Unit 5: Management Accounting Principles and Techniques Report

VerifiedAdded on 2023/04/10

|13

|1060

|234

Report

AI Summary

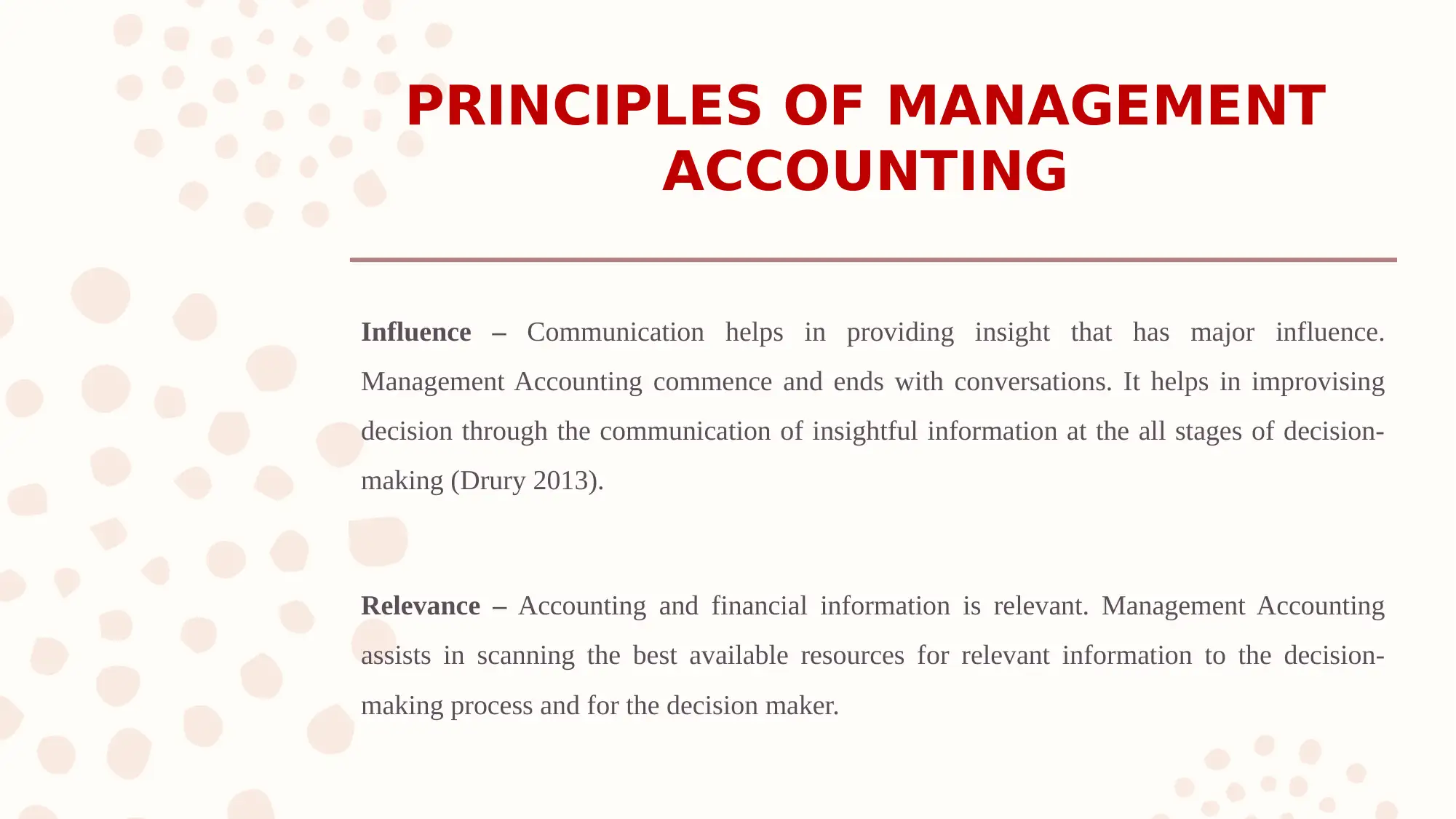

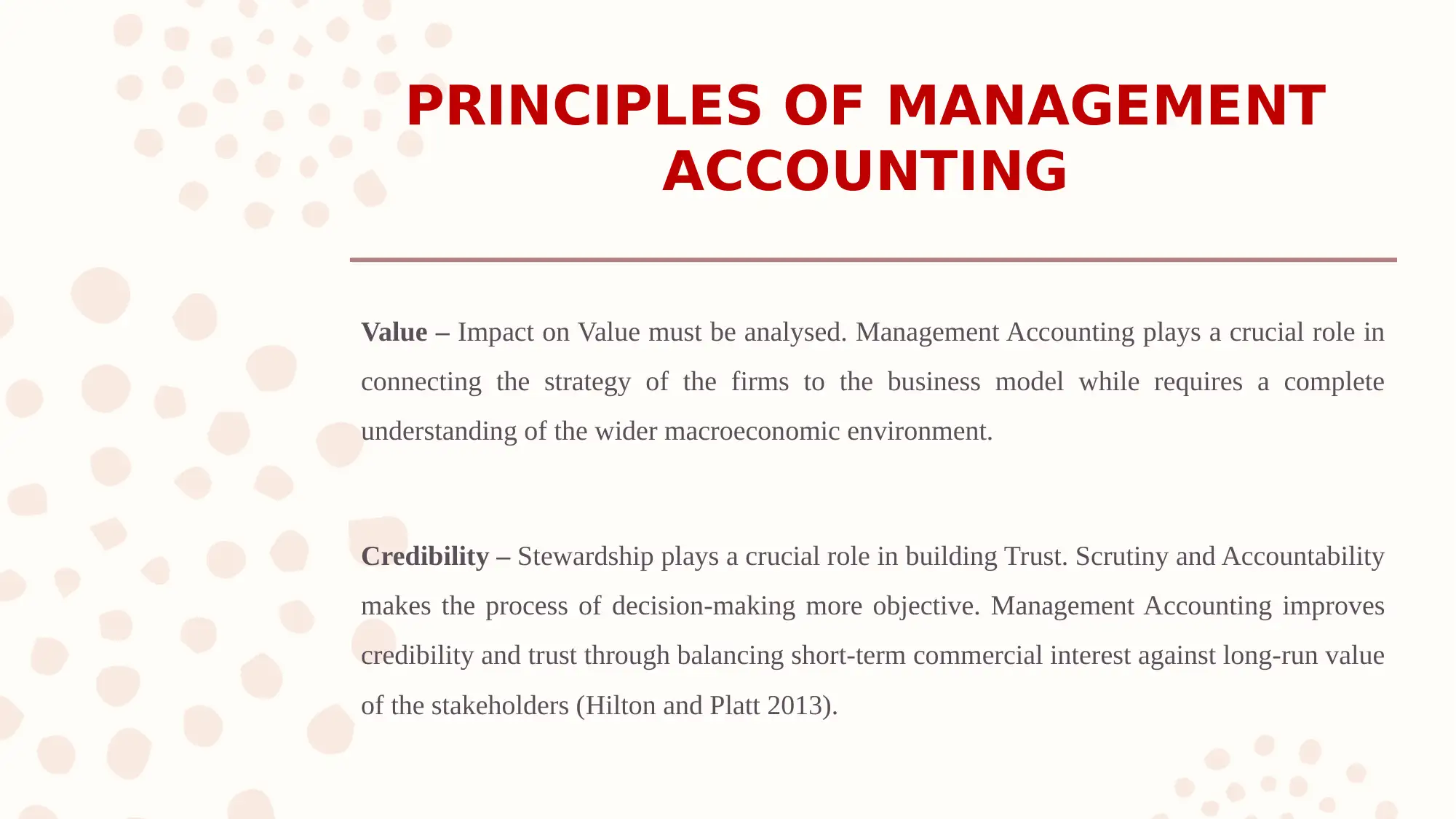

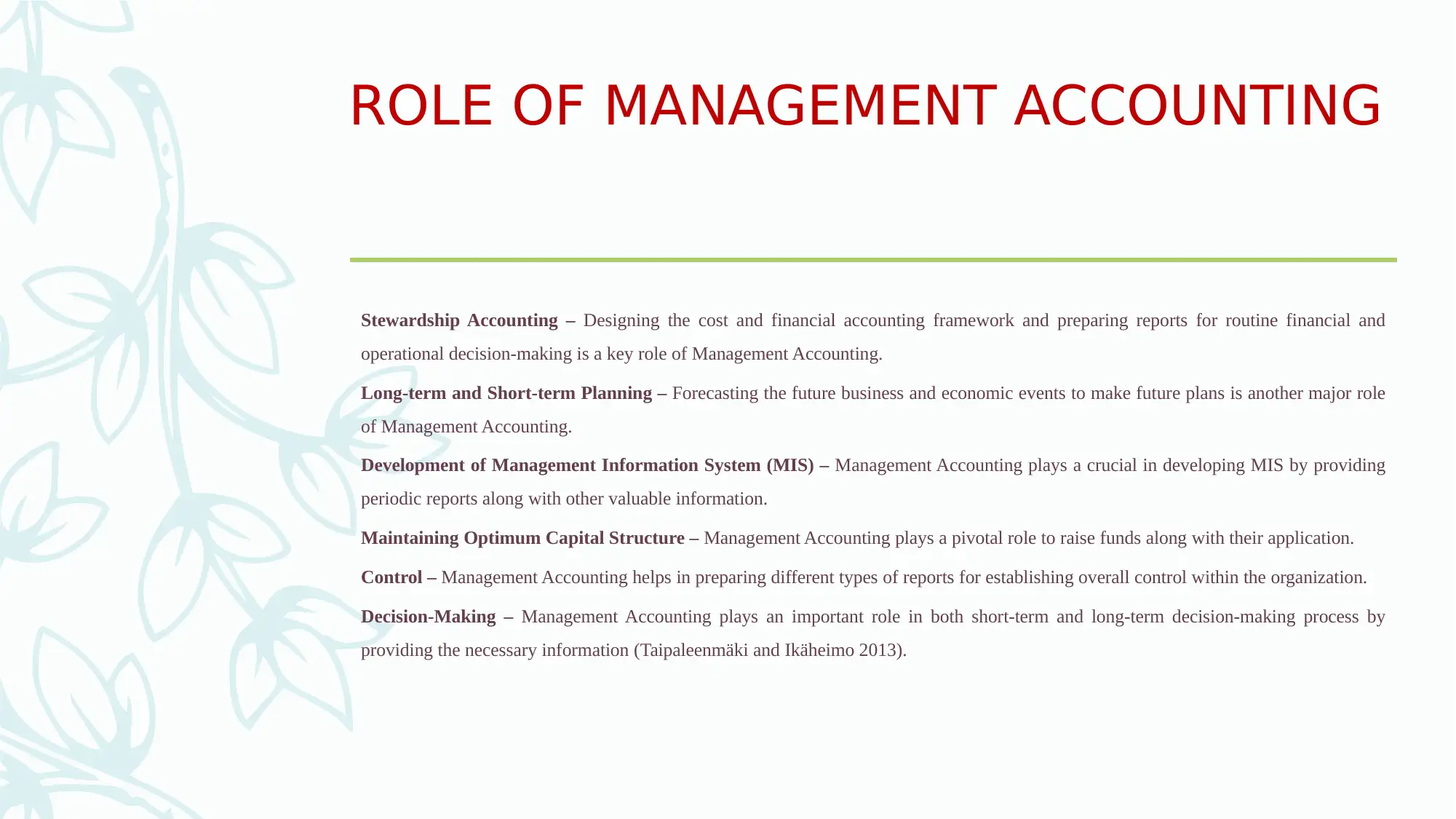

This report delves into the core principles of management accounting, emphasizing their significance in informed decision-making. It explores the influence of communication, relevance of information, and the importance of value and credibility within management accounting practices. The report outlines key roles, including stewardship accounting, long-term and short-term planning, development of Management Information Systems (MIS), and maintaining optimal capital structure. It also covers various techniques and methods, such as financial planning, cost accounting, and budgetary control, along with their application through income statements under marginal and absorption costing. The integration of management accounting within an organization is discussed, highlighting continuous improvements, quality management, and the benefits of these functions, including forecasting, organizing, and performance control. The report concludes with a comprehensive overview of the benefits of management accounting to organizations, detailing the role of financial analysis, communication, and asset protection. This assignment is a comprehensive overview of the subject, providing a solid foundation for understanding and applying management accounting principles.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.