Management Accounting: Customer Profitability & Transfer Pricing

VerifiedAdded on 2023/06/07

|8

|2153

|108

Report

AI Summary

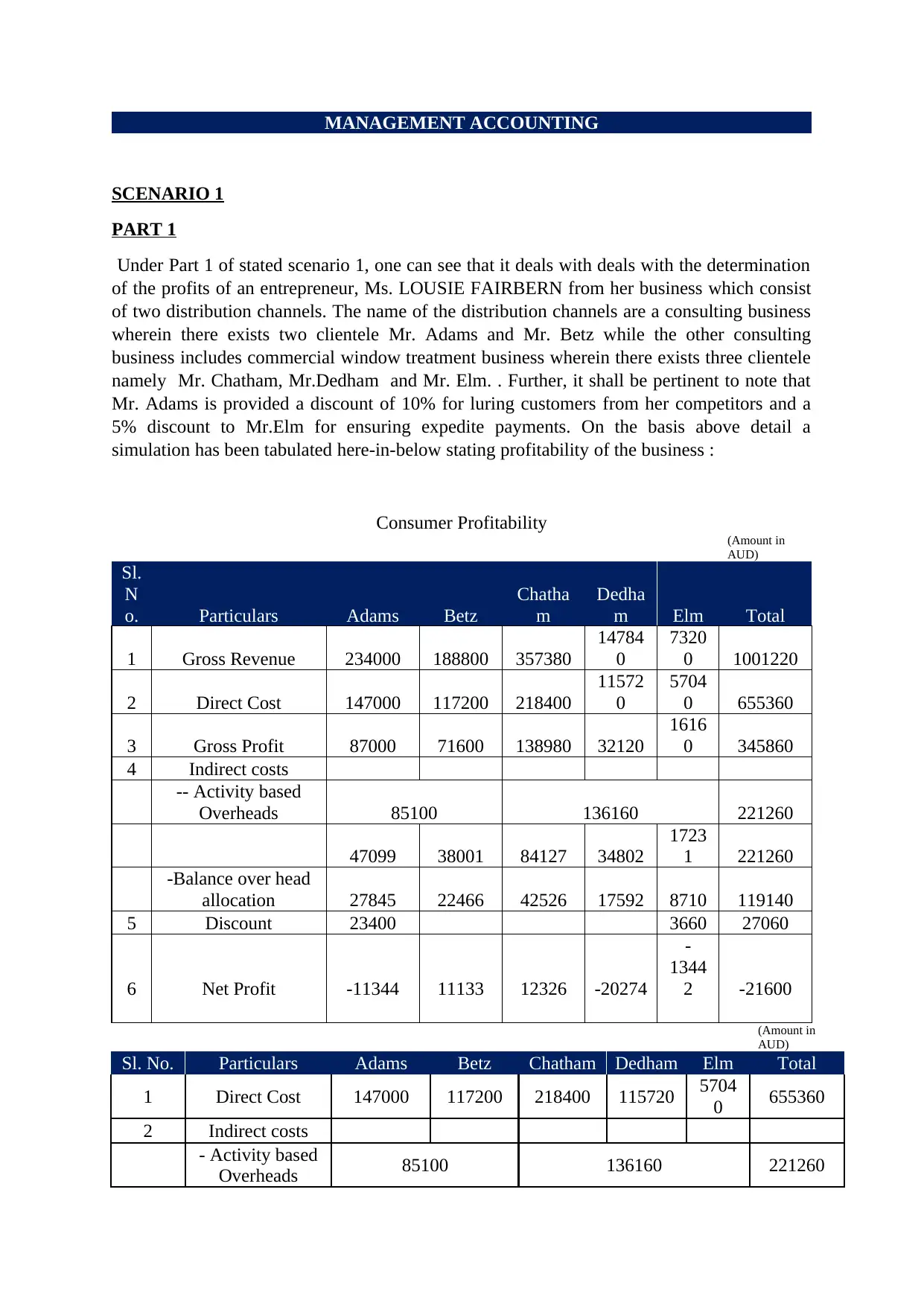

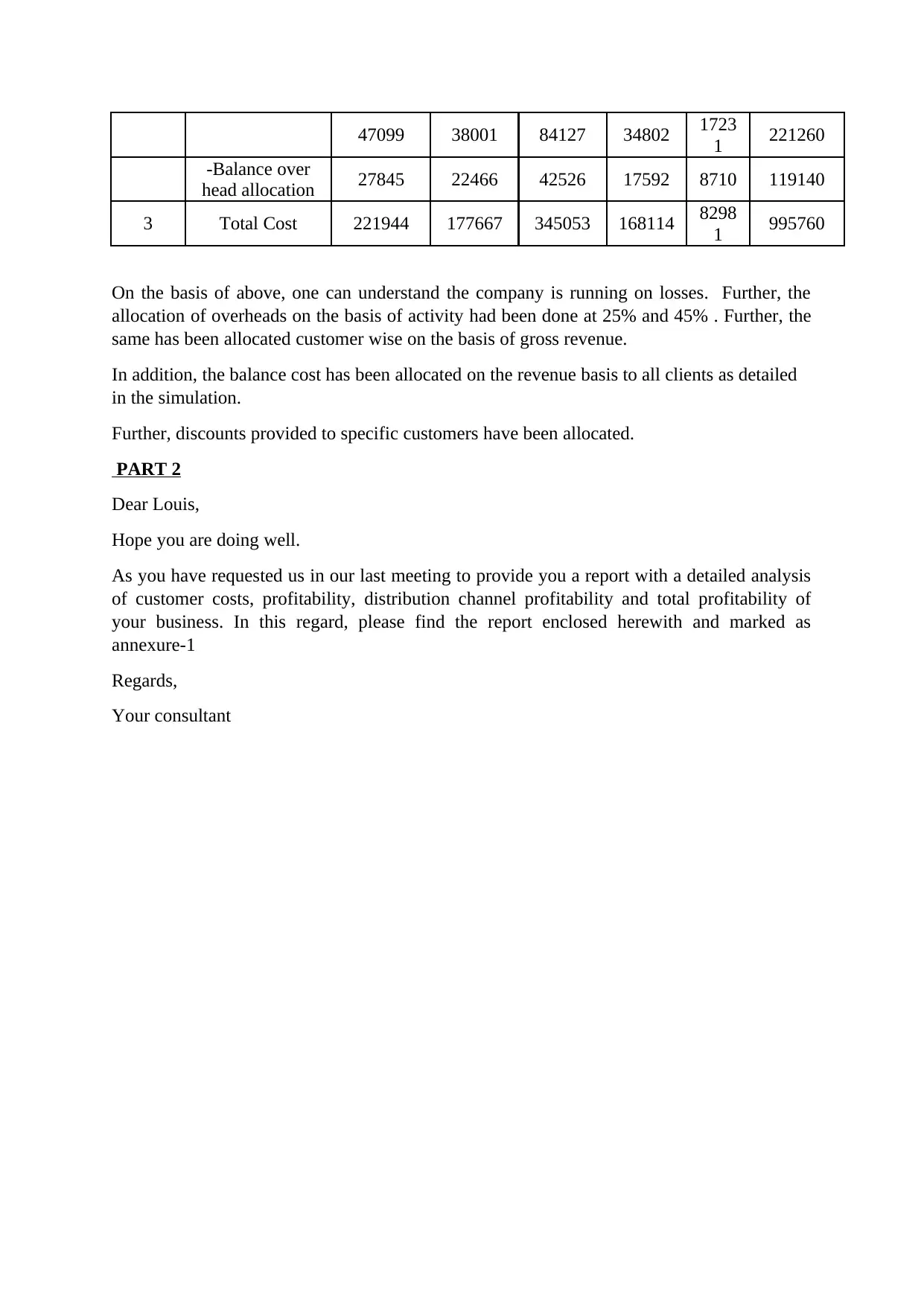

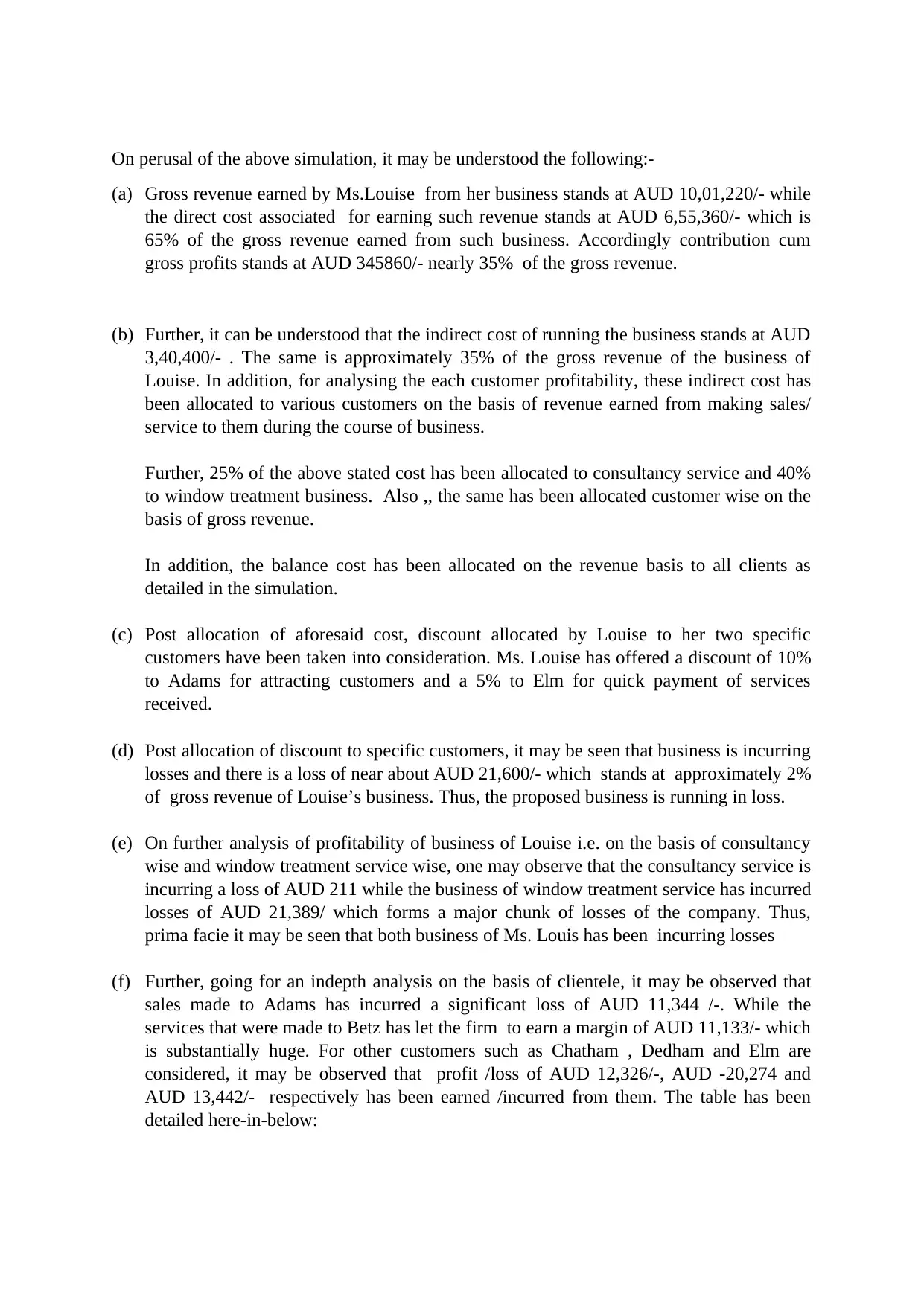

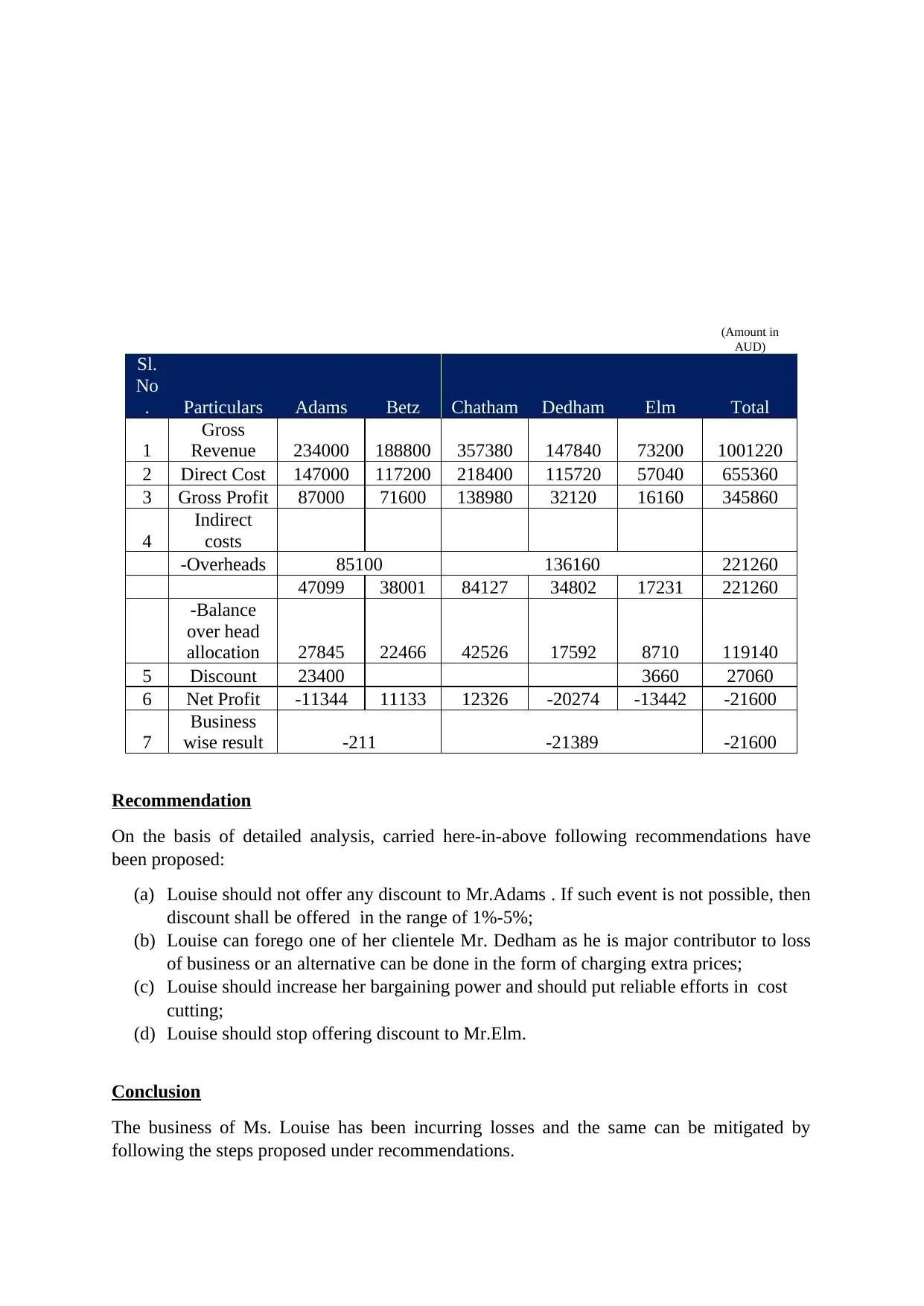

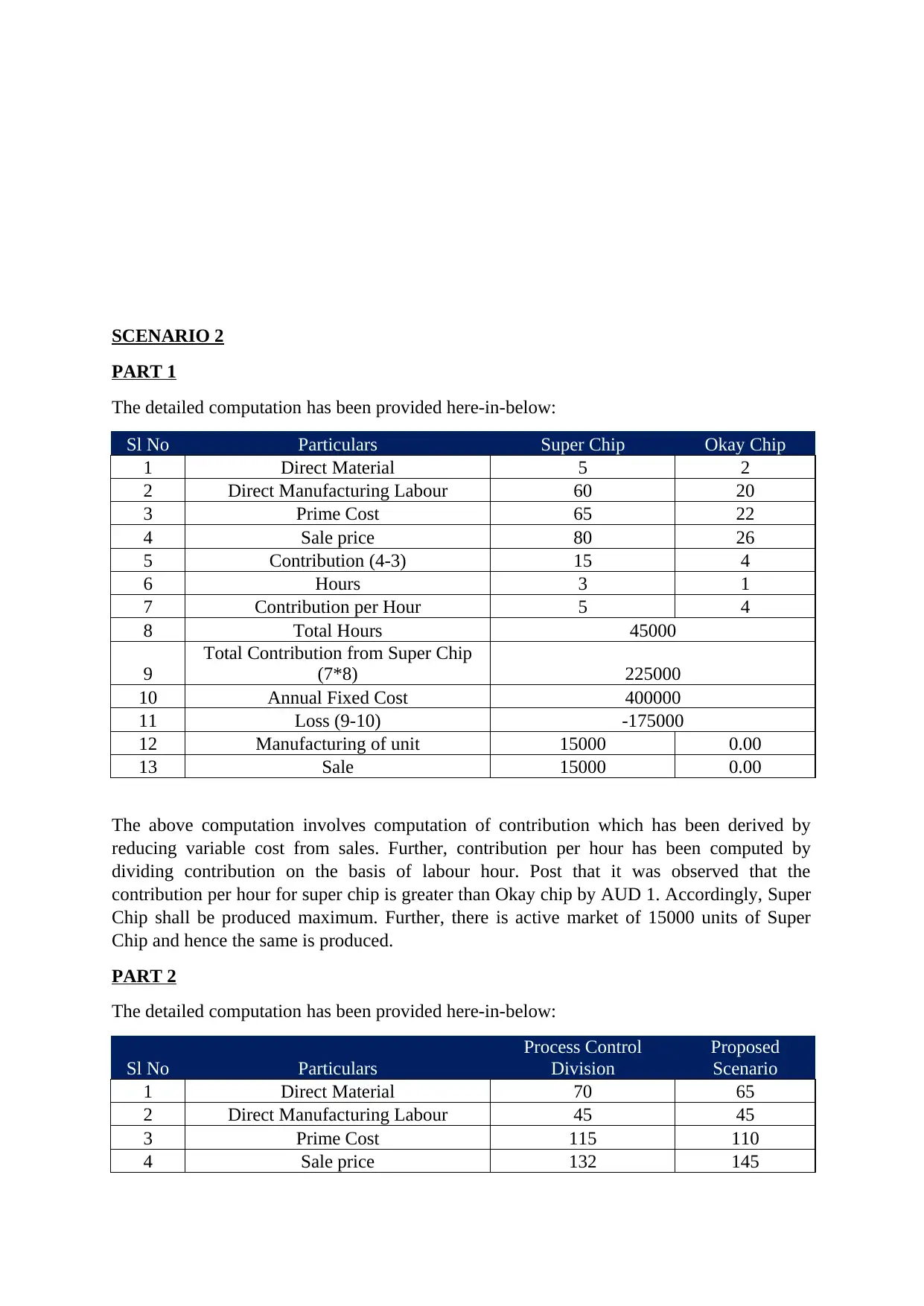

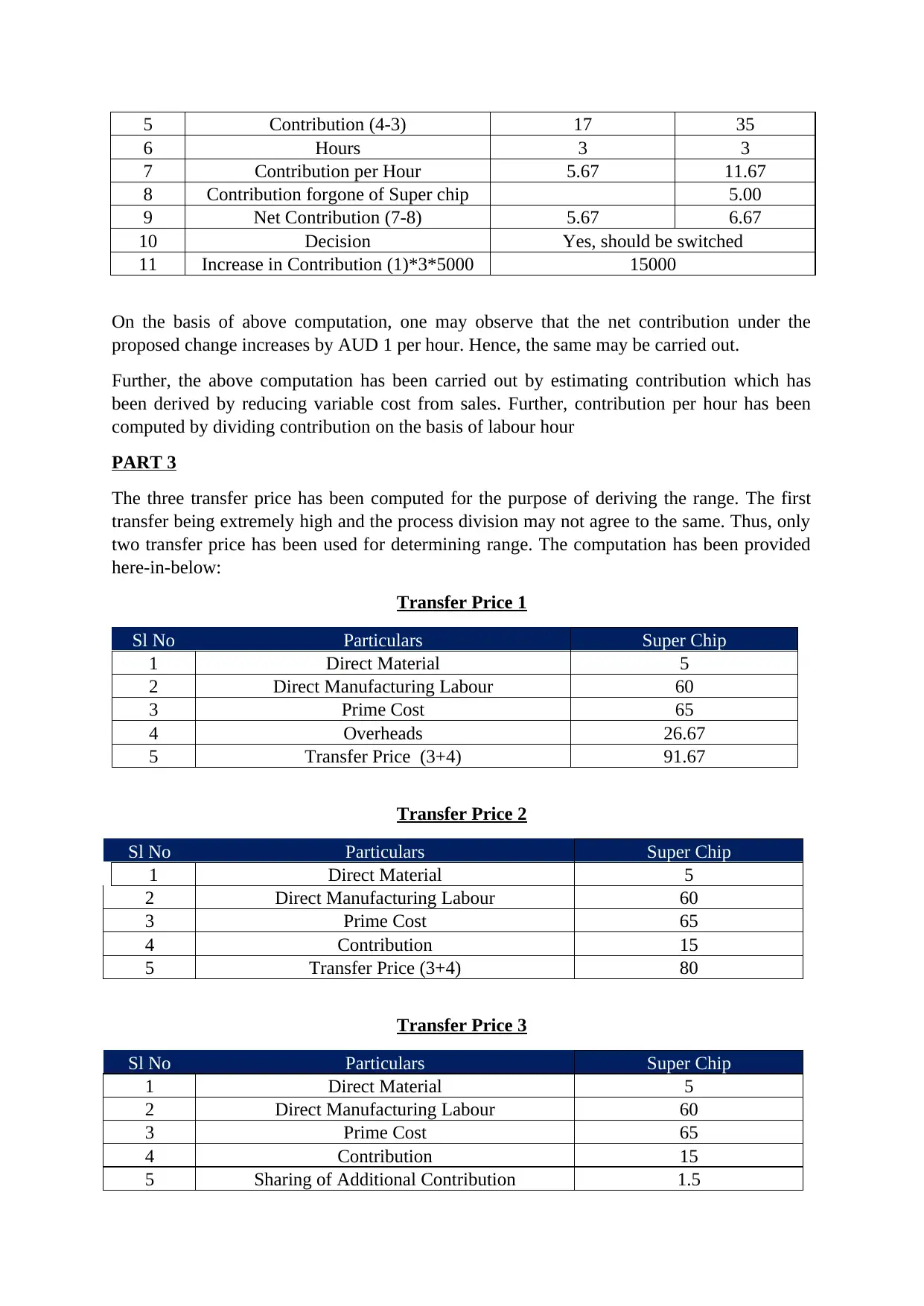

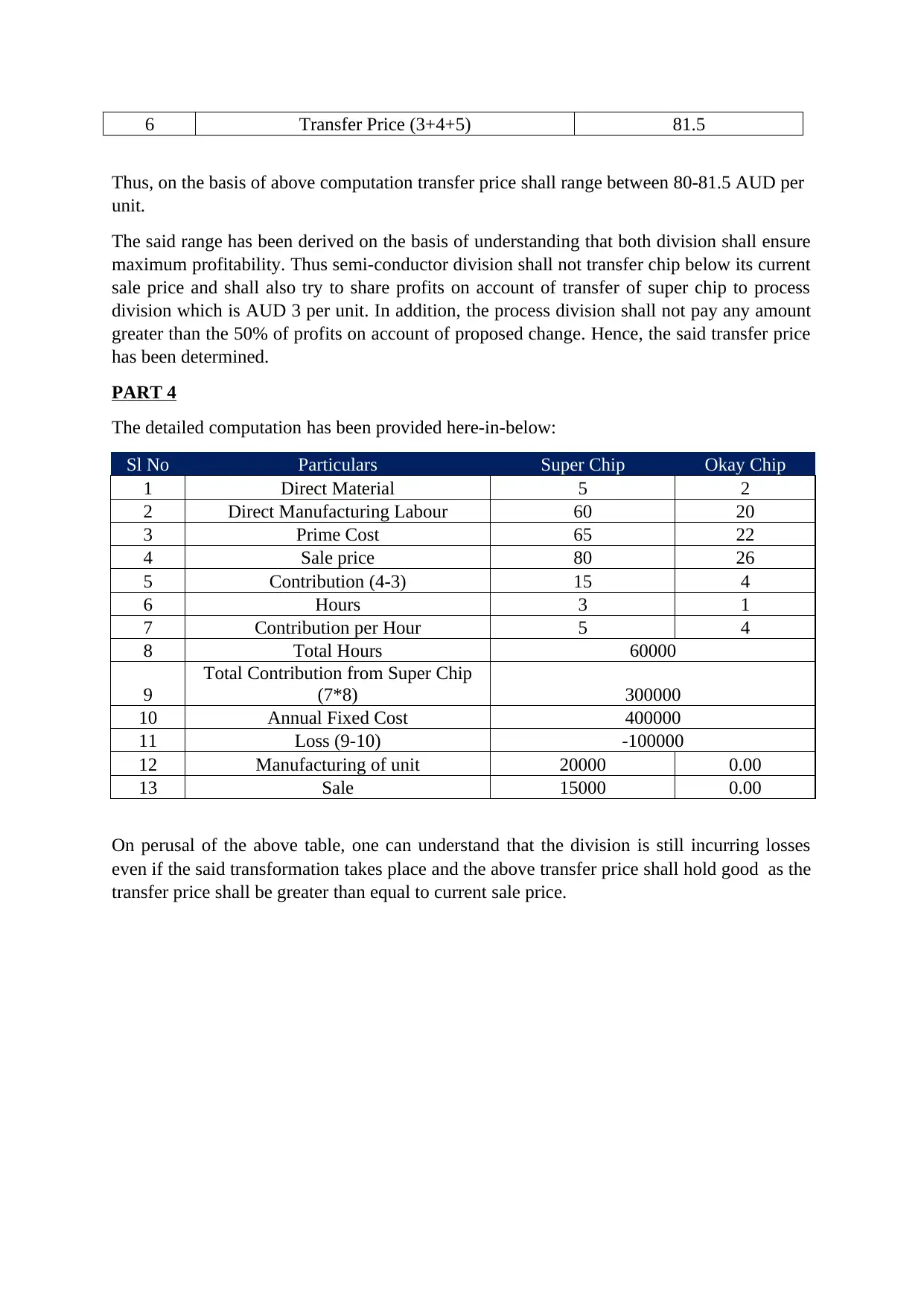

This management accounting report analyzes customer profitability for Louise Fairbern's interior design business, covering two distribution channels: consulting and commercial window treatments. The analysis includes gross revenue, direct costs, overhead allocation, and discounts to determine net profit for each client. The report recommends strategies such as reducing discounts and re-evaluating unprofitable client relationships to mitigate losses. Additionally, the report explores transfer pricing scenarios for Super Chips, aiming to optimize profitability between divisions. The document concludes that the business is incurring losses and suggests implementing the recommendations to improve financial performance. This report also provides computations for transfer pricing and the impact of switching production processes, offering a comprehensive financial overview and strategic advice.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.