Management Accounting: Principles, Techniques, and Applications

VerifiedAdded on 2024/05/17

|23

|4258

|133

AI Summary

This report delves into the fundamental principles of management accounting, exploring its role in decision-making, resource allocation, and performance evaluation. It examines various techniques, including cost computation, budgeting, and variance analysis, and demonstrates their practical application in real-world scenarios. The report also highlights the importance of integrating management accounting systems with organizational reporting for effective financial governance and sustainable success.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

Introduction..............................................................................................................................3

LO1 Systems of Management Accounting (P1, P2, M1, D1)................................................4

P1 Management Accounting and Types.............................................................................4

P2 Methods of reporting of the management accounting.................................................5

M1 Benefits of the system of the management accounting...............................................6

D1 Management Accounting system and reporting integration with the organization 7

LO2 Techniques range from management accounting (P3, M2, D2)..................................8

P3 Cost computation and income statement......................................................................8

LO3..........................................................................................................................................11

P4. Advantages and disadvantages of types of planning tools.......................................11

M3 Use of planning tools and their application...............................................................12

LO4..........................................................................................................................................16

P5 Organizations adapting management accounting systems to respond to financial

problems..............................................................................................................................16

M4 How management accounting can lead an organization to sustainable success....17

D3 How planning tools respond appropriately to solving problems.............................19

Conclusion...............................................................................................................................20

2

Introduction..............................................................................................................................3

LO1 Systems of Management Accounting (P1, P2, M1, D1)................................................4

P1 Management Accounting and Types.............................................................................4

P2 Methods of reporting of the management accounting.................................................5

M1 Benefits of the system of the management accounting...............................................6

D1 Management Accounting system and reporting integration with the organization 7

LO2 Techniques range from management accounting (P3, M2, D2)..................................8

P3 Cost computation and income statement......................................................................8

LO3..........................................................................................................................................11

P4. Advantages and disadvantages of types of planning tools.......................................11

M3 Use of planning tools and their application...............................................................12

LO4..........................................................................................................................................16

P5 Organizations adapting management accounting systems to respond to financial

problems..............................................................................................................................16

M4 How management accounting can lead an organization to sustainable success....17

D3 How planning tools respond appropriately to solving problems.............................19

Conclusion...............................................................................................................................20

2

Introduction

The accounting is the main part of the company or the organization through which the

performance of the current situation can be understood which will help in predicting the

future. The accounting helps the holders of the company who are interested in the position of

the company to take proper decisions for the future. The report will provide the management

accounting theories and the detailed understanding of the management accounting along with

the computations for the cost and the budgets. The methods and the responsibilities of the

management accounting where the planning tools and the tools which are used for the

budgetary control will be explained in the report below. Further, the ways of responding to

financial problems will be discussed and will be explained through the computations of the

variance and the budget.

3

The accounting is the main part of the company or the organization through which the

performance of the current situation can be understood which will help in predicting the

future. The accounting helps the holders of the company who are interested in the position of

the company to take proper decisions for the future. The report will provide the management

accounting theories and the detailed understanding of the management accounting along with

the computations for the cost and the budgets. The methods and the responsibilities of the

management accounting where the planning tools and the tools which are used for the

budgetary control will be explained in the report below. Further, the ways of responding to

financial problems will be discussed and will be explained through the computations of the

variance and the budget.

3

LO1 Systems of Management Accounting (P1, P2, M1, D1)

P1 Management Accounting and Types

The management accounting is the decision-making tool which will help in the effective and

the efficient decision making. The decisions for the resources can also be taken through

which the optimum utilisation of the resources can be done (Borad, 2017). The planning and

the controlling of the activities for the management can be done in an effective way and also

the management uses the accounting phenomenon at every level of the organization. The

various tools which are required for the decision making whether for the current of the future

can be made through the variance analysis, budgets, CVP analysis and the BEP analysis.

The accounting in financial terms and the accounting in terms of management are very

different in various contexts like the management accounting reports are prepared frequently

whenever the need occurs in a detailed form whereas the financial accounting reports are

prepared at the year end on the business activities as a whole. For the management

accounting, the standards will not be used whereas for the financial accounting the standards

will be used. The management accounting follows the orientation on the future basis while

the financial accounting follows the orientation on the basis of the history. The management

accounting does not provide the information which is precise or accurate whereas the

financial accounting provides the information which is precise and accurate (Averkamp,

2018).

The principles of accounting which the management is required to follow mandatorily where

the first principle is the communication where two communication is required to be proper

among the departments, the other principle is relevant where the information is required to be

relevant for the readers of the company, another principle is the value through which the

organization creates value and the last principle is the trust which states that the management

must be honest or trustworthy so that the management can rely and take the decisions. The

different types of the management accounting systems are as follows:

1. Tax Accounting- The financial statements are not the preference while the taxation is

a preference. The principles which are generally accepted for the preparation and

payment of the tax returns are followed by the accounting system of tax.

2. Cost Accounting- The system where the prediction of the cost took place and hence

the profit of the company can be estimated which will require the cost as the basis.

Thus the system will help in controlling or reducing the cost. The system is further

divided into two categories which are job order and the process cost.

3. Financial Accounting- The system through which the analysis and reporting can be

done of the business information and hence the decisions can be taken with the help

of the reports which are prepared in the financial terms.

4. Management Accounting- The system which helps in extraction of the financial and

non-financial information which the management uses at all the levels and thus the

system will help the company in identifying the key performance indicators.

4

P1 Management Accounting and Types

The management accounting is the decision-making tool which will help in the effective and

the efficient decision making. The decisions for the resources can also be taken through

which the optimum utilisation of the resources can be done (Borad, 2017). The planning and

the controlling of the activities for the management can be done in an effective way and also

the management uses the accounting phenomenon at every level of the organization. The

various tools which are required for the decision making whether for the current of the future

can be made through the variance analysis, budgets, CVP analysis and the BEP analysis.

The accounting in financial terms and the accounting in terms of management are very

different in various contexts like the management accounting reports are prepared frequently

whenever the need occurs in a detailed form whereas the financial accounting reports are

prepared at the year end on the business activities as a whole. For the management

accounting, the standards will not be used whereas for the financial accounting the standards

will be used. The management accounting follows the orientation on the future basis while

the financial accounting follows the orientation on the basis of the history. The management

accounting does not provide the information which is precise or accurate whereas the

financial accounting provides the information which is precise and accurate (Averkamp,

2018).

The principles of accounting which the management is required to follow mandatorily where

the first principle is the communication where two communication is required to be proper

among the departments, the other principle is relevant where the information is required to be

relevant for the readers of the company, another principle is the value through which the

organization creates value and the last principle is the trust which states that the management

must be honest or trustworthy so that the management can rely and take the decisions. The

different types of the management accounting systems are as follows:

1. Tax Accounting- The financial statements are not the preference while the taxation is

a preference. The principles which are generally accepted for the preparation and

payment of the tax returns are followed by the accounting system of tax.

2. Cost Accounting- The system where the prediction of the cost took place and hence

the profit of the company can be estimated which will require the cost as the basis.

Thus the system will help in controlling or reducing the cost. The system is further

divided into two categories which are job order and the process cost.

3. Financial Accounting- The system through which the analysis and reporting can be

done of the business information and hence the decisions can be taken with the help

of the reports which are prepared in the financial terms.

4. Management Accounting- The system which helps in extraction of the financial and

non-financial information which the management uses at all the levels and thus the

system will help the company in identifying the key performance indicators.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

P2 Methods of reporting of the management accounting

The reports which the management prepares are the trading and profit and loss account,

income statement, cost of goods sold report, balance sheet and the cash flow statement. The

trading p & l account is prepared so that the profitability is known and the decision of the

dividend can be taken easily (Kumar, 2011). The income statement is prepared to predict the

expenses and the income of the company whereas the cost of goods sold report the company

prepares so that the deduction and the reduction in the tax can be done. The balance sheet and

eh cash flow statement is prepared for understanding the position of the activities of the

business along with the position of the cash flow respectively. The systems of management

accounting are as follows:

1. Price optimisation- The mathematical analysis helps the companies in analysing the

responses of the customer and the price will be accordingly decided. For example, the

newly identified product price can be decided (McCormick, 2017).

2. Cost accounting system- The profit can be earned by the companies if the cost is

controlled and the types are the process costing and the job order costing. For

example, the tracking of the goods can be done when the transferring of the goods is

taking place.

3. Job costing system- The material cost, labour cost and the overheads can be easily

identified with the help of the job costing system for the product or the particular job.

For example, the cost of the job will be proportionately allocated as per the job or the

product in the cost sheet (Walther & Skousen, 2010).

4. Inventory management- The inventory which is the most important component of

the organizations which can be easily managed with the help of the system. For

example, the system will help the company in order the inventory in advance.

5

The reports which the management prepares are the trading and profit and loss account,

income statement, cost of goods sold report, balance sheet and the cash flow statement. The

trading p & l account is prepared so that the profitability is known and the decision of the

dividend can be taken easily (Kumar, 2011). The income statement is prepared to predict the

expenses and the income of the company whereas the cost of goods sold report the company

prepares so that the deduction and the reduction in the tax can be done. The balance sheet and

eh cash flow statement is prepared for understanding the position of the activities of the

business along with the position of the cash flow respectively. The systems of management

accounting are as follows:

1. Price optimisation- The mathematical analysis helps the companies in analysing the

responses of the customer and the price will be accordingly decided. For example, the

newly identified product price can be decided (McCormick, 2017).

2. Cost accounting system- The profit can be earned by the companies if the cost is

controlled and the types are the process costing and the job order costing. For

example, the tracking of the goods can be done when the transferring of the goods is

taking place.

3. Job costing system- The material cost, labour cost and the overheads can be easily

identified with the help of the job costing system for the product or the particular job.

For example, the cost of the job will be proportionately allocated as per the job or the

product in the cost sheet (Walther & Skousen, 2010).

4. Inventory management- The inventory which is the most important component of

the organizations which can be easily managed with the help of the system. For

example, the system will help the company in order the inventory in advance.

5

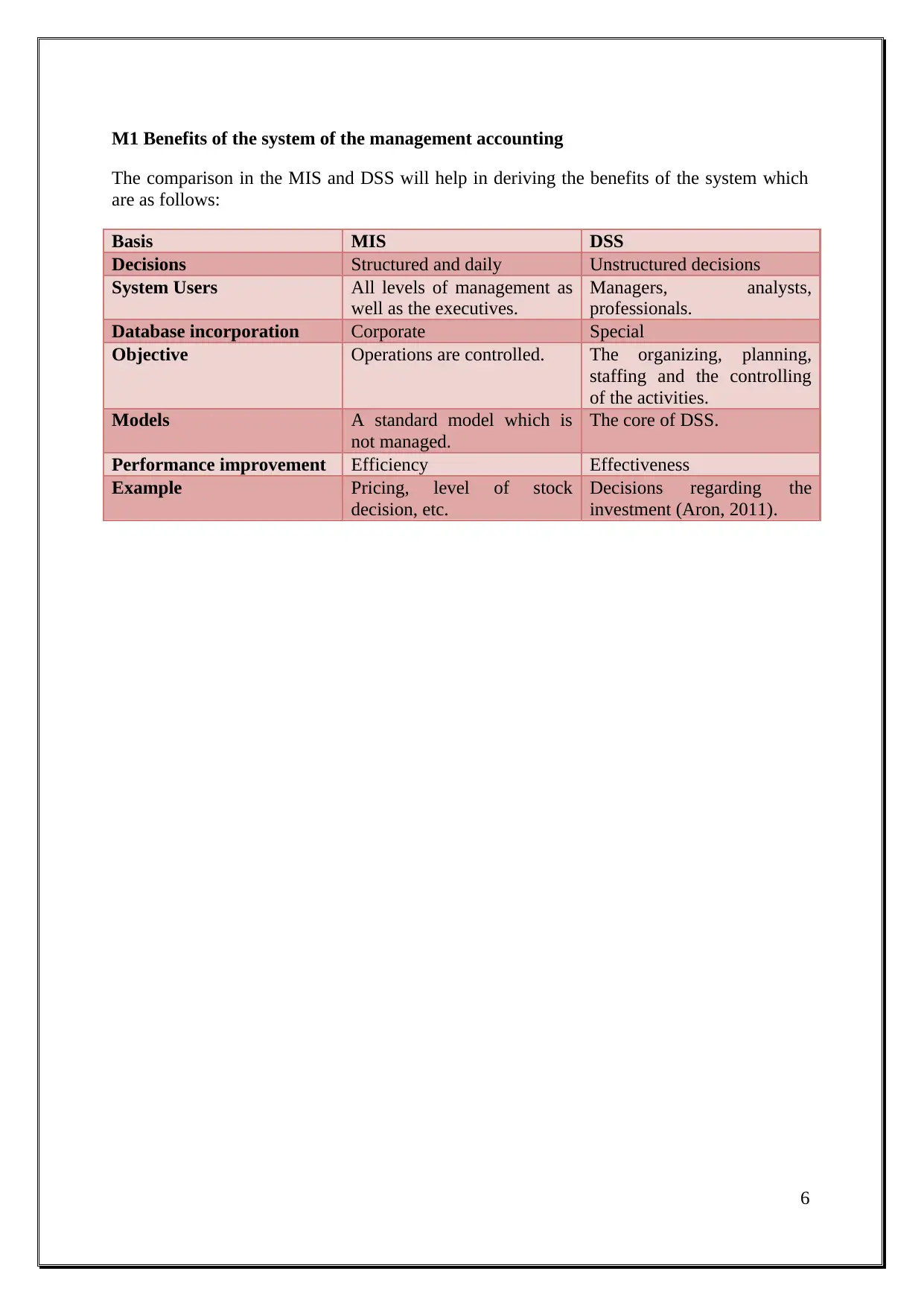

M1 Benefits of the system of the management accounting

The comparison in the MIS and DSS will help in deriving the benefits of the system which

are as follows:

Basis MIS DSS

Decisions Structured and daily Unstructured decisions

System Users All levels of management as

well as the executives.

Managers, analysts,

professionals.

Database incorporation Corporate Special

Objective Operations are controlled. The organizing, planning,

staffing and the controlling

of the activities.

Models A standard model which is

not managed.

The core of DSS.

Performance improvement Efficiency Effectiveness

Example Pricing, level of stock

decision, etc.

Decisions regarding the

investment (Aron, 2011).

6

The comparison in the MIS and DSS will help in deriving the benefits of the system which

are as follows:

Basis MIS DSS

Decisions Structured and daily Unstructured decisions

System Users All levels of management as

well as the executives.

Managers, analysts,

professionals.

Database incorporation Corporate Special

Objective Operations are controlled. The organizing, planning,

staffing and the controlling

of the activities.

Models A standard model which is

not managed.

The core of DSS.

Performance improvement Efficiency Effectiveness

Example Pricing, level of stock

decision, etc.

Decisions regarding the

investment (Aron, 2011).

6

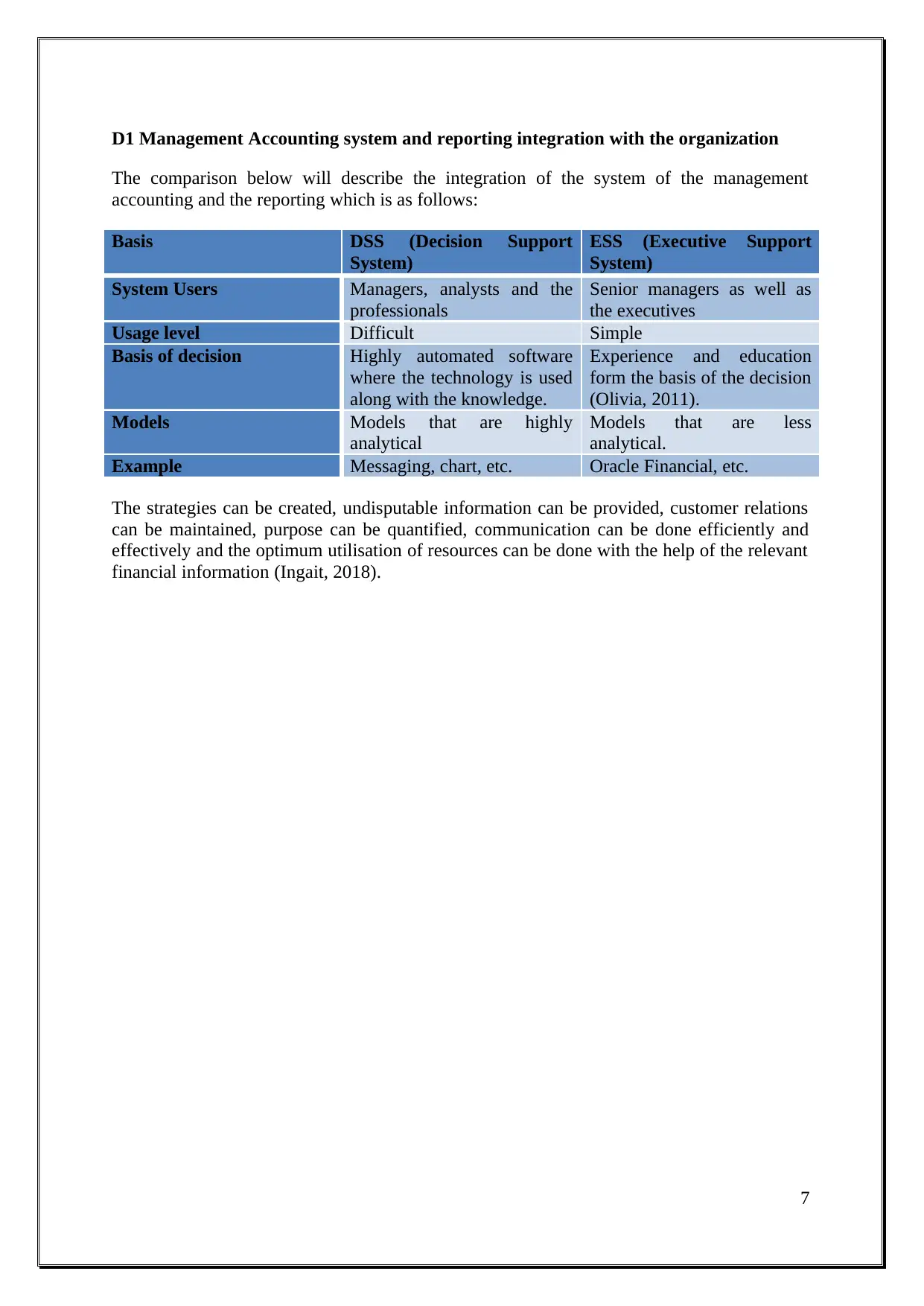

D1 Management Accounting system and reporting integration with the organization

The comparison below will describe the integration of the system of the management

accounting and the reporting which is as follows:

Basis DSS (Decision Support

System)

ESS (Executive Support

System)

System Users Managers, analysts and the

professionals

Senior managers as well as

the executives

Usage level Difficult Simple

Basis of decision Highly automated software

where the technology is used

along with the knowledge.

Experience and education

form the basis of the decision

(Olivia, 2011).

Models Models that are highly

analytical

Models that are less

analytical.

Example Messaging, chart, etc. Oracle Financial, etc.

The strategies can be created, undisputable information can be provided, customer relations

can be maintained, purpose can be quantified, communication can be done efficiently and

effectively and the optimum utilisation of resources can be done with the help of the relevant

financial information (Ingait, 2018).

7

The comparison below will describe the integration of the system of the management

accounting and the reporting which is as follows:

Basis DSS (Decision Support

System)

ESS (Executive Support

System)

System Users Managers, analysts and the

professionals

Senior managers as well as

the executives

Usage level Difficult Simple

Basis of decision Highly automated software

where the technology is used

along with the knowledge.

Experience and education

form the basis of the decision

(Olivia, 2011).

Models Models that are highly

analytical

Models that are less

analytical.

Example Messaging, chart, etc. Oracle Financial, etc.

The strategies can be created, undisputable information can be provided, customer relations

can be maintained, purpose can be quantified, communication can be done efficiently and

effectively and the optimum utilisation of resources can be done with the help of the relevant

financial information (Ingait, 2018).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO2 Techniques range from management accounting (P3, M2, D2)

P3 Cost computation and income statement

The cost is the amount which the company incurs for the product or the service which will

then be increased to earn the profit and it will be charged from the ultimate user of the goods

or the service. There are various costs like the fixed, variable, product, period, implicit, sunk,

opportunity, explicit, future, semi-variable, past, etc. The CVP analysis helps the companies

in identifying the change in the cost and the effect of such change. The flexible budget is

prepared by the company so that the change in the level of activity can be determined and the

difference in the actual and the budgeted results are the variances through which the

interpretation can be done.

The costing methods can further be classified as absorption and marginal costing. The

absorption costing is the system where the total profit will be considered on the basis of the

total cost for the specific service or the product. The total cost of the service or the product

will include both the variable and the fixed cost. The cost will be taken on the average basis

and it is added to the price at which the product or the service can be sold and the profit can

be earned. The marginal costing is the system where the profit of the service or the product

will be considered only after the consideration of the variable cost. The cost of one unit extra

will then be added to the cost of one unit that is produced extra. The contribution will be

calculated firstly since the consideration of only the variable cost is there and then the net

profit will be calculated (Bragg, 2017).

The cost that remains fixed and the change in the level of activity does not affect the cost is

termed as the fixed cost otherwise where the cost is not fixed and the change in the level of

activity affects the cost then it will be termed as the variable cost. The cost which is the cost

of manufacturing is the normal cost and the cost which then is substituted as against the

actual cost is the standard cost.

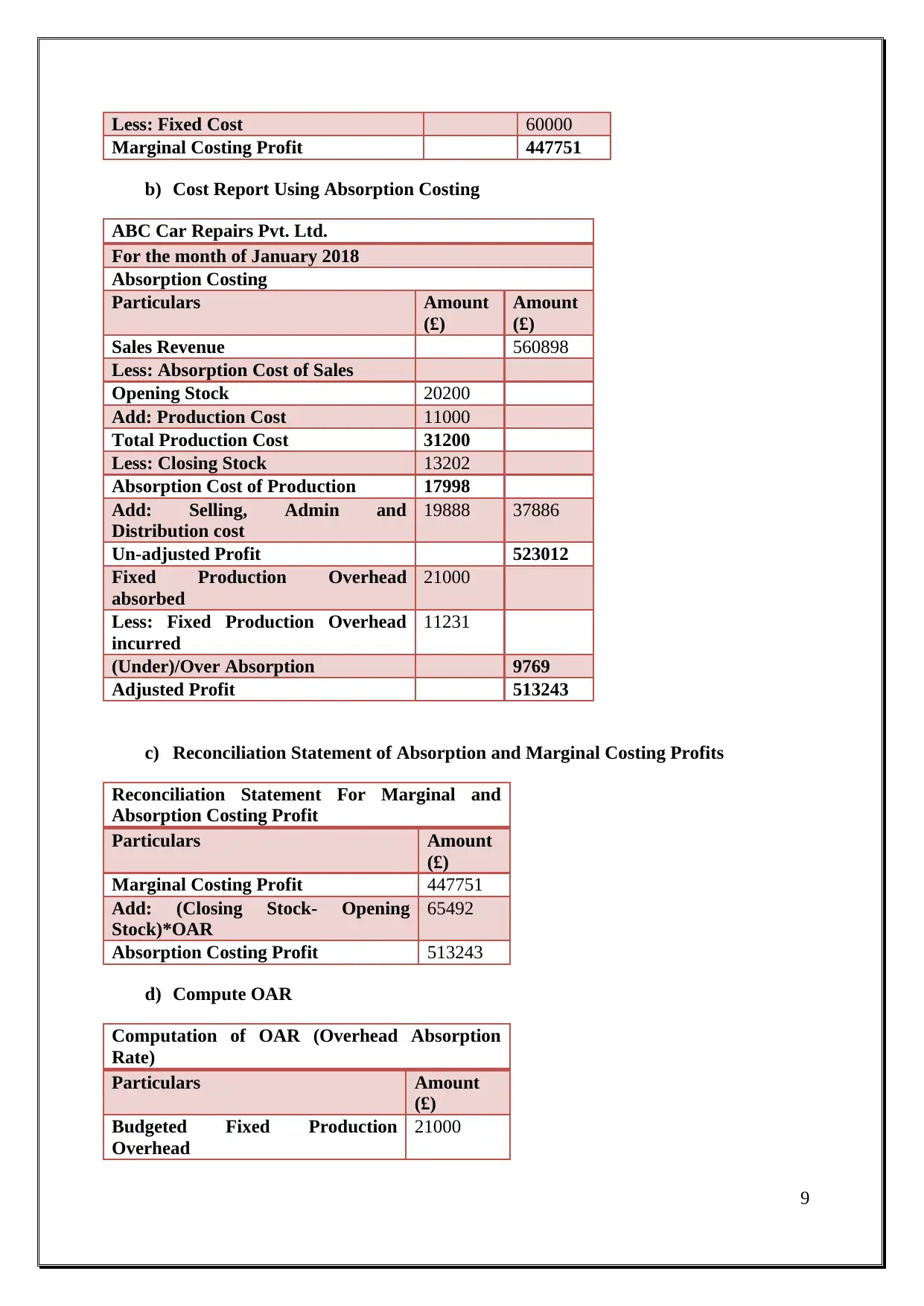

a) Cost Report Using Marginal Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Marginal Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Marginal Cost of Sales

Opening Stock 40400

Add: Production Cost 18000

Total Production Cost 58400

Less: Closing Stock 25141

Marginal Cost of Production 33259

Add: Selling, Admin and Distribution

cost

19888 53147

Contribution 507751

8

P3 Cost computation and income statement

The cost is the amount which the company incurs for the product or the service which will

then be increased to earn the profit and it will be charged from the ultimate user of the goods

or the service. There are various costs like the fixed, variable, product, period, implicit, sunk,

opportunity, explicit, future, semi-variable, past, etc. The CVP analysis helps the companies

in identifying the change in the cost and the effect of such change. The flexible budget is

prepared by the company so that the change in the level of activity can be determined and the

difference in the actual and the budgeted results are the variances through which the

interpretation can be done.

The costing methods can further be classified as absorption and marginal costing. The

absorption costing is the system where the total profit will be considered on the basis of the

total cost for the specific service or the product. The total cost of the service or the product

will include both the variable and the fixed cost. The cost will be taken on the average basis

and it is added to the price at which the product or the service can be sold and the profit can

be earned. The marginal costing is the system where the profit of the service or the product

will be considered only after the consideration of the variable cost. The cost of one unit extra

will then be added to the cost of one unit that is produced extra. The contribution will be

calculated firstly since the consideration of only the variable cost is there and then the net

profit will be calculated (Bragg, 2017).

The cost that remains fixed and the change in the level of activity does not affect the cost is

termed as the fixed cost otherwise where the cost is not fixed and the change in the level of

activity affects the cost then it will be termed as the variable cost. The cost which is the cost

of manufacturing is the normal cost and the cost which then is substituted as against the

actual cost is the standard cost.

a) Cost Report Using Marginal Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Marginal Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Marginal Cost of Sales

Opening Stock 40400

Add: Production Cost 18000

Total Production Cost 58400

Less: Closing Stock 25141

Marginal Cost of Production 33259

Add: Selling, Admin and Distribution

cost

19888 53147

Contribution 507751

8

Less: Fixed Cost 60000

Marginal Costing Profit 447751

b) Cost Report Using Absorption Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Absorption Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Absorption Cost of Sales

Opening Stock 20200

Add: Production Cost 11000

Total Production Cost 31200

Less: Closing Stock 13202

Absorption Cost of Production 17998

Add: Selling, Admin and

Distribution cost

19888 37886

Un-adjusted Profit 523012

Fixed Production Overhead

absorbed

21000

Less: Fixed Production Overhead

incurred

11231

(Under)/Over Absorption 9769

Adjusted Profit 513243

c) Reconciliation Statement of Absorption and Marginal Costing Profits

Reconciliation Statement For Marginal and

Absorption Costing Profit

Particulars Amount

(£)

Marginal Costing Profit 447751

Add: (Closing Stock- Opening

Stock)*OAR

65492

Absorption Costing Profit 513243

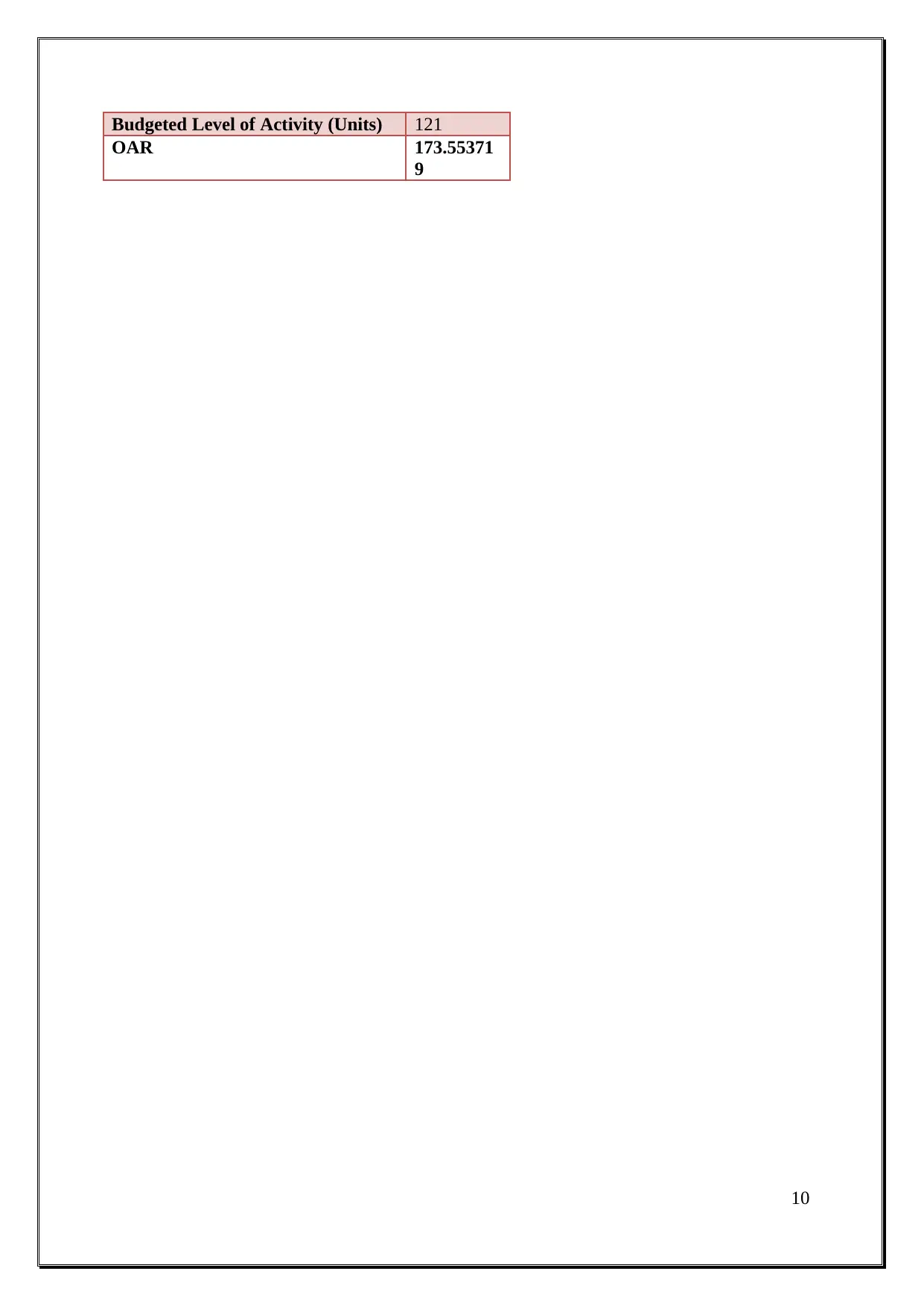

d) Compute OAR

Computation of OAR (Overhead Absorption

Rate)

Particulars Amount

(£)

Budgeted Fixed Production

Overhead

21000

9

Marginal Costing Profit 447751

b) Cost Report Using Absorption Costing

ABC Car Repairs Pvt. Ltd.

For the month of January 2018

Absorption Costing

Particulars Amount

(£)

Amount

(£)

Sales Revenue 560898

Less: Absorption Cost of Sales

Opening Stock 20200

Add: Production Cost 11000

Total Production Cost 31200

Less: Closing Stock 13202

Absorption Cost of Production 17998

Add: Selling, Admin and

Distribution cost

19888 37886

Un-adjusted Profit 523012

Fixed Production Overhead

absorbed

21000

Less: Fixed Production Overhead

incurred

11231

(Under)/Over Absorption 9769

Adjusted Profit 513243

c) Reconciliation Statement of Absorption and Marginal Costing Profits

Reconciliation Statement For Marginal and

Absorption Costing Profit

Particulars Amount

(£)

Marginal Costing Profit 447751

Add: (Closing Stock- Opening

Stock)*OAR

65492

Absorption Costing Profit 513243

d) Compute OAR

Computation of OAR (Overhead Absorption

Rate)

Particulars Amount

(£)

Budgeted Fixed Production

Overhead

21000

9

Budgeted Level of Activity (Units) 121

OAR 173.55371

9

10

OAR 173.55371

9

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

LO3

P4. Advantages and disadvantages of types of planning tools

The targets of the company can be achieved with the help of the preparation of the budget

and the budgets will help the companies in proper planning. The different budgets which can

be prepared are zero-based budgeting, incremental budget, master budget and many others

(Kovaleva et al., 2016). The budgets have many advantages and disadvantages that are

associated with it and they are as follows:

Advantages of the budgets

Optimum utilisation of resources can be done with the help of the budgets.

The plan for the activities to be performed can be presented to the management.

The wastage will be less and the information which the companies provide with the

help of budgets can help in the process of decision making.

The areas which are prone to risk and if there are any default in the activities then it

can be identified easily and accordingly to mitigate the actions can be taken.

Disadvantages of the budgets

The risk and the uncertainty in the activities of the business can be increased since the

budgets are prepared on the basis of the judgements and the assumptions.

The process of budgeting is a time-consuming phenomenon and this then can't help in

the immediate decision making.

The budgeting process is a process which is not affordable by all the companies and

hence the process is costly (Olusegun, 2016).

The different types of budgets which the company prepares are as follows:

1. Incremental Budget- The change in the level of activity or the requirements can be

handled effectively since the budget is prepared on the basis of the proportionate

increase in the level of activity and hence the budget is updated as per the need of the

business.

2. Cash budget- The transactions which will be based on the cash will be prepared as a

budget in the cash budget. The use of cash and the balance can be easily identified

and hence the expenses can be properly planned.

3. Zero-based budget- As the word suggests the budget which is prepared on the basis

of fresh data and fresh needs are the zero-based budgets i.e. from zero and not from

the historical data. Hence, the research will be required so that the decisions can be

taken and the budget can be prepared.

4. Master budget- The description of all the activities or the operations which are

prepared in one single budget is the master budget. The summary budget is the word

with which the master budget is known and hence it is helpful in providing the

information in one place.

11

P4. Advantages and disadvantages of types of planning tools

The targets of the company can be achieved with the help of the preparation of the budget

and the budgets will help the companies in proper planning. The different budgets which can

be prepared are zero-based budgeting, incremental budget, master budget and many others

(Kovaleva et al., 2016). The budgets have many advantages and disadvantages that are

associated with it and they are as follows:

Advantages of the budgets

Optimum utilisation of resources can be done with the help of the budgets.

The plan for the activities to be performed can be presented to the management.

The wastage will be less and the information which the companies provide with the

help of budgets can help in the process of decision making.

The areas which are prone to risk and if there are any default in the activities then it

can be identified easily and accordingly to mitigate the actions can be taken.

Disadvantages of the budgets

The risk and the uncertainty in the activities of the business can be increased since the

budgets are prepared on the basis of the judgements and the assumptions.

The process of budgeting is a time-consuming phenomenon and this then can't help in

the immediate decision making.

The budgeting process is a process which is not affordable by all the companies and

hence the process is costly (Olusegun, 2016).

The different types of budgets which the company prepares are as follows:

1. Incremental Budget- The change in the level of activity or the requirements can be

handled effectively since the budget is prepared on the basis of the proportionate

increase in the level of activity and hence the budget is updated as per the need of the

business.

2. Cash budget- The transactions which will be based on the cash will be prepared as a

budget in the cash budget. The use of cash and the balance can be easily identified

and hence the expenses can be properly planned.

3. Zero-based budget- As the word suggests the budget which is prepared on the basis

of fresh data and fresh needs are the zero-based budgets i.e. from zero and not from

the historical data. Hence, the research will be required so that the decisions can be

taken and the budget can be prepared.

4. Master budget- The description of all the activities or the operations which are

prepared in one single budget is the master budget. The summary budget is the word

with which the master budget is known and hence it is helpful in providing the

information in one place.

11

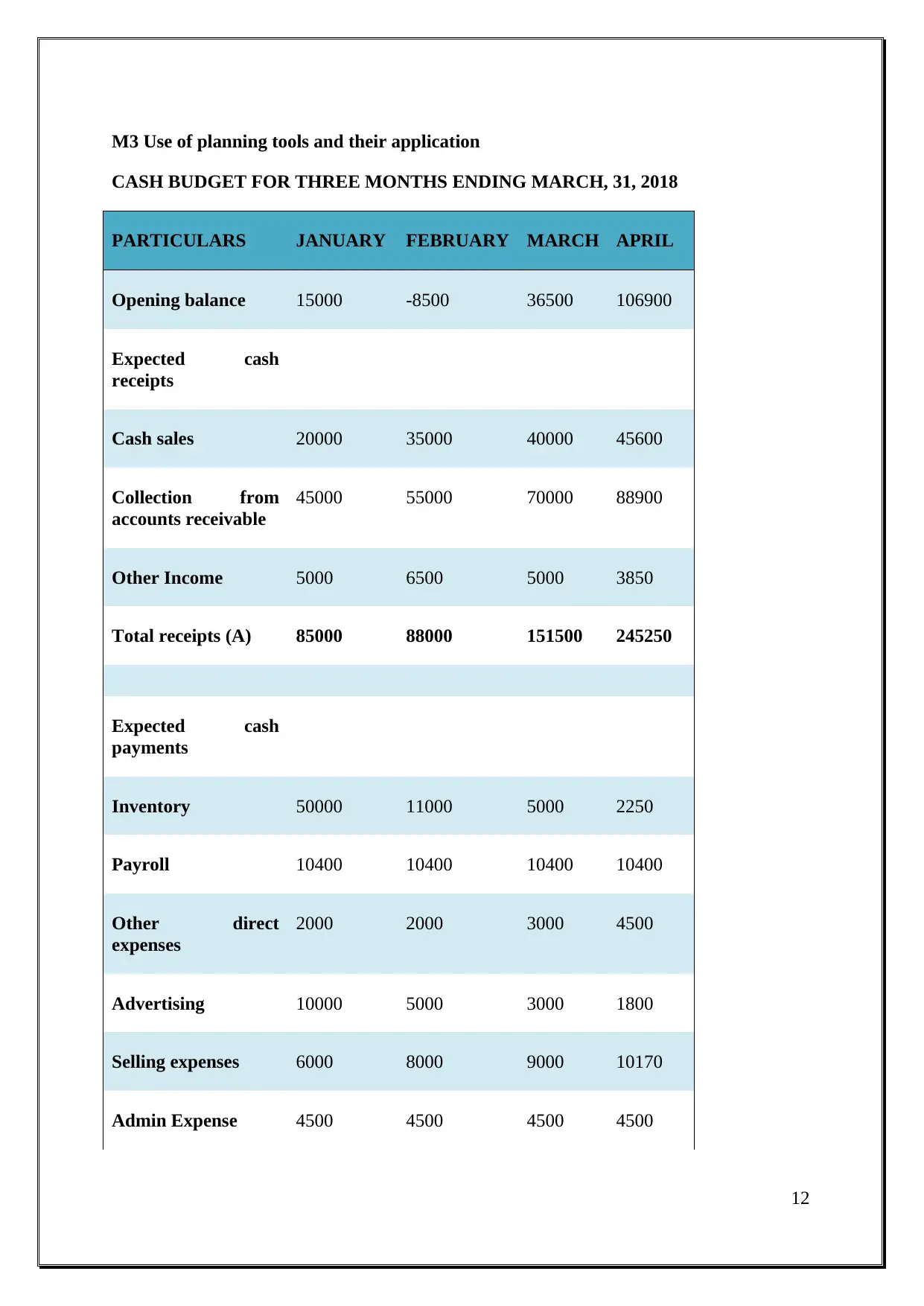

M3 Use of planning tools and their application

CASH BUDGET FOR THREE MONTHS ENDING MARCH, 31, 2018

PARTICULARS JANUARY FEBRUARY MARCH APRIL

Opening balance 15000 -8500 36500 106900

Expected cash

receipts

Cash sales 20000 35000 40000 45600

Collection from

accounts receivable

45000 55000 70000 88900

Other Income 5000 6500 5000 3850

Total receipts (A) 85000 88000 151500 245250

Expected cash

payments

Inventory 50000 11000 5000 2250

Payroll 10400 10400 10400 10400

Other direct

expenses

2000 2000 3000 4500

Advertising 10000 5000 3000 1800

Selling expenses 6000 8000 9000 10170

Admin Expense 4500 4500 4500 4500

12

CASH BUDGET FOR THREE MONTHS ENDING MARCH, 31, 2018

PARTICULARS JANUARY FEBRUARY MARCH APRIL

Opening balance 15000 -8500 36500 106900

Expected cash

receipts

Cash sales 20000 35000 40000 45600

Collection from

accounts receivable

45000 55000 70000 88900

Other Income 5000 6500 5000 3850

Total receipts (A) 85000 88000 151500 245250

Expected cash

payments

Inventory 50000 11000 5000 2250

Payroll 10400 10400 10400 10400

Other direct

expenses

2000 2000 3000 4500

Advertising 10000 5000 3000 1800

Selling expenses 6000 8000 9000 10170

Admin Expense 4500 4500 4500 4500

12

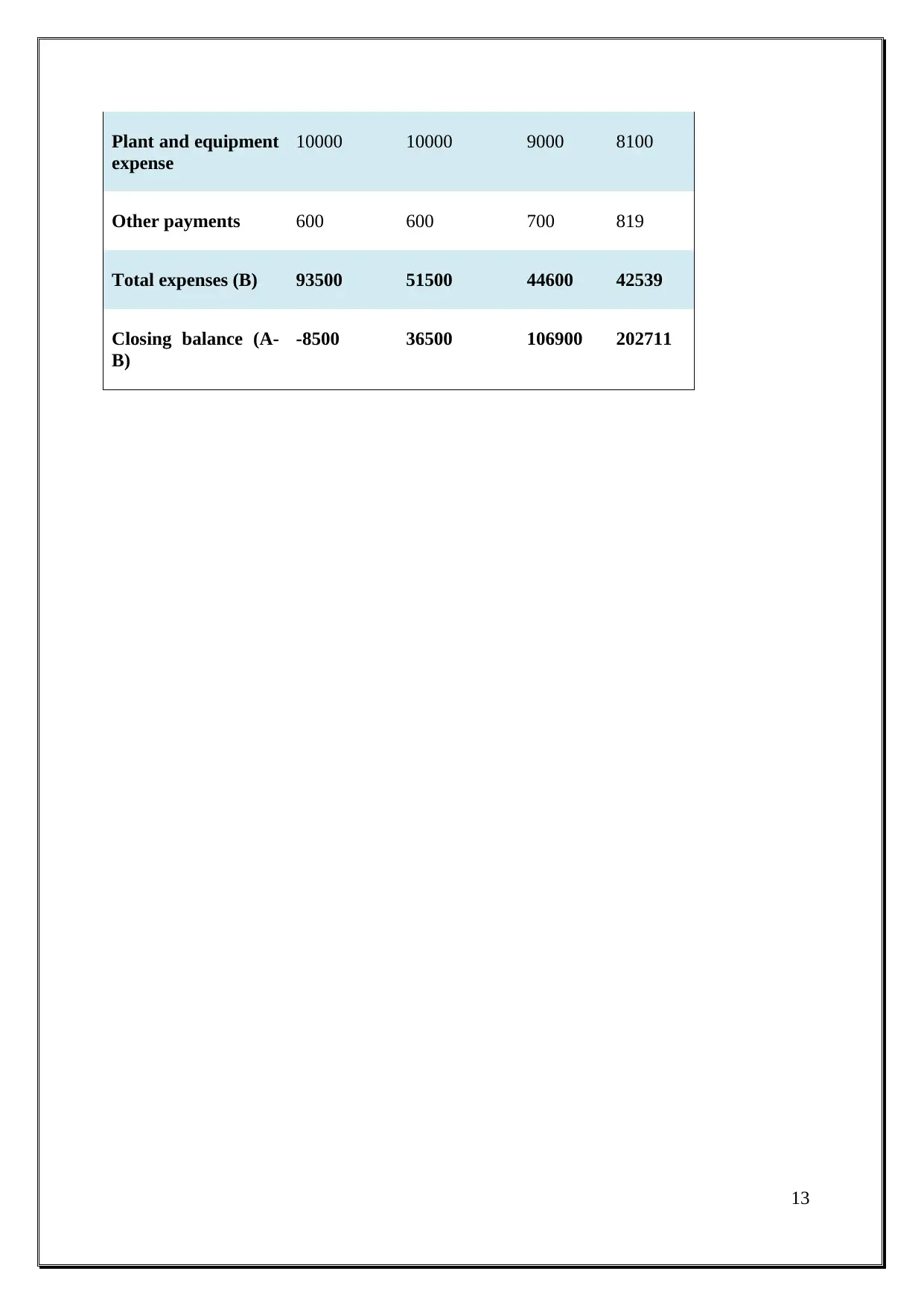

Plant and equipment

expense

10000 10000 9000 8100

Other payments 600 600 700 819

Total expenses (B) 93500 51500 44600 42539

Closing balance (A-

B)

-8500 36500 106900 202711

13

expense

10000 10000 9000 8100

Other payments 600 600 700 819

Total expenses (B) 93500 51500 44600 42539

Closing balance (A-

B)

-8500 36500 106900 202711

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

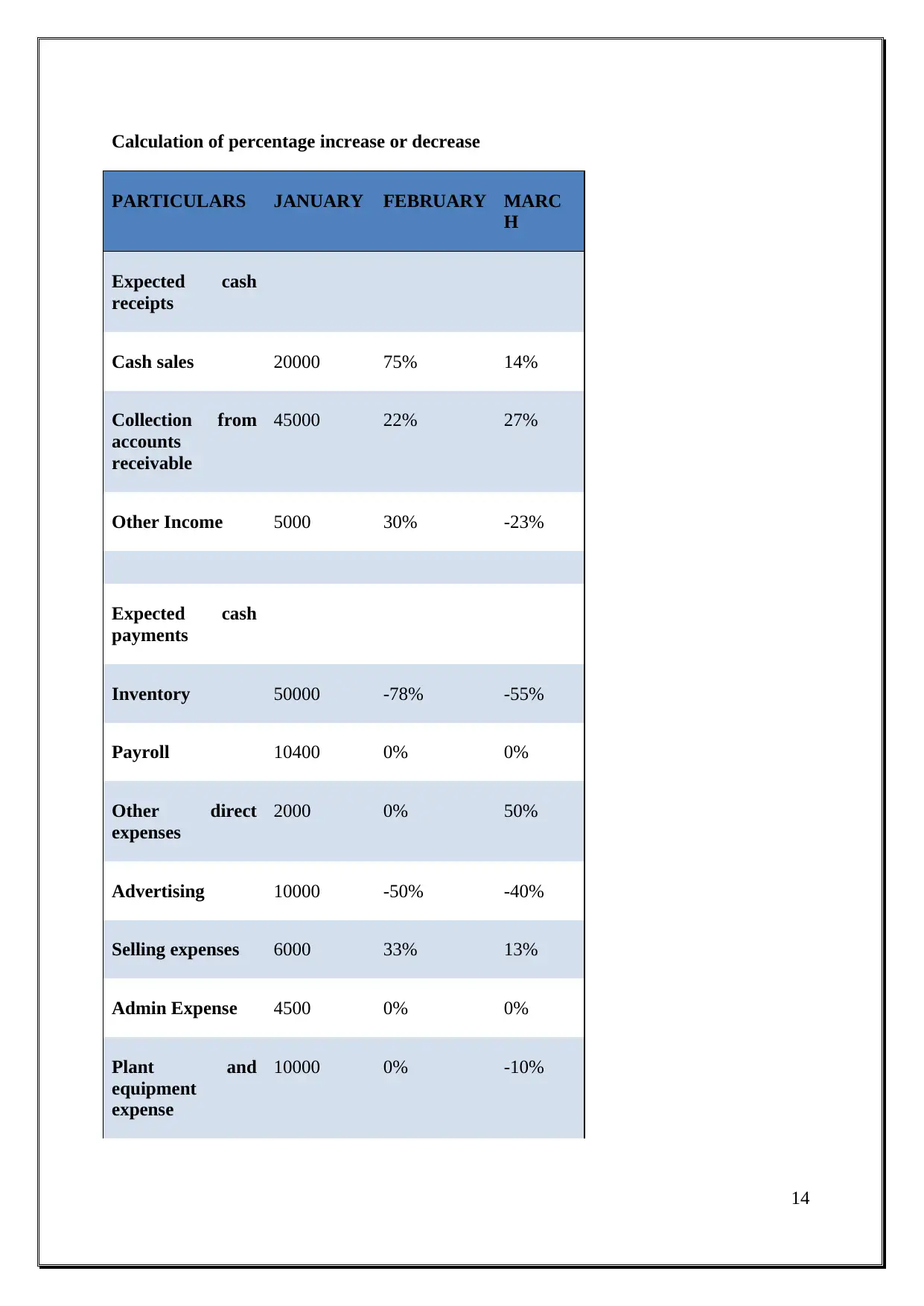

Calculation of percentage increase or decrease

PARTICULARS JANUARY FEBRUARY MARC

H

Expected cash

receipts

Cash sales 20000 75% 14%

Collection from

accounts

receivable

45000 22% 27%

Other Income 5000 30% -23%

Expected cash

payments

Inventory 50000 -78% -55%

Payroll 10400 0% 0%

Other direct

expenses

2000 0% 50%

Advertising 10000 -50% -40%

Selling expenses 6000 33% 13%

Admin Expense 4500 0% 0%

Plant and

equipment

expense

10000 0% -10%

14

PARTICULARS JANUARY FEBRUARY MARC

H

Expected cash

receipts

Cash sales 20000 75% 14%

Collection from

accounts

receivable

45000 22% 27%

Other Income 5000 30% -23%

Expected cash

payments

Inventory 50000 -78% -55%

Payroll 10400 0% 0%

Other direct

expenses

2000 0% 50%

Advertising 10000 -50% -40%

Selling expenses 6000 33% 13%

Admin Expense 4500 0% 0%

Plant and

equipment

expense

10000 0% -10%

14

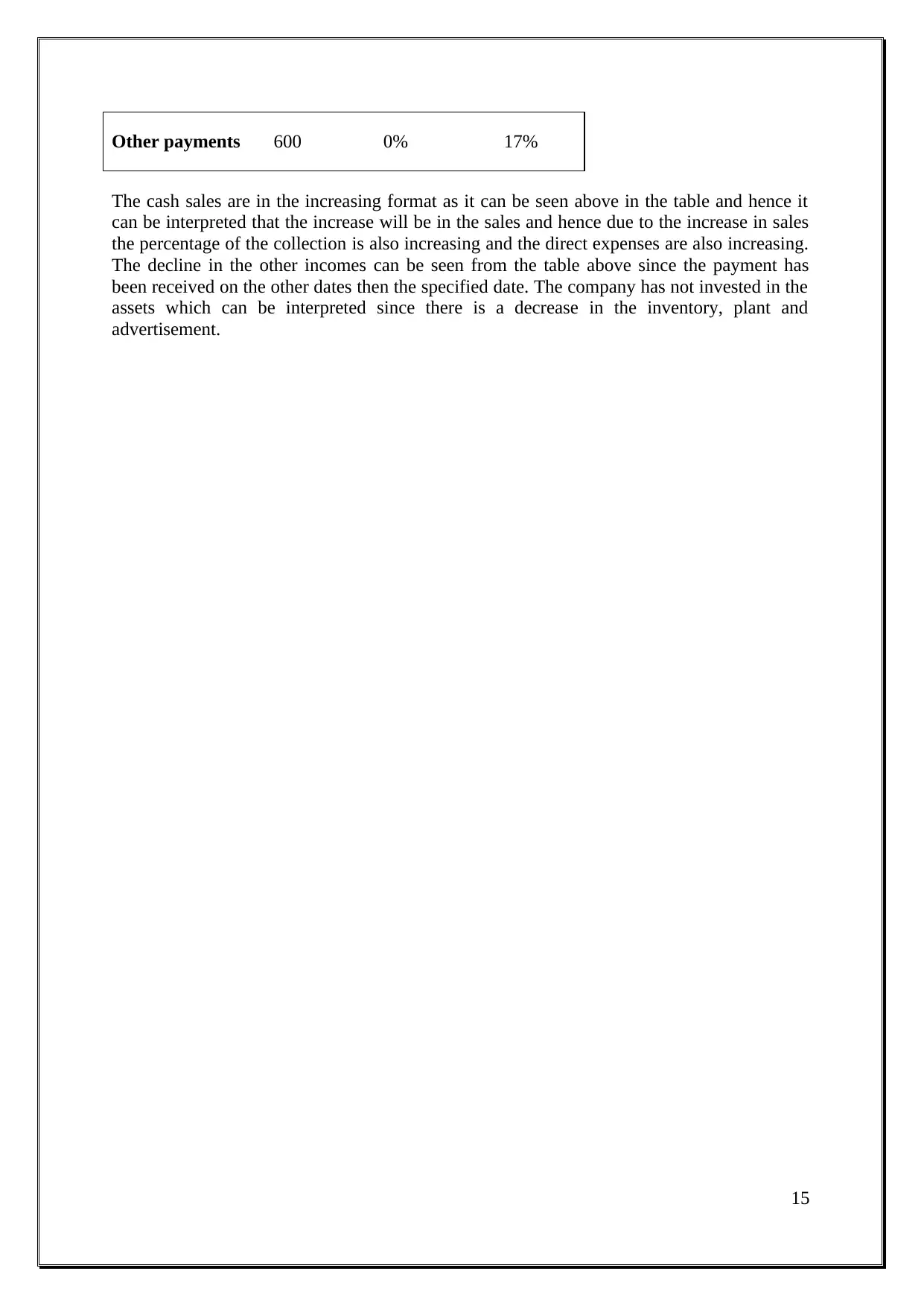

Other payments 600 0% 17%

The cash sales are in the increasing format as it can be seen above in the table and hence it

can be interpreted that the increase will be in the sales and hence due to the increase in sales

the percentage of the collection is also increasing and the direct expenses are also increasing.

The decline in the other incomes can be seen from the table above since the payment has

been received on the other dates then the specified date. The company has not invested in the

assets which can be interpreted since there is a decrease in the inventory, plant and

advertisement.

15

The cash sales are in the increasing format as it can be seen above in the table and hence it

can be interpreted that the increase will be in the sales and hence due to the increase in sales

the percentage of the collection is also increasing and the direct expenses are also increasing.

The decline in the other incomes can be seen from the table above since the payment has

been received on the other dates then the specified date. The company has not invested in the

assets which can be interpreted since there is a decrease in the inventory, plant and

advertisement.

15

LO4

P5 Organizations adapting management accounting systems to respond to financial

problems

The company does not have to face the problems if the issues or the problems are identified

in time. The problems must be analysed with the help of the techniques which will consist of

the procedures which the company follows. The techniques through which the performance

can be evaluated are as follows:

Benchmarks- The guidelines for the company are set with the help of the standards

under the benchmark technique. The standards are set and accordingly, the work will

be properly planned and performed and hence the errors or the issues will be resolved

or less and the results will be proper. The benchmarking technique does not help the

company in resolving the issue which the company faces while the procedure is being

undertaken.

Key performance indicators- The improvements which will be required can be

made and the comparison can be made in the performance of the employees and the

staff. The objectives which are set will be fulfilled as per the attained parameters

(Strenlik et al., 2017).

Budgets- The budgets which are prepared considering the past information and all

the aspects are included in the budgets and accordingly the plan is made. The

improvement will be made on the basis of the past performance and the new budget

will be the one which is improved and all the errors or issues will be less. The

probability of the errors or the problems will be reduced to the least and the chances

of occurrence will be less.

16

P5 Organizations adapting management accounting systems to respond to financial

problems

The company does not have to face the problems if the issues or the problems are identified

in time. The problems must be analysed with the help of the techniques which will consist of

the procedures which the company follows. The techniques through which the performance

can be evaluated are as follows:

Benchmarks- The guidelines for the company are set with the help of the standards

under the benchmark technique. The standards are set and accordingly, the work will

be properly planned and performed and hence the errors or the issues will be resolved

or less and the results will be proper. The benchmarking technique does not help the

company in resolving the issue which the company faces while the procedure is being

undertaken.

Key performance indicators- The improvements which will be required can be

made and the comparison can be made in the performance of the employees and the

staff. The objectives which are set will be fulfilled as per the attained parameters

(Strenlik et al., 2017).

Budgets- The budgets which are prepared considering the past information and all

the aspects are included in the budgets and accordingly the plan is made. The

improvement will be made on the basis of the past performance and the new budget

will be the one which is improved and all the errors or issues will be less. The

probability of the errors or the problems will be reduced to the least and the chances

of occurrence will be less.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

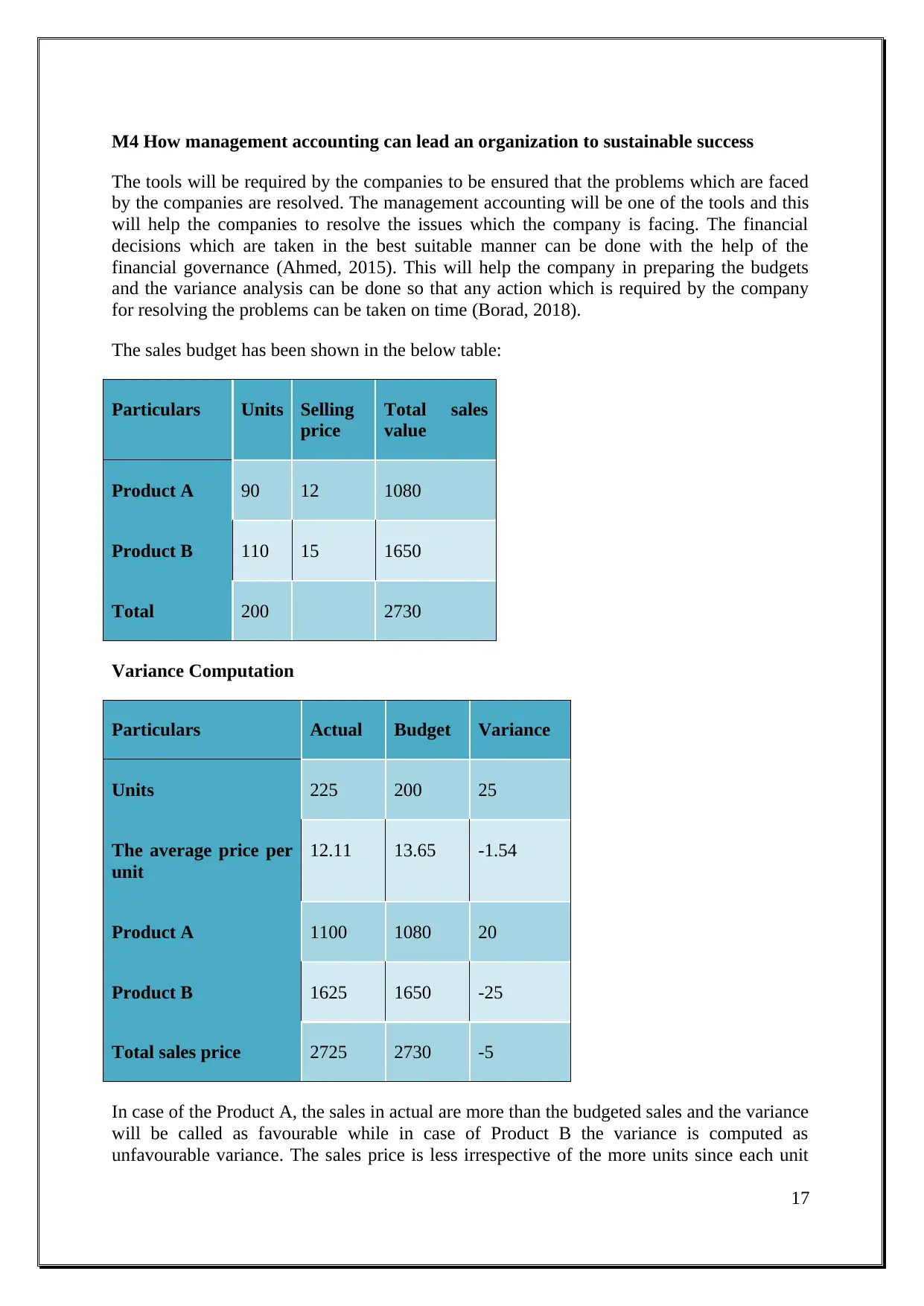

M4 How management accounting can lead an organization to sustainable success

The tools will be required by the companies to be ensured that the problems which are faced

by the companies are resolved. The management accounting will be one of the tools and this

will help the companies to resolve the issues which the company is facing. The financial

decisions which are taken in the best suitable manner can be done with the help of the

financial governance (Ahmed, 2015). This will help the company in preparing the budgets

and the variance analysis can be done so that any action which is required by the company

for resolving the problems can be taken on time (Borad, 2018).

The sales budget has been shown in the below table:

Particulars Units Selling

price

Total sales

value

Product A 90 12 1080

Product B 110 15 1650

Total 200 2730

Variance Computation

Particulars Actual Budget Variance

Units 225 200 25

The average price per

unit

12.11 13.65 -1.54

Product A 1100 1080 20

Product B 1625 1650 -25

Total sales price 2725 2730 -5

In case of the Product A, the sales in actual are more than the budgeted sales and the variance

will be called as favourable while in case of Product B the variance is computed as

unfavourable variance. The sales price is less irrespective of the more units since each unit

17

The tools will be required by the companies to be ensured that the problems which are faced

by the companies are resolved. The management accounting will be one of the tools and this

will help the companies to resolve the issues which the company is facing. The financial

decisions which are taken in the best suitable manner can be done with the help of the

financial governance (Ahmed, 2015). This will help the company in preparing the budgets

and the variance analysis can be done so that any action which is required by the company

for resolving the problems can be taken on time (Borad, 2018).

The sales budget has been shown in the below table:

Particulars Units Selling

price

Total sales

value

Product A 90 12 1080

Product B 110 15 1650

Total 200 2730

Variance Computation

Particulars Actual Budget Variance

Units 225 200 25

The average price per

unit

12.11 13.65 -1.54

Product A 1100 1080 20

Product B 1625 1650 -25

Total sales price 2725 2730 -5

In case of the Product A, the sales in actual are more than the budgeted sales and the variance

will be called as favourable while in case of Product B the variance is computed as

unfavourable variance. The sales price is less irrespective of the more units since each unit

17

price is charged less. The selling price on an average is less than which has been set in the

budget which is less than the actual (Saddam, 2015).

18

budget which is less than the actual (Saddam, 2015).

18

D3 How planning tools respond appropriately to solving problems

The objectives or the goals can be attained which will be possible for the company with the

use of the planning tools and hence the problems which the company will face will be

resolved and can be easily dealt with. The factors which affect the profitability will be

identified will be required to be understood. This can be understood with the budgets and the

variance analysis which has been undertaken in the above report. The budgets will be

evaluated and the actions for the difference can be taken and hence the reasons can be

identified. The budget will ensure the company to not to incorporate the errors which are

included in the past budgets and the modifications will be included.

19

The objectives or the goals can be attained which will be possible for the company with the

use of the planning tools and hence the problems which the company will face will be

resolved and can be easily dealt with. The factors which affect the profitability will be

identified will be required to be understood. This can be understood with the budgets and the

variance analysis which has been undertaken in the above report. The budgets will be

evaluated and the actions for the difference can be taken and hence the reasons can be

identified. The budget will ensure the company to not to incorporate the errors which are

included in the past budgets and the modifications will be included.

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Conclusion

The system and the reports will be used by the management accounting to retrieve the

information which is required at all the levels as it can be concluded from the report above.

The calculations for the cost and the income statement as per the methods of costing are done

in the report above and hence the profit is calculated. The cash budget and the forecasting

have been done on the basis of the budget in the report above so that the company will be

able to know the need of the cash for the future period of time and hence the controlling can

be done properly and easily. The detailed understanding of the variance analysis has been

shown in the report above through which the deviation can be understood in the context of

the budget as well as the sales. Hence it can be concluded that it will help the company in

identifying the deviations and the tools or the techniques are used to resolve the problems

which the company is facing.

20

The system and the reports will be used by the management accounting to retrieve the

information which is required at all the levels as it can be concluded from the report above.

The calculations for the cost and the income statement as per the methods of costing are done

in the report above and hence the profit is calculated. The cash budget and the forecasting

have been done on the basis of the budget in the report above so that the company will be

able to know the need of the cash for the future period of time and hence the controlling can

be done properly and easily. The detailed understanding of the variance analysis has been

shown in the report above through which the deviation can be understood in the context of

the budget as well as the sales. Hence it can be concluded that it will help the company in

identifying the deviations and the tools or the techniques are used to resolve the problems

which the company is facing.

20

Bibliography

Ahmed, N., 2015. Reinforcement of Good Governance in the International Financial

Institutions. Law, Social Justice & Global Development Journal.

Aron, 2011. Difference Between MIS and DSS. [Online] Available at:

http://www.differencebetween.com/difference-between-mis-and-vs-dss/ [Accessed 16

March 2018].

Averkamp, H., 2018. What is the difference between financial accounting and

management accounting? [Online] Available at:

https://www.accountingcoach.com/blog/financial-accounting-management-accounting

[Accessed 16 March 2018].

Borad, S.S., 2017. Management Accounting. [Online] Available at:

https://efinancemanagement.com/financial-accounting/management-accounting

[Accessed 16 March 2018].

Borad, S.B., 2018. Variance Analysis Formula with Example. [Online] Available at:

https://efinancemanagement.com/budgeting/variance-analysis-formula-with-example

[Accessed 16 March 2018].

Bragg, S., 2017. The difference between marginal costing and absorption costing.

[Online] Available at: https://www.accountingtools.com/articles/the-difference-between-

marginal-costing-and-absorption-costi.html [Accessed 16 March 2018].

Ingait, P.C., 2018. What Is An Integrated Accounting System? [Online] Available at:

http://smallbusiness.chron.com/integrated-accounting-system-74430.html [Accessed 16

March 2018].

21

Ahmed, N., 2015. Reinforcement of Good Governance in the International Financial

Institutions. Law, Social Justice & Global Development Journal.

Aron, 2011. Difference Between MIS and DSS. [Online] Available at:

http://www.differencebetween.com/difference-between-mis-and-vs-dss/ [Accessed 16

March 2018].

Averkamp, H., 2018. What is the difference between financial accounting and

management accounting? [Online] Available at:

https://www.accountingcoach.com/blog/financial-accounting-management-accounting

[Accessed 16 March 2018].

Borad, S.S., 2017. Management Accounting. [Online] Available at:

https://efinancemanagement.com/financial-accounting/management-accounting

[Accessed 16 March 2018].

Borad, S.B., 2018. Variance Analysis Formula with Example. [Online] Available at:

https://efinancemanagement.com/budgeting/variance-analysis-formula-with-example

[Accessed 16 March 2018].

Bragg, S., 2017. The difference between marginal costing and absorption costing.

[Online] Available at: https://www.accountingtools.com/articles/the-difference-between-

marginal-costing-and-absorption-costi.html [Accessed 16 March 2018].

Ingait, P.C., 2018. What Is An Integrated Accounting System? [Online] Available at:

http://smallbusiness.chron.com/integrated-accounting-system-74430.html [Accessed 16

March 2018].

21

Kovaleva, T.M. et al., 2016. The Budgeting Mechanism in Development Companies.

Russia: INTERNATIONAL JOURNAL OF ENVIRONMENTAL & SCIENCE

EDUCATION.

Kumar, V., 2011. Uses Of Profit and Loss Account. [Online] Available at:

http://www.svtuition.org/2011/10/uses-of-profit-and-loss-account.html [Accessed 16

MARCH 2018].

McCormick, M., 2017. What is Price Optimisation? [Online] Available at:

https://blog.blackcurve.com/what-is-price-optimisation [Accessed 16 March 2018].

Olivia, 2011. Difference Between DSS and ESS. [Online] Available at:

https://www.differencebetween.com/difference-between-dss-and-vs-ess-2/ [Accessed 16

March 2018].

Olusegun, M., 2016. The Importance of Budget and Budgetary Process among Non-

Publicly Accountable Entities (NPAEs): A Survey of Micro-Sized Firms in Nigeria . The

International Journal Of Business &Management.

Saddam, A., 2015. Variance Decomposition of Emissions, FDI, Growth and Imports in

GCC countries: A Macroeconomic Analysis. International Journal of Management

Science And Business Administration.

Strenlik, E.U., Usanova, D.S. & Khairullin, I.G., 2017. Key Performance Indicators in

Corporate Finance. Russia: Canadian Center of Science and Education.

Walther, L.M. & Skousen, C.J., 2010. Job Costing. bookboon.

22

Russia: INTERNATIONAL JOURNAL OF ENVIRONMENTAL & SCIENCE

EDUCATION.

Kumar, V., 2011. Uses Of Profit and Loss Account. [Online] Available at:

http://www.svtuition.org/2011/10/uses-of-profit-and-loss-account.html [Accessed 16

MARCH 2018].

McCormick, M., 2017. What is Price Optimisation? [Online] Available at:

https://blog.blackcurve.com/what-is-price-optimisation [Accessed 16 March 2018].

Olivia, 2011. Difference Between DSS and ESS. [Online] Available at:

https://www.differencebetween.com/difference-between-dss-and-vs-ess-2/ [Accessed 16

March 2018].

Olusegun, M., 2016. The Importance of Budget and Budgetary Process among Non-

Publicly Accountable Entities (NPAEs): A Survey of Micro-Sized Firms in Nigeria . The

International Journal Of Business &Management.

Saddam, A., 2015. Variance Decomposition of Emissions, FDI, Growth and Imports in

GCC countries: A Macroeconomic Analysis. International Journal of Management

Science And Business Administration.

Strenlik, E.U., Usanova, D.S. & Khairullin, I.G., 2017. Key Performance Indicators in

Corporate Finance. Russia: Canadian Center of Science and Education.

Walther, L.M. & Skousen, C.J., 2010. Job Costing. bookboon.

22

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

23

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.