Management Accounting: Principles, Integration, Tools & Techniques

VerifiedAdded on 2023/06/08

|15

|4769

|244

Report

AI Summary

This report provides a comprehensive overview of management accounting, covering its principles, roles, and techniques. It begins by outlining key management accounting principles such as data presentation, accuracy, stability, punctuality, exception handling, efficiency measurement, and resource utilization. The report then discusses the roles of management accounting, including data provision, data modification, communication facilitation, control, qualitative information provision, policy formulation, and coordination. It further explores the use of techniques like marginal costing and absorption costing, presenting calculations for an income statement using variable costing. The integration of management accounting within an organization is also examined, highlighting its importance in decision-making and strategic analysis. The report concludes with a comparison of management accounting tools and recommendations for sustainable commercial enterprise.

Unit 5-Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

PART 1............................................................................................................................................3

1.Management Accounting Principles........................................................................................3

2. Role of management accounting and its systems:...................................................................4

3. Use of techniques and methods in management accounting by presenting calculations for an

income statement using variable costings:..................................................................................5

4. Integration of management accounting within the organisation:............................................7

5. Advantages of Management Accounting Functions To The Organisations:..........................8

6.Conclusion................................................................................................................................9

PART 2............................................................................................................................................9

1. Comparison between management accounting tools:.............................................................9

2. Application of management accounting for solving financial problems:.............................12

3. Recommendations for sustainable commercial enterprise....................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................3

PART 1............................................................................................................................................3

1.Management Accounting Principles........................................................................................3

2. Role of management accounting and its systems:...................................................................4

3. Use of techniques and methods in management accounting by presenting calculations for an

income statement using variable costings:..................................................................................5

4. Integration of management accounting within the organisation:............................................7

5. Advantages of Management Accounting Functions To The Organisations:..........................8

6.Conclusion................................................................................................................................9

PART 2............................................................................................................................................9

1. Comparison between management accounting tools:.............................................................9

2. Application of management accounting for solving financial problems:.............................12

3. Recommendations for sustainable commercial enterprise....................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Management accounting is an activity which includes a process of identifying, analysing

and gathering of all the important information which can improve the decisions of the

management. In present time where there is large competition in the market management

accounting plays a very vital role for the organisation (Baxter and et.al., 2019). Through the

management accounting the organisation can make an effective plan which can help them to beat

their competitors in the market. It is considered as universal activity which is used in every kind

of organisation whether it can be profit making or non profit like NGOs. This report contains two

parts 1st parts is completely include management principles and 2nd part contains effective

planning tools for managing accounts. In the part first all the important terms likes principles,

roles and importance of management accounting are explained completely with the tools and

techniques. While second part includes multiple management methods and comparisons between

them.

PART 1

1.Management Accounting Principles

Management accounting principles is a group of events which have to perform by the

organisation so that they can achieve their aim of the businesses effectively and efficiently.

These principles includes the plans and information through which the organisation can perform

their activities. The informations which are included in the principles of management accounting

can be monetary and non monetary. Some management accounting principles are as follows-

Presentation of Actual Data- The very first principles of management accounting is

presentation of actual data. It means that the organisations have to present the actual and accurate

data so that they can manage their business activities effectively. The data which is presented to

the manager must be unbiased. It should not be based on the likes and dislike of anyone. If this

type of activity is held in the organisation then the organisation can face the consequences and

issues while running their business activities.

Accuracy of Accounts- This principles of management accounting should be applied on

all the businesses department (Behnami and et.al., 2019). If the data of all the department are not

accurate then the managers of the organisation cannot be able to make the effective decisions and

the growth of the businesses also get affected.

Management accounting is an activity which includes a process of identifying, analysing

and gathering of all the important information which can improve the decisions of the

management. In present time where there is large competition in the market management

accounting plays a very vital role for the organisation (Baxter and et.al., 2019). Through the

management accounting the organisation can make an effective plan which can help them to beat

their competitors in the market. It is considered as universal activity which is used in every kind

of organisation whether it can be profit making or non profit like NGOs. This report contains two

parts 1st parts is completely include management principles and 2nd part contains effective

planning tools for managing accounts. In the part first all the important terms likes principles,

roles and importance of management accounting are explained completely with the tools and

techniques. While second part includes multiple management methods and comparisons between

them.

PART 1

1.Management Accounting Principles

Management accounting principles is a group of events which have to perform by the

organisation so that they can achieve their aim of the businesses effectively and efficiently.

These principles includes the plans and information through which the organisation can perform

their activities. The informations which are included in the principles of management accounting

can be monetary and non monetary. Some management accounting principles are as follows-

Presentation of Actual Data- The very first principles of management accounting is

presentation of actual data. It means that the organisations have to present the actual and accurate

data so that they can manage their business activities effectively. The data which is presented to

the manager must be unbiased. It should not be based on the likes and dislike of anyone. If this

type of activity is held in the organisation then the organisation can face the consequences and

issues while running their business activities.

Accuracy of Accounts- This principles of management accounting should be applied on

all the businesses department (Behnami and et.al., 2019). If the data of all the department are not

accurate then the managers of the organisation cannot be able to make the effective decisions and

the growth of the businesses also get affected.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Stability and Consistency- The plan of action and the process of management

accounting must be stable and consistent. It is because if the these are changing continuously

then managers of the organisations cannot be able to focus on the objectives and can face the

losses in future (Bhatia and Mulenga, 2019).

Punctuality- Punctuality is considered as the most important principle of the

management of accounting. It is because If the managers of the organisations gets correct

information at the right time then they can take very effective decision for the growth of the

businesses.

Principle of Exception- The next principle of management accounting is principles of

exception. The main objective of this principle is to provide the focus of the managers towards

exceptional important problems. If any difference is observed between estimated result and the

actual result. Then it is very important for the managers to make a report on that matter and

explain the cause of that differences.

Measuring Efficiency- The another important principle of management accounting is to

measure the efficiency of the managers in different management related activities. Various tools

of ratio analysis and management accounting are utilise in that case.

Best Utilisation of Resources- In this principle the managers have to be ensure that the

resources of the organisation are to be utilise efficiently or not. If the the resources of the

organisation are not utilised perfectly then through management accounting the managers can

bring back their position in the market again.

2. Role of management accounting and its systems:

The role of management accounting are as follows-

Provide Data- The very first role of management accounting is that it helps the

organisation by providing data (Brescia and et.al., 2019). The organisations contains the data in a

very large quantity and management accounting helps the organisation to manage the data in a

proper way so that the managers can easily take the important decisions regarding to the

improvement.

Modify The Data- The next and very important role of management accounting is to

modify the available data in a effective way which can easily understandable to the management.

This function became very useful for the management. Through the modified data the

organisation can easily make the effective and efficient decisions for the improvement.

accounting must be stable and consistent. It is because if the these are changing continuously

then managers of the organisations cannot be able to focus on the objectives and can face the

losses in future (Bhatia and Mulenga, 2019).

Punctuality- Punctuality is considered as the most important principle of the

management of accounting. It is because If the managers of the organisations gets correct

information at the right time then they can take very effective decision for the growth of the

businesses.

Principle of Exception- The next principle of management accounting is principles of

exception. The main objective of this principle is to provide the focus of the managers towards

exceptional important problems. If any difference is observed between estimated result and the

actual result. Then it is very important for the managers to make a report on that matter and

explain the cause of that differences.

Measuring Efficiency- The another important principle of management accounting is to

measure the efficiency of the managers in different management related activities. Various tools

of ratio analysis and management accounting are utilise in that case.

Best Utilisation of Resources- In this principle the managers have to be ensure that the

resources of the organisation are to be utilise efficiently or not. If the the resources of the

organisation are not utilised perfectly then through management accounting the managers can

bring back their position in the market again.

2. Role of management accounting and its systems:

The role of management accounting are as follows-

Provide Data- The very first role of management accounting is that it helps the

organisation by providing data (Brescia and et.al., 2019). The organisations contains the data in a

very large quantity and management accounting helps the organisation to manage the data in a

proper way so that the managers can easily take the important decisions regarding to the

improvement.

Modify The Data- The next and very important role of management accounting is to

modify the available data in a effective way which can easily understandable to the management.

This function became very useful for the management. Through the modified data the

organisation can easily make the effective and efficient decisions for the improvement.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Communication- Management accounting also plays a very important in the

communication (Egan and Tweedie, 2018). Through management accounting the organisation

can communicate the information between the top level, middle level and lower level. It is

because the management accounting consist all types of information like top level require the

information of long interval, middle level require the information of regular interval and lower

level require the information of short interval. And all these types of information can be provided

by the management accounting.

Facilitate control- Management accounting helps the organisation in evaluating the

objectives and plan of the businesses. It include the specific time in the which the organisations

have to achieve their goals. All these things can be happen through the budgetary control and

standard costing, and both them are consider as a very important part of the management

accounting.

Qualitative Information- Management accounting is not only provide the financial data

but also provide the qualitative information to the organisation. These informations can only be

carried out by the special surveys, mathematical collections, engineering records and many more.

Policy Formulation- The next and very important role of management accounting is

policy formulation. It is because it provide numerical data and costing which can be utilised in

setting up of goals and formation of upcoming period policies.

Coordinating- The next and last role of management accounting is coordination.

Through management accounting the organisation can easily coordinate their activities by

making of functional budget, then coordinating the complete activities of the businesses, at first ,

by making functional budget and at last coordinate all the event of budget so that the master

budget can be prepared.

3. Use of techniques and methods in management accounting by presenting calculations for an

income statement using variable costings:

The amount which is spend on acquiring of an assets or producing of commodity in the

business organisation called cost. The cost can divided into two parts fixed cost and variable cost

(Fisher, 2018). Fixed cost are those cost which does not with the change in the production

capacity while variable cost are those cost which can change with change in production

production capacity. The different types of costing are as follows-

communication (Egan and Tweedie, 2018). Through management accounting the organisation

can communicate the information between the top level, middle level and lower level. It is

because the management accounting consist all types of information like top level require the

information of long interval, middle level require the information of regular interval and lower

level require the information of short interval. And all these types of information can be provided

by the management accounting.

Facilitate control- Management accounting helps the organisation in evaluating the

objectives and plan of the businesses. It include the specific time in the which the organisations

have to achieve their goals. All these things can be happen through the budgetary control and

standard costing, and both them are consider as a very important part of the management

accounting.

Qualitative Information- Management accounting is not only provide the financial data

but also provide the qualitative information to the organisation. These informations can only be

carried out by the special surveys, mathematical collections, engineering records and many more.

Policy Formulation- The next and very important role of management accounting is

policy formulation. It is because it provide numerical data and costing which can be utilised in

setting up of goals and formation of upcoming period policies.

Coordinating- The next and last role of management accounting is coordination.

Through management accounting the organisation can easily coordinate their activities by

making of functional budget, then coordinating the complete activities of the businesses, at first ,

by making functional budget and at last coordinate all the event of budget so that the master

budget can be prepared.

3. Use of techniques and methods in management accounting by presenting calculations for an

income statement using variable costings:

The amount which is spend on acquiring of an assets or producing of commodity in the

business organisation called cost. The cost can divided into two parts fixed cost and variable cost

(Fisher, 2018). Fixed cost are those cost which does not with the change in the production

capacity while variable cost are those cost which can change with change in production

production capacity. The different types of costing are as follows-

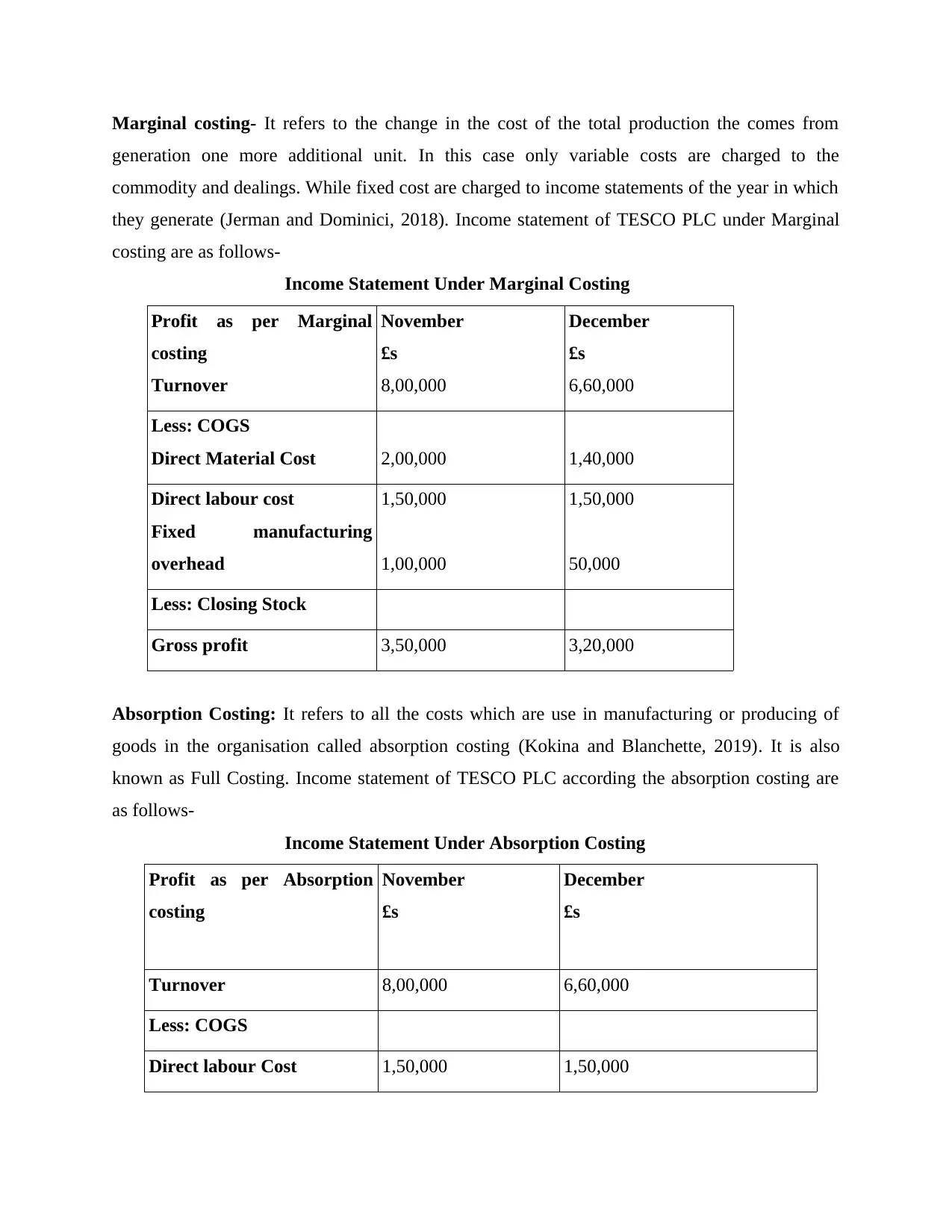

Marginal costing- It refers to the change in the cost of the total production the comes from

generation one more additional unit. In this case only variable costs are charged to the

commodity and dealings. While fixed cost are charged to income statements of the year in which

they generate (Jerman and Dominici, 2018). Income statement of TESCO PLC under Marginal

costing are as follows-

Income Statement Under Marginal Costing

Profit as per Marginal

costing

Turnover

November

£s

8,00,000

December

£s

6,60,000

Less: COGS

Direct Material Cost 2,00,000 1,40,000

Direct labour cost

Fixed manufacturing

overhead

1,50,000

1,00,000

1,50,000

50,000

Less: Closing Stock

Gross profit 3,50,000 3,20,000

Absorption Costing: It refers to all the costs which are use in manufacturing or producing of

goods in the organisation called absorption costing (Kokina and Blanchette, 2019). It is also

known as Full Costing. Income statement of TESCO PLC according the absorption costing are

as follows-

Income Statement Under Absorption Costing

Profit as per Absorption

costing

November

£s

December

£s

Turnover 8,00,000 6,60,000

Less: COGS

Direct labour Cost 1,50,000 1,50,000

generation one more additional unit. In this case only variable costs are charged to the

commodity and dealings. While fixed cost are charged to income statements of the year in which

they generate (Jerman and Dominici, 2018). Income statement of TESCO PLC under Marginal

costing are as follows-

Income Statement Under Marginal Costing

Profit as per Marginal

costing

Turnover

November

£s

8,00,000

December

£s

6,60,000

Less: COGS

Direct Material Cost 2,00,000 1,40,000

Direct labour cost

Fixed manufacturing

overhead

1,50,000

1,00,000

1,50,000

50,000

Less: Closing Stock

Gross profit 3,50,000 3,20,000

Absorption Costing: It refers to all the costs which are use in manufacturing or producing of

goods in the organisation called absorption costing (Kokina and Blanchette, 2019). It is also

known as Full Costing. Income statement of TESCO PLC according the absorption costing are

as follows-

Income Statement Under Absorption Costing

Profit as per Absorption

costing

November

£s

December

£s

Turnover 8,00,000 6,60,000

Less: COGS

Direct labour Cost 1,50,000 1,50,000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

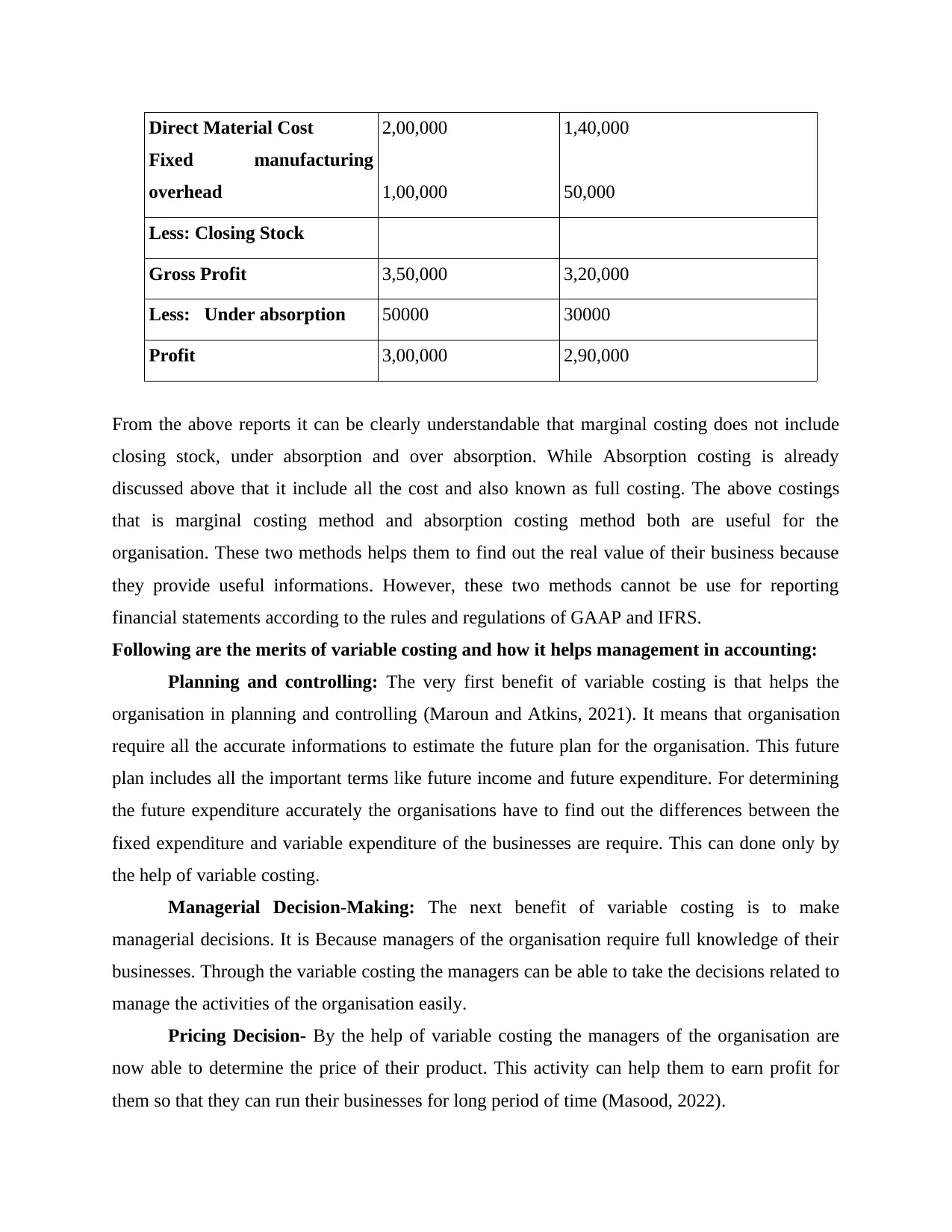

Direct Material Cost

Fixed manufacturing

overhead

2,00,000

1,00,000

1,40,000

50,000

Less: Closing Stock

Gross Profit 3,50,000 3,20,000

Less: Under absorption 50000 30000

Profit 3,00,000 2,90,000

From the above reports it can be clearly understandable that marginal costing does not include

closing stock, under absorption and over absorption. While Absorption costing is already

discussed above that it include all the cost and also known as full costing. The above costings

that is marginal costing method and absorption costing method both are useful for the

organisation. These two methods helps them to find out the real value of their business because

they provide useful informations. However, these two methods cannot be use for reporting

financial statements according to the rules and regulations of GAAP and IFRS.

Following are the merits of variable costing and how it helps management in accounting:

Planning and controlling: The very first benefit of variable costing is that helps the

organisation in planning and controlling (Maroun and Atkins, 2021). It means that organisation

require all the accurate informations to estimate the future plan for the organisation. This future

plan includes all the important terms like future income and future expenditure. For determining

the future expenditure accurately the organisations have to find out the differences between the

fixed expenditure and variable expenditure of the businesses are require. This can done only by

the help of variable costing.

Managerial Decision-Making: The next benefit of variable costing is to make

managerial decisions. It is Because managers of the organisation require full knowledge of their

businesses. Through the variable costing the managers can be able to take the decisions related to

manage the activities of the organisation easily.

Pricing Decision- By the help of variable costing the managers of the organisation are

now able to determine the price of their product. This activity can help them to earn profit for

them so that they can run their businesses for long period of time (Masood, 2022).

Fixed manufacturing

overhead

2,00,000

1,00,000

1,40,000

50,000

Less: Closing Stock

Gross Profit 3,50,000 3,20,000

Less: Under absorption 50000 30000

Profit 3,00,000 2,90,000

From the above reports it can be clearly understandable that marginal costing does not include

closing stock, under absorption and over absorption. While Absorption costing is already

discussed above that it include all the cost and also known as full costing. The above costings

that is marginal costing method and absorption costing method both are useful for the

organisation. These two methods helps them to find out the real value of their business because

they provide useful informations. However, these two methods cannot be use for reporting

financial statements according to the rules and regulations of GAAP and IFRS.

Following are the merits of variable costing and how it helps management in accounting:

Planning and controlling: The very first benefit of variable costing is that helps the

organisation in planning and controlling (Maroun and Atkins, 2021). It means that organisation

require all the accurate informations to estimate the future plan for the organisation. This future

plan includes all the important terms like future income and future expenditure. For determining

the future expenditure accurately the organisations have to find out the differences between the

fixed expenditure and variable expenditure of the businesses are require. This can done only by

the help of variable costing.

Managerial Decision-Making: The next benefit of variable costing is to make

managerial decisions. It is Because managers of the organisation require full knowledge of their

businesses. Through the variable costing the managers can be able to take the decisions related to

manage the activities of the organisation easily.

Pricing Decision- By the help of variable costing the managers of the organisation are

now able to determine the price of their product. This activity can help them to earn profit for

them so that they can run their businesses for long period of time (Masood, 2022).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Integration of management accounting within the organisation:

Today's managers cannot forget the status of the management accountant, as the

opposition increasingly demands high-quality services and products. According to a survey, for

all industries, the follow-up factors prioritized by managers are: "buyer satisfaction, product or

product quality, operation and control of control operations, business profitability". To achieve

this, managers felt they needed a solid control machine, and control accounting was seen as the

primary means of guiding them to achieve their stated aspirations (Matějka, Merchant and

O'Grady, 2021). Through many studies, it is clear that managerial accounting is more valued and

relevant to the production industry as they have to constantly show their production expenses,

manage their pricing, budget their capital to maximize gifts and future availability Sustainability,

and effective options. Because agencies can differ according to their operations and activities,

controlling accountants must be hired through a foundational approach that identifies the

fundamental operational components of each unit or division. There are many management

accounting strategies such as Activity Based Costing (ABC), Grenzplankosterechnung (GPK),

Lean Accounting, Resource Intake Accounting (RCA), etc. ABC, GPK, and RCA are the most

popular because they are suitable for a variety of businesses. One of the most reliable techniques

to ensure the statistical function of cost accounting control accounting is to combine different

management accounting techniques in strategic analysis and guiding statistical improvement. In

this regard, the opportunity to integrate some of these methods must be continually exploited to

ensure that the lifestyle of control accounting is equally accurate and specific. Over a long period

of time, the overall performance of the company has improved, ending with positive advantages,

in addition, the control system is equipped with a help machine that can meet its wishes. One of

the strongest techniques to apply when looking to create a subculture in an institution is a worthy

lifestyle. This leads to an addiction to overall performance or that the technique continues to

improve even further. A successful management accounting software can be illustrated in many

ways, including: maximization of an organization's assets, continued control of expenses as the

organization's profits grow, and better employee and buyer satisfaction.

5. Advantages of Management Accounting Functions To The Organisations:

Inventory Management System- This function of management accounting helps the

organisation be managing the inventory. TESCO PLC have face the issues like lack of inventory

and increasing of wastage before adopting this system (Ofoegbu, Okaro and Okafor, 2018). But

Today's managers cannot forget the status of the management accountant, as the

opposition increasingly demands high-quality services and products. According to a survey, for

all industries, the follow-up factors prioritized by managers are: "buyer satisfaction, product or

product quality, operation and control of control operations, business profitability". To achieve

this, managers felt they needed a solid control machine, and control accounting was seen as the

primary means of guiding them to achieve their stated aspirations (Matějka, Merchant and

O'Grady, 2021). Through many studies, it is clear that managerial accounting is more valued and

relevant to the production industry as they have to constantly show their production expenses,

manage their pricing, budget their capital to maximize gifts and future availability Sustainability,

and effective options. Because agencies can differ according to their operations and activities,

controlling accountants must be hired through a foundational approach that identifies the

fundamental operational components of each unit or division. There are many management

accounting strategies such as Activity Based Costing (ABC), Grenzplankosterechnung (GPK),

Lean Accounting, Resource Intake Accounting (RCA), etc. ABC, GPK, and RCA are the most

popular because they are suitable for a variety of businesses. One of the most reliable techniques

to ensure the statistical function of cost accounting control accounting is to combine different

management accounting techniques in strategic analysis and guiding statistical improvement. In

this regard, the opportunity to integrate some of these methods must be continually exploited to

ensure that the lifestyle of control accounting is equally accurate and specific. Over a long period

of time, the overall performance of the company has improved, ending with positive advantages,

in addition, the control system is equipped with a help machine that can meet its wishes. One of

the strongest techniques to apply when looking to create a subculture in an institution is a worthy

lifestyle. This leads to an addiction to overall performance or that the technique continues to

improve even further. A successful management accounting software can be illustrated in many

ways, including: maximization of an organization's assets, continued control of expenses as the

organization's profits grow, and better employee and buyer satisfaction.

5. Advantages of Management Accounting Functions To The Organisations:

Inventory Management System- This function of management accounting helps the

organisation be managing the inventory. TESCO PLC have face the issues like lack of inventory

and increasing of wastage before adopting this system (Ofoegbu, Okaro and Okafor, 2018). But

after applying this system they area able to manage their inventory and also reduce the wastage

which increase their profitability.

Cost bookkeeping system- The next function of management accounting is cost

bookkeeping system. It helps the organisation by determining the each cost which incurred in the

operations of the businesses (Phan, Yapa and Nguyen, 2020). After adopting this function

TESCO PLC is now able to analyse or evaluate the performance of the business regarding to the

operations.

6.Conclusion

From the part 1st of this report it can be concluded that the management accounting is

considered as very integral part of the organisation. Through the management accounting the

TESCO PLC is now able to determine their growth of the businesses in the future. In this part

various costing methods are also discussed above which are marginal costing methods and

absorption costing method. These two methods helps the TESCO PLC in determining their cost

through which they decide their prices of the product. The TESCO PLC also able to find out the

their fixed and variable costs through which they can estimate their future performance.

PART 2

1. Comparison between management accounting tools:

Financial Planning and Analysis:

The position of the organisations can be evaluate by the four main activities which are

planning, budgeting, performance reporting and management. All these activities helps the

businesses to run their operations effectively (Roberts, 2020).

Various Advantages and Disadvantages of financial planning Analysis are as follows-

Advantages Disadvantages

It help the organisation in determining the

expenses through which they can estimate their

their funds which they require in future. This

will helps them to finding out the future

opportunities to grow their business operations.

This activity can be done by the professionals

only. Because it requires a separate set of

knowledge and skill. So organisations have to

hire the professionals which require huge

amount of funds.

which increase their profitability.

Cost bookkeeping system- The next function of management accounting is cost

bookkeeping system. It helps the organisation by determining the each cost which incurred in the

operations of the businesses (Phan, Yapa and Nguyen, 2020). After adopting this function

TESCO PLC is now able to analyse or evaluate the performance of the business regarding to the

operations.

6.Conclusion

From the part 1st of this report it can be concluded that the management accounting is

considered as very integral part of the organisation. Through the management accounting the

TESCO PLC is now able to determine their growth of the businesses in the future. In this part

various costing methods are also discussed above which are marginal costing methods and

absorption costing method. These two methods helps the TESCO PLC in determining their cost

through which they decide their prices of the product. The TESCO PLC also able to find out the

their fixed and variable costs through which they can estimate their future performance.

PART 2

1. Comparison between management accounting tools:

Financial Planning and Analysis:

The position of the organisations can be evaluate by the four main activities which are

planning, budgeting, performance reporting and management. All these activities helps the

businesses to run their operations effectively (Roberts, 2020).

Various Advantages and Disadvantages of financial planning Analysis are as follows-

Advantages Disadvantages

It help the organisation in determining the

expenses through which they can estimate their

their funds which they require in future. This

will helps them to finding out the future

opportunities to grow their business operations.

This activity can be done by the professionals

only. Because it requires a separate set of

knowledge and skill. So organisations have to

hire the professionals which require huge

amount of funds.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Through the financial planning and analysis

the managers will able to manage the debts of

their businesses. It is because the analysis

include various ratios through which they can

easily determine assets and liabilities of the

businesses.

The next demerit of the financial planning and

analysis is that it only focus on the monetary

information and ignore the non monetary data.

Some time it will lead to them to bring chaos

and confusion in the organisation.

Through this analysis the organisation can be

able to maintain the liquidity in the

organisation. This can only be done by

determining the payment of the organisation.

The organisation can extend their payments

time with their creditors. Through they can

maintain the liquidity balance.

Financial planning and analysis are totally

based on principles and concepts. If the value

of raw material and finished good of the

organisation are carried out wrong. Then it will

lead the organisation to losses.

Through the financial planning and analysis

the organisation will be able to determine the

risks. Through this also able to increase their

efficiency of doing operations.

The financial planning and analysis includes

the data and documents. All these informations

are totally based on estimation of future. These

can also be inaccurate and the organisation can

face the losses also.

Cost Accounting:

Cost accounting refers to the process which include recording of all the transactions

related to the cost which are incurred in business activity are known as cost accounting (Saputro,

Wardi and Abror, 2018). It contains some merits and demerits which are as follows-

Merits Demerits

Cost accounting helps the organisation in

understanding the frame work that how the

cost has been incurred in the operations of the

business activities.

The cost accounting does not include include

the present data it always contain historical

data. That only past performance of the

company can be evaluate.

It helps in determining the losses or profit of

the company. It is very important for the

Costs always keep varies every year. It is

because the raw material, wages of labour are

the managers will able to manage the debts of

their businesses. It is because the analysis

include various ratios through which they can

easily determine assets and liabilities of the

businesses.

The next demerit of the financial planning and

analysis is that it only focus on the monetary

information and ignore the non monetary data.

Some time it will lead to them to bring chaos

and confusion in the organisation.

Through this analysis the organisation can be

able to maintain the liquidity in the

organisation. This can only be done by

determining the payment of the organisation.

The organisation can extend their payments

time with their creditors. Through they can

maintain the liquidity balance.

Financial planning and analysis are totally

based on principles and concepts. If the value

of raw material and finished good of the

organisation are carried out wrong. Then it will

lead the organisation to losses.

Through the financial planning and analysis

the organisation will be able to determine the

risks. Through this also able to increase their

efficiency of doing operations.

The financial planning and analysis includes

the data and documents. All these informations

are totally based on estimation of future. These

can also be inaccurate and the organisation can

face the losses also.

Cost Accounting:

Cost accounting refers to the process which include recording of all the transactions

related to the cost which are incurred in business activity are known as cost accounting (Saputro,

Wardi and Abror, 2018). It contains some merits and demerits which are as follows-

Merits Demerits

Cost accounting helps the organisation in

understanding the frame work that how the

cost has been incurred in the operations of the

business activities.

The cost accounting does not include include

the present data it always contain historical

data. That only past performance of the

company can be evaluate.

It helps in determining the losses or profit of

the company. It is very important for the

Costs always keep varies every year. It is

because the raw material, wages of labour are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation to determine the profit or loss so

that they can estimate their tax amount to be

paid or also helps in determining their

positions.

changing regularly due to the economic factors

like inflation, recession, or changing in the

policies of the government.

If there is a regular evaluation of cost held in

the organisation then it will also reduce the

fraud which can be done in the organisation

due to greedy nature of the employees and

workers.

Cost accounting require proper maintenance

regularly. Without maintaining them properly

the organisation cannot be able to estimate the

future profit earning opportunities.

It also helps the organisation in forecasting the

future growth of the businesses. Because cost

accounting shows the pattern of the business

that how it expand their money in their

operations. Through this information the

managers of the organisation are able to

forecast growth.

The next demerit of the cost accounting is hat

it require an expert who knows hoe record all

the transaction and how analyse them. For

hiring an expert the organisations require

money which also increase the costs.

Budgetary Control:

It is defined as proper plan which helps the organisations manges their incomes and

expenditures (Tingey-Holyoak and et.al., 2020). It is considered as document through the

managers perform their operations.

The advantages and disadvantages of budgetary control are as follows-

Advantages Disadvantages

It helps the organisation in analysing the

performance of the businesses.

Budgetary control require so much time to

prepare and also not easy to make it effective.

This tool helps the businesses in finding out

the sectors in which require modification for

their benefits..

It create some kind of barrier to the employees

due to which the they are not able to work

freely as result the employees starts feeling

demotivated.

that they can estimate their tax amount to be

paid or also helps in determining their

positions.

changing regularly due to the economic factors

like inflation, recession, or changing in the

policies of the government.

If there is a regular evaluation of cost held in

the organisation then it will also reduce the

fraud which can be done in the organisation

due to greedy nature of the employees and

workers.

Cost accounting require proper maintenance

regularly. Without maintaining them properly

the organisation cannot be able to estimate the

future profit earning opportunities.

It also helps the organisation in forecasting the

future growth of the businesses. Because cost

accounting shows the pattern of the business

that how it expand their money in their

operations. Through this information the

managers of the organisation are able to

forecast growth.

The next demerit of the cost accounting is hat

it require an expert who knows hoe record all

the transaction and how analyse them. For

hiring an expert the organisations require

money which also increase the costs.

Budgetary Control:

It is defined as proper plan which helps the organisations manges their incomes and

expenditures (Tingey-Holyoak and et.al., 2020). It is considered as document through the

managers perform their operations.

The advantages and disadvantages of budgetary control are as follows-

Advantages Disadvantages

It helps the organisation in analysing the

performance of the businesses.

Budgetary control require so much time to

prepare and also not easy to make it effective.

This tool helps the businesses in finding out

the sectors in which require modification for

their benefits..

It create some kind of barrier to the employees

due to which the they are not able to work

freely as result the employees starts feeling

demotivated.

Helps in achieving the organisational goal. This tool can only be prepared by the top level

management. Some time it crease different of

pressure in the mind of the employees.

The main target of the budgetary control is to

decrease the cost and increase the profit

margin.

Some time it require coordination between the

departments which is very difficult to maintain.

2. Application of management accounting for solving financial problems:

Financial problem is that problem which can be found in every type of organisation. This

problem is totally depend on the nature and size of the organisation. Management accounting

helps the organisation in maintaining the fund so that can continue their operations in their day to

day life for a long period of time (Udalova and Zubareva, 2021). To better understand the

situation and its impact as well as solution, following case studies are assessed:

During the period of the Covid19 many organisation have to shut their office due

to the guidelines of the government. This can affect the operation of businesses

very badly but the mangers of the organisation bring the policy known as Work

from home policy. Company like KPMG adopt that policy and start their

operations the employees did not have to come to the offices for their work. They

continue their work from their home. This policy also helps them in reducing the

cost by not using the office facility. The profit margin of the organisation get

increase due to this policy.

The next example can be explained by the company known as Deloitte. In 2017

this company face a cyber attack where the hackers get an access of the very

important data of the company. The company did not take get frustrate in this

situation and start analysing the internal working operations. Due to this they are

able to find out the week point and rectify the mistake and gain takeover all

important data of their businesses. This can only be done by the help of proper

management accounting.

management. Some time it crease different of

pressure in the mind of the employees.

The main target of the budgetary control is to

decrease the cost and increase the profit

margin.

Some time it require coordination between the

departments which is very difficult to maintain.

2. Application of management accounting for solving financial problems:

Financial problem is that problem which can be found in every type of organisation. This

problem is totally depend on the nature and size of the organisation. Management accounting

helps the organisation in maintaining the fund so that can continue their operations in their day to

day life for a long period of time (Udalova and Zubareva, 2021). To better understand the

situation and its impact as well as solution, following case studies are assessed:

During the period of the Covid19 many organisation have to shut their office due

to the guidelines of the government. This can affect the operation of businesses

very badly but the mangers of the organisation bring the policy known as Work

from home policy. Company like KPMG adopt that policy and start their

operations the employees did not have to come to the offices for their work. They

continue their work from their home. This policy also helps them in reducing the

cost by not using the office facility. The profit margin of the organisation get

increase due to this policy.

The next example can be explained by the company known as Deloitte. In 2017

this company face a cyber attack where the hackers get an access of the very

important data of the company. The company did not take get frustrate in this

situation and start analysing the internal working operations. Due to this they are

able to find out the week point and rectify the mistake and gain takeover all

important data of their businesses. This can only be done by the help of proper

management accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.