Management Accounting Problem (Case Study)

VerifiedAdded on 2023/03/23

|15

|2781

|42

AI Summary

This report discusses the use of job costing system in Connette's Limited and suggests the implementation of activity based costing to overcome its deficiencies. It also provides calculations for work in progress inventory, cost of chairs in finished goods inventory, and over applied or undersupplied overhead.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGEMENT ACCOUNTING PROBLEM

(CASE STUDY)

Page 1 of 15

(CASE STUDY)

Page 1 of 15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Executive Summary

This report is based on Connette's limited and application of job-based costing system for the

calculation of the cost of production. Job costing system is used by those business

organisations who undertake manufacturing process on the demand of their customers. In

other words, by those organisations in which various cost are incurred on the same product or

service. Closing stock of chairs amounts to $ 455,600 during the period and $ 92 is per unit

cost of chair i.e. one product line of Connette's limited. The undervalued overhead of

Connette's limited is $ 2,500, which means actual overhead is higher than the overhead

applied. Activity based costing is the better costing method that can be used by Conneotta’s

limited in order to curb the disadvantages of job costing method.

Page 2 of 15

This report is based on Connette's limited and application of job-based costing system for the

calculation of the cost of production. Job costing system is used by those business

organisations who undertake manufacturing process on the demand of their customers. In

other words, by those organisations in which various cost are incurred on the same product or

service. Closing stock of chairs amounts to $ 455,600 during the period and $ 92 is per unit

cost of chair i.e. one product line of Connette's limited. The undervalued overhead of

Connette's limited is $ 2,500, which means actual overhead is higher than the overhead

applied. Activity based costing is the better costing method that can be used by Conneotta’s

limited in order to curb the disadvantages of job costing method.

Page 2 of 15

Contents

Introduction................................................................................................................................4

Questions....................................................................................................................................5

1- Describe when it is appropriate for a company to use a job costing system.....................5

2- Calculate the balance in Conneotta’s work in progress inventory account as at 31

December...............................................................................................................................6

3- Calculate the cost of the chairs in finished goods inventory at 31st December................7

4- Actual manufacturing overhead incurred in December amounted to $ 252,000. Calculate

Conneotta’s over applied or undersupplied overhead for the year........................................7

5- Explain two alternative accounting treatments for over applied or under applied

overhead balance when using job costing system..................................................................8

6- Explain how activity based costing could overcome the deficiencies inherent in the

existing costing system..........................................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Appendix..................................................................................................................................12

Page 3 of 15

Introduction................................................................................................................................4

Questions....................................................................................................................................5

1- Describe when it is appropriate for a company to use a job costing system.....................5

2- Calculate the balance in Conneotta’s work in progress inventory account as at 31

December...............................................................................................................................6

3- Calculate the cost of the chairs in finished goods inventory at 31st December................7

4- Actual manufacturing overhead incurred in December amounted to $ 252,000. Calculate

Conneotta’s over applied or undersupplied overhead for the year........................................7

5- Explain two alternative accounting treatments for over applied or under applied

overhead balance when using job costing system..................................................................8

6- Explain how activity based costing could overcome the deficiencies inherent in the

existing costing system..........................................................................................................9

Conclusion................................................................................................................................10

References................................................................................................................................11

Appendix..................................................................................................................................12

Page 3 of 15

Introduction

Connette's Limited is a manufacturing business organisation using job costing method for the

identification and allocation of the various cost related to the manufacturing process. In this

report, different aspects of job costing method used by Conneotta’s Limited have been

discussed for the audiences. In this report, calculations related to the cost of finished goods

and work in progress has been reflected in this report. Treatment of overvaluation and

undervaluation has been discussed in this report. The last section contains an analysis of

activity based costing and its importance on the basis of its application in Conneotta’s

Limited.

Page 4 of 15

Connette's Limited is a manufacturing business organisation using job costing method for the

identification and allocation of the various cost related to the manufacturing process. In this

report, different aspects of job costing method used by Conneotta’s Limited have been

discussed for the audiences. In this report, calculations related to the cost of finished goods

and work in progress has been reflected in this report. Treatment of overvaluation and

undervaluation has been discussed in this report. The last section contains an analysis of

activity based costing and its importance on the basis of its application in Conneotta’s

Limited.

Page 4 of 15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Questions

1- Describe when it is appropriate for a company to use a job costing

system

Costing methods can be defined as the methods which are required to be used for

identification, allocation and applying different cost related to manufactured product.

Business operations of different business organisation are different from each other and

therefore their cost management (in terms of cost identification and allocation to product) are

different from each other. This arises the concept of different costing methods or costing

systems.

In order to arrive or decide the selling price of any product, the management of every

business organisation is required to calculate the total cost of the product (manufactured or

service provided). Job costing system is the method of calculating the cost of work done by

service or product provider on the request of service or product recipient. Under job costing

system cost of all related activities which are essential to develop a product or provide

services are added to arrive at a total cost of a particular job. In other words, it can be said

that the job costing system is used by those business organisation which are engaged in

providing customised services or customised manufacturing of the product (Braun, 2013).

Job costing method of costing is also used by those business organisations in which a

particular manufactured product has different cost or resources involved from other products.

Attributes of the manufactured product involve the cost of material used in manufacturing,

labour hours and different skill set of labours are involved, other direct cost related to

manufactured product and at last some portion of fixed cost is also added. In order to allocate

the fixed cost of manufacturing unit, there are some methods of cost allocation that are to be

followed by costing manager to arrive at a correct total cost of product or services (Wagner,

2015).

Page 5 of 15

1- Describe when it is appropriate for a company to use a job costing

system

Costing methods can be defined as the methods which are required to be used for

identification, allocation and applying different cost related to manufactured product.

Business operations of different business organisation are different from each other and

therefore their cost management (in terms of cost identification and allocation to product) are

different from each other. This arises the concept of different costing methods or costing

systems.

In order to arrive or decide the selling price of any product, the management of every

business organisation is required to calculate the total cost of the product (manufactured or

service provided). Job costing system is the method of calculating the cost of work done by

service or product provider on the request of service or product recipient. Under job costing

system cost of all related activities which are essential to develop a product or provide

services are added to arrive at a total cost of a particular job. In other words, it can be said

that the job costing system is used by those business organisation which are engaged in

providing customised services or customised manufacturing of the product (Braun, 2013).

Job costing method of costing is also used by those business organisations in which a

particular manufactured product has different cost or resources involved from other products.

Attributes of the manufactured product involve the cost of material used in manufacturing,

labour hours and different skill set of labours are involved, other direct cost related to

manufactured product and at last some portion of fixed cost is also added. In order to allocate

the fixed cost of manufacturing unit, there are some methods of cost allocation that are to be

followed by costing manager to arrive at a correct total cost of product or services (Wagner,

2015).

Page 5 of 15

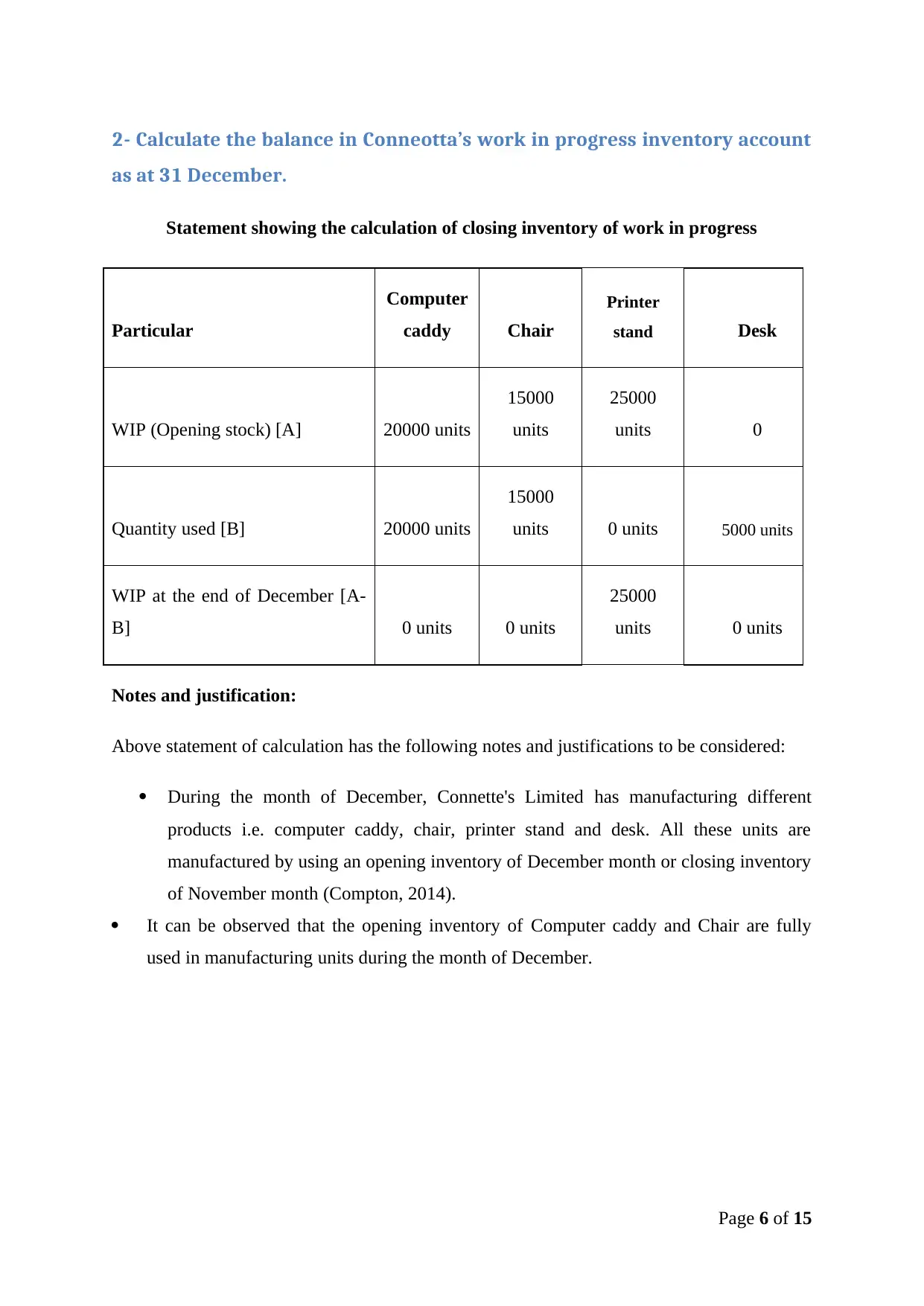

2- Calculate the balance in Conneotta’s work in progress inventory account

as at 31 December.

Statement showing the calculation of closing inventory of work in progress

Particular

Computer

caddy Chair

Printer

stand Desk

WIP (Opening stock) [A] 20000 units

15000

units

25000

units 0

Quantity used [B] 20000 units

15000

units 0 units 5000 units

WIP at the end of December [A-

B] 0 units 0 units

25000

units 0 units

Notes and justification:

Above statement of calculation has the following notes and justifications to be considered:

During the month of December, Connette's Limited has manufacturing different

products i.e. computer caddy, chair, printer stand and desk. All these units are

manufactured by using an opening inventory of December month or closing inventory

of November month (Compton, 2014).

It can be observed that the opening inventory of Computer caddy and Chair are fully

used in manufacturing units during the month of December.

Page 6 of 15

as at 31 December.

Statement showing the calculation of closing inventory of work in progress

Particular

Computer

caddy Chair

Printer

stand Desk

WIP (Opening stock) [A] 20000 units

15000

units

25000

units 0

Quantity used [B] 20000 units

15000

units 0 units 5000 units

WIP at the end of December [A-

B] 0 units 0 units

25000

units 0 units

Notes and justification:

Above statement of calculation has the following notes and justifications to be considered:

During the month of December, Connette's Limited has manufacturing different

products i.e. computer caddy, chair, printer stand and desk. All these units are

manufactured by using an opening inventory of December month or closing inventory

of November month (Compton, 2014).

It can be observed that the opening inventory of Computer caddy and Chair are fully

used in manufacturing units during the month of December.

Page 6 of 15

3- Calculate the cost of the chairs in finished goods inventory at 31st

December

Please see calculations in appendix

4- Actual manufacturing overhead incurred in December amounted to $

252,000. Calculate Conneotta’s over applied or undersupplied overhead for

the year

In every manufacturing business organisation issue related to charging manufacturing

overhead of the product for calculating the total cost. In this case, two concepts arise related

to the application of manufacturing overhead and they are under application of overhead and

over application of overhead. Over application is the situation under which manufacturing

overhead related to work in progress is charged higher than the actual manufacturing

overhead (Greenberg and Schneider, 2010). On the other hand, under application of overhead

is the situation under which manufacturing overheads are charged less as compared to actual

overhead for calculating the cost of production. In the present case, the following is the total

overhead applied by the management of Connette's Limited on 4 products:

Computer caddy = $ 60000

Chair = $ 22000

Printed stand = $ 97500

Desk = $ 70000

Total overhead applied = $ 249,500

Actual overhead incurred amounted to $ 252,000

Undervalued overhead = ($ 252,000 - $ 249,500) = $ 2,500

(Pleis, 2016)

Page 7 of 15

December

Please see calculations in appendix

4- Actual manufacturing overhead incurred in December amounted to $

252,000. Calculate Conneotta’s over applied or undersupplied overhead for

the year

In every manufacturing business organisation issue related to charging manufacturing

overhead of the product for calculating the total cost. In this case, two concepts arise related

to the application of manufacturing overhead and they are under application of overhead and

over application of overhead. Over application is the situation under which manufacturing

overhead related to work in progress is charged higher than the actual manufacturing

overhead (Greenberg and Schneider, 2010). On the other hand, under application of overhead

is the situation under which manufacturing overheads are charged less as compared to actual

overhead for calculating the cost of production. In the present case, the following is the total

overhead applied by the management of Connette's Limited on 4 products:

Computer caddy = $ 60000

Chair = $ 22000

Printed stand = $ 97500

Desk = $ 70000

Total overhead applied = $ 249,500

Actual overhead incurred amounted to $ 252,000

Undervalued overhead = ($ 252,000 - $ 249,500) = $ 2,500

(Pleis, 2016)

Page 7 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

On the other hand, it is given that the actual overhead incurred amounted to $ 252,000 in

December. Therefore, management of Connette's Limited has under applied their

manufacturing overhead

5- Explain two alternative accounting treatments for over applied or under

applied overhead balance when using job costing system

In the case of underapplied or overapplied manufacturing overheads, the business

organisation needs to charge the same over items of the cost schedule. Accounting treatment

of over applied or under applied overhead balance when using job costing system is

important because financial accounting and cost accounting is to be balanced. In other words,

to reconcile between financial and cost accounting different between actual overhead and

overhead charged is to be done (Mu, Jiang and Leng, 2017). There are 2 major methods that

can be used to charge under or overapplied overheads which the organisation uses. Therefore

the management of Connette's Limited can use either of the following two alternatives:

Using Income statement or profit & loss account:

1- Under this method, the management or financial manager of business organisations

charge the difference between actual and already charged overhead directly to the

profit and loss accounting of the year. In this case, overvalued or undervalued

manufacturing overhead will be directly charged to profit or loss of the business

organisation earned during the reporting period (Mu, Jiang and Leng, 2017).

2- Another method to charge overvalued and undervalued manufacturing overhead is to

charge the difference in work in progress, finished goods and cost of goods sold on a

proportionate basis. In other words, the amount charged to these accounts will be used

as a ratio or proportionate base to charge excess or less overhead during the period.

Page 8 of 15

December. Therefore, management of Connette's Limited has under applied their

manufacturing overhead

5- Explain two alternative accounting treatments for over applied or under

applied overhead balance when using job costing system

In the case of underapplied or overapplied manufacturing overheads, the business

organisation needs to charge the same over items of the cost schedule. Accounting treatment

of over applied or under applied overhead balance when using job costing system is

important because financial accounting and cost accounting is to be balanced. In other words,

to reconcile between financial and cost accounting different between actual overhead and

overhead charged is to be done (Mu, Jiang and Leng, 2017). There are 2 major methods that

can be used to charge under or overapplied overheads which the organisation uses. Therefore

the management of Connette's Limited can use either of the following two alternatives:

Using Income statement or profit & loss account:

1- Under this method, the management or financial manager of business organisations

charge the difference between actual and already charged overhead directly to the

profit and loss accounting of the year. In this case, overvalued or undervalued

manufacturing overhead will be directly charged to profit or loss of the business

organisation earned during the reporting period (Mu, Jiang and Leng, 2017).

2- Another method to charge overvalued and undervalued manufacturing overhead is to

charge the difference in work in progress, finished goods and cost of goods sold on a

proportionate basis. In other words, the amount charged to these accounts will be used

as a ratio or proportionate base to charge excess or less overhead during the period.

Page 8 of 15

6- Explain how activity based costing could overcome the deficiencies

inherent in the existing costing system

Activity costing system uses cost drivers i.e. on the basis of which cost is incurred as the base

for cost allocation during the period. In this costing system, actual cost related to different

products or different departments is calculated because the cost is divided on the basis of

resources used by the department or product. There are many resources like material, labour,

different machines and other resources are used in manufacturing products (Namazi, 2016).

Under activity costing method, use of these resources in the manufacturing process will

become the base of cost allocation. Therefore under this costing method, there is a question

of under application or over application of manufacturing overheads during the year.

Cost of product is primarily calculated on the basis of resources used in the manufacturing

process. Activity based costing is used to allocate the indirect cost of the business

organisation during the year (Oseifuah, 2014.). Activity costing method is totally different

from conventional methods of costing in terms of allocating the cost of the business

organisation i.e. it does not take into account cost incurred on the cost of sales, work in

progress and finished but they consider resources used in the manufacturing process.

In the present case of Connette's limited, activity based costing is considered to be the best

costing method for cost allocation of indirect resources used for manufacturing different

products. In the existing costing system, there is a deficiency of not valuing manufacturing

overheads accurately and during the end of the period, they need to make adjustments

(Warren, Moffitt and Byrnes, 2015). Therefore by using an activity based costing system,

they can effectively allocate their indirect cost by considering cost involve in using different

resources in the manufacturing process.

Page 9 of 15

inherent in the existing costing system

Activity costing system uses cost drivers i.e. on the basis of which cost is incurred as the base

for cost allocation during the period. In this costing system, actual cost related to different

products or different departments is calculated because the cost is divided on the basis of

resources used by the department or product. There are many resources like material, labour,

different machines and other resources are used in manufacturing products (Namazi, 2016).

Under activity costing method, use of these resources in the manufacturing process will

become the base of cost allocation. Therefore under this costing method, there is a question

of under application or over application of manufacturing overheads during the year.

Cost of product is primarily calculated on the basis of resources used in the manufacturing

process. Activity based costing is used to allocate the indirect cost of the business

organisation during the year (Oseifuah, 2014.). Activity costing method is totally different

from conventional methods of costing in terms of allocating the cost of the business

organisation i.e. it does not take into account cost incurred on the cost of sales, work in

progress and finished but they consider resources used in the manufacturing process.

In the present case of Connette's limited, activity based costing is considered to be the best

costing method for cost allocation of indirect resources used for manufacturing different

products. In the existing costing system, there is a deficiency of not valuing manufacturing

overheads accurately and during the end of the period, they need to make adjustments

(Warren, Moffitt and Byrnes, 2015). Therefore by using an activity based costing system,

they can effectively allocate their indirect cost by considering cost involve in using different

resources in the manufacturing process.

Page 9 of 15

Conclusion

From the above report, it can be concluded that job costing method is used by those business

organisation that are manufacturing products or providing services on demand of their

prospective customers. It can be concluded that job costing method has many flaws in terms

of its application while calculating and charging manufacturing overhead. Connette's limited

is the business organisation using job costing method and management have charged less

amount of manufacturing overhead i.e. under application of overhead. There are two methods

to charge underapplied overhead i.e. charge to profit or loss of the year or charge on a

proportionate basis to WIP, finished goods cost and cost of goods sold. It can be concluded

that activity based costing is the best costing method to charge overheads i.e. on the basis of

use of resources.

Page 10 of 15

From the above report, it can be concluded that job costing method is used by those business

organisation that are manufacturing products or providing services on demand of their

prospective customers. It can be concluded that job costing method has many flaws in terms

of its application while calculating and charging manufacturing overhead. Connette's limited

is the business organisation using job costing method and management have charged less

amount of manufacturing overhead i.e. under application of overhead. There are two methods

to charge underapplied overhead i.e. charge to profit or loss of the year or charge on a

proportionate basis to WIP, finished goods cost and cost of goods sold. It can be concluded

that activity based costing is the best costing method to charge overheads i.e. on the basis of

use of resources.

Page 10 of 15

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

Braun, Karen W. "Custom Fabric Ventures: An Instructional Resource in Job Costing for the

Introductory Managerial Accounting Course." Journal of Accounting Education 31.4 (2013):

400-29

Compton, Jim. "JOB CO$TING ON A BUDGET." Automotive Body Repair Network53.10

(2014): 24,26,28.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Greenberg, Rochelle K., and Schneider, Arnold. "Job Order Costing: A Simulation and

Vehicle for Conceptual Discussion.(Report)." Academy of Educational Leadership

Journal 14.3 (2010): 39-57.

Mu, H., Jiang, P. and Leng, J., 2017. Costing-based coordination between mt-iPSS customer

and providers for job shop production using game theory. International Journal of

Production Research, 55(2), pp.430-446.

Namazi, M., 2016. Time Driven Activity Based Costing: Theory, Applications, and

Limitations. Iranian Journal of Management Studies, 9(3), pp.457-482.

Oseifuah, E.K., 2014. Activity-based costing (ABC) in the public sector: Benefits and

challenges. Problems and Perspectives in Management, 12(4), pp.581-588.

Pleis, L.M., 2016. Cost Accounting: Linking Necessary Concepts. Business Education

Innovation Journal volume 8 number 2 December 2016, p.180.

Wagner, B., 2015. A report on the origins of Material Flow Cost Accounting (MFCA)

research activities. Journal of Cleaner Production, 108, pp.1255-1261.

Warren Jr, J.D., Moffitt, K.C. and Byrnes, P., 2015. How Big Data will change

accounting. Accounting Horizons, 29(2), pp.397-407.

Page 11 of 15

Braun, Karen W. "Custom Fabric Ventures: An Instructional Resource in Job Costing for the

Introductory Managerial Accounting Course." Journal of Accounting Education 31.4 (2013):

400-29

Compton, Jim. "JOB CO$TING ON A BUDGET." Automotive Body Repair Network53.10

(2014): 24,26,28.

Fisher, J.G. and Krumwiede, K., 2015. Product costing systems: Finding the right

approach. Journal of Corporate Accounting & Finance, 26(4), pp.13-21.

Greenberg, Rochelle K., and Schneider, Arnold. "Job Order Costing: A Simulation and

Vehicle for Conceptual Discussion.(Report)." Academy of Educational Leadership

Journal 14.3 (2010): 39-57.

Mu, H., Jiang, P. and Leng, J., 2017. Costing-based coordination between mt-iPSS customer

and providers for job shop production using game theory. International Journal of

Production Research, 55(2), pp.430-446.

Namazi, M., 2016. Time Driven Activity Based Costing: Theory, Applications, and

Limitations. Iranian Journal of Management Studies, 9(3), pp.457-482.

Oseifuah, E.K., 2014. Activity-based costing (ABC) in the public sector: Benefits and

challenges. Problems and Perspectives in Management, 12(4), pp.581-588.

Pleis, L.M., 2016. Cost Accounting: Linking Necessary Concepts. Business Education

Innovation Journal volume 8 number 2 December 2016, p.180.

Wagner, B., 2015. A report on the origins of Material Flow Cost Accounting (MFCA)

research activities. Journal of Cleaner Production, 108, pp.1255-1261.

Warren Jr, J.D., Moffitt, K.C. and Byrnes, P., 2015. How Big Data will change

accounting. Accounting Horizons, 29(2), pp.397-407.

Page 11 of 15

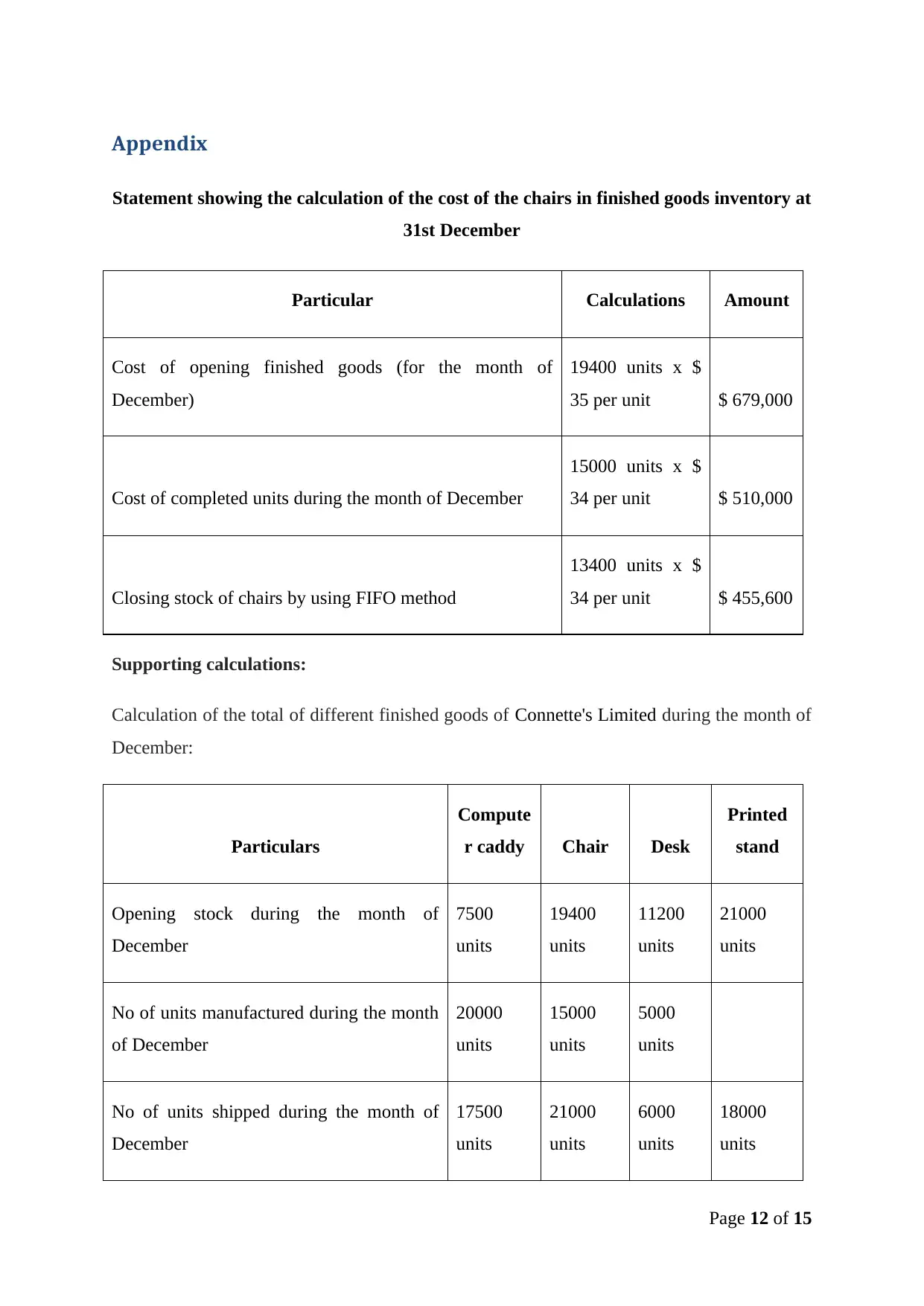

Appendix

Statement showing the calculation of the cost of the chairs in finished goods inventory at

31st December

Particular Calculations Amount

Cost of opening finished goods (for the month of

December)

19400 units x $

35 per unit $ 679,000

Cost of completed units during the month of December

15000 units x $

34 per unit $ 510,000

Closing stock of chairs by using FIFO method

13400 units x $

34 per unit $ 455,600

Supporting calculations:

Calculation of the total of different finished goods of Connette's Limited during the month of

December:

Particulars

Compute

r caddy Chair Desk

Printed

stand

Opening stock during the month of

December

7500

units

19400

units

11200

units

21000

units

No of units manufactured during the month

of December

20000

units

15000

units

5000

units

No of units shipped during the month of

December

17500

units

21000

units

6000

units

18000

units

Page 12 of 15

Statement showing the calculation of the cost of the chairs in finished goods inventory at

31st December

Particular Calculations Amount

Cost of opening finished goods (for the month of

December)

19400 units x $

35 per unit $ 679,000

Cost of completed units during the month of December

15000 units x $

34 per unit $ 510,000

Closing stock of chairs by using FIFO method

13400 units x $

34 per unit $ 455,600

Supporting calculations:

Calculation of the total of different finished goods of Connette's Limited during the month of

December:

Particulars

Compute

r caddy Chair Desk

Printed

stand

Opening stock during the month of

December

7500

units

19400

units

11200

units

21000

units

No of units manufactured during the month

of December

20000

units

15000

units

5000

units

No of units shipped during the month of

December

17500

units

21000

units

6000

units

18000

units

Page 12 of 15

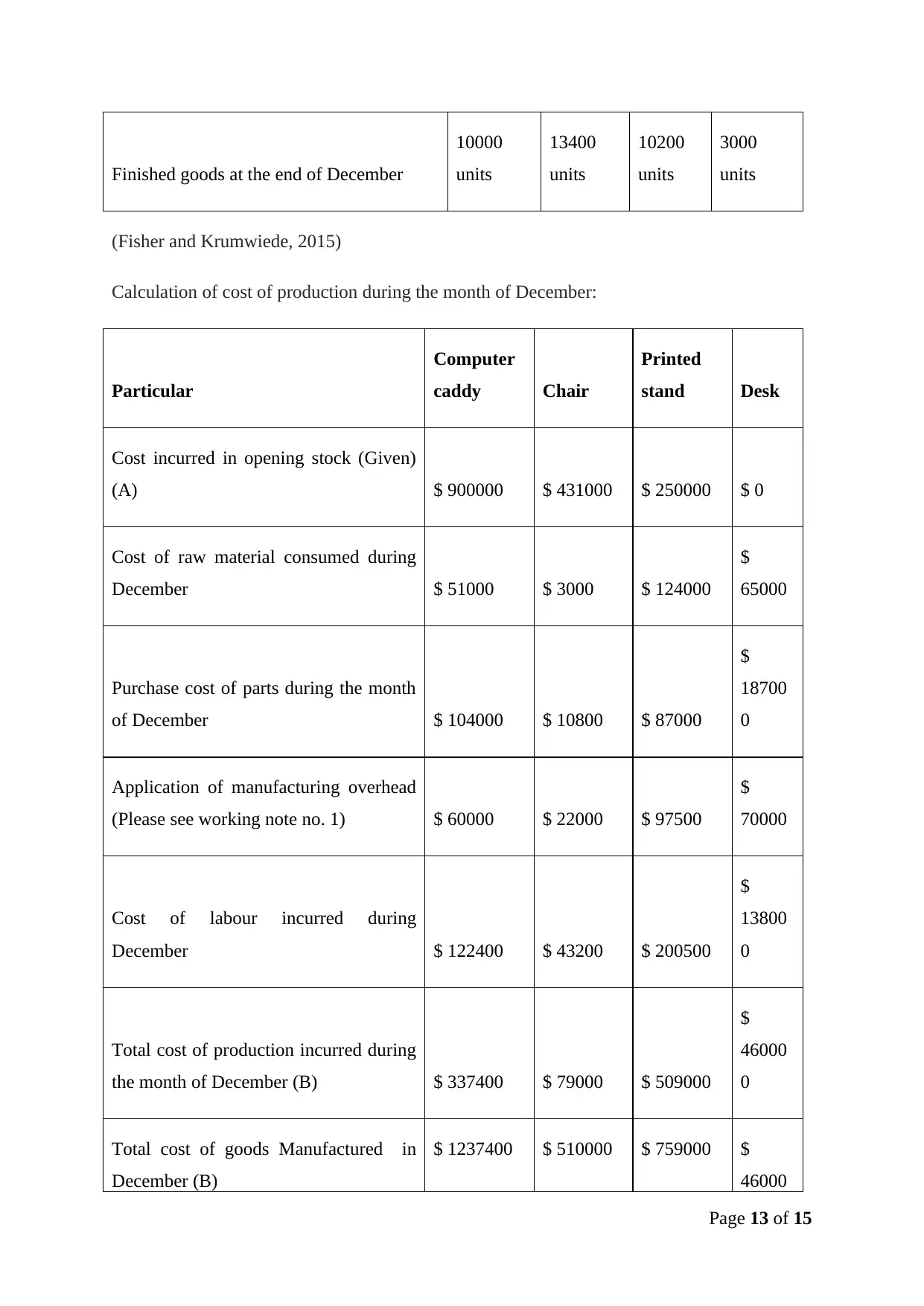

Finished goods at the end of December

10000

units

13400

units

10200

units

3000

units

(Fisher and Krumwiede, 2015)

Calculation of cost of production during the month of December:

Particular

Computer

caddy Chair

Printed

stand Desk

Cost incurred in opening stock (Given)

(A) $ 900000 $ 431000 $ 250000 $ 0

Cost of raw material consumed during

December $ 51000 $ 3000 $ 124000

$

65000

Purchase cost of parts during the month

of December $ 104000 $ 10800 $ 87000

$

18700

0

Application of manufacturing overhead

(Please see working note no. 1) $ 60000 $ 22000 $ 97500

$

70000

Cost of labour incurred during

December $ 122400 $ 43200 $ 200500

$

13800

0

Total cost of production incurred during

the month of December (B) $ 337400 $ 79000 $ 509000

$

46000

0

Total cost of goods Manufactured in

December (B)

$ 1237400 $ 510000 $ 759000 $

46000

Page 13 of 15

10000

units

13400

units

10200

units

3000

units

(Fisher and Krumwiede, 2015)

Calculation of cost of production during the month of December:

Particular

Computer

caddy Chair

Printed

stand Desk

Cost incurred in opening stock (Given)

(A) $ 900000 $ 431000 $ 250000 $ 0

Cost of raw material consumed during

December $ 51000 $ 3000 $ 124000

$

65000

Purchase cost of parts during the month

of December $ 104000 $ 10800 $ 87000

$

18700

0

Application of manufacturing overhead

(Please see working note no. 1) $ 60000 $ 22000 $ 97500

$

70000

Cost of labour incurred during

December $ 122400 $ 43200 $ 200500

$

13800

0

Total cost of production incurred during

the month of December (B) $ 337400 $ 79000 $ 509000

$

46000

0

Total cost of goods Manufactured in

December (B)

$ 1237400 $ 510000 $ 759000 $

46000

Page 13 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

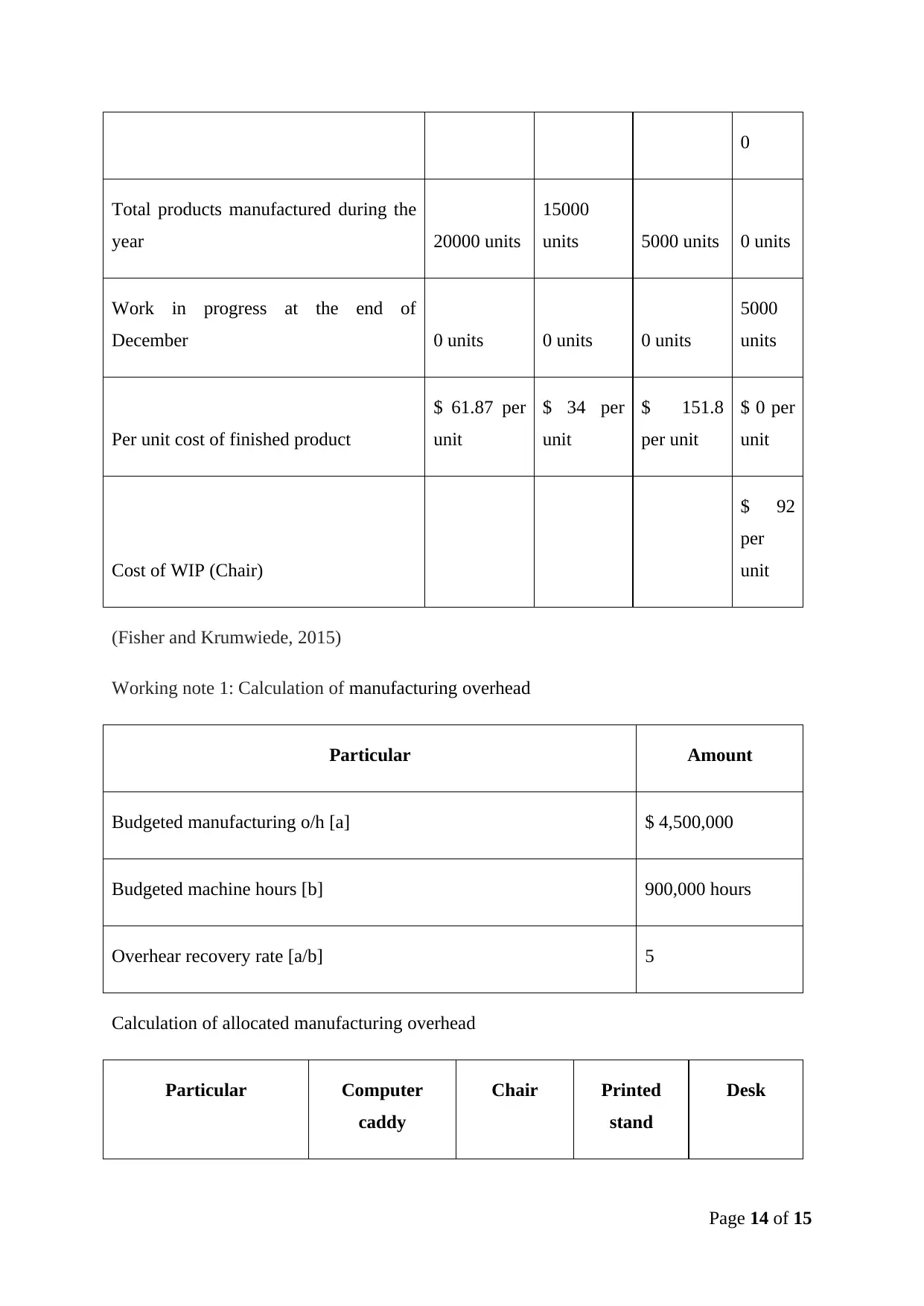

0

Total products manufactured during the

year 20000 units

15000

units 5000 units 0 units

Work in progress at the end of

December 0 units 0 units 0 units

5000

units

Per unit cost of finished product

$ 61.87 per

unit

$ 34 per

unit

$ 151.8

per unit

$ 0 per

unit

Cost of WIP (Chair)

$ 92

per

unit

(Fisher and Krumwiede, 2015)

Working note 1: Calculation of manufacturing overhead

Particular Amount

Budgeted manufacturing o/h [a] $ 4,500,000

Budgeted machine hours [b] 900,000 hours

Overhear recovery rate [a/b] 5

Calculation of allocated manufacturing overhead

Particular Computer

caddy

Chair Printed

stand

Desk

Page 14 of 15

Total products manufactured during the

year 20000 units

15000

units 5000 units 0 units

Work in progress at the end of

December 0 units 0 units 0 units

5000

units

Per unit cost of finished product

$ 61.87 per

unit

$ 34 per

unit

$ 151.8

per unit

$ 0 per

unit

Cost of WIP (Chair)

$ 92

per

unit

(Fisher and Krumwiede, 2015)

Working note 1: Calculation of manufacturing overhead

Particular Amount

Budgeted manufacturing o/h [a] $ 4,500,000

Budgeted machine hours [b] 900,000 hours

Overhear recovery rate [a/b] 5

Calculation of allocated manufacturing overhead

Particular Computer

caddy

Chair Printed

stand

Desk

Page 14 of 15

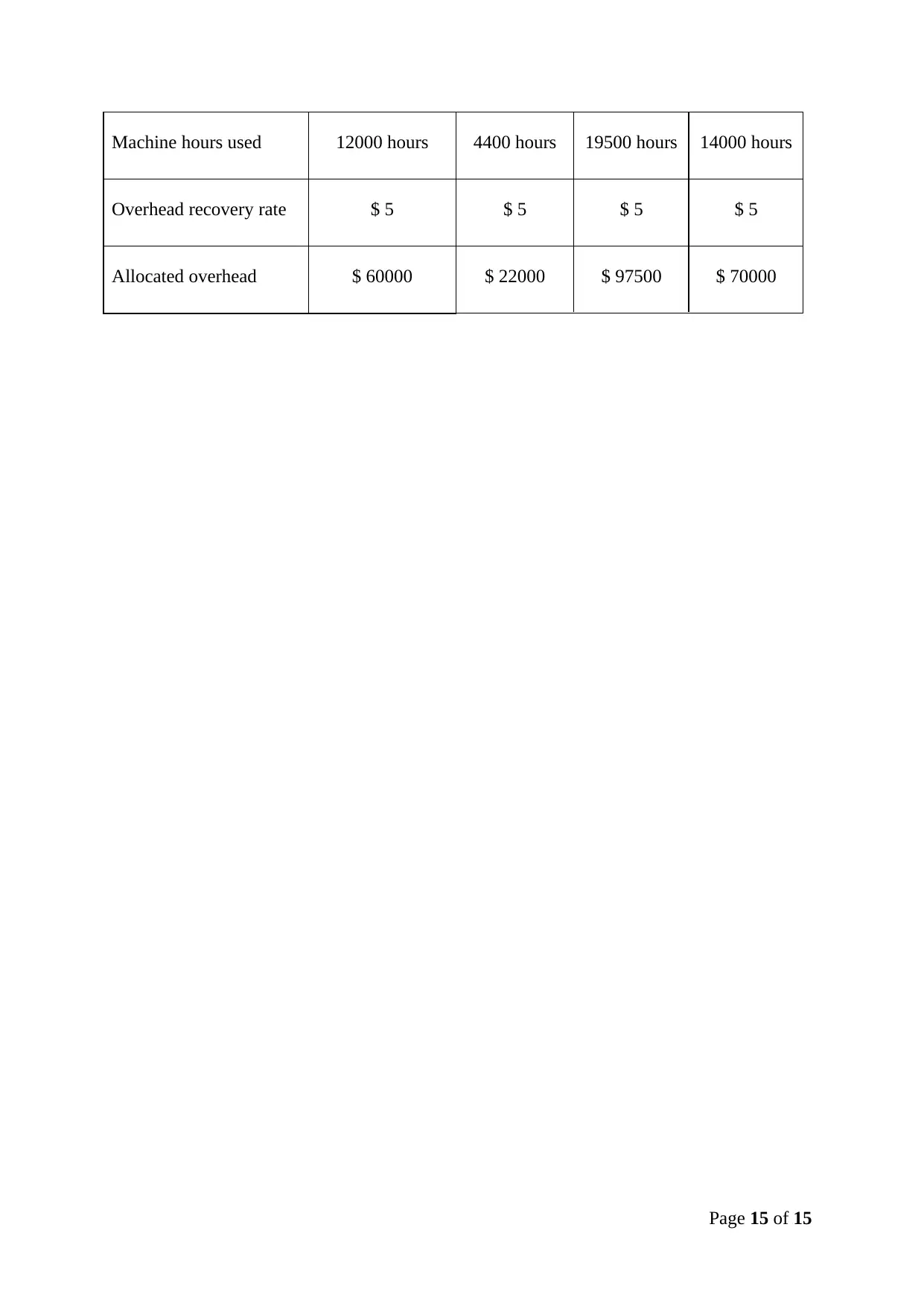

Machine hours used 12000 hours 4400 hours 19500 hours 14000 hours

Overhead recovery rate $ 5 $ 5 $ 5 $ 5

Allocated overhead $ 60000 $ 22000 $ 97500 $ 70000

Page 15 of 15

Overhead recovery rate $ 5 $ 5 $ 5 $ 5

Allocated overhead $ 60000 $ 22000 $ 97500 $ 70000

Page 15 of 15

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.