Rolling budget

Rolling budget is a technique of budgetary control used by financial department of JM. It

allows an enterprise continuously extending the accounting period for which the budget is being

prepared. Under this technique, a budget for a period of 6 months or a year is created and then

rolls forward by a month, bimonthly or quarterly.

Advantages

This planning tool of budgetary control provides flexibility to the companies as they are

prepared for a short period. Because of this, the company can easily make necessary changes

whenever required (Henttu-Aho, 2018). It further reduces the uncertainty and helps in the

management of cash strategically and take corrective measures immediately whenever required

to minimize the impact of the any misconduct. It improves the efficiency of the organization as it

is easier for the management and the company to meet the short term targets as compared to the

budgets planned by way of traditional methods.

Disadvantages

The main disadvantage of rolling budget is that it occupies the staff for most of the time in a

year. As rolling budgets are created for a short period and are continuously prepared during a

year, most of the employees gets occupied in preparation of rolling budget. It affects the working

of other departments of organization and leads to mismanagement.

Part -B

Management accounting is among the most significant practice that is used and applied in

corporate entities. The role of management accounting practice is to allow the companies to

record the financial transaction in the best way possible and further to use the same in delivering

the business objectives. Companies in different industries and sectors such as retail, clothing,

fashion, information technology, manufacturing and many more sector are involved using the

management accounting practice as a way to record the business transactions and further to make

important decisions in business (Rikhardsson and Yigitbasioglu, 2018). the role of, management

accounting is to allow the companies like Marks and Spencer, Tesco and many more to assess

information.

Rolling budget

Rolling budget is a technique of budgetary control used by financial department of JM. It

allows an enterprise continuously extending the accounting period for which the budget is being

prepared. Under this technique, a budget for a period of 6 months or a year is created and then

rolls forward by a month, bimonthly or quarterly.

Advantages

This planning tool of budgetary control provides flexibility to the companies as they are

prepared for a short period. Because of this, the company can easily make necessary changes

whenever required (Henttu-Aho, 2018). It further reduces the uncertainty and helps in the

management of cash strategically and take corrective measures immediately whenever required

to minimize the impact of the any misconduct. It improves the efficiency of the organization as it

is easier for the management and the company to meet the short term targets as compared to the

budgets planned by way of traditional methods.

Disadvantages

The main disadvantage of rolling budget is that it occupies the staff for most of the time in a

year. As rolling budgets are created for a short period and are continuously prepared during a

year, most of the employees gets occupied in preparation of rolling budget. It affects the working

of other departments of organization and leads to mismanagement.

Part -B

Management accounting is among the most significant practice that is used and applied in

corporate entities. The role of management accounting practice is to allow the companies to

record the financial transaction in the best way possible and further to use the same in delivering

the business objectives. Companies in different industries and sectors such as retail, clothing,

fashion, information technology, manufacturing and many more sector are involved using the

management accounting practice as a way to record the business transactions and further to make

important decisions in business (Rikhardsson and Yigitbasioglu, 2018). the role of, management

accounting is to allow the companies like Marks and Spencer, Tesco and many more to assess

the performance of the organisation with the use of technique like ratio analysis that can direct

the venture about the overall performance of the venture. This has presented as a fact that the

management accounting practice play a vital role for the company to analysis the all areas of

performance and financial aspect of the venture and make relevant decision to maximise the

growth and development of the company. Management accounting as a technique also play role

in building the community partnership or alliances between the business venture. This is a key

aspect associated with management accounting practice is that it is highly engaged in developing

and establishing the community partnerships. Partnership and strategic alliance are one of the

core need companies hold as in order to deliver or execute any operation or business function

partnership and strategic alliance play a fundamental role. Strategic partnership allows to the

organisation to maximise its reach in respect to execute operations and functions of the venture.

In retail setting management accounting practices play a fundamental role. Today

companies like Marks and Spencer are one step ahead of its other competitors in market. The

way company has adopted different technique of management accounting like costing related

methods, investment appraisal, ratio analysis and such related methods are adopted to execute

the business functions (Ameen, Ahmed and Abd Hafez, 2018). These techniques and method of

management accounting could completely strengthen the decision making area of the company

which could further maximise to the overall growth and development of the venture. The key

role management accounting practice is to provide the competitive advantage to the organisation

in respective target market.

Operating a statutory body also require the use of management accounting practice. This

could allow the government to establish the statutory bodies every time they tend to utilise the

technique of management accounting. Government intervene in the market in order to regulate

the whole market and the act or actions companies in market are taking to execute the business

objectives (Juliana, Gani and Jermias, 2021). Management accounting play a fundamental role

for the government to strategically regulate the business operations and further to control the

same tragically. Role of management accounting is in every aspect and area of industry that can

regulate by the body. Costing is an important aspect and the management accounting practices

could favour to the management to control the cost of production along with controlling other

operational cost as well to make production cheaper in the market.

the venture about the overall performance of the venture. This has presented as a fact that the

management accounting practice play a vital role for the company to analysis the all areas of

performance and financial aspect of the venture and make relevant decision to maximise the

growth and development of the company. Management accounting as a technique also play role

in building the community partnership or alliances between the business venture. This is a key

aspect associated with management accounting practice is that it is highly engaged in developing

and establishing the community partnerships. Partnership and strategic alliance are one of the

core need companies hold as in order to deliver or execute any operation or business function

partnership and strategic alliance play a fundamental role. Strategic partnership allows to the

organisation to maximise its reach in respect to execute operations and functions of the venture.

In retail setting management accounting practices play a fundamental role. Today

companies like Marks and Spencer are one step ahead of its other competitors in market. The

way company has adopted different technique of management accounting like costing related

methods, investment appraisal, ratio analysis and such related methods are adopted to execute

the business functions (Ameen, Ahmed and Abd Hafez, 2018). These techniques and method of

management accounting could completely strengthen the decision making area of the company

which could further maximise to the overall growth and development of the venture. The key

role management accounting practice is to provide the competitive advantage to the organisation

in respective target market.

Operating a statutory body also require the use of management accounting practice. This

could allow the government to establish the statutory bodies every time they tend to utilise the

technique of management accounting. Government intervene in the market in order to regulate

the whole market and the act or actions companies in market are taking to execute the business

objectives (Juliana, Gani and Jermias, 2021). Management accounting play a fundamental role

for the government to strategically regulate the business operations and further to control the

same tragically. Role of management accounting is in every aspect and area of industry that can

regulate by the body. Costing is an important aspect and the management accounting practices

could favour to the management to control the cost of production along with controlling other

operational cost as well to make production cheaper in the market.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Management accounting has also been involved in managing the supply chain of the

organisation. Operation management is among the key area of function in organisation and

management accounting could completely influence to the operation management related

practice of the venture. With the use of effective technique like economic order quantity method

and such other of management accounting the organisation get to make the decision in respect to

the supply chain management feature of the organisation. Wincanton in United Kingdom is one

of the leading logistic company based in United Kingdom by holding the 13% market share of

the entire market (Zyznarska-Dworczak, 2018). The management accounting also contributed in

growing the value of the firm. This practice cold also secure the interest of the shareholders and

investor involve in the business by providing sufficient right to such stakeholders. Audit involve

in the management accounting could allow to the organisation for achieving better public

services. Adopt assure to the stakeholders that the money invested in the company are utilising in

conducting the relevant business operations. This is important that the shareholders are

convinced with the use company is utilising its resources. Management accounting payed a

fundamental role in improving the feasibility of the way funds in business are use. This entire

practice allows the organisation to make important decision related to different functional area in

business (Endenich and Trapp, 2020). The role management accounting play is to allow the

organisation to make all important business decision that can favour the venture in maximising

the overall growth and development of the venture. The role management accounting play is also

to support companies in taking competitive advantage in respective business environment.

Management accounting allow the company to ensure control over the operations and functional

areas of the organisation. Strengthening control over operation is among the key advantage

management accounting provide to the organisation.

CONCLUSION

From the above report, it can be concluded that the management accounting is must for

any organization in order to deal with financial problems within an organization. The principles

of management accounting guides the enterprises with the process of accounting to make

organisation. Operation management is among the key area of function in organisation and

management accounting could completely influence to the operation management related

practice of the venture. With the use of effective technique like economic order quantity method

and such other of management accounting the organisation get to make the decision in respect to

the supply chain management feature of the organisation. Wincanton in United Kingdom is one

of the leading logistic company based in United Kingdom by holding the 13% market share of

the entire market (Zyznarska-Dworczak, 2018). The management accounting also contributed in

growing the value of the firm. This practice cold also secure the interest of the shareholders and

investor involve in the business by providing sufficient right to such stakeholders. Audit involve

in the management accounting could allow to the organisation for achieving better public

services. Adopt assure to the stakeholders that the money invested in the company are utilising in

conducting the relevant business operations. This is important that the shareholders are

convinced with the use company is utilising its resources. Management accounting payed a

fundamental role in improving the feasibility of the way funds in business are use. This entire

practice allows the organisation to make important decision related to different functional area in

business (Endenich and Trapp, 2020). The role management accounting play is to allow the

organisation to make all important business decision that can favour the venture in maximising

the overall growth and development of the venture. The role management accounting play is also

to support companies in taking competitive advantage in respective business environment.

Management accounting allow the company to ensure control over the operations and functional

areas of the organisation. Strengthening control over operation is among the key advantage

management accounting provide to the organisation.

CONCLUSION

From the above report, it can be concluded that the management accounting is must for

any organization in order to deal with financial problems within an organization. The principles

of management accounting guides the enterprises with the process of accounting to make

informed financial decisions within the organization. Further, the planning tools of budgetary

control helps the company in forecasting the budget for future period and compares the actual

performance with them. It helps the company in taking corrective measures for the deviations

found. With the evaluation of different systems of management accounting, it can be stated that

it helps the company in enhancing its profitability.

control helps the company in forecasting the budget for future period and compares the actual

performance with them. It helps the company in taking corrective measures for the deviations

found. With the evaluation of different systems of management accounting, it can be stated that

it helps the company in enhancing its profitability.

REFERENCES

Books and journals

Ameen, A. M., Ahmed, M. F. and Abd Hafez, M. A., 2018. The impact of management

accounting and how it can be implemented into the organizational culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review. 23(3). pp.222-226.

business ethics. 163(2). pp.309-328.

Cescon, F., Costantini, A. and Grassetti, L., 2019. Strategic choices and strategic management

accounting in large manufacturing firms. Journal of Management and Governance.

23(3). pp.605-636.

Das, S.C., 2019. Management control systems: principles and practices. PHI Learning Pvt. Ltd..

Henttu-Aho, T., 2018. The role of rolling forecasting in budgetary control systems: reactive and

proactive types of planning. Journal of management control.29(3). pp.327-360.

Ho, A.T.K., 2018. From performance budgeting to performance budget management: theory and

practice. Public Administration Review.78(5). pp.748-758.

Juliana, C., Gani, L. and Jermias, J., 2021. Performance implications of misalignment among

business strategy, leadership style, organizational culture and management accounting

systems. International Journal of Ethics and Systems.

Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, M.S.K., 2021. Principles of Management

Accounting. Sultan Chand & Sons.

Mishra, C.R., A STUDY ON BUDGET AND BUDGETARY CONTROL: ANALYSIS OF

CASH BUDGET.

Nikulina, S.N., Butyugina, A.A. and Gorbunova, E.E., 2019, October. Investment activity in

conditions of automation use of budgeting system. In IOP Conference Series: Earth and

Environmental Science (Vol. 341, No. 1, p. 012217). IOP Publishing.

Pedroso, E. and Gomes, C.F., 2020. The effectiveness of management accounting systems in

SMEs: A multidimensional measurement approach. Journal of Applied Accounting

Research.

Pellerin, R. and Perrier, N., 2019. A review of methods, techniques and tools for project planning

and control. International Journal of Production Research. 57(7). pp.2160-2178.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Yakupova, L.R., 2019. BASIC PRINCIPLES OF IMPLEMENTATION OF STRATEGIC

MANAGEMENT ACCOUNTING AT THE ENTERPRISE. In Развитие

бухгалтерского учета и аудита в условиях цифровой экономики (pp. 302-308).

Zahid, N.A. and Vagif, L.M., 2020. ROLE OF MANAGEMENT ACCOUNTING IN THE

ORGANIZATION. Economic and Social Development: Book of Proceedings. 3.

pp.367-372.

1

Books and journals

Ameen, A. M., Ahmed, M. F. and Abd Hafez, M. A., 2018. The impact of management

accounting and how it can be implemented into the organizational culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Ameen, A.M., Ahmed, M.F. and Abd Hafez, M.A., 2018. The Impact of Management

Accounting and How It Can Be Implemented into the Organizational Culture. Dutch

Journal of Finance and Management. 2(1). p.02.

Azudin, A. and Mansor, N., 2018. Management accounting practices of SMEs: The impact of

organizational DNA, business potential and operational technology. Asia Pacific

Management Review. 23(3). pp.222-226.

business ethics. 163(2). pp.309-328.

Cescon, F., Costantini, A. and Grassetti, L., 2019. Strategic choices and strategic management

accounting in large manufacturing firms. Journal of Management and Governance.

23(3). pp.605-636.

Das, S.C., 2019. Management control systems: principles and practices. PHI Learning Pvt. Ltd..

Henttu-Aho, T., 2018. The role of rolling forecasting in budgetary control systems: reactive and

proactive types of planning. Journal of management control.29(3). pp.327-360.

Ho, A.T.K., 2018. From performance budgeting to performance budget management: theory and

practice. Public Administration Review.78(5). pp.748-758.

Juliana, C., Gani, L. and Jermias, J., 2021. Performance implications of misalignment among

business strategy, leadership style, organizational culture and management accounting

systems. International Journal of Ethics and Systems.

Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, M.S.K., 2021. Principles of Management

Accounting. Sultan Chand & Sons.

Mishra, C.R., A STUDY ON BUDGET AND BUDGETARY CONTROL: ANALYSIS OF

CASH BUDGET.

Nikulina, S.N., Butyugina, A.A. and Gorbunova, E.E., 2019, October. Investment activity in

conditions of automation use of budgeting system. In IOP Conference Series: Earth and

Environmental Science (Vol. 341, No. 1, p. 012217). IOP Publishing.

Pedroso, E. and Gomes, C.F., 2020. The effectiveness of management accounting systems in

SMEs: A multidimensional measurement approach. Journal of Applied Accounting

Research.

Pellerin, R. and Perrier, N., 2019. A review of methods, techniques and tools for project planning

and control. International Journal of Production Research. 57(7). pp.2160-2178.

Rikhardsson, P. and Yigitbasioglu, O., 2018. Business intelligence & analytics in management

accounting research: Status and future focus. International Journal of Accounting

Information Systems. 29. pp.37-58.

Yakupova, L.R., 2019. BASIC PRINCIPLES OF IMPLEMENTATION OF STRATEGIC

MANAGEMENT ACCOUNTING AT THE ENTERPRISE. In Развитие

бухгалтерского учета и аудита в условиях цифровой экономики (pp. 302-308).

Zahid, N.A. and Vagif, L.M., 2020. ROLE OF MANAGEMENT ACCOUNTING IN THE

ORGANIZATION. Economic and Social Development: Book of Proceedings. 3.

pp.367-372.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Zyznarska-Dworczak, B., 2018. Legitimacy theory in management accounting

research. Problemy Zarządzania. 16(1 (72)). pp.195-203.

2

research. Problemy Zarządzania. 16(1 (72)). pp.195-203.

2

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.