Management Accounting and Financial Research Studies

VerifiedAdded on 2020/10/22

|17

|5402

|89

AI Summary

This assignment provides a comprehensive overview of various management accounting research studies. It includes papers on job costing, human resource accounting, key performance indicators, and other related topics. The studies cover different aspects of management accounting, such as cost analysis, financial reporting, and economic consequences. The assignment also highlights the importance of qualitative perspectives in management accounting research.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essentials requirements of various type of management

systems........................................................................................................................................3

P2. Various methods used for management accounting reporting..............................................6

M1. Merits of using management accounting system.................................................................7

D1. Integration of management accounting systems and management accounting report.........8

TASK 2............................................................................................................................................8

P3 Calculate cost using marginal and absorption costing...........................................................8

M2. Use of management accounting techniques.......................................................................10

D2 Financial report that apply for interpret business activities................................................10

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantage of various planning tools.....................................................11

M3. Evaluation of planning tools .............................................................................................13

TASK 4..........................................................................................................................................13

P5. Adaption of management accounting system to respond financial problems.....................13

M4. Evaluation of financial issues ...........................................................................................15

D3. Evaluation of planning tools for responding to financial problems...................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and essentials requirements of various type of management

systems........................................................................................................................................3

P2. Various methods used for management accounting reporting..............................................6

M1. Merits of using management accounting system.................................................................7

D1. Integration of management accounting systems and management accounting report.........8

TASK 2............................................................................................................................................8

P3 Calculate cost using marginal and absorption costing...........................................................8

M2. Use of management accounting techniques.......................................................................10

D2 Financial report that apply for interpret business activities................................................10

TASK 3..........................................................................................................................................11

P4 Advantages and disadvantage of various planning tools.....................................................11

M3. Evaluation of planning tools .............................................................................................13

TASK 4..........................................................................................................................................13

P5. Adaption of management accounting system to respond financial problems.....................13

M4. Evaluation of financial issues ...........................................................................................15

D3. Evaluation of planning tools for responding to financial problems...................................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting system is the procedure of preparing the financial report that

helps manager in taking right decisions and also attains control on the business operations ehich

directly contributes towards the attainment of company's desired goals and objectives. This gives

information related to the financial situations of the firm and also used in taking decisions of

organising, directing and controlling the cost by optimal utilisation of resources. AGMET is

small business enterprise which is incorporated on 29 April 1980 and manufacture chemical

products (Balakrishnan, Labro and Soderstrom, 2014). This report contains various kinds of

managerial accounting system and their significance. Further, it describes about different tools

and techniques of cost analysis that is used for preparing income statement by using absorption

and marginal cost. In addition to this, project also includes different planning tools which

provides direction for performing their task more effectively. This report also contains different

types of managerial accounting system which assist in AGMET to make business operations

more profitable.

TASK 1

P1. Management accounting and essentials requirements of various type of management systems

Management accounting can be defined as the process of identifying, analysing,

measuring, communicating and interpreting information to manager for achievement of the

organisational goals and objectives. It is action related to making sense of costing and financial

data and converting that in a productive information for management and employees in the

company. Advantage of management accounting is that it assists in getting better control on the

business activities that helps in the growth and success of the organisation (Bedford, 2015). In

the context of AGMET, managers of the company evaluate the the information that is related to

the financial aspects that is variation in stock, raw materials, financial condition of an enterprise

and many more which aids in performing business operations in minimum cost and in an

effective manner. One of the major benefit of management accounting is that it helps in

improving the financial situation of the firm and also provides stability in the financial system.

An organisation may faces problems and issues while performing business functions and

management accounting helps in finding solution to these problems and contributing towards the

achievement of overall goals of the firm. AGMET have to manage and keep a record of whole

Management accounting system is the procedure of preparing the financial report that

helps manager in taking right decisions and also attains control on the business operations ehich

directly contributes towards the attainment of company's desired goals and objectives. This gives

information related to the financial situations of the firm and also used in taking decisions of

organising, directing and controlling the cost by optimal utilisation of resources. AGMET is

small business enterprise which is incorporated on 29 April 1980 and manufacture chemical

products (Balakrishnan, Labro and Soderstrom, 2014). This report contains various kinds of

managerial accounting system and their significance. Further, it describes about different tools

and techniques of cost analysis that is used for preparing income statement by using absorption

and marginal cost. In addition to this, project also includes different planning tools which

provides direction for performing their task more effectively. This report also contains different

types of managerial accounting system which assist in AGMET to make business operations

more profitable.

TASK 1

P1. Management accounting and essentials requirements of various type of management systems

Management accounting can be defined as the process of identifying, analysing,

measuring, communicating and interpreting information to manager for achievement of the

organisational goals and objectives. It is action related to making sense of costing and financial

data and converting that in a productive information for management and employees in the

company. Advantage of management accounting is that it assists in getting better control on the

business activities that helps in the growth and success of the organisation (Bedford, 2015). In

the context of AGMET, managers of the company evaluate the the information that is related to

the financial aspects that is variation in stock, raw materials, financial condition of an enterprise

and many more which aids in performing business operations in minimum cost and in an

effective manner. One of the major benefit of management accounting is that it helps in

improving the financial situation of the firm and also provides stability in the financial system.

An organisation may faces problems and issues while performing business functions and

management accounting helps in finding solution to these problems and contributing towards the

achievement of overall goals of the firm. AGMET have to manage and keep a record of whole

financial activities which helps in growth and success of the business. There are various

importance of management accounting system that are mentioned below in points:

Assist in decision making: Management accounting system is the procedure of analysis

and collection of data that can be used by AGMET to formulate policies and plans. This

assist in taking correct decision which results in attainment of set organisational goals

and objectives.

Safety and security from trade cycle: The useful information collected with the help of

management accounting system provides real picture of past trade cycle that aids

company in ascertaining the cause of effects and errors (Bennett and James, 2017).

Therefore, it helps AGMET in protecting the organisation from the negative impact that

may arises because of the trade cycle.

Increases efficiency of business: One of the major importance of management

accounting system is that it helps in improving the efficiency of business activities. It

determines the objectives of various departments in advance and achieve of these goals

are used as an efficiency management tool. It is useful for AGMET in planning,

managing, coordinating and controlling activities of the enterprise.

Types of accounting system:

Cost accounting system: It is the type of management accounting system which helps in

analysing the cost of organisation's products and services for controlling the cost,

inventory valuation and profitability. It is very necessary to estimate the exact production

cost of AGMET which helps in making business operations more profitable and also

developing financial statement of enterprise that determines the financial condition of

company for whole year.

Job costing: It is the another type of management accounting system which accumulates

the information of cost that is associated with a specific production and service is known

as job costing (Job Costing, 2018). This helps AGMET in recording and tracking the kind

of cost incurred like labour, manufacturing cost, overheads, etc. Job costing focuses on

managing and controlling the expenditures and increases the profitability of the firm.

importance of management accounting system that are mentioned below in points:

Assist in decision making: Management accounting system is the procedure of analysis

and collection of data that can be used by AGMET to formulate policies and plans. This

assist in taking correct decision which results in attainment of set organisational goals

and objectives.

Safety and security from trade cycle: The useful information collected with the help of

management accounting system provides real picture of past trade cycle that aids

company in ascertaining the cause of effects and errors (Bennett and James, 2017).

Therefore, it helps AGMET in protecting the organisation from the negative impact that

may arises because of the trade cycle.

Increases efficiency of business: One of the major importance of management

accounting system is that it helps in improving the efficiency of business activities. It

determines the objectives of various departments in advance and achieve of these goals

are used as an efficiency management tool. It is useful for AGMET in planning,

managing, coordinating and controlling activities of the enterprise.

Types of accounting system:

Cost accounting system: It is the type of management accounting system which helps in

analysing the cost of organisation's products and services for controlling the cost,

inventory valuation and profitability. It is very necessary to estimate the exact production

cost of AGMET which helps in making business operations more profitable and also

developing financial statement of enterprise that determines the financial condition of

company for whole year.

Job costing: It is the another type of management accounting system which accumulates

the information of cost that is associated with a specific production and service is known

as job costing (Job Costing, 2018). This helps AGMET in recording and tracking the kind

of cost incurred like labour, manufacturing cost, overheads, etc. Job costing focuses on

managing and controlling the expenditures and increases the profitability of the firm.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

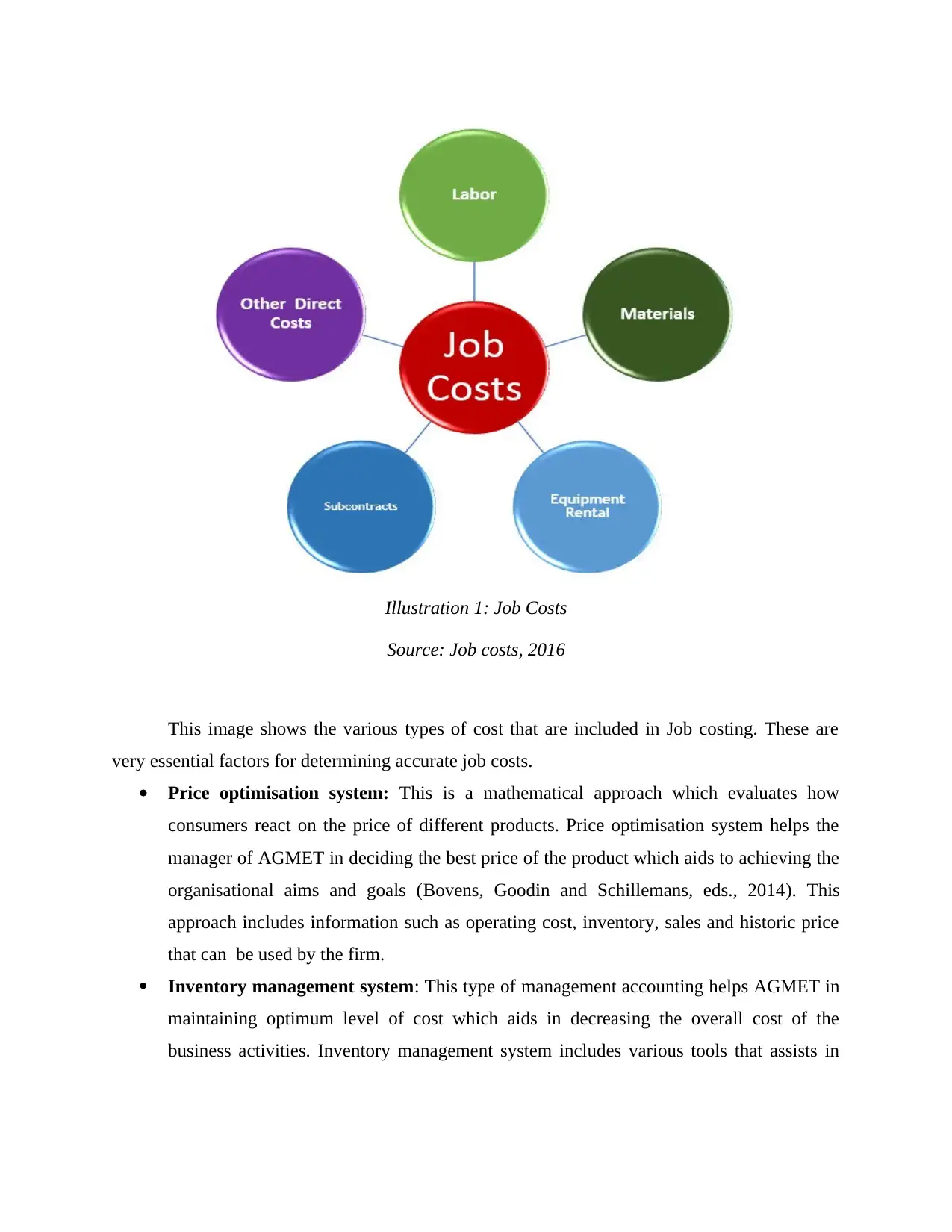

This image shows the various types of cost that are included in Job costing. These are

very essential factors for determining accurate job costs.

Price optimisation system: This is a mathematical approach which evaluates how

consumers react on the price of different products. Price optimisation system helps the

manager of AGMET in deciding the best price of the product which aids to achieving the

organisational aims and goals (Bovens, Goodin and Schillemans, eds., 2014). This

approach includes information such as operating cost, inventory, sales and historic price

that can be used by the firm.

Inventory management system: This type of management accounting helps AGMET in

maintaining optimum level of cost which aids in decreasing the overall cost of the

business activities. Inventory management system includes various tools that assists in

Illustration 1: Job Costs

Source: Job costs, 2016

very essential factors for determining accurate job costs.

Price optimisation system: This is a mathematical approach which evaluates how

consumers react on the price of different products. Price optimisation system helps the

manager of AGMET in deciding the best price of the product which aids to achieving the

organisational aims and goals (Bovens, Goodin and Schillemans, eds., 2014). This

approach includes information such as operating cost, inventory, sales and historic price

that can be used by the firm.

Inventory management system: This type of management accounting helps AGMET in

maintaining optimum level of cost which aids in decreasing the overall cost of the

business activities. Inventory management system includes various tools that assists in

Illustration 1: Job Costs

Source: Job costs, 2016

reducing the cost such as economic order quantity, just in time, etc. that helps in

accomplishing organisational goals.

P2. Various methods used for management accounting reporting

Management accounting reports are very essential for planning, regulating, measuring

performance and in decision making. These reports are developed on continuous basis in

financial year as per the requirements. Decisions and future planning are dependent on

accounting report (Grossi and Steccolini, 2014). Manager of AGMET determines the managerial

accounting report and turns them in productive information for an enterprise.

There are various methods that can be utilised by AGMET for developing accounting

reports that are as follows:

Budget report: This is an important method that is used by AGMET to evaluate the

performance of company and analysing department operations. Budget report helps

manger of the firm in comparing actual performance with the estimated budgeted

statement. This report includes all the revenue and expenditure. According to the

budgeted report, AGMET have set their goals and objectives. This helps in guiding

manager to provide incentives, bonuses to their staff member.

Job costing report: It is another method of managerial accounting method which

includes all expenditures for particular task that is funded by firm. Job costing report

helps in identifying the more profitable areas of AGMET. Therefore, manager have to

emphasis on extra efforts and do not funded the projects which has less earnings. This

method of managerial accounting report useful in measuring the expenses when project is

in process. So it helps in decreasing the waste before cost spiral out of control. Manager

of AGMET have to evaluate the records of task done and also increases the performance

of the employees. The objective of firm is to reduce the wastage and maximize the

revenue in an effective way.

Performance reporting system: This report is crafted to evaluate the operations of an

organisation. It helps in taking strategical decisions that are related to future actions of an

enterprise. Performance reporting system is focuses on financial statement which assist in

determining and regulating the actual performance of the firm (Jack,2015). This type of

managerial accounting report plays an important role in AGMET by keeping exact

measure of their strategies towards the set objectives of the entity.

accomplishing organisational goals.

P2. Various methods used for management accounting reporting

Management accounting reports are very essential for planning, regulating, measuring

performance and in decision making. These reports are developed on continuous basis in

financial year as per the requirements. Decisions and future planning are dependent on

accounting report (Grossi and Steccolini, 2014). Manager of AGMET determines the managerial

accounting report and turns them in productive information for an enterprise.

There are various methods that can be utilised by AGMET for developing accounting

reports that are as follows:

Budget report: This is an important method that is used by AGMET to evaluate the

performance of company and analysing department operations. Budget report helps

manger of the firm in comparing actual performance with the estimated budgeted

statement. This report includes all the revenue and expenditure. According to the

budgeted report, AGMET have set their goals and objectives. This helps in guiding

manager to provide incentives, bonuses to their staff member.

Job costing report: It is another method of managerial accounting method which

includes all expenditures for particular task that is funded by firm. Job costing report

helps in identifying the more profitable areas of AGMET. Therefore, manager have to

emphasis on extra efforts and do not funded the projects which has less earnings. This

method of managerial accounting report useful in measuring the expenses when project is

in process. So it helps in decreasing the waste before cost spiral out of control. Manager

of AGMET have to evaluate the records of task done and also increases the performance

of the employees. The objective of firm is to reduce the wastage and maximize the

revenue in an effective way.

Performance reporting system: This report is crafted to evaluate the operations of an

organisation. It helps in taking strategical decisions that are related to future actions of an

enterprise. Performance reporting system is focuses on financial statement which assist in

determining and regulating the actual performance of the firm (Jack,2015). This type of

managerial accounting report plays an important role in AGMET by keeping exact

measure of their strategies towards the set objectives of the entity.

Manufacturing and inventory report: This is another method of managerial accounting

report which helps in maintaining production procedure and physical stock more

efficiently and effectively. This report includes several items that are hourly labour cost,

inventory waste and per unit overhead expenses. Manager of AGMET have to compare

various assemble lines of an organisation that helpful in finding out areas of betterment

and also provides rewards to employees over their good performance.

Accounts receivable aging report: It is type of managerial accounting report which is

periodic in nature and categories company's account receivable according to the time

duration of invoices that has been outstanding (Ji, 2017). Manager of AGMET utilises

accounts receivable aging report to finding out the problem of firm's payment collection

process. When more number of customers are not paying their amounts and company

have to tighten their credit policy. It is very essential that there must be ongoing

evaluation of this report to maintaining the collection department from overlooking old

liability.

Cost managerial accounting reports: This report helps in computing the cost of product

which is produced in the firm. Cost managerial accounting report is consist of several

items that are labour, raw materials, overheads and other cost. It provides the brief of all

data which is related to the manufacturing process. It is very essential for the managers of

AGMET to use this report for the better performance of firm which helps in attaining set

objectives of an enterprise.

M1. Merits of using management accounting system

Management accounting system plays vital role in an organisation that is helpful in

managing and controlling the financial transactions which takes place in effective way. It is

important for AGMET to use several accounting systems such as price optimisation, job costing,

cost accounting system and inventory management system that helps in achieving more

profitability (Lachmann, Trapp and Trapp, 2017). Management accounting system useful in

increasing the effectiveness of the business performance and also helps in taking better decisions.

The information collected by process of management accounting throws light over several

problems which is faced during the trade cycle and identifying the reasons behind them.

Therefore, firm can increase their efficiency by eliminating the problems.

report which helps in maintaining production procedure and physical stock more

efficiently and effectively. This report includes several items that are hourly labour cost,

inventory waste and per unit overhead expenses. Manager of AGMET have to compare

various assemble lines of an organisation that helpful in finding out areas of betterment

and also provides rewards to employees over their good performance.

Accounts receivable aging report: It is type of managerial accounting report which is

periodic in nature and categories company's account receivable according to the time

duration of invoices that has been outstanding (Ji, 2017). Manager of AGMET utilises

accounts receivable aging report to finding out the problem of firm's payment collection

process. When more number of customers are not paying their amounts and company

have to tighten their credit policy. It is very essential that there must be ongoing

evaluation of this report to maintaining the collection department from overlooking old

liability.

Cost managerial accounting reports: This report helps in computing the cost of product

which is produced in the firm. Cost managerial accounting report is consist of several

items that are labour, raw materials, overheads and other cost. It provides the brief of all

data which is related to the manufacturing process. It is very essential for the managers of

AGMET to use this report for the better performance of firm which helps in attaining set

objectives of an enterprise.

M1. Merits of using management accounting system

Management accounting system plays vital role in an organisation that is helpful in

managing and controlling the financial transactions which takes place in effective way. It is

important for AGMET to use several accounting systems such as price optimisation, job costing,

cost accounting system and inventory management system that helps in achieving more

profitability (Lachmann, Trapp and Trapp, 2017). Management accounting system useful in

increasing the effectiveness of the business performance and also helps in taking better decisions.

The information collected by process of management accounting throws light over several

problems which is faced during the trade cycle and identifying the reasons behind them.

Therefore, firm can increase their efficiency by eliminating the problems.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D1. Integration of management accounting systems and management accounting report

According to Hoque, Z., stability in growth is the major objective of every organisation

that can be attained by utilising an integrated approach of accounting that involves management

accounting system and reporting system. Manager of AGMET uses managerial accounting

system to develop a report for evaluating the performance of the company based on past data.

This aids company in taking investment decisions and also reduces the expenses that is incurred

in operational and financial activities.

TASK 2

P3 Calculate cost using marginal and absorption costing

Managerial accounting refers to the process of determining, analysing measuring,

interpreting and communicating information to managers in order to achieve organisational goal

more effectively. It includes various cost approach which help AGMET in achieving effective

and better outcome:-

Marginal costing:- This approach help in increasing or decreasing the cost of production

by producing one more unit. Marginal costing combines the standard costing with

budgetary control which in turn will provide better control over cost.

Absorption costing:- This approach is based on assumption that the incurred cost can be

recover from selling price. Under this method all the cost related to manufacturing of

goods and services are taken into consideration while setting the selling price of a

product.

Following table shows the comparison between marginal and absorption costing:

Basis Marginal costing Absorption costing

Meaning Marginal costing refer to a

decision making technique by

ascertaining the total cost of

production (Luft and Shields,

2014).

Absorption costing refers to

the calculation of

manufacturing cost along with

overhead expenses.

Cost recognition The fixed cost is considered as

period cost while the variable

cost is consider as production

Under absorption costing the

both fixed and variable cost

are consider as production

According to Hoque, Z., stability in growth is the major objective of every organisation

that can be attained by utilising an integrated approach of accounting that involves management

accounting system and reporting system. Manager of AGMET uses managerial accounting

system to develop a report for evaluating the performance of the company based on past data.

This aids company in taking investment decisions and also reduces the expenses that is incurred

in operational and financial activities.

TASK 2

P3 Calculate cost using marginal and absorption costing

Managerial accounting refers to the process of determining, analysing measuring,

interpreting and communicating information to managers in order to achieve organisational goal

more effectively. It includes various cost approach which help AGMET in achieving effective

and better outcome:-

Marginal costing:- This approach help in increasing or decreasing the cost of production

by producing one more unit. Marginal costing combines the standard costing with

budgetary control which in turn will provide better control over cost.

Absorption costing:- This approach is based on assumption that the incurred cost can be

recover from selling price. Under this method all the cost related to manufacturing of

goods and services are taken into consideration while setting the selling price of a

product.

Following table shows the comparison between marginal and absorption costing:

Basis Marginal costing Absorption costing

Meaning Marginal costing refer to a

decision making technique by

ascertaining the total cost of

production (Luft and Shields,

2014).

Absorption costing refers to

the calculation of

manufacturing cost along with

overhead expenses.

Cost recognition The fixed cost is considered as

period cost while the variable

cost is consider as production

Under absorption costing the

both fixed and variable cost

are consider as production

cost. cost.

Profitability In marginal costing the

profitability is measured using

profit volume ratio.

Profitability in absorption cost

is affected as it includes fixed

cost.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

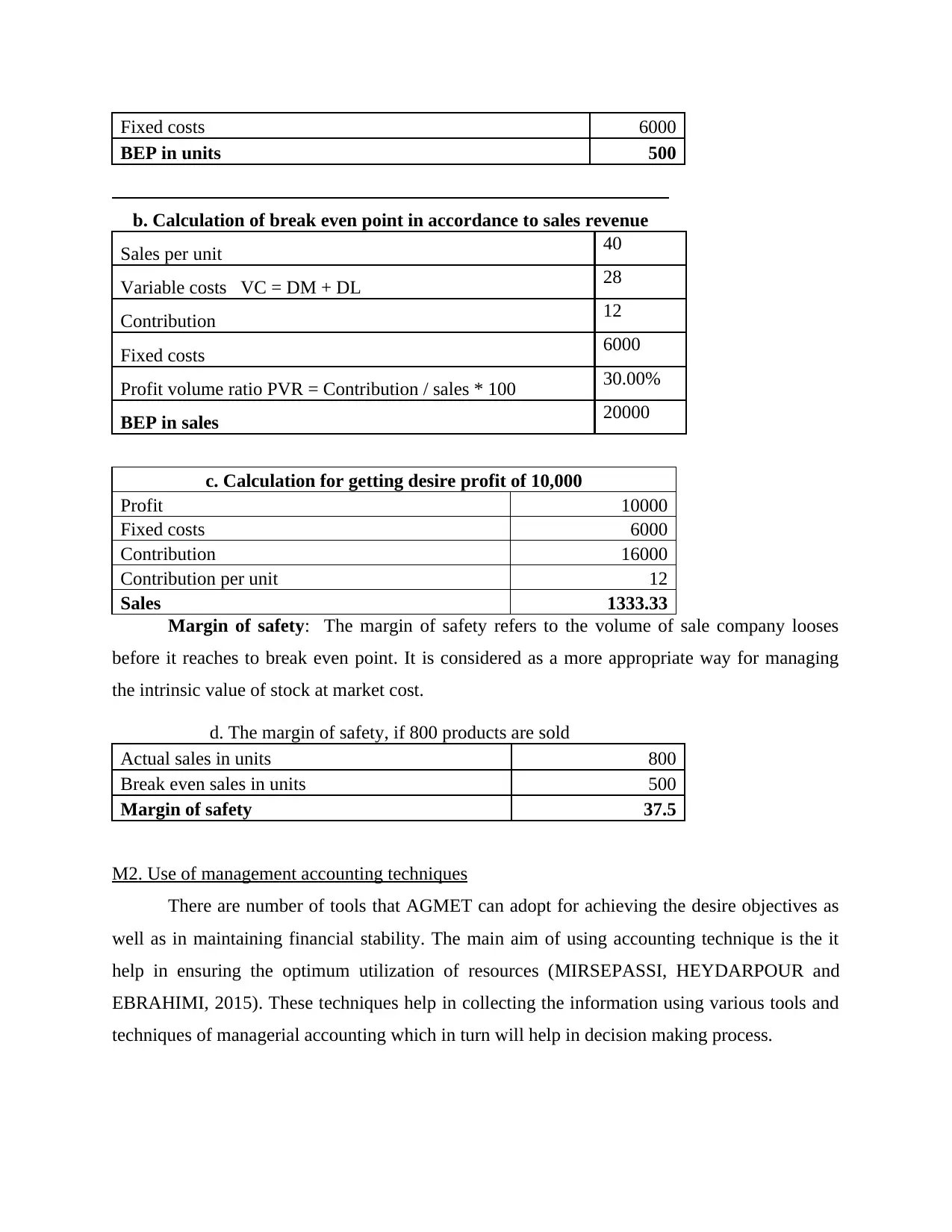

Break even analysis: An important point where all the revenues and expenses are equal

for AGMET and that point is known as break even point (McLean, McGovern and Davie,

2015). This point shows the position where company neither generate profit nor it incurred any

loss.

Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Profitability In marginal costing the

profitability is measured using

profit volume ratio.

Profitability in absorption cost

is affected as it includes fixed

cost.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: An important point where all the revenues and expenses are equal

for AGMET and that point is known as break even point (McLean, McGovern and Davie,

2015). This point shows the position where company neither generate profit nor it incurred any

loss.

Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: The margin of safety refers to the volume of sale company looses

before it reaches to break even point. It is considered as a more appropriate way for managing

the intrinsic value of stock at market cost.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2. Use of management accounting techniques

There are number of tools that AGMET can adopt for achieving the desire objectives as

well as in maintaining financial stability. The main aim of using accounting technique is the it

help in ensuring the optimum utilization of resources (MIRSEPASSI, HEYDARPOUR and

EBRAHIMI, 2015). These techniques help in collecting the information using various tools and

techniques of managerial accounting which in turn will help in decision making process.

BEP in units 500

b. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: The margin of safety refers to the volume of sale company looses

before it reaches to break even point. It is considered as a more appropriate way for managing

the intrinsic value of stock at market cost.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2. Use of management accounting techniques

There are number of tools that AGMET can adopt for achieving the desire objectives as

well as in maintaining financial stability. The main aim of using accounting technique is the it

help in ensuring the optimum utilization of resources (MIRSEPASSI, HEYDARPOUR and

EBRAHIMI, 2015). These techniques help in collecting the information using various tools and

techniques of managerial accounting which in turn will help in decision making process.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

D2 Financial report that apply for interpret business activities

Managerial accounting uses two techniques generally known as absorption costing and

marginal costing which help an organisation in calculating the net profit. This help company in

making investment decision by evaluating fixed and variable cost which in turn will find out the

estimated amount of net profit in near future.

TASK 3

P4 Advantages and disadvantage of various planning tools

Budgetary control:- Budgetary control refers to the managerial process of monitoring or

controlling the operational cost using budget statement in a given accounting period. In this

process manager set some performance and financial goal along with certain budget and then

compare actual performance with planned, adjust actions whenever required (Nikoomaram,

Taghavi and Ahmadzadeh, 2014). It is very essential tool which help company in determining

the gap between performance and in eliminating the waste of resources as well as in reducing the

cost of company. Following is the process of budgetary control:-

Consult with manager:- For proper functioning of a business coordination among

various department is very essential, as success of a company is depend on the overall

performance of organisation and its personnels. So, it is very necessary for AGMET to

maintain a proper coordination among various department and its manager. For the

preparation of budget management must communicate with other departments in order to

determine the past data to set future cost for business activities.

Do assumption:- After getting all the relevant data next step is to make assumptions

related to future course of actions that are essential to perform and the cost required by

them. This assists AGMET in estimating the cost that may occur in future while

operating business activities and also to prepare a budget accordingly.

Fix data to attain business targets:- In this step manager decide the goals and targets

for future course of actions using the collected information and assumption. This will

help AGMET in setting the objectives along with their budget which in turn will support

company in improving their financial position (Parker, 2014). It also assists in

eliminating the extra cost in order to reduce expenses of firm.

Managerial accounting uses two techniques generally known as absorption costing and

marginal costing which help an organisation in calculating the net profit. This help company in

making investment decision by evaluating fixed and variable cost which in turn will find out the

estimated amount of net profit in near future.

TASK 3

P4 Advantages and disadvantage of various planning tools

Budgetary control:- Budgetary control refers to the managerial process of monitoring or

controlling the operational cost using budget statement in a given accounting period. In this

process manager set some performance and financial goal along with certain budget and then

compare actual performance with planned, adjust actions whenever required (Nikoomaram,

Taghavi and Ahmadzadeh, 2014). It is very essential tool which help company in determining

the gap between performance and in eliminating the waste of resources as well as in reducing the

cost of company. Following is the process of budgetary control:-

Consult with manager:- For proper functioning of a business coordination among

various department is very essential, as success of a company is depend on the overall

performance of organisation and its personnels. So, it is very necessary for AGMET to

maintain a proper coordination among various department and its manager. For the

preparation of budget management must communicate with other departments in order to

determine the past data to set future cost for business activities.

Do assumption:- After getting all the relevant data next step is to make assumptions

related to future course of actions that are essential to perform and the cost required by

them. This assists AGMET in estimating the cost that may occur in future while

operating business activities and also to prepare a budget accordingly.

Fix data to attain business targets:- In this step manager decide the goals and targets

for future course of actions using the collected information and assumption. This will

help AGMET in setting the objectives along with their budget which in turn will support

company in improving their financial position (Parker, 2014). It also assists in

eliminating the extra cost in order to reduce expenses of firm.

Compare actual data with budgeted information:- Under this step manager compares

the actual actions with the planned performance of the employees for identifying the

deviations between them. So that correct actions should be taken to eliminate the gaps

between performance for enhancing business operations. This assist AGMET in

determining the factors that are responsible for increasing the cost of operations and areas

Review analysis:- This is a very crucial step of budgetary control in which all the

activities performed in above step are reviewed for analysing its efficiency (Renz, 2016).

It support AGMET in achieving the set objectives at a minimum cost as this step make

sure that all the task should execute in an effective manner.

Planning tool:

Planning refers to the process of deciding in advance the future course of action which

guides the manager by providing the directions of performing their task and also ensures the

optimum utilization of business as well as financial resources. There are various planning tool

which AGMET can use in order to create an efficient plan, these tools are as follows:

Forecasting tools:- The forecasting tool help manager in predicting the future activities

that are required to be perform. It also help in analysing the risk or cost that may occur in

future which need to be eliminated for proper functioning of business (Salterio, 2015).

Under this tool manager analyse the past performance data as well as external and

internal economical data for forecasting future actions.

Advantages:- This tool help in estimating tasks to be perform in future along with cost

required by them which in turn will help in taking corrective decisions.

Disadvantages:- the estimated cost and sale is not always true hence it may mislead the

workforce.

Scenario tools:- Another type of tool which help the manger of AGMET in identifying

different option that are available to perform business operations. This tool provide

guideline and also direct in performing the functional as well as operational activities

within the organisation.

Advantage:- This tool help in performing task more effectively by providing information

related to various method of performing operations.

Disadvantage:- Scenario tool is more time consuming.

the actual actions with the planned performance of the employees for identifying the

deviations between them. So that correct actions should be taken to eliminate the gaps

between performance for enhancing business operations. This assist AGMET in

determining the factors that are responsible for increasing the cost of operations and areas

Review analysis:- This is a very crucial step of budgetary control in which all the

activities performed in above step are reviewed for analysing its efficiency (Renz, 2016).

It support AGMET in achieving the set objectives at a minimum cost as this step make

sure that all the task should execute in an effective manner.

Planning tool:

Planning refers to the process of deciding in advance the future course of action which

guides the manager by providing the directions of performing their task and also ensures the

optimum utilization of business as well as financial resources. There are various planning tool

which AGMET can use in order to create an efficient plan, these tools are as follows:

Forecasting tools:- The forecasting tool help manager in predicting the future activities

that are required to be perform. It also help in analysing the risk or cost that may occur in

future which need to be eliminated for proper functioning of business (Salterio, 2015).

Under this tool manager analyse the past performance data as well as external and

internal economical data for forecasting future actions.

Advantages:- This tool help in estimating tasks to be perform in future along with cost

required by them which in turn will help in taking corrective decisions.

Disadvantages:- the estimated cost and sale is not always true hence it may mislead the

workforce.

Scenario tools:- Another type of tool which help the manger of AGMET in identifying

different option that are available to perform business operations. This tool provide

guideline and also direct in performing the functional as well as operational activities

within the organisation.

Advantage:- This tool help in performing task more effectively by providing information

related to various method of performing operations.

Disadvantage:- Scenario tool is more time consuming.

Contingency planning tool:- This tool support AGMET in planning future actions in

order to deal with some obstacles or events that may or may not occur, but have a huge

impact over functioning of company. Under this approach manager analyse risks that

organisation may face in future and planning actions that help in eliminating those risks.

Advantage:- It helps manager in reducing the risk of uncertainty.

Disadvantage:- this tool is not suitable for all the situations.

M3. Evaluation of planning tools

Budgetary control is utilised by AGMET for getting exact information such as operating

and cash budget. Operating budget assists firm in determining the total expenses and cost that is

incurred by firm throughout the year (Schaltegger, Burritt and Petersen, 2017). Cash budget

helps company in identifying the total cash inflow and outflows occur from different operations.

There are several planning tools that are utilised by AGMET for analysing future actions. These

tools and techniques assist manger in increasing efficiency by appropriate utilisation of

resources and also helps in developing contingency plan that includes deciding course of actions

for risk that may or may not occur in future and have negative impact on the growth of the

organisation.

TASK 4

P5. Adaption of management accounting system to respond financial problems

The growth of an organisation is depend upon its financial position, so managers of

AGMET must identify all the factors that contribute toward the financial health and stability of

company. Every organisation faces number of difficulties while performing its operations that

may affect the functioning of business operations Following are the financial issues that may be

faced by AGMET are as follows:

Profitability:- There are various issue that affects the profit margin of AGMET such as

additional expenses occurred during performance of business operations. These expenses

increases the cost of company and hence reduces the profitability.

Financial performance:- This issue consists of financial position of a company, if there

is variation in planned and actual performance then it directly affect the productivity of an

organisation (Subramaniam and Watson, 2016). Hence it also affects the financial stability of

company.

order to deal with some obstacles or events that may or may not occur, but have a huge

impact over functioning of company. Under this approach manager analyse risks that

organisation may face in future and planning actions that help in eliminating those risks.

Advantage:- It helps manager in reducing the risk of uncertainty.

Disadvantage:- this tool is not suitable for all the situations.

M3. Evaluation of planning tools

Budgetary control is utilised by AGMET for getting exact information such as operating

and cash budget. Operating budget assists firm in determining the total expenses and cost that is

incurred by firm throughout the year (Schaltegger, Burritt and Petersen, 2017). Cash budget

helps company in identifying the total cash inflow and outflows occur from different operations.

There are several planning tools that are utilised by AGMET for analysing future actions. These

tools and techniques assist manger in increasing efficiency by appropriate utilisation of

resources and also helps in developing contingency plan that includes deciding course of actions

for risk that may or may not occur in future and have negative impact on the growth of the

organisation.

TASK 4

P5. Adaption of management accounting system to respond financial problems

The growth of an organisation is depend upon its financial position, so managers of

AGMET must identify all the factors that contribute toward the financial health and stability of

company. Every organisation faces number of difficulties while performing its operations that

may affect the functioning of business operations Following are the financial issues that may be

faced by AGMET are as follows:

Profitability:- There are various issue that affects the profit margin of AGMET such as

additional expenses occurred during performance of business operations. These expenses

increases the cost of company and hence reduces the profitability.

Financial performance:- This issue consists of financial position of a company, if there

is variation in planned and actual performance then it directly affect the productivity of an

organisation (Subramaniam and Watson, 2016). Hence it also affects the financial stability of

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Following are the measures that must be taken in order to bring financial efficiency and

overcome from above explained issues:-

Key performance indicator (KPI):- KPI refers to the tool which demonstrate how

effectively a company is achieving their set tasks and objectives (Key performance

indicators, 2018). This approach help in analysing and eliminating the barrier which

affects the performance. KPI track the performance of employees and shows the

variations that are need to be improve which in turn will bring efficiency in operations.

Financial governance:- There are various issues occurs during performing business

operations which have an huge impact over the profitability of a company. So financial

governance is very essential approach which help in managing the finance of a company

and in eliminating the extra cost incurred (Wickramasinghe, 2015). This tool provide

guidance for better utilisation of financial resources which also help in increasing the

marginal profit.

Benchmarking:- Under this approach managers set certain goal for their workforce

which help in achieving organisational objective. Benchmarks are very essential for

determining that whether the enterprise is moving in right direction. In this process

manager set certain standards which are then compare with actual performance to find the

area of improvement which helps in enhancing the productivity.

Comparison of AGMET with another company

AGMET Monarch Chemicals

AGMET is a small scale company which

works for recycling of metal-bearing industrial

products. It is a full service resource recovery

company which handles all the risk associated

with management and recycling of industrial

products.

Monarch chemical Ltd is the largest

manufacturer and distributors of chemical in

UK. It provides a complete package which

includes everything from simple commodity

chemicals to complex blend.

It is small scale industry hence company uses

key performance indicator and benchmarking

tool which motivates the employees for

enhancing their performance (Renz, 2016).

This company is operated at large scale, so

they must follow financial governance tool

which help in maintaining the financial

stability of organisation. This tool is very

overcome from above explained issues:-

Key performance indicator (KPI):- KPI refers to the tool which demonstrate how

effectively a company is achieving their set tasks and objectives (Key performance

indicators, 2018). This approach help in analysing and eliminating the barrier which

affects the performance. KPI track the performance of employees and shows the

variations that are need to be improve which in turn will bring efficiency in operations.

Financial governance:- There are various issues occurs during performing business

operations which have an huge impact over the profitability of a company. So financial

governance is very essential approach which help in managing the finance of a company

and in eliminating the extra cost incurred (Wickramasinghe, 2015). This tool provide

guidance for better utilisation of financial resources which also help in increasing the

marginal profit.

Benchmarking:- Under this approach managers set certain goal for their workforce

which help in achieving organisational objective. Benchmarks are very essential for

determining that whether the enterprise is moving in right direction. In this process

manager set certain standards which are then compare with actual performance to find the

area of improvement which helps in enhancing the productivity.

Comparison of AGMET with another company

AGMET Monarch Chemicals

AGMET is a small scale company which

works for recycling of metal-bearing industrial

products. It is a full service resource recovery

company which handles all the risk associated

with management and recycling of industrial

products.

Monarch chemical Ltd is the largest

manufacturer and distributors of chemical in

UK. It provides a complete package which

includes everything from simple commodity

chemicals to complex blend.

It is small scale industry hence company uses

key performance indicator and benchmarking

tool which motivates the employees for

enhancing their performance (Renz, 2016).

This company is operated at large scale, so

they must follow financial governance tool

which help in maintaining the financial

stability of organisation. This tool is very

These tool help firm expanding their business

and in improving the performance of their staff

members which in turn will increase the

profitability and productivity.

essential in eliminating the extra expenses and

in performing operation more effectively.

Scope of AGMET is very wide. It has limited scope.

M4. Evaluation of financial issues

There are several problems that faced by the firm that may affects the profitability and

productivity that are competitive strategies, non performance of employees, missing accounting

reports and many more (Jack, 2015). It is very necessary for AGMET to adopt several financial

tools and techniques to solve the financial issues in a particular time span. There is need of

selecting upgraded and advance technology that aids to improvement in the productivity and

profitability. The manager of AGMET must analysis the barriers and issues related to funds by

using various tools such as Key Performance Indicator (KPI), benchmarking and financial

governance. These helps in providing positive outcome that aids increment in margin of profit.

D3. Evaluation of planning tools for responding to financial problems

Planning tool is used by management in order to formulate a plan which provides

direction to perform future course of action and help in achieving the optimum utilisation of

available resources (Lachmann, Trapp and Trapp, 2017). There are number of planning tools

used by the managers of AGMET such as scenario tools, contingency planning tool and

forecasting tools. Further Key Performance Indicator and Benchmarking are the methods used

for removing the financial issues. These tools and techniques are used to improve the

productivity as well as overall performance of organisation.

CONCLUSION

From the above report, it is summarized that management accounting system plays very

vital role in an enterprise for operating effective and efficient functions in the firm. Major benefit

of managerial accounting system is that it helps an organisation in bring efficiency in their

operations. There are several methods of reporting system that helpful in preparing budget also

find out the deviations between standard and actual performance. This file also explains about

different kind of planning tool that are scenario tool, forecasting tool, etc. that helps manager of

and in improving the performance of their staff

members which in turn will increase the

profitability and productivity.

essential in eliminating the extra expenses and

in performing operation more effectively.

Scope of AGMET is very wide. It has limited scope.

M4. Evaluation of financial issues

There are several problems that faced by the firm that may affects the profitability and

productivity that are competitive strategies, non performance of employees, missing accounting

reports and many more (Jack, 2015). It is very necessary for AGMET to adopt several financial

tools and techniques to solve the financial issues in a particular time span. There is need of

selecting upgraded and advance technology that aids to improvement in the productivity and

profitability. The manager of AGMET must analysis the barriers and issues related to funds by

using various tools such as Key Performance Indicator (KPI), benchmarking and financial

governance. These helps in providing positive outcome that aids increment in margin of profit.

D3. Evaluation of planning tools for responding to financial problems

Planning tool is used by management in order to formulate a plan which provides

direction to perform future course of action and help in achieving the optimum utilisation of

available resources (Lachmann, Trapp and Trapp, 2017). There are number of planning tools

used by the managers of AGMET such as scenario tools, contingency planning tool and

forecasting tools. Further Key Performance Indicator and Benchmarking are the methods used

for removing the financial issues. These tools and techniques are used to improve the

productivity as well as overall performance of organisation.

CONCLUSION

From the above report, it is summarized that management accounting system plays very

vital role in an enterprise for operating effective and efficient functions in the firm. Major benefit

of managerial accounting system is that it helps an organisation in bring efficiency in their

operations. There are several methods of reporting system that helpful in preparing budget also

find out the deviations between standard and actual performance. This file also explains about

different kind of planning tool that are scenario tool, forecasting tool, etc. that helps manager of

AGMET to plan about the future operations. In addition to this, company faces various issues

and for overcoming these problems company have to adopt certain tools & techniques like

benchmarking and KPI.

REFERENCES

Books and journals

Balakrishnan, R., Labro, E. and Soderstrom, N. S., 2014. Cost structure and sticky costs. Journal

of management accounting research. 26(2). pp.91-116.

Bedford, D. S., 2015. Management control systems across different modes of innovation:

Implications for firm performance. Management Accounting Research. 28. pp.12-30.

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bovens, M., Goodin, R. E. and Schillemans, T. eds., 2014. The Oxford handbook public

accountability. Oxford University Press.

Grossi, G. and Steccolini, I., 2014. Guest Editorial: Accounting for public governance.

Qualitative Research in Accounting & Management. 11(2). pp.86-91.

Jack, L., 2015. Future making in farm management accounting: The Australian “Blue Book”.

Accounting History. 20(2). pp.158-182.

Ji, X. D., 2017. Development of accounting and auditing systems in China. Routledge.

Lachmann, M., Trapp, I. and Trapp, R., 2017. Diversity and validity in positivist management

accounting research—A longitudinal perspective over four decades. Management

Accounting Research. 34. pp.42-58.

Luft, J. and Shields, M. D., 2014. Subjectivity in developing and validating causal explanations

in positivist accounting research. Accounting, Organizations and Society. 39(7). pp.550-

558.

McLean, T., McGovern, T. and Davie, S., 2015. Management accounting, engineering and the

management of company growth: Clarke Chapman, 1864–1914. The British Accounting

Review. 47(2). pp.177-190.

MIRSEPASSI, N., HEYDARPOUR, F. and EBRAHIMI, R., 2015. Feasibility study of human

resource accounting Case study at institute of international energy studies (iies).

Nikoomaram, H., Taghavi, M. and Ahmadzadeh, H., 2014. Economic Consequences of

Accounting Information Quality focused on Earnings persistence.

Parker, L., 2014. Qualitative perspectives: Through a methodological lens. Qualitative Research

in Accounting & Management. 11(1). pp.13-28.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Salterio, S.E., 2015. Barriers to knowledge creation in management accounting research. Journal

of Management Accounting Research. 27(1). pp.151-170.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

and for overcoming these problems company have to adopt certain tools & techniques like

benchmarking and KPI.

REFERENCES

Books and journals

Balakrishnan, R., Labro, E. and Soderstrom, N. S., 2014. Cost structure and sticky costs. Journal

of management accounting research. 26(2). pp.91-116.

Bedford, D. S., 2015. Management control systems across different modes of innovation:

Implications for firm performance. Management Accounting Research. 28. pp.12-30.

Bennett, M. and James, P., 2017. The Green bottom line: environmental accounting for

management: current practice and future trends. Routledge.

Bovens, M., Goodin, R. E. and Schillemans, T. eds., 2014. The Oxford handbook public

accountability. Oxford University Press.

Grossi, G. and Steccolini, I., 2014. Guest Editorial: Accounting for public governance.

Qualitative Research in Accounting & Management. 11(2). pp.86-91.

Jack, L., 2015. Future making in farm management accounting: The Australian “Blue Book”.

Accounting History. 20(2). pp.158-182.

Ji, X. D., 2017. Development of accounting and auditing systems in China. Routledge.

Lachmann, M., Trapp, I. and Trapp, R., 2017. Diversity and validity in positivist management

accounting research—A longitudinal perspective over four decades. Management

Accounting Research. 34. pp.42-58.

Luft, J. and Shields, M. D., 2014. Subjectivity in developing and validating causal explanations

in positivist accounting research. Accounting, Organizations and Society. 39(7). pp.550-

558.

McLean, T., McGovern, T. and Davie, S., 2015. Management accounting, engineering and the

management of company growth: Clarke Chapman, 1864–1914. The British Accounting

Review. 47(2). pp.177-190.

MIRSEPASSI, N., HEYDARPOUR, F. and EBRAHIMI, R., 2015. Feasibility study of human

resource accounting Case study at institute of international energy studies (iies).

Nikoomaram, H., Taghavi, M. and Ahmadzadeh, H., 2014. Economic Consequences of

Accounting Information Quality focused on Earnings persistence.

Parker, L., 2014. Qualitative perspectives: Through a methodological lens. Qualitative Research

in Accounting & Management. 11(1). pp.13-28.

Renz, D. O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Salterio, S.E., 2015. Barriers to knowledge creation in management accounting research. Journal

of Management Accounting Research. 27(1). pp.151-170.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Schaltegger, S., Burritt, R. and Petersen, H., 2017. An introduction to corporate environmental

management: Striving for sustainability. Routledge.

Smith, D., Brännström, D. and Jansson, A., 2015. Redovisningens språk. Studentlitteratur.

Subramaniam, C. and Watson, M. W., 2016. Additional evidence on the sticky behavior of costs.

In Advances in Management Accounting (pp. 275-305). Emerald Group Publishing

Limited.

Wickramasinghe, D., 2015. Getting management accounting off the ground: post-colonial

neoliberalism in healthcare budgets. Accounting and Business Research. 45(3). pp.323-

355.

Online

Key performance indicators. 2018. [Online] Available through

<https://searchbusinessanalytics.techtarget.com/definition/key-performance-indicators-

KPIs>./

Job Costing. 2018. [Online] Available through <https://strategiccfo.com/job-costing/>./

management: Striving for sustainability. Routledge.

Smith, D., Brännström, D. and Jansson, A., 2015. Redovisningens språk. Studentlitteratur.

Subramaniam, C. and Watson, M. W., 2016. Additional evidence on the sticky behavior of costs.

In Advances in Management Accounting (pp. 275-305). Emerald Group Publishing

Limited.

Wickramasinghe, D., 2015. Getting management accounting off the ground: post-colonial

neoliberalism in healthcare budgets. Accounting and Business Research. 45(3). pp.323-

355.

Online

Key performance indicators. 2018. [Online] Available through

<https://searchbusinessanalytics.techtarget.com/definition/key-performance-indicators-

KPIs>./

Job Costing. 2018. [Online] Available through <https://strategiccfo.com/job-costing/>./

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.