Management Accounting

VerifiedAdded on 2022/11/25

|11

|2535

|58

AI Summary

This assessment analyzes the costing process and activities carried out by Connectta Ltd. It focuses on job costing system, allocation of overhead costs, treatment of under/over applied overheads, and the application of activity-based costing system.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Management Accounting

Name of the Student:

Name of the University:

Author’s Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

MANAGEMENT ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Application of Job Costing System.............................................................................................3

Work in Progress Inventory Account..........................................................................................4

Computation of Costs of Finished goods.....................................................................................4

Over Applied and Under Applied Overhead of the Business......................................................5

Treatment of Under or Over Applied Overheads of the business...............................................5

Activity Based Costing System and its Application....................................................................6

Conclusion.......................................................................................................................................8

Reference.........................................................................................................................................9

MANAGEMENT ACCOUNTING

Table of Contents

Introduction......................................................................................................................................2

Discussion........................................................................................................................................3

Application of Job Costing System.............................................................................................3

Work in Progress Inventory Account..........................................................................................4

Computation of Costs of Finished goods.....................................................................................4

Over Applied and Under Applied Overhead of the Business......................................................5

Treatment of Under or Over Applied Overheads of the business...............................................5

Activity Based Costing System and its Application....................................................................6

Conclusion.......................................................................................................................................8

Reference.........................................................................................................................................9

2

MANAGEMENT ACCOUNTING

Introduction

The assessment would be aiming to analyse the costing process and the activities which is

carried out by Connectta Ltd. The management of Connectta Ltd follows the policy of

maintaining costs under Job costing system and the same also helps the management of the

company for appropriating the costs of the business. The assessment would be focusing on

alternative costing techniques which is available to the management of the company for

presenting the costs of the business in an appropriate manner. The assessment would also be

presenting and allocating the overhead costs of the business in an appropriate manner under

relevant costing technique which would be applied by the business (Armitage, Webb and Glynn

2016). The assessment would further be highlighting the application of over applied and

underapplied overhead costs with respect to the costing process of the business. The role of

Activity based costing would also be assessed from the perspective of costing and how the same

assist the management of the company in taking appropriate decision for the business. The

advantages of job costing system and how the same tackles the deficiencies of traditional costing

system would be discussed in the assessment provided below.

Discussion

Application of Job Costing System

The reporting framework which is used by the management of Connectta Ltd would be

assessed on the basis of the effectiveness of the same. In a business environment, it is very

important to appropriately determine the costs of the business so that an accurate estimate of

profits can be made and also the total costs of the business (Cole 2019). It is also to be noted that

the price which is to be charged for the product is also decided on the basis of the costing

MANAGEMENT ACCOUNTING

Introduction

The assessment would be aiming to analyse the costing process and the activities which is

carried out by Connectta Ltd. The management of Connectta Ltd follows the policy of

maintaining costs under Job costing system and the same also helps the management of the

company for appropriating the costs of the business. The assessment would be focusing on

alternative costing techniques which is available to the management of the company for

presenting the costs of the business in an appropriate manner. The assessment would also be

presenting and allocating the overhead costs of the business in an appropriate manner under

relevant costing technique which would be applied by the business (Armitage, Webb and Glynn

2016). The assessment would further be highlighting the application of over applied and

underapplied overhead costs with respect to the costing process of the business. The role of

Activity based costing would also be assessed from the perspective of costing and how the same

assist the management of the company in taking appropriate decision for the business. The

advantages of job costing system and how the same tackles the deficiencies of traditional costing

system would be discussed in the assessment provided below.

Discussion

Application of Job Costing System

The reporting framework which is used by the management of Connectta Ltd would be

assessed on the basis of the effectiveness of the same. In a business environment, it is very

important to appropriately determine the costs of the business so that an accurate estimate of

profits can be made and also the total costs of the business (Cole 2019). It is also to be noted that

the price which is to be charged for the product is also decided on the basis of the costing

3

MANAGEMENT ACCOUNTING

information which is available to the business (Patassini 2017). Job Costing technique is used by

businesses which mainly depends on making revenue from batches of orders which is received

from a client. Job Costing techniques are used by the management of the company for the

purpose of exercising control over the operations of the business (Clinton and Whisnant 2019).

In a job costing system, the costs of the business would increase on the basis of the demand in

the market and the number of orders which is received by the management of the company in

this respect. The system of job costing basically relies on the demands of the customers and on

the basis of the same costing data are recorded and analyzed by the management of the company

for taking appropriate decisions for the business. It is to be also noted that the process of Job

costing technique is mainly used in a manufacturing concern for effectively meeting their costing

requirements (Ashworth and Perera 2015).

The costing records for a manufacturing concern is generally prepared following Job

Costing system in the business. Some other businesses or institutions which uses job costing

system for the purpose of maintaining the costing records of the business are hospitals, industries

and other business concerns.

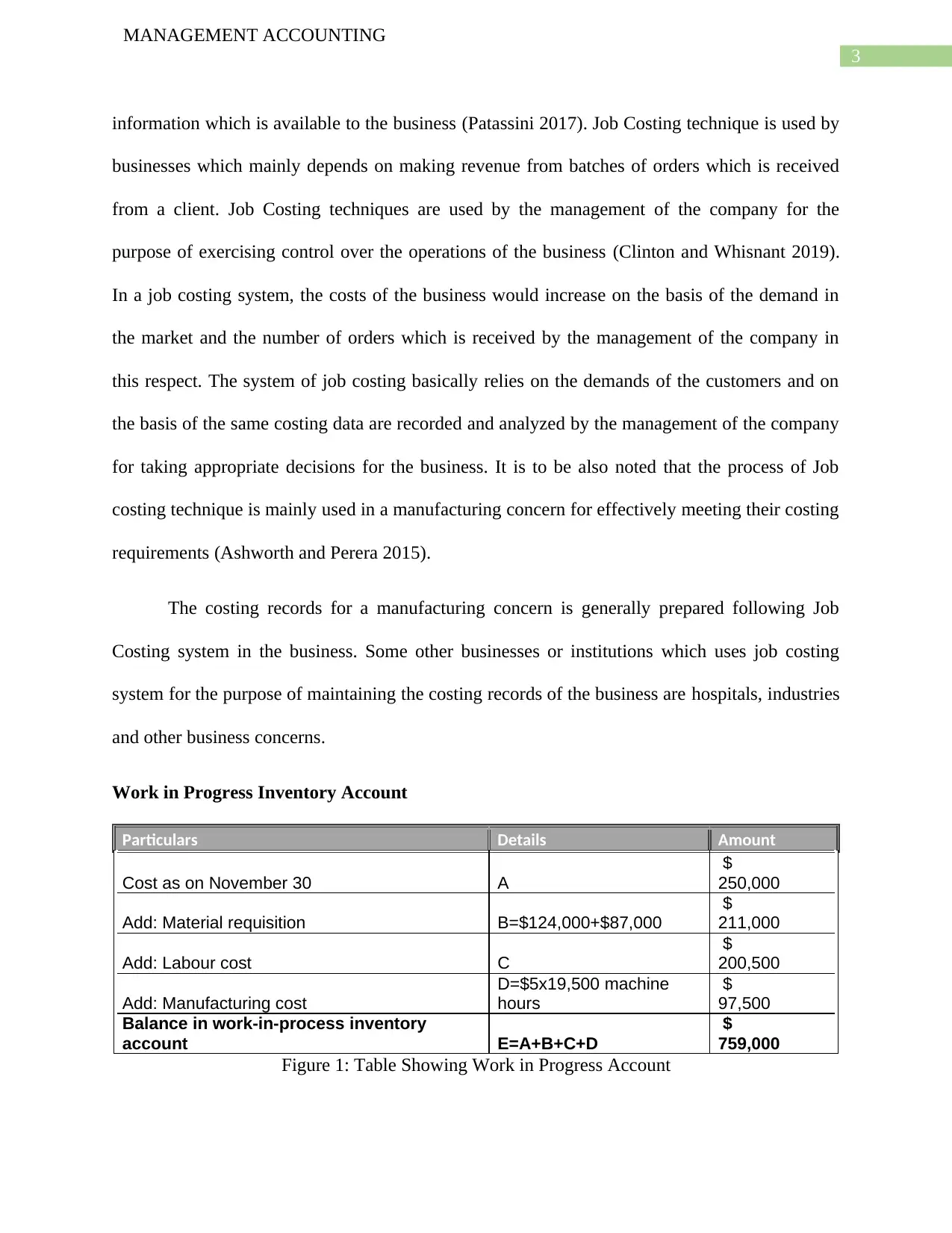

Work in Progress Inventory Account

Particulars Details Amount

Cost as on November 30 A

$

250,000

Add: Material requisition B=$124,000+$87,000

$

211,000

Add: Labour cost C

$

200,500

Add: Manufacturing cost

D=$5x19,500 machine

hours

$

97,500

Balance in work-in-process inventory

account E=A+B+C+D

$

759,000

Figure 1: Table Showing Work in Progress Account

MANAGEMENT ACCOUNTING

information which is available to the business (Patassini 2017). Job Costing technique is used by

businesses which mainly depends on making revenue from batches of orders which is received

from a client. Job Costing techniques are used by the management of the company for the

purpose of exercising control over the operations of the business (Clinton and Whisnant 2019).

In a job costing system, the costs of the business would increase on the basis of the demand in

the market and the number of orders which is received by the management of the company in

this respect. The system of job costing basically relies on the demands of the customers and on

the basis of the same costing data are recorded and analyzed by the management of the company

for taking appropriate decisions for the business. It is to be also noted that the process of Job

costing technique is mainly used in a manufacturing concern for effectively meeting their costing

requirements (Ashworth and Perera 2015).

The costing records for a manufacturing concern is generally prepared following Job

Costing system in the business. Some other businesses or institutions which uses job costing

system for the purpose of maintaining the costing records of the business are hospitals, industries

and other business concerns.

Work in Progress Inventory Account

Particulars Details Amount

Cost as on November 30 A

$

250,000

Add: Material requisition B=$124,000+$87,000

$

211,000

Add: Labour cost C

$

200,500

Add: Manufacturing cost

D=$5x19,500 machine

hours

$

97,500

Balance in work-in-process inventory

account E=A+B+C+D

$

759,000

Figure 1: Table Showing Work in Progress Account

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

MANAGEMENT ACCOUNTING

Source: (Created by the Author)

The above table effectively shows the computation of work in progress of the business

considering the material requisition, labour costs and manufacturing costs of Connectta Ltd. The

balances which is demonstrated in the work in progress account is shown to be $ 759,000. The

computation of inventory cost is considered to be important so that the closing value of work in

progress can be determined and important decisions can be taken on the basis of the same.

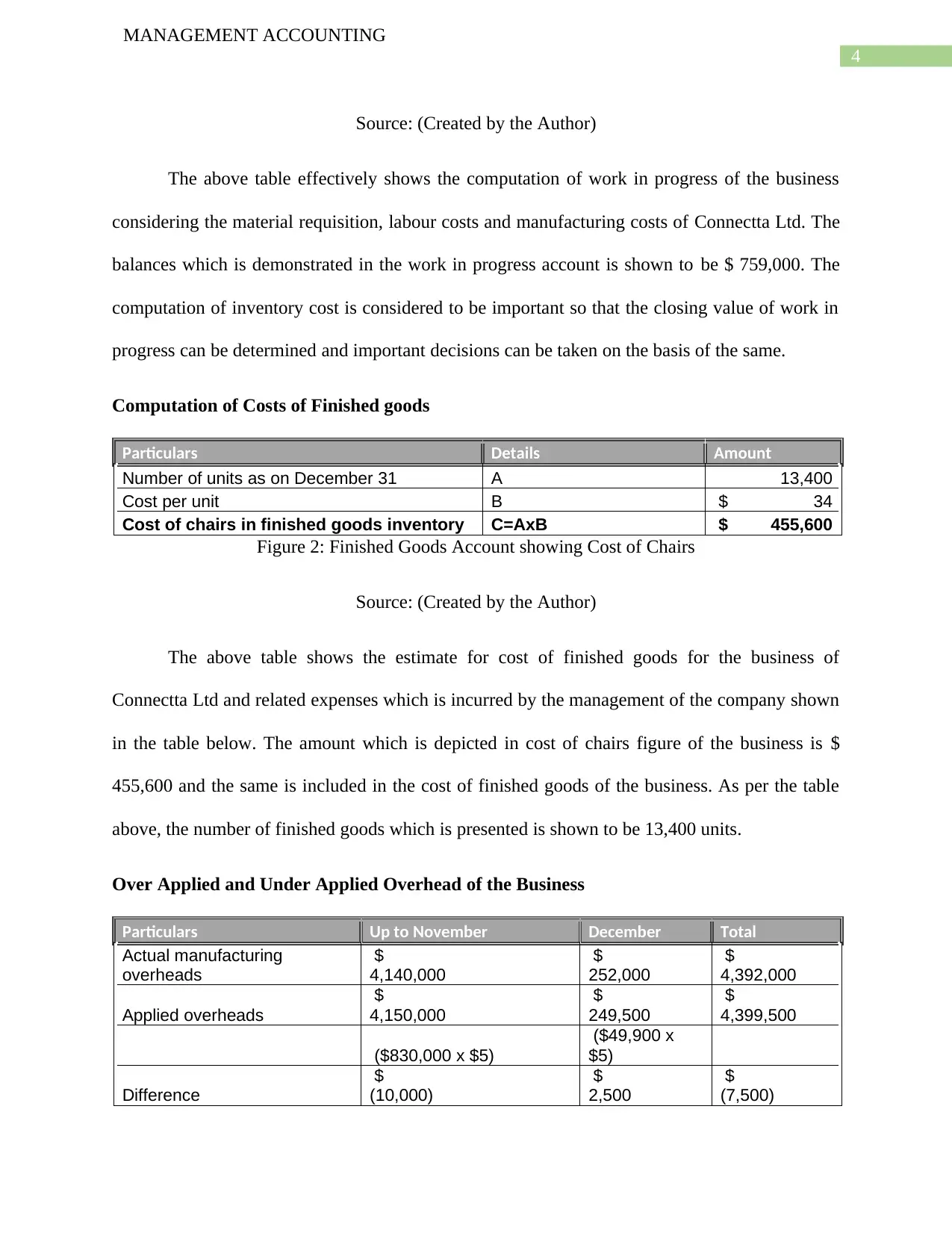

Computation of Costs of Finished goods

Particulars Details Amount

Number of units as on December 31 A 13,400

Cost per unit B $ 34

Cost of chairs in finished goods inventory C=AxB $ 455,600

Figure 2: Finished Goods Account showing Cost of Chairs

Source: (Created by the Author)

The above table shows the estimate for cost of finished goods for the business of

Connectta Ltd and related expenses which is incurred by the management of the company shown

in the table below. The amount which is depicted in cost of chairs figure of the business is $

455,600 and the same is included in the cost of finished goods of the business. As per the table

above, the number of finished goods which is presented is shown to be 13,400 units.

Over Applied and Under Applied Overhead of the Business

Particulars Up to November December Total

Actual manufacturing

overheads

$

4,140,000

$

252,000

$

4,392,000

Applied overheads

$

4,150,000

$

249,500

$

4,399,500

($830,000 x $5)

($49,900 x

$5)

Difference

$

(10,000)

$

2,500

$

(7,500)

MANAGEMENT ACCOUNTING

Source: (Created by the Author)

The above table effectively shows the computation of work in progress of the business

considering the material requisition, labour costs and manufacturing costs of Connectta Ltd. The

balances which is demonstrated in the work in progress account is shown to be $ 759,000. The

computation of inventory cost is considered to be important so that the closing value of work in

progress can be determined and important decisions can be taken on the basis of the same.

Computation of Costs of Finished goods

Particulars Details Amount

Number of units as on December 31 A 13,400

Cost per unit B $ 34

Cost of chairs in finished goods inventory C=AxB $ 455,600

Figure 2: Finished Goods Account showing Cost of Chairs

Source: (Created by the Author)

The above table shows the estimate for cost of finished goods for the business of

Connectta Ltd and related expenses which is incurred by the management of the company shown

in the table below. The amount which is depicted in cost of chairs figure of the business is $

455,600 and the same is included in the cost of finished goods of the business. As per the table

above, the number of finished goods which is presented is shown to be 13,400 units.

Over Applied and Under Applied Overhead of the Business

Particulars Up to November December Total

Actual manufacturing

overheads

$

4,140,000

$

252,000

$

4,392,000

Applied overheads

$

4,150,000

$

249,500

$

4,399,500

($830,000 x $5)

($49,900 x

$5)

Difference

$

(10,000)

$

2,500

$

(7,500)

5

MANAGEMENT ACCOUNTING

Over-applied or Under-

applied Over-Applied

Under-

Applied Over-Applied

Figure 3: Over applied or under applied overhead of the company

Source: (Created by the Author)

The above table effectively shows that the over applied and under applied table is

effectively computed. The application of the overheads of the business is appropriately shown in

the table which is presented above.

Treatment of Under or Over Applied Overheads of the business

The businesses in most of the sectors incurs certain indirect costs which needs to be

treated appropriately and the same should be related to the activities of the business. The

operational process of the business is considered for the purpose of identifying the costs of the

business and also recording the same in the costing records of the business (Schaltegger and

Wagner 2017). The concept of over applied and under applied cost is derived when the cost

accountants of companies charges overhead costs which is more than which is applied or which

is less than what is applied. This situation leads to under applied or over applied overhead costs

which needs to be treated appropriately by the management of the company. One of the methods

which is used for treating over applied or under applied overhead cost in a business is by

following a common method of closing the sane from costs of goods sold related to the business

(Rezaei et al. 2016). This treatment is an indicator that the actual costs which is incurred by the

business was actually higher than what is represented in the records by the cost accountant. It is

to be noted that under applied overhead occurs in a situation when actual overhead costs are

exceeded by overhead applied by the business.

MANAGEMENT ACCOUNTING

Over-applied or Under-

applied Over-Applied

Under-

Applied Over-Applied

Figure 3: Over applied or under applied overhead of the company

Source: (Created by the Author)

The above table effectively shows that the over applied and under applied table is

effectively computed. The application of the overheads of the business is appropriately shown in

the table which is presented above.

Treatment of Under or Over Applied Overheads of the business

The businesses in most of the sectors incurs certain indirect costs which needs to be

treated appropriately and the same should be related to the activities of the business. The

operational process of the business is considered for the purpose of identifying the costs of the

business and also recording the same in the costing records of the business (Schaltegger and

Wagner 2017). The concept of over applied and under applied cost is derived when the cost

accountants of companies charges overhead costs which is more than which is applied or which

is less than what is applied. This situation leads to under applied or over applied overhead costs

which needs to be treated appropriately by the management of the company. One of the methods

which is used for treating over applied or under applied overhead cost in a business is by

following a common method of closing the sane from costs of goods sold related to the business

(Rezaei et al. 2016). This treatment is an indicator that the actual costs which is incurred by the

business was actually higher than what is represented in the records by the cost accountant. It is

to be noted that under applied overhead occurs in a situation when actual overhead costs are

exceeded by overhead applied by the business.

6

MANAGEMENT ACCOUNTING

In simple words, it can be assessed that if an underapplied or overapplied overhead costs

are insignificant in nature than the same would be treated as periodic costs and closed with the

costs of good sold account of the company. However, if the amount of under applied or over

applied costs are significant in nature that the same would be prorated over the relevant accounts.

The relevant accounts which would be considered is from the perspective of costing system of

the company.

Activity Based Costing System and its Application

Activity Based costing technique is one of the popular techniques in costing system

which appropriate identifies the costs of a business with respect to the activity of the business

and thereby assigns the costs in an effective manner. The relationship between costs, overhead

activities and the products are recognised superbly by the costing system (Kustiningsih, Atmadja

and Patmana 2017). The activity-based costing technique is very successful in businesses for

assigning the costs of the business which are indirect in nature and is related to one of the

activities which is carried out by the management of the company. The overhead costs which are

incurred by the business are more appropriately assigned in Activity based costing system in

comparison to traditional method of costing.

The system of activity-based costing is mainly used in manufacturing concerns where

there are lots of activities which are undertaken by the management of the company. The costing

technique enhances the reliability of the cost data and also helps the business in appropriately

presenting the same in the annual reports of the business (Weygandt et al. 2018). Furthermore, it

is on the costing data which the management of the company uses for the purpose of taking

appropriate decisions regarding the business operations (Kannaiah 2015). The method of ABC

costing considers cost drivers which is effectively related with the transactions or event which is

MANAGEMENT ACCOUNTING

In simple words, it can be assessed that if an underapplied or overapplied overhead costs

are insignificant in nature than the same would be treated as periodic costs and closed with the

costs of good sold account of the company. However, if the amount of under applied or over

applied costs are significant in nature that the same would be prorated over the relevant accounts.

The relevant accounts which would be considered is from the perspective of costing system of

the company.

Activity Based Costing System and its Application

Activity Based costing technique is one of the popular techniques in costing system

which appropriate identifies the costs of a business with respect to the activity of the business

and thereby assigns the costs in an effective manner. The relationship between costs, overhead

activities and the products are recognised superbly by the costing system (Kustiningsih, Atmadja

and Patmana 2017). The activity-based costing technique is very successful in businesses for

assigning the costs of the business which are indirect in nature and is related to one of the

activities which is carried out by the management of the company. The overhead costs which are

incurred by the business are more appropriately assigned in Activity based costing system in

comparison to traditional method of costing.

The system of activity-based costing is mainly used in manufacturing concerns where

there are lots of activities which are undertaken by the management of the company. The costing

technique enhances the reliability of the cost data and also helps the business in appropriately

presenting the same in the annual reports of the business (Weygandt et al. 2018). Furthermore, it

is on the costing data which the management of the company uses for the purpose of taking

appropriate decisions regarding the business operations (Kannaiah 2015). The method of ABC

costing considers cost drivers which is effectively related with the transactions or event which is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

considered for the purpose of costing. The process of activity-based costing is preferable by most

of the companies due to the advantages which are brought about by implementing the process in

comparison to traditional costing methods.

In an attempt to compare the traditional and ABC costing system, it is to be noted that

both the methods initially follow the same approach for the purpose of recognising the indirect

costs of the business. In addition to this, both the method uses cost drivers for the purpose of

recognising the costs of the business. The main difference between the two method arises in

terms of complexity and accuracy of the methods (Tsai et al. 2015). The method of traditional

costing has a more simplistic approach and can be considered to be less accurate in relation to

ABC costing system. The traditional system considers an arbitrary rate for assigning the

overhead costs of the business. The assigning of costs on random basis can be considered as a

deficiency which is covered by ABC costing system (Cugini and Pilonato 2017). The process of

ABC costing system initially applies the cost to the activity which it is actually associated with

and then the cost is assigned to the cost of the product on the basis of the usage of the product.

Therefore, the discussion which is conducted in the above analysis clearly indicates that ABC

costing technique is more accurate and presents a correct estimate of the costing data (Pokorná

2016). The method also helps the management to effectively breakdown the costs of the business

and on the basis of the same decisions ca be taken.

Conclusion

The above discussion covers different reporting aspects and also industries which uses

job costing techniques for appropriately representing the costs of the business. The business of

Connectta Ltd effectively follows Job costing system in the business for representing the costs of

MANAGEMENT ACCOUNTING

considered for the purpose of costing. The process of activity-based costing is preferable by most

of the companies due to the advantages which are brought about by implementing the process in

comparison to traditional costing methods.

In an attempt to compare the traditional and ABC costing system, it is to be noted that

both the methods initially follow the same approach for the purpose of recognising the indirect

costs of the business. In addition to this, both the method uses cost drivers for the purpose of

recognising the costs of the business. The main difference between the two method arises in

terms of complexity and accuracy of the methods (Tsai et al. 2015). The method of traditional

costing has a more simplistic approach and can be considered to be less accurate in relation to

ABC costing system. The traditional system considers an arbitrary rate for assigning the

overhead costs of the business. The assigning of costs on random basis can be considered as a

deficiency which is covered by ABC costing system (Cugini and Pilonato 2017). The process of

ABC costing system initially applies the cost to the activity which it is actually associated with

and then the cost is assigned to the cost of the product on the basis of the usage of the product.

Therefore, the discussion which is conducted in the above analysis clearly indicates that ABC

costing technique is more accurate and presents a correct estimate of the costing data (Pokorná

2016). The method also helps the management to effectively breakdown the costs of the business

and on the basis of the same decisions ca be taken.

Conclusion

The above discussion covers different reporting aspects and also industries which uses

job costing techniques for appropriately representing the costs of the business. The business of

Connectta Ltd effectively follows Job costing system in the business for representing the costs of

8

MANAGEMENT ACCOUNTING

the business. The above analysis also shows calculations of work in progress and finished goods

of the business which forms a part of the total assets of the business. The discussion reveals

features of overhead costs and how under applied and over applied overhead should be treated by

the cost accountant of the business. In addition to this, the importance and uses of ABC system

of costing in also included in the discussion along with comparison of the same with traditional

costing techniques of a business. Therefore, it is recommended to the management of Connectta

Ltd that they should start following ABC costing techniques as the same would allow the

management of the company to improve the cost reporting structure of the business.

MANAGEMENT ACCOUNTING

the business. The above analysis also shows calculations of work in progress and finished goods

of the business which forms a part of the total assets of the business. The discussion reveals

features of overhead costs and how under applied and over applied overhead should be treated by

the cost accountant of the business. In addition to this, the importance and uses of ABC system

of costing in also included in the discussion along with comparison of the same with traditional

costing techniques of a business. Therefore, it is recommended to the management of Connectta

Ltd that they should start following ABC costing techniques as the same would allow the

management of the company to improve the cost reporting structure of the business.

9

MANAGEMENT ACCOUNTING

Reference

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Ashworth, A. and Perera, S., 2015. Cost studies of buildings. Routledge.

Clinton, L. and Whisnant, R., 2019. Business Model Innovations for Sustainability. In Managing

Sustainable Business (pp. 463-503). Springer, Dordrecht.

Cole, S.A., 2019. Managing Activity-Based Funding Using Costing Data and Activity-Based

Budgets. In Clinical Costing Techniques and Analysis in Modern Healthcare Systems (pp. 128-

143). IGI Global.

Cugini, A. and Pilonato, S., 2017. The Cost Accounting System in B-to-B Service Companies:

Cost Centers or Activity-Based Costing?. GSTF Journal on Business Review (GBR), 2(4).

Kannaiah, D., 2015. Activity based costing (ABC): Is it a tool for company to achieve

competitive advantage. International Journal of Economics and Finance, 7(12), pp.275-281.

Kustiningsih, N., Atmadja, S.S. and Patmana, O., 2017. Implementation Of Activity Based

Costing System In Making Affort To Determine The Tariff Of Operation Action (Case Study In

Surabaya Royal Hospital). Archives of Business Research, 5(11).

Patassini, D., 2017. Beyond benefit cost analysis: accounting for non-market values in planning

evaluation. Routledge.

MANAGEMENT ACCOUNTING

Reference

Armitage, H.M., Webb, A. and Glynn, J., 2016. The use of management accounting techniques

by small and medium‐sized enterprises: a field study of Canadian and Australian

practice. Accounting Perspectives, 15(1), pp.31-69.

Ashworth, A. and Perera, S., 2015. Cost studies of buildings. Routledge.

Clinton, L. and Whisnant, R., 2019. Business Model Innovations for Sustainability. In Managing

Sustainable Business (pp. 463-503). Springer, Dordrecht.

Cole, S.A., 2019. Managing Activity-Based Funding Using Costing Data and Activity-Based

Budgets. In Clinical Costing Techniques and Analysis in Modern Healthcare Systems (pp. 128-

143). IGI Global.

Cugini, A. and Pilonato, S., 2017. The Cost Accounting System in B-to-B Service Companies:

Cost Centers or Activity-Based Costing?. GSTF Journal on Business Review (GBR), 2(4).

Kannaiah, D., 2015. Activity based costing (ABC): Is it a tool for company to achieve

competitive advantage. International Journal of Economics and Finance, 7(12), pp.275-281.

Kustiningsih, N., Atmadja, S.S. and Patmana, O., 2017. Implementation Of Activity Based

Costing System In Making Affort To Determine The Tariff Of Operation Action (Case Study In

Surabaya Royal Hospital). Archives of Business Research, 5(11).

Patassini, D., 2017. Beyond benefit cost analysis: accounting for non-market values in planning

evaluation. Routledge.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

MANAGEMENT ACCOUNTING

Pokorná, J., 2016. Impact of Activity-based costing on financial performance in the Czech

Republic. Acta Universitatis agriculturae et silviculturae mendelianae brunensis, 64(2), pp.643-

652.

Rezaei, J., Nispeling, T., Sarkis, J. and Tavasszy, L., 2016. A supplier selection life cycle

approach integrating traditional and environmental criteria using the best worst method. Journal

of Cleaner Production, 135, pp.577-588.

Schaltegger, S. and Wagner, M., 2017. Managing the business case for sustainability: The

integration of social, environmental and economic performance. Routledge.

Tsai, W.H., Tsaur, T.S., Chou, Y.W., Liu, J.Y., Hsu, J.L. and Hsieh, C.L., 2015. Integrating the

activity-based costing system and life-cycle assessment into green decision-

making. International Journal of Production Research, 53(2), pp.451-465.

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial Accounting: Tools

for Business Decision-making. John Wiley & Sons Canada, Limited.

MANAGEMENT ACCOUNTING

Pokorná, J., 2016. Impact of Activity-based costing on financial performance in the Czech

Republic. Acta Universitatis agriculturae et silviculturae mendelianae brunensis, 64(2), pp.643-

652.

Rezaei, J., Nispeling, T., Sarkis, J. and Tavasszy, L., 2016. A supplier selection life cycle

approach integrating traditional and environmental criteria using the best worst method. Journal

of Cleaner Production, 135, pp.577-588.

Schaltegger, S. and Wagner, M., 2017. Managing the business case for sustainability: The

integration of social, environmental and economic performance. Routledge.

Tsai, W.H., Tsaur, T.S., Chou, Y.W., Liu, J.Y., Hsu, J.L. and Hsieh, C.L., 2015. Integrating the

activity-based costing system and life-cycle assessment into green decision-

making. International Journal of Production Research, 53(2), pp.451-465.

Weygandt, J.J., Kieso, D.E., Kimmel, P.D. and Aly, I.M., 2018. Managerial Accounting: Tools

for Business Decision-making. John Wiley & Sons Canada, Limited.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.