HA2011 Management Accounting Assignment Solution, Holmes Institute

VerifiedAdded on 2022/11/01

|17

|4423

|351

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Management Accounting assignment, focusing on cost concepts and value chain analysis. The assignment explores the value chain concept, evaluating its application within the Treasury Wine Estate Company, including its mission, objectives, competitive strategies, and value-adding processes. It delves into cost allocation, including calculating predicted allocation rates for fixed and variable overhead, determining total overhead and total costs for a specific job, and selecting appropriate cost pools and drivers. The analysis considers three cost objects, identifying cost pools and drivers, and calculating allocation rates. The solution incorporates tables and figures to illustrate calculations and concepts, providing a detailed examination of cost accounting principles and their practical application in a business context.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................3

Question 1........................................................................................................................................4

A: Value Chain Concept..............................................................................................................4

B: Evaluation of value chain concept of Treasury Wine Estate Company..................................4

Question 2........................................................................................................................................9

Computation of the predicted allocation rates for fixed and variable overhead for the current

period...........................................................................................................................................9

Computation of total overhead cost allocated to Job 20 in October..........................................10

Computation of total cost of Job 20...........................................................................................10

Computation of amounts of fixed and variable overhead allocated to jobs in October............11

Selection of the two cost pool instead of one............................................................................11

Question 3......................................................................................................................................11

By consideration of the three cost objects of interest, identification of the cost pool and

computation of cost....................................................................................................................11

Ascertainment of the cost driver for each cost pool..................................................................12

Calculation of the allocation rate for cost pool and cost driver.................................................13

Conclusion.....................................................................................................................................13

References......................................................................................................................................15

Introduction......................................................................................................................................3

Question 1........................................................................................................................................4

A: Value Chain Concept..............................................................................................................4

B: Evaluation of value chain concept of Treasury Wine Estate Company..................................4

Question 2........................................................................................................................................9

Computation of the predicted allocation rates for fixed and variable overhead for the current

period...........................................................................................................................................9

Computation of total overhead cost allocated to Job 20 in October..........................................10

Computation of total cost of Job 20...........................................................................................10

Computation of amounts of fixed and variable overhead allocated to jobs in October............11

Selection of the two cost pool instead of one............................................................................11

Question 3......................................................................................................................................11

By consideration of the three cost objects of interest, identification of the cost pool and

computation of cost....................................................................................................................11

Ascertainment of the cost driver for each cost pool..................................................................12

Calculation of the allocation rate for cost pool and cost driver.................................................13

Conclusion.....................................................................................................................................13

References......................................................................................................................................15

List of Tables

Table 1 calculation of the allocation rate for predicted variable and fixed expenses......................9

Table 2 Statement of the allocation rate........................................................................................10

Table 3 Computation of total overhead cost for Job 20.................................................................10

Table 4 Computation of total cost for Job 20...............................................................................10

Table 5 Computation of the Fixed and variable cost for the job...................................................11

Table 6 Statement showing assignment of the cost.......................................................................12

Table 7 Statement of the cost pool and cost driver........................................................................13

INTRODUCTION

Value chain analysis can be referred as a method through which an organization can analyze its

operations to assess the way through which it can create competitive advantage for itself. The

concept of value chain support management to understand the manner in which each activity

adds value to something and consequently the manner in which it can provide products to its

customer for more than cost of adding value which will eventually generate profit for the

company. Company can apply the value chain technique for creation of the value to its

consumers by the means of designing, advertisement and sales promotion, production and

manner other method. The present study is related with the value chain concept and the benefits

to the company by the implication of the value chain model in the organization. Further, in the

given study, company named as Treasury Wine Estate Company, mission, vision, strategy, value

chain model, value adding process and other aspects are also described. Along with this,

allocation of the cost to the product by identification of the cost driver and cost pool are also

evaluated in the given report.

Table 1 calculation of the allocation rate for predicted variable and fixed expenses......................9

Table 2 Statement of the allocation rate........................................................................................10

Table 3 Computation of total overhead cost for Job 20.................................................................10

Table 4 Computation of total cost for Job 20...............................................................................10

Table 5 Computation of the Fixed and variable cost for the job...................................................11

Table 6 Statement showing assignment of the cost.......................................................................12

Table 7 Statement of the cost pool and cost driver........................................................................13

INTRODUCTION

Value chain analysis can be referred as a method through which an organization can analyze its

operations to assess the way through which it can create competitive advantage for itself. The

concept of value chain support management to understand the manner in which each activity

adds value to something and consequently the manner in which it can provide products to its

customer for more than cost of adding value which will eventually generate profit for the

company. Company can apply the value chain technique for creation of the value to its

consumers by the means of designing, advertisement and sales promotion, production and

manner other method. The present study is related with the value chain concept and the benefits

to the company by the implication of the value chain model in the organization. Further, in the

given study, company named as Treasury Wine Estate Company, mission, vision, strategy, value

chain model, value adding process and other aspects are also described. Along with this,

allocation of the cost to the product by identification of the cost driver and cost pool are also

evaluated in the given report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

A: Value Chain Concept

Value chain concept

Value chain approach comprises activities conducted by organization in order to create value for

its customers such as designing, manufacturing, advertising, packaging etc. Business operations

are conducted for providing goods and services to customers in required manner. The process

begins with raw material by which products are made and include all the things that is required

before delivering it to customers (Donovan, etal, 2015). The process of value chain management

is connected with the activities of organization for analyzing them in a proper way. The major

objective is to build connection with the leaders at every level to make sure those products are

delivered to the consumers flawlessly (Simatupang, Piboonrungroj, and Williams, 2017).

Importance of value chain management in organization

Effective value chain management helps to get better skills to track, capture and organize

consumers as well as organization needs for analyzing the activities such as planning,

manufacturing, design and services for proper cost valuation besides with complete traceability.

It helps in managing research, planning and development in effective manner. For meeting the

demand of the customers VCM carry measurable and constant process by which product master

data is managed in proper way. Furthermore it helps to improve the management of vendors in

better way. Moreover its helps to reduce the costs of business, provides supports and post sales

services and besides all it improves the profitability of the company (Simatupang, Ginardy, and

Handayati, 2018).

B: Evaluation of value chain concept of Treasury Wine Estate Company

Mission and objectives of the company

The main objective of Treasury Wine Estate Company is to become world’s most famous wine

company. They are very much passionate about the wine. They eagerly work for their vision.

There are operating more than 14000 hectares of vineyards and managing approx 70 wine brands

moreover no of workers employed in the company are 3400. They deal in the most popular

wines that come from Italy, Australia, New Zealand and California (Lapsley, Alston, and

Sambucci, 2019). Brands with which they are dealing are Wolf Blass, Bringer, Beaulieu

A: Value Chain Concept

Value chain concept

Value chain approach comprises activities conducted by organization in order to create value for

its customers such as designing, manufacturing, advertising, packaging etc. Business operations

are conducted for providing goods and services to customers in required manner. The process

begins with raw material by which products are made and include all the things that is required

before delivering it to customers (Donovan, etal, 2015). The process of value chain management

is connected with the activities of organization for analyzing them in a proper way. The major

objective is to build connection with the leaders at every level to make sure those products are

delivered to the consumers flawlessly (Simatupang, Piboonrungroj, and Williams, 2017).

Importance of value chain management in organization

Effective value chain management helps to get better skills to track, capture and organize

consumers as well as organization needs for analyzing the activities such as planning,

manufacturing, design and services for proper cost valuation besides with complete traceability.

It helps in managing research, planning and development in effective manner. For meeting the

demand of the customers VCM carry measurable and constant process by which product master

data is managed in proper way. Furthermore it helps to improve the management of vendors in

better way. Moreover its helps to reduce the costs of business, provides supports and post sales

services and besides all it improves the profitability of the company (Simatupang, Ginardy, and

Handayati, 2018).

B: Evaluation of value chain concept of Treasury Wine Estate Company

Mission and objectives of the company

The main objective of Treasury Wine Estate Company is to become world’s most famous wine

company. They are very much passionate about the wine. They eagerly work for their vision.

There are operating more than 14000 hectares of vineyards and managing approx 70 wine brands

moreover no of workers employed in the company are 3400. They deal in the most popular

wines that come from Italy, Australia, New Zealand and California (Lapsley, Alston, and

Sambucci, 2019). Brands with which they are dealing are Wolf Blass, Bringer, Beaulieu

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Vineyard, Stags' Leap, Penfolds, Lindeman's, Sterling Vineyards, Wynns Coonawarra Estate, 19

Crimes, Castello di Gabbiano and Chateau St. Jean. There various career opportunities for the

people in the company (Alves, Fernandes, and Raposo, 2016.).

Mission: The mission of company is to get popular in the whole world and want be get success

worldwide. They want to be a source of achievement of their society and want to develop greater

career opportunities for their workers. They want to direct their partners into profitability, in

returns for their proprietors and make their consumers enjoy its services.

Competitive strategies

For surviving in the competitive world it is important for the Treasury Wine Estates Limited to

make clear basis for differentiation that help to stay confidently next to their rivals. Thus, in

order to sustain its position the competitive strategy followed by company is concentrating on

unique selling propositions (USPs).USPs has features like lowest cost, highest quality, and

exclusive idea. It is not enough to just recognize the USPs because the efficiency of the

competitive strategy of company will completely based in the capability of management to

converse the recognized unique selling propositions (Yanzheng, Zengxiang,. and Changhong,

2015). Thus, Porter's generic strategies model can be applied by the Treasury Wine Estates

Limited to search how competitive advantage can be made.

Crimes, Castello di Gabbiano and Chateau St. Jean. There various career opportunities for the

people in the company (Alves, Fernandes, and Raposo, 2016.).

Mission: The mission of company is to get popular in the whole world and want be get success

worldwide. They want to be a source of achievement of their society and want to develop greater

career opportunities for their workers. They want to direct their partners into profitability, in

returns for their proprietors and make their consumers enjoy its services.

Competitive strategies

For surviving in the competitive world it is important for the Treasury Wine Estates Limited to

make clear basis for differentiation that help to stay confidently next to their rivals. Thus, in

order to sustain its position the competitive strategy followed by company is concentrating on

unique selling propositions (USPs).USPs has features like lowest cost, highest quality, and

exclusive idea. It is not enough to just recognize the USPs because the efficiency of the

competitive strategy of company will completely based in the capability of management to

converse the recognized unique selling propositions (Yanzheng, Zengxiang,. and Changhong,

2015). Thus, Porter's generic strategies model can be applied by the Treasury Wine Estates

Limited to search how competitive advantage can be made.

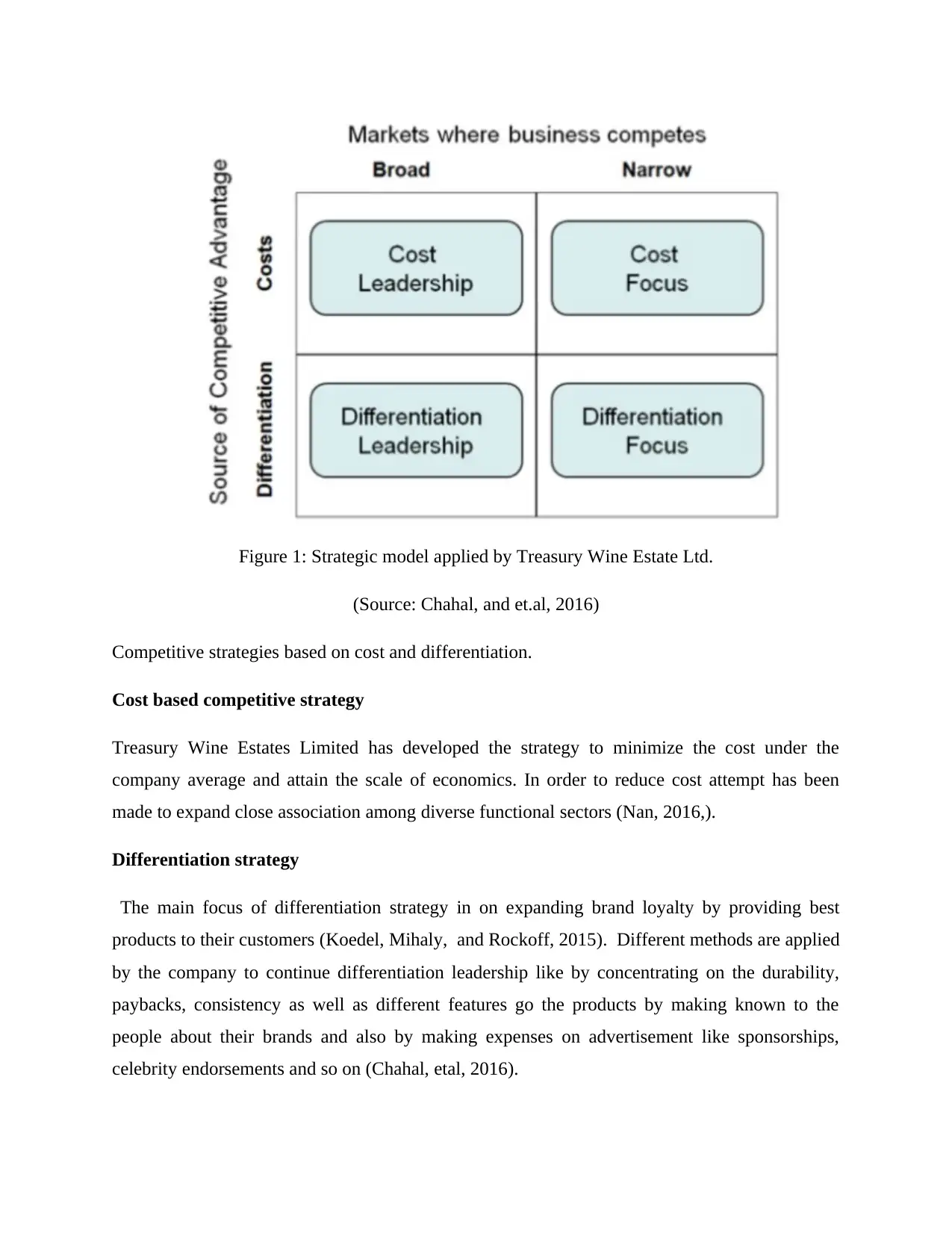

Figure 1: Strategic model applied by Treasury Wine Estate Ltd.

(Source: Chahal, and et.al, 2016)

Competitive strategies based on cost and differentiation.

Cost based competitive strategy

Treasury Wine Estates Limited has developed the strategy to minimize the cost under the

company average and attain the scale of economics. In order to reduce cost attempt has been

made to expand close association among diverse functional sectors (Nan, 2016,).

Differentiation strategy

The main focus of differentiation strategy in on expanding brand loyalty by providing best

products to their customers (Koedel, Mihaly, and Rockoff, 2015). Different methods are applied

by the company to continue differentiation leadership like by concentrating on the durability,

paybacks, consistency as well as different features go the products by making known to the

people about their brands and also by making expenses on advertisement like sponsorships,

celebrity endorsements and so on (Chahal, etal, 2016).

(Source: Chahal, and et.al, 2016)

Competitive strategies based on cost and differentiation.

Cost based competitive strategy

Treasury Wine Estates Limited has developed the strategy to minimize the cost under the

company average and attain the scale of economics. In order to reduce cost attempt has been

made to expand close association among diverse functional sectors (Nan, 2016,).

Differentiation strategy

The main focus of differentiation strategy in on expanding brand loyalty by providing best

products to their customers (Koedel, Mihaly, and Rockoff, 2015). Different methods are applied

by the company to continue differentiation leadership like by concentrating on the durability,

paybacks, consistency as well as different features go the products by making known to the

people about their brands and also by making expenses on advertisement like sponsorships,

celebrity endorsements and so on (Chahal, etal, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Treasuries Wine Estates Limited can plan to achieve competitive advantage by accepting image,

quality, product, service, and modernism differentiation (Horng, Chang, and Chen, 2016.).

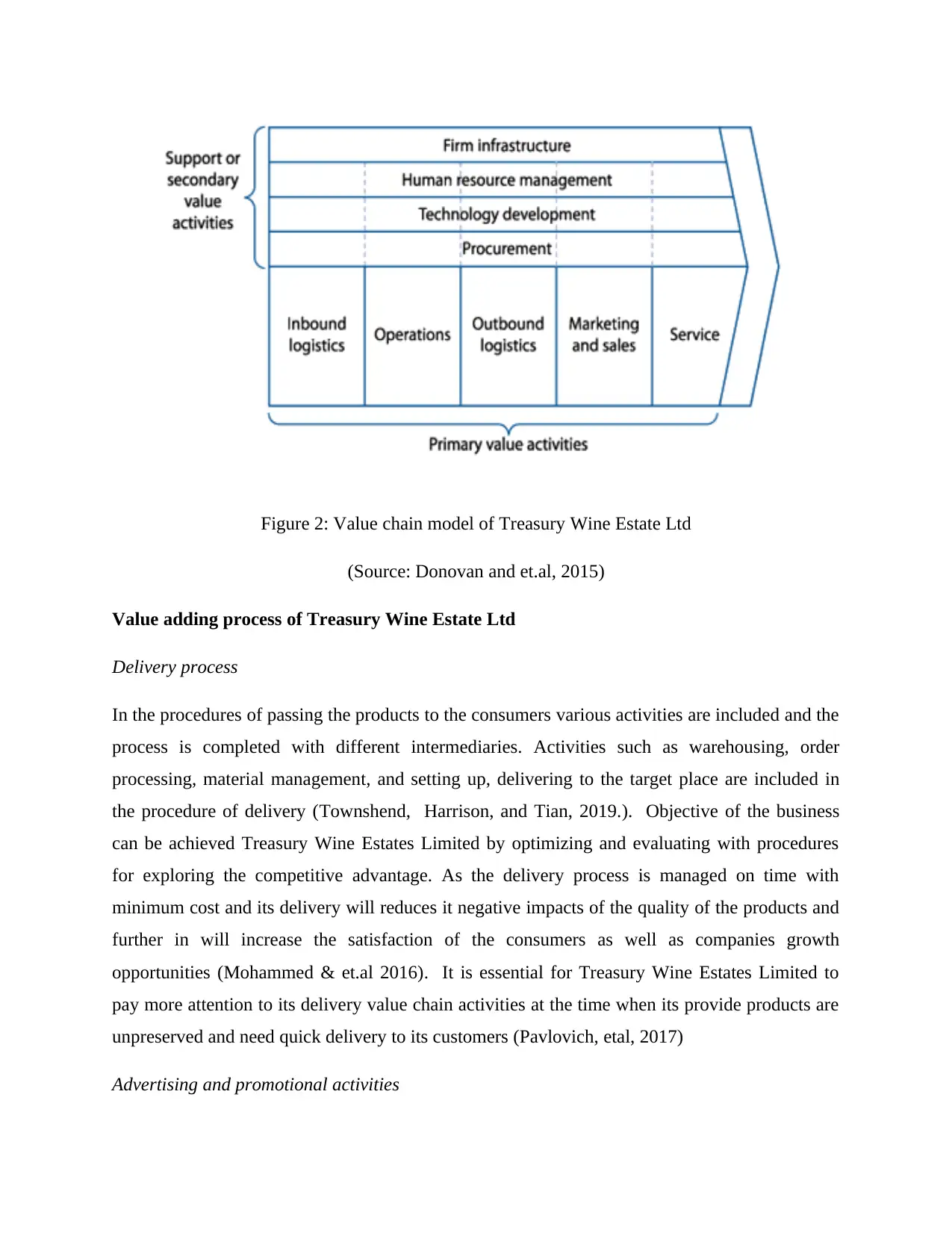

Value chain model of Treasury Wine Estate Company

By the present model it is clearly identified that how Treasury Wine Estates Limited comply

with effective competitive strategy by analyzing its products, abilities, resources as well as

recognizing variants of external environment. This model assists the company to identify the

manner in which it can generate the profit (Krishnan, 2015). In the present study, the Treasury

Wine Estate Company implements the value chain model. The company creates the value by

obtaining the raw material and implements them in the production process in a innovative and

better manner. There are chain of activities, which helps the company to build the value. These

activities are bifurcated into the primary activity and supportive activity. The primary activity of

the business is consisting of Inbound logistic, Operations, Outbound logistics, Marketing and

sales, and Services. It is the activity which is connected directly with sale, maintenance, physical

creation of the product or services.

The secondary activity helps the primary activity, which includes Human resource management,

infrastructure, purchasing, and technological development (García-Sánchez, and Noguera-

Gámez, 2017). Treasury Wine Estate Company apply the primary and supportive activity for the

creation of the value. Activities relating to flow of material are part of primary activities. The

activities relating to supply of material are efficient in case of Treasury Wine Estate Company

but the procedure relating to trans-shipping of wine for bottling is considered as non-value

adding activity as it leads to excessive motion as well as double handling. Moreover, the

approach followed by the company for merchandising, setting promotion slots, develops

significant uncertainty relating to forecasting of sales which leads to developing waste and loss

of value upstream. The activities relating to information flow are relating to secondary activities

as they provide support in delivering the product or service in required manner to the customer.

In case of Treasury Wine Estate Company, a clear correlation exists within the relationships and

information flows. However, loopholes have been assessed in downstream partners and

secondary players which can be referred as logistics providers. Thus, in order to resolve the same

it is necessary to develop understanding between upstream executives and secondary players.

quality, product, service, and modernism differentiation (Horng, Chang, and Chen, 2016.).

Value chain model of Treasury Wine Estate Company

By the present model it is clearly identified that how Treasury Wine Estates Limited comply

with effective competitive strategy by analyzing its products, abilities, resources as well as

recognizing variants of external environment. This model assists the company to identify the

manner in which it can generate the profit (Krishnan, 2015). In the present study, the Treasury

Wine Estate Company implements the value chain model. The company creates the value by

obtaining the raw material and implements them in the production process in a innovative and

better manner. There are chain of activities, which helps the company to build the value. These

activities are bifurcated into the primary activity and supportive activity. The primary activity of

the business is consisting of Inbound logistic, Operations, Outbound logistics, Marketing and

sales, and Services. It is the activity which is connected directly with sale, maintenance, physical

creation of the product or services.

The secondary activity helps the primary activity, which includes Human resource management,

infrastructure, purchasing, and technological development (García-Sánchez, and Noguera-

Gámez, 2017). Treasury Wine Estate Company apply the primary and supportive activity for the

creation of the value. Activities relating to flow of material are part of primary activities. The

activities relating to supply of material are efficient in case of Treasury Wine Estate Company

but the procedure relating to trans-shipping of wine for bottling is considered as non-value

adding activity as it leads to excessive motion as well as double handling. Moreover, the

approach followed by the company for merchandising, setting promotion slots, develops

significant uncertainty relating to forecasting of sales which leads to developing waste and loss

of value upstream. The activities relating to information flow are relating to secondary activities

as they provide support in delivering the product or service in required manner to the customer.

In case of Treasury Wine Estate Company, a clear correlation exists within the relationships and

information flows. However, loopholes have been assessed in downstream partners and

secondary players which can be referred as logistics providers. Thus, in order to resolve the same

it is necessary to develop understanding between upstream executives and secondary players.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Figure 2: Value chain model of Treasury Wine Estate Ltd

(Source: Donovan and et.al, 2015)

Value adding process of Treasury Wine Estate Ltd

Delivery process

In the procedures of passing the products to the consumers various activities are included and the

process is completed with different intermediaries. Activities such as warehousing, order

processing, material management, and setting up, delivering to the target place are included in

the procedure of delivery (Townshend, Harrison, and Tian, 2019.). Objective of the business

can be achieved Treasury Wine Estates Limited by optimizing and evaluating with procedures

for exploring the competitive advantage. As the delivery process is managed on time with

minimum cost and its delivery will reduces it negative impacts of the quality of the products and

further in will increase the satisfaction of the consumers as well as companies growth

opportunities (Mohammed & et.al 2016). It is essential for Treasury Wine Estates Limited to

pay more attention to its delivery value chain activities at the time when its provide products are

unpreserved and need quick delivery to its customers (Pavlovich, etal, 2017)

Advertising and promotional activities

(Source: Donovan and et.al, 2015)

Value adding process of Treasury Wine Estate Ltd

Delivery process

In the procedures of passing the products to the consumers various activities are included and the

process is completed with different intermediaries. Activities such as warehousing, order

processing, material management, and setting up, delivering to the target place are included in

the procedure of delivery (Townshend, Harrison, and Tian, 2019.). Objective of the business

can be achieved Treasury Wine Estates Limited by optimizing and evaluating with procedures

for exploring the competitive advantage. As the delivery process is managed on time with

minimum cost and its delivery will reduces it negative impacts of the quality of the products and

further in will increase the satisfaction of the consumers as well as companies growth

opportunities (Mohammed & et.al 2016). It is essential for Treasury Wine Estates Limited to

pay more attention to its delivery value chain activities at the time when its provide products are

unpreserved and need quick delivery to its customers (Pavlovich, etal, 2017)

Advertising and promotional activities

Another procedure that is considered is advertising and promotional process. Strategies of

marketing can be change according to the nature. It is completely based on the company’s brand

image, goals, present position, and competitive dynamics in the marketplace (Seccia, Santeramo,

and Nardone, 2016). Furthermore brand equity of Treasury Wine Estates Limited can be

successfully and sensible incorporated activities of promotion and marketing and which further

makes then stand in the situation of competition (Bragg, 2016). On the other hand company

should not make any false commitments regarding the features of its product which effect the

position of the company. It specifies the requirement to assure coordination among different

activities of value chain (Goncharuk, and Lazareva, 2017).

Relevance and usefulness of the information

It can be accessed from above analysis that value chain analysis provides systematic review of

transformation process relating to input and output at each distinctive stages. Further, the concept

can be applied to develop organization sustainable competitive advantage. It has been accessed

that value chain is linked with activities relating to conversion of input into final product or

service (Lu, Sridharan, and Tse, 2016). An organization is able to emphasize on value adding

activities through application of value chain analysis. Further, inbound logistic activities assist in

analyzing the relationship with suppliers along with activities relating to storing and

disseminating of inputs. Thus, an organization could ascertain the loop holes and make efficient

attempt to reduce the influence of same (Pangemanan, and Ramintang, 2016).

Question 2

QUESTION 2

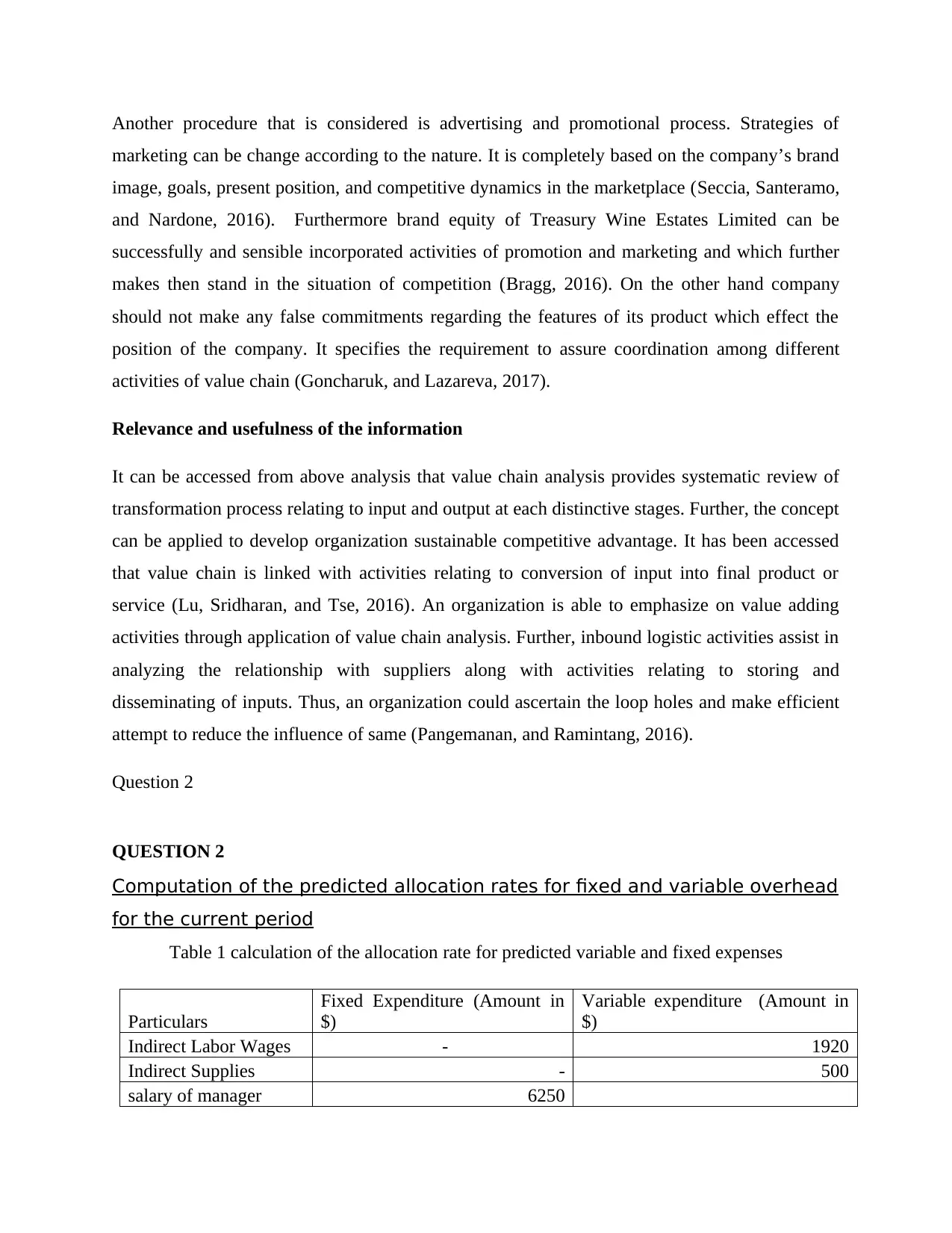

Computation of the predicted allocation rates for fixed and variable overhead

for the current period

Table 1 calculation of the allocation rate for predicted variable and fixed expenses

Particulars

Fixed Expenditure (Amount in

$)

Variable expenditure (Amount in

$)

Indirect Labor Wages - 1920

Indirect Supplies - 500

salary of manager 6250

marketing can be change according to the nature. It is completely based on the company’s brand

image, goals, present position, and competitive dynamics in the marketplace (Seccia, Santeramo,

and Nardone, 2016). Furthermore brand equity of Treasury Wine Estates Limited can be

successfully and sensible incorporated activities of promotion and marketing and which further

makes then stand in the situation of competition (Bragg, 2016). On the other hand company

should not make any false commitments regarding the features of its product which effect the

position of the company. It specifies the requirement to assure coordination among different

activities of value chain (Goncharuk, and Lazareva, 2017).

Relevance and usefulness of the information

It can be accessed from above analysis that value chain analysis provides systematic review of

transformation process relating to input and output at each distinctive stages. Further, the concept

can be applied to develop organization sustainable competitive advantage. It has been accessed

that value chain is linked with activities relating to conversion of input into final product or

service (Lu, Sridharan, and Tse, 2016). An organization is able to emphasize on value adding

activities through application of value chain analysis. Further, inbound logistic activities assist in

analyzing the relationship with suppliers along with activities relating to storing and

disseminating of inputs. Thus, an organization could ascertain the loop holes and make efficient

attempt to reduce the influence of same (Pangemanan, and Ramintang, 2016).

Question 2

QUESTION 2

Computation of the predicted allocation rates for fixed and variable overhead

for the current period

Table 1 calculation of the allocation rate for predicted variable and fixed expenses

Particulars

Fixed Expenditure (Amount in

$)

Variable expenditure (Amount in

$)

Indirect Labor Wages - 1920

Indirect Supplies - 500

salary of manager 6250

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

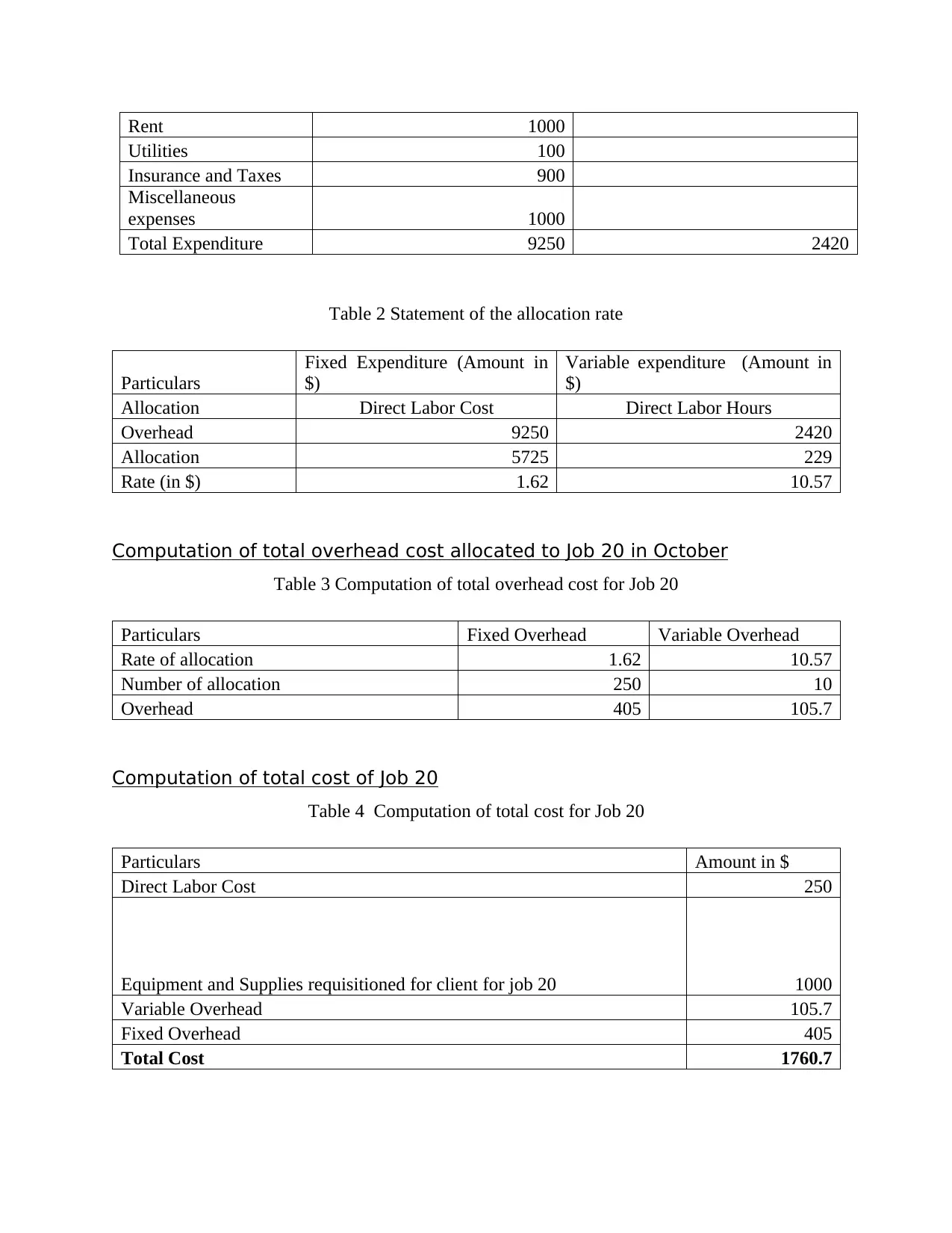

Rent 1000

Utilities 100

Insurance and Taxes 900

Miscellaneous

expenses 1000

Total Expenditure 9250 2420

Table 2 Statement of the allocation rate

Particulars

Fixed Expenditure (Amount in

$)

Variable expenditure (Amount in

$)

Allocation Direct Labor Cost Direct Labor Hours

Overhead 9250 2420

Allocation 5725 229

Rate (in $) 1.62 10.57

Computation of total overhead cost allocated to Job 20 in October

Table 3 Computation of total overhead cost for Job 20

Particulars Fixed Overhead Variable Overhead

Rate of allocation 1.62 10.57

Number of allocation 250 10

Overhead 405 105.7

Computation of total cost of Job 20

Table 4 Computation of total cost for Job 20

Particulars Amount in $

Direct Labor Cost 250

Equipment and Supplies requisitioned for client for job 20 1000

Variable Overhead 105.7

Fixed Overhead 405

Total Cost 1760.7

Utilities 100

Insurance and Taxes 900

Miscellaneous

expenses 1000

Total Expenditure 9250 2420

Table 2 Statement of the allocation rate

Particulars

Fixed Expenditure (Amount in

$)

Variable expenditure (Amount in

$)

Allocation Direct Labor Cost Direct Labor Hours

Overhead 9250 2420

Allocation 5725 229

Rate (in $) 1.62 10.57

Computation of total overhead cost allocated to Job 20 in October

Table 3 Computation of total overhead cost for Job 20

Particulars Fixed Overhead Variable Overhead

Rate of allocation 1.62 10.57

Number of allocation 250 10

Overhead 405 105.7

Computation of total cost of Job 20

Table 4 Computation of total cost for Job 20

Particulars Amount in $

Direct Labor Cost 250

Equipment and Supplies requisitioned for client for job 20 1000

Variable Overhead 105.7

Fixed Overhead 405

Total Cost 1760.7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

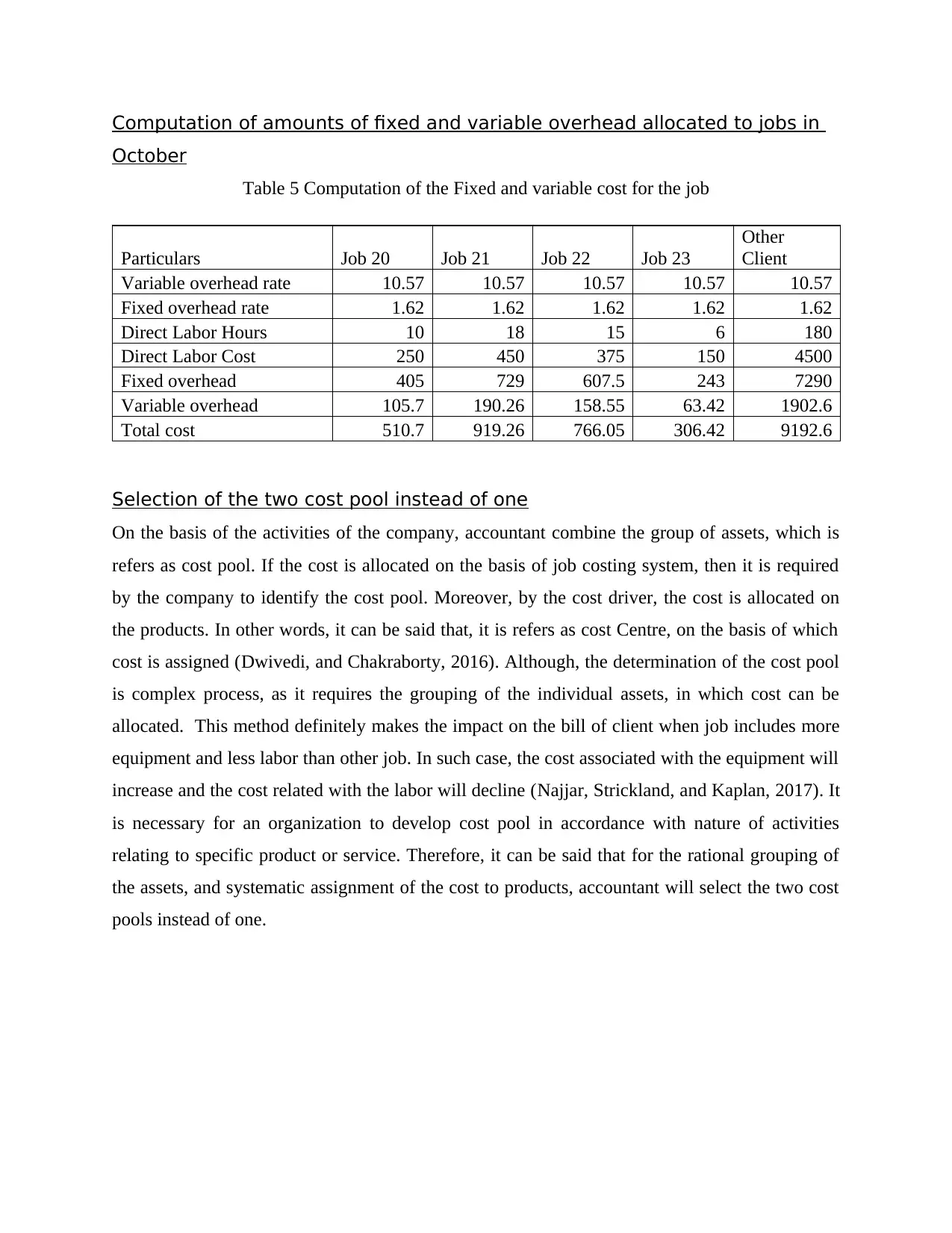

Computation of amounts of fixed and variable overhead allocated to jobs in

October

Table 5 Computation of the Fixed and variable cost for the job

Particulars Job 20 Job 21 Job 22 Job 23

Other

Client

Variable overhead rate 10.57 10.57 10.57 10.57 10.57

Fixed overhead rate 1.62 1.62 1.62 1.62 1.62

Direct Labor Hours 10 18 15 6 180

Direct Labor Cost 250 450 375 150 4500

Fixed overhead 405 729 607.5 243 7290

Variable overhead 105.7 190.26 158.55 63.42 1902.6

Total cost 510.7 919.26 766.05 306.42 9192.6

Selection of the two cost pool instead of one

On the basis of the activities of the company, accountant combine the group of assets, which is

refers as cost pool. If the cost is allocated on the basis of job costing system, then it is required

by the company to identify the cost pool. Moreover, by the cost driver, the cost is allocated on

the products. In other words, it can be said that, it is refers as cost Centre, on the basis of which

cost is assigned (Dwivedi, and Chakraborty, 2016). Although, the determination of the cost pool

is complex process, as it requires the grouping of the individual assets, in which cost can be

allocated. This method definitely makes the impact on the bill of client when job includes more

equipment and less labor than other job. In such case, the cost associated with the equipment will

increase and the cost related with the labor will decline (Najjar, Strickland, and Kaplan, 2017). It

is necessary for an organization to develop cost pool in accordance with nature of activities

relating to specific product or service. Therefore, it can be said that for the rational grouping of

the assets, and systematic assignment of the cost to products, accountant will select the two cost

pools instead of one.

October

Table 5 Computation of the Fixed and variable cost for the job

Particulars Job 20 Job 21 Job 22 Job 23

Other

Client

Variable overhead rate 10.57 10.57 10.57 10.57 10.57

Fixed overhead rate 1.62 1.62 1.62 1.62 1.62

Direct Labor Hours 10 18 15 6 180

Direct Labor Cost 250 450 375 150 4500

Fixed overhead 405 729 607.5 243 7290

Variable overhead 105.7 190.26 158.55 63.42 1902.6

Total cost 510.7 919.26 766.05 306.42 9192.6

Selection of the two cost pool instead of one

On the basis of the activities of the company, accountant combine the group of assets, which is

refers as cost pool. If the cost is allocated on the basis of job costing system, then it is required

by the company to identify the cost pool. Moreover, by the cost driver, the cost is allocated on

the products. In other words, it can be said that, it is refers as cost Centre, on the basis of which

cost is assigned (Dwivedi, and Chakraborty, 2016). Although, the determination of the cost pool

is complex process, as it requires the grouping of the individual assets, in which cost can be

allocated. This method definitely makes the impact on the bill of client when job includes more

equipment and less labor than other job. In such case, the cost associated with the equipment will

increase and the cost related with the labor will decline (Najjar, Strickland, and Kaplan, 2017). It

is necessary for an organization to develop cost pool in accordance with nature of activities

relating to specific product or service. Therefore, it can be said that for the rational grouping of

the assets, and systematic assignment of the cost to products, accountant will select the two cost

pools instead of one.

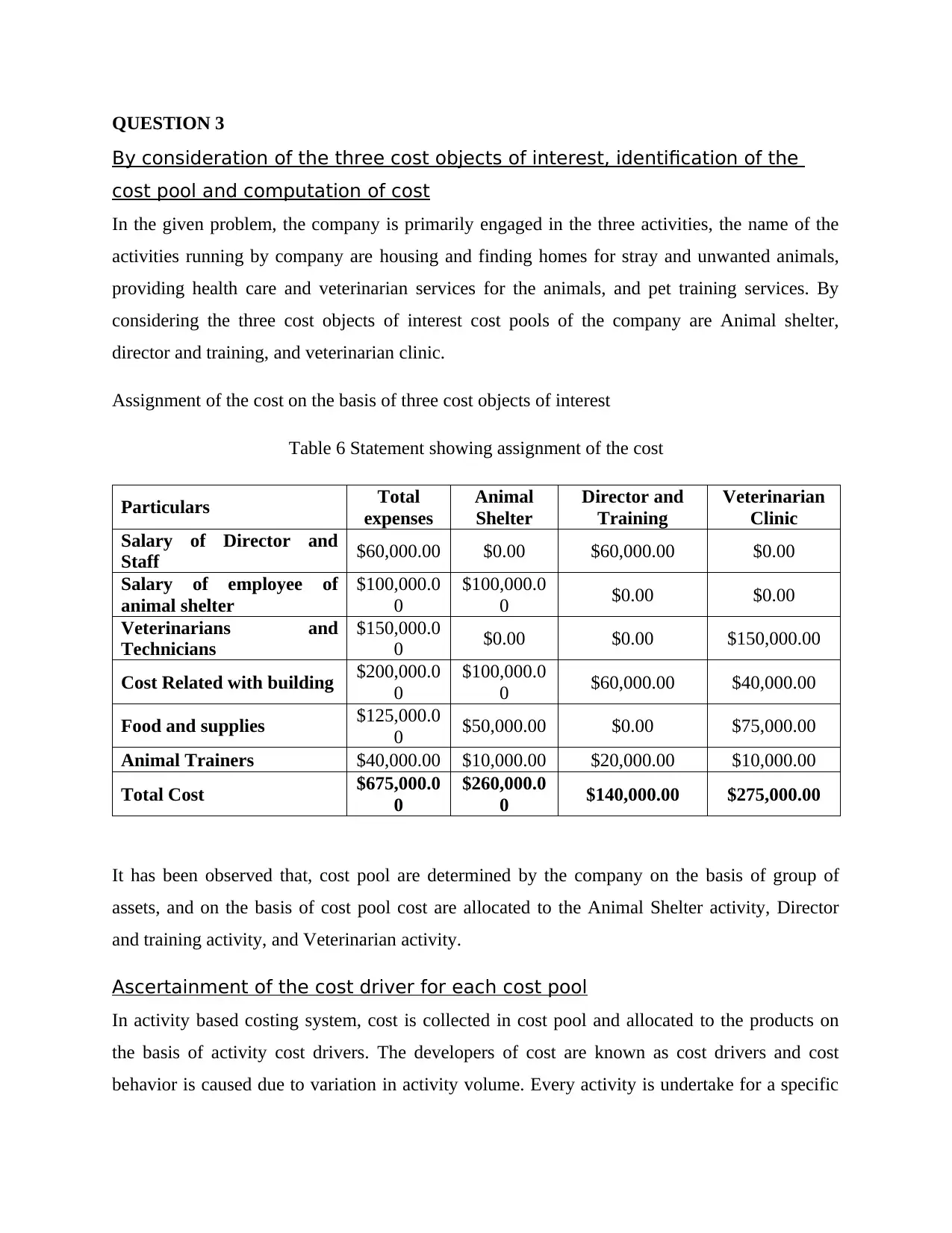

QUESTION 3

By consideration of the three cost objects of interest, identification of the

cost pool and computation of cost

In the given problem, the company is primarily engaged in the three activities, the name of the

activities running by company are housing and finding homes for stray and unwanted animals,

providing health care and veterinarian services for the animals, and pet training services. By

considering the three cost objects of interest cost pools of the company are Animal shelter,

director and training, and veterinarian clinic.

Assignment of the cost on the basis of three cost objects of interest

Table 6 Statement showing assignment of the cost

Particulars Total

expenses

Animal

Shelter

Director and

Training

Veterinarian

Clinic

Salary of Director and

Staff $60,000.00 $0.00 $60,000.00 $0.00

Salary of employee of

animal shelter

$100,000.0

0

$100,000.0

0 $0.00 $0.00

Veterinarians and

Technicians

$150,000.0

0 $0.00 $0.00 $150,000.00

Cost Related with building $200,000.0

0

$100,000.0

0 $60,000.00 $40,000.00

Food and supplies $125,000.0

0 $50,000.00 $0.00 $75,000.00

Animal Trainers $40,000.00 $10,000.00 $20,000.00 $10,000.00

Total Cost $675,000.0

0

$260,000.0

0 $140,000.00 $275,000.00

It has been observed that, cost pool are determined by the company on the basis of group of

assets, and on the basis of cost pool cost are allocated to the Animal Shelter activity, Director

and training activity, and Veterinarian activity.

Ascertainment of the cost driver for each cost pool

In activity based costing system, cost is collected in cost pool and allocated to the products on

the basis of activity cost drivers. The developers of cost are known as cost drivers and cost

behavior is caused due to variation in activity volume. Every activity is undertake for a specific

By consideration of the three cost objects of interest, identification of the

cost pool and computation of cost

In the given problem, the company is primarily engaged in the three activities, the name of the

activities running by company are housing and finding homes for stray and unwanted animals,

providing health care and veterinarian services for the animals, and pet training services. By

considering the three cost objects of interest cost pools of the company are Animal shelter,

director and training, and veterinarian clinic.

Assignment of the cost on the basis of three cost objects of interest

Table 6 Statement showing assignment of the cost

Particulars Total

expenses

Animal

Shelter

Director and

Training

Veterinarian

Clinic

Salary of Director and

Staff $60,000.00 $0.00 $60,000.00 $0.00

Salary of employee of

animal shelter

$100,000.0

0

$100,000.0

0 $0.00 $0.00

Veterinarians and

Technicians

$150,000.0

0 $0.00 $0.00 $150,000.00

Cost Related with building $200,000.0

0

$100,000.0

0 $60,000.00 $40,000.00

Food and supplies $125,000.0

0 $50,000.00 $0.00 $75,000.00

Animal Trainers $40,000.00 $10,000.00 $20,000.00 $10,000.00

Total Cost $675,000.0

0

$260,000.0

0 $140,000.00 $275,000.00

It has been observed that, cost pool are determined by the company on the basis of group of

assets, and on the basis of cost pool cost are allocated to the Animal Shelter activity, Director

and training activity, and Veterinarian activity.

Ascertainment of the cost driver for each cost pool

In activity based costing system, cost is collected in cost pool and allocated to the products on

the basis of activity cost drivers. The developers of cost are known as cost drivers and cost

behavior is caused due to variation in activity volume. Every activity is undertake for a specific

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.