Management Accounting Report: Neptune International Ltd Analysis

VerifiedAdded on 2023/01/19

|11

|2357

|94

Report

AI Summary

This management accounting report, prepared for Neptune International Ltd, a diversified manufacturing company, analyzes various aspects of financial management. It begins with an examination of manufacturing cost flows and cost behavior, including production capacity and its constraints. The report then constructs a comprehensive manufacturing budget and evaluates strategic management reports, particularly focusing on the potential for expanding production capacity and the financial implications of such expansion. Furthermore, it delves into strategic and international issues, considering the growth opportunities in the Chinese market, the importance of Guanxi in Chinese business practices, and the challenges of integrating Western accounting methods. The report also includes comparative analyses of revenue and cost structures, and offers recommendations based on the financial data provided, assessing the impact of strategic decisions on profitability and return on total assets (ROTA). The assignment provides detailed financial analysis and strategic insights for Neptune International Ltd.

Running head: MANAGEMENT ACCOUNTING

Management accounting

Name of the student

Name of the university

Student ID

Author note

Management accounting

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MANAGEMENT ACCOUNTING

Table of Contents

Question 1 – Manufacturing cost flows.....................................................................................2

Question 2 – Cost behaviour......................................................................................................2

Question 3 – Comprehensive Manufacturing Budget................................................................3

Question 4 - Strategic and International issues in Management Accounting............................4

Question 5 – Strategic management accounting........................................................................6

Reference....................................................................................................................................9

Table of Contents

Question 1 – Manufacturing cost flows.....................................................................................2

Question 2 – Cost behaviour......................................................................................................2

Question 3 – Comprehensive Manufacturing Budget................................................................3

Question 4 - Strategic and International issues in Management Accounting............................4

Question 5 – Strategic management accounting........................................................................6

Reference....................................................................................................................................9

2MANAGEMENT ACCOUNTING

Question 1 – Manufacturing cost flows

Refer to Excel sheet

Question 2 – Cost behaviour

Production capacity

It is defined as the products volume that can be generated through the production

plant or through the enterprise in the given period of time by utilising the current resources.

Practical capacity is the level of output for the manufacturer that is generally expressed in

terms of machine hours, labour hours or pounds and it is lower than the ideal or theoretical

capacity. On the other hand, theoretical capacity is the manufacturer’s production level that

will be achieved if all of the operations and equipments perform continuously at the optimum

efficiency. It is also known as the ideal capacity (Qian, Burritt & Chen, 2015).

Practical capacity is most realistic to take place on the basis of space, people and

machines. On the contrary, theoretical capacity is the perfect scenario for the world with full

utilization of everything. However, virtually the theoretical capacity is unachievable.

Constraints impacting production capacity

Relevant range of the production capacity is budget within which the entity expects

operating generally during the short term period. Hence, the relevant range has maximum as

well as minimum limits for budgeting and cost accounting that the entity shall operate within.

If the entity operates below or above the relevant range within the given frame of time, it

shall make adjustments for operating (van Helden & Uddin, 2016). However, different types

of constraints that may impact the production capacity as follows –

Question 1 – Manufacturing cost flows

Refer to Excel sheet

Question 2 – Cost behaviour

Production capacity

It is defined as the products volume that can be generated through the production

plant or through the enterprise in the given period of time by utilising the current resources.

Practical capacity is the level of output for the manufacturer that is generally expressed in

terms of machine hours, labour hours or pounds and it is lower than the ideal or theoretical

capacity. On the other hand, theoretical capacity is the manufacturer’s production level that

will be achieved if all of the operations and equipments perform continuously at the optimum

efficiency. It is also known as the ideal capacity (Qian, Burritt & Chen, 2015).

Practical capacity is most realistic to take place on the basis of space, people and

machines. On the contrary, theoretical capacity is the perfect scenario for the world with full

utilization of everything. However, virtually the theoretical capacity is unachievable.

Constraints impacting production capacity

Relevant range of the production capacity is budget within which the entity expects

operating generally during the short term period. Hence, the relevant range has maximum as

well as minimum limits for budgeting and cost accounting that the entity shall operate within.

If the entity operates below or above the relevant range within the given frame of time, it

shall make adjustments for operating (van Helden & Uddin, 2016). However, different types

of constraints that may impact the production capacity as follows –

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MANAGEMENT ACCOUNTING

Raw materials – material shall be readily available in the sufficient quantity for

supplying to the production line. Quality and delivery time of raw materials can be the

issue that have an impact on production capacity (Rieckhof, Bergmann & Guenther,

2015)

Labour – staffing is most effective variable in management of short term production

capacity. Reducing or adding the staff may have an impact on the production

(Klychova, Faskhutdinova & Sadrieva, 2014)

Equipment – throughput and speed of equipment have limiting factors that may

impact the production capacity

Storage – warehouse storage have an impact on outbound as well as inbound capacity

that may in turn affect the production capacity as the products has shelf time and

cannot be stored for indefinite time period (Boulaksil, Fransoo & Tan, 2017).

Question 3 – Comprehensive Manufacturing Budget

(a) Refer to Excel sheet

(b) Refer to Excel sheet

(c) Strategic management report

It has been identified from the stated situation that export sales growth in Kiewa Milk

Baby Formula are constrained by the present theoretical limit of the factory which is 50

million per annum. Hence, the company is thinking of converting the former yoghurt and

milk sections of Kiewa Milk factory that will increase the production limit by 100%. The

upgrade will be completed by the year 2020 that can be financed by additional $ 1 million per

annum. It can be found from the gross profit and sales budget for the 5 years period starting

from 2019 to 2023 it can be identified that without up-gradation the gross profit will be

increased from -56% to 52%. However, after up-gradation the gross profit will be increased

Raw materials – material shall be readily available in the sufficient quantity for

supplying to the production line. Quality and delivery time of raw materials can be the

issue that have an impact on production capacity (Rieckhof, Bergmann & Guenther,

2015)

Labour – staffing is most effective variable in management of short term production

capacity. Reducing or adding the staff may have an impact on the production

(Klychova, Faskhutdinova & Sadrieva, 2014)

Equipment – throughput and speed of equipment have limiting factors that may

impact the production capacity

Storage – warehouse storage have an impact on outbound as well as inbound capacity

that may in turn affect the production capacity as the products has shelf time and

cannot be stored for indefinite time period (Boulaksil, Fransoo & Tan, 2017).

Question 3 – Comprehensive Manufacturing Budget

(a) Refer to Excel sheet

(b) Refer to Excel sheet

(c) Strategic management report

It has been identified from the stated situation that export sales growth in Kiewa Milk

Baby Formula are constrained by the present theoretical limit of the factory which is 50

million per annum. Hence, the company is thinking of converting the former yoghurt and

milk sections of Kiewa Milk factory that will increase the production limit by 100%. The

upgrade will be completed by the year 2020 that can be financed by additional $ 1 million per

annum. It can be found from the gross profit and sales budget for the 5 years period starting

from 2019 to 2023 it can be identified that without up-gradation the gross profit will be

increased from -56% to 52%. However, after up-gradation the gross profit will be increased

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MANAGEMENT ACCOUNTING

from 56% to 68% over the years from 2019 to 2023. Further, it is found that rates of gross

profit margin are significantly high after up-gradation. Further, it can be stated that without

up-gradation the entity will face the production limit constraint. Hence, even if the entity gets

the opportunity of selling more units owing to production limit constraint it will not have

sufficient number of units to be sold. Hence, it is suggested that the entity shall ignore the

short term benefits and taking into consideration the long term benefits up-gradation shall be

made to the product line for overcoming the production constraint (Jamil et al., 2015).

Question 4 - Strategic and International issues in Management Accounting

Part 1

As urbanisation is rapidly growing in China and number of middle class people are

increasing the demand of the consumers for the high quality of the dairy products are

expected to be increased in the next ten years. Further, the sales channels are changing

rapidly in context of pricing, regulation for new entry like cross border e-commerce.

However, the leading Australian dairy firms are exploring the opportunities for growth and

collaboration in rapidly expanding dairy market of China. Further, the recent closure of

Murray Goulburn which left number of people jobless in Kiewa valley will provide an

opportunity for Neptune International in the same place. Based on the projected sales and

profit it can be seen that proposed purchase of can be printable (Otley, 2016). However the

inherent risks are as follows –

Expected sales and profits are just the budget and prepared on the basis of

assumption. In actual the scenario may be different and the sales and profit can be

much lower as compared to the expectation.

Due to unfavourable situation in market that may arise in any time, the Australian

dollar value may fall against the Chinese Yuan that will have adverse impact on the

from 56% to 68% over the years from 2019 to 2023. Further, it is found that rates of gross

profit margin are significantly high after up-gradation. Further, it can be stated that without

up-gradation the entity will face the production limit constraint. Hence, even if the entity gets

the opportunity of selling more units owing to production limit constraint it will not have

sufficient number of units to be sold. Hence, it is suggested that the entity shall ignore the

short term benefits and taking into consideration the long term benefits up-gradation shall be

made to the product line for overcoming the production constraint (Jamil et al., 2015).

Question 4 - Strategic and International issues in Management Accounting

Part 1

As urbanisation is rapidly growing in China and number of middle class people are

increasing the demand of the consumers for the high quality of the dairy products are

expected to be increased in the next ten years. Further, the sales channels are changing

rapidly in context of pricing, regulation for new entry like cross border e-commerce.

However, the leading Australian dairy firms are exploring the opportunities for growth and

collaboration in rapidly expanding dairy market of China. Further, the recent closure of

Murray Goulburn which left number of people jobless in Kiewa valley will provide an

opportunity for Neptune International in the same place. Based on the projected sales and

profit it can be seen that proposed purchase of can be printable (Otley, 2016). However the

inherent risks are as follows –

Expected sales and profits are just the budget and prepared on the basis of

assumption. In actual the scenario may be different and the sales and profit can be

much lower as compared to the expectation.

Due to unfavourable situation in market that may arise in any time, the Australian

dollar value may fall against the Chinese Yuan that will have adverse impact on the

5MANAGEMENT ACCOUNTING

revenue that will be generated by the head office of Neptune International in Australia

(Otley, 2016).

Part 2

In China, Guanxi is the crucial aspect of carrying out the business. In English it is best

terms as connections. The term explains the relationship that can be leveraged for making the

life easier and for gaining advantages. Building Guanxi requires long term approach and can

be carried out at various ways. It is used to describe the contract networks. These networks

have direct impact on business conduct style in china and include the sales growth and

expansion (Wang, 2014). On the other hand, power distance is the extent till which the

society will accept that the power is unequally distributed and is established through the

superiors and subordinates. The societies with the high power distance like China, the

individuals with the power avail greater privilege and status as compared to those without the

power. Here, the subordinates are unlikely to express or challenge disagreement with their

superiors. Hence, rank structure is defined clearly among the subordinates and management

(Chen, Zhang & Wang, 2014).

However, Australian business practices may struggle in integrating the Guanxi and

power distance specifically for the difference in budgeting and management accounting

system as follows –

Main obstacle in implementing the western methods is not the political sensitivity

rather it is the technical constraints. Management information system in China is still

under development stage whereas in western system activity based costing requires

numerous data which is not possible to implement under the current situation of China

(Kamal, 2015).

revenue that will be generated by the head office of Neptune International in Australia

(Otley, 2016).

Part 2

In China, Guanxi is the crucial aspect of carrying out the business. In English it is best

terms as connections. The term explains the relationship that can be leveraged for making the

life easier and for gaining advantages. Building Guanxi requires long term approach and can

be carried out at various ways. It is used to describe the contract networks. These networks

have direct impact on business conduct style in china and include the sales growth and

expansion (Wang, 2014). On the other hand, power distance is the extent till which the

society will accept that the power is unequally distributed and is established through the

superiors and subordinates. The societies with the high power distance like China, the

individuals with the power avail greater privilege and status as compared to those without the

power. Here, the subordinates are unlikely to express or challenge disagreement with their

superiors. Hence, rank structure is defined clearly among the subordinates and management

(Chen, Zhang & Wang, 2014).

However, Australian business practices may struggle in integrating the Guanxi and

power distance specifically for the difference in budgeting and management accounting

system as follows –

Main obstacle in implementing the western methods is not the political sensitivity

rather it is the technical constraints. Management information system in China is still

under development stage whereas in western system activity based costing requires

numerous data which is not possible to implement under the current situation of China

(Kamal, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MANAGEMENT ACCOUNTING

Changes in the management accounting has been identified only in some areas like

quality of the products that is promoted and profitability

China uses the compliance oriented budget management whereas in western countries

performance based budget managements are used. Hence, the China is required to

move the focus from inputs and shall focus on outputs to know how the objectives of

original budget are fulfilled.

Management accounting requires accurate information and the main difference in

Chinese accounting system and western accounting system is the accounting

measurement and recognition. As per western approach different accounting methods

can be used while in China possibility for the accounting options are limited for

numerous issues (Wang, 2014).

Question 5 – Strategic management accounting

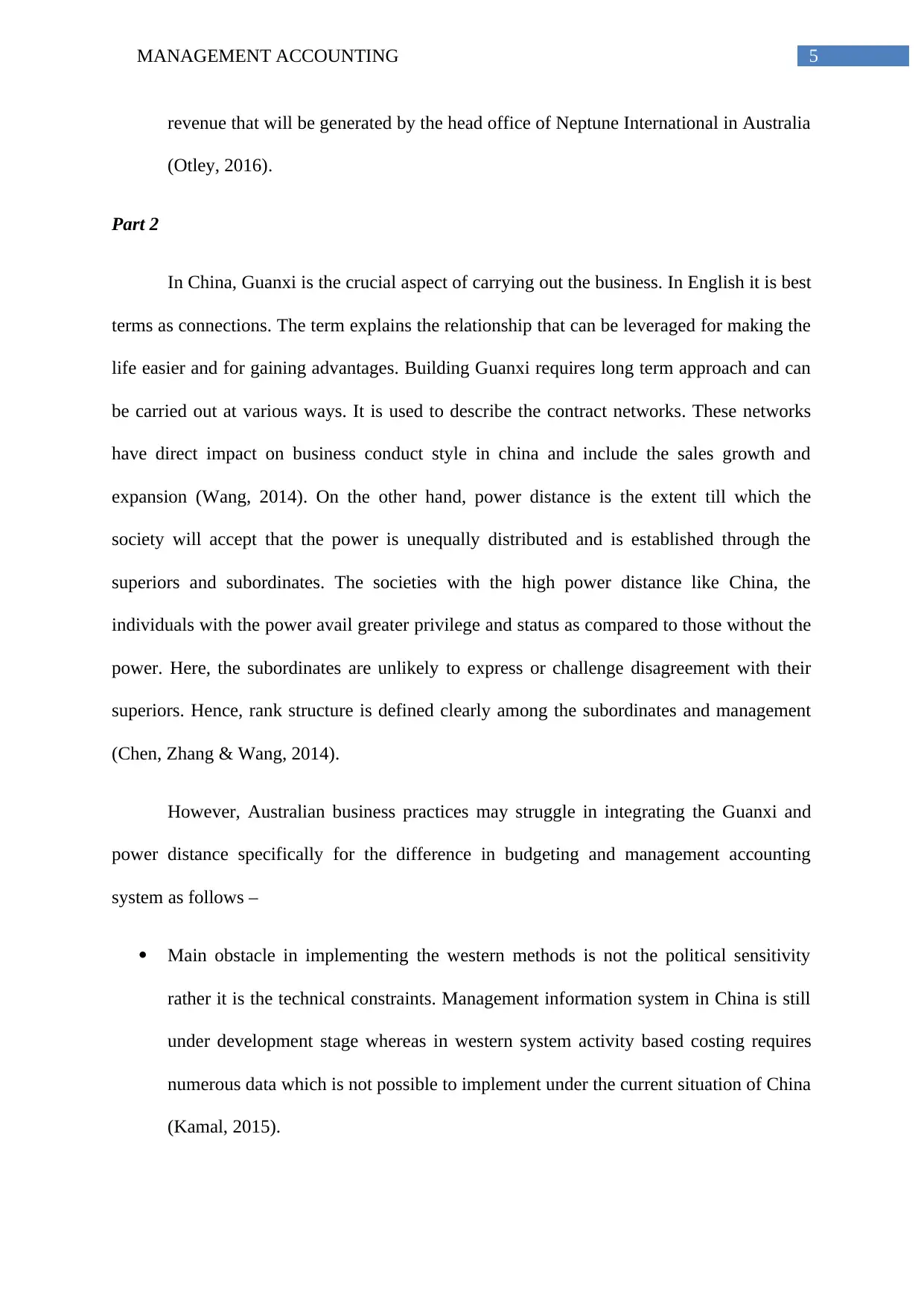

(i) Comparative analysis of revenue and cost of Nutty Nut product

Changes in the management accounting has been identified only in some areas like

quality of the products that is promoted and profitability

China uses the compliance oriented budget management whereas in western countries

performance based budget managements are used. Hence, the China is required to

move the focus from inputs and shall focus on outputs to know how the objectives of

original budget are fulfilled.

Management accounting requires accurate information and the main difference in

Chinese accounting system and western accounting system is the accounting

measurement and recognition. As per western approach different accounting methods

can be used while in China possibility for the accounting options are limited for

numerous issues (Wang, 2014).

Question 5 – Strategic management accounting

(i) Comparative analysis of revenue and cost of Nutty Nut product

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MANAGEMENT ACCOUNTING

(ii) Report to strategic management committee

(a) Profit and cost structure of Neptune Confectionary

From the given data it can be understood that though the sales volume will increase

by 20% and 10% savings will be there in prime cost, due to additional discount of 0.25 per

unit the sales revenue will be reduced to $ 2.75 per units from $ 3 per unit. Further, due to

additional discounts contribution margin will be reduced from $ 0.65 per unit to $ 0.475 per

unit. Hence it can be identified that the gross profit margin will be reduced from 8.33% to

2.73% (Yin, Nishi & Zhang, 2016). Further, the ROTA will be reduced from 15% to 10.20%.

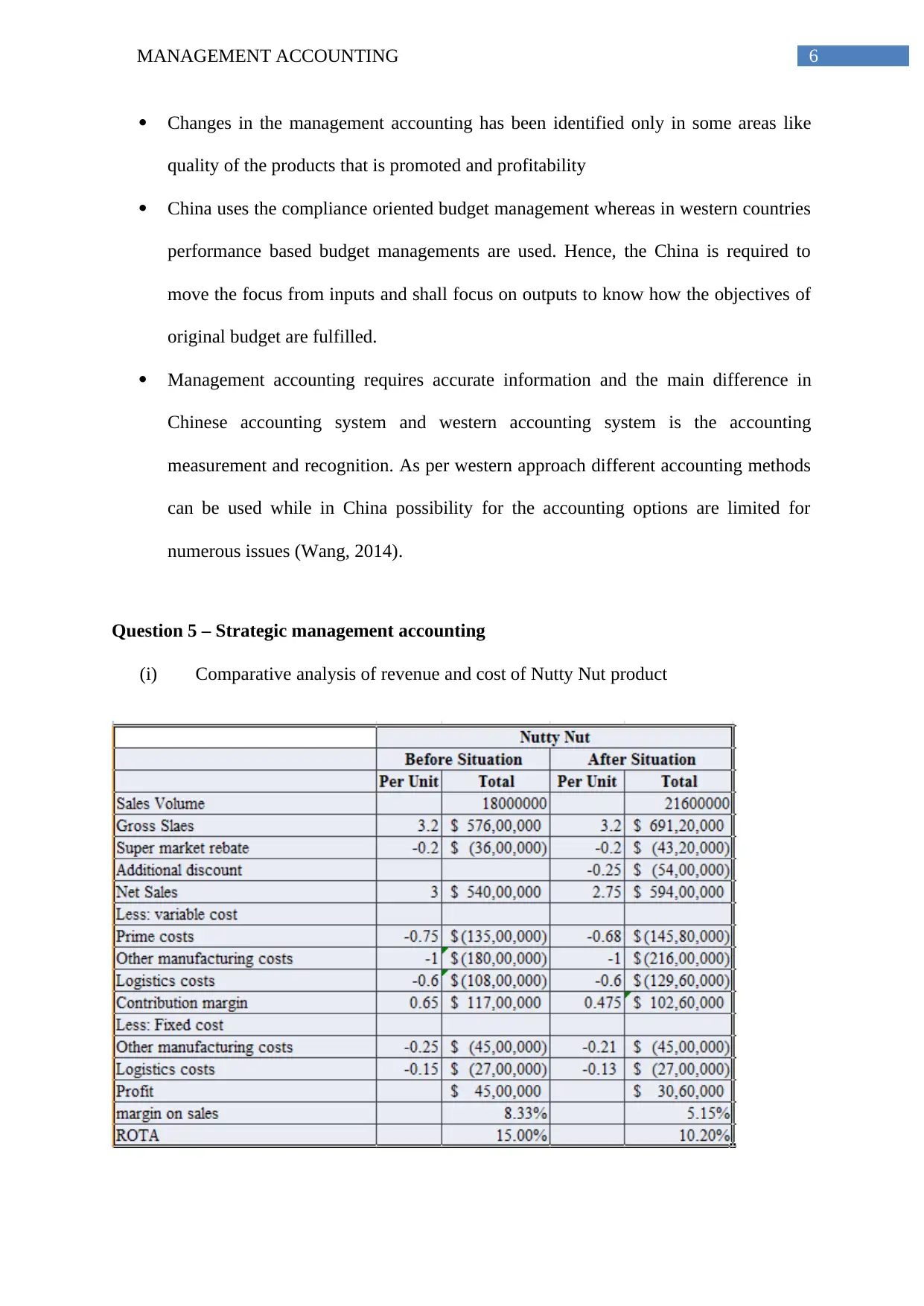

(b) Changes in cost structure of N&N

It can be identified from the above table that increase in sales volume of nutty nut will

take place at the cost of N & N’s sales volumes. Further, N & N will not be able to make any

immediate changes in the sales price and the unit costs will be same as the Nutty Nut. Hence,

(ii) Report to strategic management committee

(a) Profit and cost structure of Neptune Confectionary

From the given data it can be understood that though the sales volume will increase

by 20% and 10% savings will be there in prime cost, due to additional discount of 0.25 per

unit the sales revenue will be reduced to $ 2.75 per units from $ 3 per unit. Further, due to

additional discounts contribution margin will be reduced from $ 0.65 per unit to $ 0.475 per

unit. Hence it can be identified that the gross profit margin will be reduced from 8.33% to

2.73% (Yin, Nishi & Zhang, 2016). Further, the ROTA will be reduced from 15% to 10.20%.

(b) Changes in cost structure of N&N

It can be identified from the above table that increase in sales volume of nutty nut will

take place at the cost of N & N’s sales volumes. Further, N & N will not be able to make any

immediate changes in the sales price and the unit costs will be same as the Nutty Nut. Hence,

8MANAGEMENT ACCOUNTING

the sales volume will be reduced from 90,00,000 units to 57,60,000 units. However the profit

margin will be reduced from 8.33% to 0.83% (Balakrishnan, Labro & Soderstrom, 2014).

(c) Recommendation

It can be seen from the above comparison of before and after situation analysis that

for Nutty Nut the profit has been reduced from 8.33% to 5.15%. The reason behind that is for

achieving higher sales the company had to offer additional discount of 0.25 per unit that will

reduce the net sales revenue to $ 2.75 per units from $ 3 per unit. Due to additional discounts

contribution margin will be reduced from $ 0.25 per unit to $ 0.075 per unit. On the other

hand, the sales margin for N & N will be reduced from 8.33% to 0.83% and the ROTA will

be reduced from 7.50% to 0.48%. Hence, it is recommended that the company shall not go

ahead with the planned changes as the ROTA of Nutty Nut will be reduced from 15% to

10.20% which is much lower than the required ROTA of the company that is 17.255.

the sales volume will be reduced from 90,00,000 units to 57,60,000 units. However the profit

margin will be reduced from 8.33% to 0.83% (Balakrishnan, Labro & Soderstrom, 2014).

(c) Recommendation

It can be seen from the above comparison of before and after situation analysis that

for Nutty Nut the profit has been reduced from 8.33% to 5.15%. The reason behind that is for

achieving higher sales the company had to offer additional discount of 0.25 per unit that will

reduce the net sales revenue to $ 2.75 per units from $ 3 per unit. Due to additional discounts

contribution margin will be reduced from $ 0.25 per unit to $ 0.075 per unit. On the other

hand, the sales margin for N & N will be reduced from 8.33% to 0.83% and the ROTA will

be reduced from 7.50% to 0.48%. Hence, it is recommended that the company shall not go

ahead with the planned changes as the ROTA of Nutty Nut will be reduced from 15% to

10.20% which is much lower than the required ROTA of the company that is 17.255.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MANAGEMENT ACCOUNTING

Reference

Balakrishnan, R., Labro, E., & Soderstrom, N. S. (2014). Cost structure and sticky

costs. Journal of management accounting research, 26(2), 91-116.

Boulaksil, Y., Fransoo, J. C., & Tan, T. (2017). Capacity reservation and utilization for a

manufacturer with uncertain capacity and demand. OR Spectrum, 39(3), 689-709.

Chen, C. C., Zhang, A. Y., & Wang, H. (2014). Enhancing the effects of power sharing on

psychological empowerment: The roles of management control and power distance

orientation. Management and Organization Review, 10(1), 135-156.

Jamil, C. Z. M., Mohamed, R., Muhammad, F., & Ali, A. (2015). Environmental

management accounting practices in small medium manufacturing firms. Procedia-

Social and Behavioral Sciences, 172, 619-626.

Kamal, S. (2015). Historical evolution of management accounting. The cost and

management, 43(4), 12-19.

Klychova, G.S., Faskhutdinova, М.S. & Sadrieva, E.R., (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), p.79.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Qian, W., Burritt, R., & Chen, J. (2015). The potential for environmental management

accounting development in China. Journal of Accounting & Organizational

Change, 11(3), 406-428.

Reference

Balakrishnan, R., Labro, E., & Soderstrom, N. S. (2014). Cost structure and sticky

costs. Journal of management accounting research, 26(2), 91-116.

Boulaksil, Y., Fransoo, J. C., & Tan, T. (2017). Capacity reservation and utilization for a

manufacturer with uncertain capacity and demand. OR Spectrum, 39(3), 689-709.

Chen, C. C., Zhang, A. Y., & Wang, H. (2014). Enhancing the effects of power sharing on

psychological empowerment: The roles of management control and power distance

orientation. Management and Organization Review, 10(1), 135-156.

Jamil, C. Z. M., Mohamed, R., Muhammad, F., & Ali, A. (2015). Environmental

management accounting practices in small medium manufacturing firms. Procedia-

Social and Behavioral Sciences, 172, 619-626.

Kamal, S. (2015). Historical evolution of management accounting. The cost and

management, 43(4), 12-19.

Klychova, G.S., Faskhutdinova, М.S. & Sadrieva, E.R., (2014). Budget efficiency for cost

control purposes in management accounting system. Mediterranean journal of social

sciences, 5(24), p.79.

Otley, D. (2016). The contingency theory of management accounting and control: 1980–

2014. Management accounting research, 31, 45-62.

Qian, W., Burritt, R., & Chen, J. (2015). The potential for environmental management

accounting development in China. Journal of Accounting & Organizational

Change, 11(3), 406-428.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MANAGEMENT ACCOUNTING

Rieckhof, R., Bergmann, A. & Guenther, E., (2015). Interrelating material flow cost

accounting with management control systems to introduce resource efficiency into

strategy. Journal of Cleaner Production, 108, pp.1262-1278.

van Helden, J., & Uddin, S. (2016). Public sector management accounting in emerging

economies: A literature review. Critical Perspectives on Accounting, 41, 34-62.

Wang, P. (2014). Extra-legal protection in China: How guanxi distorts China’s legal system

and facilitates the rise of unlawful protectors. British Journal of Criminology, 54(5),

809-830.

Yin, S., Nishi, T., & Zhang, G. (2016). A game theoretic model for coordination of single

manufacturer and multiple suppliers with quality variations under uncertain

demands. International Journal of Systems Science: Operations & Logistics, 3(2), 79-

91.

Rieckhof, R., Bergmann, A. & Guenther, E., (2015). Interrelating material flow cost

accounting with management control systems to introduce resource efficiency into

strategy. Journal of Cleaner Production, 108, pp.1262-1278.

van Helden, J., & Uddin, S. (2016). Public sector management accounting in emerging

economies: A literature review. Critical Perspectives on Accounting, 41, 34-62.

Wang, P. (2014). Extra-legal protection in China: How guanxi distorts China’s legal system

and facilitates the rise of unlawful protectors. British Journal of Criminology, 54(5),

809-830.

Yin, S., Nishi, T., & Zhang, G. (2016). A game theoretic model for coordination of single

manufacturer and multiple suppliers with quality variations under uncertain

demands. International Journal of Systems Science: Operations & Logistics, 3(2), 79-

91.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.