Management Accounting: Principles, Techniques, and Applications

VerifiedAdded on 2024/05/31

|39

|6721

|128

AI Summary

This comprehensive report delves into the fundamental principles of management accounting, exploring its role in decision-making, planning, and control within organizations. It examines various management accounting systems, including cost accounting, inventory management, and job costing, and analyzes their benefits and applications. The report also discusses different types of budgets, pricing strategies, and the significance of financial governance in preventing financial problems. Furthermore, it explores the use of planning tools like SWOT analysis and PEST analysis for preparing and forecasting budgets. The report concludes by evaluating how management accounting can contribute to sustainable success by addressing financial challenges and optimizing organizational performance.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

1

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

Introduction.................................................................................................................................................5

TASK 1.......................................................................................................................................................6

1.1 Define and explain management accounting.....................................................................................6

1.2 What is management accounting system and why it is important to integrate it within the

organisation.............................................................................................................................................7

1.3 Distinguishing Management Accounting from Financial Accounting...............................................8

1.4 Define and explain different types of management accounting systems and their benefits within the

organisation.............................................................................................................................................9

1.5 Explain the different types of management accounting reports and methods used for reporting.....10

1.6 Discuss why the information needs to be accurate and understandable to the user..........................10

1.7 Evaluate the benefits of management accounting systems and their application in the organisation

context. (M1).........................................................................................................................................12

1.8 Critically evaluate how management accounting systems and management accounting reporting is

integrated within the organizational processes. Provide justifications to your proposed methods and

benefits in the organizational context. (D1)...........................................................................................13

TASK 2.....................................................................................................................................................14

2.1 What is the meant by cost? Explain different types of cost and cost analysis?................................14

2.2 define following terms with their explanation:................................................................................15

2.3 income statement with the helps of marginal and absorption costing..............................................17

2.4 What is the minimum number of unit that Zak needs to sell per year for X products? Use formula

product?.................................................................................................................................................19

2.5 Prepare a flexible budget.................................................................................................................19

2

Introduction.................................................................................................................................................5

TASK 1.......................................................................................................................................................6

1.1 Define and explain management accounting.....................................................................................6

1.2 What is management accounting system and why it is important to integrate it within the

organisation.............................................................................................................................................7

1.3 Distinguishing Management Accounting from Financial Accounting...............................................8

1.4 Define and explain different types of management accounting systems and their benefits within the

organisation.............................................................................................................................................9

1.5 Explain the different types of management accounting reports and methods used for reporting.....10

1.6 Discuss why the information needs to be accurate and understandable to the user..........................10

1.7 Evaluate the benefits of management accounting systems and their application in the organisation

context. (M1).........................................................................................................................................12

1.8 Critically evaluate how management accounting systems and management accounting reporting is

integrated within the organizational processes. Provide justifications to your proposed methods and

benefits in the organizational context. (D1)...........................................................................................13

TASK 2.....................................................................................................................................................14

2.1 What is the meant by cost? Explain different types of cost and cost analysis?................................14

2.2 define following terms with their explanation:................................................................................15

2.3 income statement with the helps of marginal and absorption costing..............................................17

2.4 What is the minimum number of unit that Zak needs to sell per year for X products? Use formula

product?.................................................................................................................................................19

2.5 Prepare a flexible budget.................................................................................................................19

2

2.6 Prepare a financial reporting document...........................................................................................20

2.7 produce financial report that apply and interpret the range of business activities............................20

Task 3........................................................................................................................................................21

Introduction...........................................................................................................................................21

3.1 What are budgets and how are they prepared. (P4)..........................................................................22

3.2 Discuss different types of Budget....................................................................................................24

3.3 Discuss different pricing strategies and how do competitors determine their price.........................25

3.4 What is meant by supply and demand consideration and how does demand and supply affect

pricing...................................................................................................................................................26

3.5 How does cost system differ depending upon the cost activity........................................................27

3.6 How SWOT analysis improve financial position of organization....................................................28

3.7 Analyze the use of different planning tools for preparing and forecasting budget (M3)..................29

Conclusion.............................................................................................................................................30

TASK 4.....................................................................................................................................................31

4.1 Identify financial problems using indicators such as:......................................................................31

4.2 Define financial governance and how these are used to prevent the financial problems. How do we

use it to monitor strategy.......................................................................................................................32

4.3 Discuss characteristics of effective management accountant and how these are used to solve

problems................................................................................................................................................33

4.4 Discuss the significance of developing strategies which requires effective and timely reporting....34

4.5 Analyze how in respond to financial problem management accounting can solve lead to sustainable

success (M4)..........................................................................................................................................35

3

2.7 produce financial report that apply and interpret the range of business activities............................20

Task 3........................................................................................................................................................21

Introduction...........................................................................................................................................21

3.1 What are budgets and how are they prepared. (P4)..........................................................................22

3.2 Discuss different types of Budget....................................................................................................24

3.3 Discuss different pricing strategies and how do competitors determine their price.........................25

3.4 What is meant by supply and demand consideration and how does demand and supply affect

pricing...................................................................................................................................................26

3.5 How does cost system differ depending upon the cost activity........................................................27

3.6 How SWOT analysis improve financial position of organization....................................................28

3.7 Analyze the use of different planning tools for preparing and forecasting budget (M3)..................29

Conclusion.............................................................................................................................................30

TASK 4.....................................................................................................................................................31

4.1 Identify financial problems using indicators such as:......................................................................31

4.2 Define financial governance and how these are used to prevent the financial problems. How do we

use it to monitor strategy.......................................................................................................................32

4.3 Discuss characteristics of effective management accountant and how these are used to solve

problems................................................................................................................................................33

4.4 Discuss the significance of developing strategies which requires effective and timely reporting....34

4.5 Analyze how in respond to financial problem management accounting can solve lead to sustainable

success (M4)..........................................................................................................................................35

3

4.6 Evaluate how planning tools for accounting respond to solve financial problem to attain the

sustainable success. (D3).......................................................................................................................36

Conclusion.................................................................................................................................................37

References.................................................................................................................................................38

4

sustainable success. (D3).......................................................................................................................36

Conclusion.................................................................................................................................................37

References.................................................................................................................................................38

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Introduction

The report deals with the explanation of management accounting with that how it is different

from financial accounting is also highlighted. With this the use of management accounting in

Zak Limited is explained which helps them in management accounting reporting. The analysis of

variance is also done so that the performance can be evaluated. Budgets are also highlighted and

the merits and demerits of those are also explained. The ways in with the management

accounting can solve the financial problem to attain the sustainable success is also highlighted.

The planning tools used for planning and controlling budget are also depicted.

5

The report deals with the explanation of management accounting with that how it is different

from financial accounting is also highlighted. With this the use of management accounting in

Zak Limited is explained which helps them in management accounting reporting. The analysis of

variance is also done so that the performance can be evaluated. Budgets are also highlighted and

the merits and demerits of those are also explained. The ways in with the management

accounting can solve the financial problem to attain the sustainable success is also highlighted.

The planning tools used for planning and controlling budget are also depicted.

5

TASK 1

1.1 Define and explain management accounting.

Definition of management accounting: It is a managerial process which involves planning,

identifying, controlling, measuring and communicating of information of the organisation.

Management accounting helps in decision making, formulation of plans and other things.

Further it helps to achieve its goals as the focus is on making of cash flows, budget planning,

financial statements (Johansson, et. al., 2012). On the other hand it truly differs from the

financial planning as it focuses on only organisation financial strategies.

It helps the firm to restructure its plans and actions with the management accounting techniques

which helps a company to gain the competitive edge. In all it is the internal focus on organisation

development through accounting techniques and tools like ABC model, ERM management

(Johansson, et. al., 2012).

6

1.1 Define and explain management accounting.

Definition of management accounting: It is a managerial process which involves planning,

identifying, controlling, measuring and communicating of information of the organisation.

Management accounting helps in decision making, formulation of plans and other things.

Further it helps to achieve its goals as the focus is on making of cash flows, budget planning,

financial statements (Johansson, et. al., 2012). On the other hand it truly differs from the

financial planning as it focuses on only organisation financial strategies.

It helps the firm to restructure its plans and actions with the management accounting techniques

which helps a company to gain the competitive edge. In all it is the internal focus on organisation

development through accounting techniques and tools like ABC model, ERM management

(Johansson, et. al., 2012).

6

1.2 What is management accounting system and why it is important to integrate it within

the organisation.

Management accounting system involved the formulation of plans preparation of reports,

financial statements, cash flow statement, balance sheets and other agendas which help managers

to achieve organisation goals by quick and accurate decision making.

It also includes managerial accounting reports like financial reports, cash flow pro forma and

everything making of financial items (Johansson, et. al., 2012).

It is important to integrate within the organisation to improve decision making of managers,

helping in the issues like mergers, takeovers and acquisition. The management accounting is

helping to analyze about the future outcomes of risk, measuring of our results which

management tools (Johansson, et. al., 2012). In overall it helps us to pursue the goals of

organisation with the financial information and the statistical information provided by the

financial accounts.

7

the organisation.

Management accounting system involved the formulation of plans preparation of reports,

financial statements, cash flow statement, balance sheets and other agendas which help managers

to achieve organisation goals by quick and accurate decision making.

It also includes managerial accounting reports like financial reports, cash flow pro forma and

everything making of financial items (Johansson, et. al., 2012).

It is important to integrate within the organisation to improve decision making of managers,

helping in the issues like mergers, takeovers and acquisition. The management accounting is

helping to analyze about the future outcomes of risk, measuring of our results which

management tools (Johansson, et. al., 2012). In overall it helps us to pursue the goals of

organisation with the financial information and the statistical information provided by the

financial accounts.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

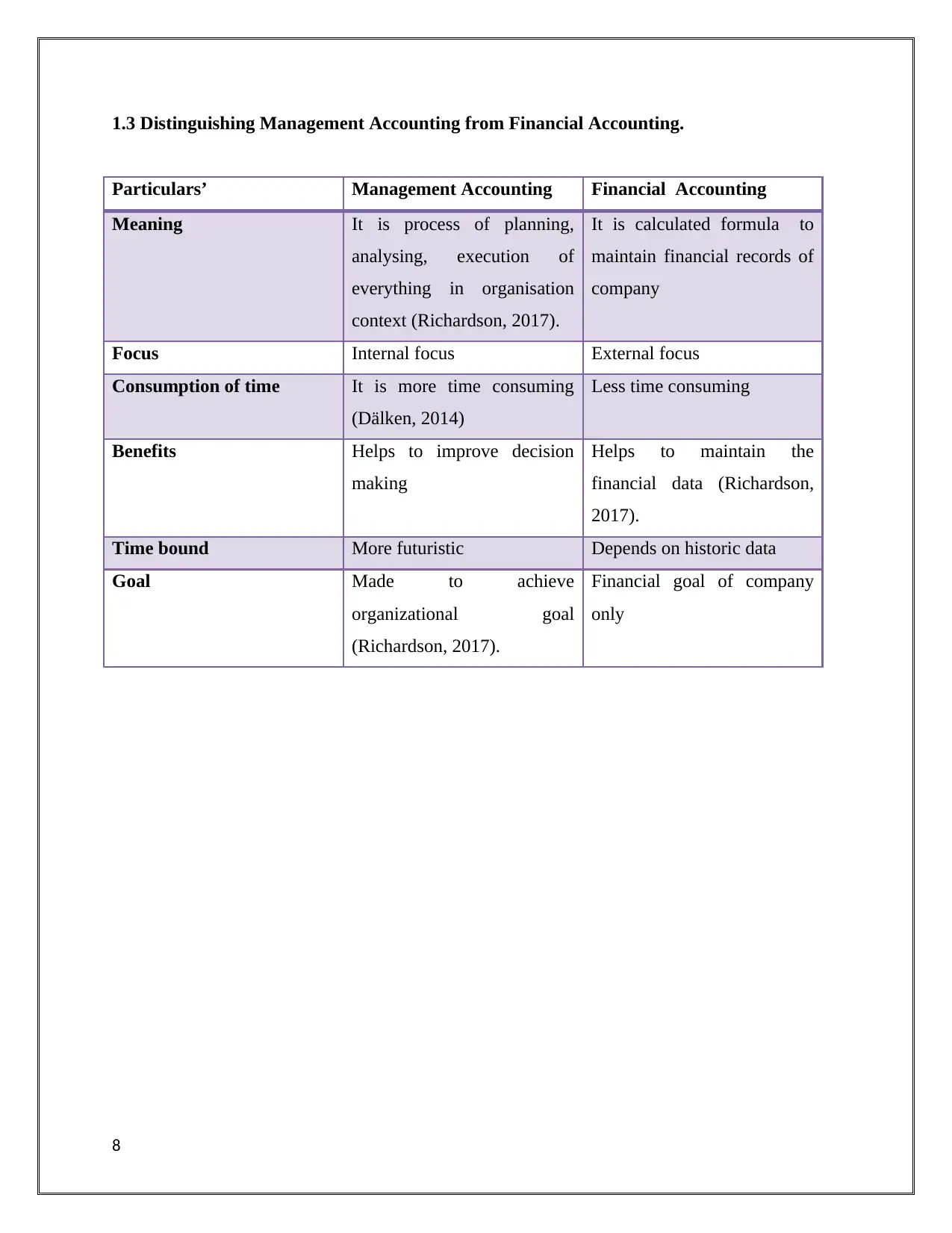

1.3 Distinguishing Management Accounting from Financial Accounting.

Particulars’ Management Accounting Financial Accounting

Meaning It is process of planning,

analysing, execution of

everything in organisation

context (Richardson, 2017).

It is calculated formula to

maintain financial records of

company

Focus Internal focus External focus

Consumption of time It is more time consuming

(Dälken, 2014)

Less time consuming

Benefits Helps to improve decision

making

Helps to maintain the

financial data (Richardson,

2017).

Time bound More futuristic Depends on historic data

Goal Made to achieve

organizational goal

(Richardson, 2017).

Financial goal of company

only

8

Particulars’ Management Accounting Financial Accounting

Meaning It is process of planning,

analysing, execution of

everything in organisation

context (Richardson, 2017).

It is calculated formula to

maintain financial records of

company

Focus Internal focus External focus

Consumption of time It is more time consuming

(Dälken, 2014)

Less time consuming

Benefits Helps to improve decision

making

Helps to maintain the

financial data (Richardson,

2017).

Time bound More futuristic Depends on historic data

Goal Made to achieve

organizational goal

(Richardson, 2017).

Financial goal of company

only

8

1.4 Define and explain different types of management accounting systems and their benefits

within the organisation

1.4.1 Cost accounting systems.

It is also called as costing system used by firms to know the cost of the product for the stock

valuation and profitability analysis. Estimated cost is monitored by the actual cost.

Normal costing: used to measure manufactured products (Johansson, et. al., 2012).

Actual costing: it involves recording of product cost.

Standard costing: it involves substitution of estimated and actual cost.

1.4.2 Inventory management systems

This system helps in managing the inventory from factory place till the goods are delivered to the

distribution place to the customers. In short it’s the whole management of inventory at it each

stage of product. It includes keeping a month to month record of inventory. This can be done by

using a ERP system (Johansson, et. al., 2012).

Valuation of inventory can be done by methods:

FIFO: “first in first out” means goods added first to the inventory are assumed to be the first

goods.

LIFO: “last in, First out” means goods added last in the category are assumed to be the first

goods.

Average: It’s a rarely used method with less accuracy.

1.4.3 Job costing systems

Job costing or the job order costing is the method of assigning a manufacturing cost to each

product manufactured in a company, this method is used by a company when the companies

product is slightly different from each other (Modell, 2012).

Job costing method uses some information for its use like:

1. Direct materials 2. Direct Labour: 3. Overheads

1.4.4 Price optimizing systems

This system is used by the company to know which price should be used to gain maximum

profits or using a pricing strategy to determine how customers will respond.

It is used of historical cost past data and other figures (Johansson, et. al., 2012).

9

within the organisation

1.4.1 Cost accounting systems.

It is also called as costing system used by firms to know the cost of the product for the stock

valuation and profitability analysis. Estimated cost is monitored by the actual cost.

Normal costing: used to measure manufactured products (Johansson, et. al., 2012).

Actual costing: it involves recording of product cost.

Standard costing: it involves substitution of estimated and actual cost.

1.4.2 Inventory management systems

This system helps in managing the inventory from factory place till the goods are delivered to the

distribution place to the customers. In short it’s the whole management of inventory at it each

stage of product. It includes keeping a month to month record of inventory. This can be done by

using a ERP system (Johansson, et. al., 2012).

Valuation of inventory can be done by methods:

FIFO: “first in first out” means goods added first to the inventory are assumed to be the first

goods.

LIFO: “last in, First out” means goods added last in the category are assumed to be the first

goods.

Average: It’s a rarely used method with less accuracy.

1.4.3 Job costing systems

Job costing or the job order costing is the method of assigning a manufacturing cost to each

product manufactured in a company, this method is used by a company when the companies

product is slightly different from each other (Modell, 2012).

Job costing method uses some information for its use like:

1. Direct materials 2. Direct Labour: 3. Overheads

1.4.4 Price optimizing systems

This system is used by the company to know which price should be used to gain maximum

profits or using a pricing strategy to determine how customers will respond.

It is used of historical cost past data and other figures (Johansson, et. al., 2012).

9

1.5 Explain the different types of management accounting reports and methods used for

reporting.

Managerial accounting reports like:

1. Financial Reports: it consists of making of profit and loss statement, balance sheet (GÜREL

and TAT, 2017).

2. Pro Forma Cash Flow: It gives a month to month summary of inflow and outflow of cash

from the business operations.

3. Sales reports: Tool as it shows the profits on sale and let us know the revenue generation in

terms of the company expenses (GÜREL and TAT, 2017).

4. Item cost reports: it helps us to make you more accurate knowing of your expenditures in

terms of direct labor, material and overheads expenses.

Methods used in reporting:

Cost reports: reports made for identifying cost of business.

Budgets: a futuristic plan made for an organisation.

Execution reports: a report which is made directly to be executed and has everything within it

(Gomes and Romão, 2017).

Image: Types of reports

Source: By Author, 2018

1.6 Discuss why the information needs to be accurate and understandable to the user.

Financial information are the final records of the business organisation, it is presented accurately

because they reveal the true value of company (GÜREL and TAT, 2017). Goodwill of company

depends on net worth, so it should be shown correctly to the public. As well as the public are the

investors so they need accuracy in financial terms.

10

CostreportsBudgets

reporting.

Managerial accounting reports like:

1. Financial Reports: it consists of making of profit and loss statement, balance sheet (GÜREL

and TAT, 2017).

2. Pro Forma Cash Flow: It gives a month to month summary of inflow and outflow of cash

from the business operations.

3. Sales reports: Tool as it shows the profits on sale and let us know the revenue generation in

terms of the company expenses (GÜREL and TAT, 2017).

4. Item cost reports: it helps us to make you more accurate knowing of your expenditures in

terms of direct labor, material and overheads expenses.

Methods used in reporting:

Cost reports: reports made for identifying cost of business.

Budgets: a futuristic plan made for an organisation.

Execution reports: a report which is made directly to be executed and has everything within it

(Gomes and Romão, 2017).

Image: Types of reports

Source: By Author, 2018

1.6 Discuss why the information needs to be accurate and understandable to the user.

Financial information are the final records of the business organisation, it is presented accurately

because they reveal the true value of company (GÜREL and TAT, 2017). Goodwill of company

depends on net worth, so it should be shown correctly to the public. As well as the public are the

investors so they need accuracy in financial terms.

10

CostreportsBudgets

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial statements, balance sheet, profit &loss do reveal company true position. Like showing

of contingent liabilities at the foot note of balance sheet needs to disclosed as it gives true

information of company policies to the public (GÜREL and TAT, 2017).

11

of contingent liabilities at the foot note of balance sheet needs to disclosed as it gives true

information of company policies to the public (GÜREL and TAT, 2017).

11

1.7 Evaluate the benefits of management accounting systems and their application in the

organisation context. (M1)

It helps in better decision making as making of reports and accounts, better controlling which

improves the efficiency of the organisation (GÜREL and TAT, 2017). It helps in better

management so that it serves customer satisfaction. It provides motivation to employers and

better flow of communication among the employees (Modell, 2012).

Benefits of management accounting in the context of Zak Ltd it provides better flow of

communication between the employees, it’s a manufacturing company which needs coordination

and utilization of units which now is happening with it (GÜREL and TAT, 2017).

12

organisation context. (M1)

It helps in better decision making as making of reports and accounts, better controlling which

improves the efficiency of the organisation (GÜREL and TAT, 2017). It helps in better

management so that it serves customer satisfaction. It provides motivation to employers and

better flow of communication among the employees (Modell, 2012).

Benefits of management accounting in the context of Zak Ltd it provides better flow of

communication between the employees, it’s a manufacturing company which needs coordination

and utilization of units which now is happening with it (GÜREL and TAT, 2017).

12

1.8 Critically evaluate how management accounting systems and management accounting

reporting is integrated within the organizational processes. Provide justifications to your

proposed methods and benefits in the organizational context. (D1)

Both are correlated with each other as management systems include the overall process of

making of financial records and annual statement (GÜREL and TAT, 2017). Whereas the

management accounting reporting includes making of management reports as sales reports, cash

flow reports etc. Both are correlated in each term.

It is integrated through well developed tools and techniques and for that C.A and practitioners

are appointed.

Use of ABC model ERM management tools as well as other costing methods this methods can

help the Zak ltd to overcome its issues. This method is economical, more utilisation and yields

better results (GÜREL and TAT, 2017).

13

reporting is integrated within the organizational processes. Provide justifications to your

proposed methods and benefits in the organizational context. (D1)

Both are correlated with each other as management systems include the overall process of

making of financial records and annual statement (GÜREL and TAT, 2017). Whereas the

management accounting reporting includes making of management reports as sales reports, cash

flow reports etc. Both are correlated in each term.

It is integrated through well developed tools and techniques and for that C.A and practitioners

are appointed.

Use of ABC model ERM management tools as well as other costing methods this methods can

help the Zak ltd to overcome its issues. This method is economical, more utilisation and yields

better results (GÜREL and TAT, 2017).

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

2.1 What is the meant by cost? Explain different types of cost and cost analysis?

Cost:

Cost can be referred to the monetary expenditure by which firm can incur in order to purchase or hire all

those factors which are necessary to the production and management. It is determined as expense of

purchasing, investing and hiring factors and different services for production and managerial activities.

Cost analysis:

Types of cost:

1. Fixed cost: fixed cost can be defined as fixed inputs managed in production of products. These costs

cannot varies changes with the fluctuation occurred in volume of production.

2. Variable cost: it is the cost in which variable inputs can be used in the production level. These costs are

able to vary with the changes in the production level (Laudon

&Laudon, 2016)

3. Semi-variable cost: semi-variable cost is those cost which are the mixture of fixed and variable cost.

Such kinds of cost cannot be affected directly with the changes in the level of production. For instance;

administration cost, selling and distribution cost etc.

4. Total cost: total cost is related to the aggregate of production cost. It is defined by summing up all fixed

and variable cost of production.

5. Marginal cost: it refers to the cost which is related to the production of additional units of the product.

MC= TCN –TCN-1

On the basis of expense:

1. Material cost: such kinds of costs are directly related to the production and cost of procurement which

is utilised in the raw material for production.

2. Labour Cost: such kinds of costs are related to the payment made to the permanents and temporary

purposes. It is meant to be and directly related to payment provided to labour as wages and remunerations

etc.

3. Overhead cost: such cost is those costs which are likely to be semi-variable cost and vary with the level

of production units for instance; administration expense, selling expense and distribution expense etc.

Other cost:

1. Sunk cost: sunk costs are referred to the costs which are not be altered by the fluctuation in current

state of business and in activity.

2. Opportunity cost: these kinds of costs are taken as foregone opportunity or nest best alternative actions

which can be sacrificed in subject to pursue the alternative actions.

14

2.1 What is the meant by cost? Explain different types of cost and cost analysis?

Cost:

Cost can be referred to the monetary expenditure by which firm can incur in order to purchase or hire all

those factors which are necessary to the production and management. It is determined as expense of

purchasing, investing and hiring factors and different services for production and managerial activities.

Cost analysis:

Types of cost:

1. Fixed cost: fixed cost can be defined as fixed inputs managed in production of products. These costs

cannot varies changes with the fluctuation occurred in volume of production.

2. Variable cost: it is the cost in which variable inputs can be used in the production level. These costs are

able to vary with the changes in the production level (Laudon

&Laudon, 2016)

3. Semi-variable cost: semi-variable cost is those cost which are the mixture of fixed and variable cost.

Such kinds of cost cannot be affected directly with the changes in the level of production. For instance;

administration cost, selling and distribution cost etc.

4. Total cost: total cost is related to the aggregate of production cost. It is defined by summing up all fixed

and variable cost of production.

5. Marginal cost: it refers to the cost which is related to the production of additional units of the product.

MC= TCN –TCN-1

On the basis of expense:

1. Material cost: such kinds of costs are directly related to the production and cost of procurement which

is utilised in the raw material for production.

2. Labour Cost: such kinds of costs are related to the payment made to the permanents and temporary

purposes. It is meant to be and directly related to payment provided to labour as wages and remunerations

etc.

3. Overhead cost: such cost is those costs which are likely to be semi-variable cost and vary with the level

of production units for instance; administration expense, selling expense and distribution expense etc.

Other cost:

1. Sunk cost: sunk costs are referred to the costs which are not be altered by the fluctuation in current

state of business and in activity.

2. Opportunity cost: these kinds of costs are taken as foregone opportunity or nest best alternative actions

which can be sacrificed in subject to pursue the alternative actions.

14

2.2 define following terms with their explanation:

1. Cost volume profit: Cost-Volume-Profit analysis (CVP) analysis can be taken as managerial

accounting technique which is concerned with the influences of sales volume and production costs in the

basis of operating profit in the business. It deals with the management and how all operating profit can be

affected by changes in variable costs, fixed and semi variable costs while setting prices and management

criteria.

It follows following assumptions:

1. All costs are categorised as variable and fixed expense.

2. Sales price per unit, variable cost p.u. and total fixed cost are defined are constant.

3. All units are determined as to be sold.

CVP analysis formula:

PX = vx + FC+ Profit

2. Flexible budgeting: flexible budgeting are the method which are made to flex and adjust all changes in

the volume of production activity, it is more sophisticated in nature while measuring volume of

production.

3. Cost variances: it is amount or a value of money which is actually spent on such project related to

production. It is the budgeted cost of work performed subtracted form the actual cost of work performed.

4. Absorption and marginal accounting: marginal costing technique differentiates between fixed and

variable cost. Only variable costs in ascertained while making or valuating cost. Absorption costing are

those costing techniques, in which all production costs are equally determined including both variable

plus fixed cost while make valuation of closing stock for absorption method.

5. Normal and standard costing:

Normal costing: it is adopted as usual accounting costing technique of production in which while

evaluating manufactured costs with actual production costs.

Standards costing: in the standards costing, all costs of production are determined on the basis of setting

standard and expected costs based on predetermined manufacturing overheads.

6. Activity based costing: ABC costing is the costing which are used to determine production and actual

level of inventory. It is management tools which are used to determine and set cost of production based

on level or activity (Mussati, et .al.,2018).

7. Overhead cost: Overhead cost is referred to other operating and factory costs and expense which are

related to such expense associated with running activity in the business. Such kinds of activities cannot be

related to running production or service.

8. Cost allocation method:cost allocation can be defined as cost researching assignment. It is a concept of

finding cost of different objects such as projects, department, units and branches etc. cost allocation is

15

1. Cost volume profit: Cost-Volume-Profit analysis (CVP) analysis can be taken as managerial

accounting technique which is concerned with the influences of sales volume and production costs in the

basis of operating profit in the business. It deals with the management and how all operating profit can be

affected by changes in variable costs, fixed and semi variable costs while setting prices and management

criteria.

It follows following assumptions:

1. All costs are categorised as variable and fixed expense.

2. Sales price per unit, variable cost p.u. and total fixed cost are defined are constant.

3. All units are determined as to be sold.

CVP analysis formula:

PX = vx + FC+ Profit

2. Flexible budgeting: flexible budgeting are the method which are made to flex and adjust all changes in

the volume of production activity, it is more sophisticated in nature while measuring volume of

production.

3. Cost variances: it is amount or a value of money which is actually spent on such project related to

production. It is the budgeted cost of work performed subtracted form the actual cost of work performed.

4. Absorption and marginal accounting: marginal costing technique differentiates between fixed and

variable cost. Only variable costs in ascertained while making or valuating cost. Absorption costing are

those costing techniques, in which all production costs are equally determined including both variable

plus fixed cost while make valuation of closing stock for absorption method.

5. Normal and standard costing:

Normal costing: it is adopted as usual accounting costing technique of production in which while

evaluating manufactured costs with actual production costs.

Standards costing: in the standards costing, all costs of production are determined on the basis of setting

standard and expected costs based on predetermined manufacturing overheads.

6. Activity based costing: ABC costing is the costing which are used to determine production and actual

level of inventory. It is management tools which are used to determine and set cost of production based

on level or activity (Mussati, et .al.,2018).

7. Overhead cost: Overhead cost is referred to other operating and factory costs and expense which are

related to such expense associated with running activity in the business. Such kinds of activities cannot be

related to running production or service.

8. Cost allocation method:cost allocation can be defined as cost researching assignment. It is a concept of

finding cost of different objects such as projects, department, units and branches etc. cost allocation is

15

allocating activity which defined different methods of rendering services and helps to categorise business

cost and profit.

9. Role of costing in setting prices:

Costing is the process of determining expense and accuracy process of profit and revenue; it is based on

cost based analysis which is allowed the company to setting prices through sales and production

department. It reduces all costs and additional wastage to increase profit after setting profitable prices.

10. Inventory cost and their different types:

Inventory cost can be classified into three parts, first is raw material, semi-finished costs and finished

costs depending on business activities and process, companies use to adopt different inventory cost

techniques in their management (Dale and Plunkett, 2017)

Inventory cost is those cost which are regulatory performed to measure inventory expense

Types:

1. Inventory holding cost: it is the cost which is incurred while storing various inventory and stock of

products in company’s warehouses. Invoice, bills, warehouses duties are known as inventory holding

costs (Lomas, et. al., 2018).

2. Processing costs: Processing costs are those costs which are used or performed while working on

inventory at the time of production or when it is ready to sale. It is the costs which are regulatory related

to various procedure or steps at workplace.

16

cost and profit.

9. Role of costing in setting prices:

Costing is the process of determining expense and accuracy process of profit and revenue; it is based on

cost based analysis which is allowed the company to setting prices through sales and production

department. It reduces all costs and additional wastage to increase profit after setting profitable prices.

10. Inventory cost and their different types:

Inventory cost can be classified into three parts, first is raw material, semi-finished costs and finished

costs depending on business activities and process, companies use to adopt different inventory cost

techniques in their management (Dale and Plunkett, 2017)

Inventory cost is those cost which are regulatory performed to measure inventory expense

Types:

1. Inventory holding cost: it is the cost which is incurred while storing various inventory and stock of

products in company’s warehouses. Invoice, bills, warehouses duties are known as inventory holding

costs (Lomas, et. al., 2018).

2. Processing costs: Processing costs are those costs which are used or performed while working on

inventory at the time of production or when it is ready to sale. It is the costs which are regulatory related

to various procedure or steps at workplace.

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

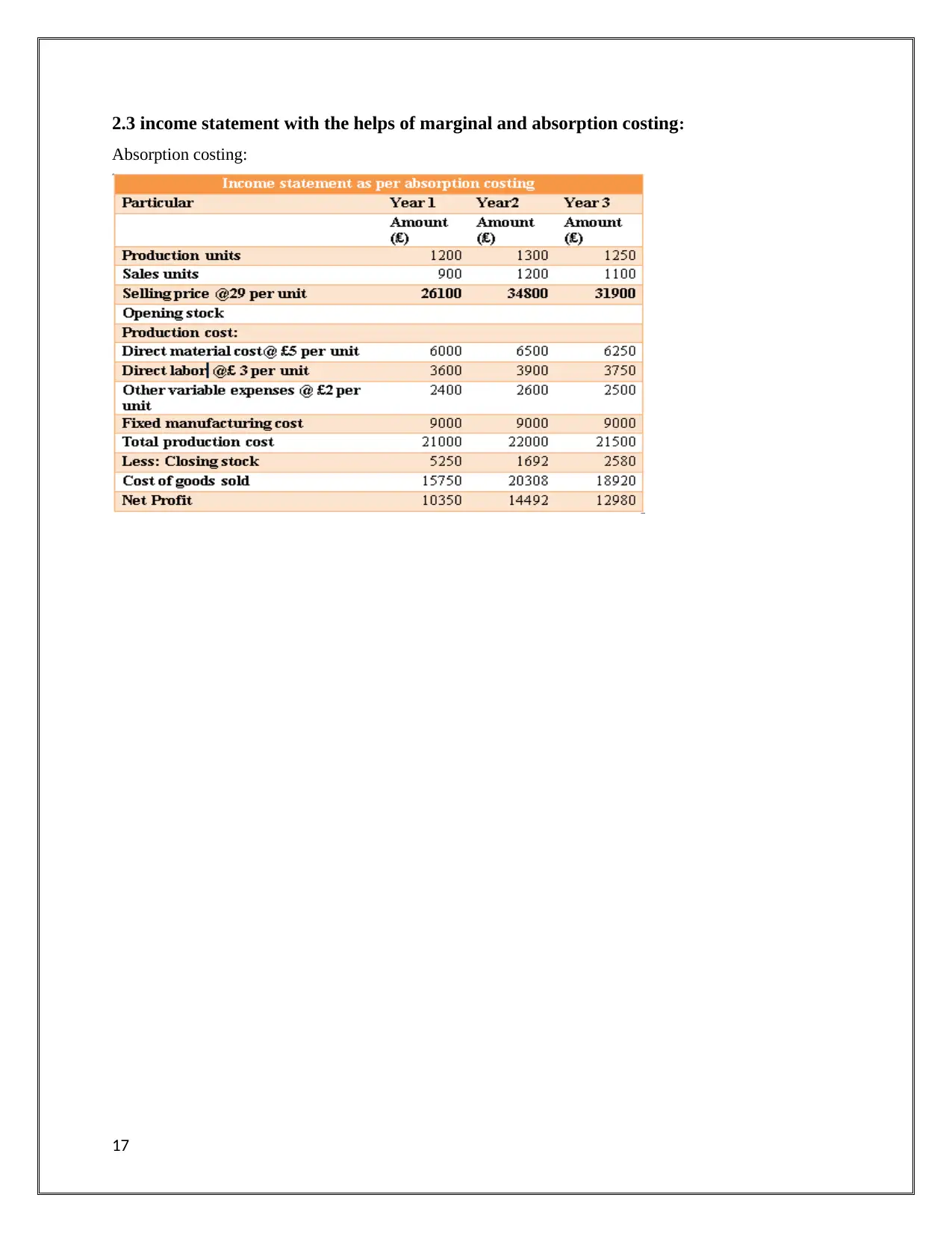

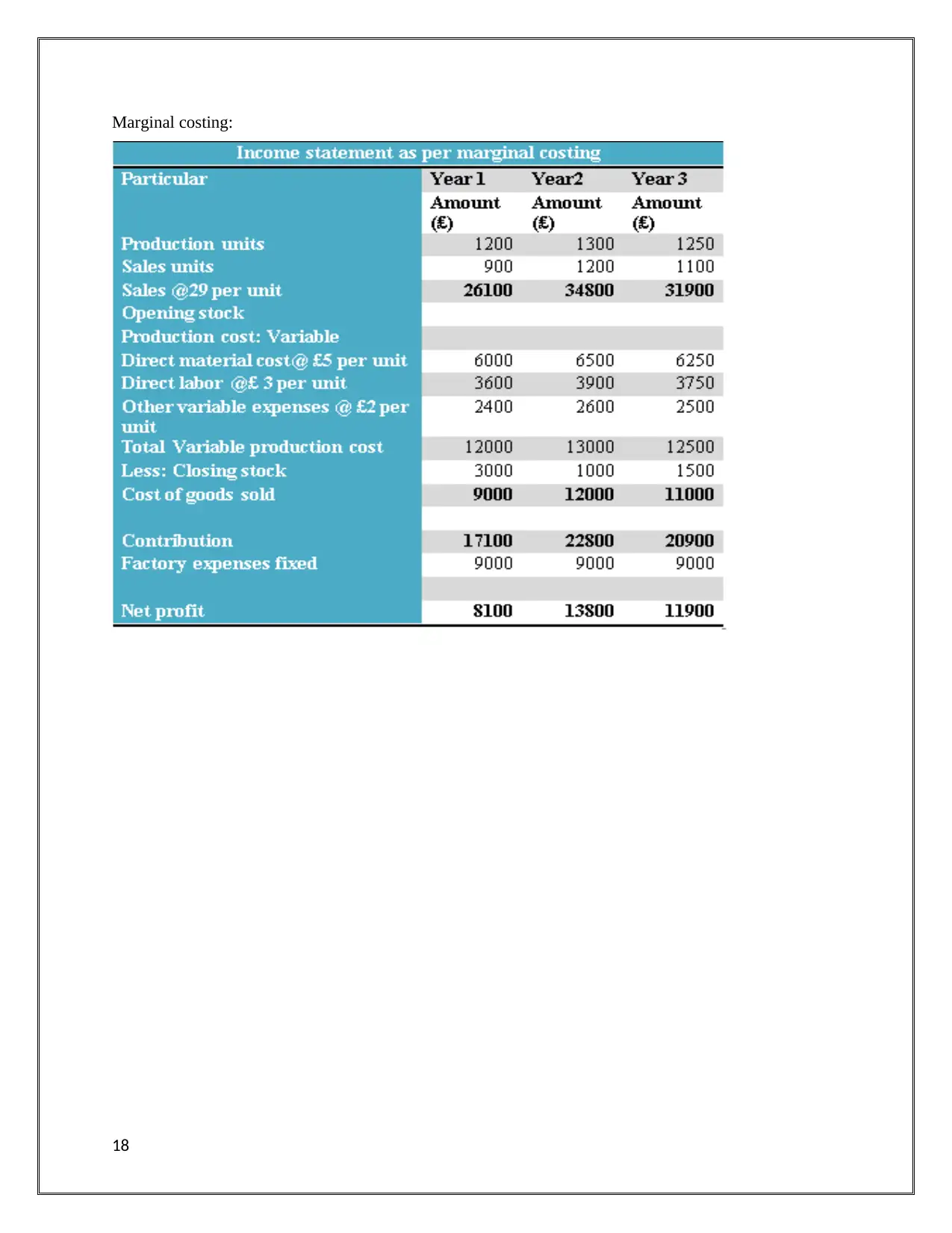

2.3 income statement with the helps of marginal and absorption costing:

Absorption costing:

17

Absorption costing:

17

Marginal costing:

18

18

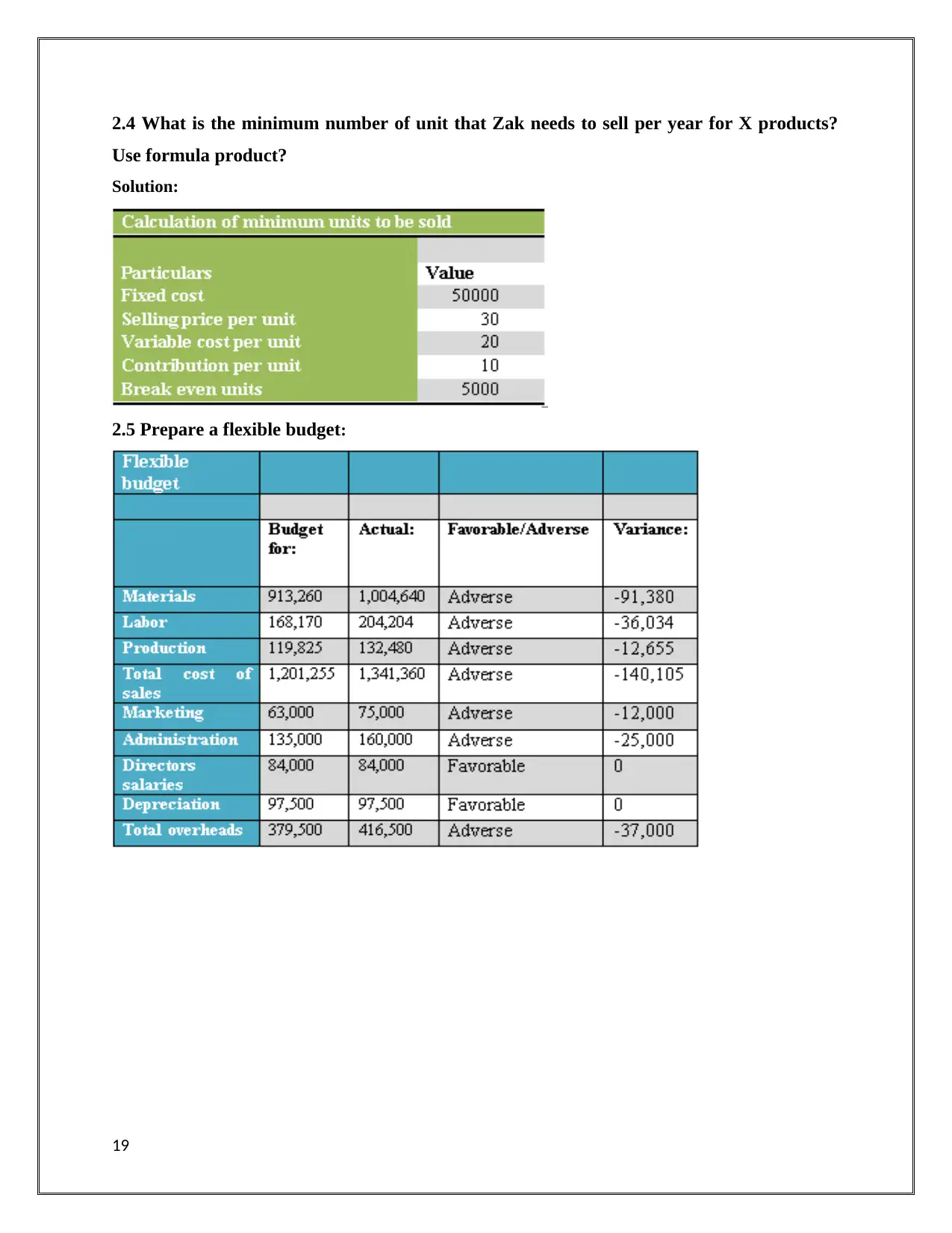

2.4 What is the minimum number of unit that Zak needs to sell per year for X products?

Use formula product?

Solution:

2.5 Prepare a flexible budget:

19

Use formula product?

Solution:

2.5 Prepare a flexible budget:

19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.6 Prepare a financial reporting document:

Management accounting techniques can be used for better accounting and financial decision in the

company. Company can utilize such method as costing methodologies and for the long term analysis of

business projects so that accuracy and flexibility of decision can be measured through management

accounting systems, costing techniques such as variable costing, marginal costing, variance analysis and

cost analysis are such types of management techniques which allows the company to support and regulate

financial threats and prepare financial report more accurate and exact to achieve long term objectives.

2.7 produce financial report that apply and interpret the range of business activities:

Financial report:

Management accounting techniques and accounting systems are these systems which are used in

observing, designing, implementing and executing financial plans to get long term achievements in the

business. It helps in managing financial plans effectively and regulates budget and sale forecasting

decision by controlling budget and make financial decision. Variance analysis is the analysis which helps

in controlling and management of financial decision. It helps the management to achieve business

financial and non-financial objectives in order to reduce cost and increase productivity and efficiency in

the business (Cooper, 2017)

20

Management accounting techniques can be used for better accounting and financial decision in the

company. Company can utilize such method as costing methodologies and for the long term analysis of

business projects so that accuracy and flexibility of decision can be measured through management

accounting systems, costing techniques such as variable costing, marginal costing, variance analysis and

cost analysis are such types of management techniques which allows the company to support and regulate

financial threats and prepare financial report more accurate and exact to achieve long term objectives.

2.7 produce financial report that apply and interpret the range of business activities:

Financial report:

Management accounting techniques and accounting systems are these systems which are used in

observing, designing, implementing and executing financial plans to get long term achievements in the

business. It helps in managing financial plans effectively and regulates budget and sale forecasting

decision by controlling budget and make financial decision. Variance analysis is the analysis which helps

in controlling and management of financial decision. It helps the management to achieve business

financial and non-financial objectives in order to reduce cost and increase productivity and efficiency in

the business (Cooper, 2017)

20

Task 3

Introduction

This part of the report deals with explanation of different types of budget and their advantages as

well as disadvantages. With that it also explains the use of various planning tools which are used for

planning and controlling the budget.

21

Introduction

This part of the report deals with explanation of different types of budget and their advantages as

well as disadvantages. With that it also explains the use of various planning tools which are used for

planning and controlling the budget.

21

3.1 What are budgets and how are they prepared. (P4)

Budget is the statement which shows estimation of the revenues and expenses for the future

period of time. It includes the plans which are related to the cost, sales volume, revenue,

quantities of resources and assets (GÜREL and TAT, 2017).

Advantages:

The advantage of the budget is that it will help in focusing for the long term objectives of the

business by controlling the cost and increasing revenues (GÜREL and TAT, 2017).

Disadvantage:

The main disadvantage is that the future is uncertain and the budgets are prepared by forecasting

the future (Gupta, 2013).

The budget preparation involves specified steps which are:

Image: Steps for budget preparation

Source: By Author, 2018

Obtaining Estimates: At this stage the estimation of expected cost, sales and production level

are done. With this estimation of the future cost and the revenues which may impact the business

are also considered (Gupta, 2013).

Coordinating Estimates: The plans which are submitted by the organizational units are

evaluated. This evaluation is done so as to utilize the resources accordingly.

22

ObtainingEstimatesCoordinatingEstimatesCommunicatingBudgetImplementationReportingProgressTowardsBudgetObjectives

Budget is the statement which shows estimation of the revenues and expenses for the future

period of time. It includes the plans which are related to the cost, sales volume, revenue,

quantities of resources and assets (GÜREL and TAT, 2017).

Advantages:

The advantage of the budget is that it will help in focusing for the long term objectives of the

business by controlling the cost and increasing revenues (GÜREL and TAT, 2017).

Disadvantage:

The main disadvantage is that the future is uncertain and the budgets are prepared by forecasting

the future (Gupta, 2013).

The budget preparation involves specified steps which are:

Image: Steps for budget preparation

Source: By Author, 2018

Obtaining Estimates: At this stage the estimation of expected cost, sales and production level

are done. With this estimation of the future cost and the revenues which may impact the business

are also considered (Gupta, 2013).

Coordinating Estimates: The plans which are submitted by the organizational units are

evaluated. This evaluation is done so as to utilize the resources accordingly.

22

ObtainingEstimatesCoordinatingEstimatesCommunicatingBudgetImplementationReportingProgressTowardsBudgetObjectives

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Communicating Budget: Once the estimates are coordinated then the budget is communicated

to various departments. At this stage the managers of the organization can modify the plan

according to the availability of resources (Gupta, 2013).

Implementation: The final budget is presented to all the managers and the plan is adopted for

the current accounting period.

Reporting Progress: The performance reports are prepared so that the performance of the report

can be evaluated according to the determined plan. If there are any variances then it requires the

need for the revision of plan.

23

to various departments. At this stage the managers of the organization can modify the plan

according to the availability of resources (Gupta, 2013).

Implementation: The final budget is presented to all the managers and the plan is adopted for

the current accounting period.

Reporting Progress: The performance reports are prepared so that the performance of the report

can be evaluated according to the determined plan. If there are any variances then it requires the

need for the revision of plan.

23

3.2 Discuss different types of Budget.

Operating Budget: The operating budget helps in analysis of projected income and expenses

over the period of time (Shpak, 2018). These budgets are created on weekly, quarterly and the

monthly basis. The managers of the organization can compare on the monthly basis about the

suppliers of company.

Advantages: The advantage of the operating budget is that it helps in managing the current

expenses as it helps in evaluating the areas where the considerable savings can benefit the total

budget of the organization.

Disadvantages: The projections which are done for the long term can lead to the shortage of

funds so as to meet the financial obligations (Shpak, 2018).

Capital Budgeting: These are the planning process which is used to determine whether the

organizations for the long term investment are worth for the funding or not of the capitalization

structure.

Advantages:

It helps the organization for taking the long term strategic decisions.

It also offers the control over expenditure for the projects (Shpak, 2018).

Disadvantages:

These budgeting are for the long term decisions which are irreversible in nature.

24

Operating Budget: The operating budget helps in analysis of projected income and expenses

over the period of time (Shpak, 2018). These budgets are created on weekly, quarterly and the

monthly basis. The managers of the organization can compare on the monthly basis about the

suppliers of company.

Advantages: The advantage of the operating budget is that it helps in managing the current

expenses as it helps in evaluating the areas where the considerable savings can benefit the total

budget of the organization.

Disadvantages: The projections which are done for the long term can lead to the shortage of

funds so as to meet the financial obligations (Shpak, 2018).

Capital Budgeting: These are the planning process which is used to determine whether the

organizations for the long term investment are worth for the funding or not of the capitalization

structure.

Advantages:

It helps the organization for taking the long term strategic decisions.

It also offers the control over expenditure for the projects (Shpak, 2018).

Disadvantages:

These budgeting are for the long term decisions which are irreversible in nature.

24

3.3 Discuss different pricing strategies and how do competitors determine their price.

Pricing for market Penetration: The market penetration is the strategy in the market for

offering the goods and services at lower price. This strategy is adopted in the initial stage so that

the market share can be captured and the customers can be attracted.

Advantages: This strategy will help in increasing the growth of the business at the initial stage

as the better prices will be offered than the competitors.

Disadvantages: As the company has the various product lines so the penetration strategy might

be harmful for the degrading the company image (Wise GEEK, 2018).

Price skimming: It is the strategy for setting the price at high rate during the initial stage. The

main motive of this strategy is just to capture the market share and increase profits.

Advantages: The main advantage is that through this strategy the business can attain the profits

at the introductory stage before dropping the price to attract more of the customers (Shpak,

2018).

Disadvantages: It cannot be applied to those countries where there are strict rights regarding

legal and government regulations.

The competitors set their prices according to the pricing strategy of the organization who is the

competitor. If the price of organization’s products and services are high so the competitor will

keep low price and vice versa (Wise GEEK, 2018). But in some cases the price of goods and

services can also be kept equal to the competitor’s price.

25

Pricing for market Penetration: The market penetration is the strategy in the market for

offering the goods and services at lower price. This strategy is adopted in the initial stage so that

the market share can be captured and the customers can be attracted.

Advantages: This strategy will help in increasing the growth of the business at the initial stage

as the better prices will be offered than the competitors.

Disadvantages: As the company has the various product lines so the penetration strategy might

be harmful for the degrading the company image (Wise GEEK, 2018).

Price skimming: It is the strategy for setting the price at high rate during the initial stage. The

main motive of this strategy is just to capture the market share and increase profits.

Advantages: The main advantage is that through this strategy the business can attain the profits

at the introductory stage before dropping the price to attract more of the customers (Shpak,

2018).

Disadvantages: It cannot be applied to those countries where there are strict rights regarding

legal and government regulations.

The competitors set their prices according to the pricing strategy of the organization who is the

competitor. If the price of organization’s products and services are high so the competitor will

keep low price and vice versa (Wise GEEK, 2018). But in some cases the price of goods and

services can also be kept equal to the competitor’s price.

25

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3.4 What is meant by supply and demand consideration and how does demand and supply

affect pricing.

The supply and demand are the major factor in determining the market place. The supply of

goods helps in determining the price of the goods and services (Market Business, 2018). Another

factor is the demand which means the willingness and the ability of the customer to purchase

goods and services. If the demand for the product will be low so its supply will also decrease and

if the demand for product is high then the supply will also increase. So, the demand and supply

are inversely related to each other (Market Business, 2018).

Image: Supply and Demand

Source: Market Business, 2018

The demand and supply affects pricing as when the demand rises the supply falls and the prices

of the products and services rises whereas the price falls when the demand falls and the supply

rises (Wise GEEK, 2018).

26

affect pricing.

The supply and demand are the major factor in determining the market place. The supply of

goods helps in determining the price of the goods and services (Market Business, 2018). Another

factor is the demand which means the willingness and the ability of the customer to purchase

goods and services. If the demand for the product will be low so its supply will also decrease and

if the demand for product is high then the supply will also increase. So, the demand and supply

are inversely related to each other (Market Business, 2018).

Image: Supply and Demand

Source: Market Business, 2018

The demand and supply affects pricing as when the demand rises the supply falls and the prices

of the products and services rises whereas the price falls when the demand falls and the supply

rises (Wise GEEK, 2018).

26

3.5 How does cost system differ depending upon the cost activity.

Job Costing: it is system which tracks the cost and revenues of the particular job. The advantage

is that the cost can be estimated of the job according to the past records of the job costing (Albu

Consulting, 2017). With this it also has disadvantages as the comparison is difficult during

inflation.

Process Costing: It ascertains the cost of product at each stage of the production process

(Dulčić, et. al., 2012). The main advantage of process costing is that it is easier to use when the

homogeneous costing products are compared. There are production cost errors which is the

major disadvantage (Wise GEEK, 2018).

Batch Costing: It assigns the cost to the particular batch. Through this the cost can be reduced of

production arised out of batch quantity. These systems are costly to use.

Contract Costing: These costs are assigned for the contract basis. The advantage of this costing

is that the delay for the work is reduced and the disadvantage is the contractors have to pay for

all the inefficiencies.

27

Job Costing: it is system which tracks the cost and revenues of the particular job. The advantage

is that the cost can be estimated of the job according to the past records of the job costing (Albu

Consulting, 2017). With this it also has disadvantages as the comparison is difficult during

inflation.

Process Costing: It ascertains the cost of product at each stage of the production process

(Dulčić, et. al., 2012). The main advantage of process costing is that it is easier to use when the

homogeneous costing products are compared. There are production cost errors which is the

major disadvantage (Wise GEEK, 2018).

Batch Costing: It assigns the cost to the particular batch. Through this the cost can be reduced of

production arised out of batch quantity. These systems are costly to use.

Contract Costing: These costs are assigned for the contract basis. The advantage of this costing

is that the delay for the work is reduced and the disadvantage is the contractors have to pay for

all the inefficiencies.

27

3.6 How SWOT analysis improve financial position of organization.

The SWOT analysis improves the financial performance in the following ways:

Strategies: The organization can prepare the strategies accordingly once the weakness of the

organization will be determined (Albu Consulting, 2017).

Clear View: The SWOT analysis gives the clear view to the organization about the strength,

weaknesses, and opportunities and threats so that the organization can predict its overall

performance in the competitive market (Albu Consulting, 2017).

Improves operations: The operations of the organization can be improved by looking forward

for the opportunities and the weaknesses of business.

28

The SWOT analysis improves the financial performance in the following ways:

Strategies: The organization can prepare the strategies accordingly once the weakness of the

organization will be determined (Albu Consulting, 2017).

Clear View: The SWOT analysis gives the clear view to the organization about the strength,

weaknesses, and opportunities and threats so that the organization can predict its overall

performance in the competitive market (Albu Consulting, 2017).

Improves operations: The operations of the organization can be improved by looking forward

for the opportunities and the weaknesses of business.

28

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

3.7 Analyze the use of different planning tools for preparing and forecasting budget (M3).

PEST Analysis: The PEST analysis is done to determine the position of the company in the

external market. Here the PEST stands for political, economical, social and technological factors

(Gupta, 2013).

SWOT Analysis: This is the analysis which is done to determine the internal ability of the

organization to compete with the external environment. It identifies the area of improvement so

that the profits can be increased (Albu Consulting, 2017).

Balance Score Card: It defines the objectives that can be considered by the organization so as to

increase the position of the organization. It also provides the measures for improvements.

Porter’s Five Forces: It is the tool which helps in identifying those forces which may impact the

profitability of the organization (Gupta, 2013).

29

PEST Analysis: The PEST analysis is done to determine the position of the company in the

external market. Here the PEST stands for political, economical, social and technological factors

(Gupta, 2013).

SWOT Analysis: This is the analysis which is done to determine the internal ability of the

organization to compete with the external environment. It identifies the area of improvement so

that the profits can be increased (Albu Consulting, 2017).

Balance Score Card: It defines the objectives that can be considered by the organization so as to

increase the position of the organization. It also provides the measures for improvements.

Porter’s Five Forces: It is the tool which helps in identifying those forces which may impact the

profitability of the organization (Gupta, 2013).

29

Conclusion

It can be concluded that budgets help the organization in determining the future. The planning

tools of the organization help in analyzing the financial position of the organization. Supply and

demand both are useful for evaluating the price of product.

30

It can be concluded that budgets help the organization in determining the future. The planning

tools of the organization help in analyzing the financial position of the organization. Supply and

demand both are useful for evaluating the price of product.

30

TASK 4

4.1 Identify financial problems using indicators such as:

4.1.1 Benchmark: The benchmark means that the particular standards are set by the

organization from which the comparison is done and the financial performance of the

organization is evaluated. It also shows the reasons for the variance in the revenues and the cost

(Richardson, 2017).

4.1.2 Key Performance Indicator: It is the indicator to recognize that the organization is going

according to the accounting standards or not. These are the indicators through which weaknesses

can be evaluated. The KPI’s are both financial as well as non financial (Albu Consulting, 2017).

4.1.3 Budgetary targets to identify variances: These are the targets which are set by the

organization to evaluate the performances on the timely basis (Richardson, 2017). The managers

of the organizations evaluate the performances and calculate variances so that the accountability

can be maintained within the organization.

31

4.1 Identify financial problems using indicators such as:

4.1.1 Benchmark: The benchmark means that the particular standards are set by the

organization from which the comparison is done and the financial performance of the

organization is evaluated. It also shows the reasons for the variance in the revenues and the cost

(Richardson, 2017).

4.1.2 Key Performance Indicator: It is the indicator to recognize that the organization is going

according to the accounting standards or not. These are the indicators through which weaknesses

can be evaluated. The KPI’s are both financial as well as non financial (Albu Consulting, 2017).

4.1.3 Budgetary targets to identify variances: These are the targets which are set by the

organization to evaluate the performances on the timely basis (Richardson, 2017). The managers

of the organizations evaluate the performances and calculate variances so that the accountability

can be maintained within the organization.

31

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4.2 Define financial governance and how these are used to prevent the financial problems.

How do we use it to monitor strategy.

The financial governance can be described as the set or rules which are set within the

organization so that the financial processes can be ensured (Lunkes, et. al., 2013). These will

help in preventing from the financial problems as it will help the managers of the organization

for taking the decisions according to the rules. The internal and the external auditing are done to

ensure the control in the organization. The auditing committee is set so that the performance of

the organization can be evaluated (Richardson, 2017).

They helps in monitoring the strategy as the budgetary reports are prepared so as to measure the

actual performance with the budgeted one. The strategic planning reports are also prepared so

that the planning for the future can be done. It will help in bringing the effectiveness in the

organization (Lunkes, et. al., 2013).

32

How do we use it to monitor strategy.

The financial governance can be described as the set or rules which are set within the

organization so that the financial processes can be ensured (Lunkes, et. al., 2013). These will

help in preventing from the financial problems as it will help the managers of the organization

for taking the decisions according to the rules. The internal and the external auditing are done to

ensure the control in the organization. The auditing committee is set so that the performance of

the organization can be evaluated (Richardson, 2017).

They helps in monitoring the strategy as the budgetary reports are prepared so as to measure the

actual performance with the budgeted one. The strategic planning reports are also prepared so

that the planning for the future can be done. It will help in bringing the effectiveness in the

organization (Lunkes, et. al., 2013).

32

4.3 Discuss characteristics of effective management accountant and how these are used to

solve problems.

The characteristics of the effective management accountants are:

Ability to work in team: The accountant must work with the team so that the quality of work

can be delivered and the task of the organization can be coordinated (Lunkes, et. al., 2013).

Knowledge of field: The manager should have the required skills of the field so that right skills

can be required for determining the proceeds of accounting.

Emphasizing Accuracy: The accuracy should be maintained so that risk in the organization can

be reduced and the accuracy can be maintained within the organization (Lunkes, et. al., 2013).

These skills will solve the problem as it will help in maintaing the accountability in the

organization and will also help the managers of the organization to increasing the productivity

within itself and the employees (Richardson, 2017).

33

solve problems.

The characteristics of the effective management accountants are:

Ability to work in team: The accountant must work with the team so that the quality of work

can be delivered and the task of the organization can be coordinated (Lunkes, et. al., 2013).

Knowledge of field: The manager should have the required skills of the field so that right skills

can be required for determining the proceeds of accounting.

Emphasizing Accuracy: The accuracy should be maintained so that risk in the organization can

be reduced and the accuracy can be maintained within the organization (Lunkes, et. al., 2013).

These skills will solve the problem as it will help in maintaing the accountability in the

organization and will also help the managers of the organization to increasing the productivity

within itself and the employees (Richardson, 2017).

33

4.4 Discuss the significance of developing strategies which requires effective and timely

reporting.

The significance of developing strategies are:

Customer Retention: The business strategies help in retaining the customers by designing those

strategies which are according to the needs of the customers (Root III, 2018). The customer

services programme should so be designed so that the customer can be retained.

Company Expansion: The business strategies also help in expanding the company by

promoting the new ideas and the frontiers which could help in expanding the business by

adopting the new technologies. The new business opportunity helps in inspiring the company’s

standards (Root III, 2018).

34

reporting.

The significance of developing strategies are:

Customer Retention: The business strategies help in retaining the customers by designing those

strategies which are according to the needs of the customers (Root III, 2018). The customer

services programme should so be designed so that the customer can be retained.

Company Expansion: The business strategies also help in expanding the company by

promoting the new ideas and the frontiers which could help in expanding the business by

adopting the new technologies. The new business opportunity helps in inspiring the company’s

standards (Root III, 2018).

34

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4.5 Analyze how in respond to financial problem management accounting can solve lead to

sustainable success (M4).

The management accounting can help in solving the financial problem as with the use of the

management accounting the performance of the organization can be evaluated and the

sustainable success can be achieved (Root III, 2018). The decisions of the organization should be

taken by including the risk factor so that the evaluation can be done. The companies should

indulge in themselves the risk management factors so that the financial performance of the

organization can be increased by solving the financial problem and the sustainability can be

attained (Root III, 2018).

35

sustainable success (M4).

The management accounting can help in solving the financial problem as with the use of the

management accounting the performance of the organization can be evaluated and the

sustainable success can be achieved (Root III, 2018). The decisions of the organization should be

taken by including the risk factor so that the evaluation can be done. The companies should

indulge in themselves the risk management factors so that the financial performance of the

organization can be increased by solving the financial problem and the sustainability can be

attained (Root III, 2018).

35

4.6 Evaluate how planning tools for accounting respond to solve financial problem to attain

the sustainable success. (D3)

The planning tools can also solve the financial performance as the financial statements are

prepared through which the areas of improvements can be evaluated and the sustainable success

can be achieved (Market Business, 2018). With this variance analysis is also one of the tool

through which the difference between the actual and the budgeted is calculated and this helps in

solving the financial problem so that the sustainability can be attained (Root III, 2018). These

planning tools also help in increasing the productivity as well as the accountability in the

organization.

36

the sustainable success. (D3)

The planning tools can also solve the financial performance as the financial statements are

prepared through which the areas of improvements can be evaluated and the sustainable success

can be achieved (Market Business, 2018). With this variance analysis is also one of the tool

through which the difference between the actual and the budgeted is calculated and this helps in

solving the financial problem so that the sustainability can be attained (Root III, 2018). These

planning tools also help in increasing the productivity as well as the accountability in the

organization.

36

Conclusion

From the above discussion it can be concluded that the management accounting is the process

through which the analysis of the financial statements are done so as to increase the profits of the

business. Various reports are prepared by the Zak Limited so that the cost can be controlled and

the revenues can be increased which in turn helps in increasing the productivity within the

organization. Budgets are prepared so that the actual results can be compared with the budgeted

one and the variances can be calculated so that the areas of improvement can be determined.

Beside this the reports also explains that how the management accounting and the planning tools

helps in solving the financial problem so that the sustainability can be attained and the

profitability can be increased.

37

From the above discussion it can be concluded that the management accounting is the process

through which the analysis of the financial statements are done so as to increase the profits of the

business. Various reports are prepared by the Zak Limited so that the cost can be controlled and

the revenues can be increased which in turn helps in increasing the productivity within the

organization. Budgets are prepared so that the actual results can be compared with the budgeted

one and the variances can be calculated so that the areas of improvement can be determined.