Application of Management Accounting Principles in a Business Context

VerifiedAdded on 2023/01/06

|11

|3162

|96

Report

AI Summary

This report delves into the core principles of management accounting and their application within a business context. It begins with an introduction to management accounting systems, differentiating them from financial accounting and highlighting their importance in planning, decision-making, and strategic planning. The report then examines various components of management accounting systems, including cost accounting, inventory management, and price optimization. Furthermore, it explores management accounting reports such as budget reports, inventory management reports, performance reports, and accounts receivable aging reports. The report also analyzes cost analysis techniques, specifically marginal costing and absorption costing, and their application. Finally, it discusses planning tools used for budgetary control, including cash budgets and capital budgeting, and their advantages and disadvantages, concluding with the relationship between management accounting systems and financial problems.

Management

Accounting Principles

Accounting Principles

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction.................................................................................................................................................3

Task 1..........................................................................................................................................................3

P1 Management accounting system.........................................................................................................3

P2 Management accounting reports.........................................................................................................6

Task 2..........................................................................................................................................................7

P3 Techniques of cost analysis................................................................................................................7

P4 Planning tools used for budgetary control..........................................................................................8

P5 relationship between management accounting system and financial problems...................................9

Conclusion.................................................................................................................................................10

Task 1..........................................................................................................................................................3

P1 Management accounting system.........................................................................................................3

P2 Management accounting reports.........................................................................................................6

Task 2..........................................................................................................................................................7

P3 Techniques of cost analysis................................................................................................................7

P4 Planning tools used for budgetary control..........................................................................................8

P5 relationship between management accounting system and financial problems...................................9

Conclusion.................................................................................................................................................10

Introduction

Management accounting is an integral part of management of any organization. It

basically takes care of analysis and interpretation of financial data. This process aids in planning

and decision making process of the company. There are several theories and techniques those

can be used for the above process. Ultimate objective of any organization is to earn maximized

profits which can only be achieved by formulation of efficient strategies. Tools and techniques of

management accounting help in formulation of such strategies that assist in reaching the desired

objective. In this report, prime focus is on application of management accounting principles on a

particular business. Various concepts like management accounting system, management

accounting reports, costing methods, absorption costing, marginal costing will be discussed in

order to develop understanding of concepts so as to apply them to achieve desired outcomes.

Task 1

P1 Management accounting system

Management accounting refers to most important helping tool that is available to

managers. It helps in monitoring and controlling of financial transactions and related things of

business operations. It is not using whole of data that is provided by financial accounting

process. Rather, it is very selective in nature and therefore, uses only some information. Choice

of information is basically on the basis of their capabilities of contributing in formulation of

efficient and effective strategies (Chan and et.al., 2015). One of the most important concept

under the big umbrella of management accounting is management accounting system. It refers to

the analysis of processes of every branch of that organization in a systematic manner and this

manner is known as management accounting system.

There is huge difference between management accounting and financial accounting which are

enumerated below:

Basis Management accounting Financial accounting

User It acts as helping aid for internal

stakeholders such as managers

(Chen, Lee and Shevlin, 2016).

This information is used by both

internal and external users, so as to

know about the financial position of

the company.

Management accounting is an integral part of management of any organization. It

basically takes care of analysis and interpretation of financial data. This process aids in planning

and decision making process of the company. There are several theories and techniques those

can be used for the above process. Ultimate objective of any organization is to earn maximized

profits which can only be achieved by formulation of efficient strategies. Tools and techniques of

management accounting help in formulation of such strategies that assist in reaching the desired

objective. In this report, prime focus is on application of management accounting principles on a

particular business. Various concepts like management accounting system, management

accounting reports, costing methods, absorption costing, marginal costing will be discussed in

order to develop understanding of concepts so as to apply them to achieve desired outcomes.

Task 1

P1 Management accounting system

Management accounting refers to most important helping tool that is available to

managers. It helps in monitoring and controlling of financial transactions and related things of

business operations. It is not using whole of data that is provided by financial accounting

process. Rather, it is very selective in nature and therefore, uses only some information. Choice

of information is basically on the basis of their capabilities of contributing in formulation of

efficient and effective strategies (Chan and et.al., 2015). One of the most important concept

under the big umbrella of management accounting is management accounting system. It refers to

the analysis of processes of every branch of that organization in a systematic manner and this

manner is known as management accounting system.

There is huge difference between management accounting and financial accounting which are

enumerated below:

Basis Management accounting Financial accounting

User It acts as helping aid for internal

stakeholders such as managers

(Chen, Lee and Shevlin, 2016).

This information is used by both

internal and external users, so as to

know about the financial position of

the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Regulation This is not mandatory to follow in

organization, as it is not regulated

by any legal obligation.

It is essential to follow as it is

regulated by laws and policies.

Audit As it is not compulsory to conduct,

therefore, audit also becomes a

option that if not followed do not

invite any intervention.

Audit of financial statements is a

mandatory process to be followed

as it checks the true and fairness of

financial statements. This is

conducted by the professionals and

stakeholders do depend on

judgments of these professionals

(Christensen, Skærbæk and

Tryggestad, 2019).

To certify the importance of management accounting for an organization following arguments

can be given:

Planning and decision making- Management accountant play the important role by

formulating decisions and strategies for organization, these policies and strategies help

lower level executives to work and achieve desired objectives. These strategies are

formed with the help of useful information like budgeting, ratios, etc. that is generated

from methods and techniques of management accounting.

Pro activeness- This means being prepared in advance for the problems that may occur in

future. With this strategy, possible losses can be mitigated. Management accounting plays

this important role in a company as it identifies the areas of problems and also attracts

attention of managers to that area. This will help in preparing company before hand and

losses can also be reduced. For instance, budgeting calculates variation in actual

performance and expected (or budgeted) performance, this process helps in identifying

those areas due to which expected results could not be generated. Now the company can

prepare itself for those areas and can also take corrective measures if required.

Strategic planning- Management accounting helps managers in identifying any fault in

already formulated strategies and policies. This will result in formulation of appropriate

strategies which ultimately results in success of organization (Dunbar, Laing and

Wynder, 2016).

Branch of management accounting coordinates with every department of a company and then

this established connection produces a separate management accounting system which manages

organization, as it is not regulated

by any legal obligation.

It is essential to follow as it is

regulated by laws and policies.

Audit As it is not compulsory to conduct,

therefore, audit also becomes a

option that if not followed do not

invite any intervention.

Audit of financial statements is a

mandatory process to be followed

as it checks the true and fairness of

financial statements. This is

conducted by the professionals and

stakeholders do depend on

judgments of these professionals

(Christensen, Skærbæk and

Tryggestad, 2019).

To certify the importance of management accounting for an organization following arguments

can be given:

Planning and decision making- Management accountant play the important role by

formulating decisions and strategies for organization, these policies and strategies help

lower level executives to work and achieve desired objectives. These strategies are

formed with the help of useful information like budgeting, ratios, etc. that is generated

from methods and techniques of management accounting.

Pro activeness- This means being prepared in advance for the problems that may occur in

future. With this strategy, possible losses can be mitigated. Management accounting plays

this important role in a company as it identifies the areas of problems and also attracts

attention of managers to that area. This will help in preparing company before hand and

losses can also be reduced. For instance, budgeting calculates variation in actual

performance and expected (or budgeted) performance, this process helps in identifying

those areas due to which expected results could not be generated. Now the company can

prepare itself for those areas and can also take corrective measures if required.

Strategic planning- Management accounting helps managers in identifying any fault in

already formulated strategies and policies. This will result in formulation of appropriate

strategies which ultimately results in success of organization (Dunbar, Laing and

Wynder, 2016).

Branch of management accounting coordinates with every department of a company and then

this established connection produces a separate management accounting system which manages

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

all transaction of that function of company. Various management accounting concepts have been

discussed below:

Cost accounting system: It is most used technique by manufacturing industries. The main

role of this system is to monitor and control every type of cost that is incurred in

company. These cost may relate to any department of organization, for example, cost of

procuring raw material, cost incurred in production process, day to day expenses, cost of

logistics department, etc. This pervasive process helps managers in identifying the areas

which are incurring higher cost than what is required to be spent. This system will help

in deciding that which area needs cost cutting and which is that department which if

invested more will generate higher profits. This system helps in improving productivity

and profitability of organization (Ho and et.al., 2015). In this system, there is a break up

of cost under different heads like fixed cost, variable cost, semi variable cost, marginal

cost, etc. This break up of costs under different heads according to their nature helps

managers to take decisions regarding strategy formulation of cost in the given company.

Inventory management system: This system is basically governing the flow of stock in

company. This means it regulates the policies that states from where the inventory will be

procured, in how much quantity and what value, when it will be ordered, how it will be

allocated for further production, etc. these all tasks are performed under this system. This

system also manages related databases like barcode, labels, etc. This will ensure

uninterrupted flow of inventory and also no overstocking and under stocking. This

system maintains availability of raw material as and when required. This system also

ensures that there is no duplication at the time of ordering of stock.

Price optimizing system- This is a process of determining prices of products and services

of a business. This tool helps management in identifying appropriate pricing strategy so

that they can establish the business well in the market place and within the targeted

customers. An appropriate pricing strategy can be defined as that price level of products

and services which attempts to attract more and more customers and also creates a loyal

customer base. This will generate competitive advantage for business. This setup of price

is in accordance of willingness and ability to pay by customers.

P2 Management accounting reports

Reporting refers to the process of communicating results of management accounting

systems to the managers so that they can use this information in formulation of strategies and

policies (Hrabal, 2016). Some reports are explained below:

discussed below:

Cost accounting system: It is most used technique by manufacturing industries. The main

role of this system is to monitor and control every type of cost that is incurred in

company. These cost may relate to any department of organization, for example, cost of

procuring raw material, cost incurred in production process, day to day expenses, cost of

logistics department, etc. This pervasive process helps managers in identifying the areas

which are incurring higher cost than what is required to be spent. This system will help

in deciding that which area needs cost cutting and which is that department which if

invested more will generate higher profits. This system helps in improving productivity

and profitability of organization (Ho and et.al., 2015). In this system, there is a break up

of cost under different heads like fixed cost, variable cost, semi variable cost, marginal

cost, etc. This break up of costs under different heads according to their nature helps

managers to take decisions regarding strategy formulation of cost in the given company.

Inventory management system: This system is basically governing the flow of stock in

company. This means it regulates the policies that states from where the inventory will be

procured, in how much quantity and what value, when it will be ordered, how it will be

allocated for further production, etc. these all tasks are performed under this system. This

system also manages related databases like barcode, labels, etc. This will ensure

uninterrupted flow of inventory and also no overstocking and under stocking. This

system maintains availability of raw material as and when required. This system also

ensures that there is no duplication at the time of ordering of stock.

Price optimizing system- This is a process of determining prices of products and services

of a business. This tool helps management in identifying appropriate pricing strategy so

that they can establish the business well in the market place and within the targeted

customers. An appropriate pricing strategy can be defined as that price level of products

and services which attempts to attract more and more customers and also creates a loyal

customer base. This will generate competitive advantage for business. This setup of price

is in accordance of willingness and ability to pay by customers.

P2 Management accounting reports

Reporting refers to the process of communicating results of management accounting

systems to the managers so that they can use this information in formulation of strategies and

policies (Hrabal, 2016). Some reports are explained below:

Budget reports: This refers to those statements which generate results or information for

the pre set budgets related o specific department. For instance, budgets are prepared for

standard output, now the budget report will tell the outcome of all these matters showing

the difference between the expected output and actual output. This will help in taking

corrective measures to see how the productivity can be improved.

Inventory management report- This report shows data relating to inventory of

organization, such as, EOQ, amount of wastage, quantity of raw materials used in

production process, lead time, etc. This will make the maintenance of records of

inventory a very easy task and will also reduce the chances of frauds due to transparent

management of whole inventory process in organization. This is a very useful method for

a manufacturing industry (Lippert, 2015).

Performance report: This is a statement showing performance of employees and

company as well. To achieve desired objectives, it is necessary that all the aspects of an

organization perform well. Therefore, it becomes necessary that it is evaluated from time

to time. For this purpose, performance reports are formed. This also plays a vital role in

evaluating financial position of business. This report contains various important data like

profitability statements, returns, flow of cash, etc. This report provides assistance to

management of enterprise to plan for future course of action so that efficient and effective

operations can be ensured.

Accounts receivable ageing report- This report focuses on management of flow of cash

related to the credits allowed by the company. This report contains particulars like name

of debtors, transaction date and amount blocked with debtor, etc. There are different

rimes allowed as credit time, therefore, transactions for different periods are recorded

separately. Taking this system into use, managers of Prime furniture can manage their

debtors with better credit policies and can help company to recover money sooner.

Task 2

P3 Techniques of cost analysis

Marginal costing: This is a tool for analyzing additional cost for producing one more unit

in addition to the present production. This helps in inspecting into appropriate scale of

production where the cost is minimized and profits are maximized (Shipman, Swanquist and

Whited, 2017).

the pre set budgets related o specific department. For instance, budgets are prepared for

standard output, now the budget report will tell the outcome of all these matters showing

the difference between the expected output and actual output. This will help in taking

corrective measures to see how the productivity can be improved.

Inventory management report- This report shows data relating to inventory of

organization, such as, EOQ, amount of wastage, quantity of raw materials used in

production process, lead time, etc. This will make the maintenance of records of

inventory a very easy task and will also reduce the chances of frauds due to transparent

management of whole inventory process in organization. This is a very useful method for

a manufacturing industry (Lippert, 2015).

Performance report: This is a statement showing performance of employees and

company as well. To achieve desired objectives, it is necessary that all the aspects of an

organization perform well. Therefore, it becomes necessary that it is evaluated from time

to time. For this purpose, performance reports are formed. This also plays a vital role in

evaluating financial position of business. This report contains various important data like

profitability statements, returns, flow of cash, etc. This report provides assistance to

management of enterprise to plan for future course of action so that efficient and effective

operations can be ensured.

Accounts receivable ageing report- This report focuses on management of flow of cash

related to the credits allowed by the company. This report contains particulars like name

of debtors, transaction date and amount blocked with debtor, etc. There are different

rimes allowed as credit time, therefore, transactions for different periods are recorded

separately. Taking this system into use, managers of Prime furniture can manage their

debtors with better credit policies and can help company to recover money sooner.

Task 2

P3 Techniques of cost analysis

Marginal costing: This is a tool for analyzing additional cost for producing one more unit

in addition to the present production. This helps in inspecting into appropriate scale of

production where the cost is minimized and profits are maximized (Shipman, Swanquist and

Whited, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

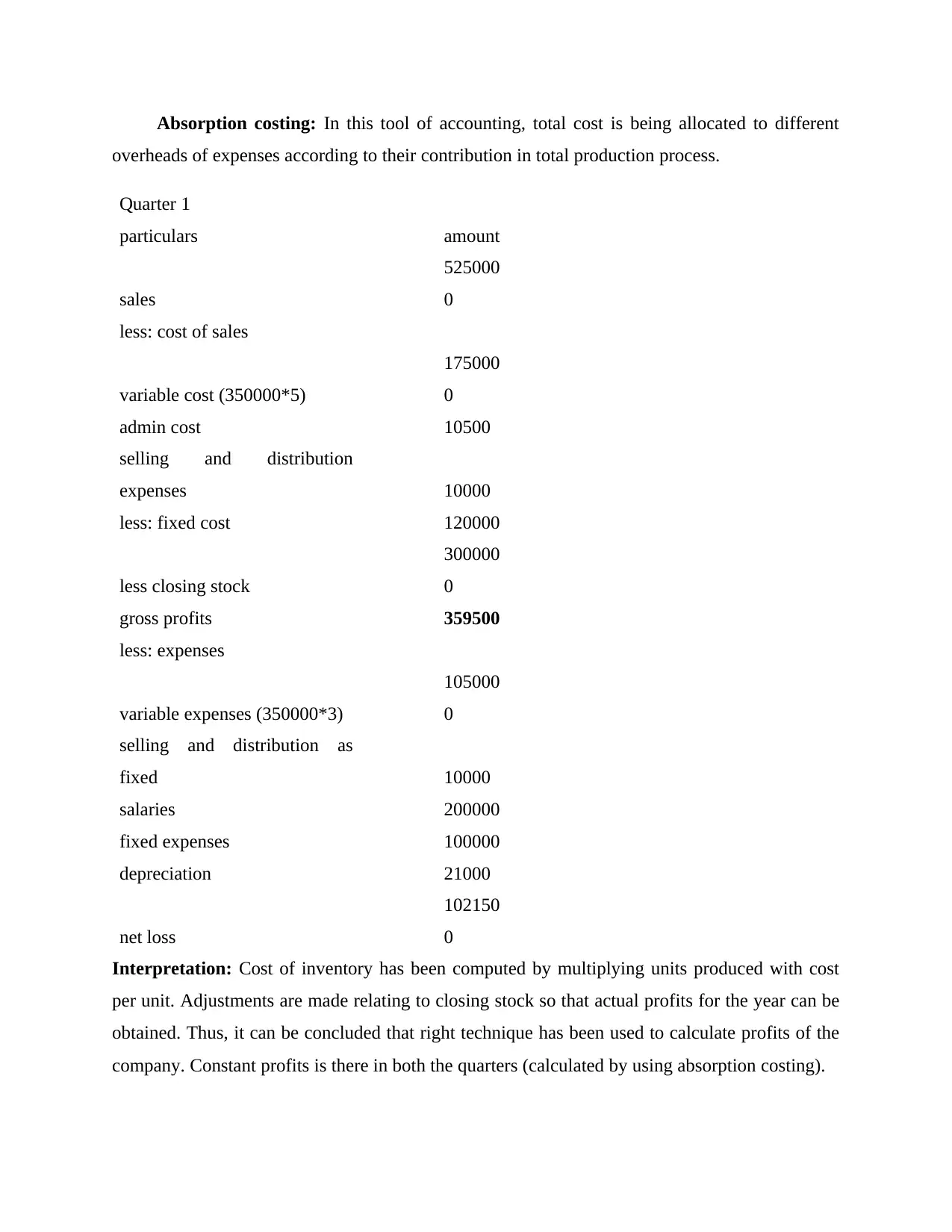

Absorption costing: In this tool of accounting, total cost is being allocated to different

overheads of expenses according to their contribution in total production process.

Quarter 1

particulars amount

sales

525000

0

less: cost of sales

variable cost (350000*5)

175000

0

admin cost 10500

selling and distribution

expenses 10000

less: fixed cost 120000

less closing stock

300000

0

gross profits 359500

less: expenses

variable expenses (350000*3)

105000

0

selling and distribution as

fixed 10000

salaries 200000

fixed expenses 100000

depreciation 21000

net loss

102150

0

Interpretation: Cost of inventory has been computed by multiplying units produced with cost

per unit. Adjustments are made relating to closing stock so that actual profits for the year can be

obtained. Thus, it can be concluded that right technique has been used to calculate profits of the

company. Constant profits is there in both the quarters (calculated by using absorption costing).

overheads of expenses according to their contribution in total production process.

Quarter 1

particulars amount

sales

525000

0

less: cost of sales

variable cost (350000*5)

175000

0

admin cost 10500

selling and distribution

expenses 10000

less: fixed cost 120000

less closing stock

300000

0

gross profits 359500

less: expenses

variable expenses (350000*3)

105000

0

selling and distribution as

fixed 10000

salaries 200000

fixed expenses 100000

depreciation 21000

net loss

102150

0

Interpretation: Cost of inventory has been computed by multiplying units produced with cost

per unit. Adjustments are made relating to closing stock so that actual profits for the year can be

obtained. Thus, it can be concluded that right technique has been used to calculate profits of the

company. Constant profits is there in both the quarters (calculated by using absorption costing).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P4 Planning tools used for budgetary control

Budgetary control is a control process that is used to evaluate the comparison between

budgeted and actual performance for a defined period. This procedure is used for evaluating the

performance by management. After monitoring performance, differences are calculated and

accordingly corrective measures will be taken and implemented in the organization. Following

planning tools can be used:

Cash budget: In this budget, cash inflow and outflows are estimated for a future specified time

period. These budgets are based on past records and performance. This budget helps

management to ascertain whether company will confront surplus of liquidity or deficit in the

coming future. It will help in management of business in optimizing planning and utilization of

cash and cash equivalents.

Advantages – Cash planning helps management in planning smooth disbursement of cash

according to availability and inflow of cash. They could avoid both cash crunch as well

as over liquidation in cash. Disadvantages – It is prepared on the basis of past records and future estimation.

Uncertainties in external business environment can upset cash planning and can cause

rigidity in business operations.

Capital budgeting:

The main objective of every business is to grow. This growth is possible only in the case

when business takes up new projects and proposals. These projects requires huge amount of

investment, thus, it will require an in- depth study of all aspects of that new project. One of the

important analysis in this direction is capital budgeting. It means comparing expected revenues

and cost of proposed project. This will help in finding the profitability value of that project. This

technique is applied to all the alternatives available, so that the most profitable can be chosen and

this huge investment is not blocked. This technique is very important as it involved large amount

of funds and if the project fail that it may lead to wastage of those funds and also a hazardous

effect on business. This may even lead to shut down of enterprise.

Budgetary control is a control process that is used to evaluate the comparison between

budgeted and actual performance for a defined period. This procedure is used for evaluating the

performance by management. After monitoring performance, differences are calculated and

accordingly corrective measures will be taken and implemented in the organization. Following

planning tools can be used:

Cash budget: In this budget, cash inflow and outflows are estimated for a future specified time

period. These budgets are based on past records and performance. This budget helps

management to ascertain whether company will confront surplus of liquidity or deficit in the

coming future. It will help in management of business in optimizing planning and utilization of

cash and cash equivalents.

Advantages – Cash planning helps management in planning smooth disbursement of cash

according to availability and inflow of cash. They could avoid both cash crunch as well

as over liquidation in cash. Disadvantages – It is prepared on the basis of past records and future estimation.

Uncertainties in external business environment can upset cash planning and can cause

rigidity in business operations.

Capital budgeting:

The main objective of every business is to grow. This growth is possible only in the case

when business takes up new projects and proposals. These projects requires huge amount of

investment, thus, it will require an in- depth study of all aspects of that new project. One of the

important analysis in this direction is capital budgeting. It means comparing expected revenues

and cost of proposed project. This will help in finding the profitability value of that project. This

technique is applied to all the alternatives available, so that the most profitable can be chosen and

this huge investment is not blocked. This technique is very important as it involved large amount

of funds and if the project fail that it may lead to wastage of those funds and also a hazardous

effect on business. This may even lead to shut down of enterprise.

Advantages – Capital investments require huge funds and then those funds get blocked

for a long time. Any wrong investment can create problems for financial health of whole

organization. Evaluating investment alternative helps management in averting such risks.

Disadvantages – Capital budgeting techniques are based on understanding of financial

managers. Any wrong assumption taken by them can give financial well being of

company a fatal blow.

Planning tools used in budgetary controlling

Planning tools are used by management to prepare plans for monitoring and controlling. Tools

such as multiple types of budgets present management with various targets that company has to

fulfill over the specified period of budget. It also helps management in identification of variances

and serves as basis for corrective actions. With the help of tools such as capital budgeting,

management can avoid major financial problems (Sithole, 2015).

P5 relationship between management accounting system and financial problems

Financial problem: This issue can be defined as those issues which are confronted by an

enterprise while operating in a business environment. These are the problems which arise due to

failure in managing financial stability of business. These issues can arise due to various reasons

like decrease in sales volume, increased expenses, loss of growth opportunities, etc.

Sales downfall: In lifecycle of products, there are stages which confront decline in sales.

This is due to several reasons like increased competition, difficult business environment,

uncertainties in factors affecting sales volume, etc. reduction in sales volume puts direct impact

on revenue generation cycle and growth opportunities of business. This istuation is usually

confronted in maturity and decline stage of business.

Increased cost of raw materials: Increase in cost of raw materials can be due to multiple factors

such as increase in prices of logistics, increase in bargaining power of vendor, taxes hike, etc.

Increase in cost increases operational expenses and decreases profit margin. It can also lead to

increase in price of product which again can have negative impact on sales of company products.

Financial governance – It refers to the system of practices in which a company control

its financial information. Companies track their financial transactions and perform control

operations in the interest of its stakeholders. If a company is able to identify its risk earlier, it can

for a long time. Any wrong investment can create problems for financial health of whole

organization. Evaluating investment alternative helps management in averting such risks.

Disadvantages – Capital budgeting techniques are based on understanding of financial

managers. Any wrong assumption taken by them can give financial well being of

company a fatal blow.

Planning tools used in budgetary controlling

Planning tools are used by management to prepare plans for monitoring and controlling. Tools

such as multiple types of budgets present management with various targets that company has to

fulfill over the specified period of budget. It also helps management in identification of variances

and serves as basis for corrective actions. With the help of tools such as capital budgeting,

management can avoid major financial problems (Sithole, 2015).

P5 relationship between management accounting system and financial problems

Financial problem: This issue can be defined as those issues which are confronted by an

enterprise while operating in a business environment. These are the problems which arise due to

failure in managing financial stability of business. These issues can arise due to various reasons

like decrease in sales volume, increased expenses, loss of growth opportunities, etc.

Sales downfall: In lifecycle of products, there are stages which confront decline in sales.

This is due to several reasons like increased competition, difficult business environment,

uncertainties in factors affecting sales volume, etc. reduction in sales volume puts direct impact

on revenue generation cycle and growth opportunities of business. This istuation is usually

confronted in maturity and decline stage of business.

Increased cost of raw materials: Increase in cost of raw materials can be due to multiple factors

such as increase in prices of logistics, increase in bargaining power of vendor, taxes hike, etc.

Increase in cost increases operational expenses and decreases profit margin. It can also lead to

increase in price of product which again can have negative impact on sales of company products.

Financial governance – It refers to the system of practices in which a company control

its financial information. Companies track their financial transactions and perform control

operations in the interest of its stakeholders. If a company is able to identify its risk earlier, it can

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

devise a strategy accordingly to avoid it. Proper governance with monitoring and control allows

an organisation to identify the risk coming its way faster.

Benchmarking - There are multiple companies working in an industry as close

competition of each other. Benchmarking is a performance indicator in which

performance of one particular organisation is taken as standard of average performance of

the other company's of that industry. This technique is used by managers to identify the

areas where they can improve to reach benchmark.

Key performance indicators (KPI) – This technique is used to assess the multiple aspects

that effect an organisation. They can be financial and non-financial aspects. Financial

aspects includes indicators such as profits, debts, etc. while non-financial aspects refers to

the external factors such technological factors, market factors, etc.

Budgetary targets – Companies prepare multiple budgets and budgetary targets. Managers then

evaluate organisation's actual performance against those set targets. Deviations are determined

and corrective measures are taken

Conclusion

In above report, various concepts relating to management accounting have been

understood. This will help in formulating effective and efficient business strategies for future.

This formulation is in accordance of the objective to gain maximized profits. Concept of

management accounting relates to every function of organization so that overall performance can

be ensured.

an organisation to identify the risk coming its way faster.

Benchmarking - There are multiple companies working in an industry as close

competition of each other. Benchmarking is a performance indicator in which

performance of one particular organisation is taken as standard of average performance of

the other company's of that industry. This technique is used by managers to identify the

areas where they can improve to reach benchmark.

Key performance indicators (KPI) – This technique is used to assess the multiple aspects

that effect an organisation. They can be financial and non-financial aspects. Financial

aspects includes indicators such as profits, debts, etc. while non-financial aspects refers to

the external factors such technological factors, market factors, etc.

Budgetary targets – Companies prepare multiple budgets and budgetary targets. Managers then

evaluate organisation's actual performance against those set targets. Deviations are determined

and corrective measures are taken

Conclusion

In above report, various concepts relating to management accounting have been

understood. This will help in formulating effective and efficient business strategies for future.

This formulation is in accordance of the objective to gain maximized profits. Concept of

management accounting relates to every function of organization so that overall performance can

be ensured.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Books and Journals

Chan, L.H. and et.al., 2015. Substitution between real and accruals-based earnings management

after voluntary adoption of compensation clawback provisions. The Accounting

Review. 90(1). pp.147-174.

Cheng, Q., Lee, J. and Shevlin, T., 2016. Internal governance and real earnings management. The

accounting review, 91(4), pp.1051-1085.

Christensen, M., Skærbæk, P. and Tryggestad, K., 2019. Contested organizational change and

accounting in trials of incompatibility. Management Accounting Research. 45. p.100641.

Dunbar, K., Laing, G. and Wynder, M., 2016. A Content Analysis of Accounting Job

Advertisements: Skill Requirements for Graduates. e-Journal of Business Education and

Scholarship of Teaching. 10(1). pp.58-72.

Ho, S.S. and et.al., 2015. CEO gender, ethical leadership, and accounting conservatism. Journal

of Business Ethics. 127(2). pp.351-370.

Hrabal, M., 2016. Process-Oriented Managerial Accounting. International advances in economic

research. 22(2). pp.225-227.

Lippert, I., 2015. Environment as datascape: Enacting emission realities in corporate carbon

accounting. Geoforum. 66. pp.126-135.

Shipman, J.E., Swanquist, Q.T. and Whited, R.L., 2017. Propensity score matching in accounting

research. The Accounting Review. 92(1). pp.213-244.

Sithole, S., 2015. Quality in accounting graduates: Employer expectations of the graduate skills

in the bachelor of accounting degree. European Scientific Journal, 11(22), pp.165-180.

Books and Journals

Chan, L.H. and et.al., 2015. Substitution between real and accruals-based earnings management

after voluntary adoption of compensation clawback provisions. The Accounting

Review. 90(1). pp.147-174.

Cheng, Q., Lee, J. and Shevlin, T., 2016. Internal governance and real earnings management. The

accounting review, 91(4), pp.1051-1085.

Christensen, M., Skærbæk, P. and Tryggestad, K., 2019. Contested organizational change and

accounting in trials of incompatibility. Management Accounting Research. 45. p.100641.

Dunbar, K., Laing, G. and Wynder, M., 2016. A Content Analysis of Accounting Job

Advertisements: Skill Requirements for Graduates. e-Journal of Business Education and

Scholarship of Teaching. 10(1). pp.58-72.

Ho, S.S. and et.al., 2015. CEO gender, ethical leadership, and accounting conservatism. Journal

of Business Ethics. 127(2). pp.351-370.

Hrabal, M., 2016. Process-Oriented Managerial Accounting. International advances in economic

research. 22(2). pp.225-227.

Lippert, I., 2015. Environment as datascape: Enacting emission realities in corporate carbon

accounting. Geoforum. 66. pp.126-135.

Shipman, J.E., Swanquist, Q.T. and Whited, R.L., 2017. Propensity score matching in accounting

research. The Accounting Review. 92(1). pp.213-244.

Sithole, S., 2015. Quality in accounting graduates: Employer expectations of the graduate skills

in the bachelor of accounting degree. European Scientific Journal, 11(22), pp.165-180.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.